Directors Report: Management Accounting for British American Tobacco

VerifiedAdded on 2023/04/21

|12

|2683

|482

Report

AI Summary

This report serves as a Directors Report, focusing on management accounting principles and their application within British American Tobacco (BAT). It begins with an introduction to management accounting, defining its importance and various techniques, including financial planning, standard costing, marginal costing, and analysis of financial statements. The report then delves into the practical application of accounting techniques, specifically absorption costing and contribution costing, providing detailed cost analyses and income statements for two BAT products. A key aspect is the interpretation of findings from these techniques, highlighting their roles in decision-making. Furthermore, the report proposes future strategies for BAT, such as product diversification, predicting future demands, risk management, and innovation, to maintain market leadership. Finally, the conclusion emphasizes the crucial role of management accounting in providing information for effective decision-making and the importance of coordination between managers and management accountants.

BAT DIRECTORS REPORT 1

MANAGEMENT REPORT FOR THE DIRECTOR

BY (NAME)

Name

Instructor

Institution

Date

MANAGEMENT REPORT FOR THE DIRECTOR

BY (NAME)

Name

Instructor

Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BAT DIRECTORS REPORT 2

Table of Contents

Introduction......................................................................................................................................3

Importance of management accounting.......................................................................................3

Management accounting techniques................................................................................................4

Financial planning........................................................................................................................4

Standard costing...........................................................................................................................4

Costing using Marginal technique...............................................................................................4

Historical cost accounting............................................................................................................4

Analysis of financial statements..................................................................................................4

Application of accounting techniques.............................................................................................5

Absorption costing.......................................................................................................................5

Contribution costing technique....................................................................................................6

Interpretation of the findings...........................................................................................................7

Future strategies for BAT................................................................................................................7

Product diversification.................................................................................................................8

Predict future demands.................................................................................................................8

Identify and manage risks............................................................................................................8

Innovation....................................................................................................................................8

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

Table of Contents

Introduction......................................................................................................................................3

Importance of management accounting.......................................................................................3

Management accounting techniques................................................................................................4

Financial planning........................................................................................................................4

Standard costing...........................................................................................................................4

Costing using Marginal technique...............................................................................................4

Historical cost accounting............................................................................................................4

Analysis of financial statements..................................................................................................4

Application of accounting techniques.............................................................................................5

Absorption costing.......................................................................................................................5

Contribution costing technique....................................................................................................6

Interpretation of the findings...........................................................................................................7

Future strategies for BAT................................................................................................................7

Product diversification.................................................................................................................8

Predict future demands.................................................................................................................8

Identify and manage risks............................................................................................................8

Innovation....................................................................................................................................8

Conclusion.......................................................................................................................................8

References......................................................................................................................................10

BAT DIRECTORS REPORT 3

Introduction

British American Tobacco was founded in the year 1902. It came into existence

following a joint venture between the then Imperial Tobacco Company and the United States

American Tobacco Company. The two companies agreed to join hands and reach out to other

territories. Since then, British American Tobacco has been the leading multination cigarette and

tobacco producing company with its head offices located in London. British American Tobacco

is also said to be the largest tobacco company in the world.

Definitions

Management accounting can be defined as an art of identifying, measuring, analyzing,

interpreting and communicating accurate and timely financial or statistical information to

managers with an aim of helping them to make decisions (Drury & Drury, 2013). This definition as

according to Drury.

According to (Maryanne, et al., 2006) management accounting is defined as providing

accounting information in a manner that will help the managers make decision and strategize.

As per the accounting association of America, Management accounting is defined as the

technique for proper laying down of strategies for better future performance (Drury, 2015)

India’s Chartered Institute for Accountants puts management accounting as those methods and

channels which help management to make decisions (Sinha & Vinayakam, n.d.)

Importance of management accounting (Drury & Drury, 2013)

Management accounting will help British American Tobacco in forecasting. Management

accountant will provide sufficient information to the managers on whether to invest on more

assets, to acquire more market or even to increase on the production by buying another

organization. Managers will be able to make decisions of whether to buy or produce raw

Introduction

British American Tobacco was founded in the year 1902. It came into existence

following a joint venture between the then Imperial Tobacco Company and the United States

American Tobacco Company. The two companies agreed to join hands and reach out to other

territories. Since then, British American Tobacco has been the leading multination cigarette and

tobacco producing company with its head offices located in London. British American Tobacco

is also said to be the largest tobacco company in the world.

Definitions

Management accounting can be defined as an art of identifying, measuring, analyzing,

interpreting and communicating accurate and timely financial or statistical information to

managers with an aim of helping them to make decisions (Drury & Drury, 2013). This definition as

according to Drury.

According to (Maryanne, et al., 2006) management accounting is defined as providing

accounting information in a manner that will help the managers make decision and strategize.

As per the accounting association of America, Management accounting is defined as the

technique for proper laying down of strategies for better future performance (Drury, 2015)

India’s Chartered Institute for Accountants puts management accounting as those methods and

channels which help management to make decisions (Sinha & Vinayakam, n.d.)

Importance of management accounting (Drury & Drury, 2013)

Management accounting will help British American Tobacco in forecasting. Management

accountant will provide sufficient information to the managers on whether to invest on more

assets, to acquire more market or even to increase on the production by buying another

organization. Managers will be able to make decisions of whether to buy or produce raw

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BAT DIRECTORS REPORT 4

materials. Management accounting will provide information on the cheaper alternative between

producing and buying and then the managers will be expected to opt for the alternative that

maximizes organizations revenue.

Management accounting will help to forecast cash flows. For British American Tobacco

group to be able to fund its future activities there must be sufficient working capital to procure

current assets and to cater for operating expenses. Management accountants are able to use

accounting tools to predict future cash flows and advise the managers on how to come up with

accurate budgets to make proper use of the available resources.

Management accounting enables managers to measure performance variance. There is a

need to keep track of company’s performance from time to time. Management accounting

therefore provides information which compares such performance over a range of period and

indicated which period the performance was poor and highlights some possible causes for the

same.

Management accounting techniques

Financial planning (Kallunki, 2010)

Financial planning is a strategic process of deciding how the business will afford to

achieve its goals. Business has both short term and long term goals which require funding

Financial planning technique helps in deciding in advance where and how to obtain these funds

to finance the business activities for the purpose of achieving the set objectives.

Standard costing

This technique involves the management accountants setting standard costs under most

efficient operation conditions. During normal production, the actual costs are compared with

standards costs and the variance is calculated and analyzed for purposes of controlling costs.

Costing using Marginal technique

This can be defined as the additional cost that is which results when a company

introduces another more product to the production line. In this technique, differential costing and

break even analysis are done to establish the contribution and the profitability of producing extra

materials. Management accounting will provide information on the cheaper alternative between

producing and buying and then the managers will be expected to opt for the alternative that

maximizes organizations revenue.

Management accounting will help to forecast cash flows. For British American Tobacco

group to be able to fund its future activities there must be sufficient working capital to procure

current assets and to cater for operating expenses. Management accountants are able to use

accounting tools to predict future cash flows and advise the managers on how to come up with

accurate budgets to make proper use of the available resources.

Management accounting enables managers to measure performance variance. There is a

need to keep track of company’s performance from time to time. Management accounting

therefore provides information which compares such performance over a range of period and

indicated which period the performance was poor and highlights some possible causes for the

same.

Management accounting techniques

Financial planning (Kallunki, 2010)

Financial planning is a strategic process of deciding how the business will afford to

achieve its goals. Business has both short term and long term goals which require funding

Financial planning technique helps in deciding in advance where and how to obtain these funds

to finance the business activities for the purpose of achieving the set objectives.

Standard costing

This technique involves the management accountants setting standard costs under most

efficient operation conditions. During normal production, the actual costs are compared with

standards costs and the variance is calculated and analyzed for purposes of controlling costs.

Costing using Marginal technique

This can be defined as the additional cost that is which results when a company

introduces another more product to the production line. In this technique, differential costing and

break even analysis are done to establish the contribution and the profitability of producing extra

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BAT DIRECTORS REPORT 5

units of organization’s goods and services. This technique provides useful information necessary

for controlling costs and making decisions on profit maximization.

Historical cost accounting

This is a technique that provides past accounting data to the management relating to the

costs of each job, process or department. This data is used to make comparison between the

current and the past costs. The variance between the two sets of costs is analyzed and any

necessary adjustments are made to help in controlling the current cost.

Analysis of financial statements

This is the technique which requires the management accountants to analyze the

organization’s financial statements and derive a significant and meaningful data that can be used

to forecast future cash flows. Management need to know how likely funds will be available to

finance future business operations. This is achieved by comparing financial statement for

different periods and analyzing the trends and ratios and using them to project future cash flows.

Application of accounting techniques (Noreen, et al., 2012)

Absorption costing.

Absorption costing is a management accounting technique used to expense all the costs

related to production into produced units. Here, costs are classified according to whether they are

incurred direct to the production process or are as a result of administrative activities. Direct

costs are those costs which are directly associated to the production process. They include direct

materials and direct labor. Overhead costs on the other hand refer to those costs which cannot

easily be traced to the finished product. These include costs such as electricity bills, water bills

and the administrative expenses.

In the given information, the total overhead costs are absorbed into machine hours (Thomas, et al.,

n.d.).

Overhead absorption rate = total overheads / total machine hours (Garrison, et al., 2013).

=350,000/100,000

=$ 3.5 per machine hour.

units of organization’s goods and services. This technique provides useful information necessary

for controlling costs and making decisions on profit maximization.

Historical cost accounting

This is a technique that provides past accounting data to the management relating to the

costs of each job, process or department. This data is used to make comparison between the

current and the past costs. The variance between the two sets of costs is analyzed and any

necessary adjustments are made to help in controlling the current cost.

Analysis of financial statements

This is the technique which requires the management accountants to analyze the

organization’s financial statements and derive a significant and meaningful data that can be used

to forecast future cash flows. Management need to know how likely funds will be available to

finance future business operations. This is achieved by comparing financial statement for

different periods and analyzing the trends and ratios and using them to project future cash flows.

Application of accounting techniques (Noreen, et al., 2012)

Absorption costing.

Absorption costing is a management accounting technique used to expense all the costs

related to production into produced units. Here, costs are classified according to whether they are

incurred direct to the production process or are as a result of administrative activities. Direct

costs are those costs which are directly associated to the production process. They include direct

materials and direct labor. Overhead costs on the other hand refer to those costs which cannot

easily be traced to the finished product. These include costs such as electricity bills, water bills

and the administrative expenses.

In the given information, the total overhead costs are absorbed into machine hours (Thomas, et al.,

n.d.).

Overhead absorption rate = total overheads / total machine hours (Garrison, et al., 2013).

=350,000/100,000

=$ 3.5 per machine hour.

BAT DIRECTORS REPORT 6

To get the selling price for each of the two products, a costing card is needed.

Cost card for B&H strawberry and B&H cherry

Fixed cost (Mishra, 2017)

Type of cost that do not chance or vary.

Total cost (Mishra, 2017)

Refer to the sum of all expenditure on production of goods and services.

Variables cost (Decoster, et al., 2012)

Refer to the type of costs that keep on changing every financial year.

Direct cost (Kallunki, 2010)

Type of cost which is directly linked to a certain operation and can traced.

Labor costs (Thomas, et al., n.d.)

Are cost incurred in hiring workers or laborers.

Overhead costs (Kieso, 2009)

Are costs incurred in the process of production, such as replacing broken equipment and

damaged machine.

B&H strawberry B&H cherry

Direct costs

Material cost 10 11

Labor costs 11 12

To get the selling price for each of the two products, a costing card is needed.

Cost card for B&H strawberry and B&H cherry

Fixed cost (Mishra, 2017)

Type of cost that do not chance or vary.

Total cost (Mishra, 2017)

Refer to the sum of all expenditure on production of goods and services.

Variables cost (Decoster, et al., 2012)

Refer to the type of costs that keep on changing every financial year.

Direct cost (Kallunki, 2010)

Type of cost which is directly linked to a certain operation and can traced.

Labor costs (Thomas, et al., n.d.)

Are cost incurred in hiring workers or laborers.

Overhead costs (Kieso, 2009)

Are costs incurred in the process of production, such as replacing broken equipment and

damaged machine.

B&H strawberry B&H cherry

Direct costs

Material cost 10 11

Labor costs 11 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BAT DIRECTORS REPORT 7

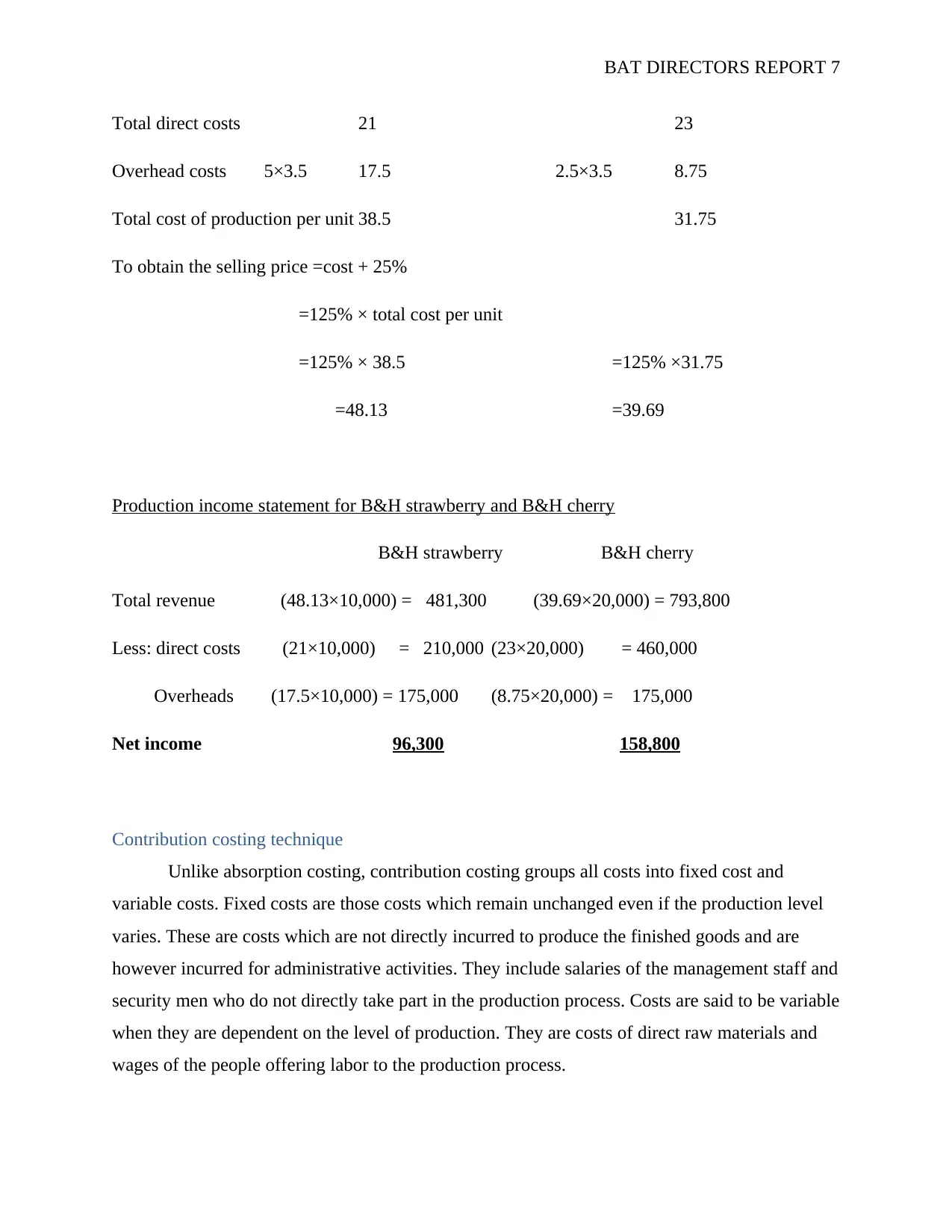

Total direct costs 21 23

Overhead costs 5×3.5 17.5 2.5×3.5 8.75

Total cost of production per unit 38.5 31.75

To obtain the selling price =cost + 25%

=125% × total cost per unit

=125% × 38.5 =125% ×31.75

=48.13 =39.69

Production income statement for B&H strawberry and B&H cherry

B&H strawberry B&H cherry

Total revenue (48.13×10,000) = 481,300 (39.69×20,000) = 793,800

Less: direct costs (21×10,000) = 210,000 (23×20,000) = 460,000

Overheads (17.5×10,000) = 175,000 (8.75×20,000) = 175,000

Net income 96,300 158,800

Contribution costing technique

Unlike absorption costing, contribution costing groups all costs into fixed cost and

variable costs. Fixed costs are those costs which remain unchanged even if the production level

varies. These are costs which are not directly incurred to produce the finished goods and are

however incurred for administrative activities. They include salaries of the management staff and

security men who do not directly take part in the production process. Costs are said to be variable

when they are dependent on the level of production. They are costs of direct raw materials and

wages of the people offering labor to the production process.

Total direct costs 21 23

Overhead costs 5×3.5 17.5 2.5×3.5 8.75

Total cost of production per unit 38.5 31.75

To obtain the selling price =cost + 25%

=125% × total cost per unit

=125% × 38.5 =125% ×31.75

=48.13 =39.69

Production income statement for B&H strawberry and B&H cherry

B&H strawberry B&H cherry

Total revenue (48.13×10,000) = 481,300 (39.69×20,000) = 793,800

Less: direct costs (21×10,000) = 210,000 (23×20,000) = 460,000

Overheads (17.5×10,000) = 175,000 (8.75×20,000) = 175,000

Net income 96,300 158,800

Contribution costing technique

Unlike absorption costing, contribution costing groups all costs into fixed cost and

variable costs. Fixed costs are those costs which remain unchanged even if the production level

varies. These are costs which are not directly incurred to produce the finished goods and are

however incurred for administrative activities. They include salaries of the management staff and

security men who do not directly take part in the production process. Costs are said to be variable

when they are dependent on the level of production. They are costs of direct raw materials and

wages of the people offering labor to the production process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BAT DIRECTORS REPORT 8

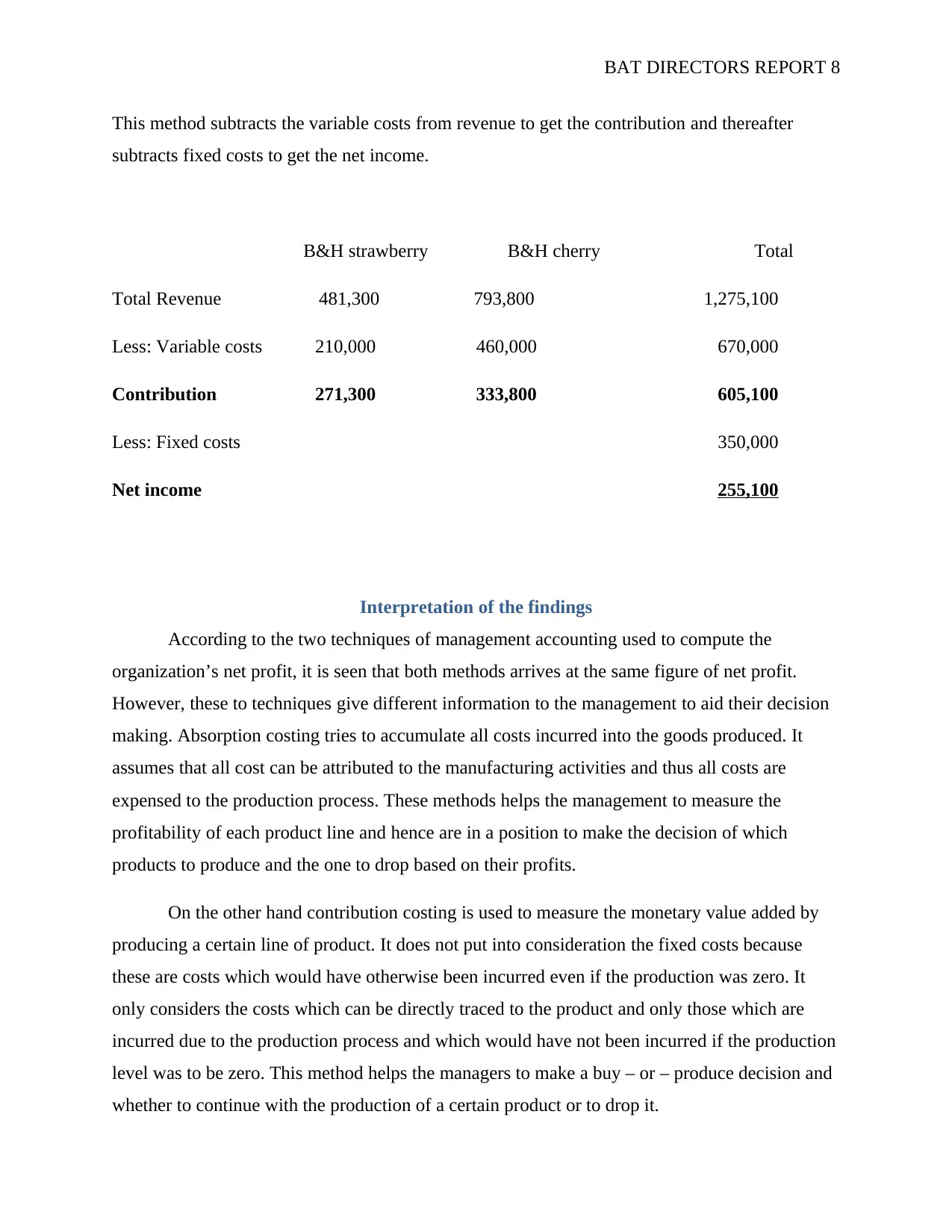

This method subtracts the variable costs from revenue to get the contribution and thereafter

subtracts fixed costs to get the net income.

B&H strawberry B&H cherry Total

Total Revenue 481,300 793,800 1,275,100

Less: Variable costs 210,000 460,000 670,000

Contribution 271,300 333,800 605,100

Less: Fixed costs 350,000

Net income 255,100

Interpretation of the findings

According to the two techniques of management accounting used to compute the

organization’s net profit, it is seen that both methods arrives at the same figure of net profit.

However, these to techniques give different information to the management to aid their decision

making. Absorption costing tries to accumulate all costs incurred into the goods produced. It

assumes that all cost can be attributed to the manufacturing activities and thus all costs are

expensed to the production process. These methods helps the management to measure the

profitability of each product line and hence are in a position to make the decision of which

products to produce and the one to drop based on their profits.

On the other hand contribution costing is used to measure the monetary value added by

producing a certain line of product. It does not put into consideration the fixed costs because

these are costs which would have otherwise been incurred even if the production was zero. It

only considers the costs which can be directly traced to the product and only those which are

incurred due to the production process and which would have not been incurred if the production

level was to be zero. This method helps the managers to make a buy – or – produce decision and

whether to continue with the production of a certain product or to drop it.

This method subtracts the variable costs from revenue to get the contribution and thereafter

subtracts fixed costs to get the net income.

B&H strawberry B&H cherry Total

Total Revenue 481,300 793,800 1,275,100

Less: Variable costs 210,000 460,000 670,000

Contribution 271,300 333,800 605,100

Less: Fixed costs 350,000

Net income 255,100

Interpretation of the findings

According to the two techniques of management accounting used to compute the

organization’s net profit, it is seen that both methods arrives at the same figure of net profit.

However, these to techniques give different information to the management to aid their decision

making. Absorption costing tries to accumulate all costs incurred into the goods produced. It

assumes that all cost can be attributed to the manufacturing activities and thus all costs are

expensed to the production process. These methods helps the management to measure the

profitability of each product line and hence are in a position to make the decision of which

products to produce and the one to drop based on their profits.

On the other hand contribution costing is used to measure the monetary value added by

producing a certain line of product. It does not put into consideration the fixed costs because

these are costs which would have otherwise been incurred even if the production was zero. It

only considers the costs which can be directly traced to the product and only those which are

incurred due to the production process and which would have not been incurred if the production

level was to be zero. This method helps the managers to make a buy – or – produce decision and

whether to continue with the production of a certain product or to drop it.

BAT DIRECTORS REPORT 9

Future strategies for BAT

For BAT to continue leading the market, it needs to lay down the following strategies

which will help in dominating the market.

Product diversification (Achimugu, n.d.)

At the moment, BAT is producing only two products, B&H strawberry and B&H cherry.

There is a need for BAT to research on other products which are likely to have a good demand in

the market. This will help the company to make more profit by having a wide variety of products

available for sale. However, while making this decision, the managers should ensure that such

products have a positive contribution to the company.

Predict future demands

The aim of producing goods and services is to sell them to the customers. The company

should be able to predict future demands of its customers. Managers should be able to identify

the customers’ needs and preferences towards the company’s products. The target here should be

to improve and maintain the product’s ability to satisfy the consumers wants. Proper research is

needed on the consumption behavior of both the existing and prospectus customers.

Identify and manage risks

There are always risks of venturing into new products. BAT managers should critically

evaluate the company’s strengths and weaknesses and capitalize on the strengths. This will

ensure that the company resources are used in the most appropriate way and that wastage is

avoided as much as possible.

Innovation

Technology has become indispensable in the modern era of business. For any business to

become a market leader, it needs to invest a lot in technology and modern methods of

production. This can be achieved by utilizing employee’s talents and using the available

technology appropriately. This will help in reducing costs and hence maximizing revenue.

Conclusion

Management accounting is a very important tool in decision making. Managers are the

most consumers of the management accounting information. It is believed that information is the

Future strategies for BAT

For BAT to continue leading the market, it needs to lay down the following strategies

which will help in dominating the market.

Product diversification (Achimugu, n.d.)

At the moment, BAT is producing only two products, B&H strawberry and B&H cherry.

There is a need for BAT to research on other products which are likely to have a good demand in

the market. This will help the company to make more profit by having a wide variety of products

available for sale. However, while making this decision, the managers should ensure that such

products have a positive contribution to the company.

Predict future demands

The aim of producing goods and services is to sell them to the customers. The company

should be able to predict future demands of its customers. Managers should be able to identify

the customers’ needs and preferences towards the company’s products. The target here should be

to improve and maintain the product’s ability to satisfy the consumers wants. Proper research is

needed on the consumption behavior of both the existing and prospectus customers.

Identify and manage risks

There are always risks of venturing into new products. BAT managers should critically

evaluate the company’s strengths and weaknesses and capitalize on the strengths. This will

ensure that the company resources are used in the most appropriate way and that wastage is

avoided as much as possible.

Innovation

Technology has become indispensable in the modern era of business. For any business to

become a market leader, it needs to invest a lot in technology and modern methods of

production. This can be achieved by utilizing employee’s talents and using the available

technology appropriately. This will help in reducing costs and hence maximizing revenue.

Conclusion

Management accounting is a very important tool in decision making. Managers are the

most consumers of the management accounting information. It is believed that information is the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BAT DIRECTORS REPORT 10

best tool for decision making and management accounting is there to provide such information.

BAT managers should ensure that they utilize all the financial and statistical date provided to

them by the management accountants. Easily interpretable statement can be interpreted to mean

easier and quicker decision making on the side of the management. On the other hand

complicated and inadequate information will inappropriate the management hence compromise

the ease and the pace at which decisions are made. Investing in research is a prudent step for

managers take if want to drive organizations towards success. There should be therefore a good

co-ordination between the managers and the management accountants if the company is to

succeed (Achimugu & Ocheni, 2015).

References

best tool for decision making and management accounting is there to provide such information.

BAT managers should ensure that they utilize all the financial and statistical date provided to

them by the management accountants. Easily interpretable statement can be interpreted to mean

easier and quicker decision making on the side of the management. On the other hand

complicated and inadequate information will inappropriate the management hence compromise

the ease and the pace at which decisions are made. Investing in research is a prudent step for

managers take if want to drive organizations towards success. There should be therefore a good

co-ordination between the managers and the management accountants if the company is to

succeed (Achimugu & Ocheni, 2015).

References

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BAT DIRECTORS REPORT 11

Achimugu, A., n.d. Management Acounting and MAnagementStrategies Decision in Organizations.

International Journal of Accounting, Volume Vol 4.

Achimugu, A. & Ocheni, S. I., 2015. Application of Management Accounting Technique in the Public

Sector of Nigerian Economy. Journal of Good Governance and Sustainable Development in Africa, 2(4),

pp. 81-87.

Charles, M., 2016. Management Accounting. 3rd ed. s.l.:s.n.

Decoster, Don, T. & Eden, S. L., 2012. Management Accounting: A Decision Emphasis. 2nd ed ed. New

York: John Wiley and Sons Inc.

Drury, C. M. & Drury, C. M., 2013. Management and Cost accounting. Second ed. New York: New York.

Drury, M. C., 2015. Management and cost accounting. Bussines Journal, pp. 12-40.

Dwivedi, D. n., n.d. Manegerial Economics. 7th ed. s.l.:s.n.

Garrison, Ray, H. & Eric, W. N., 2013. Mangement accounting. 2nd ed. Chicago: Richard D. Irwin.

Kallunki, J.-p., 2010. The Effect of Organizational Life Cycle Stage on the Use of activity-Based Costing.

2nd ed. Olulu: University of Olulu.

Kieso, K. K., 2009. Managerial Accounting. 2nd ed ed. Santa: University of California.

Maryanne, . M. M., Don , R. & Hansen, 2006. Management Accounting. 2nd ed. Ohio: South-western

College Publishing.

Mishra, T., 2017. Elementary Cost Accounting. 3rd ed. s.l.:s.n.

Mishra, T., 2017. Manegerial Economics. 2nd ed. Bombay: s.n.

Noreen, E. W., Ray, H. & Garrison, 2012. Management Accounting. 3rd ed. Chicago: UP.

Saker, S., 2007. Manegement Accounting. 4th ed. Chicago: s.n.

Sinha, I. B. & Vinayakam, N., n.d. Management Accounting-Tools and Techniques. Mumbai: Himalaya

Publishing House.

Thomas, C. R., Charles, M. S. & etl, n.d. Manegerial Economics. 2nd ed. s.l.:s.n.

Achimugu, A., n.d. Management Acounting and MAnagementStrategies Decision in Organizations.

International Journal of Accounting, Volume Vol 4.

Achimugu, A. & Ocheni, S. I., 2015. Application of Management Accounting Technique in the Public

Sector of Nigerian Economy. Journal of Good Governance and Sustainable Development in Africa, 2(4),

pp. 81-87.

Charles, M., 2016. Management Accounting. 3rd ed. s.l.:s.n.

Decoster, Don, T. & Eden, S. L., 2012. Management Accounting: A Decision Emphasis. 2nd ed ed. New

York: John Wiley and Sons Inc.

Drury, C. M. & Drury, C. M., 2013. Management and Cost accounting. Second ed. New York: New York.

Drury, M. C., 2015. Management and cost accounting. Bussines Journal, pp. 12-40.

Dwivedi, D. n., n.d. Manegerial Economics. 7th ed. s.l.:s.n.

Garrison, Ray, H. & Eric, W. N., 2013. Mangement accounting. 2nd ed. Chicago: Richard D. Irwin.

Kallunki, J.-p., 2010. The Effect of Organizational Life Cycle Stage on the Use of activity-Based Costing.

2nd ed. Olulu: University of Olulu.

Kieso, K. K., 2009. Managerial Accounting. 2nd ed ed. Santa: University of California.

Maryanne, . M. M., Don , R. & Hansen, 2006. Management Accounting. 2nd ed. Ohio: South-western

College Publishing.

Mishra, T., 2017. Elementary Cost Accounting. 3rd ed. s.l.:s.n.

Mishra, T., 2017. Manegerial Economics. 2nd ed. Bombay: s.n.

Noreen, E. W., Ray, H. & Garrison, 2012. Management Accounting. 3rd ed. Chicago: UP.

Saker, S., 2007. Manegement Accounting. 4th ed. Chicago: s.n.

Sinha, I. B. & Vinayakam, N., n.d. Management Accounting-Tools and Techniques. Mumbai: Himalaya

Publishing House.

Thomas, C. R., Charles, M. S. & etl, n.d. Manegerial Economics. 2nd ed. s.l.:s.n.

BAT DIRECTORS REPORT 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.