Financial Assessment of British Airways and KLM Airlines

VerifiedAdded on 2022/12/12

|18

|4346

|208

Report

AI Summary

This report presents a comprehensive financial analysis and comparison of British Airways and KLM Royal Dutch Airlines, focusing on their performance from 2016 to 2018. The analysis includes trend analysis, ratio analysis (profitability, asset efficiency, liquidity, gearing, and investment ratios), and industry average comparisons. The report evaluates key financial metrics such as net profit, revenues, assets, and various ratios to determine each company's financial health and efficiency. It also explores strategic management accounting and cost reduction techniques within the context of the aviation industry, providing insights into the companies' operational and financial strategies. The findings offer a detailed assessment of the financial implications and performance of both airlines, highlighting their strengths, weaknesses, and overall financial stability while also considering the impact of the 2008 financial crisis on the airline industry.

Running Head: Finance Reporting and Accounting Management

Finance Reporting and Accounting Management

Finance Reporting and Accounting Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Reporting and Accounting Management

Contents

1. Introduction...................................................................................................................................2

2. Financial Assessment and Comparison of British Airways and KLM Royal Dutch Airlines........3

I. Trend Analysis...........................................................................................................................3

II. Ratio Analysis...........................................................................................................................6

1. Profitability Ratios.................................................................................................................6

2. Assets Efficiency Ratio..........................................................................................................7

3. Liquidity Ratio.......................................................................................................................8

4. Gearing Ratio.........................................................................................................................8

5. Investment Ratio....................................................................................................................9

III. Industry Average.................................................................................................................10

1. Available seat kilometres (ASK) mln..................................................................................10

2. Revenue passenger kilometres (RPK) mln...........................................................................11

3. Passenger load factor (%)....................................................................................................11

3. Strategic Management Accounting and Cost Reduction Techniques...........................................12

4. Conclusion...................................................................................................................................15

References...........................................................................................................................................16

1

Contents

1. Introduction...................................................................................................................................2

2. Financial Assessment and Comparison of British Airways and KLM Royal Dutch Airlines........3

I. Trend Analysis...........................................................................................................................3

II. Ratio Analysis...........................................................................................................................6

1. Profitability Ratios.................................................................................................................6

2. Assets Efficiency Ratio..........................................................................................................7

3. Liquidity Ratio.......................................................................................................................8

4. Gearing Ratio.........................................................................................................................8

5. Investment Ratio....................................................................................................................9

III. Industry Average.................................................................................................................10

1. Available seat kilometres (ASK) mln..................................................................................10

2. Revenue passenger kilometres (RPK) mln...........................................................................11

3. Passenger load factor (%)....................................................................................................11

3. Strategic Management Accounting and Cost Reduction Techniques...........................................12

4. Conclusion...................................................................................................................................15

References...........................................................................................................................................16

1

Finance Reporting and Accounting Management

1. Introduction

Aviation Industry plays a major role towards the growth of the economy both socially and

economically. It is not only one of the main modes of transportation but it is also a source of

employment of many people and contributes heavily to the GDP of the country (Goyal and

Negi, 2014). No, doubt the global financial crisis of 2008 had a great adverse impact on

almost all the sectors but it had a severe impact on the airlines industry. The companies like

British Airways and KLM Royal Dutch Airlines had also suffered because of the crisis whose

impact could still be felt by the companies.

British Airways and KLM Royal Dutch Airlines were the biggest companies in the whole

wide world in terms of its presence, profits, technological advance etc. There are many

efforts which were and still being made by both of the companies to provide “value for

money” to their customers and win their satisfaction by satisfying them with the innovative

services driven by technology.

2

1. Introduction

Aviation Industry plays a major role towards the growth of the economy both socially and

economically. It is not only one of the main modes of transportation but it is also a source of

employment of many people and contributes heavily to the GDP of the country (Goyal and

Negi, 2014). No, doubt the global financial crisis of 2008 had a great adverse impact on

almost all the sectors but it had a severe impact on the airlines industry. The companies like

British Airways and KLM Royal Dutch Airlines had also suffered because of the crisis whose

impact could still be felt by the companies.

British Airways and KLM Royal Dutch Airlines were the biggest companies in the whole

wide world in terms of its presence, profits, technological advance etc. There are many

efforts which were and still being made by both of the companies to provide “value for

money” to their customers and win their satisfaction by satisfying them with the innovative

services driven by technology.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Reporting and Accounting Management

2. Financial Assessment and Comparison of British Airways and KLM Royal Dutch

Airlines

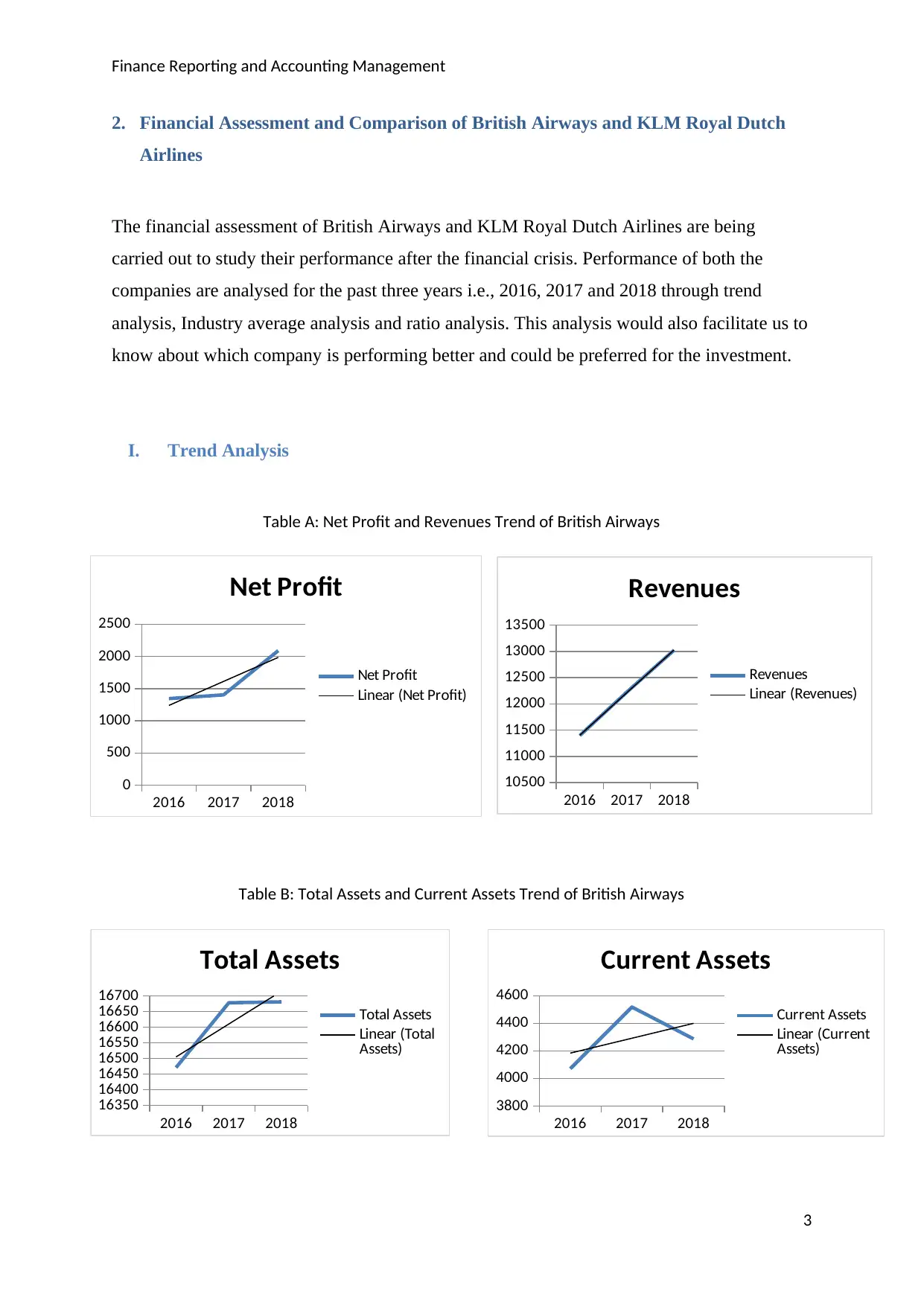

The financial assessment of British Airways and KLM Royal Dutch Airlines are being

carried out to study their performance after the financial crisis. Performance of both the

companies are analysed for the past three years i.e., 2016, 2017 and 2018 through trend

analysis, Industry average analysis and ratio analysis. This analysis would also facilitate us to

know about which company is performing better and could be preferred for the investment.

I. Trend Analysis

Table A: Net Profit and Revenues Trend of British Airways

Table B: Total Assets and Current Assets Trend of British Airways

3

2016 2017 2018

0

500

1000

1500

2000

2500

Net Profit

Net Profit

Linear (Net Profit)

2016 2017 2018

16350

16400

16450

16500

16550

16600

16650

16700

Total Assets

Total Assets

Linear (Total

Assets)

2016 2017 2018

3800

4000

4200

4400

4600

Current Assets

Current Assets

Linear (Current

Assets)

2016 2017 2018

10500

11000

11500

12000

12500

13000

13500

Revenues

Revenues

Linear (Revenues)

2. Financial Assessment and Comparison of British Airways and KLM Royal Dutch

Airlines

The financial assessment of British Airways and KLM Royal Dutch Airlines are being

carried out to study their performance after the financial crisis. Performance of both the

companies are analysed for the past three years i.e., 2016, 2017 and 2018 through trend

analysis, Industry average analysis and ratio analysis. This analysis would also facilitate us to

know about which company is performing better and could be preferred for the investment.

I. Trend Analysis

Table A: Net Profit and Revenues Trend of British Airways

Table B: Total Assets and Current Assets Trend of British Airways

3

2016 2017 2018

0

500

1000

1500

2000

2500

Net Profit

Net Profit

Linear (Net Profit)

2016 2017 2018

16350

16400

16450

16500

16550

16600

16650

16700

Total Assets

Total Assets

Linear (Total

Assets)

2016 2017 2018

3800

4000

4200

4400

4600

Current Assets

Current Assets

Linear (Current

Assets)

2016 2017 2018

10500

11000

11500

12000

12500

13000

13500

Revenues

Revenues

Linear (Revenues)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Reporting and Accounting Management

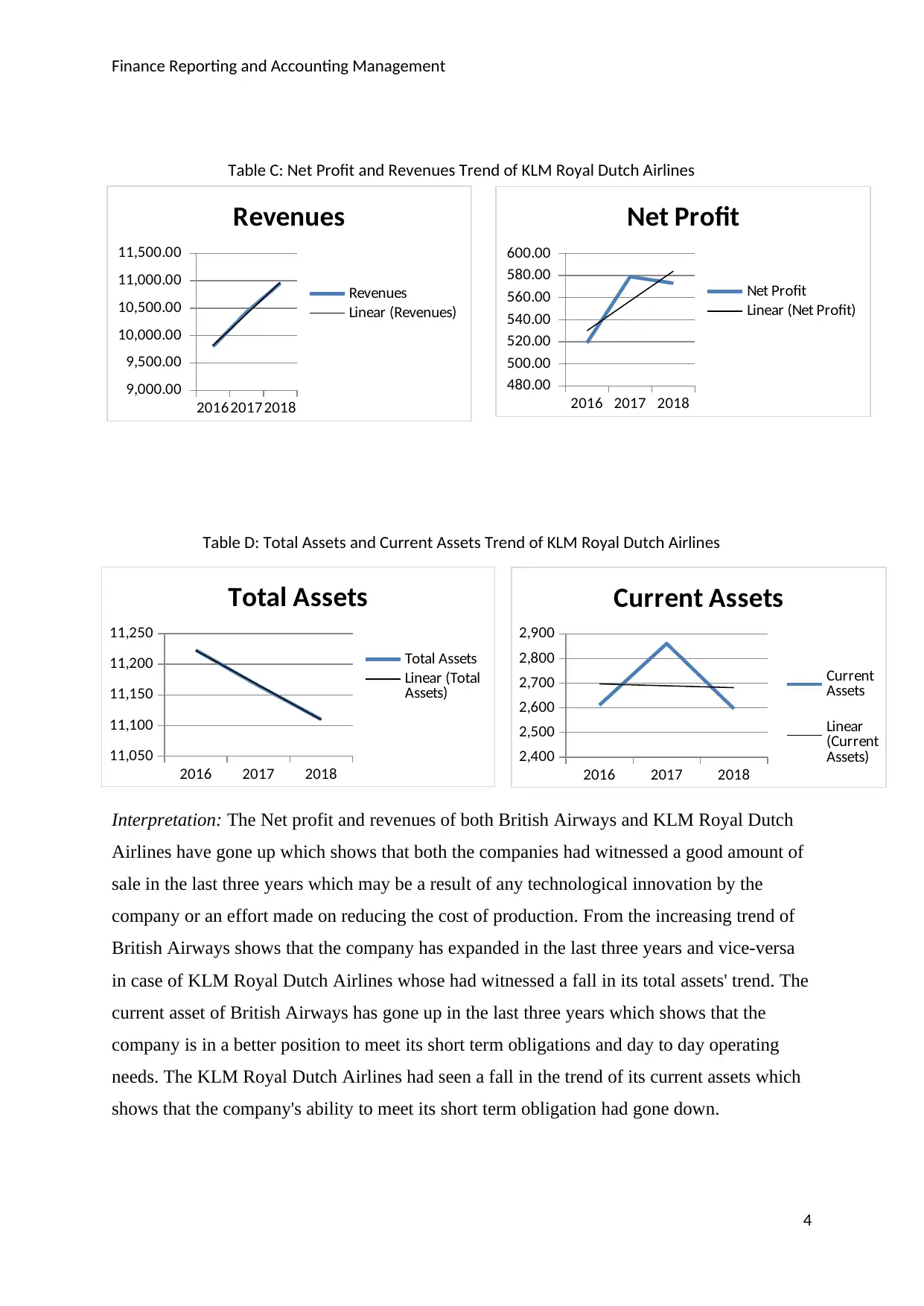

Table C: Net Profit and Revenues Trend of KLM Royal Dutch Airlines

Table D: Total Assets and Current Assets Trend of KLM Royal Dutch Airlines

Interpretation: The Net profit and revenues of both British Airways and KLM Royal Dutch

Airlines have gone up which shows that both the companies had witnessed a good amount of

sale in the last three years which may be a result of any technological innovation by the

company or an effort made on reducing the cost of production. From the increasing trend of

British Airways shows that the company has expanded in the last three years and vice-versa

in case of KLM Royal Dutch Airlines whose had witnessed a fall in its total assets' trend. The

current asset of British Airways has gone up in the last three years which shows that the

company is in a better position to meet its short term obligations and day to day operating

needs. The KLM Royal Dutch Airlines had seen a fall in the trend of its current assets which

shows that the company's ability to meet its short term obligation had gone down.

4

201620172018

9,000.00

9,500.00

10,000.00

10,500.00

11,000.00

11,500.00

Revenues

Revenues

Linear (Revenues)

2016 2017 2018

11,050

11,100

11,150

11,200

11,250

Total Assets

Total Assets

Linear (Total

Assets)

2016 2017 2018

2,400

2,500

2,600

2,700

2,800

2,900

Current Assets

Current

Assets

Linear

(Current

Assets)

2016 2017 2018

480.00

500.00

520.00

540.00

560.00

580.00

600.00

Net Profit

Net Profit

Linear (Net Profit)

Table C: Net Profit and Revenues Trend of KLM Royal Dutch Airlines

Table D: Total Assets and Current Assets Trend of KLM Royal Dutch Airlines

Interpretation: The Net profit and revenues of both British Airways and KLM Royal Dutch

Airlines have gone up which shows that both the companies had witnessed a good amount of

sale in the last three years which may be a result of any technological innovation by the

company or an effort made on reducing the cost of production. From the increasing trend of

British Airways shows that the company has expanded in the last three years and vice-versa

in case of KLM Royal Dutch Airlines whose had witnessed a fall in its total assets' trend. The

current asset of British Airways has gone up in the last three years which shows that the

company is in a better position to meet its short term obligations and day to day operating

needs. The KLM Royal Dutch Airlines had seen a fall in the trend of its current assets which

shows that the company's ability to meet its short term obligation had gone down.

4

201620172018

9,000.00

9,500.00

10,000.00

10,500.00

11,000.00

11,500.00

Revenues

Revenues

Linear (Revenues)

2016 2017 2018

11,050

11,100

11,150

11,200

11,250

Total Assets

Total Assets

Linear (Total

Assets)

2016 2017 2018

2,400

2,500

2,600

2,700

2,800

2,900

Current Assets

Current

Assets

Linear

(Current

Assets)

2016 2017 2018

480.00

500.00

520.00

540.00

560.00

580.00

600.00

Net Profit

Net Profit

Linear (Net Profit)

Finance Reporting and Accounting Management

II. Ratio Analysis

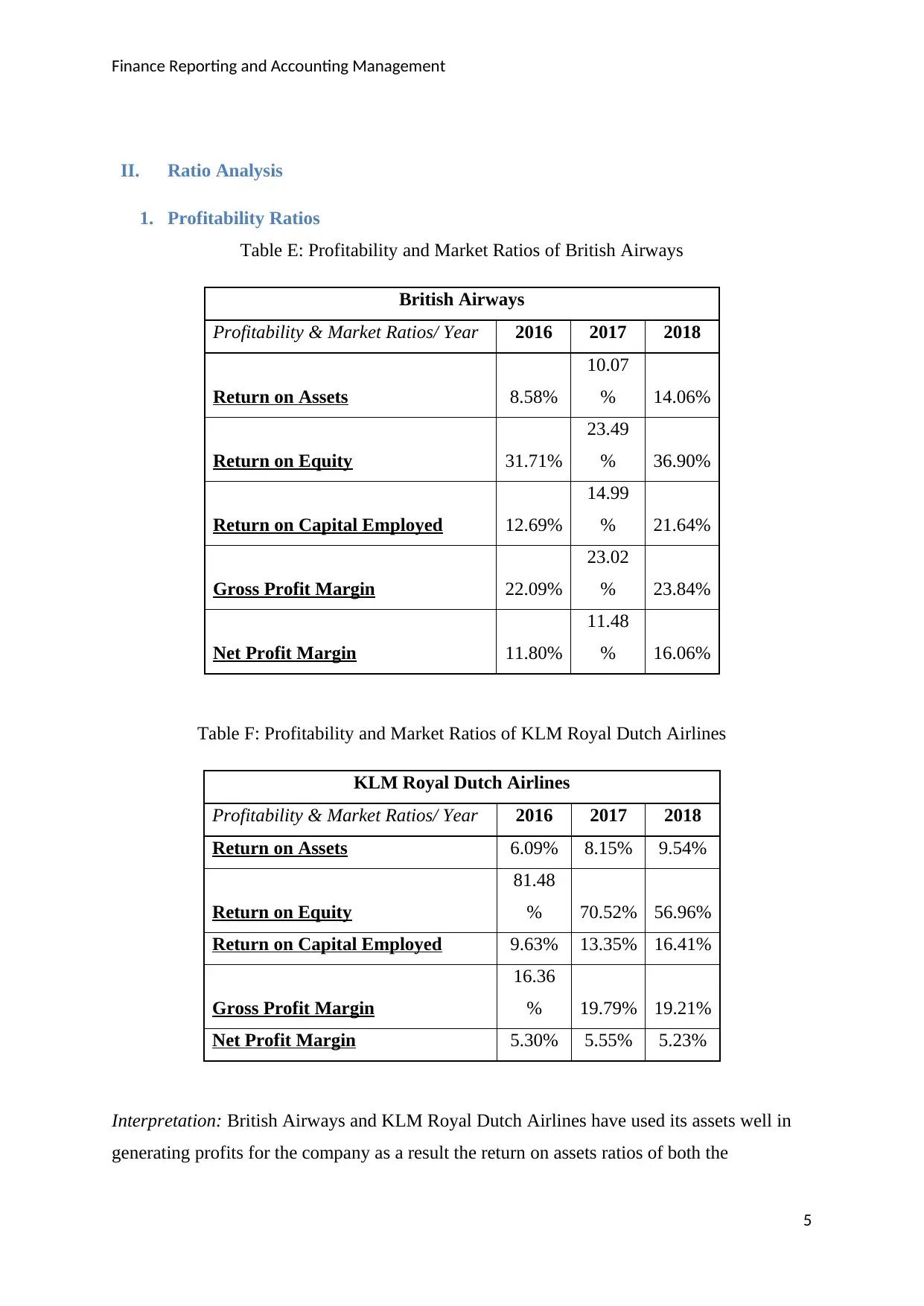

1. Profitability Ratios

Table E: Profitability and Market Ratios of British Airways

British Airways

Profitability & Market Ratios/ Year 2016 2017 2018

Return on Assets 8.58%

10.07

% 14.06%

Return on Equity 31.71%

23.49

% 36.90%

Return on Capital Employed 12.69%

14.99

% 21.64%

Gross Profit Margin 22.09%

23.02

% 23.84%

Net Profit Margin 11.80%

11.48

% 16.06%

Table F: Profitability and Market Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Profitability & Market Ratios/ Year 2016 2017 2018

Return on Assets 6.09% 8.15% 9.54%

Return on Equity

81.48

% 70.52% 56.96%

Return on Capital Employed 9.63% 13.35% 16.41%

Gross Profit Margin

16.36

% 19.79% 19.21%

Net Profit Margin 5.30% 5.55% 5.23%

Interpretation: British Airways and KLM Royal Dutch Airlines have used its assets well in

generating profits for the company as a result the return on assets ratios of both the

5

II. Ratio Analysis

1. Profitability Ratios

Table E: Profitability and Market Ratios of British Airways

British Airways

Profitability & Market Ratios/ Year 2016 2017 2018

Return on Assets 8.58%

10.07

% 14.06%

Return on Equity 31.71%

23.49

% 36.90%

Return on Capital Employed 12.69%

14.99

% 21.64%

Gross Profit Margin 22.09%

23.02

% 23.84%

Net Profit Margin 11.80%

11.48

% 16.06%

Table F: Profitability and Market Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Profitability & Market Ratios/ Year 2016 2017 2018

Return on Assets 6.09% 8.15% 9.54%

Return on Equity

81.48

% 70.52% 56.96%

Return on Capital Employed 9.63% 13.35% 16.41%

Gross Profit Margin

16.36

% 19.79% 19.21%

Net Profit Margin 5.30% 5.55% 5.23%

Interpretation: British Airways and KLM Royal Dutch Airlines have used its assets well in

generating profits for the company as a result the return on assets ratios of both the

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Reporting and Accounting Management

companies have gone up in the last three years. British Airways has utilised the shareholder's

funds effectively to generate profit as a result the return on equity figure has gone up.

However, the case is not the same with KLM Royal Dutch Airlines where the figure of return

on equity has declined. The return on capital employed of both the companies has gone up

over the three years. However, individually British Airways is utilizing its capital

comparatively well. Gross profit margin ratio of British Airways has gone up in the last three

years but the same ratio had declined in case of KLM Royal Dutch Airlines. The industry

average of gross profit ratio had been 8.5%, 7.7% and 6.8% for 2016, 2017 and 2018

respectively. This shows that both the airline companies have performed far better than the

industry average. Net profit margin shows how efficient the company is at converting its

sales into profit. This ratio of British Airways has gone up and over the three years and it

declined for KLM Royal Dutch Airlines. The industry average of net profit margin stood at

4.8%, 5% and 3.9% for 2016, 2017 and 2018 respectively. This depicts that both the airline

companies have converted their sales into profit effectively over their other competitors.

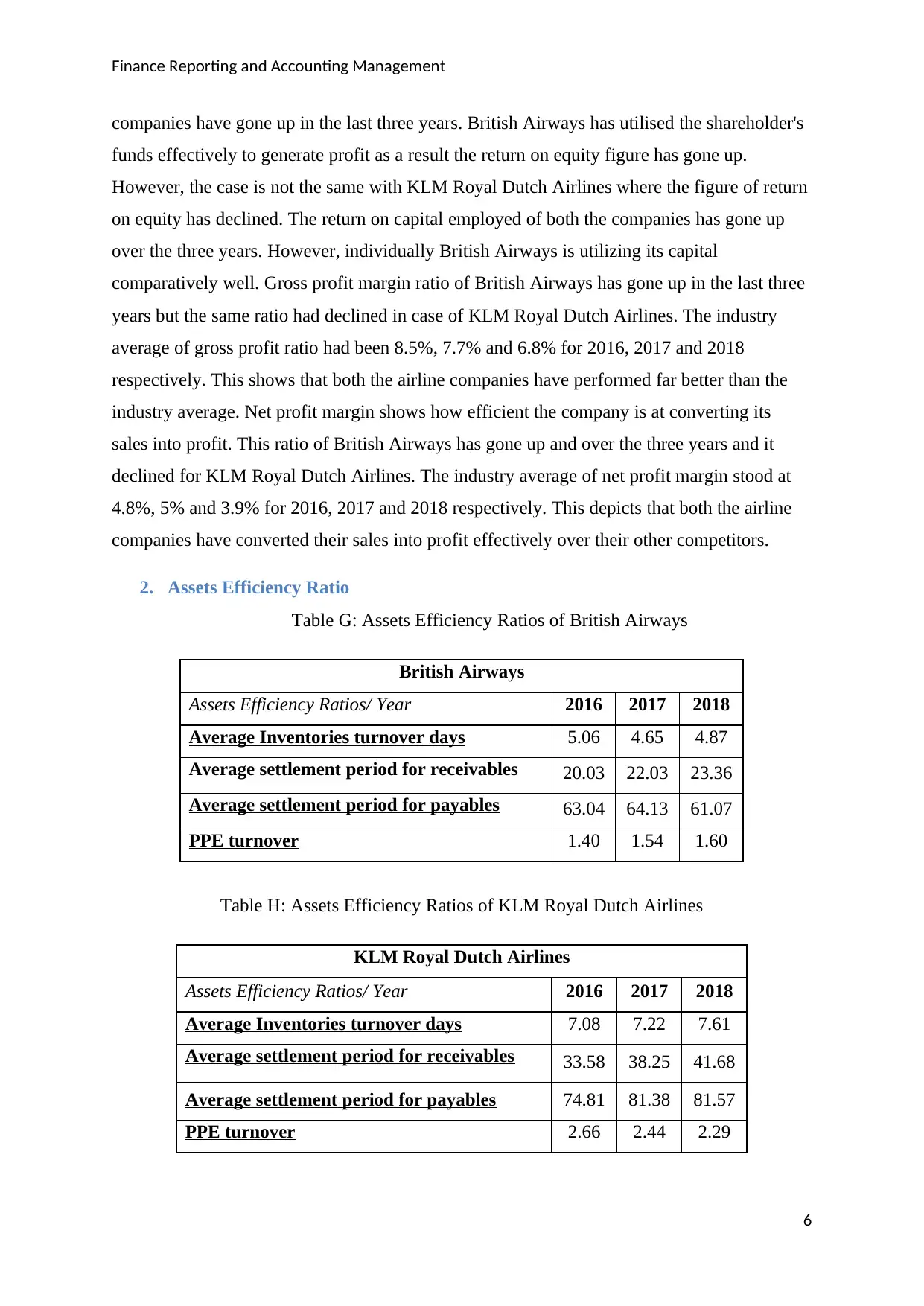

2. Assets Efficiency Ratio

Table G: Assets Efficiency Ratios of British Airways

Table H: Assets Efficiency Ratios of KLM Royal Dutch Airlines

6

British Airways

Assets Efficiency Ratios/ Year 2016 2017 2018

Average Inventories turnover days 5.06 4.65 4.87

Average settlement period for receivables 20.03 22.03 23.36

Average settlement period for payables 63.04 64.13 61.07

PPE turnover 1.40 1.54 1.60

KLM Royal Dutch Airlines

Assets Efficiency Ratios/ Year 2016 2017 2018

Average Inventories turnover days 7.08 7.22 7.61

Average settlement period for receivables 33.58 38.25 41.68

Average settlement period for payables 74.81 81.38 81.57

PPE turnover 2.66 2.44 2.29

companies have gone up in the last three years. British Airways has utilised the shareholder's

funds effectively to generate profit as a result the return on equity figure has gone up.

However, the case is not the same with KLM Royal Dutch Airlines where the figure of return

on equity has declined. The return on capital employed of both the companies has gone up

over the three years. However, individually British Airways is utilizing its capital

comparatively well. Gross profit margin ratio of British Airways has gone up in the last three

years but the same ratio had declined in case of KLM Royal Dutch Airlines. The industry

average of gross profit ratio had been 8.5%, 7.7% and 6.8% for 2016, 2017 and 2018

respectively. This shows that both the airline companies have performed far better than the

industry average. Net profit margin shows how efficient the company is at converting its

sales into profit. This ratio of British Airways has gone up and over the three years and it

declined for KLM Royal Dutch Airlines. The industry average of net profit margin stood at

4.8%, 5% and 3.9% for 2016, 2017 and 2018 respectively. This depicts that both the airline

companies have converted their sales into profit effectively over their other competitors.

2. Assets Efficiency Ratio

Table G: Assets Efficiency Ratios of British Airways

Table H: Assets Efficiency Ratios of KLM Royal Dutch Airlines

6

British Airways

Assets Efficiency Ratios/ Year 2016 2017 2018

Average Inventories turnover days 5.06 4.65 4.87

Average settlement period for receivables 20.03 22.03 23.36

Average settlement period for payables 63.04 64.13 61.07

PPE turnover 1.40 1.54 1.60

KLM Royal Dutch Airlines

Assets Efficiency Ratios/ Year 2016 2017 2018

Average Inventories turnover days 7.08 7.22 7.61

Average settlement period for receivables 33.58 38.25 41.68

Average settlement period for payables 74.81 81.38 81.57

PPE turnover 2.66 2.44 2.29

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Reporting and Accounting Management

Interpretation: The average time taken by the British Airways to convert the inventory into

sales has become less over the past three years and these days have gone up in case of KLM

Royal Dutch Airlines. This shows that KLM is inefficient in turning its assets speedily. The

average time taken by the British Airways to collect the cash on accounts or trade receivables

has been nearly between 20-23days in the past three years. However, the time taken by KLM

Royal Dutch Airlines for converting the trade receivables into cash lies between 33- 42days.

This shows that British Airways has a very good credit policy and the sound creditors who

return the borrowed amount timely and KLM Royal Dutch Airlines is having a very poor

credit policy as a result it is taking more than one month to recover the lent amount. Now if

we look at the average number of days taken by both the companies in paying back the

amount on accounts payables, then we would see that British Airways have taken less time in

comparison to KLM Royal Dutch Airlines. The British Airways has also improved in

utilising its property, plant and equipment to generate sales but KLM Royal Dutch has not

improved in utilising its Property, plant and equipment to generate sales.

3. Liquidity Ratio

Table I: Liquidity Ratios of British Airways

British Airways

Liquidity Ratios/ Year 2016 2017 2018

Current Ratio 0.76 0.83 0.73

Acid test ratio 0.66 0.73 0.63

Table J: Liquidity Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Liquidity Ratios/ Year 2016 2017 2018

Current Ratio 0.63 0.66 0.56

Acid test ratio 0.56 0.59 0.48

Interpretation: Liquidity ratios of the companies are calculated to know about the ability of

the company to pay back its debt on the given due date (Samonas, 2015).In terms of Liquidity

both the companies are really stable and in a good position which would ultimately help the

7

Interpretation: The average time taken by the British Airways to convert the inventory into

sales has become less over the past three years and these days have gone up in case of KLM

Royal Dutch Airlines. This shows that KLM is inefficient in turning its assets speedily. The

average time taken by the British Airways to collect the cash on accounts or trade receivables

has been nearly between 20-23days in the past three years. However, the time taken by KLM

Royal Dutch Airlines for converting the trade receivables into cash lies between 33- 42days.

This shows that British Airways has a very good credit policy and the sound creditors who

return the borrowed amount timely and KLM Royal Dutch Airlines is having a very poor

credit policy as a result it is taking more than one month to recover the lent amount. Now if

we look at the average number of days taken by both the companies in paying back the

amount on accounts payables, then we would see that British Airways have taken less time in

comparison to KLM Royal Dutch Airlines. The British Airways has also improved in

utilising its property, plant and equipment to generate sales but KLM Royal Dutch has not

improved in utilising its Property, plant and equipment to generate sales.

3. Liquidity Ratio

Table I: Liquidity Ratios of British Airways

British Airways

Liquidity Ratios/ Year 2016 2017 2018

Current Ratio 0.76 0.83 0.73

Acid test ratio 0.66 0.73 0.63

Table J: Liquidity Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Liquidity Ratios/ Year 2016 2017 2018

Current Ratio 0.63 0.66 0.56

Acid test ratio 0.56 0.59 0.48

Interpretation: Liquidity ratios of the companies are calculated to know about the ability of

the company to pay back its debt on the given due date (Samonas, 2015).In terms of Liquidity

both the companies are really stable and in a good position which would ultimately help the

7

Finance Reporting and Accounting Management

company in meeting its working capital requirements without any difficulty. Comparatively,

British Airways is more liquid than KLM Royal Dutch Airlines.

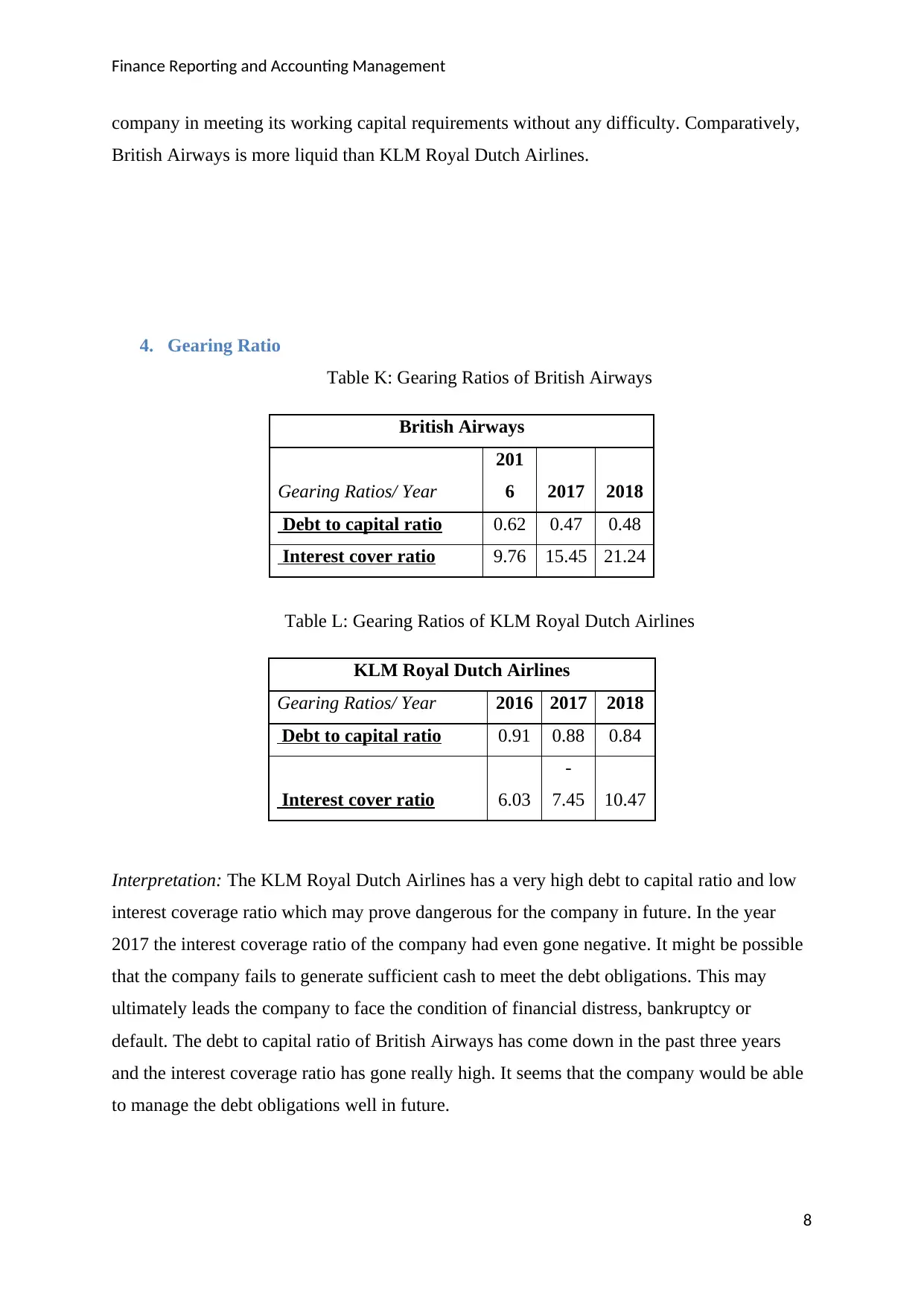

4. Gearing Ratio

Table K: Gearing Ratios of British Airways

British Airways

Gearing Ratios/ Year

201

6 2017 2018

Debt to capital ratio 0.62 0.47 0.48

Interest cover ratio 9.76 15.45 21.24

Table L: Gearing Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Gearing Ratios/ Year 2016 2017 2018

Debt to capital ratio 0.91 0.88 0.84

Interest cover ratio 6.03

-

7.45 10.47

Interpretation: The KLM Royal Dutch Airlines has a very high debt to capital ratio and low

interest coverage ratio which may prove dangerous for the company in future. In the year

2017 the interest coverage ratio of the company had even gone negative. It might be possible

that the company fails to generate sufficient cash to meet the debt obligations. This may

ultimately leads the company to face the condition of financial distress, bankruptcy or

default. The debt to capital ratio of British Airways has come down in the past three years

and the interest coverage ratio has gone really high. It seems that the company would be able

to manage the debt obligations well in future.

8

company in meeting its working capital requirements without any difficulty. Comparatively,

British Airways is more liquid than KLM Royal Dutch Airlines.

4. Gearing Ratio

Table K: Gearing Ratios of British Airways

British Airways

Gearing Ratios/ Year

201

6 2017 2018

Debt to capital ratio 0.62 0.47 0.48

Interest cover ratio 9.76 15.45 21.24

Table L: Gearing Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Gearing Ratios/ Year 2016 2017 2018

Debt to capital ratio 0.91 0.88 0.84

Interest cover ratio 6.03

-

7.45 10.47

Interpretation: The KLM Royal Dutch Airlines has a very high debt to capital ratio and low

interest coverage ratio which may prove dangerous for the company in future. In the year

2017 the interest coverage ratio of the company had even gone negative. It might be possible

that the company fails to generate sufficient cash to meet the debt obligations. This may

ultimately leads the company to face the condition of financial distress, bankruptcy or

default. The debt to capital ratio of British Airways has come down in the past three years

and the interest coverage ratio has gone really high. It seems that the company would be able

to manage the debt obligations well in future.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance Reporting and Accounting Management

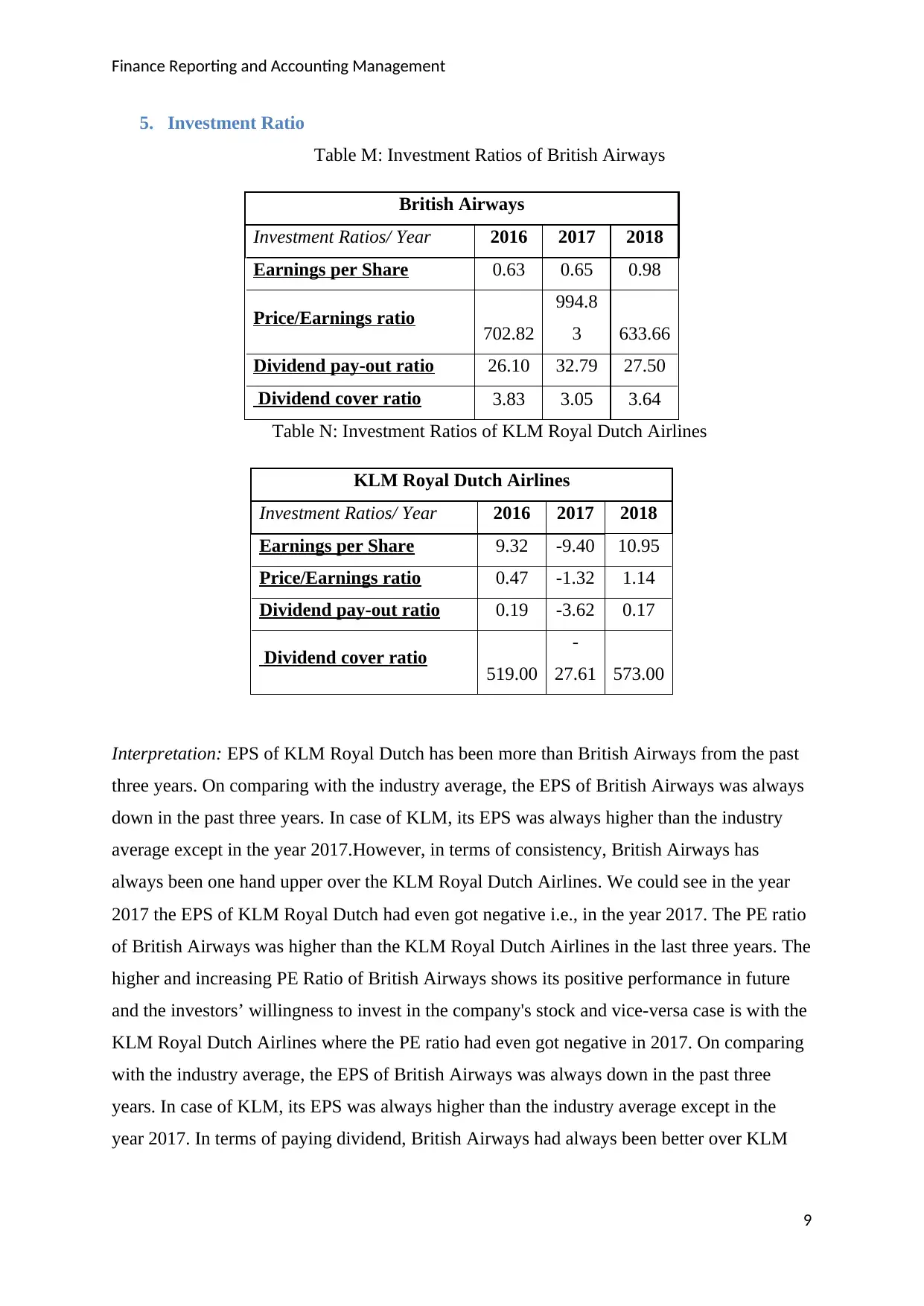

5. Investment Ratio

Table M: Investment Ratios of British Airways

British Airways

Investment Ratios/ Year 2016 2017 2018

Earnings per Share 0.63 0.65 0.98

Price/Earnings ratio 702.82

994.8

3 633.66

Dividend pay-out ratio 26.10 32.79 27.50

Dividend cover ratio 3.83 3.05 3.64

Table N: Investment Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Investment Ratios/ Year 2016 2017 2018

Earnings per Share 9.32 -9.40 10.95

Price/Earnings ratio 0.47 -1.32 1.14

Dividend pay-out ratio 0.19 -3.62 0.17

Dividend cover ratio 519.00

-

27.61 573.00

Interpretation: EPS of KLM Royal Dutch has been more than British Airways from the past

three years. On comparing with the industry average, the EPS of British Airways was always

down in the past three years. In case of KLM, its EPS was always higher than the industry

average except in the year 2017.However, in terms of consistency, British Airways has

always been one hand upper over the KLM Royal Dutch Airlines. We could see in the year

2017 the EPS of KLM Royal Dutch had even got negative i.e., in the year 2017. The PE ratio

of British Airways was higher than the KLM Royal Dutch Airlines in the last three years. The

higher and increasing PE Ratio of British Airways shows its positive performance in future

and the investors’ willingness to invest in the company's stock and vice-versa case is with the

KLM Royal Dutch Airlines where the PE ratio had even got negative in 2017. On comparing

with the industry average, the EPS of British Airways was always down in the past three

years. In case of KLM, its EPS was always higher than the industry average except in the

year 2017. In terms of paying dividend, British Airways had always been better over KLM

9

5. Investment Ratio

Table M: Investment Ratios of British Airways

British Airways

Investment Ratios/ Year 2016 2017 2018

Earnings per Share 0.63 0.65 0.98

Price/Earnings ratio 702.82

994.8

3 633.66

Dividend pay-out ratio 26.10 32.79 27.50

Dividend cover ratio 3.83 3.05 3.64

Table N: Investment Ratios of KLM Royal Dutch Airlines

KLM Royal Dutch Airlines

Investment Ratios/ Year 2016 2017 2018

Earnings per Share 9.32 -9.40 10.95

Price/Earnings ratio 0.47 -1.32 1.14

Dividend pay-out ratio 0.19 -3.62 0.17

Dividend cover ratio 519.00

-

27.61 573.00

Interpretation: EPS of KLM Royal Dutch has been more than British Airways from the past

three years. On comparing with the industry average, the EPS of British Airways was always

down in the past three years. In case of KLM, its EPS was always higher than the industry

average except in the year 2017.However, in terms of consistency, British Airways has

always been one hand upper over the KLM Royal Dutch Airlines. We could see in the year

2017 the EPS of KLM Royal Dutch had even got negative i.e., in the year 2017. The PE ratio

of British Airways was higher than the KLM Royal Dutch Airlines in the last three years. The

higher and increasing PE Ratio of British Airways shows its positive performance in future

and the investors’ willingness to invest in the company's stock and vice-versa case is with the

KLM Royal Dutch Airlines where the PE ratio had even got negative in 2017. On comparing

with the industry average, the EPS of British Airways was always down in the past three

years. In case of KLM, its EPS was always higher than the industry average except in the

year 2017. In terms of paying dividend, British Airways had always been better over KLM

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Finance Reporting and Accounting Management

Royal Dutch Airlines. The low dividend pay-out ratio of British Airways shows that the

company had paid a large amount of company's total earnings towards the dividend payment.

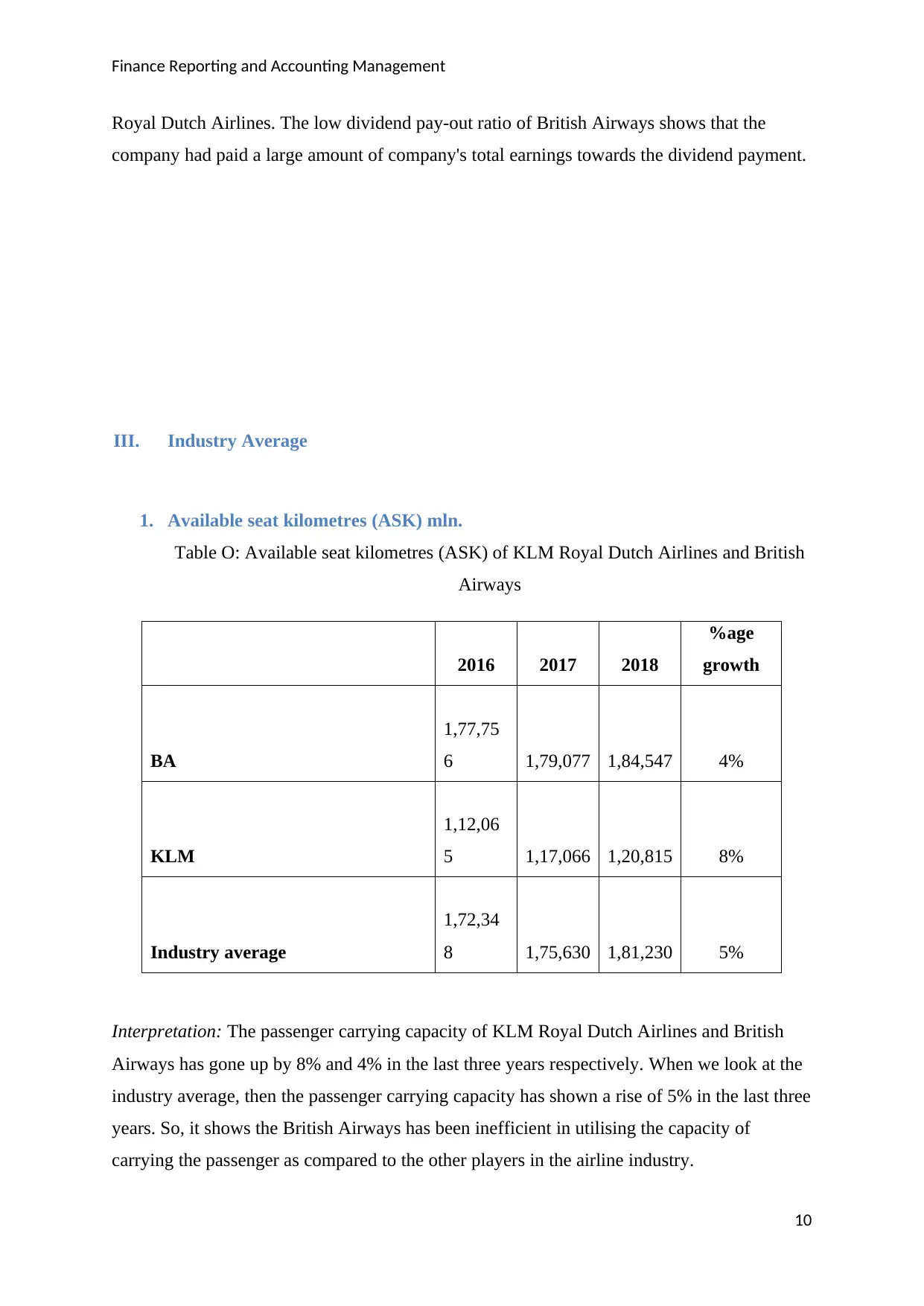

III. Industry Average

1. Available seat kilometres (ASK) mln.

Table O: Available seat kilometres (ASK) of KLM Royal Dutch Airlines and British

Airways

2016 2017 2018

%age

growth

BA

1,77,75

6 1,79,077 1,84,547 4%

KLM

1,12,06

5 1,17,066 1,20,815 8%

Industry average

1,72,34

8 1,75,630 1,81,230 5%

Interpretation: The passenger carrying capacity of KLM Royal Dutch Airlines and British

Airways has gone up by 8% and 4% in the last three years respectively. When we look at the

industry average, then the passenger carrying capacity has shown a rise of 5% in the last three

years. So, it shows the British Airways has been inefficient in utilising the capacity of

carrying the passenger as compared to the other players in the airline industry.

10

Royal Dutch Airlines. The low dividend pay-out ratio of British Airways shows that the

company had paid a large amount of company's total earnings towards the dividend payment.

III. Industry Average

1. Available seat kilometres (ASK) mln.

Table O: Available seat kilometres (ASK) of KLM Royal Dutch Airlines and British

Airways

2016 2017 2018

%age

growth

BA

1,77,75

6 1,79,077 1,84,547 4%

KLM

1,12,06

5 1,17,066 1,20,815 8%

Industry average

1,72,34

8 1,75,630 1,81,230 5%

Interpretation: The passenger carrying capacity of KLM Royal Dutch Airlines and British

Airways has gone up by 8% and 4% in the last three years respectively. When we look at the

industry average, then the passenger carrying capacity has shown a rise of 5% in the last three

years. So, it shows the British Airways has been inefficient in utilising the capacity of

carrying the passenger as compared to the other players in the airline industry.

10

Finance Reporting and Accounting Management

2. Revenue passenger kilometres (RPK) mln.

Table P: Revenue passenger kilometres (RPK) of KLM Royal Dutch Airlines and

British Airways

Interpretation: Revenue passengers are the one from whom the airline charges a sum of

money for the trip. The RPK of KLM has gone up by 10% in the last three years and by 5%

for British Airways. As per industry average, RPK has increased by 12%. This RPK shows

the amount of production created by an airline company. On the basis of industry average

both the airlines companies had not performed well. Still on comparing with British Airways,

KLM had given somewhat an acceptable production.

3. Passenger load factor (%)

Table Q: Passenger load factor of KLM Royal Dutch Airlines and British Airways

2016 2017 2018

BA 81.2 81.8 82.5

KLM 87.2 88.4 89.1

Industry average 82.4 83.3 81.9

Interpretation: KLM has very well managed to fill the seats and generate revenues from fare

over the past three years but comparatively, British Airways did not utilize the plane capacity

11

2016 2017 2018

%age

growth

BA

1,44,39

9 1,46,561 1,52,177 5%

KLM 97,737 1,03,487 1,07,676 10%

Industry average

1,47,00

1 1,51,102 1,64,830 12%

2. Revenue passenger kilometres (RPK) mln.

Table P: Revenue passenger kilometres (RPK) of KLM Royal Dutch Airlines and

British Airways

Interpretation: Revenue passengers are the one from whom the airline charges a sum of

money for the trip. The RPK of KLM has gone up by 10% in the last three years and by 5%

for British Airways. As per industry average, RPK has increased by 12%. This RPK shows

the amount of production created by an airline company. On the basis of industry average

both the airlines companies had not performed well. Still on comparing with British Airways,

KLM had given somewhat an acceptable production.

3. Passenger load factor (%)

Table Q: Passenger load factor of KLM Royal Dutch Airlines and British Airways

2016 2017 2018

BA 81.2 81.8 82.5

KLM 87.2 88.4 89.1

Industry average 82.4 83.3 81.9

Interpretation: KLM has very well managed to fill the seats and generate revenues from fare

over the past three years but comparatively, British Airways did not utilize the plane capacity

11

2016 2017 2018

%age

growth

BA

1,44,39

9 1,46,561 1,52,177 5%

KLM 97,737 1,03,487 1,07,676 10%

Industry average

1,47,00

1 1,51,102 1,64,830 12%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.