ACCT20076 Breakeven Analysis: Analyzing Profitability and Costs

VerifiedAdded on 2022/10/31

|10

|931

|480

Report

AI Summary

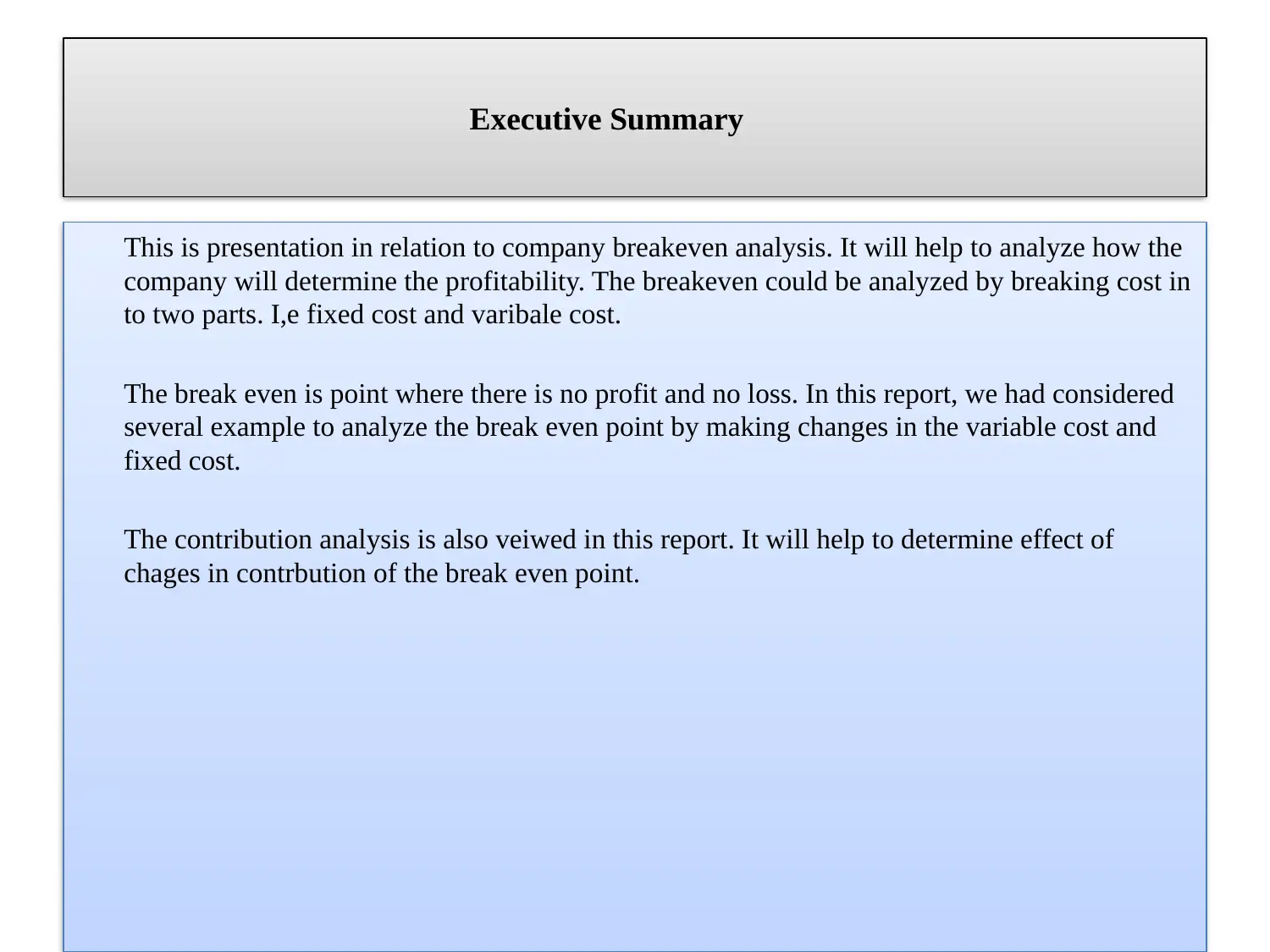

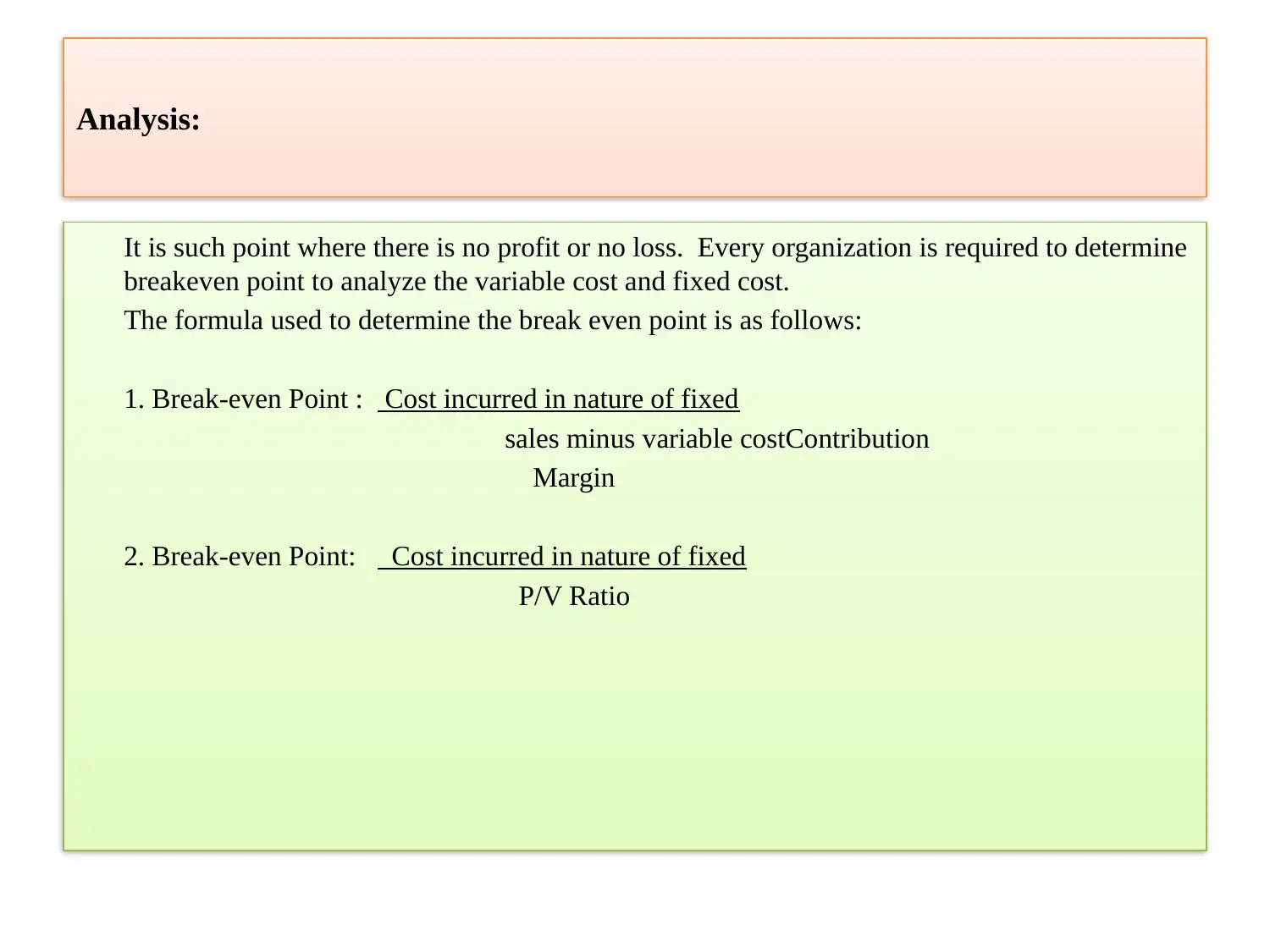

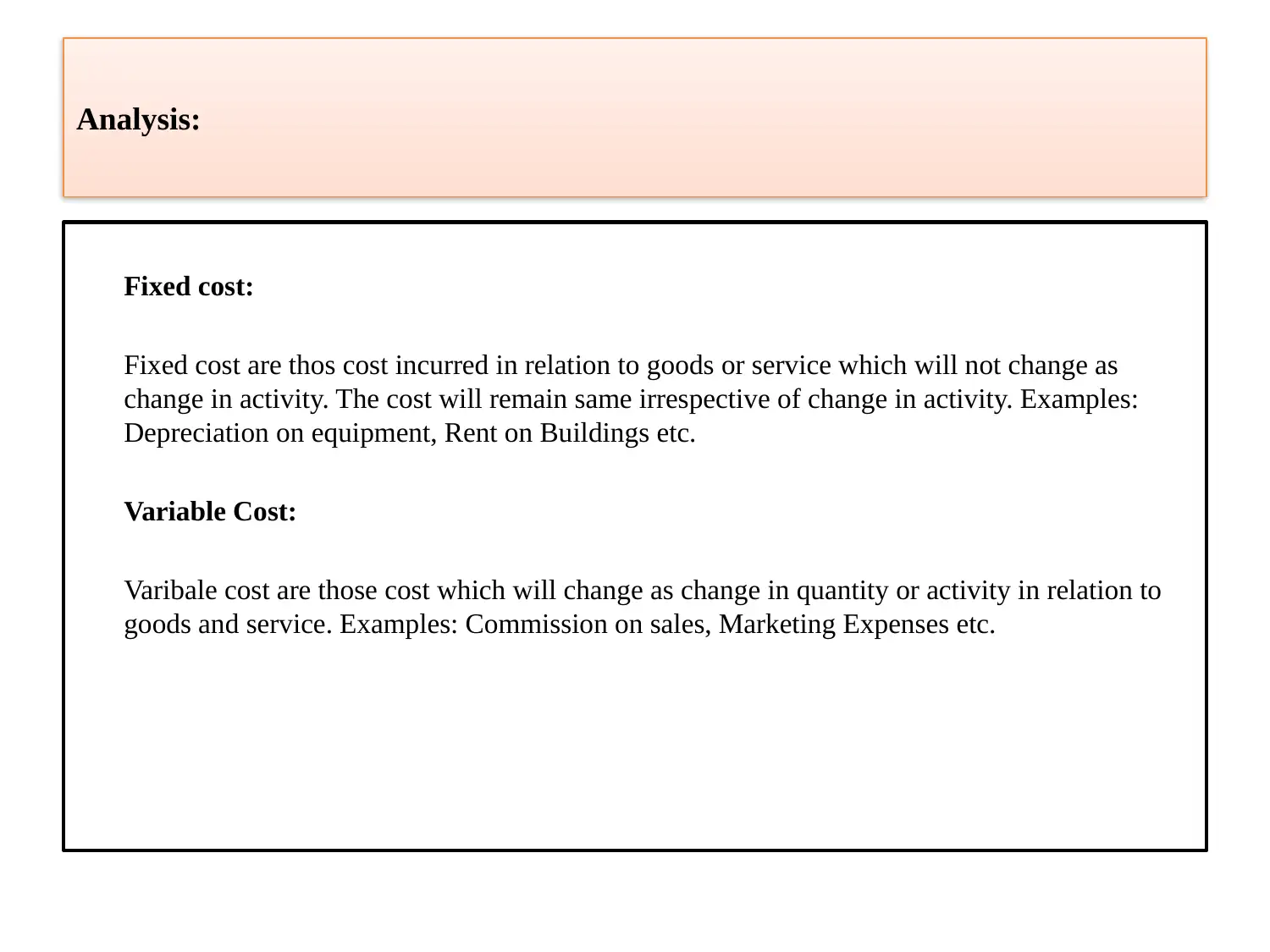

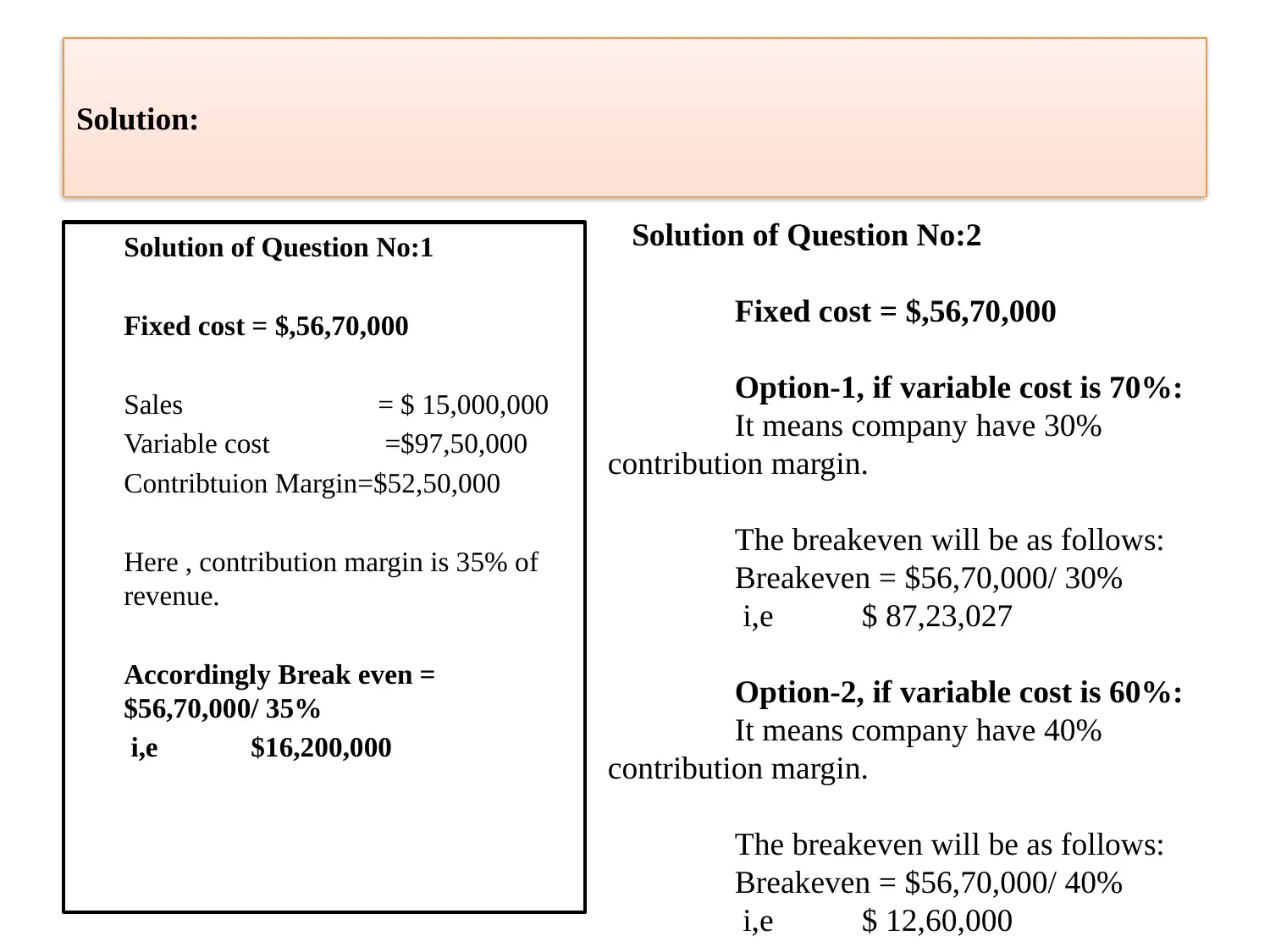

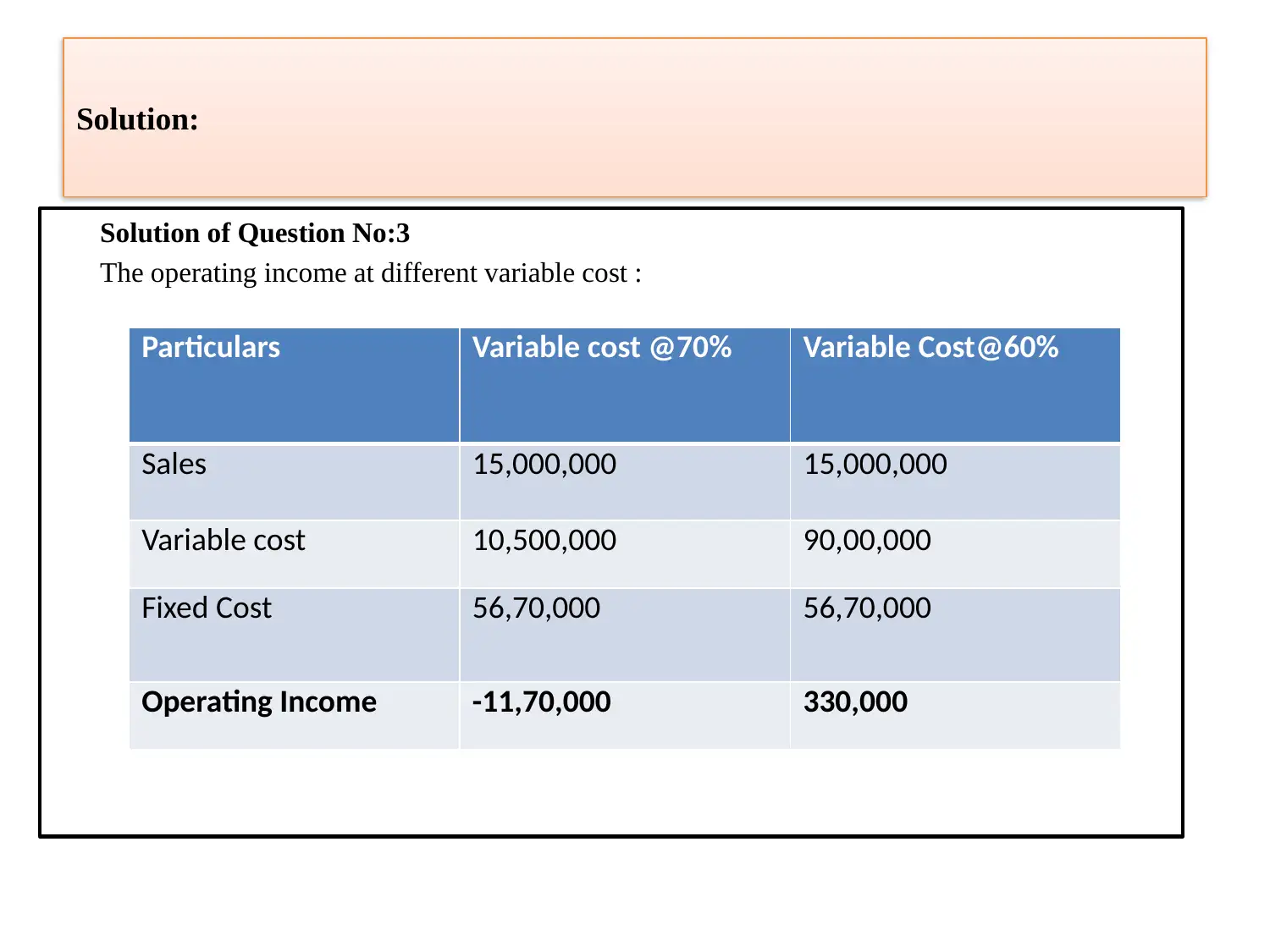

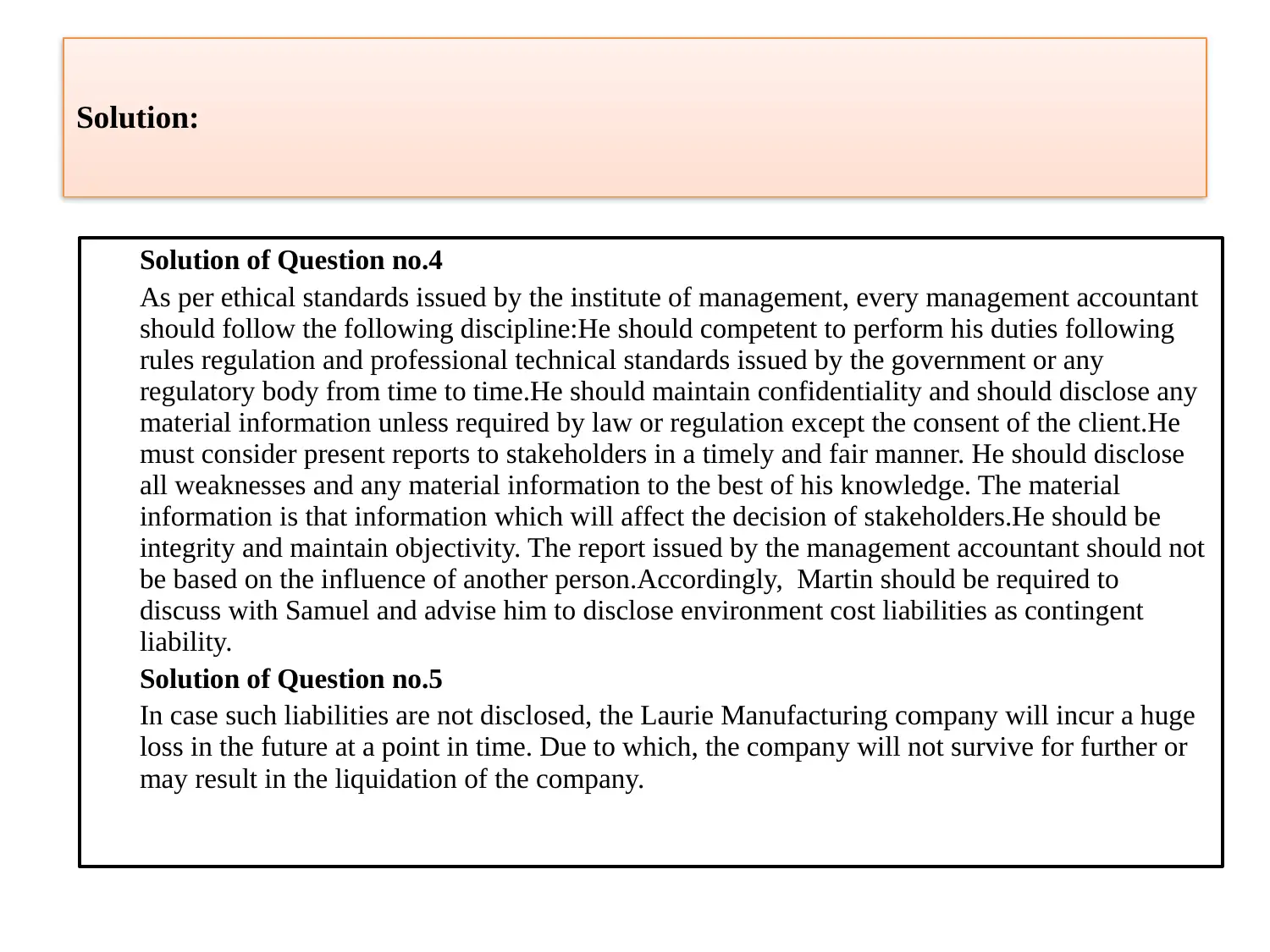

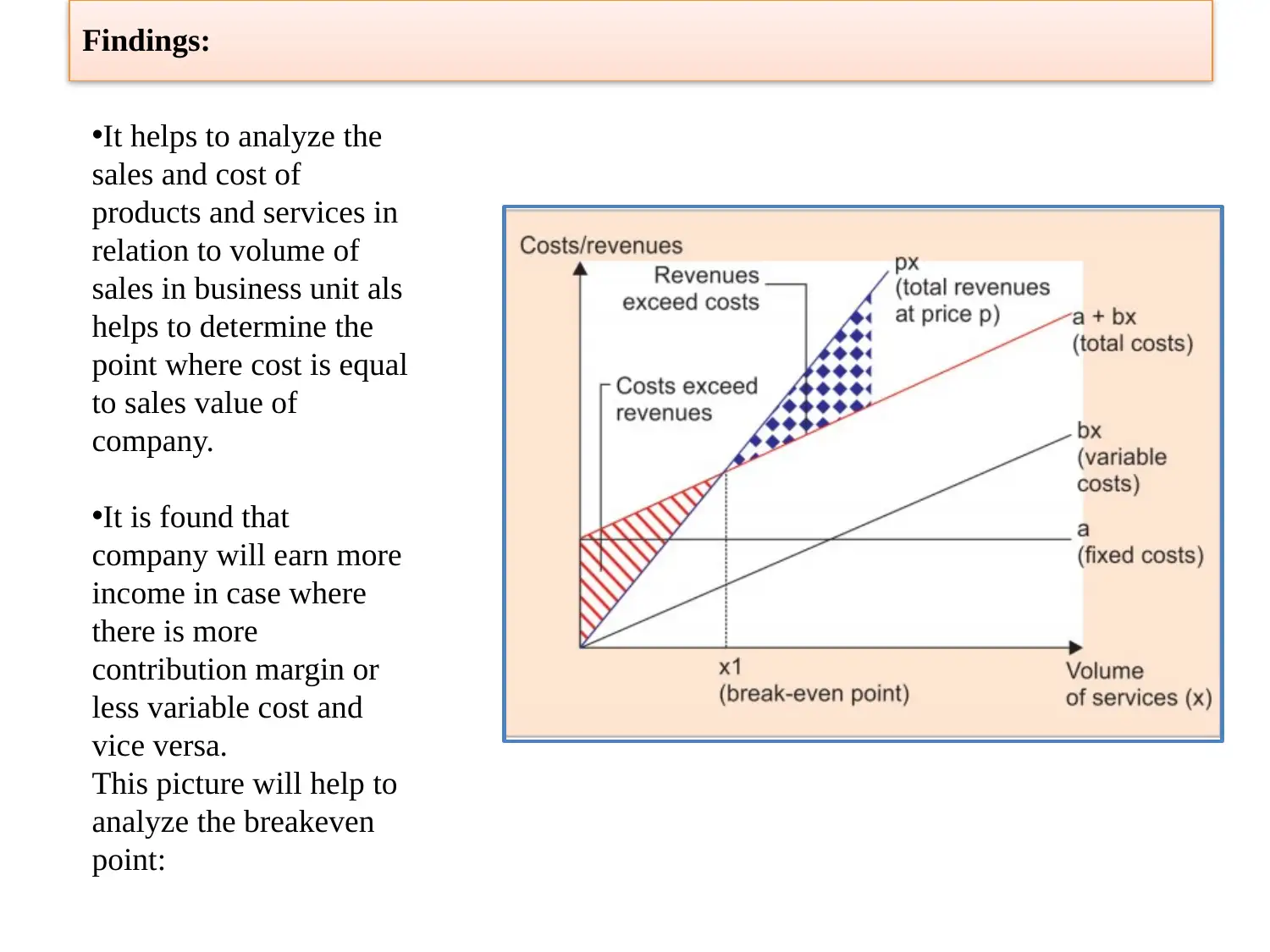

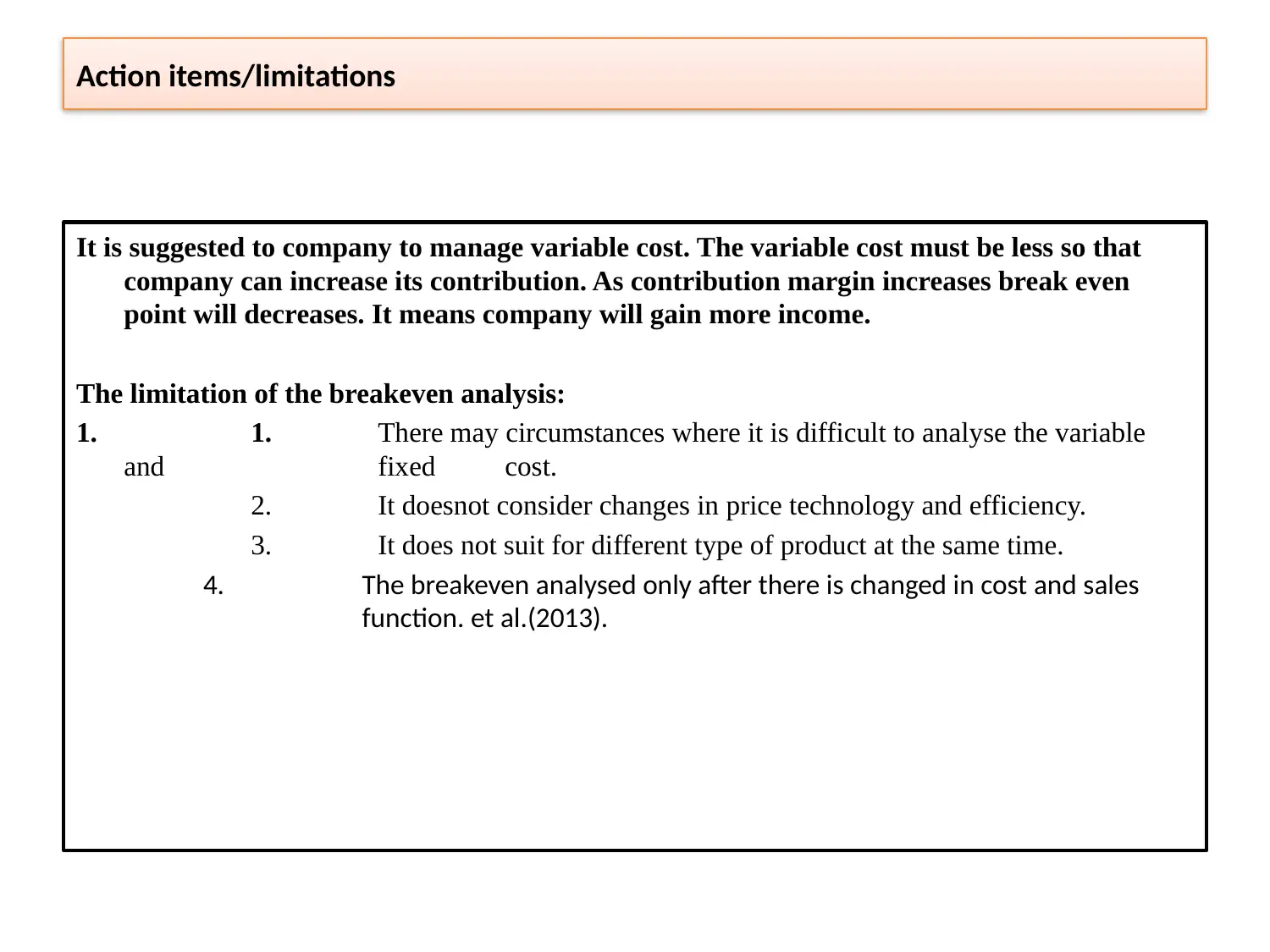

This report provides a detailed analysis of breakeven points, a crucial concept in financial analysis. It begins with an executive summary that outlines the purpose of the analysis, which is to determine a company's profitability by examining fixed and variable costs. The report then delves into the core concepts, including the formulas used to calculate the breakeven point and the distinction between fixed and variable costs, providing examples of each. The report presents solutions to several questions, including calculating the breakeven point under different scenarios involving changes in variable costs and fixed costs. It also explores the impact of contribution margin on the breakeven point and addresses ethical considerations for management accountants regarding the disclosure of liabilities. The report concludes with findings, action items, limitations of breakeven analysis, and references to relevant sources, offering a comprehensive understanding of the topic.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.