FIN1 Investment Feasibility Report: Brisbane Manufacturing Company Ltd

VerifiedAdded on 2023/06/11

|4

|818

|159

Report

AI Summary

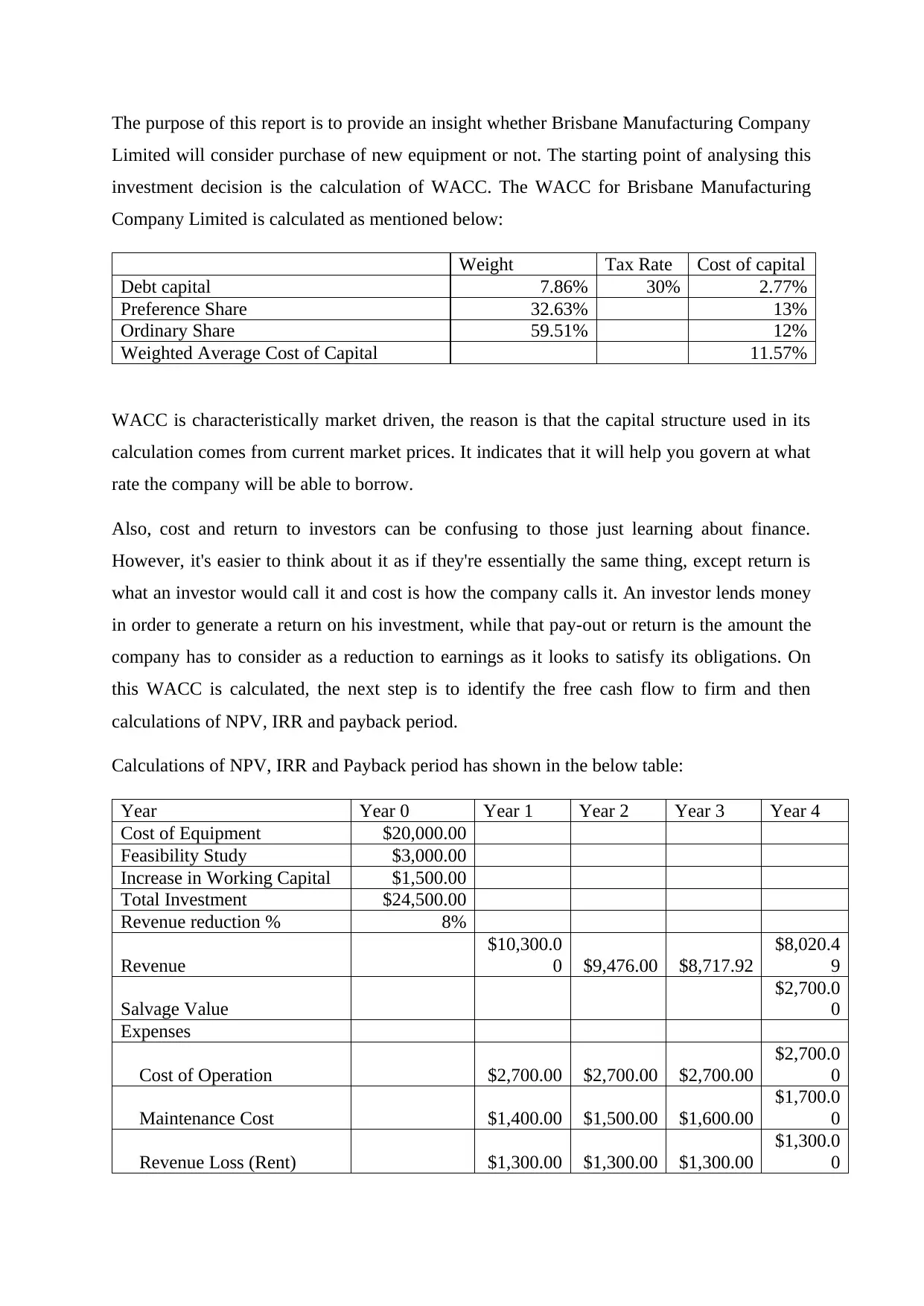

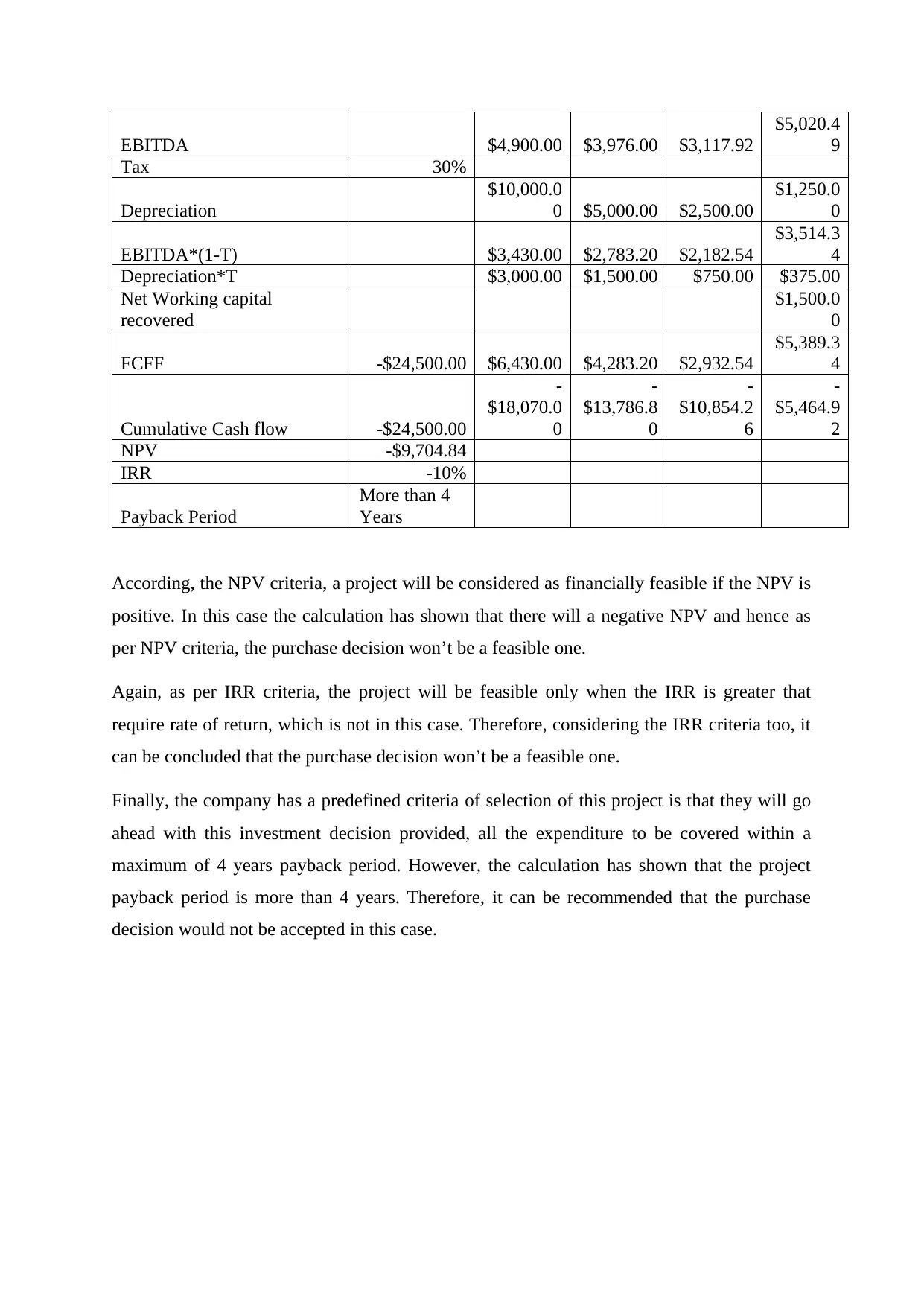

This report provides a detailed analysis of whether Brisbane Manufacturing Company Limited should purchase new equipment. The analysis begins with the calculation of the Weighted Average Cost of Capital (WACC), which is determined to be market-driven and crucial for understanding borrowing rates. Following the WACC calculation, the report identifies free cash flow to the firm and calculates the Net Present Value (NPV), Internal Rate of Return (IRR), and payback period. The calculations reveal a negative NPV and an IRR lower than the required rate of return, alongside a payback period exceeding the company's four-year criterion. Based on these findings, the report recommends against the purchase decision, as it does not meet the company's financial feasibility requirements according to NPV, IRR, and payback period criteria.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.