Macroeconomics Report: Brexit, Fiscal Policy, and Interest Rates

VerifiedAdded on 2023/06/10

|10

|2173

|271

Report

AI Summary

This macroeconomics report delves into the economic consequences of the Brexit referendum on the United Kingdom. It examines the slowdown in economic growth, currency depreciation, and the challenges faced by policymakers in formulating effective fiscal policies. The report analyzes the government's options in managing public debt, including spending cuts, tax increases, and the limitations of fiscal policy in the face of uncertainty. It also explores the potential of monetary policy and structural reforms, drawing parallels with Japan's Abenomics strategy. Furthermore, the report investigates the factors influencing interest rate decisions by central banks, including monetary stability, economic growth, unemployment rates, and spare capacity. It highlights how these factors impact consumption, investment, and overall economic activity, providing a comprehensive overview of macroeconomic dynamics in the context of Brexit and beyond.

Running Head: MACROECONOMICS

Macroeconomics

Name of the Student

Name of the University

Course ID

Macroeconomics

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MACROECONOMICS

Table of Contents

Answer to question 1.......................................................................................................................2

Brexit referendum and effectiveness of fiscal policy..................................................................2

Answer to question 2.......................................................................................................................4

Factors affecting interest rate decision........................................................................................4

References list..................................................................................................................................8

Table of Contents

Answer to question 1.......................................................................................................................2

Brexit referendum and effectiveness of fiscal policy..................................................................2

Answer to question 2.......................................................................................................................4

Factors affecting interest rate decision........................................................................................4

References list..................................................................................................................................8

2MACROECONOMICS

Answer to question 1

Brexit referendum and effectiveness of fiscal policy

Prior to Brexit in June, 2016 United Kingdom was one of the fastest growing nation

across the world. However, after Brexit economic growth has significantly slowed down

following internal and external changes in the economy. Slow economic growth in United

Kingdom is representative of a material loss of Britain in the global market. Productivity growth

has been slowed down with output per hour remained almost flat or declined. Another factor

contributing to a sluggish economic growth is depreciation of currency (Young 2017).

Depreciation of sterling results in an increase in price of exported item leading to a deficit in

trade balance. The economy thus in a need of effective policy support from government and

regulatory authority.

Government in an economy can provide stimulus to the economy either through fiscal

policy or through monetary policy. The policymakers are facing problem in formulating suitable

policies in a phase of uncertainty about future productivity growth. The Office for Budget

Responsibility (OBR) assumed productivity growth to be increased from a current rate of 1.4

percent to 1.8 percent but 2021. Despite the slow productivity growth, policy maker still remains

optimistic about economic recovery as experienced after global financial crisis in 2008. Based

upon these assumptions government announced no change in spending plans and hoped to

maintain a balanced budget (Johnson and Mitchell 2017). However, there remain substantial risk

regarding the assumption of productivity growth and hence, design and effectiveness of fiscal

policy. If weak productivity is continued for a very long period, then government might

experience a net borrowing of substantial size.

Answer to question 1

Brexit referendum and effectiveness of fiscal policy

Prior to Brexit in June, 2016 United Kingdom was one of the fastest growing nation

across the world. However, after Brexit economic growth has significantly slowed down

following internal and external changes in the economy. Slow economic growth in United

Kingdom is representative of a material loss of Britain in the global market. Productivity growth

has been slowed down with output per hour remained almost flat or declined. Another factor

contributing to a sluggish economic growth is depreciation of currency (Young 2017).

Depreciation of sterling results in an increase in price of exported item leading to a deficit in

trade balance. The economy thus in a need of effective policy support from government and

regulatory authority.

Government in an economy can provide stimulus to the economy either through fiscal

policy or through monetary policy. The policymakers are facing problem in formulating suitable

policies in a phase of uncertainty about future productivity growth. The Office for Budget

Responsibility (OBR) assumed productivity growth to be increased from a current rate of 1.4

percent to 1.8 percent but 2021. Despite the slow productivity growth, policy maker still remains

optimistic about economic recovery as experienced after global financial crisis in 2008. Based

upon these assumptions government announced no change in spending plans and hoped to

maintain a balanced budget (Johnson and Mitchell 2017). However, there remain substantial risk

regarding the assumption of productivity growth and hence, design and effectiveness of fiscal

policy. If weak productivity is continued for a very long period, then government might

experience a net borrowing of substantial size.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MACROECONOMICS

On the front of fiscal policy government then has three option to cut the net borrowing.

First is to maintain a tight policy regarding government spending. Second is to increase tax rate

and third is to accept that it is not possible to achieve a balanced budget in the next few years.

People have less tendency to accept a tighter government spending (Sinn 2018). United

Kingdom’s current government is not at all high and a further reduction might report in an

austerity fatigue. This indicates higher taxes to be a more preferable option. Given current

economic and political environment, increasing taxes might prove unpalatable.

United Kingdom government therefore seeks to utilize full fiscal space in line with

existing rules to accommodate post-Brexit economic scenario. In this regards, government aims

to reduce net borrowing of the public sector below 2 percent and a gradual decline of net debt of

public sector as a percentage of GDP. The focus of United Kingdom government to reduces

public debt as a percentage of GDP is however misplaced. A portion of public debt is going to

the service sector which is unlikely to undergo sudden change (Thompson 2017).

Fiscal policy is able to provide necessary stimulus to the economy in the form of rising

government expenditure or reducing tax rate. Fallacy of fiscal policy is that it might end up with

huge public debt. The Increased net borrowing has a detrimental effect on the economy. In order

to recover public borrowing government needs to take a tight fiscal policy (Miles, Scott and

Breedon 2012). The contractionary fiscal policy tends to create resentment in the economy. In a

phase of uncertain economic and political environment, people are unlikely to accept either a

decline in government spending or an increase in the tax rate (Gudgin et al. 2018). Fiscal policy

thus can make short term recovery but at the cost of reducing long term growth prospects.

United Kingdom needs a more comprehensive approach to make quick recovery from

post-Brexit shock. More preciously, the strategic version of Abenomics is now more suitable in

On the front of fiscal policy government then has three option to cut the net borrowing.

First is to maintain a tight policy regarding government spending. Second is to increase tax rate

and third is to accept that it is not possible to achieve a balanced budget in the next few years.

People have less tendency to accept a tighter government spending (Sinn 2018). United

Kingdom’s current government is not at all high and a further reduction might report in an

austerity fatigue. This indicates higher taxes to be a more preferable option. Given current

economic and political environment, increasing taxes might prove unpalatable.

United Kingdom government therefore seeks to utilize full fiscal space in line with

existing rules to accommodate post-Brexit economic scenario. In this regards, government aims

to reduce net borrowing of the public sector below 2 percent and a gradual decline of net debt of

public sector as a percentage of GDP. The focus of United Kingdom government to reduces

public debt as a percentage of GDP is however misplaced. A portion of public debt is going to

the service sector which is unlikely to undergo sudden change (Thompson 2017).

Fiscal policy is able to provide necessary stimulus to the economy in the form of rising

government expenditure or reducing tax rate. Fallacy of fiscal policy is that it might end up with

huge public debt. The Increased net borrowing has a detrimental effect on the economy. In order

to recover public borrowing government needs to take a tight fiscal policy (Miles, Scott and

Breedon 2012). The contractionary fiscal policy tends to create resentment in the economy. In a

phase of uncertain economic and political environment, people are unlikely to accept either a

decline in government spending or an increase in the tax rate (Gudgin et al. 2018). Fiscal policy

thus can make short term recovery but at the cost of reducing long term growth prospects.

United Kingdom needs a more comprehensive approach to make quick recovery from

post-Brexit shock. More preciously, the strategic version of Abenomics is now more suitable in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MACROECONOMICS

context of United Kingdom economy. The strategy of Abenomics as proposed by Japan’s prime

minister, Shinzo Abe, has three components monetary policy, fiscal policy and structural reform.

The monetary policy in United Kingdom is designed by Bank of England. BOE controls

economic activity by influencing borrowing cost, exchanging securities through open market

operation, changing supply of money or through different lending and funding program. The

monetary policy has the advantage that it can stimulate economic activity in the quickest possible

ways. This is reason why monetary policy is considered as the first escape route from recession

in the post-Brexit period (theguardian.com 2018). Structural reform involve change in the

structure of the economy to make it work more effectively. This include reform in health and

education system and infrastructural development.

The economy needs to understand that Brexit has a long term implication for the

economy that cannot be healed with short term policy measures. Rather it needs a combination to

sustainable policies to bring back the economy to the previous path of growth and development.

Answer to question 2

Factors affecting interest rate decision

In the phase of sudden economic shocks, macroeconomic stability of an economy gets

disturbed. Such sudden shocks are unlikely to be overcome in the hands of free market forces.

Instead, it needs government intervention to overcome the shock and restore economic stability.

Monetary policy is a demand side policy to control economic activity. Central bank of a nation

has the responsibility of designing monetary policy (Goodwin et al. 2015). The common tool

used by the central bank is interest rate. Interest rate is the cost of borrowing fund. A change in

interest rate by changing borrowing cost affects consumption and investment decision. An

context of United Kingdom economy. The strategy of Abenomics as proposed by Japan’s prime

minister, Shinzo Abe, has three components monetary policy, fiscal policy and structural reform.

The monetary policy in United Kingdom is designed by Bank of England. BOE controls

economic activity by influencing borrowing cost, exchanging securities through open market

operation, changing supply of money or through different lending and funding program. The

monetary policy has the advantage that it can stimulate economic activity in the quickest possible

ways. This is reason why monetary policy is considered as the first escape route from recession

in the post-Brexit period (theguardian.com 2018). Structural reform involve change in the

structure of the economy to make it work more effectively. This include reform in health and

education system and infrastructural development.

The economy needs to understand that Brexit has a long term implication for the

economy that cannot be healed with short term policy measures. Rather it needs a combination to

sustainable policies to bring back the economy to the previous path of growth and development.

Answer to question 2

Factors affecting interest rate decision

In the phase of sudden economic shocks, macroeconomic stability of an economy gets

disturbed. Such sudden shocks are unlikely to be overcome in the hands of free market forces.

Instead, it needs government intervention to overcome the shock and restore economic stability.

Monetary policy is a demand side policy to control economic activity. Central bank of a nation

has the responsibility of designing monetary policy (Goodwin et al. 2015). The common tool

used by the central bank is interest rate. Interest rate is the cost of borrowing fund. A change in

interest rate by changing borrowing cost affects consumption and investment decision. An

5MACROECONOMICS

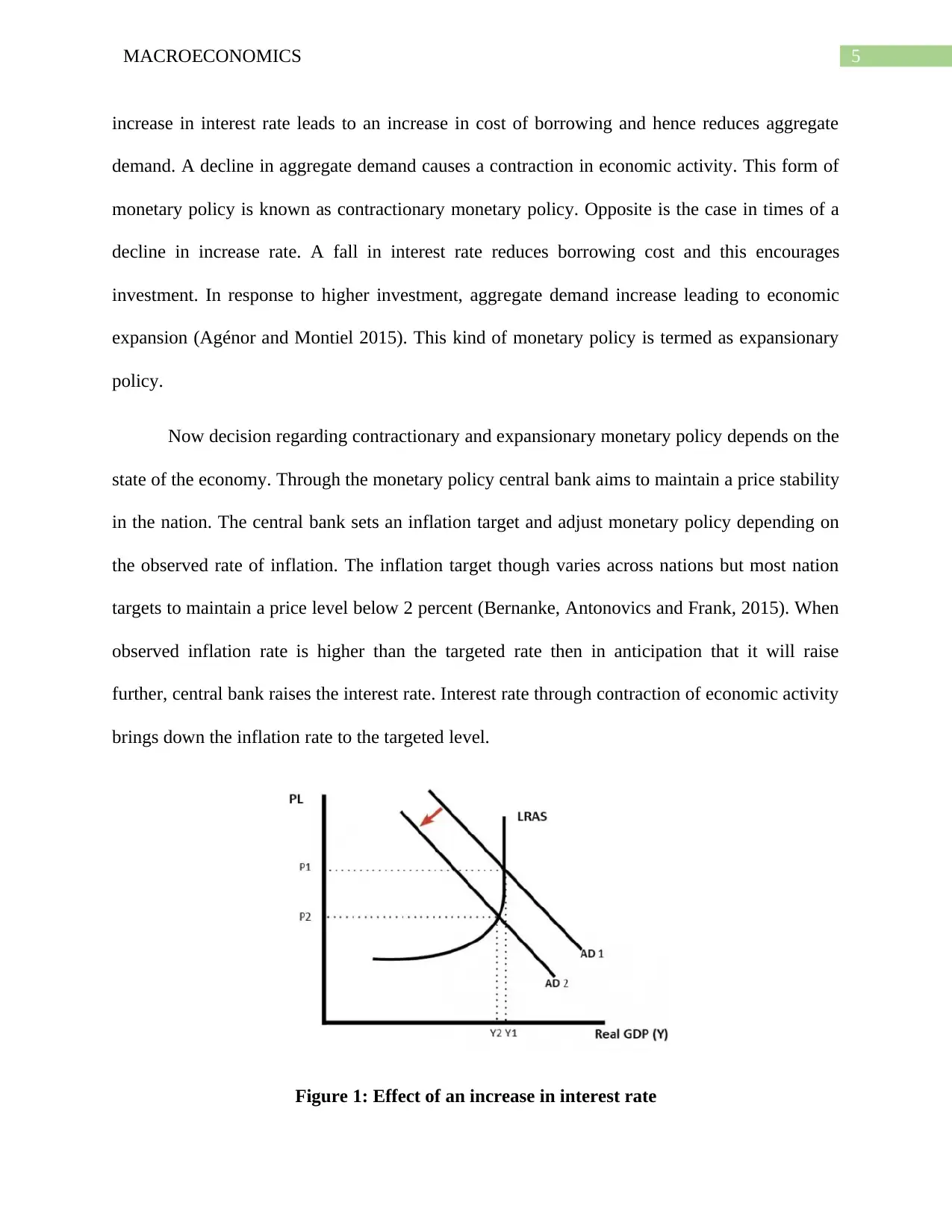

increase in interest rate leads to an increase in cost of borrowing and hence reduces aggregate

demand. A decline in aggregate demand causes a contraction in economic activity. This form of

monetary policy is known as contractionary monetary policy. Opposite is the case in times of a

decline in increase rate. A fall in interest rate reduces borrowing cost and this encourages

investment. In response to higher investment, aggregate demand increase leading to economic

expansion (Agénor and Montiel 2015). This kind of monetary policy is termed as expansionary

policy.

Now decision regarding contractionary and expansionary monetary policy depends on the

state of the economy. Through the monetary policy central bank aims to maintain a price stability

in the nation. The central bank sets an inflation target and adjust monetary policy depending on

the observed rate of inflation. The inflation target though varies across nations but most nation

targets to maintain a price level below 2 percent (Bernanke, Antonovics and Frank, 2015). When

observed inflation rate is higher than the targeted rate then in anticipation that it will raise

further, central bank raises the interest rate. Interest rate through contraction of economic activity

brings down the inflation rate to the targeted level.

Figure 1: Effect of an increase in interest rate

increase in interest rate leads to an increase in cost of borrowing and hence reduces aggregate

demand. A decline in aggregate demand causes a contraction in economic activity. This form of

monetary policy is known as contractionary monetary policy. Opposite is the case in times of a

decline in increase rate. A fall in interest rate reduces borrowing cost and this encourages

investment. In response to higher investment, aggregate demand increase leading to economic

expansion (Agénor and Montiel 2015). This kind of monetary policy is termed as expansionary

policy.

Now decision regarding contractionary and expansionary monetary policy depends on the

state of the economy. Through the monetary policy central bank aims to maintain a price stability

in the nation. The central bank sets an inflation target and adjust monetary policy depending on

the observed rate of inflation. The inflation target though varies across nations but most nation

targets to maintain a price level below 2 percent (Bernanke, Antonovics and Frank, 2015). When

observed inflation rate is higher than the targeted rate then in anticipation that it will raise

further, central bank raises the interest rate. Interest rate through contraction of economic activity

brings down the inflation rate to the targeted level.

Figure 1: Effect of an increase in interest rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MACROECONOMICS

(Source: Bernanke, Antonovics and Frank 2015)

Given below are some factors that influence whether central bank will raise the interest rate

Monetary Stability

One primary objective of central bank is to ensure stability in price level and confidence

of domestic currency. Price level is considered to be under control as long as it is within the

targeted inflation rate as set by the central bank. The target is to maintain a low to moderate

inflation rate in the economy (Kiley and Roberts 2017). Once the inflation exceeds the targeted

inflation rate, it is rational for the central bank to raise the interest rate. Inflation rate thus has a

key role to play in determining movement of the interest rate within the economy.

The policy of raising interest rate is also supported on the ground of boosting confidence

of domestic currency. With a lower interest currency foreign investors withdraw their fund from

the nation. The outflow of foreign capital causes a depreciation of currency reducing value of the

domestic currency in the world market. In order to revamp the value of currency central bank

then raises the interest rate. With a higher interest rate, investors abroad are interested to invest in

the nation following a higher return from the investment (Galí 2015). This raises the demand for

concerned currency along with an increase in relative price.

Economic growth and underlying unemployment rate

In the phase of economic contraction, due to lack of demand many production unit closes

down. As output fall, there is a decline in employment opportunity causing unemployment and

job losses to rise in the economy (Miles, Scott and Breedon 2012). During this time, central

banks considers a downward revision in the interest rate. The lower borrowing cost then

encourage investors to make more investment. With increase in productive investment new

(Source: Bernanke, Antonovics and Frank 2015)

Given below are some factors that influence whether central bank will raise the interest rate

Monetary Stability

One primary objective of central bank is to ensure stability in price level and confidence

of domestic currency. Price level is considered to be under control as long as it is within the

targeted inflation rate as set by the central bank. The target is to maintain a low to moderate

inflation rate in the economy (Kiley and Roberts 2017). Once the inflation exceeds the targeted

inflation rate, it is rational for the central bank to raise the interest rate. Inflation rate thus has a

key role to play in determining movement of the interest rate within the economy.

The policy of raising interest rate is also supported on the ground of boosting confidence

of domestic currency. With a lower interest currency foreign investors withdraw their fund from

the nation. The outflow of foreign capital causes a depreciation of currency reducing value of the

domestic currency in the world market. In order to revamp the value of currency central bank

then raises the interest rate. With a higher interest rate, investors abroad are interested to invest in

the nation following a higher return from the investment (Galí 2015). This raises the demand for

concerned currency along with an increase in relative price.

Economic growth and underlying unemployment rate

In the phase of economic contraction, due to lack of demand many production unit closes

down. As output fall, there is a decline in employment opportunity causing unemployment and

job losses to rise in the economy (Miles, Scott and Breedon 2012). During this time, central

banks considers a downward revision in the interest rate. The lower borrowing cost then

encourage investors to make more investment. With increase in productive investment new

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MACROECONOMICS

employment opportunities are created causing a decline in unemployment (Cúrdia and Woodford

2016). With productive expansion aggregate output in the economy increases and so is the

economic growth.

Spare capacity

The spare capacity of a nation is measured in terms of output gap. Output gap measures

the difference between actual and potential GDP. The presence of higher output gap indicates

that the economy fails to achieve full extent of growth. Additional stimulus needs to be provided

to explore the unutilized capacity. This can be done through a decline in interest rate. On the

other hand, if the economy operates beyond the level of potential output then that cannot be

sustained for a long period of time (Bernanke, Antonovics and Frank 2015). In order to make a

contraction in volatile economic activity the central bank raises interest rate.

employment opportunities are created causing a decline in unemployment (Cúrdia and Woodford

2016). With productive expansion aggregate output in the economy increases and so is the

economic growth.

Spare capacity

The spare capacity of a nation is measured in terms of output gap. Output gap measures

the difference between actual and potential GDP. The presence of higher output gap indicates

that the economy fails to achieve full extent of growth. Additional stimulus needs to be provided

to explore the unutilized capacity. This can be done through a decline in interest rate. On the

other hand, if the economy operates beyond the level of potential output then that cannot be

sustained for a long period of time (Bernanke, Antonovics and Frank 2015). In order to make a

contraction in volatile economic activity the central bank raises interest rate.

8MACROECONOMICS

References list

Agénor, P. R., and Montiel, P. J., 2015. Development macroeconomics. Princeton University

Press.

Bernanke, B., Antonovics, K. and Frank, R., 2015. Principles of macroeconomics. McGraw-Hill

Higher Education.

Cúrdia, V. and Woodford, M., 2016. Credit frictions and optimal monetary policy. Journal of

Monetary Economics, 84, 30-65.

Elliott, L. (2018). Brexit offers key opportunity to reboot UK economy. [online] the Guardian.

Available at: https://www.theguardian.com/business/2016/jul/24/brexit-offers-key-opportunity-

to-reboot-uk-economy [Accessed 3 Aug. 2018].

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2015. Macroeconomics in

context. Routledge.

Gudgin, G., Coutts, K., Gibson, N. and Buchanan, J., 2018. The macro-economic impact of

Brexit: using the CBR macro-economic model of the UK economy (UKMOD). Journal of Self-

Governance and Management Economics, 6(2), pp.7-49.

Johnson, P. and Mitchell, I., 2017. The Brexit vote, economics, and economic policy. Oxford

review of economic policy, 33(suppl_1), S12-S21.

Kiley, M. T. and Roberts, J. M., 2017. Monetary policy in a low interest rate world. Brookings

Papers on Economic Activity, 2017(1), 317-396.

References list

Agénor, P. R., and Montiel, P. J., 2015. Development macroeconomics. Princeton University

Press.

Bernanke, B., Antonovics, K. and Frank, R., 2015. Principles of macroeconomics. McGraw-Hill

Higher Education.

Cúrdia, V. and Woodford, M., 2016. Credit frictions and optimal monetary policy. Journal of

Monetary Economics, 84, 30-65.

Elliott, L. (2018). Brexit offers key opportunity to reboot UK economy. [online] the Guardian.

Available at: https://www.theguardian.com/business/2016/jul/24/brexit-offers-key-opportunity-

to-reboot-uk-economy [Accessed 3 Aug. 2018].

Galí, J., 2015. Monetary policy, inflation, and the business cycle: an introduction to the new

Keynesian framework and its applications. Princeton University Press.

Goodwin, N., Harris, J.M., Nelson, J.A., Roach, B. and Torras, M., 2015. Macroeconomics in

context. Routledge.

Gudgin, G., Coutts, K., Gibson, N. and Buchanan, J., 2018. The macro-economic impact of

Brexit: using the CBR macro-economic model of the UK economy (UKMOD). Journal of Self-

Governance and Management Economics, 6(2), pp.7-49.

Johnson, P. and Mitchell, I., 2017. The Brexit vote, economics, and economic policy. Oxford

review of economic policy, 33(suppl_1), S12-S21.

Kiley, M. T. and Roberts, J. M., 2017. Monetary policy in a low interest rate world. Brookings

Papers on Economic Activity, 2017(1), 317-396.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MACROECONOMICS

Miles, D., Scott, A. and Breedon, F., 2012. Macroeconomics: understanding the global economy.

John Wiley & Sons.

Sinn, H. W., 2018. The ECB's Fiscal Policy (No. w24613). National Bureau of Economic

Research.

Thompson, H., 2017. Inevitability and contingency: The political economy of Brexit. The British

journal of politics and international relations, 19(3), 434-449.

Young, G., 2017. Commentary: Monetary and Fiscal Policy Normalisation as Brexit is

Negotiated. National Institute Economic Review, 242(1), F4-F9.

Miles, D., Scott, A. and Breedon, F., 2012. Macroeconomics: understanding the global economy.

John Wiley & Sons.

Sinn, H. W., 2018. The ECB's Fiscal Policy (No. w24613). National Bureau of Economic

Research.

Thompson, H., 2017. Inevitability and contingency: The political economy of Brexit. The British

journal of politics and international relations, 19(3), 434-449.

Young, G., 2017. Commentary: Monetary and Fiscal Policy Normalisation as Brexit is

Negotiated. National Institute Economic Review, 242(1), F4-F9.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.