Management Accounting: Breakeven Analysis and Financial Report

VerifiedAdded on 2023/06/18

|8

|1337

|143

Report

AI Summary

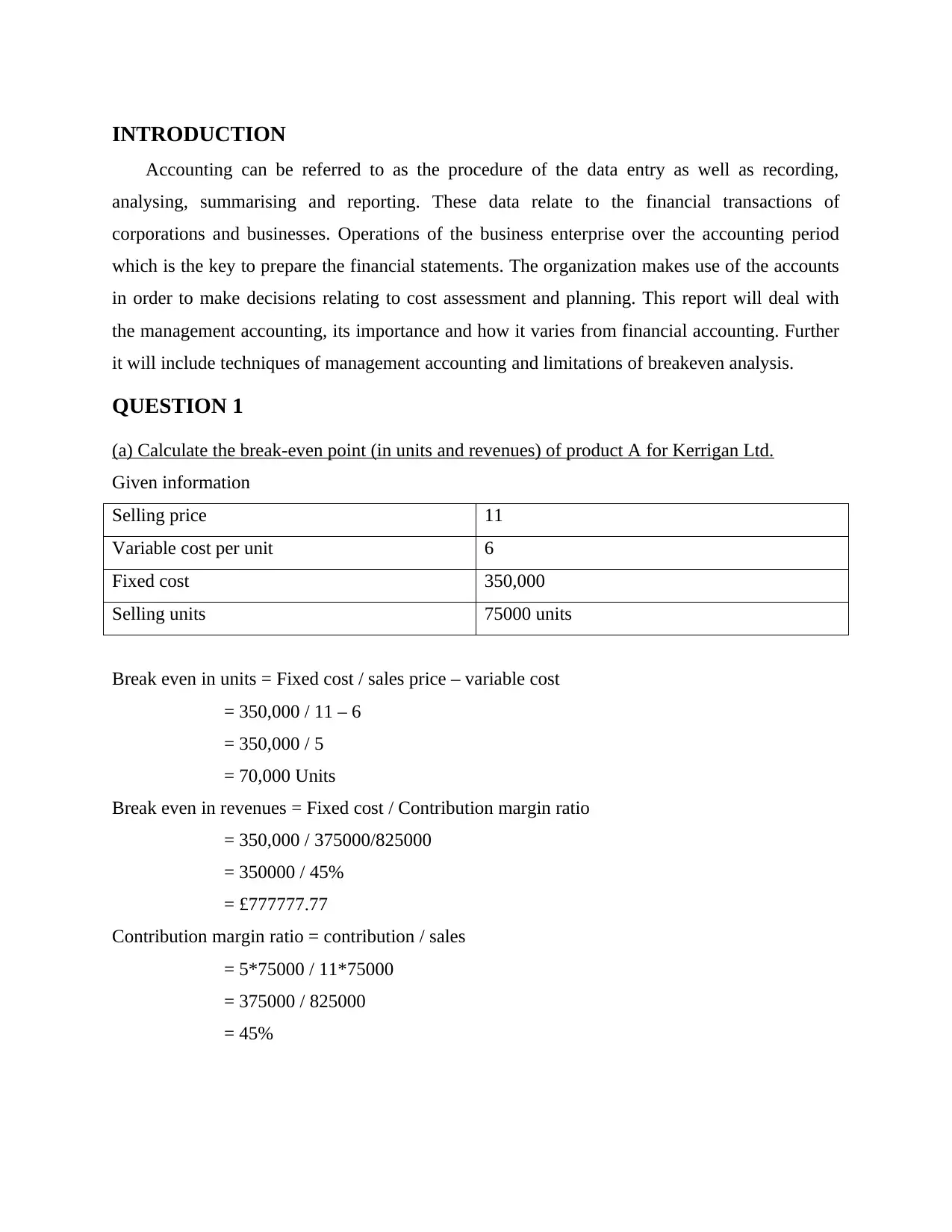

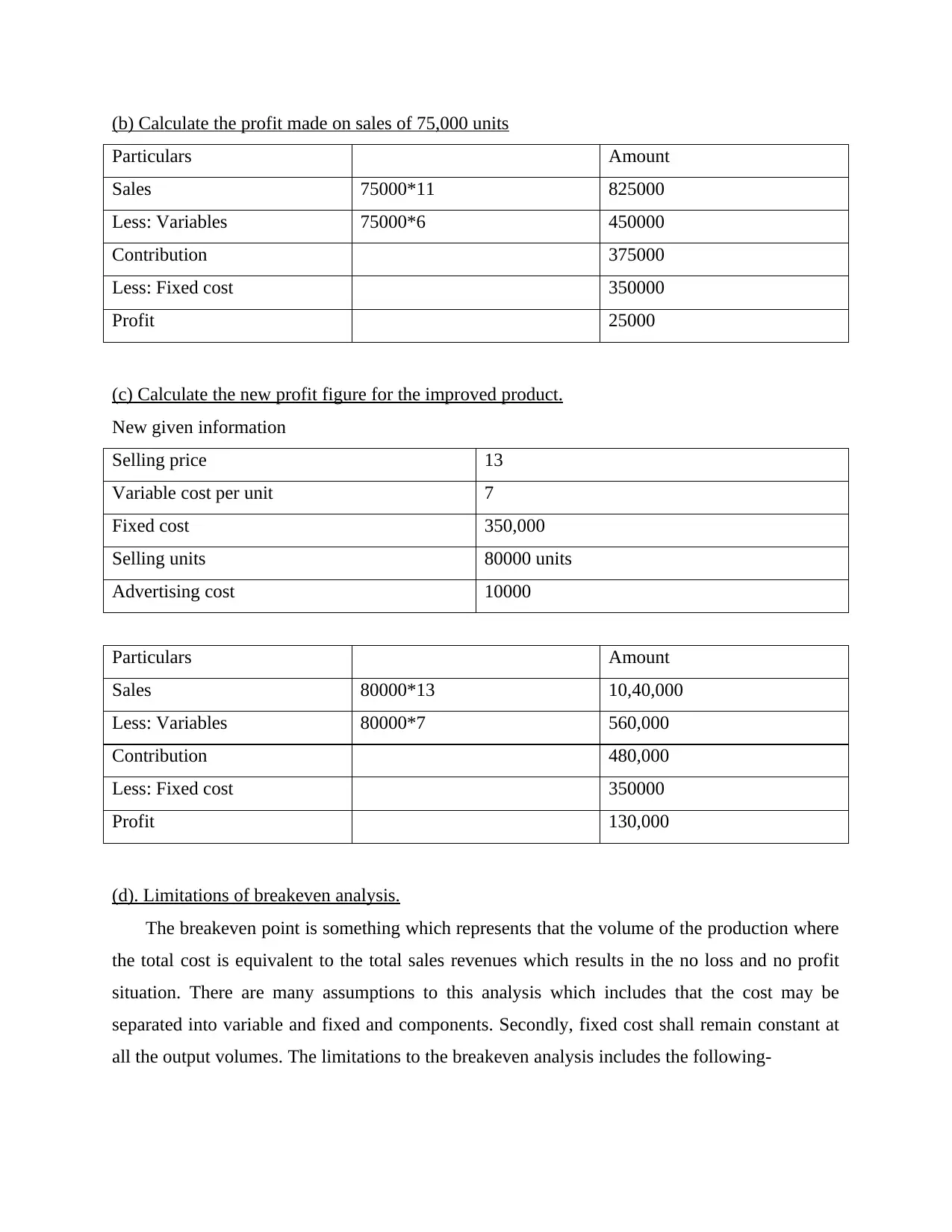

This report provides a comprehensive analysis of breakeven points, calculating unit and revenue break-even for a product, profit at specified sales volumes, and the impact of product improvements on profitability. It discusses the limitations of breakeven analysis, emphasizing assumptions about fixed and variable costs and product mix. The report also explores the significance of management accounting, contrasting it with financial accounting, and details techniques such as funds flow statements, cash flow statements, and revaluation accounting used by management accountants to achieve organizational objectives. It concludes that management accounting is crucial for planning, controlling, and analyzing a company's finances, aiding in informed decision-making.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.