British Airways Case Study: Data Types, Financials, and Business Risks

VerifiedAdded on 2022/09/27

|12

|3861

|30

Report

AI Summary

This report presents a comprehensive case study of British Airways, addressing various aspects of data analysis and financial performance. The report begins by differentiating between qualitative and quantitative data, exploring their collection methods and applications. It then delves into the analysis of British Airways' aircraft fleet, comparing manufacturers and calculating percentages. Furthermore, the report examines the airline's financial health through key ratios such as Return on Employed Capital, Return on Equity, and the Current Ratio, offering insights into its efficiency and liquidity. Finally, the report identifies and discusses the major business risks faced by British Airways, including competition, economic conditions, government intervention, and employee relations, providing a holistic view of the airline's operational environment and financial strategies. The report uses data from the company's 2017 annual report.

USING INFORMATION 1

Using information

Name:

Tutor:

Institution:

A case study of British Airways

Using information

Name:

Tutor:

Institution:

A case study of British Airways

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

USING INFORMATION 2

PART 1:

Qualitative data is data that provides understanding and perceptions concerning a given problem.

It is mostly approximated thus the researcher should be well equipped with knowledge

concerning the type of data that is required way before it is collected. Nature of this data is

descriptive thus analyzing it becomes a little bit complex and difficult. Data is categorized in

terms of physical characteristics and object properties. Interpretation of this data, that is in terms

of appearance, smell, texture, gender, nationality, and others, is done either verbally or written

descriptions form assuming numbers. To collect this data, there are several strategies that are

used; observation, interviews, focus group, archival materials such as newspapers and

magazines.

Quantitative data is the type of data that focuses on numbers or quantity, as it computes values

and counts. This data is stated in numerical form and it is majorly used for statistical analysis

(Crowder 2017). It is used in statistical tests and computation. It deals with measurements such

as weights, heights, volume, size, length, speed and humidity among others. Its presented in

tables, graphs, charts and diagrams, and other forms. It is either continuous or discrete and is

collected using surveys, observations, interviews and experiments (Hurst Relander & Cordes

2016).

The key differences between qualitative and quantitative data are elaborated. Qualitative data

involves objects categorization that is based on attributes while as quantitative mainly involves

countable data that is in number and value form (Goertzen 2017). The research methodology in

qualitative is exploratory as in quantitative its conclusive naturally. Basing on the inquiry

approach, qualitative data is subjective and complete while as quantitative is objective and has a

certain aim. Analysis of qualitative data is usually non statistical whereas quantitative data is

analyzed using statistical methods (Mihas 2019). Data collection method in qualitative is

unstructured while in quantitative the methods involved has a structure. Qualitative data is used

to show the level of understanding but quantitative data indicates the occurrence level. Small

non-representatives’ samples are used in drawing qualitative data in small amounts while as

large sized data drawn for quantitative is from representative samples. Quantitative data provides

an initial understanding as it elaborates a problem unlike quantitative that gives

recommendations that require actions to be taken (Mertens, Pugliese & Recker, 2017).

PART 1:

Qualitative data is data that provides understanding and perceptions concerning a given problem.

It is mostly approximated thus the researcher should be well equipped with knowledge

concerning the type of data that is required way before it is collected. Nature of this data is

descriptive thus analyzing it becomes a little bit complex and difficult. Data is categorized in

terms of physical characteristics and object properties. Interpretation of this data, that is in terms

of appearance, smell, texture, gender, nationality, and others, is done either verbally or written

descriptions form assuming numbers. To collect this data, there are several strategies that are

used; observation, interviews, focus group, archival materials such as newspapers and

magazines.

Quantitative data is the type of data that focuses on numbers or quantity, as it computes values

and counts. This data is stated in numerical form and it is majorly used for statistical analysis

(Crowder 2017). It is used in statistical tests and computation. It deals with measurements such

as weights, heights, volume, size, length, speed and humidity among others. Its presented in

tables, graphs, charts and diagrams, and other forms. It is either continuous or discrete and is

collected using surveys, observations, interviews and experiments (Hurst Relander & Cordes

2016).

The key differences between qualitative and quantitative data are elaborated. Qualitative data

involves objects categorization that is based on attributes while as quantitative mainly involves

countable data that is in number and value form (Goertzen 2017). The research methodology in

qualitative is exploratory as in quantitative its conclusive naturally. Basing on the inquiry

approach, qualitative data is subjective and complete while as quantitative is objective and has a

certain aim. Analysis of qualitative data is usually non statistical whereas quantitative data is

analyzed using statistical methods (Mihas 2019). Data collection method in qualitative is

unstructured while in quantitative the methods involved has a structure. Qualitative data is used

to show the level of understanding but quantitative data indicates the occurrence level. Small

non-representatives’ samples are used in drawing qualitative data in small amounts while as

large sized data drawn for quantitative is from representative samples. Quantitative data provides

an initial understanding as it elaborates a problem unlike quantitative that gives

recommendations that require actions to be taken (Mertens, Pugliese & Recker, 2017).

USING INFORMATION 3

The main difference between horizontal and vertical analysis is basically concerned with time

frame. Analyzing horizontally gives an eye at a number of years and vertical involves just a

single year. Horizontal analysis offers the financial information difference of one company that

has same financial income types in different years. It is majorly beneficial when looking for the

change in percentage that has occurred in the company over each of the past years. Vertical

analysis shows all of the company’s financial information of a specific year. Every item is

expressed as a percentage of a given statistic. This analysis allows the organization to compare it

production with that of other organizations under the same field. On horizontal, analysis focuses

on the amounts in the financial statements that have been in the past and are converted to be a

percentage of the amount from a specific base year. On the other hand, vertical analysis involves

results in each of the amount of the balance sheet and each amount of the income statement that

are expressed in a percentage of the total assets and net sales respectively.

Big data is the gathering and analysis of data sets that are compound in volume, velocity

of where collection was done and variety dimensions. It involves massive volume of structured

and unstructured data that is difficult to process using database and a software that is traditional.

It is used to develop an analysis of comprehensions that promote good decisions and business

moves that are strategic and systematic (De Mauro et al., 2016). This is achieved by the use of

multidisciplinary groups that has subject area experts, computational experts, statisticians and

machine learner experts. Statistical data is gathering, analysis and interpretation of numerical

data with the help of the theory of probability that include methods that draw inferences

concerning properties of a given population from a conducted examination of a randomly

selected sample. It is used in analyzing things and updating on current happenings

mathematically. The distinction that is present between these two types of data is that, big data

requires statistical tools and methods to compute and perform analysis while as the statistical

data requires these tools and an addition of well trained and skilled personnel (De Mauro et al.,

2015).

Data quality is the state in which a set of properties of qualitative or quantitative data

satisfies its requirements (Madar 2015). These properties are in terms of its completeness, how

accurate, validity, availability, rate of consistency, timeliness and its relevance. Data quality is

important in financial statement as it shows accuracy, data timelines and completeness that help

The main difference between horizontal and vertical analysis is basically concerned with time

frame. Analyzing horizontally gives an eye at a number of years and vertical involves just a

single year. Horizontal analysis offers the financial information difference of one company that

has same financial income types in different years. It is majorly beneficial when looking for the

change in percentage that has occurred in the company over each of the past years. Vertical

analysis shows all of the company’s financial information of a specific year. Every item is

expressed as a percentage of a given statistic. This analysis allows the organization to compare it

production with that of other organizations under the same field. On horizontal, analysis focuses

on the amounts in the financial statements that have been in the past and are converted to be a

percentage of the amount from a specific base year. On the other hand, vertical analysis involves

results in each of the amount of the balance sheet and each amount of the income statement that

are expressed in a percentage of the total assets and net sales respectively.

Big data is the gathering and analysis of data sets that are compound in volume, velocity

of where collection was done and variety dimensions. It involves massive volume of structured

and unstructured data that is difficult to process using database and a software that is traditional.

It is used to develop an analysis of comprehensions that promote good decisions and business

moves that are strategic and systematic (De Mauro et al., 2016). This is achieved by the use of

multidisciplinary groups that has subject area experts, computational experts, statisticians and

machine learner experts. Statistical data is gathering, analysis and interpretation of numerical

data with the help of the theory of probability that include methods that draw inferences

concerning properties of a given population from a conducted examination of a randomly

selected sample. It is used in analyzing things and updating on current happenings

mathematically. The distinction that is present between these two types of data is that, big data

requires statistical tools and methods to compute and perform analysis while as the statistical

data requires these tools and an addition of well trained and skilled personnel (De Mauro et al.,

2015).

Data quality is the state in which a set of properties of qualitative or quantitative data

satisfies its requirements (Madar 2015). These properties are in terms of its completeness, how

accurate, validity, availability, rate of consistency, timeliness and its relevance. Data quality is

important in financial statement as it shows accuracy, data timelines and completeness that help

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

USING INFORMATION 4

in meeting the relevant regulatory needs (Enyi 2019). This also help in amenability to assess with

their own objectives of data quality. Accuracy is very crucial in financial reports as they help the

organizations management to make effective and well-versed decisions concerning the

objectives, goals and strategies of the company. They also provide financial information of the

company that is then presented to shareholders and investors. The accuracy of the information

provided in the financial statements, helps in increasing the reliability as they take that the health

and performance information to be complete (Adeneye & Ahmed 2015). The information should

be relevant since the investors require it so that they can make decisions on matters involving the

company financially. It calls for cautiousness as this involves a huge risk of losing money.

Therefore, the quality of these financial statements should be commendable and of high

dependence on making the rightful profitable decisions for the company. Also when quality is

maintained, through the financial statements, finance organizations are able to understand the

relationships among its customers (Williams & Dobelman 2017). This understanding makes it

easier for this firms to comply with the laundering regulations of anti-money to meet the needs of

the customers. Since financial statements are used in giving a clear picture of the company

finances management, data quality ensure no false information or misinterpretation that affects

the value add is avoided (Fraser et al., 2010).

Part 2: BRITISH AIRWAYS CASE STUDY

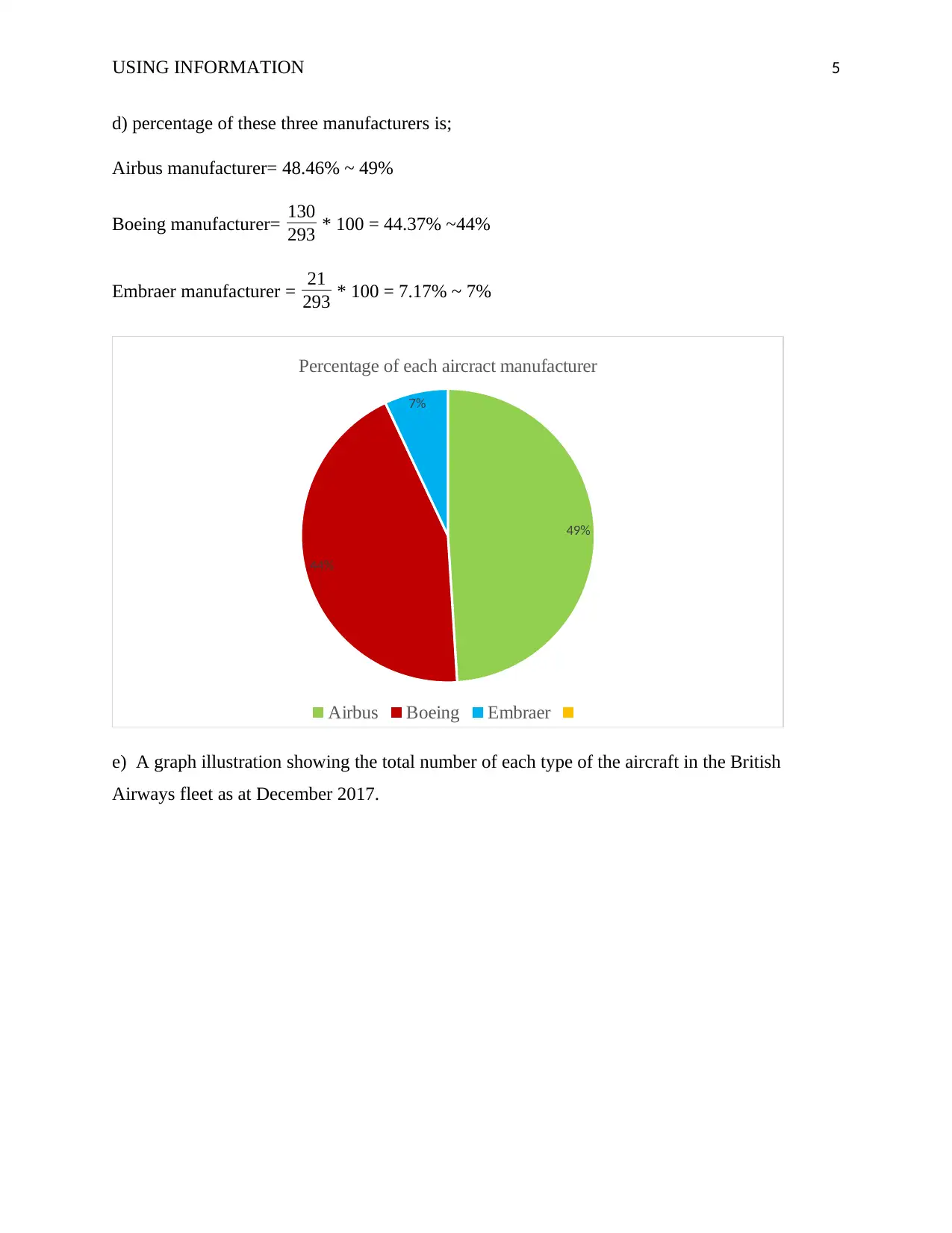

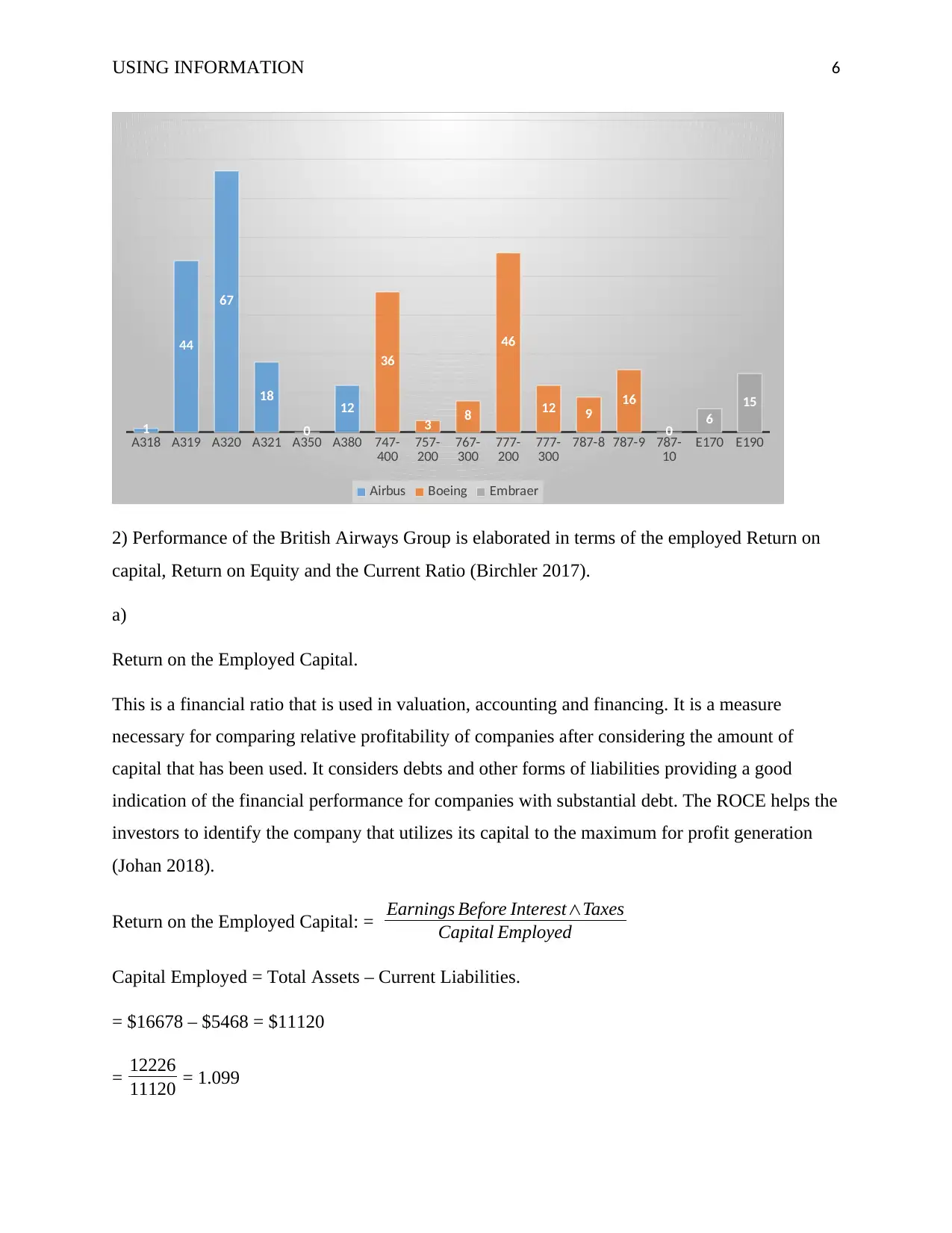

1 a) As at December 2017, the aircraft type that had the largest number of aircraft was the Airbus

A320 that was at sixty-seven aircrafts.

b) As at December 2017, Airbus manufacturer had a total of one hundred and forty-two aircrafts,

that is, (1+44+67+18+12= 142), Boeing manufacturer represented its aircraft type with a total of

one hundred and thirty, that is, (36+3+8+46+12+9+16=130) and the Embraer manufacturer had a

representation of a total of twenty-one aircrafts, that is, (6+15=21). Basing on this analysis, the

Airbus aircraft manufacturer had the biggest representation in the British Airways fleet (Petrescu

et al,. 2017).

c) The percentage that the Airbus manufacturer takes in representing itself in the British Airways

fleet over the total in 2017 is:

= 142

293 * 100 = 48.46%

in meeting the relevant regulatory needs (Enyi 2019). This also help in amenability to assess with

their own objectives of data quality. Accuracy is very crucial in financial reports as they help the

organizations management to make effective and well-versed decisions concerning the

objectives, goals and strategies of the company. They also provide financial information of the

company that is then presented to shareholders and investors. The accuracy of the information

provided in the financial statements, helps in increasing the reliability as they take that the health

and performance information to be complete (Adeneye & Ahmed 2015). The information should

be relevant since the investors require it so that they can make decisions on matters involving the

company financially. It calls for cautiousness as this involves a huge risk of losing money.

Therefore, the quality of these financial statements should be commendable and of high

dependence on making the rightful profitable decisions for the company. Also when quality is

maintained, through the financial statements, finance organizations are able to understand the

relationships among its customers (Williams & Dobelman 2017). This understanding makes it

easier for this firms to comply with the laundering regulations of anti-money to meet the needs of

the customers. Since financial statements are used in giving a clear picture of the company

finances management, data quality ensure no false information or misinterpretation that affects

the value add is avoided (Fraser et al., 2010).

Part 2: BRITISH AIRWAYS CASE STUDY

1 a) As at December 2017, the aircraft type that had the largest number of aircraft was the Airbus

A320 that was at sixty-seven aircrafts.

b) As at December 2017, Airbus manufacturer had a total of one hundred and forty-two aircrafts,

that is, (1+44+67+18+12= 142), Boeing manufacturer represented its aircraft type with a total of

one hundred and thirty, that is, (36+3+8+46+12+9+16=130) and the Embraer manufacturer had a

representation of a total of twenty-one aircrafts, that is, (6+15=21). Basing on this analysis, the

Airbus aircraft manufacturer had the biggest representation in the British Airways fleet (Petrescu

et al,. 2017).

c) The percentage that the Airbus manufacturer takes in representing itself in the British Airways

fleet over the total in 2017 is:

= 142

293 * 100 = 48.46%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

USING INFORMATION 5

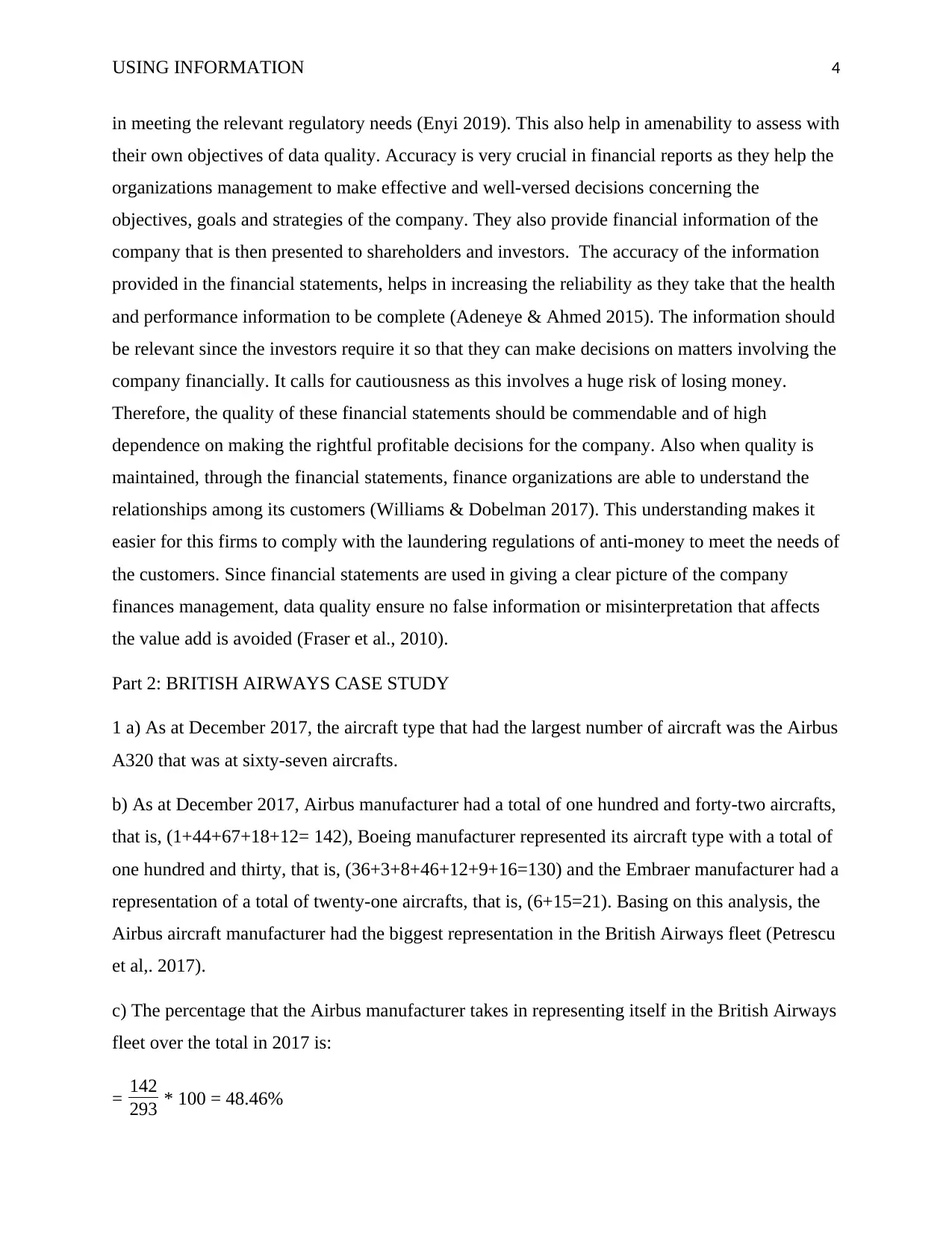

d) percentage of these three manufacturers is;

Airbus manufacturer= 48.46% ~ 49%

Boeing manufacturer= 130

293 * 100 = 44.37% ~44%

Embraer manufacturer = 21

293 * 100 = 7.17% ~ 7%

49%

44%

7%

Percentage of each aircract manufacturer

Airbus Boeing Embraer

e) A graph illustration showing the total number of each type of the aircraft in the British

Airways fleet as at December 2017.

d) percentage of these three manufacturers is;

Airbus manufacturer= 48.46% ~ 49%

Boeing manufacturer= 130

293 * 100 = 44.37% ~44%

Embraer manufacturer = 21

293 * 100 = 7.17% ~ 7%

49%

44%

7%

Percentage of each aircract manufacturer

Airbus Boeing Embraer

e) A graph illustration showing the total number of each type of the aircraft in the British

Airways fleet as at December 2017.

USING INFORMATION 6

A318 A319 A320 A321 A350 A380 747-

400 757-

200 767-

300 777-

200 777-

300 787-8 787-9 787-

10 E170 E190

1

44

67

18

0

12

36

3 8

46

12 9 16

0 6

15

Airbus Boeing Embraer

2) Performance of the British Airways Group is elaborated in terms of the employed Return on

capital, Return on Equity and the Current Ratio (Birchler 2017).

a)

Return on the Employed Capital.

This is a financial ratio that is used in valuation, accounting and financing. It is a measure

necessary for comparing relative profitability of companies after considering the amount of

capital that has been used. It considers debts and other forms of liabilities providing a good

indication of the financial performance for companies with substantial debt. The ROCE helps the

investors to identify the company that utilizes its capital to the maximum for profit generation

(Johan 2018).

Return on the Employed Capital: = Earnings Before Interest∧Taxes

Capital Employed

Capital Employed = Total Assets – Current Liabilities.

= $16678 – $5468 = $11120

= 12226

11120 = 1.099

A318 A319 A320 A321 A350 A380 747-

400 757-

200 767-

300 777-

200 777-

300 787-8 787-9 787-

10 E170 E190

1

44

67

18

0

12

36

3 8

46

12 9 16

0 6

15

Airbus Boeing Embraer

2) Performance of the British Airways Group is elaborated in terms of the employed Return on

capital, Return on Equity and the Current Ratio (Birchler 2017).

a)

Return on the Employed Capital.

This is a financial ratio that is used in valuation, accounting and financing. It is a measure

necessary for comparing relative profitability of companies after considering the amount of

capital that has been used. It considers debts and other forms of liabilities providing a good

indication of the financial performance for companies with substantial debt. The ROCE helps the

investors to identify the company that utilizes its capital to the maximum for profit generation

(Johan 2018).

Return on the Employed Capital: = Earnings Before Interest∧Taxes

Capital Employed

Capital Employed = Total Assets – Current Liabilities.

= $16678 – $5468 = $11120

= 12226

11120 = 1.099

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

USING INFORMATION 7

Since the British Airways company has a higher Return on the Employed Capital, that is, 1.099,

it is clear that they utilize their finances effectively.

Return on equity ratio is a profitability ratio that shows the amount of profits generated by the

firm and the investments of the shareholders. It acts an indicator of management effectiveness

after using financing equity to fund operations and promote company’s growth. It helps in

tracking the progress of the company and how it maintains a profitable trending rate of what it is

earning and hence keeping it on top of the competition (Ichsani & Suhardi 2015).

Return on Equity: = Net Income

Shareholder s' Equity

Net income = Total Revenue - total expenses.

= $12226 – $4144 = $8082

Since the total revenue exceeds the expenses, after the deductions, the amount obtained is the

profit. This profit is used by the company to pay debts, make payments to the shareholders and

invest more in new equipment.

= 8082

5774 = 1. 400

The Return on equity ratio is higher than the Return on Capital Employed ratio, thus there is a

high utilization of the debts available (Marx, Mojon & Velde 2019).

Current ratio is liquidity ratio that measures the ability of the company to pay for the obligations

that are due within a year. Investors and analysts are able to tell of the maximization strategies

that the company uses on the current assets so as it can cover the current debts. The current ratio

gives the Airways an idea on how it is going to operate and strategic conduction of its activities.

The Airways is able to meet the demands of their creditors.

Current Ratio: = Current Assets

Current Liabilities

= 16678

5468 = 3.050

Since the British Airways company has a higher Return on the Employed Capital, that is, 1.099,

it is clear that they utilize their finances effectively.

Return on equity ratio is a profitability ratio that shows the amount of profits generated by the

firm and the investments of the shareholders. It acts an indicator of management effectiveness

after using financing equity to fund operations and promote company’s growth. It helps in

tracking the progress of the company and how it maintains a profitable trending rate of what it is

earning and hence keeping it on top of the competition (Ichsani & Suhardi 2015).

Return on Equity: = Net Income

Shareholder s' Equity

Net income = Total Revenue - total expenses.

= $12226 – $4144 = $8082

Since the total revenue exceeds the expenses, after the deductions, the amount obtained is the

profit. This profit is used by the company to pay debts, make payments to the shareholders and

invest more in new equipment.

= 8082

5774 = 1. 400

The Return on equity ratio is higher than the Return on Capital Employed ratio, thus there is a

high utilization of the debts available (Marx, Mojon & Velde 2019).

Current ratio is liquidity ratio that measures the ability of the company to pay for the obligations

that are due within a year. Investors and analysts are able to tell of the maximization strategies

that the company uses on the current assets so as it can cover the current debts. The current ratio

gives the Airways an idea on how it is going to operate and strategic conduction of its activities.

The Airways is able to meet the demands of their creditors.

Current Ratio: = Current Assets

Current Liabilities

= 16678

5468 = 3.050

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

USING INFORMATION 8

This ratio suggests that the British Airways company has an efficient management concerning

the capital involved. This is because the ratio is above the standard ratio of 1.5. It also shows that

the company has the ability to pay off its debts and they do not depend on the current assets for

finances.

3) a) Competition- The operative markets involved are highly competitive. British Airways face

competition from the other airlines and indirect flights, charter services and other transport

modes (Pel, Njegovan & Behrens 2017). A few competitors have lower cost structures thus

having a high competitive advantage like government involvement. Instead of comparing the

competitors’ fare with theirs, the discounts being offered to customers affect the Airways

negatively failing to maintain the passengers’ congestion. This risk is easily pointed out due to its

market position, that is globally and their network, alliances and customer diversification

(Borenstein 2017).

b) The conditions of the economy- British Airways revenue is delicate towards the economic

state in the field of operation. Declination in the global economy affects the Airways financial

position. Reviews of the revenue are made by the Revenue Projection Group frequently and the

outcome is later analyzed by the management and effective actions are taken (Shaw 2016).

c) Government intervention- Airline industry regulation policy has increased covering a number

of activities such as rights of flying routes, security controls, airport slot access and

environmental controls. The Airways ability to comply and take in any changes concerning these

regulations maintains the financial and operational performance. Government plan to add

environmental taxes through the introduction of taxation procedure per flight (Jaimovich &

Rebelo 2017). This change benefits even all of their as it reduces the relative cost of doing

business from their necessary hubs (Camilleri 2018).

d) Employee relations- British Airways has a large workforce that is unionized. Joint negotiating

takes place on a regular ordered basis and strategized bargaining process interferes with

operations that highly affects the performance of the business. Airways continued determination

to manage the cost of employment upsurges the risk in terms of employment field.

e) Brand reputation – The Brand of the Airways has an important marketable value. Brand loss

especially through one event or several events may greatly impact the Airways leadership

This ratio suggests that the British Airways company has an efficient management concerning

the capital involved. This is because the ratio is above the standard ratio of 1.5. It also shows that

the company has the ability to pay off its debts and they do not depend on the current assets for

finances.

3) a) Competition- The operative markets involved are highly competitive. British Airways face

competition from the other airlines and indirect flights, charter services and other transport

modes (Pel, Njegovan & Behrens 2017). A few competitors have lower cost structures thus

having a high competitive advantage like government involvement. Instead of comparing the

competitors’ fare with theirs, the discounts being offered to customers affect the Airways

negatively failing to maintain the passengers’ congestion. This risk is easily pointed out due to its

market position, that is globally and their network, alliances and customer diversification

(Borenstein 2017).

b) The conditions of the economy- British Airways revenue is delicate towards the economic

state in the field of operation. Declination in the global economy affects the Airways financial

position. Reviews of the revenue are made by the Revenue Projection Group frequently and the

outcome is later analyzed by the management and effective actions are taken (Shaw 2016).

c) Government intervention- Airline industry regulation policy has increased covering a number

of activities such as rights of flying routes, security controls, airport slot access and

environmental controls. The Airways ability to comply and take in any changes concerning these

regulations maintains the financial and operational performance. Government plan to add

environmental taxes through the introduction of taxation procedure per flight (Jaimovich &

Rebelo 2017). This change benefits even all of their as it reduces the relative cost of doing

business from their necessary hubs (Camilleri 2018).

d) Employee relations- British Airways has a large workforce that is unionized. Joint negotiating

takes place on a regular ordered basis and strategized bargaining process interferes with

operations that highly affects the performance of the business. Airways continued determination

to manage the cost of employment upsurges the risk in terms of employment field.

e) Brand reputation – The Brand of the Airways has an important marketable value. Brand loss

especially through one event or several events may greatly impact the Airways leadership

USING INFORMATION 9

positions. This also influence the customers position and may eventually affect the future of the

revenue generation and the Airways profitability. The top management group frequently

monitors the customers’ fulfillment by conducting a Survey monthly of the Think Customer

globally and checking the advancement made by using the BA product to moderate this Brand

risk (Tsao 2016).

f) Debt funding- Airways carry significant debt that require to be repaid. Their ability to finance

all the operations that are currently working, the committed aircrafts tips and the future growth

plans of the fleet are fragile to factors such as the conditions of the financial market. Most of its

capital commitments are related on the assets and financed early such that there is no assurance

that this Airway will further offer attractive security for their lenders especially in the future. The

Treasury Committee review the financial position whereby the outcomes are tabled and further

discussed to offer the necessary remedies.

g) Price of the fuel and the fluctuation of the currency.

This Airways company uses an estimated amount of tones of the jet fuel per year, that is, about

six million. The price volatility of petroleum products and the oil mostly has a material impact

on their operation process and outcomes. The risk of price is circumvented via the petroleum

products derived and oil purchase in advancing markets that produce a profit or loss. There is

exposure to the current revenue risk, borrowings in the foreign currencies and purchases. The

Group involved helps in seeking the reduced exposure of foreign exchange that arise during

transactions while performing a matching policy that involves receipts and payments made. It

also reduced when selling the excess or buying the downfall of the obligations that comes with

this currency. This exposure tends to reach the group at an extent of non-performing towards the

financial contract that may result into financial loss.

h) Long term network disruptions event- A few events can bring the rise of disruptions that are

long term. This may lead to revenue loss and additional of extra costs. Management plans on

how to deal with the risks to a point they are easy to handle or feasible.

i) Consolidation or deregulation – With the airways competitive market, there is need for

rationality with the given conditions of the market. Rationalizing takes in airways future failures

and consolidation, Acquiring and merging among its competitors creating chance for the

positions. This also influence the customers position and may eventually affect the future of the

revenue generation and the Airways profitability. The top management group frequently

monitors the customers’ fulfillment by conducting a Survey monthly of the Think Customer

globally and checking the advancement made by using the BA product to moderate this Brand

risk (Tsao 2016).

f) Debt funding- Airways carry significant debt that require to be repaid. Their ability to finance

all the operations that are currently working, the committed aircrafts tips and the future growth

plans of the fleet are fragile to factors such as the conditions of the financial market. Most of its

capital commitments are related on the assets and financed early such that there is no assurance

that this Airway will further offer attractive security for their lenders especially in the future. The

Treasury Committee review the financial position whereby the outcomes are tabled and further

discussed to offer the necessary remedies.

g) Price of the fuel and the fluctuation of the currency.

This Airways company uses an estimated amount of tones of the jet fuel per year, that is, about

six million. The price volatility of petroleum products and the oil mostly has a material impact

on their operation process and outcomes. The risk of price is circumvented via the petroleum

products derived and oil purchase in advancing markets that produce a profit or loss. There is

exposure to the current revenue risk, borrowings in the foreign currencies and purchases. The

Group involved helps in seeking the reduced exposure of foreign exchange that arise during

transactions while performing a matching policy that involves receipts and payments made. It

also reduced when selling the excess or buying the downfall of the obligations that comes with

this currency. This exposure tends to reach the group at an extent of non-performing towards the

financial contract that may result into financial loss.

h) Long term network disruptions event- A few events can bring the rise of disruptions that are

long term. This may lead to revenue loss and additional of extra costs. Management plans on

how to deal with the risks to a point they are easy to handle or feasible.

i) Consolidation or deregulation – With the airways competitive market, there is need for

rationality with the given conditions of the market. Rationalizing takes in airways future failures

and consolidation, Acquiring and merging among its competitors creating chance for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

USING INFORMATION 10

potential of the market revenue and position being affected. Iberia mergers and American airlines

with joint Business Agreement introduces risks of planning, that is, set up processes, design that

is sub optimal delivery risks like planned benefits realization. This risks are addressed by the

management. Operative markets are always regulated by the government to control or resist the

entry of the market. Once there is a no consistent regulation, growth opportunities that may bear

negative influence on the Airways margin can chip in (Wong 2018).

j) Safety and security incidents – This is a concern that need attention especially that of the

customers and the airways staff members. Failure for the airways management to being

responsive to these incidents may reduce their operation, financial and performance rate. Once

operations have been controlled by the Operations Control Incident Centre, a structured strategy

is adopted to deal with these incidents.

4) The British airways has been increasing in terms of it production. From the chart below, it is

clear that the revenues of the company are steadily going up year after year. There has been a

noticeable increase in revenue from the year 2013 to the year 2014. In 2013 the British airways

company made a revenue of eleven thousand four hundred and twenty-one British pounds which

was increased to eleven thousand seven hundred and nineteen British pounds in the following

year. The revenue went down to eleven thousand one hundred and eleven in the year 2015 but

again raised in 2016 up to eleven thousand three hundred and ninety-eight. These two

consecutive years were associated with poor performance. Although 2016 can be considered

better that the previous year, since the revenue went up even though by a small percentage.

Further analysis of the chart shows that; the revenue went up dramatically in the year 2017. This

year recorded the highest revenues which was twelve thousand two hundred and twenty-six. The

deviation of the revenue is varying from year to year. However, it cannot be considered as an

average deviation since, in 2015 was rather drastic. Generally, the company has been on the

watch out for strategies that ensure its continuous growth over the five years.

potential of the market revenue and position being affected. Iberia mergers and American airlines

with joint Business Agreement introduces risks of planning, that is, set up processes, design that

is sub optimal delivery risks like planned benefits realization. This risks are addressed by the

management. Operative markets are always regulated by the government to control or resist the

entry of the market. Once there is a no consistent regulation, growth opportunities that may bear

negative influence on the Airways margin can chip in (Wong 2018).

j) Safety and security incidents – This is a concern that need attention especially that of the

customers and the airways staff members. Failure for the airways management to being

responsive to these incidents may reduce their operation, financial and performance rate. Once

operations have been controlled by the Operations Control Incident Centre, a structured strategy

is adopted to deal with these incidents.

4) The British airways has been increasing in terms of it production. From the chart below, it is

clear that the revenues of the company are steadily going up year after year. There has been a

noticeable increase in revenue from the year 2013 to the year 2014. In 2013 the British airways

company made a revenue of eleven thousand four hundred and twenty-one British pounds which

was increased to eleven thousand seven hundred and nineteen British pounds in the following

year. The revenue went down to eleven thousand one hundred and eleven in the year 2015 but

again raised in 2016 up to eleven thousand three hundred and ninety-eight. These two

consecutive years were associated with poor performance. Although 2016 can be considered

better that the previous year, since the revenue went up even though by a small percentage.

Further analysis of the chart shows that; the revenue went up dramatically in the year 2017. This

year recorded the highest revenues which was twelve thousand two hundred and twenty-six. The

deviation of the revenue is varying from year to year. However, it cannot be considered as an

average deviation since, in 2015 was rather drastic. Generally, the company has been on the

watch out for strategies that ensure its continuous growth over the five years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

USING INFORMATION 11

References

Adeneye, Y.B. and Ahmed, M., 2015. Corporate social responsibility and company

performance. Journal of Business Studies Quarterly, 7(1), p.151.

Birchler, U., 2017. The Return on Equity. In Economic Ideas You Should Forget (pp. 23-25).

Springer, Cham.

Borenstein, S., 2017. The evolution of US airline competition. In Low Cost Carriers (pp. 1-31).

Routledge.

Camilleri, M.A., 2018. The marketing environment. In Travel Marketing, Tourism Economics

and the Airline Product (pp. 51-68). Springer, Cham.

Crowder, M.J., 2017. Statistical analysis of reliability data. Routledge.

De Mauro, A., Greco, M. and Grimaldi, M., 2015, February. What is big data? A consensual

definition and a review of key research topics. In AIP conference proceedings (Vol. 1644, No. 1,

pp. 97-104). AIP.

De Mauro, A., Greco, M. and Grimaldi, M., 2016. A formal definition of Big Data based on its

essential features. Library Review, 65(3), pp.122-135.

Enyi, E.P., 2019. Relational Trend Analysis: A Simple and Effective Way to Detect Financial

Statements Fraud. Enyi, E. P,(2019). Relational Trend Analysis: A simple and effective way to

detect financial statements fraud, International Journal of Scientific and Research

Publications, 9(2), pp.538-546.

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements. Pearson.

Goertzen, M.J., 2017. . Introduction to Quantitative Research and Data. Library Technology

Reports, 53(4), pp.12-18.

Hurst, M., Relander, C. and Cordes, S., 2016. Biases and Benefits of Number Lines and Pie

Charts in Proportion Representation. In CogSci.

References

Adeneye, Y.B. and Ahmed, M., 2015. Corporate social responsibility and company

performance. Journal of Business Studies Quarterly, 7(1), p.151.

Birchler, U., 2017. The Return on Equity. In Economic Ideas You Should Forget (pp. 23-25).

Springer, Cham.

Borenstein, S., 2017. The evolution of US airline competition. In Low Cost Carriers (pp. 1-31).

Routledge.

Camilleri, M.A., 2018. The marketing environment. In Travel Marketing, Tourism Economics

and the Airline Product (pp. 51-68). Springer, Cham.

Crowder, M.J., 2017. Statistical analysis of reliability data. Routledge.

De Mauro, A., Greco, M. and Grimaldi, M., 2015, February. What is big data? A consensual

definition and a review of key research topics. In AIP conference proceedings (Vol. 1644, No. 1,

pp. 97-104). AIP.

De Mauro, A., Greco, M. and Grimaldi, M., 2016. A formal definition of Big Data based on its

essential features. Library Review, 65(3), pp.122-135.

Enyi, E.P., 2019. Relational Trend Analysis: A Simple and Effective Way to Detect Financial

Statements Fraud. Enyi, E. P,(2019). Relational Trend Analysis: A simple and effective way to

detect financial statements fraud, International Journal of Scientific and Research

Publications, 9(2), pp.538-546.

Fraser, L.M., Ormiston, A. and Fraser, L.M., 2010. Understanding financial statements. Pearson.

Goertzen, M.J., 2017. . Introduction to Quantitative Research and Data. Library Technology

Reports, 53(4), pp.12-18.

Hurst, M., Relander, C. and Cordes, S., 2016. Biases and Benefits of Number Lines and Pie

Charts in Proportion Representation. In CogSci.

USING INFORMATION 12

Ichsani, S. and Suhardi, A.R., 2015. The effect of return on equity (ROE) and return on

investment (ROI) on trading volume. Procedia-Social and Behavioral Sciences, 211, pp.896-

902.

Jaimovich, N. and Rebelo, S., 2017. Nonlinear effects of taxation on growth. Journal of Political

Economy, 125(1), pp.265-291.

Johan, S., 2018. The Relationship Between Economic Value Added, Market Value Added And

Return On Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan

Kewirausahaan, 2(1).

Madar, A., 2015. Implementation of total quality management Case study: British

Airways. Bulletin of the Transilvania University of Brasov. Series V: Economic Sciences, 8(1).

Marx, M., Mojon, B. and Velde, F.R., 2019. Why have interest rates fallen far below the return

on capital.

Mertens, W., Pugliese, A. and Recker, J., 2017. Quantitative data analysis. A companion.

Mihas, P., 2019. Qualitative data analysis. In Oxford Research Encyclopedia of Education.

Pels, E., Njegovan, N. and Behrens, C., 2017. Low-cost airlines and airport competition. In Low

Cost Carriers (pp. 125-136). Routledge.

Petrescu, R.V., Aversa, R., Akash, B., Corchado, J., Berto, F., Apicella, A. and Petrescu, F.I.,

2017. When boeing is dreaming–a review. Journal of Aircraft and Spacecraft Technology, 1(3).

Shaw, S., 2016. Airline marketing and management. Routledge.

Tsao, Y.C., 2016. Pricing and ordering under trade promotion, brand competition, and demand

uncertainty. Scientia Iranica, 23(5), pp.2407-2415.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Wong, W.K., 2018. Can we afford a defined benefit pension (No. E2018/22). Cardiff University,

Cardiff Business School, Economics Section.

Ichsani, S. and Suhardi, A.R., 2015. The effect of return on equity (ROE) and return on

investment (ROI) on trading volume. Procedia-Social and Behavioral Sciences, 211, pp.896-

902.

Jaimovich, N. and Rebelo, S., 2017. Nonlinear effects of taxation on growth. Journal of Political

Economy, 125(1), pp.265-291.

Johan, S., 2018. The Relationship Between Economic Value Added, Market Value Added And

Return On Cost Of Capital In Measuring Corporate Performance. Jurnal Manajemen Bisnis dan

Kewirausahaan, 2(1).

Madar, A., 2015. Implementation of total quality management Case study: British

Airways. Bulletin of the Transilvania University of Brasov. Series V: Economic Sciences, 8(1).

Marx, M., Mojon, B. and Velde, F.R., 2019. Why have interest rates fallen far below the return

on capital.

Mertens, W., Pugliese, A. and Recker, J., 2017. Quantitative data analysis. A companion.

Mihas, P., 2019. Qualitative data analysis. In Oxford Research Encyclopedia of Education.

Pels, E., Njegovan, N. and Behrens, C., 2017. Low-cost airlines and airport competition. In Low

Cost Carriers (pp. 125-136). Routledge.

Petrescu, R.V., Aversa, R., Akash, B., Corchado, J., Berto, F., Apicella, A. and Petrescu, F.I.,

2017. When boeing is dreaming–a review. Journal of Aircraft and Spacecraft Technology, 1(3).

Shaw, S., 2016. Airline marketing and management. Routledge.

Tsao, Y.C., 2016. Pricing and ordering under trade promotion, brand competition, and demand

uncertainty. Scientia Iranica, 23(5), pp.2407-2415.

Williams, E.E. and Dobelman, J.A., 2017. Financial statement analysis. World Scientific Book

Chapters, pp.109-169.

Wong, W.K., 2018. Can we afford a defined benefit pension (No. E2018/22). Cardiff University,

Cardiff Business School, Economics Section.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.