Financial Reporting: British Airways and KLM During Financial Crisis

VerifiedAdded on 2023/04/20

|43

|8493

|72

Report

AI Summary

This report evaluates the financial performance and risk position of British Airways and KLM Royal Dutch Airlines during a period marked by financial crises. It employs financial ratio analysis over five years, comparing the companies' performance against industry averages. The analysis covers profitability ratios (Return on Assets, Return on Equity, Return on Capital Employed, Gross Profit Margin, Net Profit Margin), liquidity ratios (Current Ratio, Quick Ratio), industry-specific ratios (Available Seat Kilometers, Revenue Passenger Kilometers, Passenger Load Factor), asset efficiency ratios (Average Inventories Turnover Period, Average Settlement Period for Receivables/Payables), gearing ratios (Debt to Capital Ratio, Interest Cover Ratio), and investment ratios (Earnings per Share, Price/Earnings Ratio, Dividend Payout Ratio, Dividend Cover Ratio). Additionally, cash flow analysis is performed, examining operating cash flow relative to sales and investments. The report aims to provide insights into the strategies used by British Airways and KLM to sustain profitability during challenging economic times.

1

Financial reporting assignment

Financial reporting assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The period of financial crises has impacted most of the businesses worldwide and

cause the need for developing the business strategies that help them to sustain the robust

profitability during the period of crises. The civil aviation market is most important as it is

the prime movers in the economic growth and the strategic element for employment

generation. Aim of this report is to evaluate the case of British Airways and KLM Royal

Dutch Airlines in order to report on the financial performance and risk position of these

companies. Financial analysis through use of ratio analysis has been carried out for both the

companies for last two years and it has also been compared with industry average.

Executive Summary

The period of financial crises has impacted most of the businesses worldwide and

cause the need for developing the business strategies that help them to sustain the robust

profitability during the period of crises. The civil aviation market is most important as it is

the prime movers in the economic growth and the strategic element for employment

generation. Aim of this report is to evaluate the case of British Airways and KLM Royal

Dutch Airlines in order to report on the financial performance and risk position of these

companies. Financial analysis through use of ratio analysis has been carried out for both the

companies for last two years and it has also been compared with industry average.

3

Contents

Executive Summary...................................................................................................................2

Part 1: Introduction....................................................................................................................4

Case of British Airways..........................................................................................................4

Case of KLM Royal Dutch Airlines.......................................................................................5

Part 2: Analysis of financial statements for last 5 years............................................................5

Financial Ratio analysis – Comparison of the two companies and industry..........................5

2.1: Profitability Ratios..............................................................................................................5

2.1.1: Return on assets............................................................................................................5

2.1.2: Return on Equity (ROE)...............................................................................................6

2.1.3: Return on Capital Employed (ROCE)..........................................................................7

2.1.4: Gross Profit Margin......................................................................................................9

2.1.5: Net profit Margin........................................................................................................10

2.2: Liquidity Ratios.................................................................................................................11

2.2.1: Current ratio...............................................................................................................11

2.2.2: Quick Ratio.................................................................................................................12

2.3: Industry Ratio....................................................................................................................13

2.3.1: Available seat kilometers (ASK)................................................................................13

2.3.2: Revenue passenger kilometers (RPK)........................................................................14

2.3.3: Passenger load factor..................................................................................................15

2.4: Asset efficiency Ratios......................................................................................................16

2.4.1: Average inventories turnover period..........................................................................16

2.4.2: Average settlement period for receivables.................................................................17

2.4.3: Average settlement period for payables.....................................................................18

2.5: Gearing Ratio....................................................................................................................19

2.5.1: Debt to capital ratio....................................................................................................19

2.5.2: Interest cover ratio......................................................................................................20

2.6. Investment ratios...............................................................................................................21

2.6.1: Earnings per Share......................................................................................................21

2.6.2: Price/Earnings ratio....................................................................................................23

2.6.3: Dividend payout ratio.................................................................................................24

2.6.4: Dividend cover ratio...................................................................................................25

Contents

Executive Summary...................................................................................................................2

Part 1: Introduction....................................................................................................................4

Case of British Airways..........................................................................................................4

Case of KLM Royal Dutch Airlines.......................................................................................5

Part 2: Analysis of financial statements for last 5 years............................................................5

Financial Ratio analysis – Comparison of the two companies and industry..........................5

2.1: Profitability Ratios..............................................................................................................5

2.1.1: Return on assets............................................................................................................5

2.1.2: Return on Equity (ROE)...............................................................................................6

2.1.3: Return on Capital Employed (ROCE)..........................................................................7

2.1.4: Gross Profit Margin......................................................................................................9

2.1.5: Net profit Margin........................................................................................................10

2.2: Liquidity Ratios.................................................................................................................11

2.2.1: Current ratio...............................................................................................................11

2.2.2: Quick Ratio.................................................................................................................12

2.3: Industry Ratio....................................................................................................................13

2.3.1: Available seat kilometers (ASK)................................................................................13

2.3.2: Revenue passenger kilometers (RPK)........................................................................14

2.3.3: Passenger load factor..................................................................................................15

2.4: Asset efficiency Ratios......................................................................................................16

2.4.1: Average inventories turnover period..........................................................................16

2.4.2: Average settlement period for receivables.................................................................17

2.4.3: Average settlement period for payables.....................................................................18

2.5: Gearing Ratio....................................................................................................................19

2.5.1: Debt to capital ratio....................................................................................................19

2.5.2: Interest cover ratio......................................................................................................20

2.6. Investment ratios...............................................................................................................21

2.6.1: Earnings per Share......................................................................................................21

2.6.2: Price/Earnings ratio....................................................................................................23

2.6.3: Dividend payout ratio.................................................................................................24

2.6.4: Dividend cover ratio...................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

3. Cash-Flow Analysis.............................................................................................................26

3.1: Operating Cash-Flow / Sales.........................................................................................26

3.2: CF from borrowings / Sales...........................................................................................27

3.3: Operating CF after tax/ (Fixed assets investment +Dividends)....................................28

Part 4: Recommendations........................................................................................................29

Part 5: Conclusion....................................................................................................................29

Part 6: References....................................................................................................................30

Appendixes...............................................................................................................................32

3. Cash-Flow Analysis.............................................................................................................26

3.1: Operating Cash-Flow / Sales.........................................................................................26

3.2: CF from borrowings / Sales...........................................................................................27

3.3: Operating CF after tax/ (Fixed assets investment +Dividends)....................................28

Part 4: Recommendations........................................................................................................29

Part 5: Conclusion....................................................................................................................29

Part 6: References....................................................................................................................30

Appendixes...............................................................................................................................32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Part 1: Introduction

The global financial crises of year 2008 and 2009 have emerged because of the failure

of some of major financial banks and institutions and it has impacted the world economy.

United Kingdom and Europe aviation sector is the most important part of world economy and

it also impacted heavily. Some of financial implication of global financial crises on aviation

sector of United Kingdom and Europe are negative growth rate, high operating cost and huge

debt. The two most valuable companies of the aviation sector of Europe and UK that have

been worst affected are British Airways (BA) and KLM Royal Dutch Airlines (KLM).

The main purpose of this report is to evaluate the case of British Airways and KLM

Royal Dutch Airlines in order to report on the financial performance and risk position of

these companies. Financial performance and risk position has been evaluated through use of

financial ratios and through using the information provided in the annual report. In this

regards financial ratios of last 5 years has been calculated for both the companies and they

have been compared with industry average in order to evaluate their business strategies

during the period of financial crises. During the financial crises period both companies have

make use of management accounting concepts and techniques such as value for money

concept, drive to reduce cost, technological innovation and other techniques to survive the

period of financial crises and to stand for future possibilities. In regards to this, report aims to

explore the potential of strategic management accounting and costing concepts and

techniques that both companies used for survival during the financial crises period and to

make strong base for future in order have comparison with similar companies.

Case of British Airways

The business of British Airways is largely impacted due to the period of global

recession due to occurrence of financial crisis in the year 2007. The sales and profit margins

of the company have depicted a major decline during the financial crisis period. It was unable

to pay nay dividend to its shareholders largely due to its negative profitability position and

operating at loss. The airline was able to overcome from the negative impact of the economic

recession by continued reinvestment in its profits and focusing on long-term growth. This is

largely on account of large-scale investment in launching crisis programs for reducing its

operational costs and aiding quick financial recovery for the company (Hunter, 2019). The

use of effective cost management strategies by the airline has enabled it to reduce its

Part 1: Introduction

The global financial crises of year 2008 and 2009 have emerged because of the failure

of some of major financial banks and institutions and it has impacted the world economy.

United Kingdom and Europe aviation sector is the most important part of world economy and

it also impacted heavily. Some of financial implication of global financial crises on aviation

sector of United Kingdom and Europe are negative growth rate, high operating cost and huge

debt. The two most valuable companies of the aviation sector of Europe and UK that have

been worst affected are British Airways (BA) and KLM Royal Dutch Airlines (KLM).

The main purpose of this report is to evaluate the case of British Airways and KLM

Royal Dutch Airlines in order to report on the financial performance and risk position of

these companies. Financial performance and risk position has been evaluated through use of

financial ratios and through using the information provided in the annual report. In this

regards financial ratios of last 5 years has been calculated for both the companies and they

have been compared with industry average in order to evaluate their business strategies

during the period of financial crises. During the financial crises period both companies have

make use of management accounting concepts and techniques such as value for money

concept, drive to reduce cost, technological innovation and other techniques to survive the

period of financial crises and to stand for future possibilities. In regards to this, report aims to

explore the potential of strategic management accounting and costing concepts and

techniques that both companies used for survival during the financial crises period and to

make strong base for future in order have comparison with similar companies.

Case of British Airways

The business of British Airways is largely impacted due to the period of global

recession due to occurrence of financial crisis in the year 2007. The sales and profit margins

of the company have depicted a major decline during the financial crisis period. It was unable

to pay nay dividend to its shareholders largely due to its negative profitability position and

operating at loss. The airline was able to overcome from the negative impact of the economic

recession by continued reinvestment in its profits and focusing on long-term growth. This is

largely on account of large-scale investment in launching crisis programs for reducing its

operational costs and aiding quick financial recovery for the company (Hunter, 2019). The

use of effective cost management strategies by the airline has enabled it to reduce its

6

operating costs and thus it was able to improve its profitability position and improve the

market share in the highly competitive airline industry.

Case of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines has also effectively responded to the global recession by

the use of adequate cost management strategies. The company operating efficacy has been

largely negatively impacted by the impact of the downturn in the global economy due to the

occurrence of global financial crisis in the year 2007. The reduction in the operating costs has

enabled the company to overcome the decline in its revenue that has occurred mainly due to

the significant impact of the global financial crisis. The airline is also striving to preserve

cash by delaying the investment in the new aircraft and minimizing its capital expenditure.

This is largely done from the perspective of reserving cash and reinvesting in profit for

promoting long-term growth of the company (Done, 2009).

Part 2: Analysis of financial statements for last 5 years

Financial Ratio analysis – Comparison of the two companies and industry

In this section of the report financial analysis of British Airways (BA) and KLM

Royal Dutch Airlines (KLM) has been examined through use of ratio analysis and

comparison has also been made to investigate company’s performance with respect to

industry. The analysis of both the companies have been evaluated from the annual report of

the financial year 2013, 2014, 2015, 2016 and 2017. Financial ratios are the key tools which

is implemented in order to understand the overall financial strength of the company.

Comparison based on the last five years of both the company gives far better picture of the

financial position as a whole.

2.1: Profitability Ratios

Profitability ratios refers to class of financial metrics that is used to evaluate ability of

entity to generate the earnings in relation to some metrics such as sales, capital employed,

assets and equity. These ratios are important from the point of view of investors as well as

from the point of management because it helps with company profitability position during the

relative year (Brigham and Michael, 2013). This ratio helps to measure the effectiveness in

generating the return for both the company for the last five years.

operating costs and thus it was able to improve its profitability position and improve the

market share in the highly competitive airline industry.

Case of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines has also effectively responded to the global recession by

the use of adequate cost management strategies. The company operating efficacy has been

largely negatively impacted by the impact of the downturn in the global economy due to the

occurrence of global financial crisis in the year 2007. The reduction in the operating costs has

enabled the company to overcome the decline in its revenue that has occurred mainly due to

the significant impact of the global financial crisis. The airline is also striving to preserve

cash by delaying the investment in the new aircraft and minimizing its capital expenditure.

This is largely done from the perspective of reserving cash and reinvesting in profit for

promoting long-term growth of the company (Done, 2009).

Part 2: Analysis of financial statements for last 5 years

Financial Ratio analysis – Comparison of the two companies and industry

In this section of the report financial analysis of British Airways (BA) and KLM

Royal Dutch Airlines (KLM) has been examined through use of ratio analysis and

comparison has also been made to investigate company’s performance with respect to

industry. The analysis of both the companies have been evaluated from the annual report of

the financial year 2013, 2014, 2015, 2016 and 2017. Financial ratios are the key tools which

is implemented in order to understand the overall financial strength of the company.

Comparison based on the last five years of both the company gives far better picture of the

financial position as a whole.

2.1: Profitability Ratios

Profitability ratios refers to class of financial metrics that is used to evaluate ability of

entity to generate the earnings in relation to some metrics such as sales, capital employed,

assets and equity. These ratios are important from the point of view of investors as well as

from the point of management because it helps with company profitability position during the

relative year (Brigham and Michael, 2013). This ratio helps to measure the effectiveness in

generating the return for both the company for the last five years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

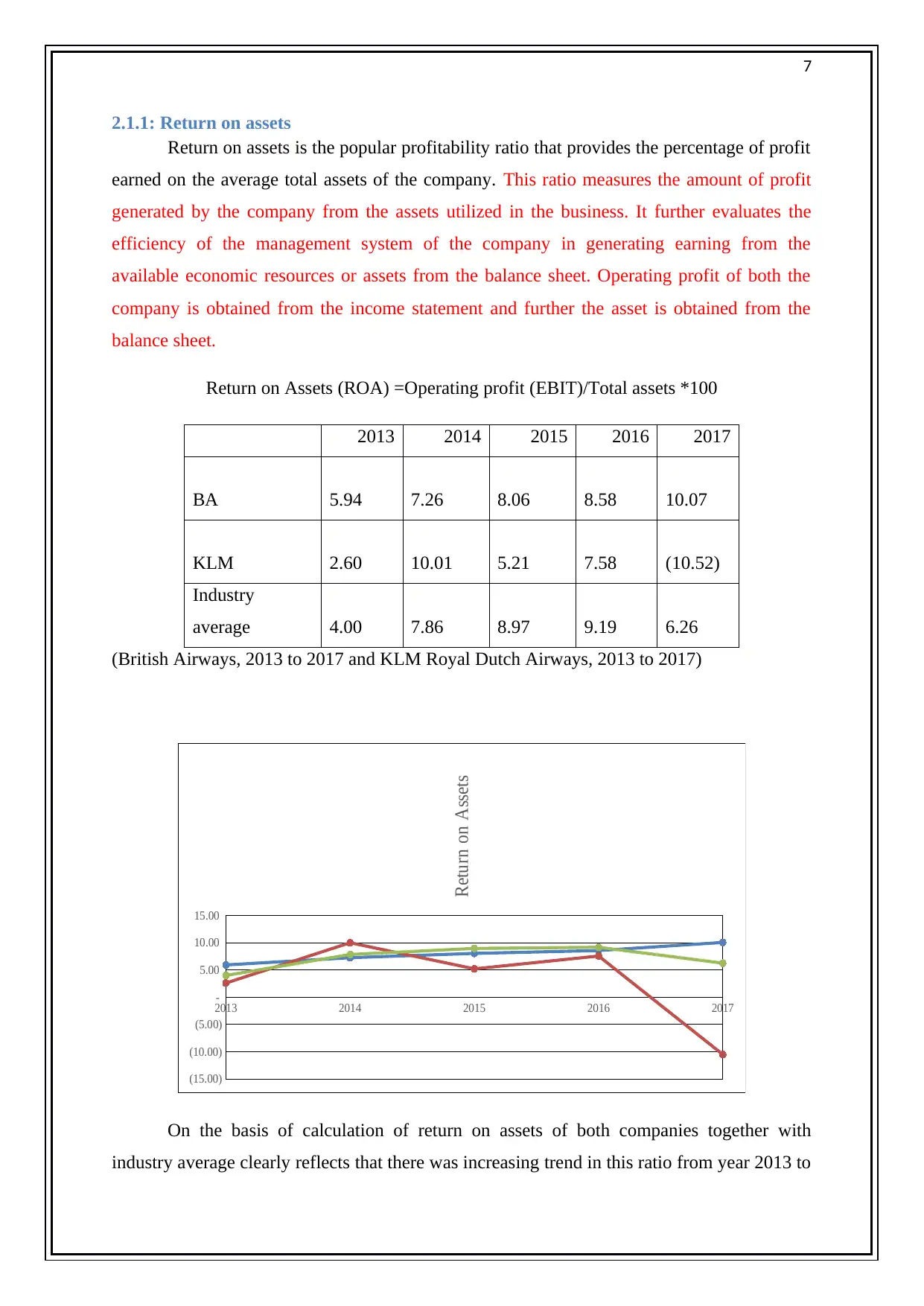

2.1.1: Return on assets

Return on assets is the popular profitability ratio that provides the percentage of profit

earned on the average total assets of the company. This ratio measures the amount of profit

generated by the company from the assets utilized in the business. It further evaluates the

efficiency of the management system of the company in generating earning from the

available economic resources or assets from the balance sheet. Operating profit of both the

company is obtained from the income statement and further the asset is obtained from the

balance sheet.

Return on Assets (ROA) =Operating profit (EBIT)/Total assets *100

2013 2014 2015 2016 2017

BA 5.94 7.26 8.06 8.58 10.07

KLM 2.60 10.01 5.21 7.58 (10.52)

Industry

average 4.00 7.86 8.97 9.19 6.26

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

Return on Assets

On the basis of calculation of return on assets of both companies together with

industry average clearly reflects that there was increasing trend in this ratio from year 2013 to

2.1.1: Return on assets

Return on assets is the popular profitability ratio that provides the percentage of profit

earned on the average total assets of the company. This ratio measures the amount of profit

generated by the company from the assets utilized in the business. It further evaluates the

efficiency of the management system of the company in generating earning from the

available economic resources or assets from the balance sheet. Operating profit of both the

company is obtained from the income statement and further the asset is obtained from the

balance sheet.

Return on Assets (ROA) =Operating profit (EBIT)/Total assets *100

2013 2014 2015 2016 2017

BA 5.94 7.26 8.06 8.58 10.07

KLM 2.60 10.01 5.21 7.58 (10.52)

Industry

average 4.00 7.86 8.97 9.19 6.26

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

Return on Assets

On the basis of calculation of return on assets of both companies together with

industry average clearly reflects that there was increasing trend in this ratio from year 2013 to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

2017. Return on assets ratio of BA from year 2013 to 2017 have increased each year from

5.94% in year 2013 to 10.07% in year 2017. It means BA has used assets more precisely as

compared to KLM. The return on assets ratio of KLM was above industry average during the

last five years and on the other hand, return on asset of KLM was below industry average. So,

BA has provided better return on assets as compared to KLM in all the five years under

review.

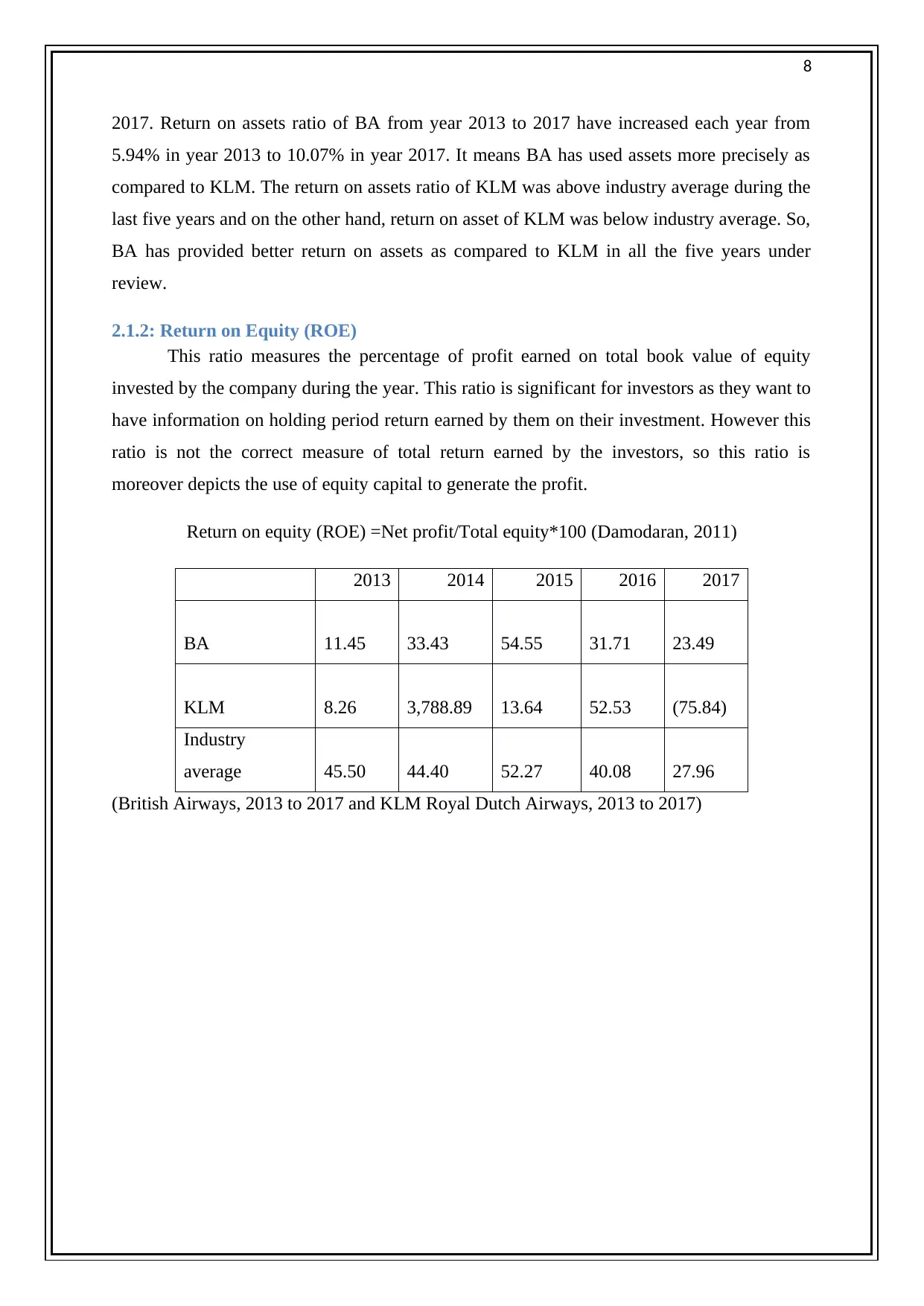

2.1.2: Return on Equity (ROE)

This ratio measures the percentage of profit earned on total book value of equity

invested by the company during the year. This ratio is significant for investors as they want to

have information on holding period return earned by them on their investment. However this

ratio is not the correct measure of total return earned by the investors, so this ratio is

moreover depicts the use of equity capital to generate the profit.

Return on equity (ROE) =Net profit/Total equity*100 (Damodaran, 2011)

2013 2014 2015 2016 2017

BA 11.45 33.43 54.55 31.71 23.49

KLM 8.26 3,788.89 13.64 52.53 (75.84)

Industry

average 45.50 44.40 52.27 40.08 27.96

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2017. Return on assets ratio of BA from year 2013 to 2017 have increased each year from

5.94% in year 2013 to 10.07% in year 2017. It means BA has used assets more precisely as

compared to KLM. The return on assets ratio of KLM was above industry average during the

last five years and on the other hand, return on asset of KLM was below industry average. So,

BA has provided better return on assets as compared to KLM in all the five years under

review.

2.1.2: Return on Equity (ROE)

This ratio measures the percentage of profit earned on total book value of equity

invested by the company during the year. This ratio is significant for investors as they want to

have information on holding period return earned by them on their investment. However this

ratio is not the correct measure of total return earned by the investors, so this ratio is

moreover depicts the use of equity capital to generate the profit.

Return on equity (ROE) =Net profit/Total equity*100 (Damodaran, 2011)

2013 2014 2015 2016 2017

BA 11.45 33.43 54.55 31.71 23.49

KLM 8.26 3,788.89 13.64 52.53 (75.84)

Industry

average 45.50 44.40 52.27 40.08 27.96

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

9

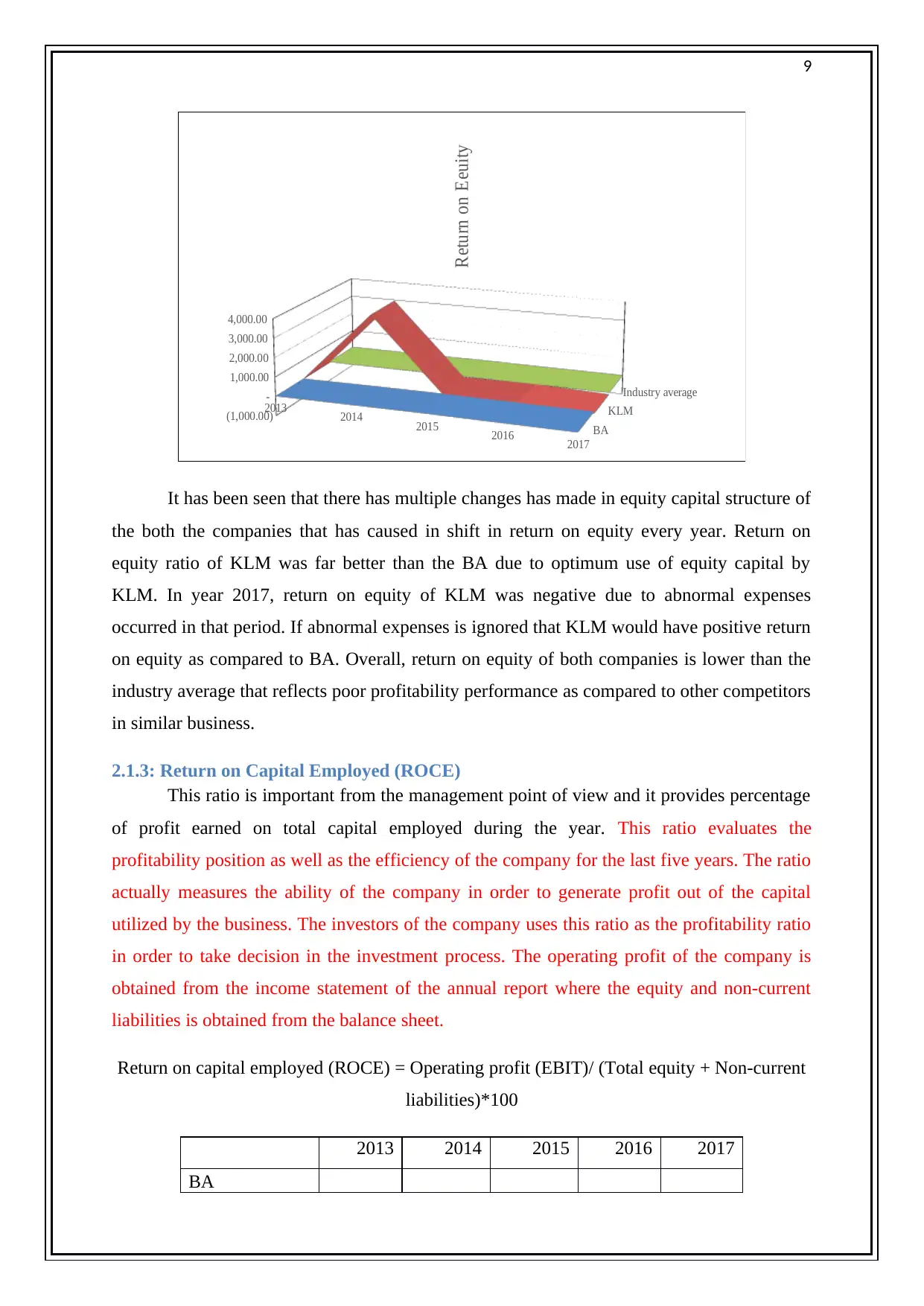

2013 2014 2015 2016 2017

(1,000.00)

-

1,000.00

2,000.00

3,000.00

4,000.00

BA

KLM

Industry average

Return on Eeuity

It has been seen that there has multiple changes has made in equity capital structure of

the both the companies that has caused in shift in return on equity every year. Return on

equity ratio of KLM was far better than the BA due to optimum use of equity capital by

KLM. In year 2017, return on equity of KLM was negative due to abnormal expenses

occurred in that period. If abnormal expenses is ignored that KLM would have positive return

on equity as compared to BA. Overall, return on equity of both companies is lower than the

industry average that reflects poor profitability performance as compared to other competitors

in similar business.

2.1.3: Return on Capital Employed (ROCE)

This ratio is important from the management point of view and it provides percentage

of profit earned on total capital employed during the year. This ratio evaluates the

profitability position as well as the efficiency of the company for the last five years. The ratio

actually measures the ability of the company in order to generate profit out of the capital

utilized by the business. The investors of the company uses this ratio as the profitability ratio

in order to take decision in the investment process. The operating profit of the company is

obtained from the income statement of the annual report where the equity and non-current

liabilities is obtained from the balance sheet.

Return on capital employed (ROCE) = Operating profit (EBIT)/ (Total equity + Non-current

liabilities)*100

2013 2014 2015 2016 2017

BA

2013 2014 2015 2016 2017

(1,000.00)

-

1,000.00

2,000.00

3,000.00

4,000.00

BA

KLM

Industry average

Return on Eeuity

It has been seen that there has multiple changes has made in equity capital structure of

the both the companies that has caused in shift in return on equity every year. Return on

equity ratio of KLM was far better than the BA due to optimum use of equity capital by

KLM. In year 2017, return on equity of KLM was negative due to abnormal expenses

occurred in that period. If abnormal expenses is ignored that KLM would have positive return

on equity as compared to BA. Overall, return on equity of both companies is lower than the

industry average that reflects poor profitability performance as compared to other competitors

in similar business.

2.1.3: Return on Capital Employed (ROCE)

This ratio is important from the management point of view and it provides percentage

of profit earned on total capital employed during the year. This ratio evaluates the

profitability position as well as the efficiency of the company for the last five years. The ratio

actually measures the ability of the company in order to generate profit out of the capital

utilized by the business. The investors of the company uses this ratio as the profitability ratio

in order to take decision in the investment process. The operating profit of the company is

obtained from the income statement of the annual report where the equity and non-current

liabilities is obtained from the balance sheet.

Return on capital employed (ROCE) = Operating profit (EBIT)/ (Total equity + Non-current

liabilities)*100

2013 2014 2015 2016 2017

BA

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

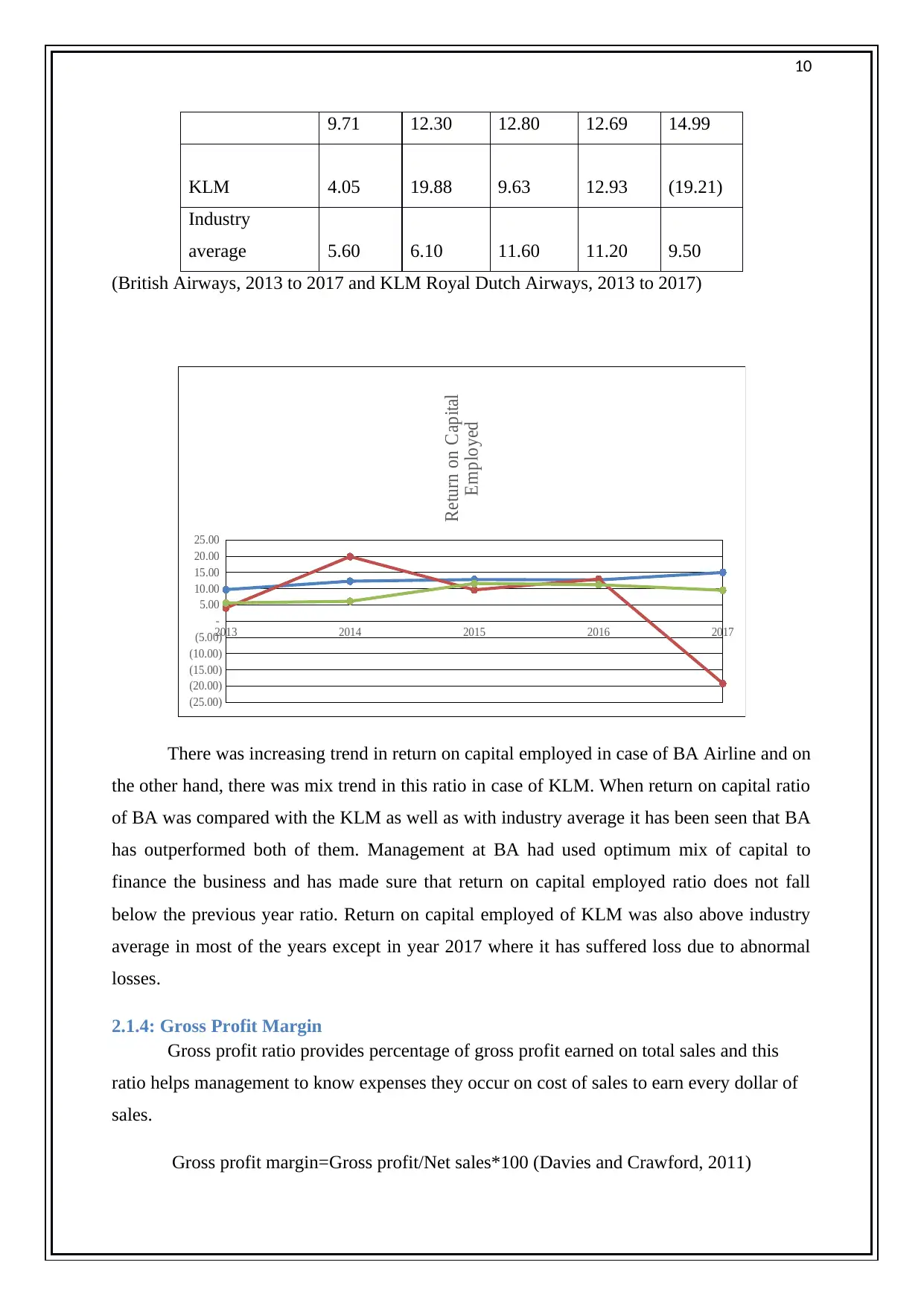

9.71 12.30 12.80 12.69 14.99

KLM 4.05 19.88 9.63 12.93 (19.21)

Industry

average 5.60 6.10 11.60 11.20 9.50

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(25.00)

(20.00)

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

25.00

Return on Capital

Employed

There was increasing trend in return on capital employed in case of BA Airline and on

the other hand, there was mix trend in this ratio in case of KLM. When return on capital ratio

of BA was compared with the KLM as well as with industry average it has been seen that BA

has outperformed both of them. Management at BA had used optimum mix of capital to

finance the business and has made sure that return on capital employed ratio does not fall

below the previous year ratio. Return on capital employed of KLM was also above industry

average in most of the years except in year 2017 where it has suffered loss due to abnormal

losses.

2.1.4: Gross Profit Margin

Gross profit ratio provides percentage of gross profit earned on total sales and this

ratio helps management to know expenses they occur on cost of sales to earn every dollar of

sales.

Gross profit margin=Gross profit/Net sales*100 (Davies and Crawford, 2011)

9.71 12.30 12.80 12.69 14.99

KLM 4.05 19.88 9.63 12.93 (19.21)

Industry

average 5.60 6.10 11.60 11.20 9.50

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(25.00)

(20.00)

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

25.00

Return on Capital

Employed

There was increasing trend in return on capital employed in case of BA Airline and on

the other hand, there was mix trend in this ratio in case of KLM. When return on capital ratio

of BA was compared with the KLM as well as with industry average it has been seen that BA

has outperformed both of them. Management at BA had used optimum mix of capital to

finance the business and has made sure that return on capital employed ratio does not fall

below the previous year ratio. Return on capital employed of KLM was also above industry

average in most of the years except in year 2017 where it has suffered loss due to abnormal

losses.

2.1.4: Gross Profit Margin

Gross profit ratio provides percentage of gross profit earned on total sales and this

ratio helps management to know expenses they occur on cost of sales to earn every dollar of

sales.

Gross profit margin=Gross profit/Net sales*100 (Davies and Crawford, 2011)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

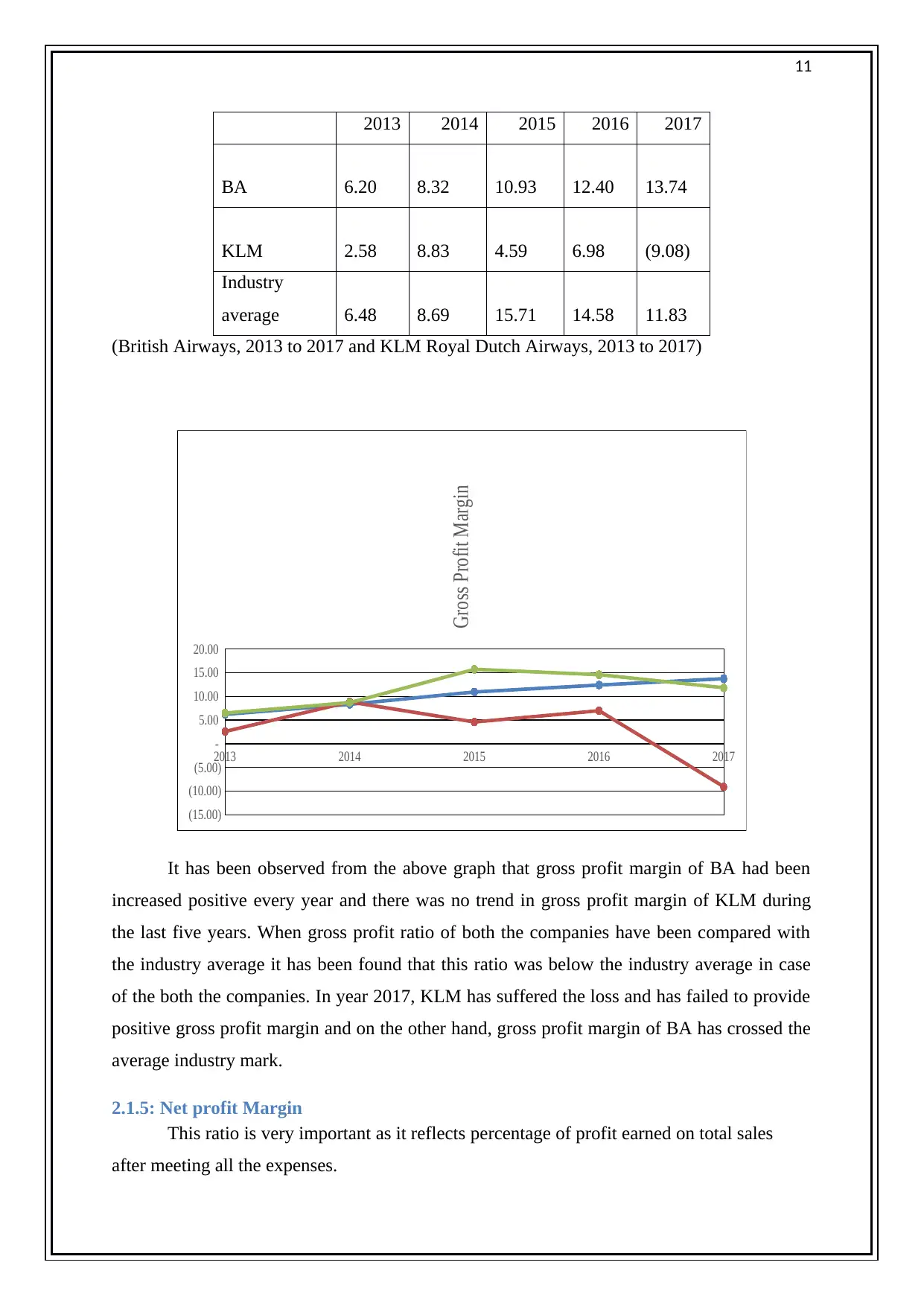

2013 2014 2015 2016 2017

BA 6.20 8.32 10.93 12.40 13.74

KLM 2.58 8.83 4.59 6.98 (9.08)

Industry

average 6.48 8.69 15.71 14.58 11.83

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

Gross Profit Margin

It has been observed from the above graph that gross profit margin of BA had been

increased positive every year and there was no trend in gross profit margin of KLM during

the last five years. When gross profit ratio of both the companies have been compared with

the industry average it has been found that this ratio was below the industry average in case

of the both the companies. In year 2017, KLM has suffered the loss and has failed to provide

positive gross profit margin and on the other hand, gross profit margin of BA has crossed the

average industry mark.

2.1.5: Net profit Margin

This ratio is very important as it reflects percentage of profit earned on total sales

after meeting all the expenses.

2013 2014 2015 2016 2017

BA 6.20 8.32 10.93 12.40 13.74

KLM 2.58 8.83 4.59 6.98 (9.08)

Industry

average 6.48 8.69 15.71 14.58 11.83

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

Gross Profit Margin

It has been observed from the above graph that gross profit margin of BA had been

increased positive every year and there was no trend in gross profit margin of KLM during

the last five years. When gross profit ratio of both the companies have been compared with

the industry average it has been found that this ratio was below the industry average in case

of the both the companies. In year 2017, KLM has suffered the loss and has failed to provide

positive gross profit margin and on the other hand, gross profit margin of BA has crossed the

average industry mark.

2.1.5: Net profit Margin

This ratio is very important as it reflects percentage of profit earned on total sales

after meeting all the expenses.

12

Net profit margin=Net profit/Net sales*100

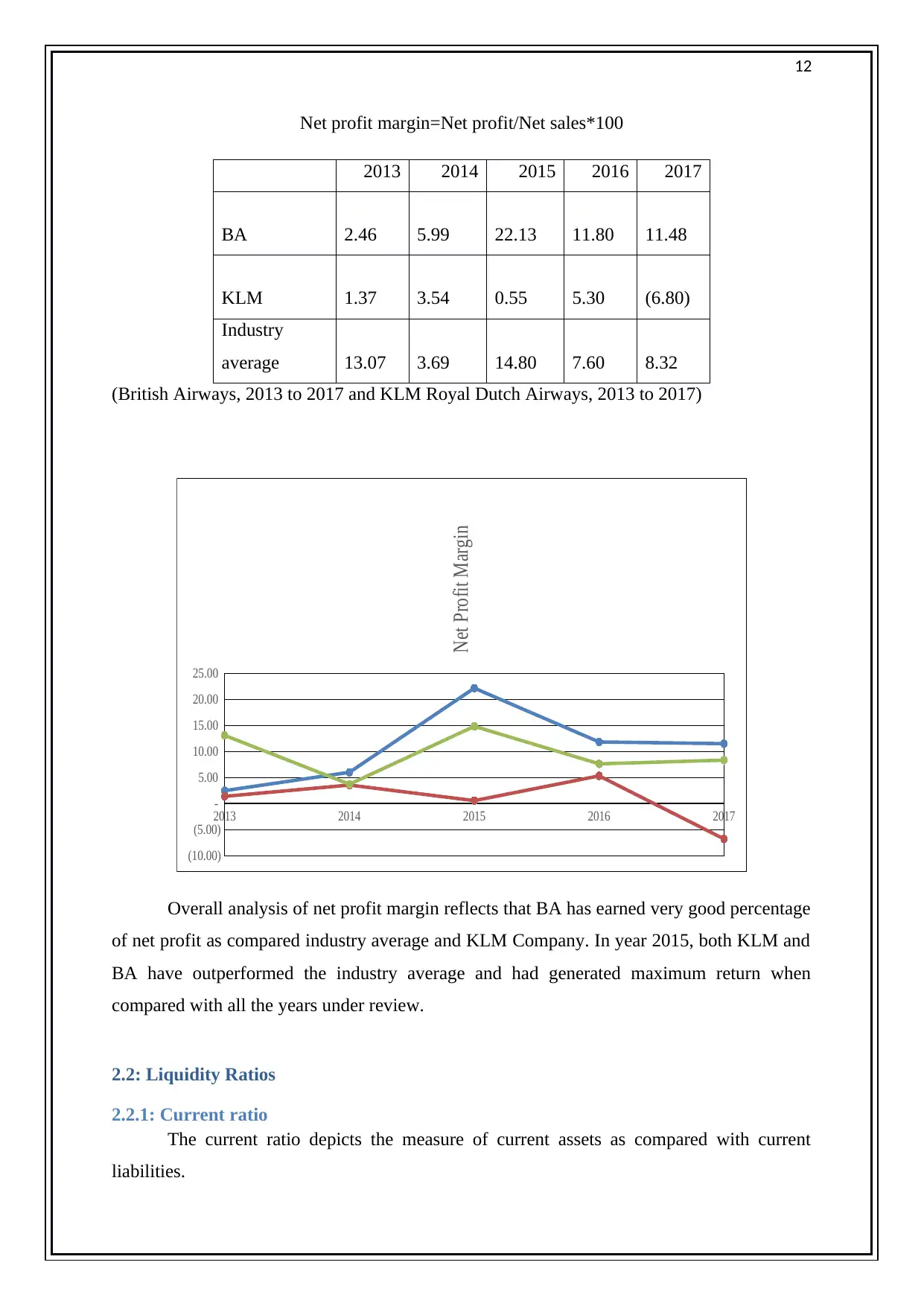

2013 2014 2015 2016 2017

BA 2.46 5.99 22.13 11.80 11.48

KLM 1.37 3.54 0.55 5.30 (6.80)

Industry

average 13.07 3.69 14.80 7.60 8.32

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

25.00

Net Profit Margin

Overall analysis of net profit margin reflects that BA has earned very good percentage

of net profit as compared industry average and KLM Company. In year 2015, both KLM and

BA have outperformed the industry average and had generated maximum return when

compared with all the years under review.

2.2: Liquidity Ratios

2.2.1: Current ratio

The current ratio depicts the measure of current assets as compared with current

liabilities.

Net profit margin=Net profit/Net sales*100

2013 2014 2015 2016 2017

BA 2.46 5.99 22.13 11.80 11.48

KLM 1.37 3.54 0.55 5.30 (6.80)

Industry

average 13.07 3.69 14.80 7.60 8.32

(British Airways, 2013 to 2017 and KLM Royal Dutch Airways, 2013 to 2017)

2013 2014 2015 2016 2017

(10.00)

(5.00)

-

5.00

10.00

15.00

20.00

25.00

Net Profit Margin

Overall analysis of net profit margin reflects that BA has earned very good percentage

of net profit as compared industry average and KLM Company. In year 2015, both KLM and

BA have outperformed the industry average and had generated maximum return when

compared with all the years under review.

2.2: Liquidity Ratios

2.2.1: Current ratio

The current ratio depicts the measure of current assets as compared with current

liabilities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.