Financial Performance Analysis of British American Tobacco: Report

VerifiedAdded on 2023/01/19

|21

|4353

|91

Report

AI Summary

This project report provides a financial analysis of British American Tobacco (BAT) using ratio analysis. It examines liquidity ratios (current and quick ratios) and profitability ratios (gross profit, net profit, operating profit, and return on capital employed) for 2017 and 2018. The analysis reveals a decreasing liquidity position in 2018 compared to 2017, as evidenced by the current and quick ratios. The report also indicates an increasing gross profit ratio in 2018, suggesting improved efficiency in generating profit from sales, while the net profit ratio decreased, possibly due to reduced net profit. Furthermore, the operating profit ratio increased, indicating better operational profit generation. The report concludes with key findings and recommendations to enhance the company's performance. This report is a valuable resource for students seeking insights into financial statement analysis and ratio interpretation, available on Desklib.

Accounting and finance

analysis of a listed

company

analysis of a listed

company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

SUMMARY AND CONCLUSION..............................................................................................18

REFERENCES..............................................................................................................................20

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

SUMMARY AND CONCLUSION..............................................................................................18

REFERENCES..............................................................................................................................20

EXECUTIVE SUMMARY

The project report summarise about role of ratio analysis in order to make better analysis

of financial performance. Under the report, vital range of ratios are calculated and interpreted in

order to assess performance of chosen business entity listed in London stock exchange. As well

as further part of report abstracts about key findings and recommendations for company in order

to enhance the performance.

MAIN BODY

Ratio analysis- In this competitive environment, there are number of techniques that are used by

business entities in order to analyse monetary performance in an effective manner. The ratio

analysis technique is one of them. It can be defined as a kinds of approach in that wide number

of ratios are calculated and analysed in order to take crucial decision in a better way (Uchide and

Imanishi, 2016). By help of proper ratio analysis, it becomes easier for companies to get aware

about which aspects are needed to be improve and which aspects are strong. Under this

technique, the key ratios are profitability ratio, liquidity ratio and many more. Basically, in order

to analyse the financial performance of companies two years consecutive years ratios are

calculated and compared in a detailed manner. Herein, below the importance of ratio analysis

technique is demonstrated in such manner that is as follows:

This type of analysis is beneficial in order to make proper financial analysis.

In addition, the ratio analysis play a significant role in order to judge monetary soundness

of a business entity.

Another key benefit of ratio analysis is that it is useful for companies for making analysis

of operational efficiency of enterprises.

The ratio analysis makes enable to identifying the risk of business firms.

So these are some key benefits of ratio analysis technique for companies. In the aspect of this

project report a company has been chosen that is listed in London stock exchange. The name of

company is British American Tobacco which operates in manufacturing of tobacco products.

Overview of company- The British American Tobacco is a British multinational cigarette and

tobacco manufacturing company. Its headquarter is in London, United Kingdom. As per the

The project report summarise about role of ratio analysis in order to make better analysis

of financial performance. Under the report, vital range of ratios are calculated and interpreted in

order to assess performance of chosen business entity listed in London stock exchange. As well

as further part of report abstracts about key findings and recommendations for company in order

to enhance the performance.

MAIN BODY

Ratio analysis- In this competitive environment, there are number of techniques that are used by

business entities in order to analyse monetary performance in an effective manner. The ratio

analysis technique is one of them. It can be defined as a kinds of approach in that wide number

of ratios are calculated and analysed in order to take crucial decision in a better way (Uchide and

Imanishi, 2016). By help of proper ratio analysis, it becomes easier for companies to get aware

about which aspects are needed to be improve and which aspects are strong. Under this

technique, the key ratios are profitability ratio, liquidity ratio and many more. Basically, in order

to analyse the financial performance of companies two years consecutive years ratios are

calculated and compared in a detailed manner. Herein, below the importance of ratio analysis

technique is demonstrated in such manner that is as follows:

This type of analysis is beneficial in order to make proper financial analysis.

In addition, the ratio analysis play a significant role in order to judge monetary soundness

of a business entity.

Another key benefit of ratio analysis is that it is useful for companies for making analysis

of operational efficiency of enterprises.

The ratio analysis makes enable to identifying the risk of business firms.

So these are some key benefits of ratio analysis technique for companies. In the aspect of this

project report a company has been chosen that is listed in London stock exchange. The name of

company is British American Tobacco which operates in manufacturing of tobacco products.

Overview of company- The British American Tobacco is a British multinational cigarette and

tobacco manufacturing company. Its headquarter is in London, United Kingdom. As per the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial report of year 2012, this company was world's second largest cigarette manufacturer.

The company operates in more then 180 nations all around the world. The company was founded

by Imperial brands and James Buchanan Duke (About British American Tobacco plc, 2019). As

per the financial information of year 2018, there were more then 55000 employees in different

branches of this company. Apart from it, some key information about this company are

mentioned below in such manner:

Stock price – 3009.50 GBX (+28.50, +0.96%) as on 25th of November, 2019.

Revenues- £2449.2 crores GBP as per financial year 2018.

Chief executive officer- Jack Bowles.

Types of ratios:

1. Liquidity ratio- This can be defined as a kinds of ratio in that defines about businesses'

efficiency in order to meet obligations when they become due (Lakshmi, Martin and Venkatesan,

2015). In broad manner, this is a type of ratio which assess business entities capability in order to

define whether they are able to make payment of short term debts or not. In the aspect of above

chosen company, British American Tobacco their accountant computes this ratio with an aim of

determining efficiency of paying short term debts. There are mainly two types of liquidity ratios

that are mentioned below in such manner:

Current ratio- It is a type of ratio which indicates the relation of a business entity current

assets to its current liabilities. This ratio is one of they key ratio for analysing liquidity

position of companies. Under it, this is considered that a higher current ratio is better for

companies as compare to a smaller one. The ideal ratio is 2 : 1 that states that companies

should have double amount of current assets for making payment of short term debts or

current liabilities. There is a particular formula which is used to compute current ratio

that is as follows: Current ratio = Current assets / current liabilities. In the context of

British American Tobacco company, the current ratio is calculated and analysed in such

manner:

2017 2018

Current assets £13966 £12655

Current liabilities £15544 £16329

The company operates in more then 180 nations all around the world. The company was founded

by Imperial brands and James Buchanan Duke (About British American Tobacco plc, 2019). As

per the financial information of year 2018, there were more then 55000 employees in different

branches of this company. Apart from it, some key information about this company are

mentioned below in such manner:

Stock price – 3009.50 GBX (+28.50, +0.96%) as on 25th of November, 2019.

Revenues- £2449.2 crores GBP as per financial year 2018.

Chief executive officer- Jack Bowles.

Types of ratios:

1. Liquidity ratio- This can be defined as a kinds of ratio in that defines about businesses'

efficiency in order to meet obligations when they become due (Lakshmi, Martin and Venkatesan,

2015). In broad manner, this is a type of ratio which assess business entities capability in order to

define whether they are able to make payment of short term debts or not. In the aspect of above

chosen company, British American Tobacco their accountant computes this ratio with an aim of

determining efficiency of paying short term debts. There are mainly two types of liquidity ratios

that are mentioned below in such manner:

Current ratio- It is a type of ratio which indicates the relation of a business entity current

assets to its current liabilities. This ratio is one of they key ratio for analysing liquidity

position of companies. Under it, this is considered that a higher current ratio is better for

companies as compare to a smaller one. The ideal ratio is 2 : 1 that states that companies

should have double amount of current assets for making payment of short term debts or

current liabilities. There is a particular formula which is used to compute current ratio

that is as follows: Current ratio = Current assets / current liabilities. In the context of

British American Tobacco company, the current ratio is calculated and analysed in such

manner:

2017 2018

Current assets £13966 £12655

Current liabilities £15544 £16329

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

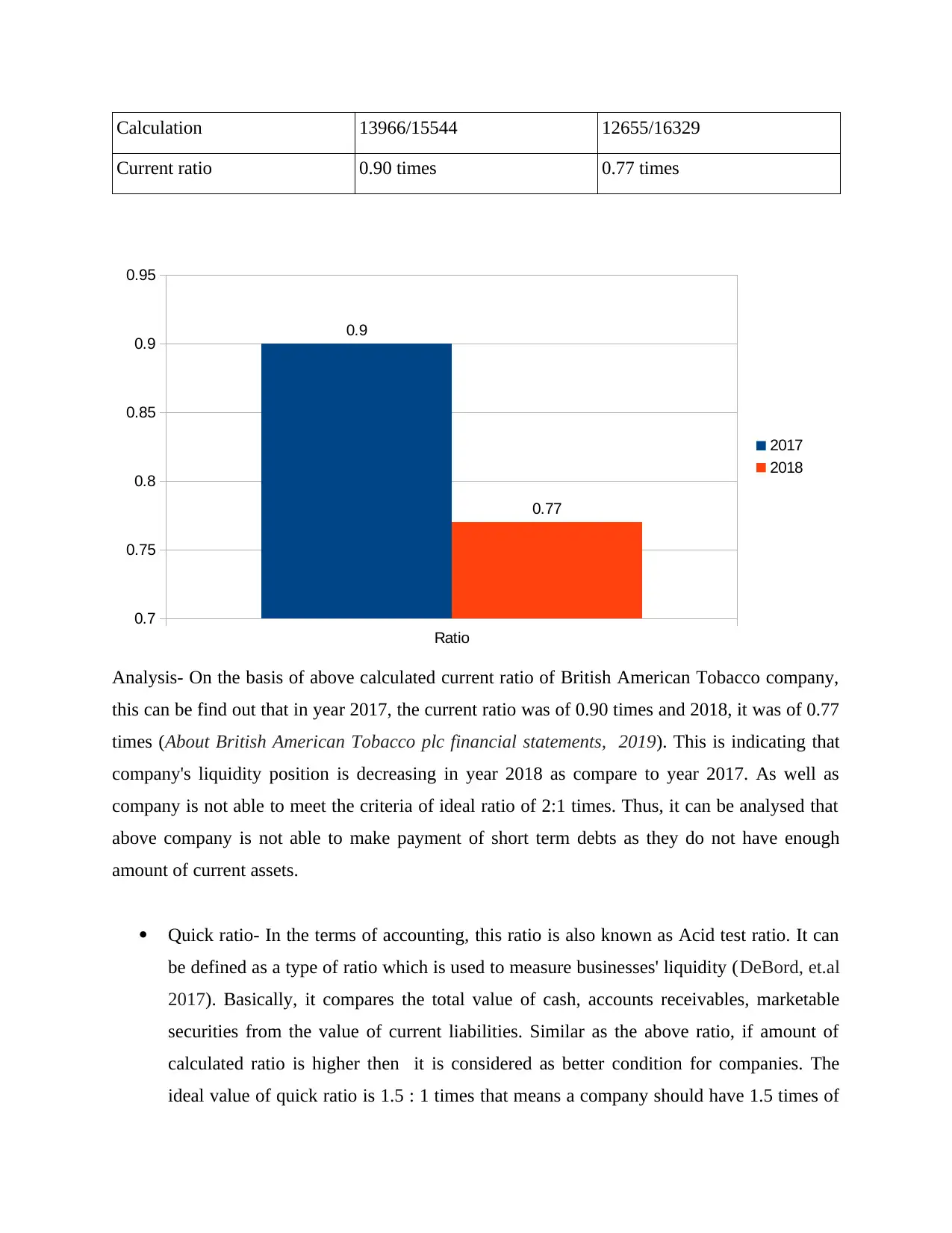

Calculation 13966/15544 12655/16329

Current ratio 0.90 times 0.77 times

Ratio

0.7

0.75

0.8

0.85

0.9

0.95

0.9

0.77

2017

2018

Analysis- On the basis of above calculated current ratio of British American Tobacco company,

this can be find out that in year 2017, the current ratio was of 0.90 times and 2018, it was of 0.77

times (About British American Tobacco plc financial statements, 2019). This is indicating that

company's liquidity position is decreasing in year 2018 as compare to year 2017. As well as

company is not able to meet the criteria of ideal ratio of 2:1 times. Thus, it can be analysed that

above company is not able to make payment of short term debts as they do not have enough

amount of current assets.

Quick ratio- In the terms of accounting, this ratio is also known as Acid test ratio. It can

be defined as a type of ratio which is used to measure businesses' liquidity (DeBord, et.al

2017). Basically, it compares the total value of cash, accounts receivables, marketable

securities from the value of current liabilities. Similar as the above ratio, if amount of

calculated ratio is higher then it is considered as better condition for companies. The

ideal value of quick ratio is 1.5 : 1 times that means a company should have 1.5 times of

Current ratio 0.90 times 0.77 times

Ratio

0.7

0.75

0.8

0.85

0.9

0.95

0.9

0.77

2017

2018

Analysis- On the basis of above calculated current ratio of British American Tobacco company,

this can be find out that in year 2017, the current ratio was of 0.90 times and 2018, it was of 0.77

times (About British American Tobacco plc financial statements, 2019). This is indicating that

company's liquidity position is decreasing in year 2018 as compare to year 2017. As well as

company is not able to meet the criteria of ideal ratio of 2:1 times. Thus, it can be analysed that

above company is not able to make payment of short term debts as they do not have enough

amount of current assets.

Quick ratio- In the terms of accounting, this ratio is also known as Acid test ratio. It can

be defined as a type of ratio which is used to measure businesses' liquidity (DeBord, et.al

2017). Basically, it compares the total value of cash, accounts receivables, marketable

securities from the value of current liabilities. Similar as the above ratio, if amount of

calculated ratio is higher then it is considered as better condition for companies. The

ideal value of quick ratio is 1.5 : 1 times that means a company should have 1.5 times of

assets in order to make payment of 1 time of current liabilities. This ratio is calculated by

a particular formula which as: Quick ratio = Quick assets – Current liabilities. In the

aspect of above company, this ratio is calculated and analysed for financial year 2017-18

that is as follows:

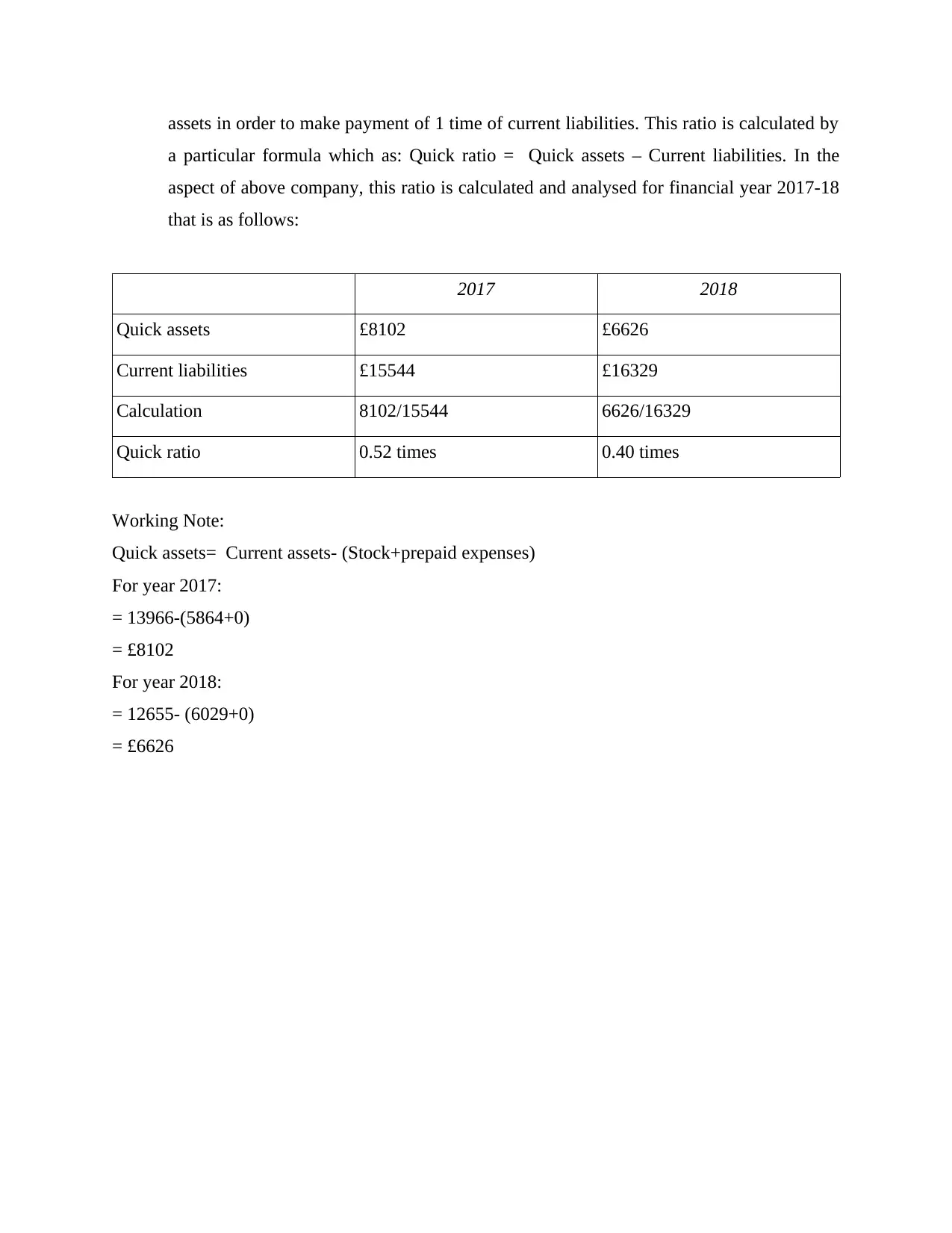

2017 2018

Quick assets £8102 £6626

Current liabilities £15544 £16329

Calculation 8102/15544 6626/16329

Quick ratio 0.52 times 0.40 times

Working Note:

Quick assets= Current assets- (Stock+prepaid expenses)

For year 2017:

= 13966-(5864+0)

= £8102

For year 2018:

= 12655- (6029+0)

= £6626

a particular formula which as: Quick ratio = Quick assets – Current liabilities. In the

aspect of above company, this ratio is calculated and analysed for financial year 2017-18

that is as follows:

2017 2018

Quick assets £8102 £6626

Current liabilities £15544 £16329

Calculation 8102/15544 6626/16329

Quick ratio 0.52 times 0.40 times

Working Note:

Quick assets= Current assets- (Stock+prepaid expenses)

For year 2017:

= 13966-(5864+0)

= £8102

For year 2018:

= 12655- (6029+0)

= £6626

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ratio

0

0.1

0.2

0.3

0.4

0.5

0.6

0.52

0.4

2017

2018

Analysis- On the basis of above computed ratio and presented diagram, this can be analysed that

chosen company's quick ratio is decreasing in significant manner during year 2017-18. Such as

in year 2017 it was of 0.52 times that decreased by 23.07% and became of 0.40 times. In both of

the year, company is not able to meet the criteria of ideal quick ratio that is of 1.5 : 1 times.

Hence, this can be analysed that company does not have enough value of current assets in order

to meet the obligations of paying short term debts.

2. Profitability ratio- This can be defined as a kinds of ratio which is calculated by companies in

order to determine efficiency to generate income by making expenses on different kinds of

operations and activities (Rashmi, Shree and Singh, 2017). It is being calculated by help of

prepared income statement of business entities. There are different types of ratios which are

covered under profitability ratio and some of them are mentioned below in such manner:

Gross profit ratio- It is a type of ratio which indicates the relation between gross profit

and net sales for a particular time period. In order to compute this ratio, there is a

particular formula that is as follows: Gross profit/ Net sales * 100. Eventually, this ratio

is measured in form of percentage (%). Higher gross profit ratio indicates better financial

position of companies. In the aspect of above British American Tobacco company, this

ratio is calculated and analysed for year 2017-18 that is as follows:

0

0.1

0.2

0.3

0.4

0.5

0.6

0.52

0.4

2017

2018

Analysis- On the basis of above computed ratio and presented diagram, this can be analysed that

chosen company's quick ratio is decreasing in significant manner during year 2017-18. Such as

in year 2017 it was of 0.52 times that decreased by 23.07% and became of 0.40 times. In both of

the year, company is not able to meet the criteria of ideal quick ratio that is of 1.5 : 1 times.

Hence, this can be analysed that company does not have enough value of current assets in order

to meet the obligations of paying short term debts.

2. Profitability ratio- This can be defined as a kinds of ratio which is calculated by companies in

order to determine efficiency to generate income by making expenses on different kinds of

operations and activities (Rashmi, Shree and Singh, 2017). It is being calculated by help of

prepared income statement of business entities. There are different types of ratios which are

covered under profitability ratio and some of them are mentioned below in such manner:

Gross profit ratio- It is a type of ratio which indicates the relation between gross profit

and net sales for a particular time period. In order to compute this ratio, there is a

particular formula that is as follows: Gross profit/ Net sales * 100. Eventually, this ratio

is measured in form of percentage (%). Higher gross profit ratio indicates better financial

position of companies. In the aspect of above British American Tobacco company, this

ratio is calculated and analysed for year 2017-18 that is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

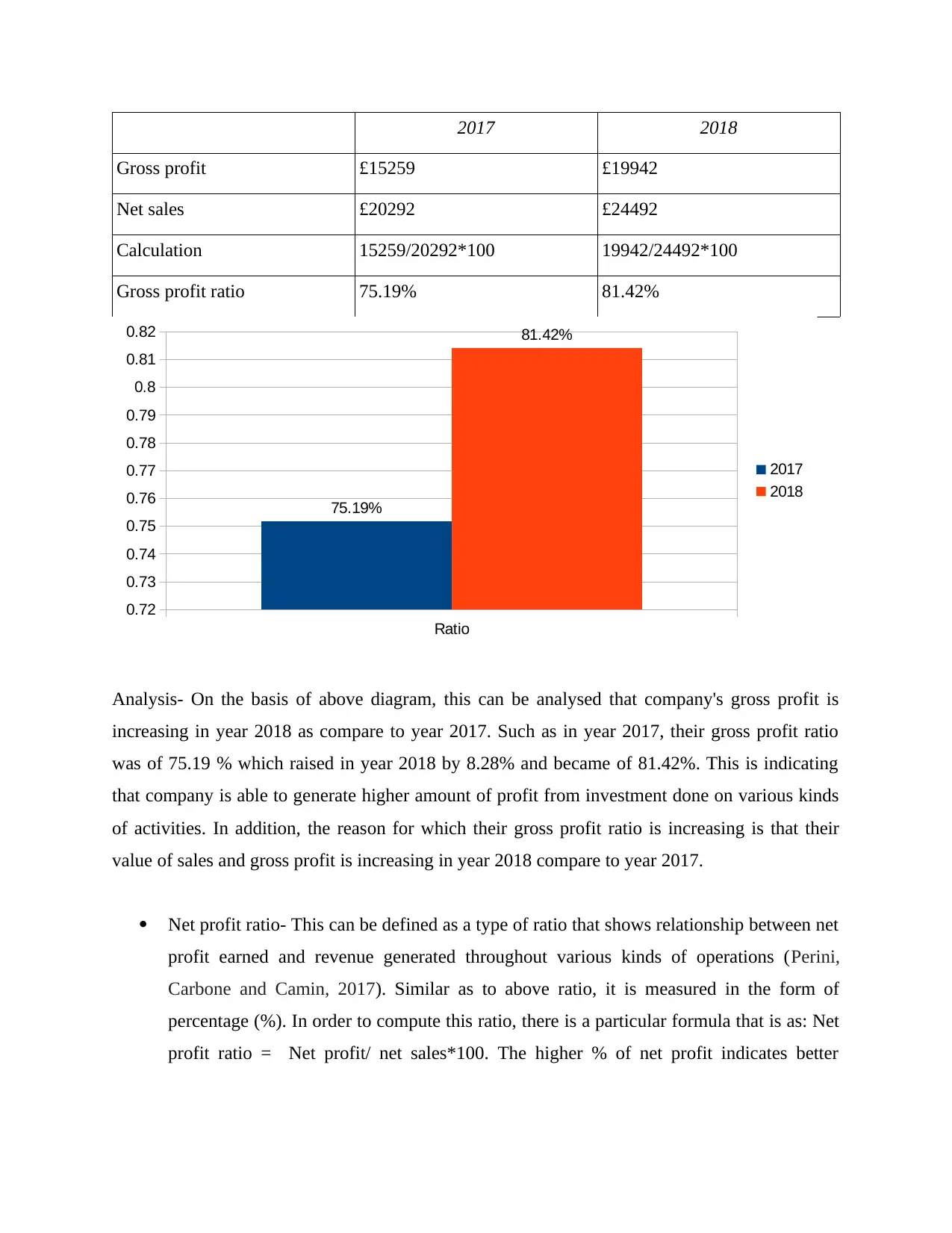

2017 2018

Gross profit £15259 £19942

Net sales £20292 £24492

Calculation 15259/20292*100 19942/24492*100

Gross profit ratio 75.19% 81.42%

Ratio

0.72

0.73

0.74

0.75

0.76

0.77

0.78

0.79

0.8

0.81

0.82

75.19%

81.42%

2017

2018

Analysis- On the basis of above diagram, this can be analysed that company's gross profit is

increasing in year 2018 as compare to year 2017. Such as in year 2017, their gross profit ratio

was of 75.19 % which raised in year 2018 by 8.28% and became of 81.42%. This is indicating

that company is able to generate higher amount of profit from investment done on various kinds

of activities. In addition, the reason for which their gross profit ratio is increasing is that their

value of sales and gross profit is increasing in year 2018 compare to year 2017.

Net profit ratio- This can be defined as a type of ratio that shows relationship between net

profit earned and revenue generated throughout various kinds of operations (Perini,

Carbone and Camin, 2017). Similar as to above ratio, it is measured in the form of

percentage (%). In order to compute this ratio, there is a particular formula that is as: Net

profit ratio = Net profit/ net sales*100. The higher % of net profit indicates better

Gross profit £15259 £19942

Net sales £20292 £24492

Calculation 15259/20292*100 19942/24492*100

Gross profit ratio 75.19% 81.42%

Ratio

0.72

0.73

0.74

0.75

0.76

0.77

0.78

0.79

0.8

0.81

0.82

75.19%

81.42%

2017

2018

Analysis- On the basis of above diagram, this can be analysed that company's gross profit is

increasing in year 2018 as compare to year 2017. Such as in year 2017, their gross profit ratio

was of 75.19 % which raised in year 2018 by 8.28% and became of 81.42%. This is indicating

that company is able to generate higher amount of profit from investment done on various kinds

of activities. In addition, the reason for which their gross profit ratio is increasing is that their

value of sales and gross profit is increasing in year 2018 compare to year 2017.

Net profit ratio- This can be defined as a type of ratio that shows relationship between net

profit earned and revenue generated throughout various kinds of operations (Perini,

Carbone and Camin, 2017). Similar as to above ratio, it is measured in the form of

percentage (%). In order to compute this ratio, there is a particular formula that is as: Net

profit ratio = Net profit/ net sales*100. The higher % of net profit indicates better

financial position of companies. In the aspect of above company, the net profit margin is

calculated in such manner:

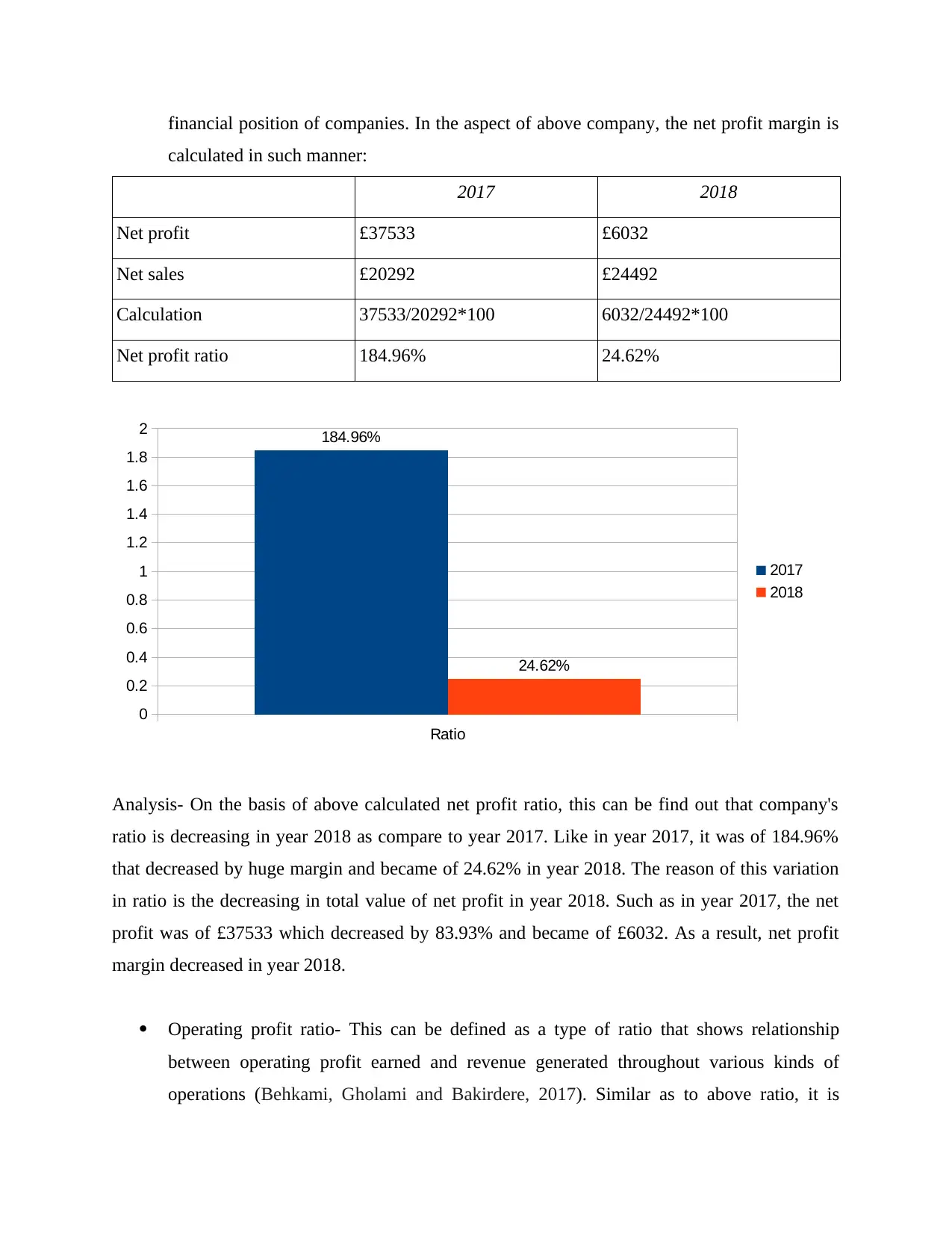

2017 2018

Net profit £37533 £6032

Net sales £20292 £24492

Calculation 37533/20292*100 6032/24492*100

Net profit ratio 184.96% 24.62%

Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2 184.96%

24.62%

2017

2018

Analysis- On the basis of above calculated net profit ratio, this can be find out that company's

ratio is decreasing in year 2018 as compare to year 2017. Like in year 2017, it was of 184.96%

that decreased by huge margin and became of 24.62% in year 2018. The reason of this variation

in ratio is the decreasing in total value of net profit in year 2018. Such as in year 2017, the net

profit was of £37533 which decreased by 83.93% and became of £6032. As a result, net profit

margin decreased in year 2018.

Operating profit ratio- This can be defined as a type of ratio that shows relationship

between operating profit earned and revenue generated throughout various kinds of

operations (Behkami, Gholami and Bakirdere, 2017). Similar as to above ratio, it is

calculated in such manner:

2017 2018

Net profit £37533 £6032

Net sales £20292 £24492

Calculation 37533/20292*100 6032/24492*100

Net profit ratio 184.96% 24.62%

Ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2 184.96%

24.62%

2017

2018

Analysis- On the basis of above calculated net profit ratio, this can be find out that company's

ratio is decreasing in year 2018 as compare to year 2017. Like in year 2017, it was of 184.96%

that decreased by huge margin and became of 24.62% in year 2018. The reason of this variation

in ratio is the decreasing in total value of net profit in year 2018. Such as in year 2017, the net

profit was of £37533 which decreased by 83.93% and became of £6032. As a result, net profit

margin decreased in year 2018.

Operating profit ratio- This can be defined as a type of ratio that shows relationship

between operating profit earned and revenue generated throughout various kinds of

operations (Behkami, Gholami and Bakirdere, 2017). Similar as to above ratio, it is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

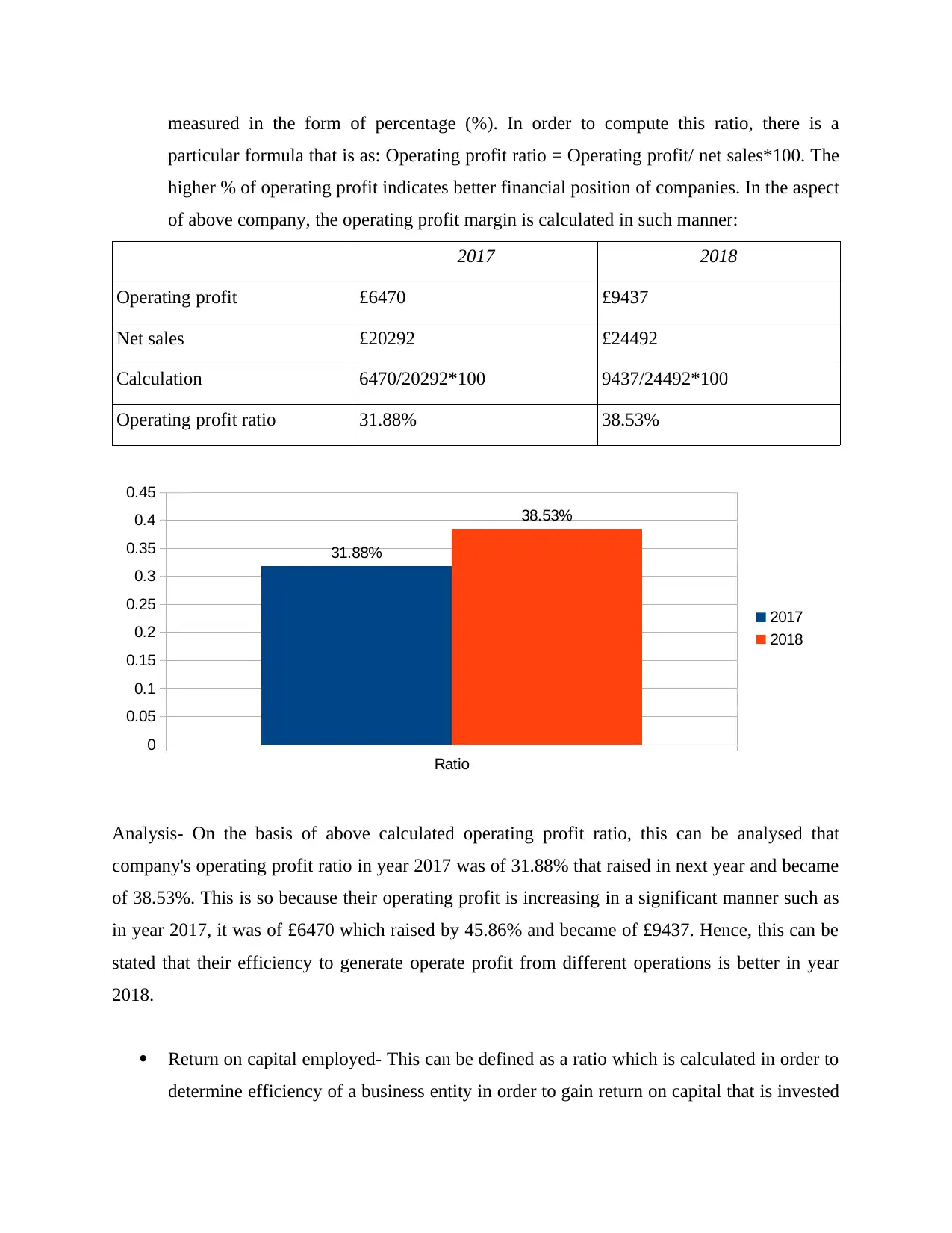

measured in the form of percentage (%). In order to compute this ratio, there is a

particular formula that is as: Operating profit ratio = Operating profit/ net sales*100. The

higher % of operating profit indicates better financial position of companies. In the aspect

of above company, the operating profit margin is calculated in such manner:

2017 2018

Operating profit £6470 £9437

Net sales £20292 £24492

Calculation 6470/20292*100 9437/24492*100

Operating profit ratio 31.88% 38.53%

Ratio

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

31.88%

38.53%

2017

2018

Analysis- On the basis of above calculated operating profit ratio, this can be analysed that

company's operating profit ratio in year 2017 was of 31.88% that raised in next year and became

of 38.53%. This is so because their operating profit is increasing in a significant manner such as

in year 2017, it was of £6470 which raised by 45.86% and became of £9437. Hence, this can be

stated that their efficiency to generate operate profit from different operations is better in year

2018.

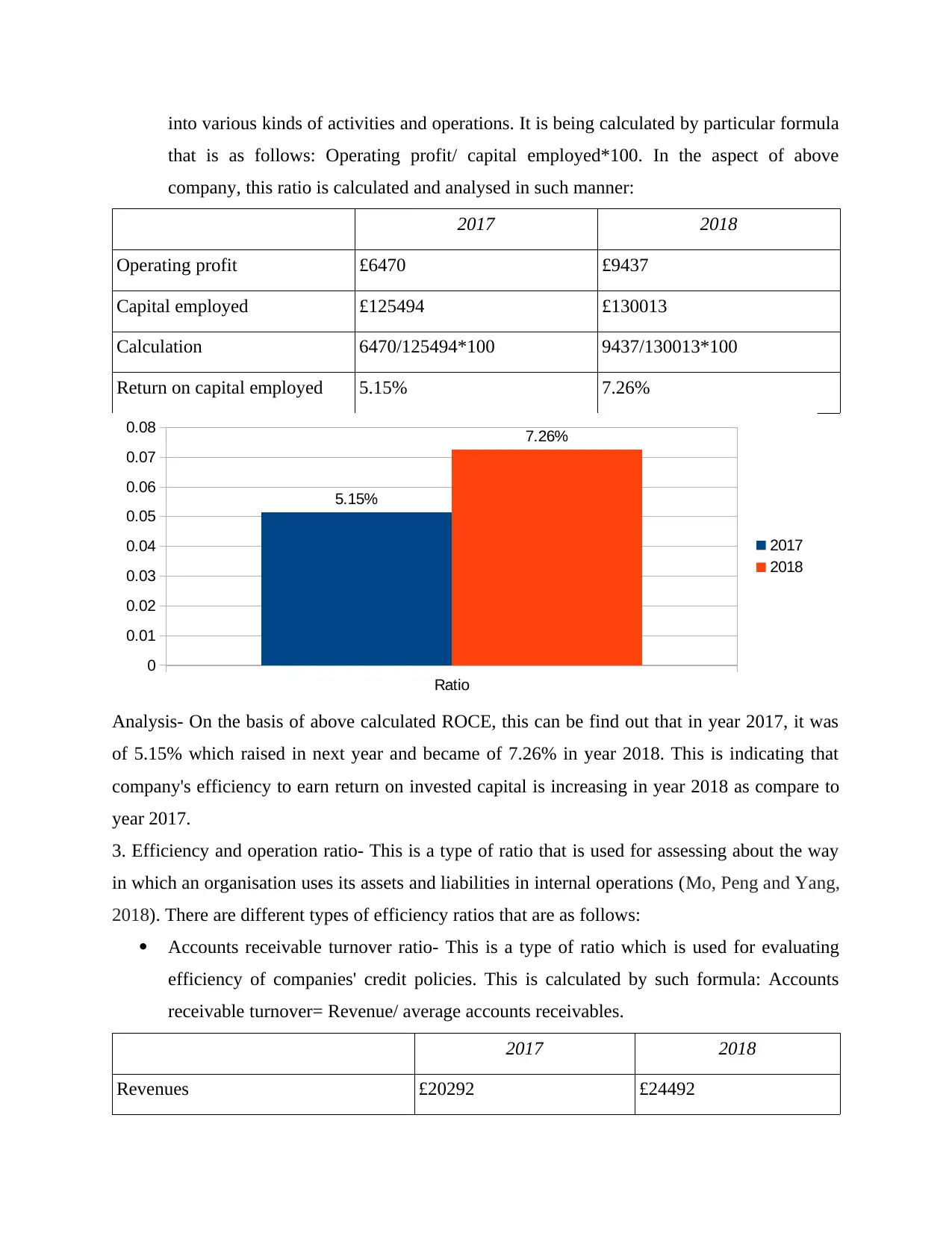

Return on capital employed- This can be defined as a ratio which is calculated in order to

determine efficiency of a business entity in order to gain return on capital that is invested

particular formula that is as: Operating profit ratio = Operating profit/ net sales*100. The

higher % of operating profit indicates better financial position of companies. In the aspect

of above company, the operating profit margin is calculated in such manner:

2017 2018

Operating profit £6470 £9437

Net sales £20292 £24492

Calculation 6470/20292*100 9437/24492*100

Operating profit ratio 31.88% 38.53%

Ratio

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

31.88%

38.53%

2017

2018

Analysis- On the basis of above calculated operating profit ratio, this can be analysed that

company's operating profit ratio in year 2017 was of 31.88% that raised in next year and became

of 38.53%. This is so because their operating profit is increasing in a significant manner such as

in year 2017, it was of £6470 which raised by 45.86% and became of £9437. Hence, this can be

stated that their efficiency to generate operate profit from different operations is better in year

2018.

Return on capital employed- This can be defined as a ratio which is calculated in order to

determine efficiency of a business entity in order to gain return on capital that is invested

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

into various kinds of activities and operations. It is being calculated by particular formula

that is as follows: Operating profit/ capital employed*100. In the aspect of above

company, this ratio is calculated and analysed in such manner:

2017 2018

Operating profit £6470 £9437

Capital employed £125494 £130013

Calculation 6470/125494*100 9437/130013*100

Return on capital employed 5.15% 7.26%

Ratio

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

5.15%

7.26%

2017

2018

Analysis- On the basis of above calculated ROCE, this can be find out that in year 2017, it was

of 5.15% which raised in next year and became of 7.26% in year 2018. This is indicating that

company's efficiency to earn return on invested capital is increasing in year 2018 as compare to

year 2017.

3. Efficiency and operation ratio- This is a type of ratio that is used for assessing about the way

in which an organisation uses its assets and liabilities in internal operations (Mo, Peng and Yang,

2018). There are different types of efficiency ratios that are as follows:

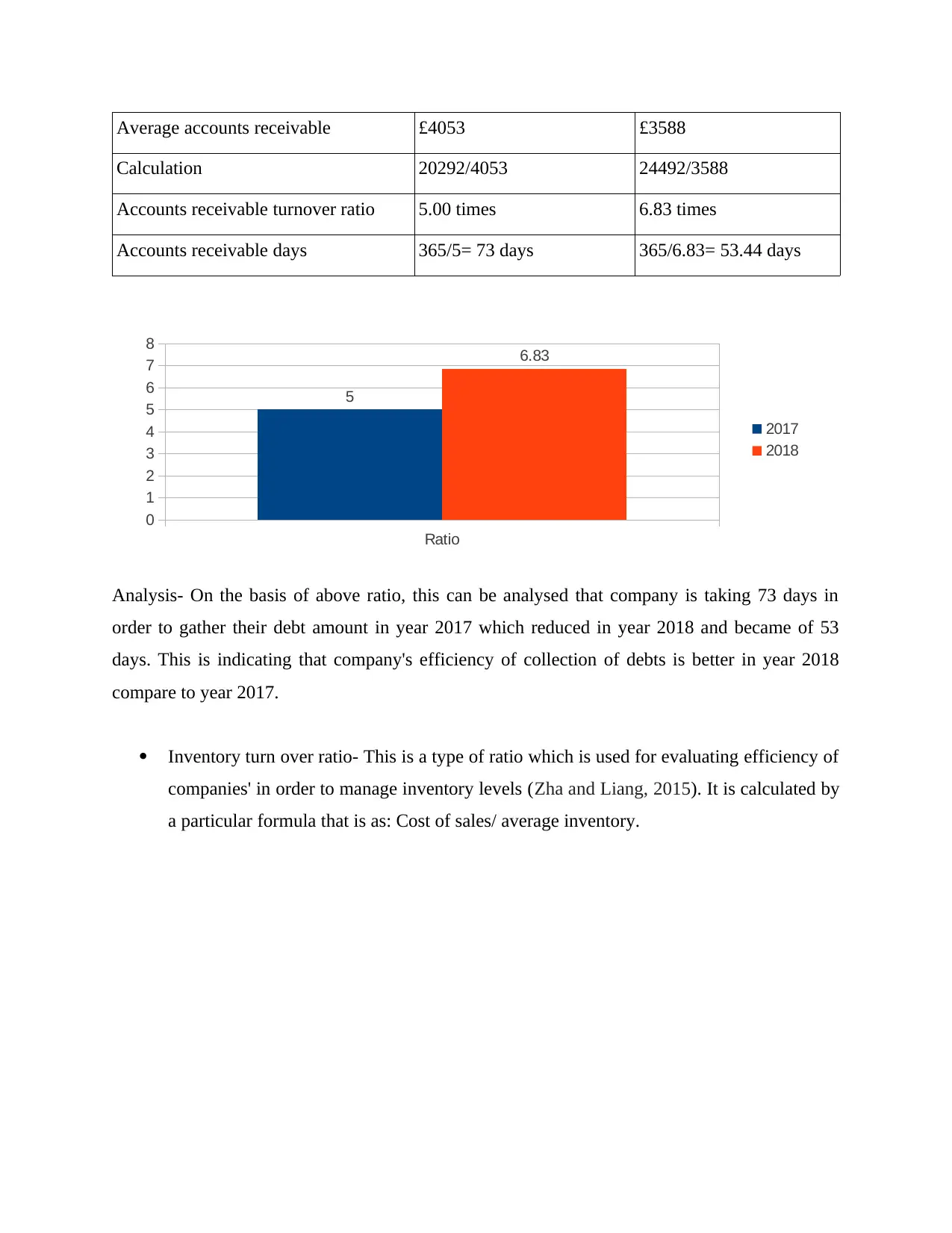

Accounts receivable turnover ratio- This is a type of ratio which is used for evaluating

efficiency of companies' credit policies. This is calculated by such formula: Accounts

receivable turnover= Revenue/ average accounts receivables.

2017 2018

Revenues £20292 £24492

that is as follows: Operating profit/ capital employed*100. In the aspect of above

company, this ratio is calculated and analysed in such manner:

2017 2018

Operating profit £6470 £9437

Capital employed £125494 £130013

Calculation 6470/125494*100 9437/130013*100

Return on capital employed 5.15% 7.26%

Ratio

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

5.15%

7.26%

2017

2018

Analysis- On the basis of above calculated ROCE, this can be find out that in year 2017, it was

of 5.15% which raised in next year and became of 7.26% in year 2018. This is indicating that

company's efficiency to earn return on invested capital is increasing in year 2018 as compare to

year 2017.

3. Efficiency and operation ratio- This is a type of ratio that is used for assessing about the way

in which an organisation uses its assets and liabilities in internal operations (Mo, Peng and Yang,

2018). There are different types of efficiency ratios that are as follows:

Accounts receivable turnover ratio- This is a type of ratio which is used for evaluating

efficiency of companies' credit policies. This is calculated by such formula: Accounts

receivable turnover= Revenue/ average accounts receivables.

2017 2018

Revenues £20292 £24492

Average accounts receivable £4053 £3588

Calculation 20292/4053 24492/3588

Accounts receivable turnover ratio 5.00 times 6.83 times

Accounts receivable days 365/5= 73 days 365/6.83= 53.44 days

Ratio

0

1

2

3

4

5

6

7

8

5

6.83

2017

2018

Analysis- On the basis of above ratio, this can be analysed that company is taking 73 days in

order to gather their debt amount in year 2017 which reduced in year 2018 and became of 53

days. This is indicating that company's efficiency of collection of debts is better in year 2018

compare to year 2017.

Inventory turn over ratio- This is a type of ratio which is used for evaluating efficiency of

companies' in order to manage inventory levels (Zha and Liang, 2015). It is calculated by

a particular formula that is as: Cost of sales/ average inventory.

Calculation 20292/4053 24492/3588

Accounts receivable turnover ratio 5.00 times 6.83 times

Accounts receivable days 365/5= 73 days 365/6.83= 53.44 days

Ratio

0

1

2

3

4

5

6

7

8

5

6.83

2017

2018

Analysis- On the basis of above ratio, this can be analysed that company is taking 73 days in

order to gather their debt amount in year 2017 which reduced in year 2018 and became of 53

days. This is indicating that company's efficiency of collection of debts is better in year 2018

compare to year 2017.

Inventory turn over ratio- This is a type of ratio which is used for evaluating efficiency of

companies' in order to manage inventory levels (Zha and Liang, 2015). It is calculated by

a particular formula that is as: Cost of sales/ average inventory.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.