British American Tobacco Plc: Contemporary Issues in Accounting

VerifiedAdded on 2023/06/15

|13

|2256

|400

Report

AI Summary

This report analyzes the financial statements of British American Tobacco Plc to determine its compliance with general purpose financial reporting standards. It examines the company's adherence to the objectives of general purpose financial reporting, including providing relevant information to investors, assessing cash flow generation, and accurately representing assets, liabilities, income, and expenses. The report also assesses the company's recognition criteria for various financial statement items like assets, liabilities, revenues, equity, and expenses, referencing Australian Accounting Standards Board (AASB) guidelines. Furthermore, it evaluates the fundamental qualitative characteristics of relevance and faithful representation, as well as enhancing qualitative characteristics such as comparability, verifiability, timeliness and understandability. The analysis concludes that British American Tobacco Plc generally adheres to the principles and standards of general purpose financial reporting, ensuring its financial statements are presentable, accurate, and informative for stakeholders.

Running head: CONTEMPORARY ISSSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Contemporary Issues in Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The main purpose of this assignment is to analyze the financial statement of a company and

inspect whether the company has been following General purpose financial reporting

appropriately. The company which has been selected for this assignment is British American

Tobacco Plc which is operating in Australia. The report will also analyze the various reporting

criteria of the company and inspect whether such criteria is as per the general financial reporting

standards.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The main purpose of this assignment is to analyze the financial statement of a company and

inspect whether the company has been following General purpose financial reporting

appropriately. The company which has been selected for this assignment is British American

Tobacco Plc which is operating in Australia. The report will also analyze the various reporting

criteria of the company and inspect whether such criteria is as per the general financial reporting

standards.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of General Purpose Financial Reporting...................................................................3

Recognition Criteria of Items of Financial Statement.................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Conclusion.......................................................................................................................................9

Reference.......................................................................................................................................11

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Discussions......................................................................................................................................3

Objectives of General Purpose Financial Reporting...................................................................3

Recognition Criteria of Items of Financial Statement.................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Conclusion.......................................................................................................................................9

Reference.......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The concept of General purpose financial reporting is related to a conceptual framework

which every business needs to follow in order to prepare the financial statement in a presentable

manner. It is very crucial for a business as the general purpose financial reports reflects the

financial position of an entity (Collis & Hussey, 2013). The reporting guidelines includes various

accounting standards and policies on the basis of which the entity is to prepare financial

statements. The framework of General purpose financial reporting was developed by

International Accounting Standard Board (IASB). The general purpose financial reporting needs

to followed by all business firms in order to ensure that the business is reporting all the items

accurately (Henderson et al., 2015).

The company for the purpose of this assessment is British American Tobacco Plc. The

company is engaged in the manufacturing tobacco goods such as cigarettes. The company has

operations in more than 180 countries and is regarded to be market leading brand. The four

largest selling brands of the company is Dunhill, Lucky strike, Pall Mall and Kent.

Discussions

Objectives of General Purpose Financial Reporting

As discussed above the frame which is provided for general purpose financial reporting is

essential to the business as it ensures that all the relevant standards are followed while preparing

the financial statements. The objectives of the General financial reporting framework are

discussed below in details:

1. The main objective of the General financial reporting framework is to ensure that the

financial statements are prepared in such a way that all the relevant information are

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

The concept of General purpose financial reporting is related to a conceptual framework

which every business needs to follow in order to prepare the financial statement in a presentable

manner. It is very crucial for a business as the general purpose financial reports reflects the

financial position of an entity (Collis & Hussey, 2013). The reporting guidelines includes various

accounting standards and policies on the basis of which the entity is to prepare financial

statements. The framework of General purpose financial reporting was developed by

International Accounting Standard Board (IASB). The general purpose financial reporting needs

to followed by all business firms in order to ensure that the business is reporting all the items

accurately (Henderson et al., 2015).

The company for the purpose of this assessment is British American Tobacco Plc. The

company is engaged in the manufacturing tobacco goods such as cigarettes. The company has

operations in more than 180 countries and is regarded to be market leading brand. The four

largest selling brands of the company is Dunhill, Lucky strike, Pall Mall and Kent.

Discussions

Objectives of General Purpose Financial Reporting

As discussed above the frame which is provided for general purpose financial reporting is

essential to the business as it ensures that all the relevant standards are followed while preparing

the financial statements. The objectives of the General financial reporting framework are

discussed below in details:

1. The main objective of the General financial reporting framework is to ensure that the

financial statements are prepared in such a way that all the relevant information are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

reflected which can help the potential investors, lenders and creditors of the company to

take decisions regarding buying, selling or holding and similar other decisions

(Lawrence, 2013). In the case of British American Tobacco Company, the financial

reports of the company contain all the relevant information which can be of use to the

shareholders, lenders and other user of financial statements for the purpose of decision

making. The profit and loss account, balance sheet and cash flow statement are

effectively prepared which can provide the shareholders information regarding the overall

performance of the company.

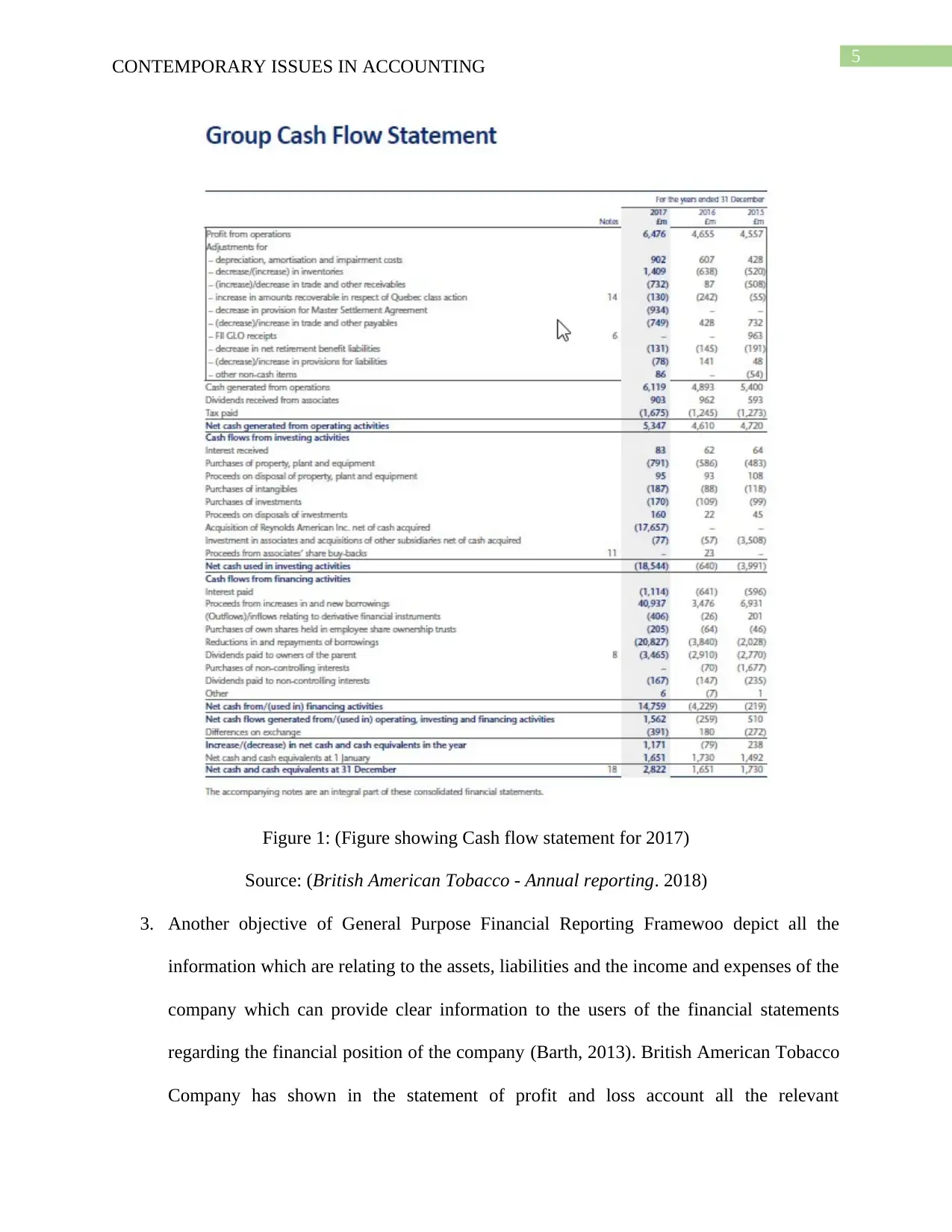

2. Another objective of General Purpose Financial reporting framework is to effectively

asses how much cash inflows can be generated by the business and what are the resources

are needed in future. As per the financial statements of the company, the business has

effectively anticipated certain expenses which the business will need to incur in 2018

which are pension payments for the people who have worked for the company in

Germany and Netherlands. Moreover, as per the notes to accounts of the company it is

also expected that the company will be taking long term loans for the business n 2018

which will result in inflow of cash. In addition to this the general purpose financial

reporting framework aims at providing all the relevant information about the cash inflows

and outflows of a business in the cash flow statement (May, 2013). The cash flow

statement of the company shows all the relevant information regarding the cash inflows

and outflows of British American Tobacco Company.

CONTEMPORARY ISSUES IN ACCOUNTING

reflected which can help the potential investors, lenders and creditors of the company to

take decisions regarding buying, selling or holding and similar other decisions

(Lawrence, 2013). In the case of British American Tobacco Company, the financial

reports of the company contain all the relevant information which can be of use to the

shareholders, lenders and other user of financial statements for the purpose of decision

making. The profit and loss account, balance sheet and cash flow statement are

effectively prepared which can provide the shareholders information regarding the overall

performance of the company.

2. Another objective of General Purpose Financial reporting framework is to effectively

asses how much cash inflows can be generated by the business and what are the resources

are needed in future. As per the financial statements of the company, the business has

effectively anticipated certain expenses which the business will need to incur in 2018

which are pension payments for the people who have worked for the company in

Germany and Netherlands. Moreover, as per the notes to accounts of the company it is

also expected that the company will be taking long term loans for the business n 2018

which will result in inflow of cash. In addition to this the general purpose financial

reporting framework aims at providing all the relevant information about the cash inflows

and outflows of a business in the cash flow statement (May, 2013). The cash flow

statement of the company shows all the relevant information regarding the cash inflows

and outflows of British American Tobacco Company.

5

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 1: (Figure showing Cash flow statement for 2017)

Source: (British American Tobacco - Annual reporting. 2018)

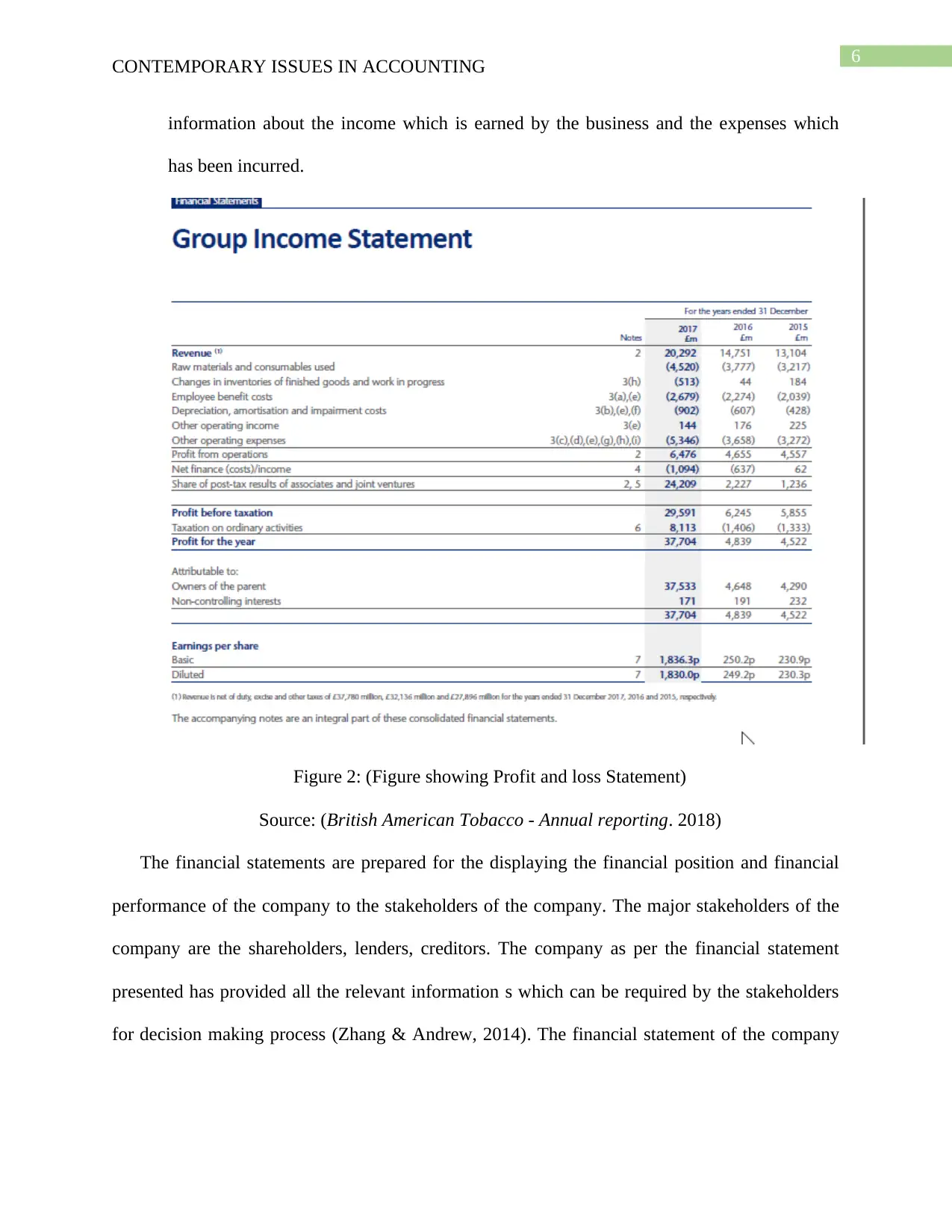

3. Another objective of General Purpose Financial Reporting Framewoo depict all the

information which are relating to the assets, liabilities and the income and expenses of the

company which can provide clear information to the users of the financial statements

regarding the financial position of the company (Barth, 2013). British American Tobacco

Company has shown in the statement of profit and loss account all the relevant

CONTEMPORARY ISSUES IN ACCOUNTING

Figure 1: (Figure showing Cash flow statement for 2017)

Source: (British American Tobacco - Annual reporting. 2018)

3. Another objective of General Purpose Financial Reporting Framewoo depict all the

information which are relating to the assets, liabilities and the income and expenses of the

company which can provide clear information to the users of the financial statements

regarding the financial position of the company (Barth, 2013). British American Tobacco

Company has shown in the statement of profit and loss account all the relevant

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

information about the income which is earned by the business and the expenses which

has been incurred.

Figure 2: (Figure showing Profit and loss Statement)

Source: (British American Tobacco - Annual reporting. 2018)

The financial statements are prepared for the displaying the financial position and financial

performance of the company to the stakeholders of the company. The major stakeholders of the

company are the shareholders, lenders, creditors. The company as per the financial statement

presented has provided all the relevant information s which can be required by the stakeholders

for decision making process (Zhang & Andrew, 2014). The financial statement of the company

CONTEMPORARY ISSUES IN ACCOUNTING

information about the income which is earned by the business and the expenses which

has been incurred.

Figure 2: (Figure showing Profit and loss Statement)

Source: (British American Tobacco - Annual reporting. 2018)

The financial statements are prepared for the displaying the financial position and financial

performance of the company to the stakeholders of the company. The major stakeholders of the

company are the shareholders, lenders, creditors. The company as per the financial statement

presented has provided all the relevant information s which can be required by the stakeholders

for decision making process (Zhang & Andrew, 2014). The financial statement of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

displays all the relevant information and the financial statement are also prepared following all

the relevant accounting standard and principles.

Recognition Criteria of Items of Financial Statement

The recognition criteria of the financial statement require recording of an item in the

financial statement of the company. Australian Accounting Standard Board (AASB) has issued

certain accounting standard which are to be followed for the purpose of recognition and

treatment of various items in the accounting statement. The various items which are of

significance and have been recognized by the company are discussed below:

1. Assets: The assets of the company are an important financial indicator which is shown in

the balance sheet of the company. The assets are further sub-divided into parts which are

namely current assets, fixed assets and intangible assets. The fixed assets of the company

as per the financial report of 2017 show that as a fixed asset the company has property,

plants and equipment which shows a figure of € 4,882 million. The fixed assets consist of

site where tobacco is processes, research and development activities and manufacturing

equipment. The assets are measured after deducting depreciation and impairment amount

of property, plant and equipment and also on intangible assets. Then there are the current

assets which are shown on a fair value basis such as inventories and other receivables.

The intangible assets of company are also shown in the balance sheet and the figure is

obtained by deducting amortization expenses.

2. Liabilities: The liabilities of the company are shown in the balance sheet and it comprises

of current liabilities and non-current liabilities. The current liabilities are made up of

short term borrowings, provisions, trade payables, retirement benefit plans and deferred

CONTEMPORARY ISSUES IN ACCOUNTING

displays all the relevant information and the financial statement are also prepared following all

the relevant accounting standard and principles.

Recognition Criteria of Items of Financial Statement

The recognition criteria of the financial statement require recording of an item in the

financial statement of the company. Australian Accounting Standard Board (AASB) has issued

certain accounting standard which are to be followed for the purpose of recognition and

treatment of various items in the accounting statement. The various items which are of

significance and have been recognized by the company are discussed below:

1. Assets: The assets of the company are an important financial indicator which is shown in

the balance sheet of the company. The assets are further sub-divided into parts which are

namely current assets, fixed assets and intangible assets. The fixed assets of the company

as per the financial report of 2017 show that as a fixed asset the company has property,

plants and equipment which shows a figure of € 4,882 million. The fixed assets consist of

site where tobacco is processes, research and development activities and manufacturing

equipment. The assets are measured after deducting depreciation and impairment amount

of property, plant and equipment and also on intangible assets. Then there are the current

assets which are shown on a fair value basis such as inventories and other receivables.

The intangible assets of company are also shown in the balance sheet and the figure is

obtained by deducting amortization expenses.

2. Liabilities: The liabilities of the company are shown in the balance sheet and it comprises

of current liabilities and non-current liabilities. The current liabilities are made up of

short term borrowings, provisions, trade payables, retirement benefit plans and deferred

8

CONTEMPORARY ISSUES IN ACCOUNTING

tax liabilities. The company has contingent liabilities which are not shown in the financial

statements and disclosed in the notes of accounts part.

3. Revenues: The revenues which the company has earned during the year has been

recorded and shown in the statement of profit and loss account of the company. The

activities which generates most amount of revenue for the company is from the sale of

cigarettes and other tobacco products.

4. Equity: The equity of the company comprises of equity shares and the shares which are

acquired by the company during mergers and acquisitions and also from subsidiaries.

5. Expenses: As per the principles of accounting, the expenses which are incurred by the

business are recorded in the statement of profit and loss account in order to display the

financial performance of the business and also get the net profit of the business.

Fundamental Qualitative Characteristics

There are two fundamental qualitative characteristics which are given discussed below on

the basis of the company:

1. Relevance: This principle states that the financial statements should include relevant

information in the financial statements which are of use to the shareholders of the

company. in the case of British American Tobacco plc, the company follows AASB, IAS

standard which makes the information contained in the financial statements relevant and

moreover the company also includes all the relevant items in the financial statements

which are further clarified in the notes to accounts (Macve, 2015).

2. Faithful representation: In order to follow such a purpose that the financial statements are

showing true and fair view or not the financial statements are audited annually. The

auditors of the company are KPMG which is an audit firm (Eierle & Schultze, 2013). The

CONTEMPORARY ISSUES IN ACCOUNTING

tax liabilities. The company has contingent liabilities which are not shown in the financial

statements and disclosed in the notes of accounts part.

3. Revenues: The revenues which the company has earned during the year has been

recorded and shown in the statement of profit and loss account of the company. The

activities which generates most amount of revenue for the company is from the sale of

cigarettes and other tobacco products.

4. Equity: The equity of the company comprises of equity shares and the shares which are

acquired by the company during mergers and acquisitions and also from subsidiaries.

5. Expenses: As per the principles of accounting, the expenses which are incurred by the

business are recorded in the statement of profit and loss account in order to display the

financial performance of the business and also get the net profit of the business.

Fundamental Qualitative Characteristics

There are two fundamental qualitative characteristics which are given discussed below on

the basis of the company:

1. Relevance: This principle states that the financial statements should include relevant

information in the financial statements which are of use to the shareholders of the

company. in the case of British American Tobacco plc, the company follows AASB, IAS

standard which makes the information contained in the financial statements relevant and

moreover the company also includes all the relevant items in the financial statements

which are further clarified in the notes to accounts (Macve, 2015).

2. Faithful representation: In order to follow such a purpose that the financial statements are

showing true and fair view or not the financial statements are audited annually. The

auditors of the company are KPMG which is an audit firm (Eierle & Schultze, 2013). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

auditor of the company confirms that the financial statements are showing true and fair

view.

Enhancing Qualitative Characteristics

The enhancing qualitative characteristics comprises of features which further improves the

financial statements which are given below:

1. Comparability: The financial statement results can be compared easily with the results of

previous years (Weil, Schipper & Francis, 2013). The company has provided significant

information which is related to previous year business performance which can be useful

for comparing the performance of the company.

2. Verifiability: This principle states that the books of accounts should be prepared in such a

way that it is verifiable by the stakeholders which can be done with the help of

explanations provided in the notes to accounts section of the annual reports (Edwards,

2013). In the case of British American Tobacco company proper notes to accounts are

given by the company.

3. Timeliness: The principle reflects the importance of time for publishing the financial

statements of the business so that it can be used by the users of financial statements.

4. Understandability: The financial statements are prepared for the users so that they are

able to interpret the financial information present in the financial statements and then

decisions based on the interpretation made on the same. This principle emphasis a

financial statement should be easily understandable by not only the users but also general

public.

CONTEMPORARY ISSUES IN ACCOUNTING

auditor of the company confirms that the financial statements are showing true and fair

view.

Enhancing Qualitative Characteristics

The enhancing qualitative characteristics comprises of features which further improves the

financial statements which are given below:

1. Comparability: The financial statement results can be compared easily with the results of

previous years (Weil, Schipper & Francis, 2013). The company has provided significant

information which is related to previous year business performance which can be useful

for comparing the performance of the company.

2. Verifiability: This principle states that the books of accounts should be prepared in such a

way that it is verifiable by the stakeholders which can be done with the help of

explanations provided in the notes to accounts section of the annual reports (Edwards,

2013). In the case of British American Tobacco company proper notes to accounts are

given by the company.

3. Timeliness: The principle reflects the importance of time for publishing the financial

statements of the business so that it can be used by the users of financial statements.

4. Understandability: The financial statements are prepared for the users so that they are

able to interpret the financial information present in the financial statements and then

decisions based on the interpretation made on the same. This principle emphasis a

financial statement should be easily understandable by not only the users but also general

public.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

Conclusion

The above analysis of the General purpose financial reporting frameworks makes it clear,

that the financial statements when prepared using the framework will display all the relevant

information. The framework which is discussed in the assignment helps the users to accurately

interpret the financial performance of the business from the financial statement. British

American Tobacco company follows the general-purpose framework and prepares its financial

statement in adherence to the principles stated. In addition to this, the financial statements are

prepared following all relevant principles and standards and conceptual framework which makes

the financial statements presentable and accurate.

CONTEMPORARY ISSUES IN ACCOUNTING

Conclusion

The above analysis of the General purpose financial reporting frameworks makes it clear,

that the financial statements when prepared using the framework will display all the relevant

information. The framework which is discussed in the assignment helps the users to accurately

interpret the financial performance of the business from the financial statement. British

American Tobacco company follows the general-purpose framework and prepares its financial

statement in adherence to the principles stated. In addition to this, the financial statements are

prepared following all relevant principles and standards and conceptual framework which makes

the financial statements presentable and accurate.

11

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Barth, M. E. (2013). Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), 331-352.

British American Tobacco - Annual reporting. (2018). Bat.com. Retrieved 6 April 2018, from

http://www.bat.com/annualreport

Collis, J., & Hussey, R. (2013). Business research: A practical guide for undergraduate and

postgraduate students. Palgrave macmillan.

Edwards, J. R. (2013). A history of financial accounting (RLE Accounting) (Vol. 29). Routledge.

Eierle, B., & Schultze, W. (2013). The role of management as a user of accounting information:

implications for standard setting.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Lawrence, A. (2013). Individual investors and financial disclosure. Journal of Accounting and

Economics, 56(1), 130-147.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

May, G. O. (2013). Financial accounting. Read Books Ltd.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

CONTEMPORARY ISSUES IN ACCOUNTING

Reference

Barth, M. E. (2013). Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), 331-352.

British American Tobacco - Annual reporting. (2018). Bat.com. Retrieved 6 April 2018, from

http://www.bat.com/annualreport

Collis, J., & Hussey, R. (2013). Business research: A practical guide for undergraduate and

postgraduate students. Palgrave macmillan.

Edwards, J. R. (2013). A history of financial accounting (RLE Accounting) (Vol. 29). Routledge.

Eierle, B., & Schultze, W. (2013). The role of management as a user of accounting information:

implications for standard setting.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial accounting.

Pearson Higher Education AU.

Lawrence, A. (2013). Individual investors and financial disclosure. Journal of Accounting and

Economics, 56(1), 130-147.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

May, G. O. (2013). Financial accounting. Read Books Ltd.

Weil, R. L., Schipper, K., & Francis, J. (2013). Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.