Impact of Hard Brexit on UK, EU, and Automotive Industry: Analysis

VerifiedAdded on 2022/10/11

|14

|3994

|14

Report

AI Summary

This report analyzes the impact of Hard Brexit on the UK, the EU, and the automotive industry, with a specific focus on Volkswagen. It begins by defining Hard Brexit and contrasting it with Soft Brexit, highlighting the automotive industry's vulnerability due to supply chain disruptions and increased costs. The report explores the theory of economic integration, detailing its stages from free trade agreements to political unions, and explains how Hard Brexit disrupts these integrations. It examines the practical consequences of Hard Brexit, including the fall of the pound, the impact on third countries, and the effects on the UK automotive industry, including increased costs and potential sales declines. The report also examines the impact on third countries, such as Bangladesh, and the potential trade disruptions. Finally, it details how Volkswagen, a multinational automotive company, could be impacted by Brexit and suggests possible strategies the company could adopt to mitigate the negative impacts of Brexit on its operations.

Running head: BREXIT 1

BREXIT

Student’s name

Institution affiliation

Date

BREXIT

Student’s name

Institution affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BREXIT 2

Abstract

The report discusses the hard Brexit and its relation to the UK, third countries and

industries affected in this case the automobile industry. The report also goes further to

explain and show how Hard Brexit affects Volkswagen an automotive company that

operates in both the EU and the UK and the strategies that Volkswagen can take post

Brexit.

Abstract

The report discusses the hard Brexit and its relation to the UK, third countries and

industries affected in this case the automobile industry. The report also goes further to

explain and show how Hard Brexit affects Volkswagen an automotive company that

operates in both the EU and the UK and the strategies that Volkswagen can take post

Brexit.

BREXIT 3

Introduction

`Hard Brexit has been defined as one of the modes to be used by the UK to

alienate itself from the European Union. There is also the second option, which is Soft

Brexit. The production of car stalls as the risks associated with Brexit accelerate. The

Society of Motor Manufacturers and Traders (SMMT) indicates that the volume of

vehicles produced as of May dropped by 45% mainly because of supply chain worries

due to Brexit (Kuger, 2019). Some of the concerns are costs associated with the

customs will increase, and logjams will be witnessed at critical areas of entry due to

Brexit, and this could jeopardize Britain's just-in-time assembly delivery strategies for

automobile manufacturers could be in jeopardy. Such strategies aim at minimizing

inventory expenses and ensure that firms hum efficiently.

The UK has benefited from the symbiotic relationship with the EU in the

automotive industry. The EU provides 81% of imports and 52.8% of the exports from the

UK (Deloitte, 2017). The lack of an alternative structure could lead to the introduction of

vehicle tariffs of 10% on all passenger automobiles,10-20% on commercial cars, and 3-

4% for automotive parts.

Economic integration

Economic integration refers to a conglomerate of states dedicated to eliminating

trade barriers to facilitate the free flow of commodities between such countries though

each state is entitled to adopting independent external trade policies (Rodrigue,

Comtois, & Slack, 2017). As such, it entails the signing of agreements between states to

allow, to some extent, the flow of labor, capital, and merchandise across their global

borders.

Theory of economic integration

This theory postulates that economic integration is a sophisticated concept

though it can be understood based on theory. Each nation is adapted to engage in

certain activities where it has a comparative advantage (Economics Online, 2019). For

instance, some states are endowed with natural resources, others with labor, and other

capital. In this context, to understand the concept of economic integration, it will be

better to limit this discussion to capital, which represents money for finances and labor

to represent workers.

Introduction

`Hard Brexit has been defined as one of the modes to be used by the UK to

alienate itself from the European Union. There is also the second option, which is Soft

Brexit. The production of car stalls as the risks associated with Brexit accelerate. The

Society of Motor Manufacturers and Traders (SMMT) indicates that the volume of

vehicles produced as of May dropped by 45% mainly because of supply chain worries

due to Brexit (Kuger, 2019). Some of the concerns are costs associated with the

customs will increase, and logjams will be witnessed at critical areas of entry due to

Brexit, and this could jeopardize Britain's just-in-time assembly delivery strategies for

automobile manufacturers could be in jeopardy. Such strategies aim at minimizing

inventory expenses and ensure that firms hum efficiently.

The UK has benefited from the symbiotic relationship with the EU in the

automotive industry. The EU provides 81% of imports and 52.8% of the exports from the

UK (Deloitte, 2017). The lack of an alternative structure could lead to the introduction of

vehicle tariffs of 10% on all passenger automobiles,10-20% on commercial cars, and 3-

4% for automotive parts.

Economic integration

Economic integration refers to a conglomerate of states dedicated to eliminating

trade barriers to facilitate the free flow of commodities between such countries though

each state is entitled to adopting independent external trade policies (Rodrigue,

Comtois, & Slack, 2017). As such, it entails the signing of agreements between states to

allow, to some extent, the flow of labor, capital, and merchandise across their global

borders.

Theory of economic integration

This theory postulates that economic integration is a sophisticated concept

though it can be understood based on theory. Each nation is adapted to engage in

certain activities where it has a comparative advantage (Economics Online, 2019). For

instance, some states are endowed with natural resources, others with labor, and other

capital. In this context, to understand the concept of economic integration, it will be

better to limit this discussion to capital, which represents money for finances and labor

to represent workers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BREXIT 4

Allowing capital and labor to move freely across global borders would enable countries

to capitalize on their comparative advantages (Economics Online, 2019). This will allow

nations that have surpluses in capital to concentrate on economic activities that

consume substantial capital investment, for instance, pharmaceuticals, aerospace, and

cotemporally technologies (Rodrigue, Comtois, & Slack, 2017). This will enable such

countries to export capital-intensive products and subsequently import labor-intensive

commodities. The fact that each country fails to concentrate on labor-intensive

enterprises will lead to an increase in the supply of labor, which will have a subsequent

decrease in wages as there will be more individuals competing for the same

occupations.

Consequently, nations that are richly endowed with labor will concentrate their

economic activities on industries that depend on substantial proportions of labor, for

instance, manufacturing, since labor is cheap (Rodrigue, Comtois, & Slack, 2017).

However, with time, there will be a decrease in labor supply, which will make wages

increase. The state will increase its capital using the profits derived from the exports,

and this will facilitate more investment.

Types of integration

There are different degrees of variations or phases of economic integration. Each

kind of integration marks a specific level of economic integration. It would be imperative

to view economic integration as a continuation where no integration can mark the

complete end as complete economic integration is attained at the other end.

Free trade agreements

Tremendous efforts stemming from economic integration arise today due to the

application of free trade agreements (Rodrigue, Comtois, & Slack, 2017). This forms the

basis of agreements between individual states entailing particular trade issues, for

instance, reduction of tariffs; in this context, tariffs refer to a tax on imported or exported

merchandise. Quotas are also part of trade agreements as they limit the volume of

imports. Countries that are not incorporated in such an arrangement are charged higher

tariffs and other trade barriers (Economics Online, 2019). However, it is imperative to

note that each member state of the agreement maintains its tariffs regarding third

Allowing capital and labor to move freely across global borders would enable countries

to capitalize on their comparative advantages (Economics Online, 2019). This will allow

nations that have surpluses in capital to concentrate on economic activities that

consume substantial capital investment, for instance, pharmaceuticals, aerospace, and

cotemporally technologies (Rodrigue, Comtois, & Slack, 2017). This will enable such

countries to export capital-intensive products and subsequently import labor-intensive

commodities. The fact that each country fails to concentrate on labor-intensive

enterprises will lead to an increase in the supply of labor, which will have a subsequent

decrease in wages as there will be more individuals competing for the same

occupations.

Consequently, nations that are richly endowed with labor will concentrate their

economic activities on industries that depend on substantial proportions of labor, for

instance, manufacturing, since labor is cheap (Rodrigue, Comtois, & Slack, 2017).

However, with time, there will be a decrease in labor supply, which will make wages

increase. The state will increase its capital using the profits derived from the exports,

and this will facilitate more investment.

Types of integration

There are different degrees of variations or phases of economic integration. Each

kind of integration marks a specific level of economic integration. It would be imperative

to view economic integration as a continuation where no integration can mark the

complete end as complete economic integration is attained at the other end.

Free trade agreements

Tremendous efforts stemming from economic integration arise today due to the

application of free trade agreements (Rodrigue, Comtois, & Slack, 2017). This forms the

basis of agreements between individual states entailing particular trade issues, for

instance, reduction of tariffs; in this context, tariffs refer to a tax on imported or exported

merchandise. Quotas are also part of trade agreements as they limit the volume of

imports. Countries that are not incorporated in such an arrangement are charged higher

tariffs and other trade barriers (Economics Online, 2019). However, it is imperative to

note that each member state of the agreement maintains its tariffs regarding third

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BREXIT 5

parties. The primary objective of free trade agreements is to facilitate the realization of

economies of scale and comparative advantages that promote economic efficiency.

Customs union

Customs union refers to a bundle of external tariffs among member states,

translating to the same duties being imposed on third countries enabling achievement of

the regime of ordinary trade (Economics Online, 2019). Customs union are essential in

leveling the competitive playing field and also in addressing the challenge of re-exports

that is utilizing preferential tariffs in one state to gain access market of another country.

The operation of a customs union is such that countries exporting to the customs union

make one payment known as duty once the merchandise crosses through the border. It

is when the commodities are inside the union that they can transit freely with no

additional tariffs (Rodrigue, Comtois, & Slack, 2017). The revenue collected from the

imposed tariff is then shared among members where the country that gathers duty

holding back a small share.

Common market

In a common market, there is free movement of services and capital among

member states enabling expansion of the scale of economies and comparative

advantages (Economics Online, 2019). However, this level of integration is

characterized by each country's market running its set of regulations, for instance,

product standards. Nevertheless, apart from eliminating tariffs, on-tariffs are either

reduced or removed in this market. The success of a common market depends on great

harmonization of policies governing micro-economic policies, and common regulations

entailing commodity standards, monopoly authority, and anti-competitive activities

(Rodrigue, Comtois, & Slack, 2017). This may involve standard policies that impact

significant industries, for instance, the Common Agricultural Policy.

Economic union

At this level, there is the removal of all tariffs for trading member countries, which

leads to a single market (Economics Online, 2019). Labour in his market is also allowed

to move freely, and this will enable employees in a member state to transit freely and

works in a member state. There is also harmonization of monetary and fiscal policies

among member states, and this translates to a phase of political integration. The next

parties. The primary objective of free trade agreements is to facilitate the realization of

economies of scale and comparative advantages that promote economic efficiency.

Customs union

Customs union refers to a bundle of external tariffs among member states,

translating to the same duties being imposed on third countries enabling achievement of

the regime of ordinary trade (Economics Online, 2019). Customs union are essential in

leveling the competitive playing field and also in addressing the challenge of re-exports

that is utilizing preferential tariffs in one state to gain access market of another country.

The operation of a customs union is such that countries exporting to the customs union

make one payment known as duty once the merchandise crosses through the border. It

is when the commodities are inside the union that they can transit freely with no

additional tariffs (Rodrigue, Comtois, & Slack, 2017). The revenue collected from the

imposed tariff is then shared among members where the country that gathers duty

holding back a small share.

Common market

In a common market, there is free movement of services and capital among

member states enabling expansion of the scale of economies and comparative

advantages (Economics Online, 2019). However, this level of integration is

characterized by each country's market running its set of regulations, for instance,

product standards. Nevertheless, apart from eliminating tariffs, on-tariffs are either

reduced or removed in this market. The success of a common market depends on great

harmonization of policies governing micro-economic policies, and common regulations

entailing commodity standards, monopoly authority, and anti-competitive activities

(Rodrigue, Comtois, & Slack, 2017). This may involve standard policies that impact

significant industries, for instance, the Common Agricultural Policy.

Economic union

At this level, there is the removal of all tariffs for trading member countries, which

leads to a single market (Economics Online, 2019). Labour in his market is also allowed

to move freely, and this will enable employees in a member state to transit freely and

works in a member state. There is also harmonization of monetary and fiscal policies

among member states, and this translates to a phase of political integration. The next

BREXIT 6

step entails a monetary union where a common currency is adopted, such as the

European Union (Economics Online, 2019). The European Union is the remaining

perfect example of a real of the Economic Union and came into existence in 1993 after

signing the Maastricht Treaty formally known as the Treaty on European Union.

Political Union

A political union features the capability of the most advanced level of integration

with one government; in this union, the sovereignty of each state is significantly reduced

(Economics Online, 2019). Such union is common in member states, for instance, the

federations where the national government and regions exercise some degree of

autonomy. An increase in the level of economic integration leads to sophistication per

level (Economics Online, 2019). This entails a series of numerous regulations,

enforcement, and arbitration strategies. Different levels of complexity attract a cost that

may lower the attractiveness of regions under economic integration as it is rigid to

national policies. Devolving economic integration could occur if complications are

arising from it are deemed irrelevant by the members.

Practical consequence resulting from hard Brexit

The fall of the pound against the Euro has provided boon and threat to the

automobile industry (Deloitte, 2017). However, this will render the UK exports getting

more competitive in the long-run. Conversely, it will increase the cost of imported parts

from the EU as they account for about 60% of components in Britain's manufactured

automobiles (Riley, 2019). It is imperative to note that depreciation of the pound has put

a stall on registrations of a commercial vehicle as a result of counteractive forces, for

instance, the decline prices of oil and competitiveness of exports.

Effect of Brexit on third countries

Third world countries such as Bangladesh, Pakistan, Egypt, among others, are

eligible for six kinds of preferential arrangements whereby three are categorized as

unilateral schemes functioning under the EU's GSP, and the other three fall under the

EU FTAs (Dasgupta, 2019). The projects operating under the auspices of GSP entail a

standard GSP scheme which serves the lower-middle-income countries(LMICs) an

improved GSP+ scheme designed to help the LMICs that anticipate particular

susceptible criteria with the inclusion of an Everything But Arms(EBA) program for UN-

step entails a monetary union where a common currency is adopted, such as the

European Union (Economics Online, 2019). The European Union is the remaining

perfect example of a real of the Economic Union and came into existence in 1993 after

signing the Maastricht Treaty formally known as the Treaty on European Union.

Political Union

A political union features the capability of the most advanced level of integration

with one government; in this union, the sovereignty of each state is significantly reduced

(Economics Online, 2019). Such union is common in member states, for instance, the

federations where the national government and regions exercise some degree of

autonomy. An increase in the level of economic integration leads to sophistication per

level (Economics Online, 2019). This entails a series of numerous regulations,

enforcement, and arbitration strategies. Different levels of complexity attract a cost that

may lower the attractiveness of regions under economic integration as it is rigid to

national policies. Devolving economic integration could occur if complications are

arising from it are deemed irrelevant by the members.

Practical consequence resulting from hard Brexit

The fall of the pound against the Euro has provided boon and threat to the

automobile industry (Deloitte, 2017). However, this will render the UK exports getting

more competitive in the long-run. Conversely, it will increase the cost of imported parts

from the EU as they account for about 60% of components in Britain's manufactured

automobiles (Riley, 2019). It is imperative to note that depreciation of the pound has put

a stall on registrations of a commercial vehicle as a result of counteractive forces, for

instance, the decline prices of oil and competitiveness of exports.

Effect of Brexit on third countries

Third world countries such as Bangladesh, Pakistan, Egypt, among others, are

eligible for six kinds of preferential arrangements whereby three are categorized as

unilateral schemes functioning under the EU's GSP, and the other three fall under the

EU FTAs (Dasgupta, 2019). The projects operating under the auspices of GSP entail a

standard GSP scheme which serves the lower-middle-income countries(LMICs) an

improved GSP+ scheme designed to help the LMICs that anticipate particular

susceptible criteria with the inclusion of an Everything But Arms(EBA) program for UN-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BREXIT 7

designated least developed nations and this entails all low-income states and some

MNCs (House of Commons, 2018). The kind of FTAs that the EU has consented with

developing nations entail Association Agreements (AA) and Economic Partnership

Agreements (EPA), among others.

A hard Brexit would impact the third world countries adversely.

As demonstrated below, extra duties would be imposed on countries such as

Bangladesh and Pakistan, affecting their exports to the UK. The trade destruction

stemming from the hard Brexit would be eight times bigger compared to soft Brexit.

Following the UK's replication of the GSP before exiting the EU, a country such as

Bangladesh that currently benefits from FTAs would be compelled to pay an additional

$181 million as other duties following transitioning to the Standard GSP program

(Deloitte, 2017). Using Bangladesh as an example of helping from FTAs would change

to the EBA scheme and still receive duty-free access (Prospect Team, 2019). This will

lead to a decline in the UK demand for their exports of about $203 million, which is

approximately 0.7% (Kuger, 2019). However, failure of the UK government to sustain

any preferential access to a country such as Bangladesh would translate to a decline in

the UK demand for its trades by more than $ 1.6 billion, which is accounts for roughly

5% (SMMT, 2019). The worst-impacted states are also some of the poorest. Least

developed nations transacting under the EBA scheme would encounter the highest

trade-weighted tariffs regarding the UK MFN of about 10% resulting in a $ 635 million

decline in the demand for their commodities.

Under hard Brexit, countries such as Cambodia, Bangladesh, and Pakistan

emerged as the most significant losers (UN, 2016). Since the UK is still ranked as the

primary trading partner for these third world countries, representing for about a tenth of

their international exports, thus removal of the UK preferences would lead to substantial

declines in their trade. However, such trade destruction impacts would be focused on a

handful of dominant Britain exporting segments that would encounter significant

increases under the terms of MFN (UN, 2016). For instance, in Cambodia, more than

20% of the decline in UK exports would happen in the bicycle manufacturing segment.

In Bangladesh, the exports from the cotton jackets and t-shirts would represent one-

designated least developed nations and this entails all low-income states and some

MNCs (House of Commons, 2018). The kind of FTAs that the EU has consented with

developing nations entail Association Agreements (AA) and Economic Partnership

Agreements (EPA), among others.

A hard Brexit would impact the third world countries adversely.

As demonstrated below, extra duties would be imposed on countries such as

Bangladesh and Pakistan, affecting their exports to the UK. The trade destruction

stemming from the hard Brexit would be eight times bigger compared to soft Brexit.

Following the UK's replication of the GSP before exiting the EU, a country such as

Bangladesh that currently benefits from FTAs would be compelled to pay an additional

$181 million as other duties following transitioning to the Standard GSP program

(Deloitte, 2017). Using Bangladesh as an example of helping from FTAs would change

to the EBA scheme and still receive duty-free access (Prospect Team, 2019). This will

lead to a decline in the UK demand for their exports of about $203 million, which is

approximately 0.7% (Kuger, 2019). However, failure of the UK government to sustain

any preferential access to a country such as Bangladesh would translate to a decline in

the UK demand for its trades by more than $ 1.6 billion, which is accounts for roughly

5% (SMMT, 2019). The worst-impacted states are also some of the poorest. Least

developed nations transacting under the EBA scheme would encounter the highest

trade-weighted tariffs regarding the UK MFN of about 10% resulting in a $ 635 million

decline in the demand for their commodities.

Under hard Brexit, countries such as Cambodia, Bangladesh, and Pakistan

emerged as the most significant losers (UN, 2016). Since the UK is still ranked as the

primary trading partner for these third world countries, representing for about a tenth of

their international exports, thus removal of the UK preferences would lead to substantial

declines in their trade. However, such trade destruction impacts would be focused on a

handful of dominant Britain exporting segments that would encounter significant

increases under the terms of MFN (UN, 2016). For instance, in Cambodia, more than

20% of the decline in UK exports would happen in the bicycle manufacturing segment.

In Bangladesh, the exports from the cotton jackets and t-shirts would represent one-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BREXIT 8

third of trade destruction. Thus, the nations' percentage decline in the global exports

may be adverse at the sectorial level compared to the country-level.

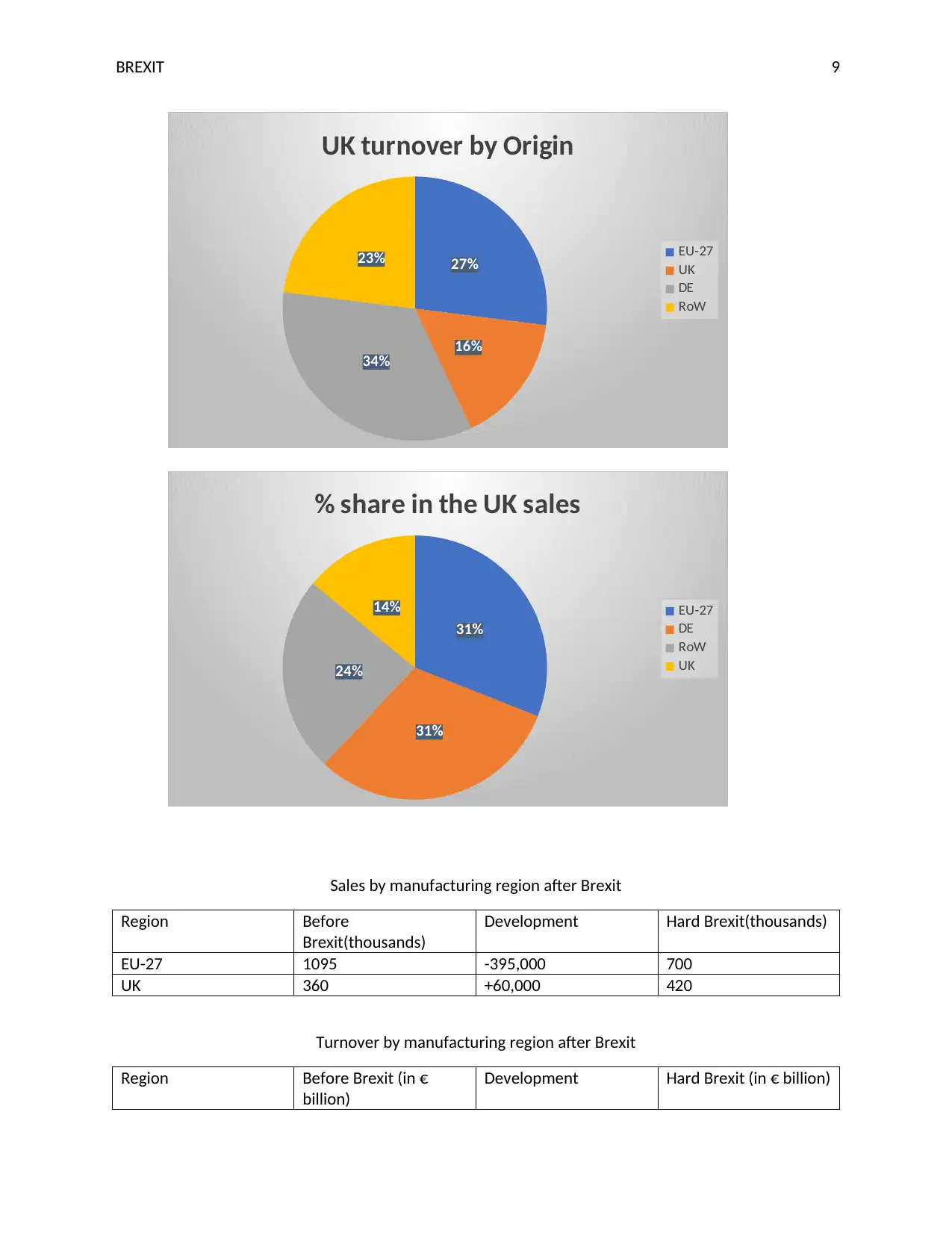

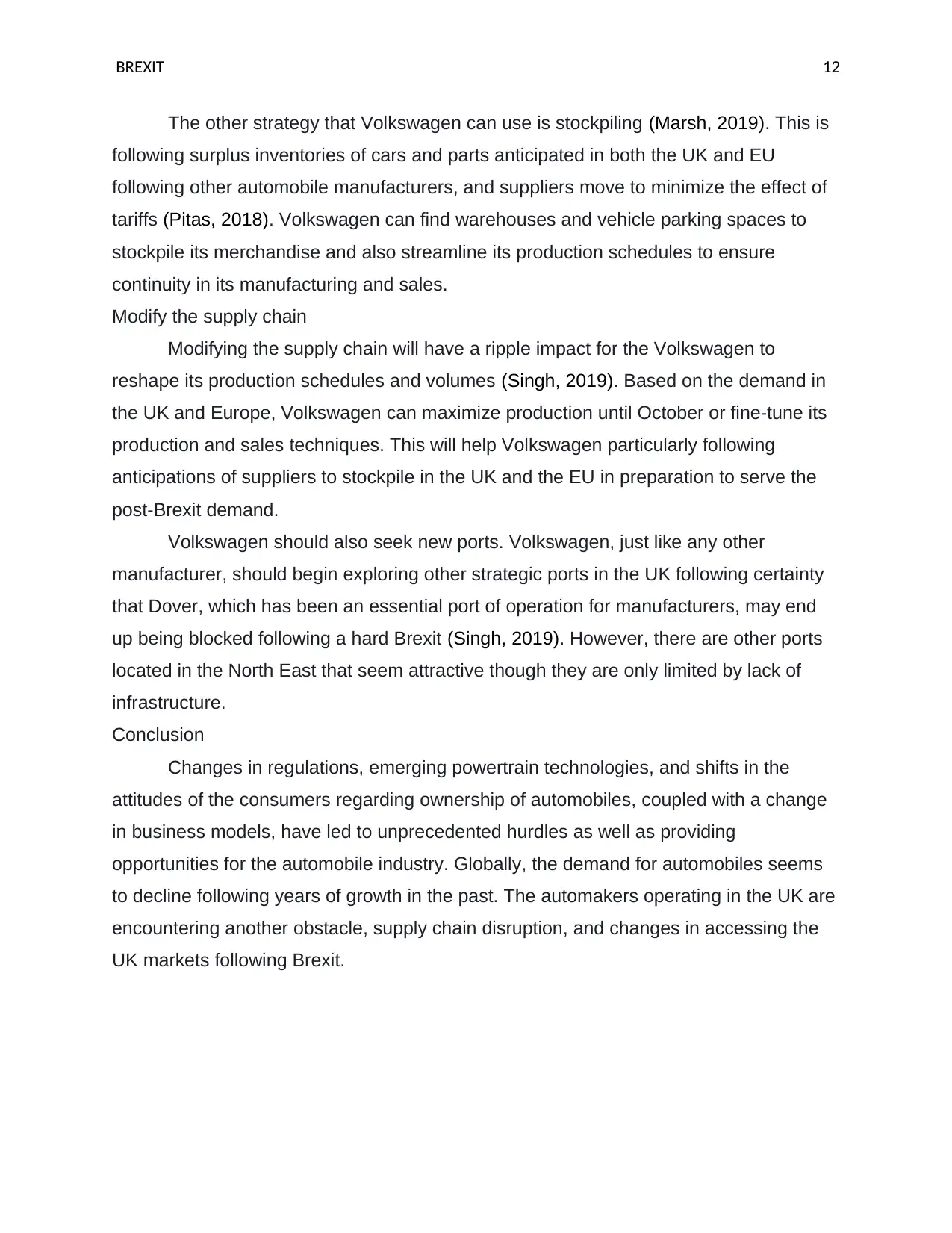

Impact of Brexit on UK automobile industry

A hard Brexit coupled with WTO duties and 10% devaluation of the pound

translates to an aggregated cost increase of € 1.9 billion, accounting for a 15% increase

for manufacturers of automobiles in the UK compared to a non-Brexit situation (Deloitte,

2017). Manufacturers transferring this cost to their customers on a 1:1 ratio would lead

to a rise in the price of an automobile in the UK by €3700 and by as much as €5600 for

manufacturers in Germany (CEBOS, 2019). Considering the consumer behavior of the

Britons, the year of exiting the EU, the increase in price would lead to a general sales

decrease of roughly 550,000 cars representing a 19% decrease in the UK (Holweg,

2019). Gross turnover from vehicles in the UK would decrease by approximately €12.4

billion, which is an 18% decrease and profits by €900 million (Kuger, 2019). Though

manufacturers from the UK and outside the EU would profit, it is estimated that EU-27

turnover would decline by more than €8.3 billion and the German manufacturers by

approximately €6.7 billion (Pfeifer, 2019). Following this decline in sales and turnovers,

it is estimated that more than 18000 jobs in the German automotive sector would be

threatened (Deloitte, 2017).

Companies such as Ford made it clear that they will be closing down their

Bridgend factory as of 2020, and this will account for the loss of more than 1700

occupations (Dasgupta, 2019) while its Japanese rival Honda also held its ground

regarding shutting down its car plant in Swindon (Reid, 2019). Though both enterprises

asserted that their decisions were for commercial motives, it is clear that they are

changing their mode of operation in anticipation of Brexit (Holweg, 2019). According to

SMMT, the UK will lose its position as the 10th largest exporter of commodities without

the automobile industry.

.

third of trade destruction. Thus, the nations' percentage decline in the global exports

may be adverse at the sectorial level compared to the country-level.

Impact of Brexit on UK automobile industry

A hard Brexit coupled with WTO duties and 10% devaluation of the pound

translates to an aggregated cost increase of € 1.9 billion, accounting for a 15% increase

for manufacturers of automobiles in the UK compared to a non-Brexit situation (Deloitte,

2017). Manufacturers transferring this cost to their customers on a 1:1 ratio would lead

to a rise in the price of an automobile in the UK by €3700 and by as much as €5600 for

manufacturers in Germany (CEBOS, 2019). Considering the consumer behavior of the

Britons, the year of exiting the EU, the increase in price would lead to a general sales

decrease of roughly 550,000 cars representing a 19% decrease in the UK (Holweg,

2019). Gross turnover from vehicles in the UK would decrease by approximately €12.4

billion, which is an 18% decrease and profits by €900 million (Kuger, 2019). Though

manufacturers from the UK and outside the EU would profit, it is estimated that EU-27

turnover would decline by more than €8.3 billion and the German manufacturers by

approximately €6.7 billion (Pfeifer, 2019). Following this decline in sales and turnovers,

it is estimated that more than 18000 jobs in the German automotive sector would be

threatened (Deloitte, 2017).

Companies such as Ford made it clear that they will be closing down their

Bridgend factory as of 2020, and this will account for the loss of more than 1700

occupations (Dasgupta, 2019) while its Japanese rival Honda also held its ground

regarding shutting down its car plant in Swindon (Reid, 2019). Though both enterprises

asserted that their decisions were for commercial motives, it is clear that they are

changing their mode of operation in anticipation of Brexit (Holweg, 2019). According to

SMMT, the UK will lose its position as the 10th largest exporter of commodities without

the automobile industry.

.

BREXIT 9

27%

16%

34%

23%

UK turnover by Origin

EU-27

UK

DE

RoW

31%

31%

24%

14%

% share in the UK sales

EU-27

DE

RoW

UK

Sales by manufacturing region after Brexit

Region Before

Brexit(thousands)

Development Hard Brexit(thousands)

EU-27 1095 -395,000 700

UK 360 +60,000 420

Turnover by manufacturing region after Brexit

Region Before Brexit (in €

billion)

Development Hard Brexit (in € billion)

27%

16%

34%

23%

UK turnover by Origin

EU-27

UK

DE

RoW

31%

31%

24%

14%

% share in the UK sales

EU-27

DE

RoW

UK

Sales by manufacturing region after Brexit

Region Before

Brexit(thousands)

Development Hard Brexit(thousands)

EU-27 1095 -395,000 700

UK 360 +60,000 420

Turnover by manufacturing region after Brexit

Region Before Brexit (in €

billion)

Development Hard Brexit (in € billion)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BREXIT 10

EU-27 23.1 -€8.3 billion turnover 14.8

UK 9.9 +€ 1.7 billion turnover 11.6

Profit by manufacturing after Brexit

Region Before Brexit (in €

million)

Development Hard Brexit (in €

million)

EU-27 1500 -€500 million profit 1000

UK 700 + € 100 million profit 800

Volkswagen

The passenger car, which is Volkswagen Group’s top brand, saw a decline in

sales by more than 850,000 units as of 2018, reaching 3.7 million units in 2018

(Statista, 2019). Despite such slumps in sales, in other countries such as China, the

passenger car accounted for roughly half of the vehicles sold by Volkswagen beyond

China and nearly one-third of all cars sold by Volkswagen Group as of 2018 (Statista,

2019). Such declines in sales have partly been attributed to uncertainty regarding the

Brexit process. The automobile industry’s predicament has been exacerbated by the

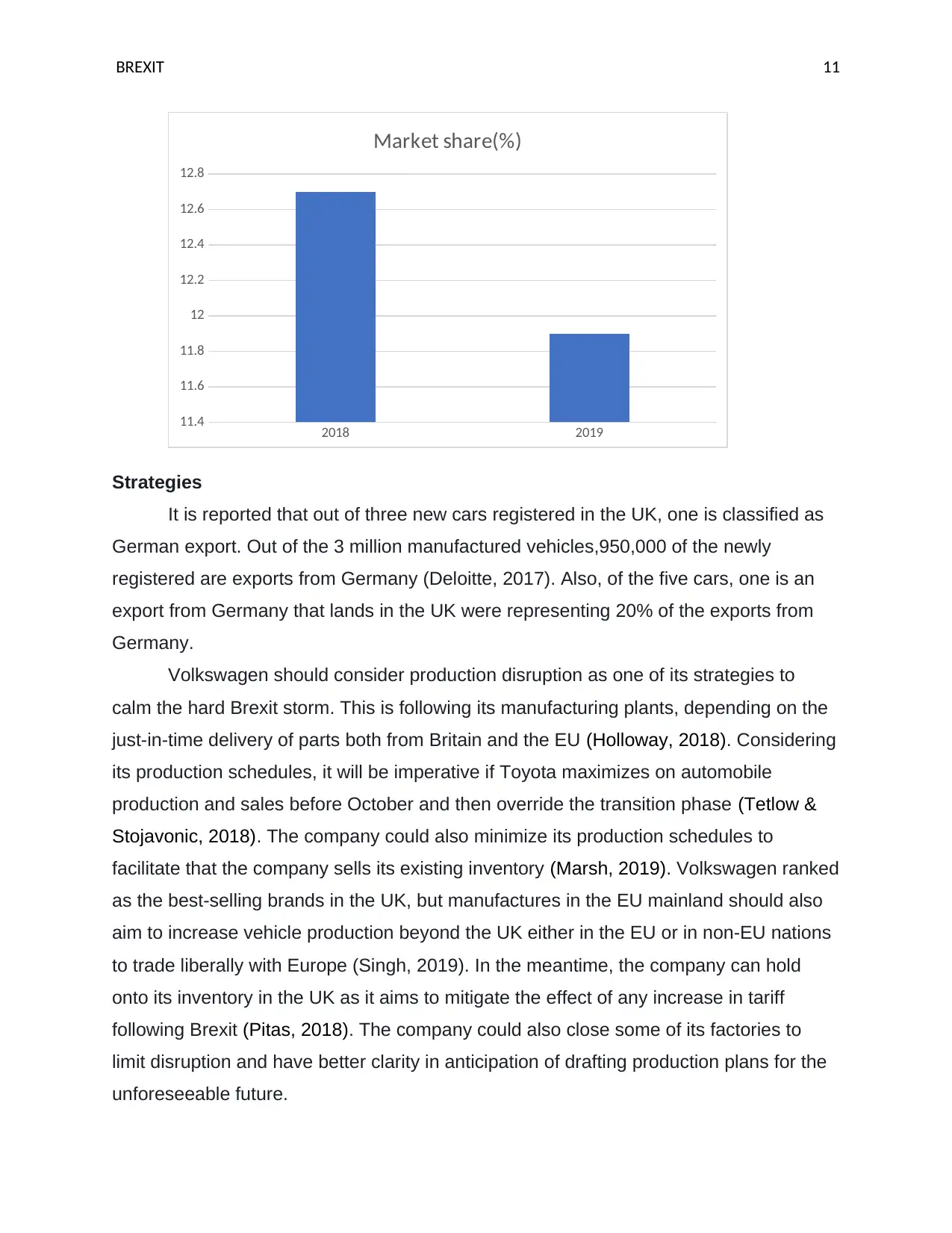

looming change regarding developments of Brexit (Dasgupta, 2019). In the third quarter

of 2019, the Volkswagen brand’s share of new-car registrations in the EU was 11.9% a

point down compared to the third quarter of 2018 (Statista, 2019). However, Skoda was

the only brand from Volkswagen that recorded a gain.

EU-27 23.1 -€8.3 billion turnover 14.8

UK 9.9 +€ 1.7 billion turnover 11.6

Profit by manufacturing after Brexit

Region Before Brexit (in €

million)

Development Hard Brexit (in €

million)

EU-27 1500 -€500 million profit 1000

UK 700 + € 100 million profit 800

Volkswagen

The passenger car, which is Volkswagen Group’s top brand, saw a decline in

sales by more than 850,000 units as of 2018, reaching 3.7 million units in 2018

(Statista, 2019). Despite such slumps in sales, in other countries such as China, the

passenger car accounted for roughly half of the vehicles sold by Volkswagen beyond

China and nearly one-third of all cars sold by Volkswagen Group as of 2018 (Statista,

2019). Such declines in sales have partly been attributed to uncertainty regarding the

Brexit process. The automobile industry’s predicament has been exacerbated by the

looming change regarding developments of Brexit (Dasgupta, 2019). In the third quarter

of 2019, the Volkswagen brand’s share of new-car registrations in the EU was 11.9% a

point down compared to the third quarter of 2018 (Statista, 2019). However, Skoda was

the only brand from Volkswagen that recorded a gain.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BREXIT 11

2018 2019

11.4

11.6

11.8

12

12.2

12.4

12.6

12.8

Market share(%)

Strategies

It is reported that out of three new cars registered in the UK, one is classified as

German export. Out of the 3 million manufactured vehicles,950,000 of the newly

registered are exports from Germany (Deloitte, 2017). Also, of the five cars, one is an

export from Germany that lands in the UK were representing 20% of the exports from

Germany.

Volkswagen should consider production disruption as one of its strategies to

calm the hard Brexit storm. This is following its manufacturing plants, depending on the

just-in-time delivery of parts both from Britain and the EU (Holloway, 2018). Considering

its production schedules, it will be imperative if Toyota maximizes on automobile

production and sales before October and then override the transition phase (Tetlow &

Stojavonic, 2018). The company could also minimize its production schedules to

facilitate that the company sells its existing inventory (Marsh, 2019). Volkswagen ranked

as the best-selling brands in the UK, but manufactures in the EU mainland should also

aim to increase vehicle production beyond the UK either in the EU or in non-EU nations

to trade liberally with Europe (Singh, 2019). In the meantime, the company can hold

onto its inventory in the UK as it aims to mitigate the effect of any increase in tariff

following Brexit (Pitas, 2018). The company could also close some of its factories to

limit disruption and have better clarity in anticipation of drafting production plans for the

unforeseeable future.

2018 2019

11.4

11.6

11.8

12

12.2

12.4

12.6

12.8

Market share(%)

Strategies

It is reported that out of three new cars registered in the UK, one is classified as

German export. Out of the 3 million manufactured vehicles,950,000 of the newly

registered are exports from Germany (Deloitte, 2017). Also, of the five cars, one is an

export from Germany that lands in the UK were representing 20% of the exports from

Germany.

Volkswagen should consider production disruption as one of its strategies to

calm the hard Brexit storm. This is following its manufacturing plants, depending on the

just-in-time delivery of parts both from Britain and the EU (Holloway, 2018). Considering

its production schedules, it will be imperative if Toyota maximizes on automobile

production and sales before October and then override the transition phase (Tetlow &

Stojavonic, 2018). The company could also minimize its production schedules to

facilitate that the company sells its existing inventory (Marsh, 2019). Volkswagen ranked

as the best-selling brands in the UK, but manufactures in the EU mainland should also

aim to increase vehicle production beyond the UK either in the EU or in non-EU nations

to trade liberally with Europe (Singh, 2019). In the meantime, the company can hold

onto its inventory in the UK as it aims to mitigate the effect of any increase in tariff

following Brexit (Pitas, 2018). The company could also close some of its factories to

limit disruption and have better clarity in anticipation of drafting production plans for the

unforeseeable future.

BREXIT 12

The other strategy that Volkswagen can use is stockpiling (Marsh, 2019). This is

following surplus inventories of cars and parts anticipated in both the UK and EU

following other automobile manufacturers, and suppliers move to minimize the effect of

tariffs (Pitas, 2018). Volkswagen can find warehouses and vehicle parking spaces to

stockpile its merchandise and also streamline its production schedules to ensure

continuity in its manufacturing and sales.

Modify the supply chain

Modifying the supply chain will have a ripple impact for the Volkswagen to

reshape its production schedules and volumes (Singh, 2019). Based on the demand in

the UK and Europe, Volkswagen can maximize production until October or fine-tune its

production and sales techniques. This will help Volkswagen particularly following

anticipations of suppliers to stockpile in the UK and the EU in preparation to serve the

post-Brexit demand.

Volkswagen should also seek new ports. Volkswagen, just like any other

manufacturer, should begin exploring other strategic ports in the UK following certainty

that Dover, which has been an essential port of operation for manufacturers, may end

up being blocked following a hard Brexit (Singh, 2019). However, there are other ports

located in the North East that seem attractive though they are only limited by lack of

infrastructure.

Conclusion

Changes in regulations, emerging powertrain technologies, and shifts in the

attitudes of the consumers regarding ownership of automobiles, coupled with a change

in business models, have led to unprecedented hurdles as well as providing

opportunities for the automobile industry. Globally, the demand for automobiles seems

to decline following years of growth in the past. The automakers operating in the UK are

encountering another obstacle, supply chain disruption, and changes in accessing the

UK markets following Brexit.

The other strategy that Volkswagen can use is stockpiling (Marsh, 2019). This is

following surplus inventories of cars and parts anticipated in both the UK and EU

following other automobile manufacturers, and suppliers move to minimize the effect of

tariffs (Pitas, 2018). Volkswagen can find warehouses and vehicle parking spaces to

stockpile its merchandise and also streamline its production schedules to ensure

continuity in its manufacturing and sales.

Modify the supply chain

Modifying the supply chain will have a ripple impact for the Volkswagen to

reshape its production schedules and volumes (Singh, 2019). Based on the demand in

the UK and Europe, Volkswagen can maximize production until October or fine-tune its

production and sales techniques. This will help Volkswagen particularly following

anticipations of suppliers to stockpile in the UK and the EU in preparation to serve the

post-Brexit demand.

Volkswagen should also seek new ports. Volkswagen, just like any other

manufacturer, should begin exploring other strategic ports in the UK following certainty

that Dover, which has been an essential port of operation for manufacturers, may end

up being blocked following a hard Brexit (Singh, 2019). However, there are other ports

located in the North East that seem attractive though they are only limited by lack of

infrastructure.

Conclusion

Changes in regulations, emerging powertrain technologies, and shifts in the

attitudes of the consumers regarding ownership of automobiles, coupled with a change

in business models, have led to unprecedented hurdles as well as providing

opportunities for the automobile industry. Globally, the demand for automobiles seems

to decline following years of growth in the past. The automakers operating in the UK are

encountering another obstacle, supply chain disruption, and changes in accessing the

UK markets following Brexit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.