Comprehensive Financial Analysis Report of British Airways

VerifiedAdded on 2022/12/30

|12

|4356

|58

Report

AI Summary

This report presents a detailed financial analysis of British Airways, examining key aspects of its financial operations. It begins with an overview of the accounting information system used by the company, including different types of systems like legacy and manual systems, and the process of financial statement preparation. The report then delves into the revenue recognition process, discussing various methods such as sales basis, cost recoverability, and percentage of completion. Further analysis focuses on the liability side of the balance sheet, classifying liabilities into current, non-current, and contingent categories, along with bond valuation and share valuation. The report also includes a ratio analysis, evaluating the company's liquidity, efficiency, and solvency through ratios like current ratio, acid test ratio, debt to total assets ratio and times interest earned ratio, providing insights into its financial performance and stability. The report concludes with an overall assessment of British Airways' financial health and provides a holistic view of its financial management practices.

Company’s Business

Financial Analysis

Report

Financial Analysis

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Accounting information system ..................................................................................................1

Revenue recognition process and structure of the revenue..........................................................3

Analysis of the liability side of balance sheet and ratio analysis ................................................4

Critically analyse the compensation system and stock compensation plans ..............................7

Leasing environment and types of lease .....................................................................................8

Conclusion ......................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Accounting information system ..................................................................................................1

Revenue recognition process and structure of the revenue..........................................................3

Analysis of the liability side of balance sheet and ratio analysis ................................................4

Critically analyse the compensation system and stock compensation plans ..............................7

Leasing environment and types of lease .....................................................................................8

Conclusion ......................................................................................................................................9

REFERENCES .............................................................................................................................10

INTRODUCTION

Financial analysis report means the analyses of the financial strength and weakness of the

organizations for communicates the financial health of the company to the shareholders and

investors in order to increase the profit of the company in the future (Akbar and et.al., 2017). It is

also help in expansion of the business in future which help the business to grow. It is helpful for

the investors because through this they decide they take the investment decisions. Through this

individuals make the reports based on the research and investors conduct financial analyst by

gathering the financial information, through calculate ratios and then determine the value. This

report is based on the British Airways which is headquartered in London, United Kingdom.

Company was founded in the year 1974 and its parent company is 'International Airlines Group'.

It is second largest airline on the basis of Fleet size as well as passenger carried. In this report

there is the analysis of the accounting information system and method of the revenue recognition

for the structure of the revenue. Their is the analysis of the ratio also see the result which is best

for the financial analyses.

MAIN BODY

Accounting information system

In the Accounting information system refers to the process or methods that is used to

collect, store, process, manage and evaluation of the financial data which is used by the

managers and business analyst and tax agencies (Białkowski and Perera, 2019). Its is the

documents used by the accountants, consultants, business analyst, managers and auditors for the

analysis of the financial report. In this various software and hardware is used to store and retrieve

the data. In this there are six component is included which is people, procedures, data, software,

instructions and information technology infrastructure. In Context to British Airways they focus

on the one of the accounting information system for the effective working in the economy

(Birch, 2017).

Types of the Accounting Information systems:

Legacy systems- It can be defined as system which is used by the business by focus on

the information technology in the sophisticated way which is old- fashioned but there are

some advantages is there for the firm which are valuable historical data for the firm and

system which is customized according to the needs of the system. In this there is the

1

Financial analysis report means the analyses of the financial strength and weakness of the

organizations for communicates the financial health of the company to the shareholders and

investors in order to increase the profit of the company in the future (Akbar and et.al., 2017). It is

also help in expansion of the business in future which help the business to grow. It is helpful for

the investors because through this they decide they take the investment decisions. Through this

individuals make the reports based on the research and investors conduct financial analyst by

gathering the financial information, through calculate ratios and then determine the value. This

report is based on the British Airways which is headquartered in London, United Kingdom.

Company was founded in the year 1974 and its parent company is 'International Airlines Group'.

It is second largest airline on the basis of Fleet size as well as passenger carried. In this report

there is the analysis of the accounting information system and method of the revenue recognition

for the structure of the revenue. Their is the analysis of the ratio also see the result which is best

for the financial analyses.

MAIN BODY

Accounting information system

In the Accounting information system refers to the process or methods that is used to

collect, store, process, manage and evaluation of the financial data which is used by the

managers and business analyst and tax agencies (Białkowski and Perera, 2019). Its is the

documents used by the accountants, consultants, business analyst, managers and auditors for the

analysis of the financial report. In this various software and hardware is used to store and retrieve

the data. In this there are six component is included which is people, procedures, data, software,

instructions and information technology infrastructure. In Context to British Airways they focus

on the one of the accounting information system for the effective working in the economy

(Birch, 2017).

Types of the Accounting Information systems:

Legacy systems- It can be defined as system which is used by the business by focus on

the information technology in the sophisticated way which is old- fashioned but there are

some advantages is there for the firm which are valuable historical data for the firm and

system which is customized according to the needs of the system. In this there is the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

disadvantage is present which is no documentation (Dichev, Graham, Harvey and

Rajgopal, 2016).

Manual systems- In this system there is the use of this system by the small businesses

and home based businesses, because it is entire manual in which there is the requirement

of the source document, general ledger, journal and subsidiary journals if there is the

need (Bilgin and et.al., 2018).

Replacement of the legacy system- In this there is the completely replace of the legacy

systems with the new up -to- date system because it is the quite expensive system which

is used in the procedure called screen scraping, through the new system it helps in

transfer the data and displayed on the computer screen which help in making the different

applications such as inventory, payroll. In the home based variety there is the use of the

accounting information system to keep the competitive in the industry (Drake, Quinn and

Thornock, 2017).

In relevance to British Airways, information technology of legacy system is utilised by an

organization for the purpose of collecting data and for managing the collected information of the

historical data that is essential for the investors for analysing options of investment associated

with entity. Application of this system of accounting information enables firm in customizing the

requirements of business and ensures consideration of operating practices which are unique to

company.

Preparation of financial systems: It is the process of aggregating accounting

information into standard set of financials which is distributed into management, lenders,

creditors and investors for the evaluation of cash flow, profitability and liquidity. In the general

purpose for the preparation of financial statements there is the preparation of the balance sheet,

income statement and cash flow for the purpose of financial accounting. In Context to British

Airways they have to focus on the financial reporting and they prepare their financial statements

at the end of the year in which there is the recording of all transactions such as incoke

statements, statement of retained earning and statement of the cash flow for the making of the

financial statements (Gabor and Brooks, 2017).

Closing and reporting activity there is the recording of the key data which is used for

support the fiscal policy and monitoring the decision making for the preparation of the Generally

accepted Accounting Principle which is produced for the reasonable period. In this there is the

2

Rajgopal, 2016).

Manual systems- In this system there is the use of this system by the small businesses

and home based businesses, because it is entire manual in which there is the requirement

of the source document, general ledger, journal and subsidiary journals if there is the

need (Bilgin and et.al., 2018).

Replacement of the legacy system- In this there is the completely replace of the legacy

systems with the new up -to- date system because it is the quite expensive system which

is used in the procedure called screen scraping, through the new system it helps in

transfer the data and displayed on the computer screen which help in making the different

applications such as inventory, payroll. In the home based variety there is the use of the

accounting information system to keep the competitive in the industry (Drake, Quinn and

Thornock, 2017).

In relevance to British Airways, information technology of legacy system is utilised by an

organization for the purpose of collecting data and for managing the collected information of the

historical data that is essential for the investors for analysing options of investment associated

with entity. Application of this system of accounting information enables firm in customizing the

requirements of business and ensures consideration of operating practices which are unique to

company.

Preparation of financial systems: It is the process of aggregating accounting

information into standard set of financials which is distributed into management, lenders,

creditors and investors for the evaluation of cash flow, profitability and liquidity. In the general

purpose for the preparation of financial statements there is the preparation of the balance sheet,

income statement and cash flow for the purpose of financial accounting. In Context to British

Airways they have to focus on the financial reporting and they prepare their financial statements

at the end of the year in which there is the recording of all transactions such as incoke

statements, statement of retained earning and statement of the cash flow for the making of the

financial statements (Gabor and Brooks, 2017).

Closing and reporting activity there is the recording of the key data which is used for

support the fiscal policy and monitoring the decision making for the preparation of the Generally

accepted Accounting Principle which is produced for the reasonable period. In this there is the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

recording of the operational financial transactions, for reconcile the module and subsidiary

ledgers.

Revenue recognition process and structure of the revenue

In the revenue recognition process it is the generally accepted accounting principle which

is help in identify the specific conditions for the generation of the revenue and determine the

account which is easily measurable in the company. It is the process for the straight forward

form the product is sold. In this there is of the recognition of the revenue in acquiring the cash

which is collected fat the workforce for the clients on the percentage of the completion method.

It is the process which is apply on the financials and seasonal trends. In this there is the risk and

rewards has been transferred from the seller to buyer. In this there is control of the goods sold is

over the long time. In this collection of the payment is come from the products and services. In

this cost of revenue is reasonably measured. (Gao, Mao, Huang and Yang, 2018).

Cost recoverability method- It is the method used in different approach to generate

revenue recognition which is used for offsetting the revenue by the expenses until all

project cost is accounted (Hapsoro and Husain, 2019).

Percentage of completion method- In this there is the recognition of the revenue by the

completion of the long term projects that help in provide the services to construction and

engineering services that help in generate of the revenue which is used for the long term

contract which is enforceable by the law. In this revenue is recognized at the time of the

milestones and it is calculated on the basis of the cost.

Sales basis method- In this method there is the sales is based on the revenue recognition

methods which is recorded at the time of the sale. It is defined as the period of time in

which goods and services are charged according to time when payment is made.

Instalment method- It is the method use by the organization in which they rely on the

customers on the timely manner for the collection of the payment. It is the method used

for the offset the related cost.

Completed contract method- In this method there is the recognize of the revenue when

the project is complete and the contract is satisfied. This method is applies to both

revenue and expenses it is the requirements for the completion of the percentage method.

In this revenue is not recognized until the project is complete (Husnin, Nawawi, Salin

and Zhou, 2016).

3

ledgers.

Revenue recognition process and structure of the revenue

In the revenue recognition process it is the generally accepted accounting principle which

is help in identify the specific conditions for the generation of the revenue and determine the

account which is easily measurable in the company. It is the process for the straight forward

form the product is sold. In this there is of the recognition of the revenue in acquiring the cash

which is collected fat the workforce for the clients on the percentage of the completion method.

It is the process which is apply on the financials and seasonal trends. In this there is the risk and

rewards has been transferred from the seller to buyer. In this there is control of the goods sold is

over the long time. In this collection of the payment is come from the products and services. In

this cost of revenue is reasonably measured. (Gao, Mao, Huang and Yang, 2018).

Cost recoverability method- It is the method used in different approach to generate

revenue recognition which is used for offsetting the revenue by the expenses until all

project cost is accounted (Hapsoro and Husain, 2019).

Percentage of completion method- In this there is the recognition of the revenue by the

completion of the long term projects that help in provide the services to construction and

engineering services that help in generate of the revenue which is used for the long term

contract which is enforceable by the law. In this revenue is recognized at the time of the

milestones and it is calculated on the basis of the cost.

Sales basis method- In this method there is the sales is based on the revenue recognition

methods which is recorded at the time of the sale. It is defined as the period of time in

which goods and services are charged according to time when payment is made.

Instalment method- It is the method use by the organization in which they rely on the

customers on the timely manner for the collection of the payment. It is the method used

for the offset the related cost.

Completed contract method- In this method there is the recognize of the revenue when

the project is complete and the contract is satisfied. This method is applies to both

revenue and expenses it is the requirements for the completion of the percentage method.

In this revenue is not recognized until the project is complete (Husnin, Nawawi, Salin

and Zhou, 2016).

3

British Airways adopts sales basis method of revenue recognition, that is, revenue is

recorded in books of accounts only after service is delivered to customers, even if payment is

received before hand. (Jones, 2017).

Analysis of the liability side of balance sheet and ratio analysis

Balance sheet is classified into factors Assets and Liabilities in which different things are

written according to their headings. In the liability side means that company owes to outside

party, there is the payment of the bills which is pay to suppliers for the interest on bonds, there is

issue of the rent, salaries and utilities. In the liability side there is the differentiation is done on

current liability and non current liability. In the current liability there are many items are include

bank indebtedness, wages payable, interest payable and dividend payable, unearned premium

and accounts payables. In the liability side there is the discuss of the shareholders equity. In this

there is the discussion of the retailed earnings which is used by business to pay off the debt and it

is distributed to shareholders in form of dividend.

Liability is structured into three types which is current liabilities, non current liabilities

and contingent liabilities.

Non current liabilities means debt or obligation that is due in over the year time, it is the

long term debt to acquire the immediate capital for the invest in new capital. The list of

the non- current liability are bonds payable, mortgage payable and deferred tax liabilities

(Pedersen, Gwozdz and Hvass, 2018).

Current liability include short term liabilities for the debt and obligation that is paid

within a year. It is closely watched by the management for the company that is possess

the liquidity form the current assets for the grantee the debts (Mukhametzyanov and

Nugaev, 2016).

Contingent liabilities is occur when there is the outcome of the future event, it is the

potential liabilities which is face by the lawsuit in this contingent liability is recorded if

the liability is probable. Examples are lawsuits and product warranties.

Bond valuation, in the valuation of bonds there is the technique is used for determining

the theoretical fair value from the specific bond (Leong and Sung, 2018). It includes calculating

the present value of the bonds in the future interest payment which is depend on the rate of return

for the investment. In context to British Airways, it bond is passed in guidelines of Trust 2018-A

Bond which offers coupon of 3.58 percent. Various types of bonds are issued by company such

4

recorded in books of accounts only after service is delivered to customers, even if payment is

received before hand. (Jones, 2017).

Analysis of the liability side of balance sheet and ratio analysis

Balance sheet is classified into factors Assets and Liabilities in which different things are

written according to their headings. In the liability side means that company owes to outside

party, there is the payment of the bills which is pay to suppliers for the interest on bonds, there is

issue of the rent, salaries and utilities. In the liability side there is the differentiation is done on

current liability and non current liability. In the current liability there are many items are include

bank indebtedness, wages payable, interest payable and dividend payable, unearned premium

and accounts payables. In the liability side there is the discuss of the shareholders equity. In this

there is the discussion of the retailed earnings which is used by business to pay off the debt and it

is distributed to shareholders in form of dividend.

Liability is structured into three types which is current liabilities, non current liabilities

and contingent liabilities.

Non current liabilities means debt or obligation that is due in over the year time, it is the

long term debt to acquire the immediate capital for the invest in new capital. The list of

the non- current liability are bonds payable, mortgage payable and deferred tax liabilities

(Pedersen, Gwozdz and Hvass, 2018).

Current liability include short term liabilities for the debt and obligation that is paid

within a year. It is closely watched by the management for the company that is possess

the liquidity form the current assets for the grantee the debts (Mukhametzyanov and

Nugaev, 2016).

Contingent liabilities is occur when there is the outcome of the future event, it is the

potential liabilities which is face by the lawsuit in this contingent liability is recorded if

the liability is probable. Examples are lawsuits and product warranties.

Bond valuation, in the valuation of bonds there is the technique is used for determining

the theoretical fair value from the specific bond (Leong and Sung, 2018). It includes calculating

the present value of the bonds in the future interest payment which is depend on the rate of return

for the investment. In context to British Airways, it bond is passed in guidelines of Trust 2018-A

Bond which offers coupon of 3.58 percent. Various types of bonds are issued by company such

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as, hybrid bond, convertible bond as well as non-convertible bonds. Focus is on international

bond as firm operates in airline industry.

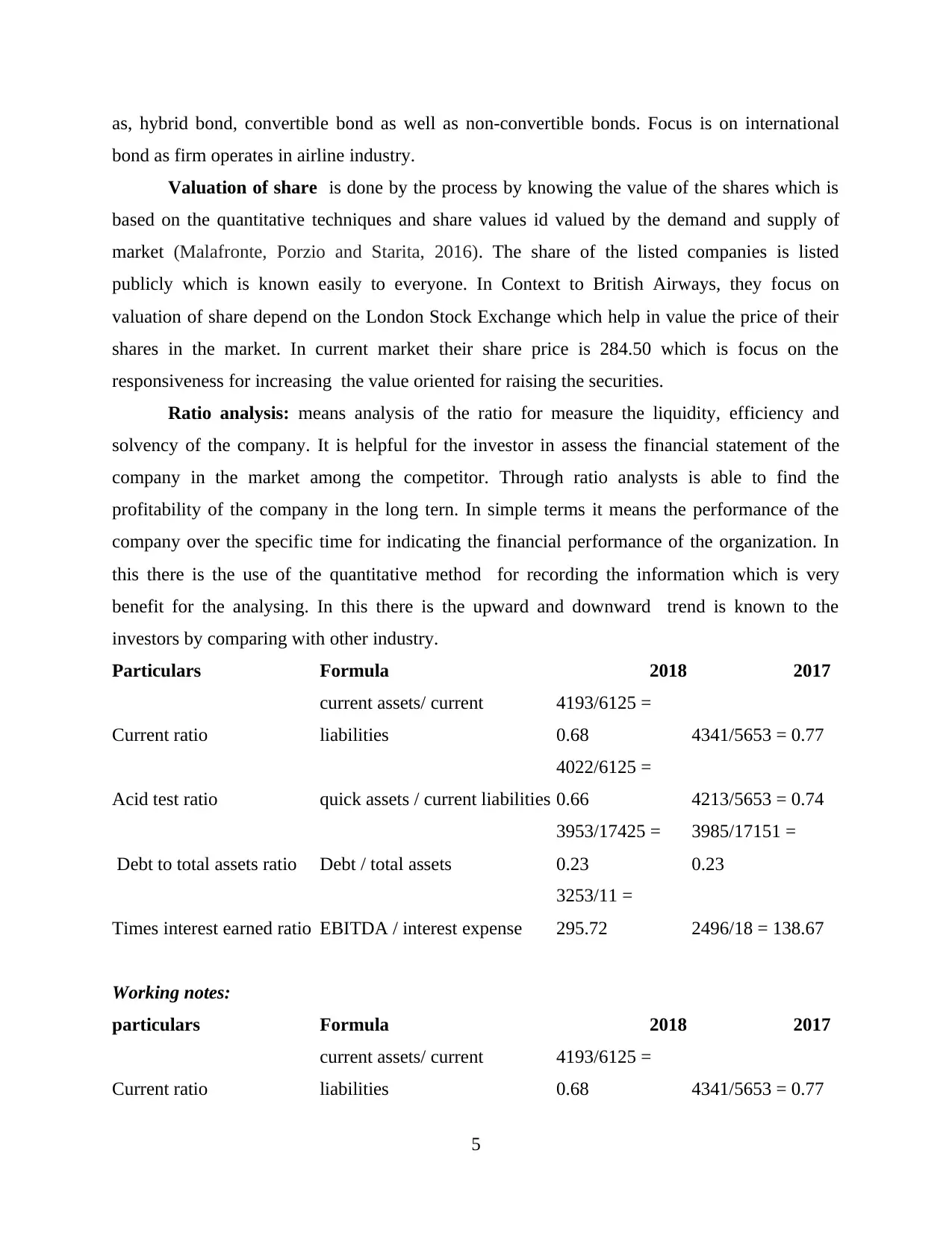

Valuation of share is done by the process by knowing the value of the shares which is

based on the quantitative techniques and share values id valued by the demand and supply of

market (Malafronte, Porzio and Starita, 2016). The share of the listed companies is listed

publicly which is known easily to everyone. In Context to British Airways, they focus on

valuation of share depend on the London Stock Exchange which help in value the price of their

shares in the market. In current market their share price is 284.50 which is focus on the

responsiveness for increasing the value oriented for raising the securities.

Ratio analysis: means analysis of the ratio for measure the liquidity, efficiency and

solvency of the company. It is helpful for the investor in assess the financial statement of the

company in the market among the competitor. Through ratio analysts is able to find the

profitability of the company in the long tern. In simple terms it means the performance of the

company over the specific time for indicating the financial performance of the organization. In

this there is the use of the quantitative method for recording the information which is very

benefit for the analysing. In this there is the upward and downward trend is known to the

investors by comparing with other industry.

Particulars Formula 2018 2017

Current ratio

current assets/ current

liabilities

4193/6125 =

0.68 4341/5653 = 0.77

Acid test ratio quick assets / current liabilities

4022/6125 =

0.66 4213/5653 = 0.74

Debt to total assets ratio Debt / total assets

3953/17425 =

0.23

3985/17151 =

0.23

Times interest earned ratio EBITDA / interest expense

3253/11 =

295.72 2496/18 = 138.67

Working notes:

particulars Formula 2018 2017

Current ratio

current assets/ current

liabilities

4193/6125 =

0.68 4341/5653 = 0.77

5

bond as firm operates in airline industry.

Valuation of share is done by the process by knowing the value of the shares which is

based on the quantitative techniques and share values id valued by the demand and supply of

market (Malafronte, Porzio and Starita, 2016). The share of the listed companies is listed

publicly which is known easily to everyone. In Context to British Airways, they focus on

valuation of share depend on the London Stock Exchange which help in value the price of their

shares in the market. In current market their share price is 284.50 which is focus on the

responsiveness for increasing the value oriented for raising the securities.

Ratio analysis: means analysis of the ratio for measure the liquidity, efficiency and

solvency of the company. It is helpful for the investor in assess the financial statement of the

company in the market among the competitor. Through ratio analysts is able to find the

profitability of the company in the long tern. In simple terms it means the performance of the

company over the specific time for indicating the financial performance of the organization. In

this there is the use of the quantitative method for recording the information which is very

benefit for the analysing. In this there is the upward and downward trend is known to the

investors by comparing with other industry.

Particulars Formula 2018 2017

Current ratio

current assets/ current

liabilities

4193/6125 =

0.68 4341/5653 = 0.77

Acid test ratio quick assets / current liabilities

4022/6125 =

0.66 4213/5653 = 0.74

Debt to total assets ratio Debt / total assets

3953/17425 =

0.23

3985/17151 =

0.23

Times interest earned ratio EBITDA / interest expense

3253/11 =

295.72 2496/18 = 138.67

Working notes:

particulars Formula 2018 2017

Current ratio

current assets/ current

liabilities

4193/6125 =

0.68 4341/5653 = 0.77

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Acid test ratio quick assets / current liabilities

4022/6125 =

0.66 4213/5653 = 0.74

Debt to total assets ratio Debt / total assets

3953/17425 =

0.23

3985/17151 =

0.23

Times interest earned ratio EBITDA / interest expense

3253/11 =

295.72 2496/18 = 138.67

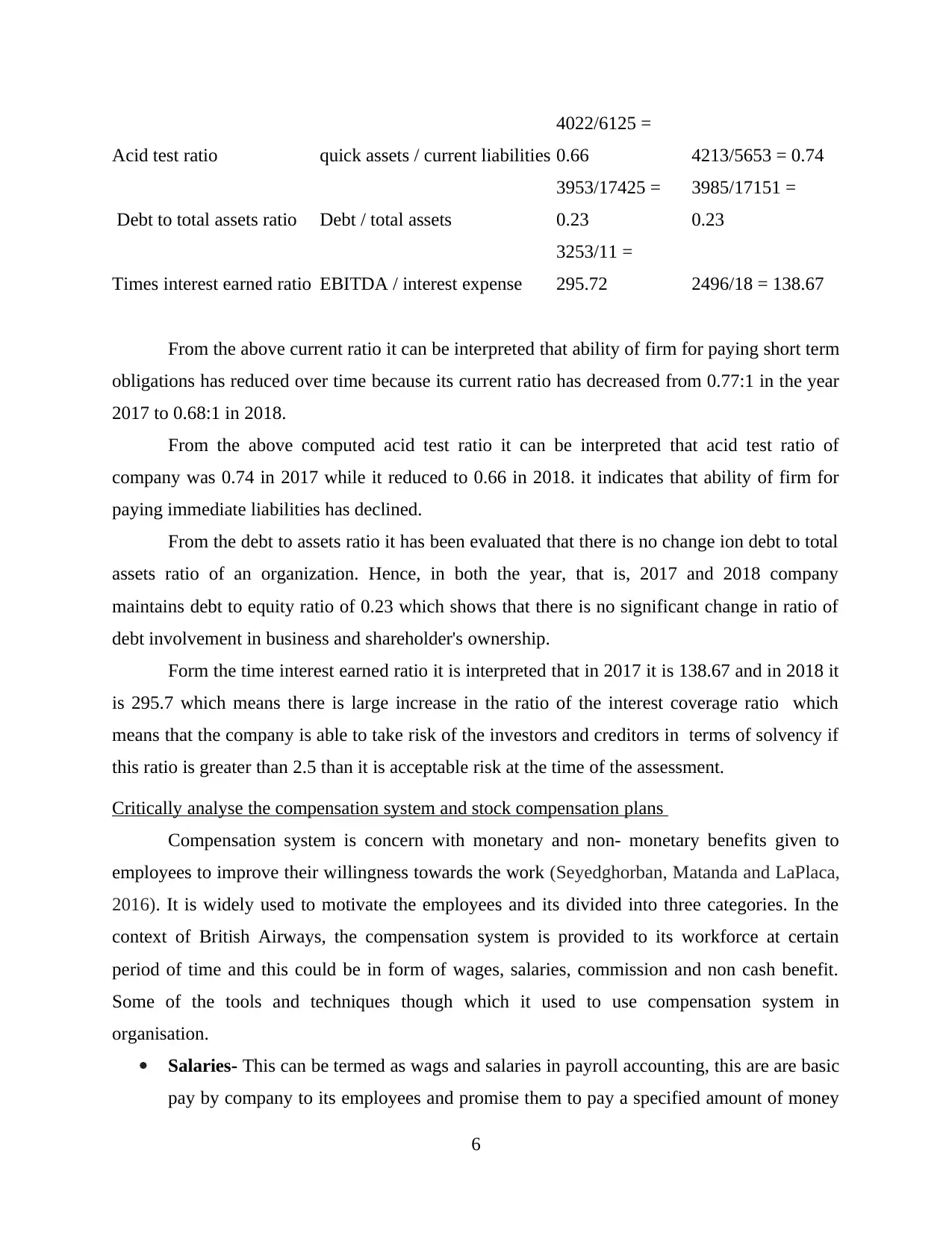

From the above current ratio it can be interpreted that ability of firm for paying short term

obligations has reduced over time because its current ratio has decreased from 0.77:1 in the year

2017 to 0.68:1 in 2018.

From the above computed acid test ratio it can be interpreted that acid test ratio of

company was 0.74 in 2017 while it reduced to 0.66 in 2018. it indicates that ability of firm for

paying immediate liabilities has declined.

From the debt to assets ratio it has been evaluated that there is no change ion debt to total

assets ratio of an organization. Hence, in both the year, that is, 2017 and 2018 company

maintains debt to equity ratio of 0.23 which shows that there is no significant change in ratio of

debt involvement in business and shareholder's ownership.

Form the time interest earned ratio it is interpreted that in 2017 it is 138.67 and in 2018 it

is 295.7 which means there is large increase in the ratio of the interest coverage ratio which

means that the company is able to take risk of the investors and creditors in terms of solvency if

this ratio is greater than 2.5 than it is acceptable risk at the time of the assessment.

Critically analyse the compensation system and stock compensation plans

Compensation system is concern with monetary and non- monetary benefits given to

employees to improve their willingness towards the work (Seyedghorban, Matanda and LaPlaca,

2016). It is widely used to motivate the employees and its divided into three categories. In the

context of British Airways, the compensation system is provided to its workforce at certain

period of time and this could be in form of wages, salaries, commission and non cash benefit.

Some of the tools and techniques though which it used to use compensation system in

organisation.

Salaries- This can be termed as wags and salaries in payroll accounting, this are are basic

pay by company to its employees and promise them to pay a specified amount of money

6

4022/6125 =

0.66 4213/5653 = 0.74

Debt to total assets ratio Debt / total assets

3953/17425 =

0.23

3985/17151 =

0.23

Times interest earned ratio EBITDA / interest expense

3253/11 =

295.72 2496/18 = 138.67

From the above current ratio it can be interpreted that ability of firm for paying short term

obligations has reduced over time because its current ratio has decreased from 0.77:1 in the year

2017 to 0.68:1 in 2018.

From the above computed acid test ratio it can be interpreted that acid test ratio of

company was 0.74 in 2017 while it reduced to 0.66 in 2018. it indicates that ability of firm for

paying immediate liabilities has declined.

From the debt to assets ratio it has been evaluated that there is no change ion debt to total

assets ratio of an organization. Hence, in both the year, that is, 2017 and 2018 company

maintains debt to equity ratio of 0.23 which shows that there is no significant change in ratio of

debt involvement in business and shareholder's ownership.

Form the time interest earned ratio it is interpreted that in 2017 it is 138.67 and in 2018 it

is 295.7 which means there is large increase in the ratio of the interest coverage ratio which

means that the company is able to take risk of the investors and creditors in terms of solvency if

this ratio is greater than 2.5 than it is acceptable risk at the time of the assessment.

Critically analyse the compensation system and stock compensation plans

Compensation system is concern with monetary and non- monetary benefits given to

employees to improve their willingness towards the work (Seyedghorban, Matanda and LaPlaca,

2016). It is widely used to motivate the employees and its divided into three categories. In the

context of British Airways, the compensation system is provided to its workforce at certain

period of time and this could be in form of wages, salaries, commission and non cash benefit.

Some of the tools and techniques though which it used to use compensation system in

organisation.

Salaries- This can be termed as wags and salaries in payroll accounting, this are are basic

pay by company to its employees and promise them to pay a specified amount of money

6

after specified period of time. In the context of British Airways, salaries are given to

workforce for the work done by them and engage them to work for longer period.

Company use systematic method to pay salaries to its employees and tried to satisfy their

expectation from organisation (Pustylnick, 2017).

Bonus system: This system of compensation plan in an organization refers to payment of

lump sum amount to employees at year end for the purpose of achieving higher efficiency

or improving their performance. As this amount is given in lump sum manner instead of

dividing into small portions, it generates the feeling of receiving high amount in

perception of working staff. Hence, they feel motivated and their commitment towards

organization and tasks that is to be performed increases. Hence, ultimately efficiency of

business improves.

Commissions system- This might consider as sales commission and they are computed

according to certain percentage of commission rate (Osadchy and et.al., 2018). In the

company British Airways, this consider same as wages and they determine the regular,

hourly rate and make sure this must be equals to minimum wages. Company ensure that

employees were paid according the exact work done by them and provide them fair

commission as possible.

Piece rate plan- In this workers paid on piece rate plan which receive for the each item

produced by them. In the context of company British Airways, they paid to its workers

who made certain activities and add some value to organisation.

Stock compensation plan is refer to the stock options that is necessary for giving the

rewards to the employees which is used for the longer time depends on the Fair market value of

the stock, if the stock is subject to tax withholding then the tax is paid in cash. Restricted stock It

is the type of stock compensation in which employees receive shares through purchase or gift for

the performance. It is done equally for the set of period for taking the rights of the stock

ownership.

Post retirement benefits refers to the benefits which is included for the payment of the

employees in the benefit plan, pension plan, life insurance and post employment benefits . There

are various plans also which are welfare benefit plans (Schaltegger and Hörisch, 2017).

7

workforce for the work done by them and engage them to work for longer period.

Company use systematic method to pay salaries to its employees and tried to satisfy their

expectation from organisation (Pustylnick, 2017).

Bonus system: This system of compensation plan in an organization refers to payment of

lump sum amount to employees at year end for the purpose of achieving higher efficiency

or improving their performance. As this amount is given in lump sum manner instead of

dividing into small portions, it generates the feeling of receiving high amount in

perception of working staff. Hence, they feel motivated and their commitment towards

organization and tasks that is to be performed increases. Hence, ultimately efficiency of

business improves.

Commissions system- This might consider as sales commission and they are computed

according to certain percentage of commission rate (Osadchy and et.al., 2018). In the

company British Airways, this consider same as wages and they determine the regular,

hourly rate and make sure this must be equals to minimum wages. Company ensure that

employees were paid according the exact work done by them and provide them fair

commission as possible.

Piece rate plan- In this workers paid on piece rate plan which receive for the each item

produced by them. In the context of company British Airways, they paid to its workers

who made certain activities and add some value to organisation.

Stock compensation plan is refer to the stock options that is necessary for giving the

rewards to the employees which is used for the longer time depends on the Fair market value of

the stock, if the stock is subject to tax withholding then the tax is paid in cash. Restricted stock It

is the type of stock compensation in which employees receive shares through purchase or gift for

the performance. It is done equally for the set of period for taking the rights of the stock

ownership.

Post retirement benefits refers to the benefits which is included for the payment of the

employees in the benefit plan, pension plan, life insurance and post employment benefits . There

are various plans also which are welfare benefit plans (Schaltegger and Hörisch, 2017).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Leasing environment and types of lease

Leasing company refers to the physical assets or service which is use by the commercial

client for the individual to established the specific time for generate the return for the regular

payments (Samoilikova, 2020). In the leasing environment there is the both risk are present

which is environmental and social risk which is involve for the combination of the worker safety

which is arising from the use of the physical assets. In Context to British Airways there is the

description of the physical assets for the regular payments,

Capital and operating lease means asset on the company balance sheet in capital lease

and in operating lease it means expense remain off in the balance sheet. In the capital lease there

is the description of the debt in which there is the transfer of the ownership of the assets at the

end of term. In the capital lease ownership is transferred to the lessee at the end of lease term

and in operating lease it is retained by the lessor during and after the lease term (Valaskova,

Kliestik and Kovacova, 2018).

There are mainly three types of lease which are explained below in context to British

Airways:

Absolute net lease- In the net lease there is included of the insurance, taxes and

maintenance. In large business there is the understand of the contract and duration. It is

follow by the British Airways for giving the lease to customers (Zeff, 2016).

Triple net lease: It associates three category of expenses, that is, real property tax,

maintenance as well as insurance. Such expenses can be termed as pass through expense

as in this, owner of property passes tenant in rent excess form.

Modified gross lease: Here, entire burden is passed in owner of property as owner makes

payment of taxes, maintenance and insurance, while tenant is responsible for utility,

interior maintenance and janitorial.

Conclusion

From the above report it has been concluded that financial report is described as the

income statement and balance sheet for the analysis of the financial position in the market. In

this there is the analysis of the accounting information system. Further, this report states that

accounting information system are of various types which are, manual system, legacy system and

replacement of legacy system. Apart from this revenue recognition process is explained and its

method are identified. Liability side of balance sheet is analysed and ratios are computed for the

8

Leasing company refers to the physical assets or service which is use by the commercial

client for the individual to established the specific time for generate the return for the regular

payments (Samoilikova, 2020). In the leasing environment there is the both risk are present

which is environmental and social risk which is involve for the combination of the worker safety

which is arising from the use of the physical assets. In Context to British Airways there is the

description of the physical assets for the regular payments,

Capital and operating lease means asset on the company balance sheet in capital lease

and in operating lease it means expense remain off in the balance sheet. In the capital lease there

is the description of the debt in which there is the transfer of the ownership of the assets at the

end of term. In the capital lease ownership is transferred to the lessee at the end of lease term

and in operating lease it is retained by the lessor during and after the lease term (Valaskova,

Kliestik and Kovacova, 2018).

There are mainly three types of lease which are explained below in context to British

Airways:

Absolute net lease- In the net lease there is included of the insurance, taxes and

maintenance. In large business there is the understand of the contract and duration. It is

follow by the British Airways for giving the lease to customers (Zeff, 2016).

Triple net lease: It associates three category of expenses, that is, real property tax,

maintenance as well as insurance. Such expenses can be termed as pass through expense

as in this, owner of property passes tenant in rent excess form.

Modified gross lease: Here, entire burden is passed in owner of property as owner makes

payment of taxes, maintenance and insurance, while tenant is responsible for utility,

interior maintenance and janitorial.

Conclusion

From the above report it has been concluded that financial report is described as the

income statement and balance sheet for the analysis of the financial position in the market. In

this there is the analysis of the accounting information system. Further, this report states that

accounting information system are of various types which are, manual system, legacy system and

replacement of legacy system. Apart from this revenue recognition process is explained and its

method are identified. Liability side of balance sheet is analysed and ratios are computed for the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purpose of analysing performance of business. Lastly, leasing environment and compensation

system is studied.

REFERENCES

Books and journals

Akbar, S. and et.al., 2017. Board structure and corporate risk taking in the UK financial sector.

International Review of Financial Analysis. 50. pp.101-110.

Aouadi, A. and Marsat, S., 2018. Do ESG controversies matter for firm value? Evidence from

international data.Journal of Business Ethics. 151(4). pp.1027-1047.

Białkowski, J. and Perera, D., 2019. Stock index futures arbitrage: Evidence from a meta-

analysis. International Review of Financial Analysis. 61. pp.284-294.

Bilgin, M. H. and et.al., 2018. The effects of uncertainty measures on the price of gold.

International Review of Financial Analysis. 58. pp.1-7.

Birch, K., 2017. Rethinking value in the bio-economy: Finance, assetization, and the

management of value.Science, Technology, & Human Values. 42(3). pp.460-490.

Dichev, I., Graham, J., Harvey, C.R. and Rajgopal, S., 2016. The misrepresentation of

earnings.Financial Analysts Journal. 72(1). pp.22-35.

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from EDGAR. Accounting Horizons.

31(3). pp.55-68.

Gabor, D. and Brooks, S., 2017. The digital revolution in financial inclusion: international

development in the fintech era.New Political Economy. 22(4). pp.423-436.

Gao, H., Mao, S., Huang, W. and Yang, X., 2018. Applying probabilistic model checking to

financial production risk evaluation and control: A case study of Alibaba’s Yu’e

Bao.IEEE Transactions on Computational Social Systems. 5(3). pp.785-795.

Gordini, N. and Rancati, E., 2017. Gender diversity in the Italian boardroom and firm financial

performance.Management Research Review.

Hapsoro, D. and Husain, Z. F., 2019. Does sustainability report moderate the effect of financial

performance on investor reaction? Evidence of Indonesian listed firms. International Journal of

Business. 24(3). pp.308-328.

Husnin, A. I., Nawawi, A., Salin, A. S. A. P. and Zhou, H., 2016. Corporate governance and

auditor quality–Malaysian evidence.Asian Review of Accounting.

Jones, S., 2017. Corporate bankruptcy prediction: a high dimensional analysis.Review of

Accounting Studies. 22(3). pp.1366-1422.

Leong, K. and Sung, A., 2018. FinTech (Financial Technology): what is it and how to use

technologies to create business value in fintech way?. International Journal of Innovation,

Management and Technology. 9(2). pp.74-78.

9

system is studied.

REFERENCES

Books and journals

Akbar, S. and et.al., 2017. Board structure and corporate risk taking in the UK financial sector.

International Review of Financial Analysis. 50. pp.101-110.

Aouadi, A. and Marsat, S., 2018. Do ESG controversies matter for firm value? Evidence from

international data.Journal of Business Ethics. 151(4). pp.1027-1047.

Białkowski, J. and Perera, D., 2019. Stock index futures arbitrage: Evidence from a meta-

analysis. International Review of Financial Analysis. 61. pp.284-294.

Bilgin, M. H. and et.al., 2018. The effects of uncertainty measures on the price of gold.

International Review of Financial Analysis. 58. pp.1-7.

Birch, K., 2017. Rethinking value in the bio-economy: Finance, assetization, and the

management of value.Science, Technology, & Human Values. 42(3). pp.460-490.

Dichev, I., Graham, J., Harvey, C.R. and Rajgopal, S., 2016. The misrepresentation of

earnings.Financial Analysts Journal. 72(1). pp.22-35.

Drake, M. S., Quinn, P. J. and Thornock, J. R., 2017. Who uses financial statements? A

demographic analysis of financial statement downloads from EDGAR. Accounting Horizons.

31(3). pp.55-68.

Gabor, D. and Brooks, S., 2017. The digital revolution in financial inclusion: international

development in the fintech era.New Political Economy. 22(4). pp.423-436.

Gao, H., Mao, S., Huang, W. and Yang, X., 2018. Applying probabilistic model checking to

financial production risk evaluation and control: A case study of Alibaba’s Yu’e

Bao.IEEE Transactions on Computational Social Systems. 5(3). pp.785-795.

Gordini, N. and Rancati, E., 2017. Gender diversity in the Italian boardroom and firm financial

performance.Management Research Review.

Hapsoro, D. and Husain, Z. F., 2019. Does sustainability report moderate the effect of financial

performance on investor reaction? Evidence of Indonesian listed firms. International Journal of

Business. 24(3). pp.308-328.

Husnin, A. I., Nawawi, A., Salin, A. S. A. P. and Zhou, H., 2016. Corporate governance and

auditor quality–Malaysian evidence.Asian Review of Accounting.

Jones, S., 2017. Corporate bankruptcy prediction: a high dimensional analysis.Review of

Accounting Studies. 22(3). pp.1366-1422.

Leong, K. and Sung, A., 2018. FinTech (Financial Technology): what is it and how to use

technologies to create business value in fintech way?. International Journal of Innovation,

Management and Technology. 9(2). pp.74-78.

9

Malafronte, I., Porzio, C. and Starita, M. G., 2016. The nature and determinants of disclosure

practices in the insurance industry: Evidence from European insurers. International Review of

Financial Analysis. 45. pp.367-382.

Mukhametzyanov, R. Z. and Nugaev, F.S., 2016. Financial statements as an information base for

the analysis and management decisions.Journal of Economics and Economic Education

Research. 17. p.47.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Pedersen, E. R. G., Gwozdz, W. and Hvass, K.K., 2018. Exploring the relationship between

business model innovation, corporate sustainability, and organisational values within

the fashion industry.Journal of Business Ethics.149(2). pp.267-284.

Pustylnick, I., 2017. Comparison of liquidity based and financial performance based indicators

in financial analysis.Oeconomia Copernicana. 8(1). pp.83-97.

Samoilikova, A., 2020. Financial Policy of Innovation Development Providing: The Impact

Formalization. Financial Markets, Institutions and Risks. 4(2). pp.5-15.

Schaltegger, S. and Hörisch, J., 2017. In search of the dominant rationale in sustainability

management: legitimacy-or profit-seeking?.journal of Business Ethics. 145(2). pp.259-

276.

Seyedghorban, Z., Matanda, M. J. and LaPlaca, P., 2016. Advancing theory and knowledge in

the business-to-business branding literature. Journal of Business Research. 69(8). pp.2664-2677.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis.Oeconomia Copernicana. 9(1). pp.105-121.

Zeff, S. A., 2016. The Trueblood Study Group on the objectives of financial statements (1971–

73): A historical study.Journal of Accounting and Public policy.35(2). pp.134-161.

Online:

British Airways. 2020. [Online],. Available through:

<\\nhttps://www.iairgroup.com/~/media/Files/I/IAG/annual-reports/ba/en/british-

airways-plc-annual-report-and-accounts-2018.pdf\\n>

10

practices in the insurance industry: Evidence from European insurers. International Review of

Financial Analysis. 45. pp.367-382.

Mukhametzyanov, R. Z. and Nugaev, F.S., 2016. Financial statements as an information base for

the analysis and management decisions.Journal of Economics and Economic Education

Research. 17. p.47.

Osadchy, E. A. and et.al., 2018. Financial statements of a company as an information base for

decision-making in a transforming economy.

Pedersen, E. R. G., Gwozdz, W. and Hvass, K.K., 2018. Exploring the relationship between

business model innovation, corporate sustainability, and organisational values within

the fashion industry.Journal of Business Ethics.149(2). pp.267-284.

Pustylnick, I., 2017. Comparison of liquidity based and financial performance based indicators

in financial analysis.Oeconomia Copernicana. 8(1). pp.83-97.

Samoilikova, A., 2020. Financial Policy of Innovation Development Providing: The Impact

Formalization. Financial Markets, Institutions and Risks. 4(2). pp.5-15.

Schaltegger, S. and Hörisch, J., 2017. In search of the dominant rationale in sustainability

management: legitimacy-or profit-seeking?.journal of Business Ethics. 145(2). pp.259-

276.

Seyedghorban, Z., Matanda, M. J. and LaPlaca, P., 2016. Advancing theory and knowledge in

the business-to-business branding literature. Journal of Business Research. 69(8). pp.2664-2677.

Valaskova, K., Kliestik, T. and Kovacova, M., 2018. Management of financial risks in Slovak

enterprises using regression analysis.Oeconomia Copernicana. 9(1). pp.105-121.

Zeff, S. A., 2016. The Trueblood Study Group on the objectives of financial statements (1971–

73): A historical study.Journal of Accounting and Public policy.35(2). pp.134-161.

Online:

British Airways. 2020. [Online],. Available through:

<\\nhttps://www.iairgroup.com/~/media/Files/I/IAG/annual-reports/ba/en/british-

airways-plc-annual-report-and-accounts-2018.pdf\\n>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.