Finance Case Study: BSB's Interest Rate Risk Management and Hedging

VerifiedAdded on 2022/09/28

|5

|972

|23

Case Study

AI Summary

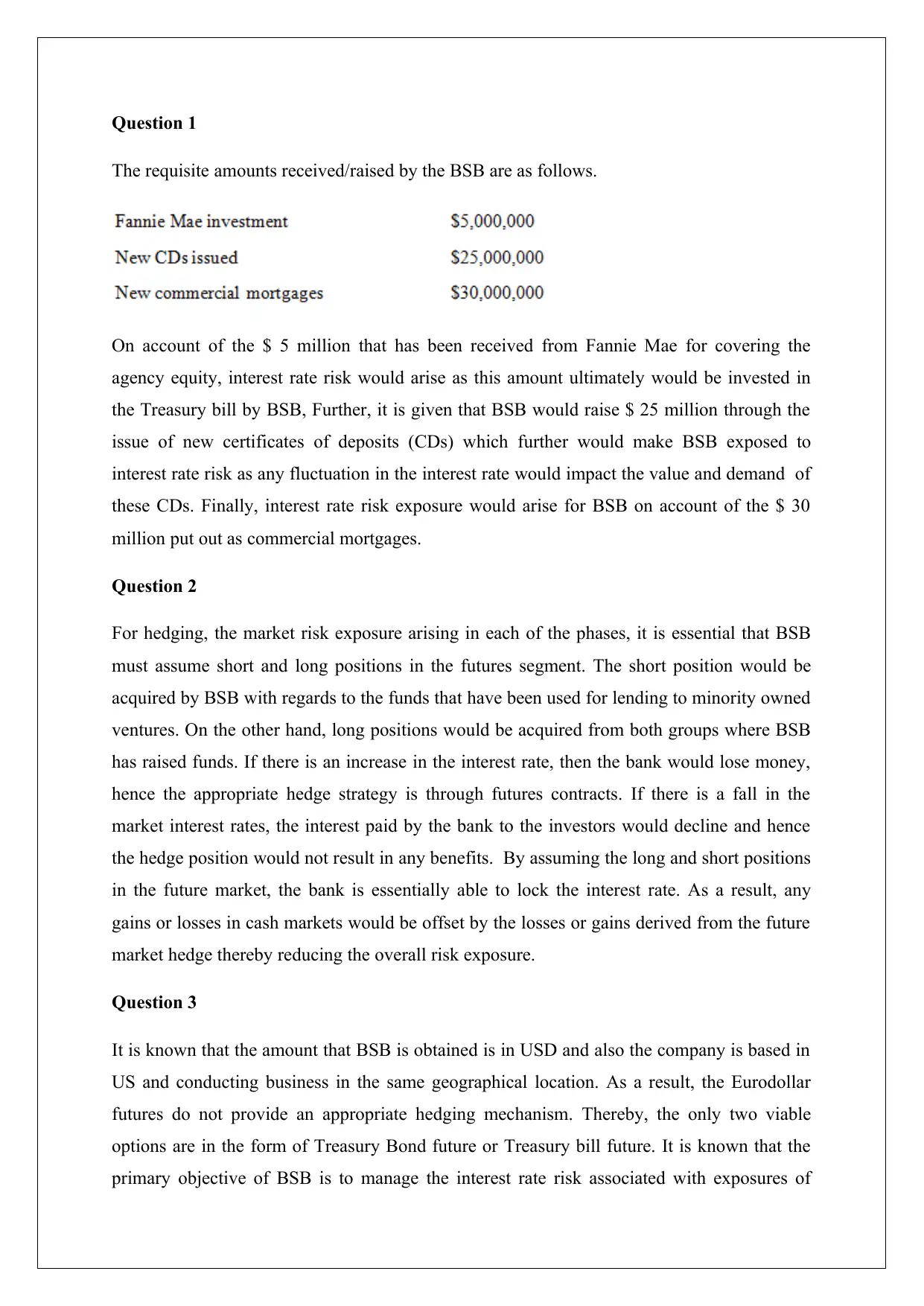

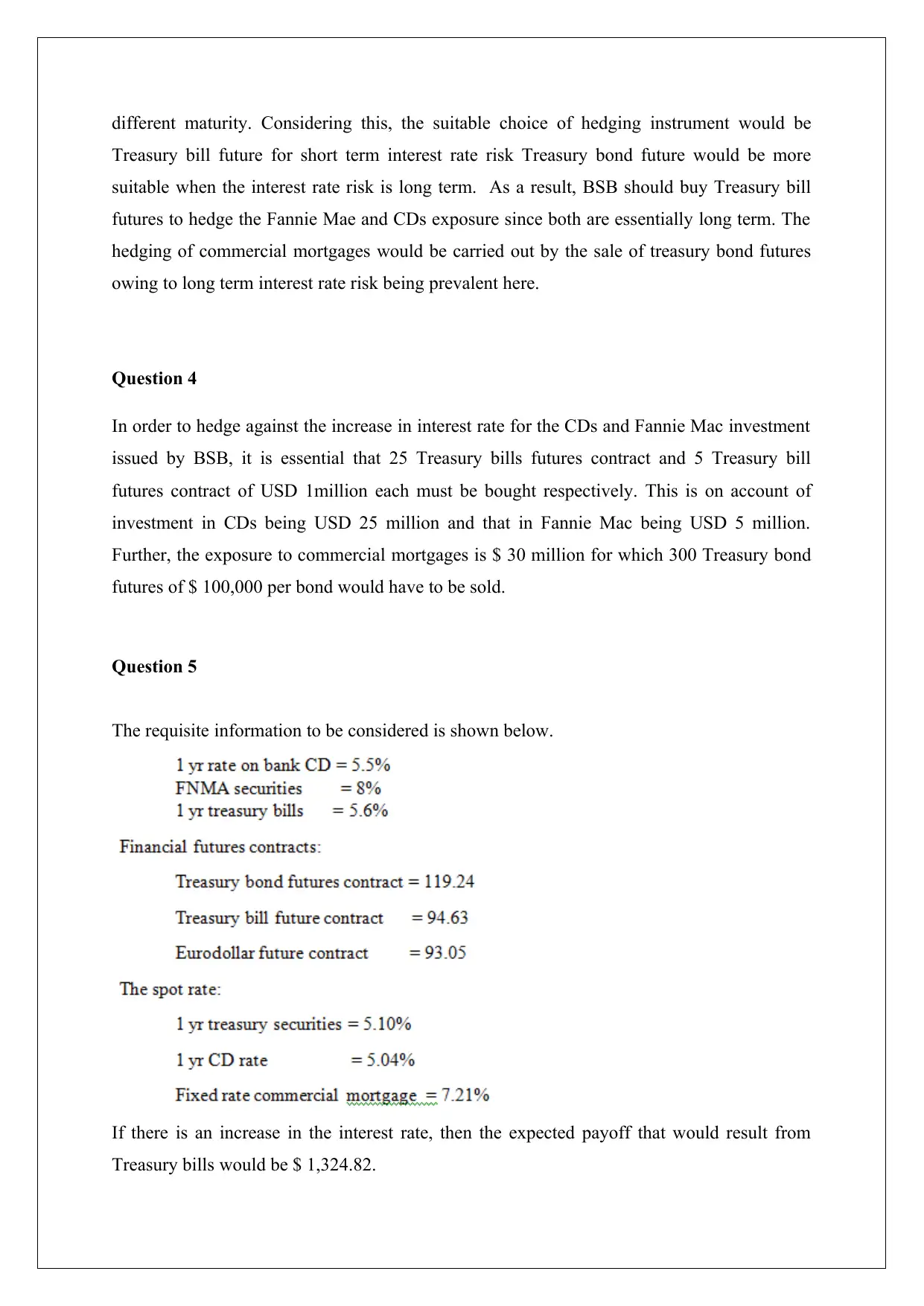

This case study analyzes BSB's interest rate risk and explores various hedging strategies. The case examines the sources of interest rate risk, including funds from Fannie Mae, new certificates of deposit (CDs), and commercial mortgages. It details the use of futures contracts (Treasury bill and Treasury bond futures) to hedge against interest rate fluctuations. The solution provides specific recommendations for hedging positions, considering the maturity of the exposures and the potential payoffs from these hedges. The document also discusses the risks associated with hedging, including margin requirements and the potential cost of hedging, and differentiates between static and dynamic hedging strategies. The case study concludes with a discussion of the best hedging strategies for BSB to minimize losses and maximize profits.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.