Brexit Capital Limited Audit Report: Financial Statement Analysis 2019

VerifiedAdded on 2022/08/14

|13

|2428

|13

Report

AI Summary

This report provides an audit analysis of Brexit Capital Limited's financial statements for the period from March 24, 2019, to December 31, 2019. It includes a review of the Director's Report, highlighting the company's principle activity, directors, and business review, which indicates financial losses. The report examines the Independent Auditor's Report, assessing the auditor's opinion, basis for the opinion, and responsibilities of both the directors and the auditor (UWL C.P.A). The analysis covers the income statement and financial position, scrutinizing revenue, corporation tax expense, amounts due to shareholders, and changes in equity. The report identifies several financial weaknesses, including inconsistencies in the income statement, balance sheet, and lack of revenue activities and tax reporting. The report concludes with recommendations for improving the company's financial position and addresses potential risks, such as fraudulence and insolvency, emphasizing the need for improved financial management and accurate reporting within six months. The report includes references and supporting documents like the letter of appointment and minutes for appointing the auditor.

1Running head: AUDITING

Auditing

Brexit Capital Limited

Directors Report and Financial Statements

Period from 24 March 2019

(Date of Incorporation)

To 31st December 2019

Auditing

Brexit Capital Limited

Directors Report and Financial Statements

Period from 24 March 2019

(Date of Incorporation)

To 31st December 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDITING

Table of Contents

1.0 Directors Report...................................................................................................................3

1.1 Brief Introduction.............................................................................................................3

1.2 Principle Activity.............................................................................................................3

1.3 Directors...........................................................................................................................3

1.4 Business Review..............................................................................................................3

1.5 Permitted Indemnity Provision........................................................................................4

1.6 Auditor.............................................................................................................................4

2.0 Independent Auditor’s Report..............................................................................................4

2.1 Title of the Auditor...........................................................................................................4

2.2 Opinion on Financial Statements.....................................................................................4

2.3 Basis for Opinion.............................................................................................................5

2.4 Additional Information Other Than Financial Statements...............................................5

2.5 Directors Responsibility...................................................................................................5

2.6 Auditor’s Responsibility..................................................................................................5

3.0 Income Statement.................................................................................................................6

4.0 Financial Position.................................................................................................................6

4.1 Revenue............................................................................................................................8

4.2 Corporation Tax Expense.................................................................................................8

4.3 Amounts Due to Shareholders.........................................................................................8

4.4 Changes in Equity............................................................................................................8

5.0 References..........................................................................................................................10

Appendix..................................................................................................................................12

1. Letter of Appointment......................................................................................................12

2. Minutes for Appointing Auditor......................................................................................12

3. Proposed Audit Adjustment.............................................................................................13

Table of Contents

1.0 Directors Report...................................................................................................................3

1.1 Brief Introduction.............................................................................................................3

1.2 Principle Activity.............................................................................................................3

1.3 Directors...........................................................................................................................3

1.4 Business Review..............................................................................................................3

1.5 Permitted Indemnity Provision........................................................................................4

1.6 Auditor.............................................................................................................................4

2.0 Independent Auditor’s Report..............................................................................................4

2.1 Title of the Auditor...........................................................................................................4

2.2 Opinion on Financial Statements.....................................................................................4

2.3 Basis for Opinion.............................................................................................................5

2.4 Additional Information Other Than Financial Statements...............................................5

2.5 Directors Responsibility...................................................................................................5

2.6 Auditor’s Responsibility..................................................................................................5

3.0 Income Statement.................................................................................................................6

4.0 Financial Position.................................................................................................................6

4.1 Revenue............................................................................................................................8

4.2 Corporation Tax Expense.................................................................................................8

4.3 Amounts Due to Shareholders.........................................................................................8

4.4 Changes in Equity............................................................................................................8

5.0 References..........................................................................................................................10

Appendix..................................................................................................................................12

1. Letter of Appointment......................................................................................................12

2. Minutes for Appointing Auditor......................................................................................12

3. Proposed Audit Adjustment.............................................................................................13

3AUDITING

1.0 Directors Report

1.1 Brief Introduction

Brexit Capital Limited has incurred losses in the year 2019. The company conducts various

business transactions within the market. The company has four key shareholders, who have

contributed well in the organisation but the asset of these shareholders can lose on demand. In

the current condition, it has been found that the growth of the company is poor.

1.2 Principle Activity

Principle activity can be defined as the process, which promotes value-added business or

financial activity, which can help in growing and making strong economic conditions for the

company (Tilastokeskus n.d.). In relation to Brexit Capital Limited, the company follows

party confirmation process for establishing a legal business. In this process, Brexit Capital

Limited provided disclose account form to know the loan amount and security type, which

can be considered to be the principal activity of the company.

1.3 Directors

The director plays a major role in any organisation because people of the entire organisation

have good faith in that person. In addition, the director must have the proper interest, skill,

and diligence towards the organisation (Delotte 2013). Dwi Jaya is the director of Brexit

Capital Limited, wherein three people are helping her to develop the business i.e. Dwi Mulia,

Dikari, and Tan Khin Pin.

1.4 Business Review

Based on the current report, Brexit Capital Limited is facing loss. It can be considered to be

bad for the organisation, as it can lead the company towards insolvency.

1.0 Directors Report

1.1 Brief Introduction

Brexit Capital Limited has incurred losses in the year 2019. The company conducts various

business transactions within the market. The company has four key shareholders, who have

contributed well in the organisation but the asset of these shareholders can lose on demand. In

the current condition, it has been found that the growth of the company is poor.

1.2 Principle Activity

Principle activity can be defined as the process, which promotes value-added business or

financial activity, which can help in growing and making strong economic conditions for the

company (Tilastokeskus n.d.). In relation to Brexit Capital Limited, the company follows

party confirmation process for establishing a legal business. In this process, Brexit Capital

Limited provided disclose account form to know the loan amount and security type, which

can be considered to be the principal activity of the company.

1.3 Directors

The director plays a major role in any organisation because people of the entire organisation

have good faith in that person. In addition, the director must have the proper interest, skill,

and diligence towards the organisation (Delotte 2013). Dwi Jaya is the director of Brexit

Capital Limited, wherein three people are helping her to develop the business i.e. Dwi Mulia,

Dikari, and Tan Khin Pin.

1.4 Business Review

Based on the current report, Brexit Capital Limited is facing loss. It can be considered to be

bad for the organisation, as it can lead the company towards insolvency.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDITING

1.5 Permitted Indemnity Provision

Permitted Indemnity Provision can be referred to as a legal process, which provides security

against the liability (Companies Registry 2012). In relation to Brexit Capital Limited, the

company has four major shareholders i.e. Dwi Mulia, Dikari, Tan Khin Pin, and Dwi Jaya

with a liability of 34,779 GBP, 15,979.57 GBP, 51,693 GBP, and 14,984 GBP respectively.

1.6 Auditor

Brexit Capital Limited hired UWL C.P.A as the auditor, which will focus on analysing the

financial background of the organisation. The company does not have any personal auditor.

2.0 Independent Auditor’s Report

2.1 Title of the Auditor

A Chartered accountant of UWL C.P.A is the main auditor in this case. The entire account of

Brexit Capital Limited has been properly checked by the above-mentioned charter

accountant. It will help the company to grow its business effectively.

2.2 Opinion on Financial Statements

The company prepares reports, which include Trial Balance, Balance Sheet, Ledger Account,

and Profit/Loss account. Each of the statements has certain drawbacks, which need to be

improved by the company. In relation to the trial balance, the company does not record all its

business activities in the financial book such as revenue activities. Only interest paid has been

reflected by the company. Other revenue activities are not shown properly. In relation to the

balance sheet, the company does not reflect any kind of assets and its depreciation value. The

working capital is not included in the report.

1.5 Permitted Indemnity Provision

Permitted Indemnity Provision can be referred to as a legal process, which provides security

against the liability (Companies Registry 2012). In relation to Brexit Capital Limited, the

company has four major shareholders i.e. Dwi Mulia, Dikari, Tan Khin Pin, and Dwi Jaya

with a liability of 34,779 GBP, 15,979.57 GBP, 51,693 GBP, and 14,984 GBP respectively.

1.6 Auditor

Brexit Capital Limited hired UWL C.P.A as the auditor, which will focus on analysing the

financial background of the organisation. The company does not have any personal auditor.

2.0 Independent Auditor’s Report

2.1 Title of the Auditor

A Chartered accountant of UWL C.P.A is the main auditor in this case. The entire account of

Brexit Capital Limited has been properly checked by the above-mentioned charter

accountant. It will help the company to grow its business effectively.

2.2 Opinion on Financial Statements

The company prepares reports, which include Trial Balance, Balance Sheet, Ledger Account,

and Profit/Loss account. Each of the statements has certain drawbacks, which need to be

improved by the company. In relation to the trial balance, the company does not record all its

business activities in the financial book such as revenue activities. Only interest paid has been

reflected by the company. Other revenue activities are not shown properly. In relation to the

balance sheet, the company does not reflect any kind of assets and its depreciation value. The

working capital is not included in the report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDITING

2.3 Basis for Opinion

Based on the above-mentioned information related to the financial statements, it can be stated

that the presented report of the company is not adequate for to analysing and understanding

the position of the company. The financial strength of the organisation cannot be understood

without the proper valuation of the company’s assets. In addition, the goodwill and

shareholder’s assurance cannot be determined, if a firm does not reflect the asset activity

(Invest Northern Ireland, n.d.). On the other hand, depreciation is the historical value of any

asset, which helps the shareholders to know the organisational capability relating to return on

asset (Thomason 2019).

2.4 Additional Information Other Than Financial Statements

Stakeholders have a major impact on any organisation (Matuleviciene & Stravinskiene 2015).

With respect to Brexit Capital Limited, the report of the company is not does not include any

relevant information. The shareholders of the company are at risk due to the lack of

information related to assets and other income activities within the market. This can help in

obtaining an inaccurate result, which can lead the company towards a complete disaster.

2.5 Directors Responsibility

The director of Brexit Capital Limited has the responsibility to consult with the management

prior to publishing any action, decision, and report. The performance of a company must be

assessed by the director, which can be considered to be one of the major responsibilities

(Larcker & Tayan 2015).

2.6 Auditor’s Responsibility

An auditor has the responsibility to find fraudulence in the financial books. The auditor must

guide the organisation if any misstatement is conducted in the financial books. An

organisation cannot survive in the market without an assistance of a skilled auditor. It

2.3 Basis for Opinion

Based on the above-mentioned information related to the financial statements, it can be stated

that the presented report of the company is not adequate for to analysing and understanding

the position of the company. The financial strength of the organisation cannot be understood

without the proper valuation of the company’s assets. In addition, the goodwill and

shareholder’s assurance cannot be determined, if a firm does not reflect the asset activity

(Invest Northern Ireland, n.d.). On the other hand, depreciation is the historical value of any

asset, which helps the shareholders to know the organisational capability relating to return on

asset (Thomason 2019).

2.4 Additional Information Other Than Financial Statements

Stakeholders have a major impact on any organisation (Matuleviciene & Stravinskiene 2015).

With respect to Brexit Capital Limited, the report of the company is not does not include any

relevant information. The shareholders of the company are at risk due to the lack of

information related to assets and other income activities within the market. This can help in

obtaining an inaccurate result, which can lead the company towards a complete disaster.

2.5 Directors Responsibility

The director of Brexit Capital Limited has the responsibility to consult with the management

prior to publishing any action, decision, and report. The performance of a company must be

assessed by the director, which can be considered to be one of the major responsibilities

(Larcker & Tayan 2015).

2.6 Auditor’s Responsibility

An auditor has the responsibility to find fraudulence in the financial books. The auditor must

guide the organisation if any misstatement is conducted in the financial books. An

organisation cannot survive in the market without an assistance of a skilled auditor. It

6AUDITING

significantly helps in ensuring the integrity of the financial books (Zagera, Malis, & Nova

2016).

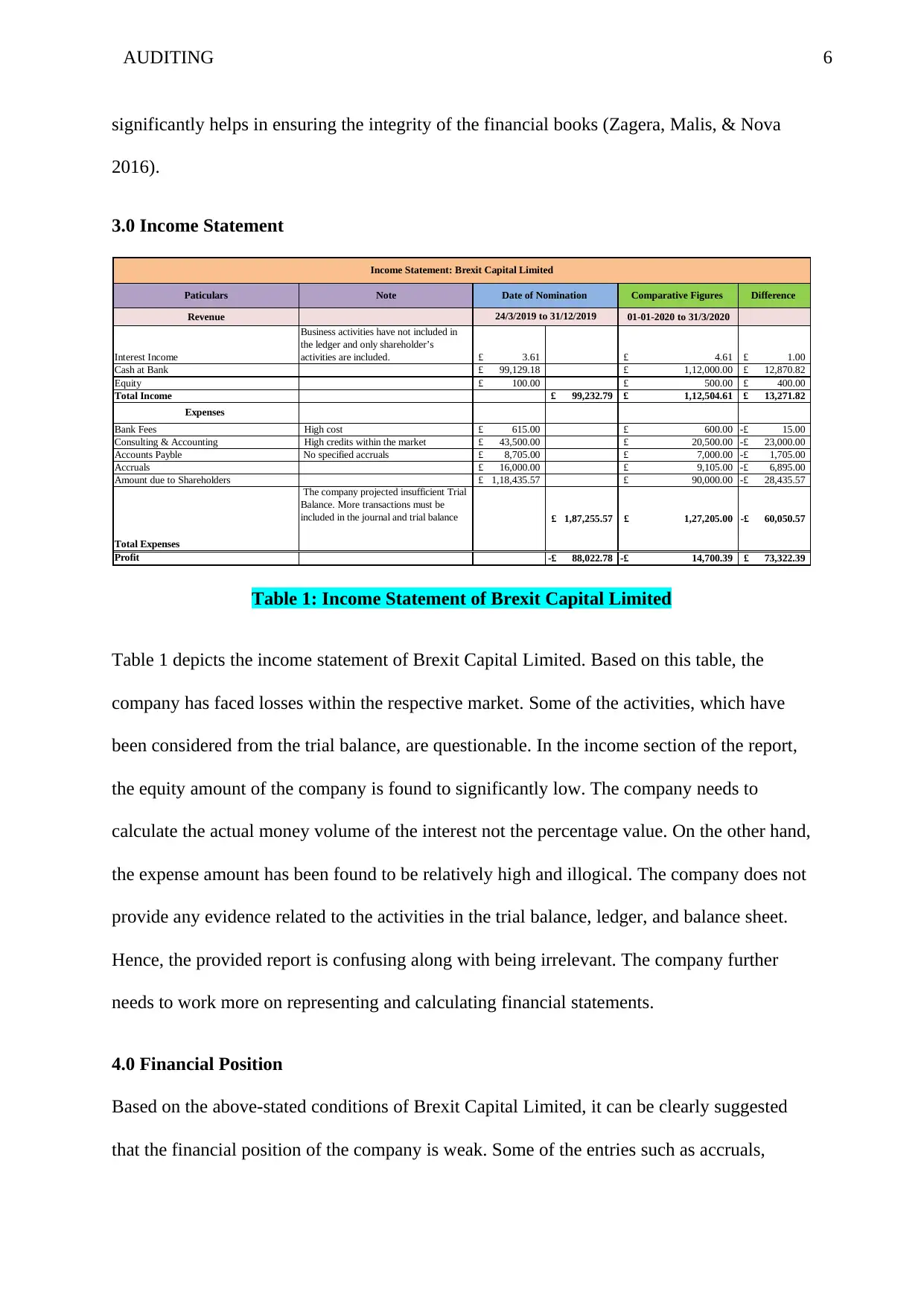

3.0 Income Statement

Paticulars Note Comparative Figures Difference

Revenue 01-01-2020 to 31/3/2020

Interest Income

Business activities have not included in

the ledger and only shareholder’s

activities are included. 3.61£ 4.61£ 1.00£

Cash at Bank 99,129.18£ 1,12,000.00£ 12,870.82£

Equity 100.00£ 500.00£ 400.00£

Total Income 99,232.79£ 1,12,504.61£ 13,271.82£

Expenses

Bank Fees High cost 615.00£ 600.00£ 15.00-£

Consulting & Accounting High credits within the market 43,500.00£ 20,500.00£ 23,000.00-£

Accounts Payble No specified accruals 8,705.00£ 7,000.00£ 1,705.00-£

Accruals 16,000.00£ 9,105.00£ 6,895.00-£

Amount due to Shareholders 1,18,435.57£ 90,000.00£ 28,435.57-£

Total Expenses

The company projected insufficient Trial

Balance. More transactions must be

included in the journal and trial balance 1,87,255.57£ 1,27,205.00£ 60,050.57-£

Profit 88,022.78-£ 14,700.39-£ 73,322.39£

24/3/2019 to 31/12/2019

Date of Nomination

Income Statement: Brexit Capital Limited

Table 1: Income Statement of Brexit Capital Limited

Table 1 depicts the income statement of Brexit Capital Limited. Based on this table, the

company has faced losses within the respective market. Some of the activities, which have

been considered from the trial balance, are questionable. In the income section of the report,

the equity amount of the company is found to significantly low. The company needs to

calculate the actual money volume of the interest not the percentage value. On the other hand,

the expense amount has been found to be relatively high and illogical. The company does not

provide any evidence related to the activities in the trial balance, ledger, and balance sheet.

Hence, the provided report is confusing along with being irrelevant. The company further

needs to work more on representing and calculating financial statements.

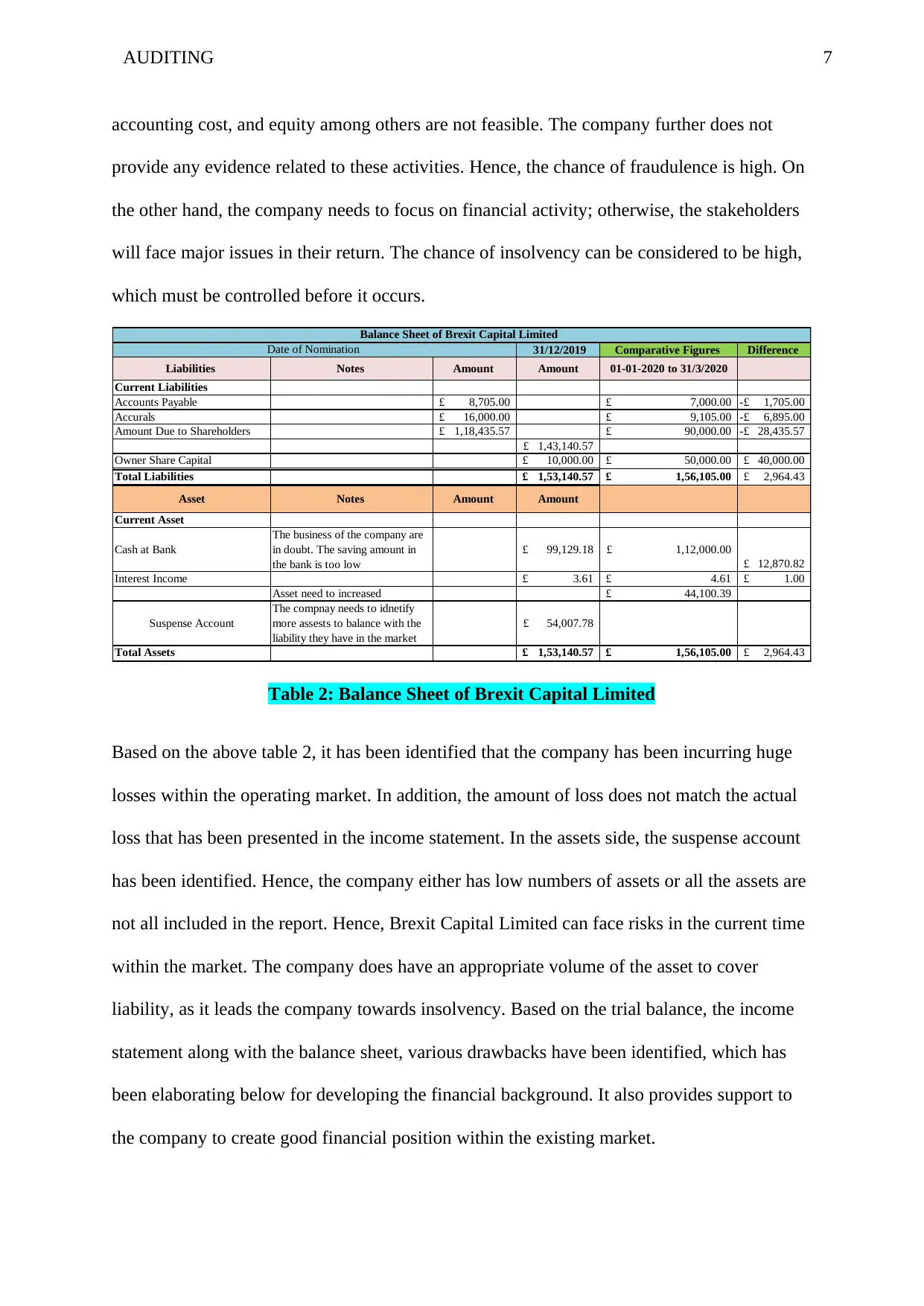

4.0 Financial Position

Based on the above-stated conditions of Brexit Capital Limited, it can be clearly suggested

that the financial position of the company is weak. Some of the entries such as accruals,

significantly helps in ensuring the integrity of the financial books (Zagera, Malis, & Nova

2016).

3.0 Income Statement

Paticulars Note Comparative Figures Difference

Revenue 01-01-2020 to 31/3/2020

Interest Income

Business activities have not included in

the ledger and only shareholder’s

activities are included. 3.61£ 4.61£ 1.00£

Cash at Bank 99,129.18£ 1,12,000.00£ 12,870.82£

Equity 100.00£ 500.00£ 400.00£

Total Income 99,232.79£ 1,12,504.61£ 13,271.82£

Expenses

Bank Fees High cost 615.00£ 600.00£ 15.00-£

Consulting & Accounting High credits within the market 43,500.00£ 20,500.00£ 23,000.00-£

Accounts Payble No specified accruals 8,705.00£ 7,000.00£ 1,705.00-£

Accruals 16,000.00£ 9,105.00£ 6,895.00-£

Amount due to Shareholders 1,18,435.57£ 90,000.00£ 28,435.57-£

Total Expenses

The company projected insufficient Trial

Balance. More transactions must be

included in the journal and trial balance 1,87,255.57£ 1,27,205.00£ 60,050.57-£

Profit 88,022.78-£ 14,700.39-£ 73,322.39£

24/3/2019 to 31/12/2019

Date of Nomination

Income Statement: Brexit Capital Limited

Table 1: Income Statement of Brexit Capital Limited

Table 1 depicts the income statement of Brexit Capital Limited. Based on this table, the

company has faced losses within the respective market. Some of the activities, which have

been considered from the trial balance, are questionable. In the income section of the report,

the equity amount of the company is found to significantly low. The company needs to

calculate the actual money volume of the interest not the percentage value. On the other hand,

the expense amount has been found to be relatively high and illogical. The company does not

provide any evidence related to the activities in the trial balance, ledger, and balance sheet.

Hence, the provided report is confusing along with being irrelevant. The company further

needs to work more on representing and calculating financial statements.

4.0 Financial Position

Based on the above-stated conditions of Brexit Capital Limited, it can be clearly suggested

that the financial position of the company is weak. Some of the entries such as accruals,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDITING

accounting cost, and equity among others are not feasible. The company further does not

provide any evidence related to these activities. Hence, the chance of fraudulence is high. On

the other hand, the company needs to focus on financial activity; otherwise, the stakeholders

will face major issues in their return. The chance of insolvency can be considered to be high,

which must be controlled before it occurs.

31/12/2019 Comparative Figures Difference

Liabilities Notes Amount Amount 01-01-2020 to 31/3/2020

Current Liabilities

Accounts Payable 8,705.00£ 7,000.00£ 1,705.00-£

Accurals 16,000.00£ 9,105.00£ 6,895.00-£

Amount Due to Shareholders 1,18,435.57£ 90,000.00£ 28,435.57-£

1,43,140.57£

Owner Share Capital 10,000.00£ 50,000.00£ 40,000.00£

Total Liabilities 1,53,140.57£ 1,56,105.00£ 2,964.43£

Asset Notes Amount Amount

Current Asset

Cash at Bank

The business of the company are

in doubt. The saving amount in

the bank is too low

99,129.18£ 1,12,000.00£

12,870.82£

Interest Income 3.61£ 4.61£ 1.00£

Asset need to increased 44,100.39£

Suspense Account

The compnay needs to idnetify

more assests to balance with the

liability they have in the market

54,007.78£

Total Assets 1,53,140.57£ 1,56,105.00£ 2,964.43£

Date of Nomination

Balance Sheet of Brexit Capital Limited

Table 2: Balance Sheet of Brexit Capital Limited

Based on the above table 2, it has been identified that the company has been incurring huge

losses within the operating market. In addition, the amount of loss does not match the actual

loss that has been presented in the income statement. In the assets side, the suspense account

has been identified. Hence, the company either has low numbers of assets or all the assets are

not all included in the report. Hence, Brexit Capital Limited can face risks in the current time

within the market. The company does have an appropriate volume of the asset to cover

liability, as it leads the company towards insolvency. Based on the trial balance, the income

statement along with the balance sheet, various drawbacks have been identified, which has

been elaborating below for developing the financial background. It also provides support to

the company to create good financial position within the existing market.

accounting cost, and equity among others are not feasible. The company further does not

provide any evidence related to these activities. Hence, the chance of fraudulence is high. On

the other hand, the company needs to focus on financial activity; otherwise, the stakeholders

will face major issues in their return. The chance of insolvency can be considered to be high,

which must be controlled before it occurs.

31/12/2019 Comparative Figures Difference

Liabilities Notes Amount Amount 01-01-2020 to 31/3/2020

Current Liabilities

Accounts Payable 8,705.00£ 7,000.00£ 1,705.00-£

Accurals 16,000.00£ 9,105.00£ 6,895.00-£

Amount Due to Shareholders 1,18,435.57£ 90,000.00£ 28,435.57-£

1,43,140.57£

Owner Share Capital 10,000.00£ 50,000.00£ 40,000.00£

Total Liabilities 1,53,140.57£ 1,56,105.00£ 2,964.43£

Asset Notes Amount Amount

Current Asset

Cash at Bank

The business of the company are

in doubt. The saving amount in

the bank is too low

99,129.18£ 1,12,000.00£

12,870.82£

Interest Income 3.61£ 4.61£ 1.00£

Asset need to increased 44,100.39£

Suspense Account

The compnay needs to idnetify

more assests to balance with the

liability they have in the market

54,007.78£

Total Assets 1,53,140.57£ 1,56,105.00£ 2,964.43£

Date of Nomination

Balance Sheet of Brexit Capital Limited

Table 2: Balance Sheet of Brexit Capital Limited

Based on the above table 2, it has been identified that the company has been incurring huge

losses within the operating market. In addition, the amount of loss does not match the actual

loss that has been presented in the income statement. In the assets side, the suspense account

has been identified. Hence, the company either has low numbers of assets or all the assets are

not all included in the report. Hence, Brexit Capital Limited can face risks in the current time

within the market. The company does have an appropriate volume of the asset to cover

liability, as it leads the company towards insolvency. Based on the trial balance, the income

statement along with the balance sheet, various drawbacks have been identified, which has

been elaborating below for developing the financial background. It also provides support to

the company to create good financial position within the existing market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDITING

4.1 Revenue

Primarily, the calculating revenue can help an organisation to determine the company’s value.

In addition, it assists in understanding the financial strength of an organisation (Chandra &

Ro 2014). In relation to Brexit Capital Limited, the company does not show revenue activities

in the financial books.

4.2 Corporation Tax Expense

The corporation tax expense is one of the major aspects for any organisation, as it reflects

valuable business activities such as income tax, business tax, and personal tax among others

(Tax Justice Network 2020). The accountants of Brexit Capital Limited do not include any

kind of tax activity in the report.

4.3 Amounts Due to Shareholders

Every shareholder has the right to claim his or her money from the organisation after the

earning profit (Office of the Director of Corporate Enforcement, 2009). Brexit Capital

Limited is unable to pay back to major shareholders of the company i.e. Dwi Mulia, Dikari,

Tan Khin Pin, and Dwi Jaya. The company needs to focus on earning business revenue to

develop the situation in an effective manner.

4.4 Changes in Equity

Equity refers to the amount that is paid to the shareholders of the company. Hence, change in

equity or low equity can be viewed to be dangerous for any organisation, as it acts as a good

source of money, which helped in increasing the revenue within the market (EFRAG 2008).

In relation to Brexit Capital Limited, the company has to show equity in the report. Though

the company faced loss in the market, it can resolve whether they focus on revenue

management.

4.1 Revenue

Primarily, the calculating revenue can help an organisation to determine the company’s value.

In addition, it assists in understanding the financial strength of an organisation (Chandra &

Ro 2014). In relation to Brexit Capital Limited, the company does not show revenue activities

in the financial books.

4.2 Corporation Tax Expense

The corporation tax expense is one of the major aspects for any organisation, as it reflects

valuable business activities such as income tax, business tax, and personal tax among others

(Tax Justice Network 2020). The accountants of Brexit Capital Limited do not include any

kind of tax activity in the report.

4.3 Amounts Due to Shareholders

Every shareholder has the right to claim his or her money from the organisation after the

earning profit (Office of the Director of Corporate Enforcement, 2009). Brexit Capital

Limited is unable to pay back to major shareholders of the company i.e. Dwi Mulia, Dikari,

Tan Khin Pin, and Dwi Jaya. The company needs to focus on earning business revenue to

develop the situation in an effective manner.

4.4 Changes in Equity

Equity refers to the amount that is paid to the shareholders of the company. Hence, change in

equity or low equity can be viewed to be dangerous for any organisation, as it acts as a good

source of money, which helped in increasing the revenue within the market (EFRAG 2008).

In relation to Brexit Capital Limited, the company has to show equity in the report. Though

the company faced loss in the market, it can resolve whether they focus on revenue

management.

9AUDITING

Based on the current condition of Brexit Capital Limited, it can be recommended that the

company has been facing a huge risk in the market. The financial condition must develop

within six months. On the other hand, Brexit Capital Limited may project inaccurate financial

activities. Fraudulence has been detected somewhere in the financial statements such as

assets, undefined accruals, high cost and no data associated with the company revenue.

Based on the current condition of Brexit Capital Limited, it can be recommended that the

company has been facing a huge risk in the market. The financial condition must develop

within six months. On the other hand, Brexit Capital Limited may project inaccurate financial

activities. Fraudulence has been detected somewhere in the financial statements such as

assets, undefined accruals, high cost and no data associated with the company revenue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDITING

5.0 References

Chandra, U. & Ro, B. T. (2014). The role of revenue in firm valuation. American Accounting

Association. 22(2), pp.199–222.

Companies Registry. (2012). Directors and company secretaries. Companies Ordinance.

pp.A4183- A4235.

Delotte. (2013). Duties of directors. A Key Feature of the Companies Act, 2008 (The Act) is

that It Clearly Emphasises the Responsibility and Accountability of Directors. pp.1-81.

EFRAG. (2008). Discussion paper distinguishing between liabilities and equity. Pro-Active

Accounting Activities In Europe (PAAinE). pp.1-95.

Invest Northern Ireland. (no date)) Importance of assets in business [online]. Available from:

https://www.nibusinessinfo.co.uk/content/importance-assets-business [Accessed 11 February

2020].

Larcker, D. F. & Tayan, B. (2015). Board of directors duties and liabilities. Stanford

Graduate School of Business. pp.1-18.

Matuleviciene, M. & Stravinskiene, J. (2015). The importance of stakeholders for corporate

reputation. Inzinerine Ekonomika-Engineering Economics. 26(1), pp.75-83.

Office of the Director of Corporate Enforcement. (2009). Members and shareholders their

duties and rights. A Quick Guide. pp.1-8.

Tax Justice Network. (2020). Taxing corporations [online]. Available from:

https://www.taxjustice.net/topics/corporate-tax/taxing-corporations/ [Accessed 11 February

2020].

5.0 References

Chandra, U. & Ro, B. T. (2014). The role of revenue in firm valuation. American Accounting

Association. 22(2), pp.199–222.

Companies Registry. (2012). Directors and company secretaries. Companies Ordinance.

pp.A4183- A4235.

Delotte. (2013). Duties of directors. A Key Feature of the Companies Act, 2008 (The Act) is

that It Clearly Emphasises the Responsibility and Accountability of Directors. pp.1-81.

EFRAG. (2008). Discussion paper distinguishing between liabilities and equity. Pro-Active

Accounting Activities In Europe (PAAinE). pp.1-95.

Invest Northern Ireland. (no date)) Importance of assets in business [online]. Available from:

https://www.nibusinessinfo.co.uk/content/importance-assets-business [Accessed 11 February

2020].

Larcker, D. F. & Tayan, B. (2015). Board of directors duties and liabilities. Stanford

Graduate School of Business. pp.1-18.

Matuleviciene, M. & Stravinskiene, J. (2015). The importance of stakeholders for corporate

reputation. Inzinerine Ekonomika-Engineering Economics. 26(1), pp.75-83.

Office of the Director of Corporate Enforcement. (2009). Members and shareholders their

duties and rights. A Quick Guide. pp.1-8.

Tax Justice Network. (2020). Taxing corporations [online]. Available from:

https://www.taxjustice.net/topics/corporate-tax/taxing-corporations/ [Accessed 11 February

2020].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDITING

Thomason, K. (2019). Why is depreciation important in accounting? [online]. Available

from: https://bizfluent.com/how-7295406-disposal-leasehold-improvements.html [Accessed

11 February 2020].

Tilastokeskus. (no date). Principal activity [online]. Available from:

https://www.stat.fi/meta/kas/paatoimiala_en.html [Accessed 11 February 2020].

Zagera, L., Malis, S.S. & Nova, A. (2016). The role and responsibility of auditors in

prevention and detection of fraudulent financial reporting. Procedia Economics and Finance.

39, pp.693-700.

Thomason, K. (2019). Why is depreciation important in accounting? [online]. Available

from: https://bizfluent.com/how-7295406-disposal-leasehold-improvements.html [Accessed

11 February 2020].

Tilastokeskus. (no date). Principal activity [online]. Available from:

https://www.stat.fi/meta/kas/paatoimiala_en.html [Accessed 11 February 2020].

Zagera, L., Malis, S.S. & Nova, A. (2016). The role and responsibility of auditors in

prevention and detection of fraudulent financial reporting. Procedia Economics and Finance.

39, pp.693-700.

12AUDITING

Appendix

1. Letter of Appointment

Date

Dear UWL C.P.A,

On behalf of Brexit Capital Limited, I am happy to inform you that company has been

appointed as the auditor for conducting the audit procedure for financial year 2019-2020 on

the books of you company.

I have further enclosed the agreement. I request for your confirmation to accept the offer at

earliest.

Regards,

Brexit Capital Limited

2. Minutes for Appointing Auditor

MEMBERS PRESENT:

1. Dwi Jaya: Director

2. Dwi Mulia: Shareholder

3. Dikari: Shareholder

4. Tan Khin Pin: Shareholder

IN PRESENCE:

Statutory Auditors of UWL C.P.A

Scrutinizer & Secretarial Auditor to Remote Evoting

Details of the Minute:

The audit will be conducted at 11 February 2020 at 11 am

The names of the auditing firm and auditors

Appendix

1. Letter of Appointment

Date

Dear UWL C.P.A,

On behalf of Brexit Capital Limited, I am happy to inform you that company has been

appointed as the auditor for conducting the audit procedure for financial year 2019-2020 on

the books of you company.

I have further enclosed the agreement. I request for your confirmation to accept the offer at

earliest.

Regards,

Brexit Capital Limited

2. Minutes for Appointing Auditor

MEMBERS PRESENT:

1. Dwi Jaya: Director

2. Dwi Mulia: Shareholder

3. Dikari: Shareholder

4. Tan Khin Pin: Shareholder

IN PRESENCE:

Statutory Auditors of UWL C.P.A

Scrutinizer & Secretarial Auditor to Remote Evoting

Details of the Minute:

The audit will be conducted at 11 February 2020 at 11 am

The names of the auditing firm and auditors

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.