BSBFIM501 - Budget Analysis and Financial Planning for Big Red Bicycle

VerifiedAdded on 2023/06/13

|22

|5227

|178

Report

AI Summary

This report provides a comprehensive analysis of Big Red Bicycle's financial plans and budget, identifying discrepancies, unrealistic estimations, and potential risks. It includes a detailed budget analysis highlighting variances in sales, commissions, and expenses, alongside recommendations for improvements. The report also presents contingency plans to mitigate risks such as economic downturns and commission imbalances, featuring strategies like exploring overseas markets and implementing performance-based commission systems. Furthermore, the document assesses the company's financial policies, training plans for employees, and modifications to the contingency plan based on budget variance reports. Finally, it reviews and evaluates the overall financial management processes, recommending improvements for data collection and solution implementation. Desklib offers a wide array of solved assignments and past papers to aid students in their studies.

Running head: MANAGING BUDGETS AND FINANCIAL PLANS

Managing Budget and Financial Plans

Name of the Student:

Name of the University:

Author’s Note:

Managing Budget and Financial Plans

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGING BUDGETS AND FINANCIAL PLANS

Table of Contents

Assessment 1...................................................................................................................................3

Introduction..................................................................................................................................3

Budget Analysis...........................................................................................................................3

Contingency Plan.............................................................................................................................4

Changes in budget............................................................................................................................8

Assessment 2...................................................................................................................................8

Financial Policies of the Company..................................................................................................9

Training Plan.................................................................................................................................10

Assessment 3.................................................................................................................................11

Budget Preparation........................................................................................................................11

Modified Contingency Plan...........................................................................................................14

Assessment 4.................................................................................................................................16

Activity 2.......................................................................................................................................17

Activity 3.......................................................................................................................................18

Activity 4.......................................................................................................................................19

Reference.......................................................................................................................................21

MANAGING BUDGETS AND FINANCIAL PLANS

Table of Contents

Assessment 1...................................................................................................................................3

Introduction..................................................................................................................................3

Budget Analysis...........................................................................................................................3

Contingency Plan.............................................................................................................................4

Changes in budget............................................................................................................................8

Assessment 2...................................................................................................................................8

Financial Policies of the Company..................................................................................................9

Training Plan.................................................................................................................................10

Assessment 3.................................................................................................................................11

Budget Preparation........................................................................................................................11

Modified Contingency Plan...........................................................................................................14

Assessment 4.................................................................................................................................16

Activity 2.......................................................................................................................................17

Activity 3.......................................................................................................................................18

Activity 4.......................................................................................................................................19

Reference.......................................................................................................................................21

2

MANAGING BUDGETS AND FINANCIAL PLANS

Assessment 1

Introduction

As per the case study provided in the question, Big Red Bicycle are manufacturer of

bicycle business and sell the bicycles in the local market of Australia. As per the strategic plan of

the management the company aims to earns net profit before tax of $ 1,000,000. The company is

also considering to expand the business by starting manufacturing in overseas market and this

will also be helping the business to take advantage

The main purpose of this assignment is to analyze the master budget prepared by the

management and also identify whether there are any discrepancies, also areas which are not

achievable for the business and also formulate a contingency plan which can counter the risks

which are faced by the business.

Budget Analysis

As per the master budget prepared by the company the figure of sales is $ 7,50,000 which

is same as estimated for every year. As per the master budget of the company, all the cost and

revenues which are estimated by the business keeping all the costs and revenues of the business

same for each year (Rubin 2016). The master budget is for the year 2011-2012 and is compared

with the actual budget of the company. The sales figure of the company as shown in the budget

for the first quarter is shown at $ 6,00,000. The sales in the second quarter for the company is $

9,00,000. The figure of sales as per the budget is evenly spread which is not possible as it is very

likely the sales of the company will fluctuate for each quarter of the company. In addition to this,

the commission amount which is shown in the based on the 2% of the sale amount which might

not be realistic in nature. The repair and maintenance expense which is shown by the company in

the budget is not clear and have been evenly distributed among the four quarter which is $

MANAGING BUDGETS AND FINANCIAL PLANS

Assessment 1

Introduction

As per the case study provided in the question, Big Red Bicycle are manufacturer of

bicycle business and sell the bicycles in the local market of Australia. As per the strategic plan of

the management the company aims to earns net profit before tax of $ 1,000,000. The company is

also considering to expand the business by starting manufacturing in overseas market and this

will also be helping the business to take advantage

The main purpose of this assignment is to analyze the master budget prepared by the

management and also identify whether there are any discrepancies, also areas which are not

achievable for the business and also formulate a contingency plan which can counter the risks

which are faced by the business.

Budget Analysis

As per the master budget prepared by the company the figure of sales is $ 7,50,000 which

is same as estimated for every year. As per the master budget of the company, all the cost and

revenues which are estimated by the business keeping all the costs and revenues of the business

same for each year (Rubin 2016). The master budget is for the year 2011-2012 and is compared

with the actual budget of the company. The sales figure of the company as shown in the budget

for the first quarter is shown at $ 6,00,000. The sales in the second quarter for the company is $

9,00,000. The figure of sales as per the budget is evenly spread which is not possible as it is very

likely the sales of the company will fluctuate for each quarter of the company. In addition to this,

the commission amount which is shown in the based on the 2% of the sale amount which might

not be realistic in nature. The repair and maintenance expense which is shown by the company in

the budget is not clear and have been evenly distributed among the four quarter which is $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGING BUDGETS AND FINANCIAL PLANS

11,250. The repair and maintenance expenses which is shown evenly through out the years is not

realistic as it is possible that in the second quarter the business might not incur any repair and

maintenance expenses. The sales which is recorded is different from the management ‘s

expectation of the same due to economical downfall of the market (Wildavsky 2017).

The sales manager needs to clarify the figures of commission which is shown in the

Master Budget as prepared by the company. The commission is allowed at 2% on the figures of

sales. as the figure of sale is not certain, the commission which is obtained from such a source

might not be reliable or accurate. The sales manager also needs to clarify from the management

about the expenses which are recorded by the management such as repair and maintenance

expenses which is shown for al the quarter equally as shown in the budget of the company. The

management needs to change the sales figure of the company and incorporate an accurate

estimate. In the case of expense, which the management expects to incur are to estimated

accurately as this determine the targeted profit of the company (Henttu-Aho and Järvinen 2013).

Due the fall in the sale figure the variances which can be expected by the business are more than

the budgeted figure. The sales managers needs to clarify the same from the management of the

company.

Contingency Plan

Contingency plan 1

MANAGING BUDGETS AND FINANCIAL PLANS

11,250. The repair and maintenance expenses which is shown evenly through out the years is not

realistic as it is possible that in the second quarter the business might not incur any repair and

maintenance expenses. The sales which is recorded is different from the management ‘s

expectation of the same due to economical downfall of the market (Wildavsky 2017).

The sales manager needs to clarify the figures of commission which is shown in the

Master Budget as prepared by the company. The commission is allowed at 2% on the figures of

sales. as the figure of sale is not certain, the commission which is obtained from such a source

might not be reliable or accurate. The sales manager also needs to clarify from the management

about the expenses which are recorded by the management such as repair and maintenance

expenses which is shown for al the quarter equally as shown in the budget of the company. The

management needs to change the sales figure of the company and incorporate an accurate

estimate. In the case of expense, which the management expects to incur are to estimated

accurately as this determine the targeted profit of the company (Henttu-Aho and Järvinen 2013).

Due the fall in the sale figure the variances which can be expected by the business are more than

the budgeted figure. The sales managers needs to clarify the same from the management of the

company.

Contingency Plan

Contingency plan 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGING BUDGETS AND FINANCIAL PLANS

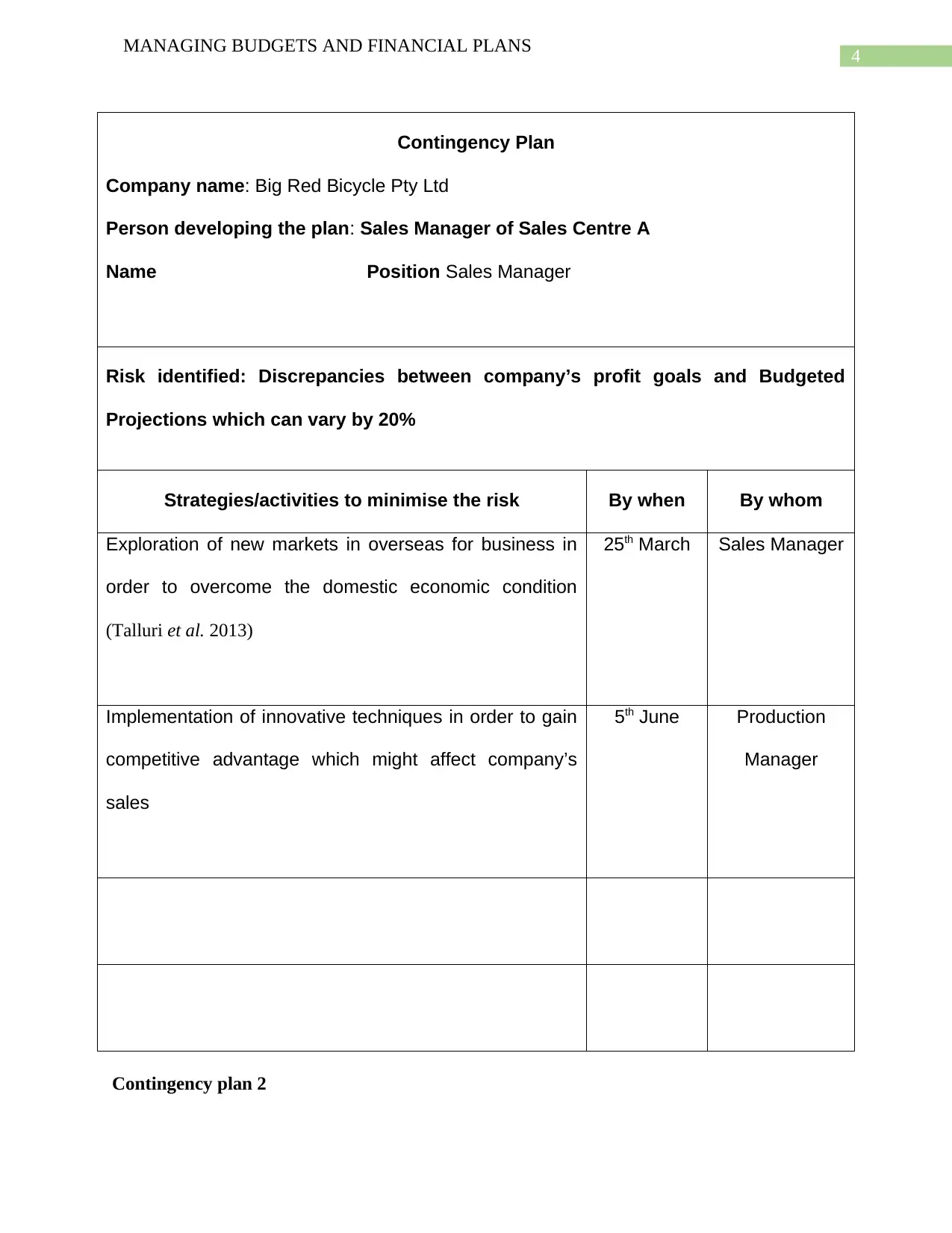

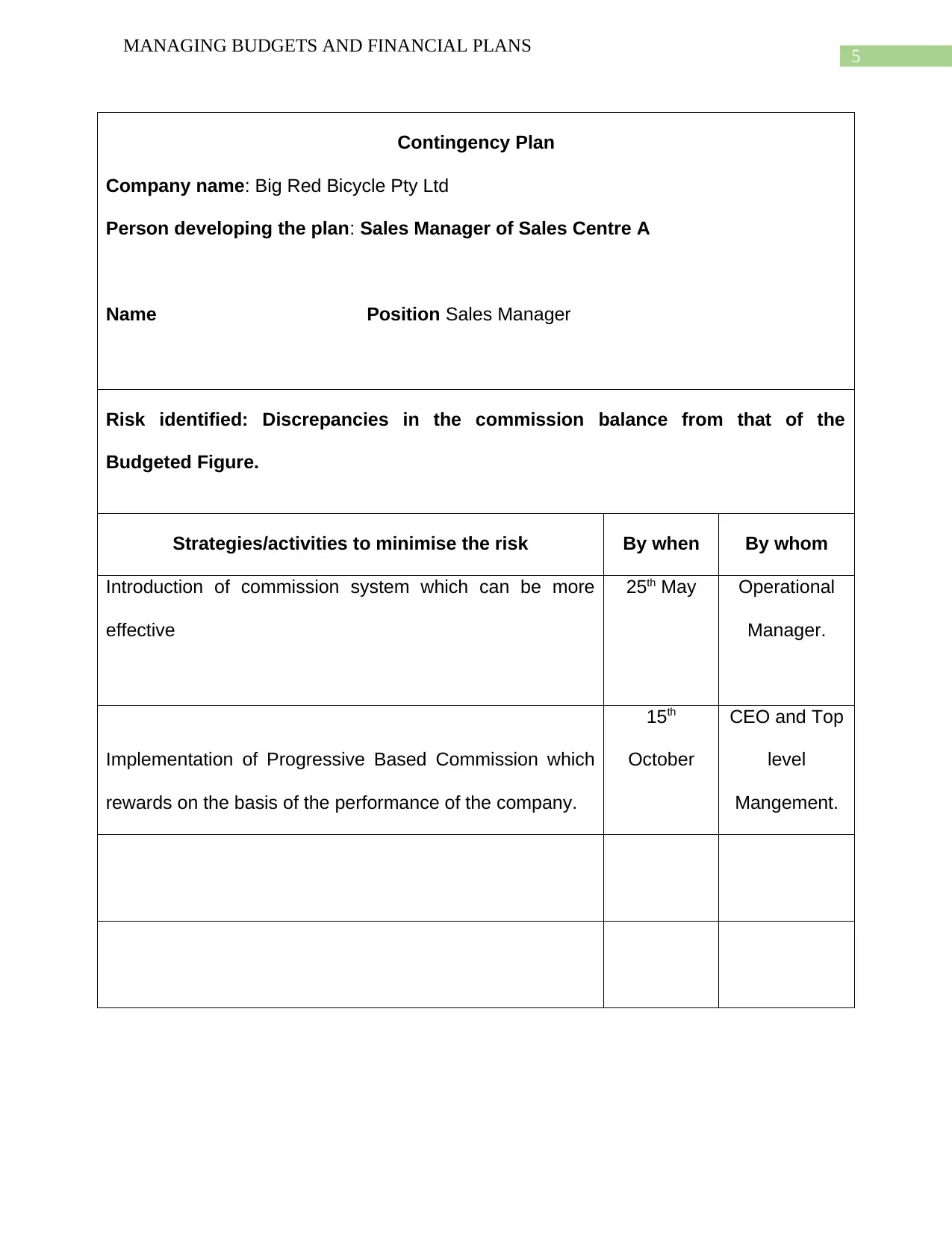

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name Position Sales Manager

Risk identified: Discrepancies between company’s profit goals and Budgeted

Projections which can vary by 20%

Strategies/activities to minimise the risk By when By whom

Exploration of new markets in overseas for business in

order to overcome the domestic economic condition

(Talluri et al. 2013)

25th March Sales Manager

Implementation of innovative techniques in order to gain

competitive advantage which might affect company’s

sales

5th June Production

Manager

Contingency plan 2

MANAGING BUDGETS AND FINANCIAL PLANS

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name Position Sales Manager

Risk identified: Discrepancies between company’s profit goals and Budgeted

Projections which can vary by 20%

Strategies/activities to minimise the risk By when By whom

Exploration of new markets in overseas for business in

order to overcome the domestic economic condition

(Talluri et al. 2013)

25th March Sales Manager

Implementation of innovative techniques in order to gain

competitive advantage which might affect company’s

sales

5th June Production

Manager

Contingency plan 2

5

MANAGING BUDGETS AND FINANCIAL PLANS

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name Position Sales Manager

Risk identified: Discrepancies in the commission balance from that of the

Budgeted Figure.

Strategies/activities to minimise the risk By when By whom

Introduction of commission system which can be more

effective

25th May Operational

Manager.

Implementation of Progressive Based Commission which

rewards on the basis of the performance of the company.

15th

October

CEO and Top

level

Mangement.

MANAGING BUDGETS AND FINANCIAL PLANS

Contingency Plan

Company name: Big Red Bicycle Pty Ltd

Person developing the plan: Sales Manager of Sales Centre A

Name Position Sales Manager

Risk identified: Discrepancies in the commission balance from that of the

Budgeted Figure.

Strategies/activities to minimise the risk By when By whom

Introduction of commission system which can be more

effective

25th May Operational

Manager.

Implementation of Progressive Based Commission which

rewards on the basis of the performance of the company.

15th

October

CEO and Top

level

Mangement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGING BUDGETS AND FINANCIAL PLANS

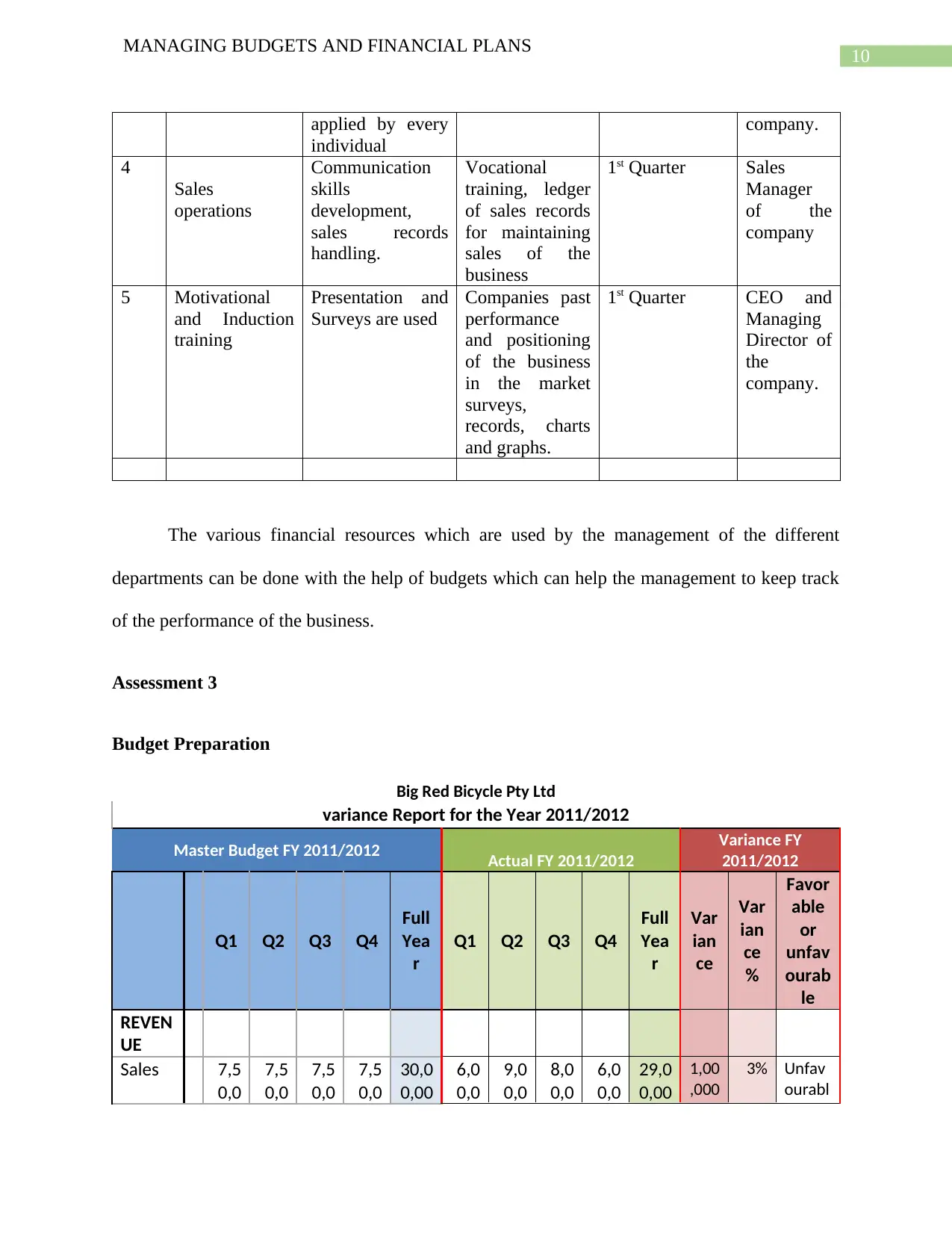

Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full Year Variance Variance

%

Favorable or

unfavourable

7,50,000 7,50,000 7,50,000 7,50,000 30,00,000 6,00,000 9,00,000 8,00,000 6,00,000 29,00,000 1,00,000 3% Unfavourable

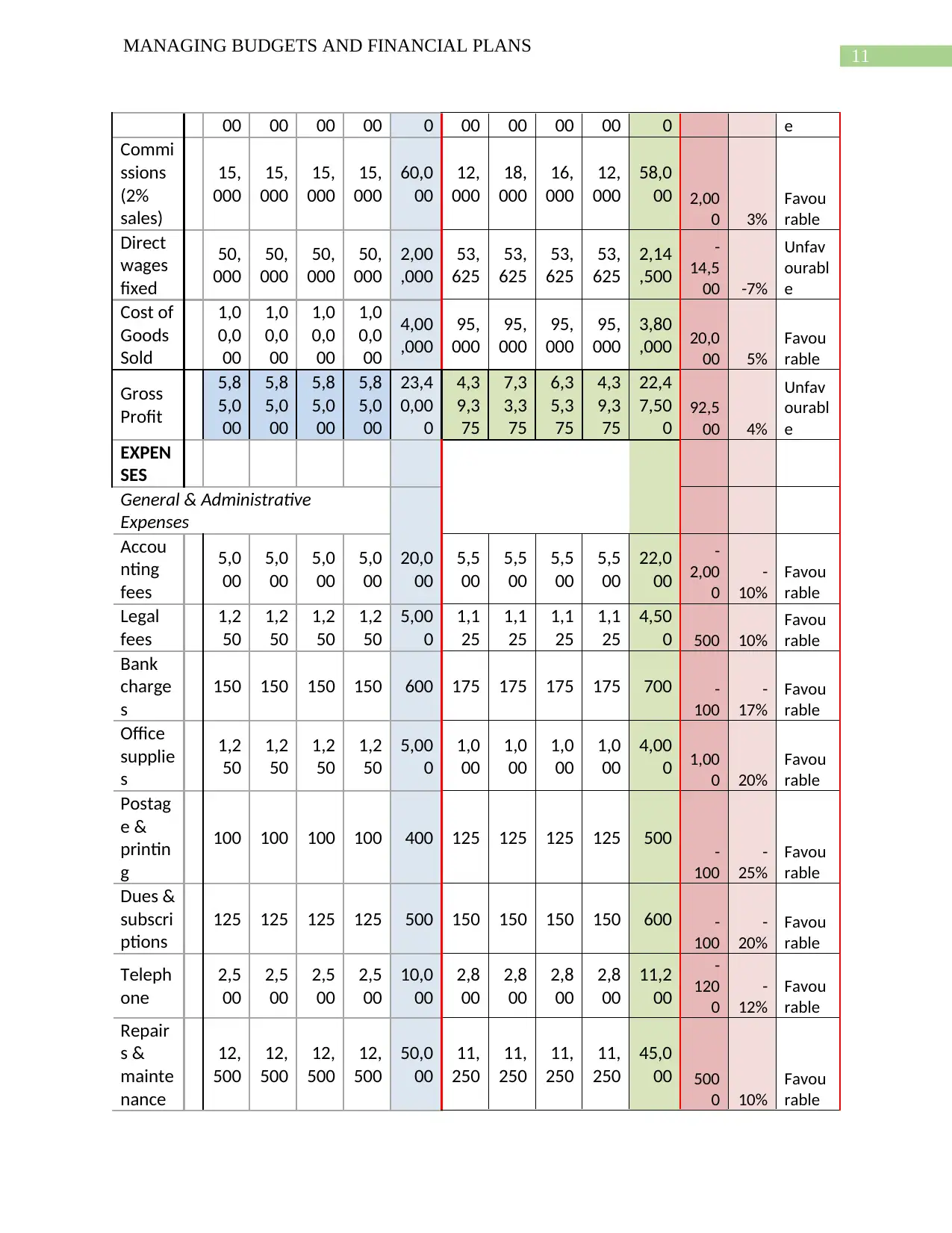

15,000 15,000 15,000 15,000 60,000 12,000 18,000 16,000 12,000 58,000 2,000 3% Favourable

50,000 50,000 50,000 50,000 2,00,000 53,625 53,625 53,625 53,625 2,14,500 -14,500 -7% Unfavourable

1,00,000 1,00,000 1,00,000 1,00,000 4,00,000 95,000 95,000 95,000 95,000 3,80,000 20,000 5% Favourable

5,85,000 5,85,000 5,85,000 5,85,000 23,40,000 4,39,375 7,33,375 6,35,375 4,39,375 22,47,500 92,500 4% Unfavourable

5,000 5,000 5,000 5,000 20,000 5,500 5,500 5,500 5,500 22,000 -2,000 -10% Favourable

1,250 1,250 1,250 1,250 5,000 1,125 1,125 1,125 1,125 4,500 500 10% Favourable

150 150 150 150 600 175 175 175 175 700 -100 -17% Favourable

1,250 1,250 1,250 1,250 5,000 1,000 1,000 1,000 1,000 4,000 1,000 20% Favourable

100 100 100 100 400 125 125 125 125 500 -100 -25% Favourable

125 125 125 125 500 150 150 150 150 600 -100 -20% Favourable

2,500 2,500 2,500 2,500 10,000 2,800 2,800 2,800 2,800 11,200 -1200 -12% Favourable

12,500 12,500 12,500 12,500 50,000 11,250 11,250 11,250 11,250 45,000 5000 10% Favourable

6,250 6,250 6,250 6,250 25,000 6,250 6,250 6,250 6,250 25,000 0 0% Favourable

50,000 50,000 50,000 50,000 2,00,000 52,000 52,000 52,000 52,000 2,08,000 -8000 -4% Favourable

11,250 11,250 11,250 11,250 45,000 11,250 11,250 11,250 11,250 45,000 0 0% Favourable

1,25,000 1,25,000 1,25,000 1,25,000 5,00,000 1,25,000 1,25,000 1,25,000 1,25,000 5,00,000 0 0% Favourable

5,000 5,000 5,000 5,000 20,000 5,750 5,750 5,750 5,750 23,000 -3000 -15% Favourable

10,000 10,000 10,000 10,000 40,000 9,500 9,500 9,500 9,500 38,000 2000 5% Favourable

25,000 25,000 25,000 25,000 1,00,000 25,000 25,000 25,000 25,000 1,00,000 0 0% Favourable

25,000 25,000 25,000 25,000 1,00,000 25,000 25,000 25,000 25,000 1,00,000 0 0% Favourable

50,000 50,000 50,000 50,000 2,00,000 50,000 50,000 50,000 50,000 2,00,000 0 0% Favourable

7,500 7,500 7,500 7,500 30,000 8,750 8,750 8,750 8,750 35,000 -5000 -17% Favourable

12,500 12,500 12,500 12,500 50,000 15,000 15,000 15,000 15,000 60,000 -10000 -20% Favourable

3,50,375 3,50,375 3,50,375 3,50,375 14,01,500 3,55,625 3,55,625 3,55,625 3,55,625 14,22,500 -21000 -1% Favourable

2,34,625 2,34,625 2,34,625 2,34,625 9,38,500 83,750 3,77,750 2,79,750 83,750 8,25,000 113500 12% Unfavourable

58,656 58,656 58,656 58,656 2,34,625 20,938 94,438 69,938 20,938 2,06,250 28375 12% Favourable

1,75,969 1,75,969 1,75,969 1,75,969 7,03,875 62,813 2,83,313 2,09,813 62,813 6,18,750 85125 12% Unfavourable

NET PROFIT (BEFORE

INTEREST & TAX)

Income Tax Expense

(25%Net)

NET PROFIT AFTER TAX

General & Administrative Expenses

Accounting fees

Legal fees

Bank charges

Office supplies

Postage & printing

Dues & subscriptions

Advertising

Occupancy Costs

TOTAL EXPENSES

Telephone

Repairs & maintenance

Payroll tax

Water

Waste removal

Actual FY 2011/2012

Marketing Expenses

Employment Expenses

Superannuation

Wages & salaries

Staff amenities

Electricity

Insurance

Rates

EXPENSES

REVENUE

Gross Profit

Commissions (2% sales)

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Variance FY 2011/2012Master Budget FY 2011/2012

Rent

Direct wages fixed

Cost of Goods Sold

Sales

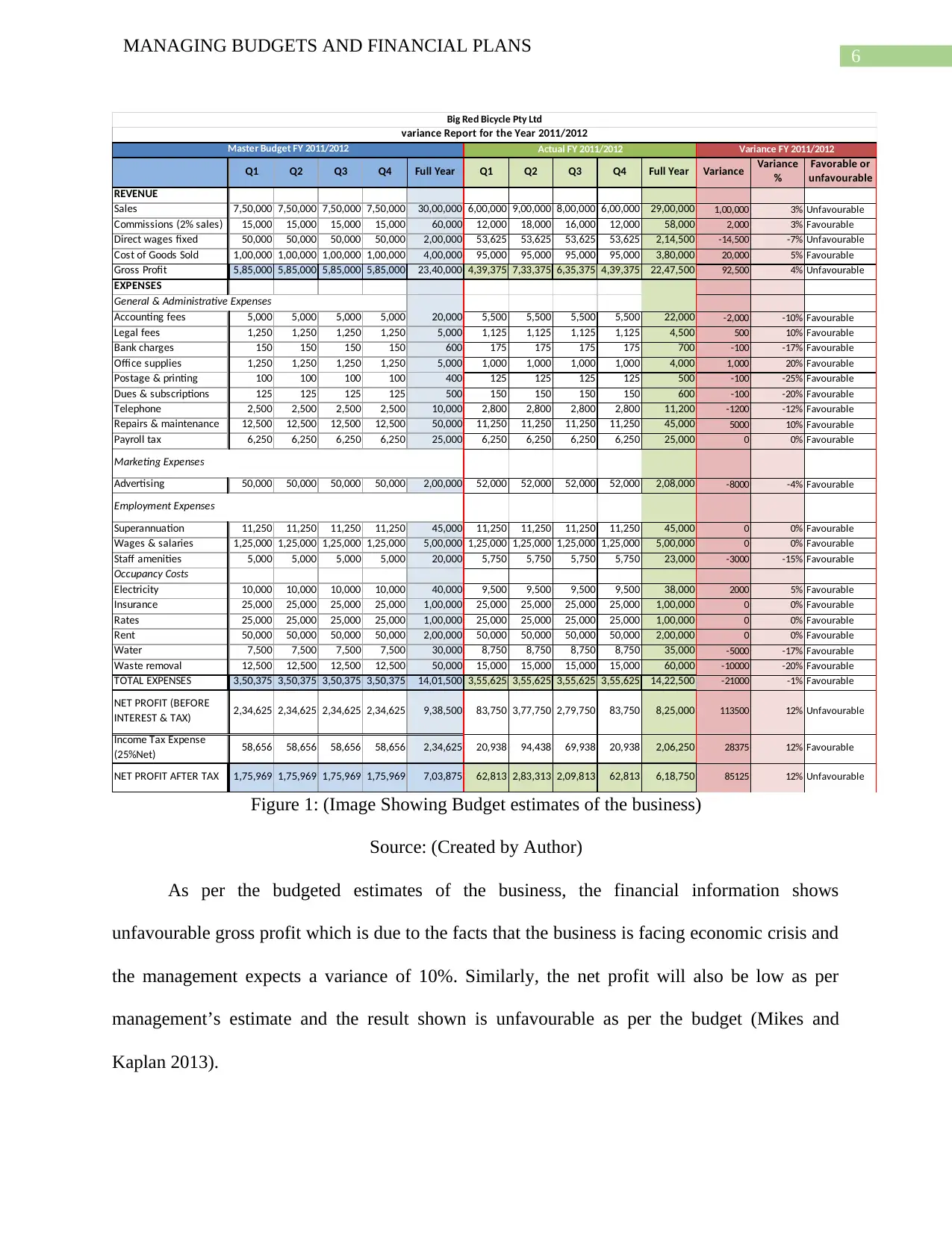

Figure 1: (Image Showing Budget estimates of the business)

Source: (Created by Author)

As per the budgeted estimates of the business, the financial information shows

unfavourable gross profit which is due to the facts that the business is facing economic crisis and

the management expects a variance of 10%. Similarly, the net profit will also be low as per

management’s estimate and the result shown is unfavourable as per the budget (Mikes and

Kaplan 2013).

MANAGING BUDGETS AND FINANCIAL PLANS

Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full Year Variance Variance

%

Favorable or

unfavourable

7,50,000 7,50,000 7,50,000 7,50,000 30,00,000 6,00,000 9,00,000 8,00,000 6,00,000 29,00,000 1,00,000 3% Unfavourable

15,000 15,000 15,000 15,000 60,000 12,000 18,000 16,000 12,000 58,000 2,000 3% Favourable

50,000 50,000 50,000 50,000 2,00,000 53,625 53,625 53,625 53,625 2,14,500 -14,500 -7% Unfavourable

1,00,000 1,00,000 1,00,000 1,00,000 4,00,000 95,000 95,000 95,000 95,000 3,80,000 20,000 5% Favourable

5,85,000 5,85,000 5,85,000 5,85,000 23,40,000 4,39,375 7,33,375 6,35,375 4,39,375 22,47,500 92,500 4% Unfavourable

5,000 5,000 5,000 5,000 20,000 5,500 5,500 5,500 5,500 22,000 -2,000 -10% Favourable

1,250 1,250 1,250 1,250 5,000 1,125 1,125 1,125 1,125 4,500 500 10% Favourable

150 150 150 150 600 175 175 175 175 700 -100 -17% Favourable

1,250 1,250 1,250 1,250 5,000 1,000 1,000 1,000 1,000 4,000 1,000 20% Favourable

100 100 100 100 400 125 125 125 125 500 -100 -25% Favourable

125 125 125 125 500 150 150 150 150 600 -100 -20% Favourable

2,500 2,500 2,500 2,500 10,000 2,800 2,800 2,800 2,800 11,200 -1200 -12% Favourable

12,500 12,500 12,500 12,500 50,000 11,250 11,250 11,250 11,250 45,000 5000 10% Favourable

6,250 6,250 6,250 6,250 25,000 6,250 6,250 6,250 6,250 25,000 0 0% Favourable

50,000 50,000 50,000 50,000 2,00,000 52,000 52,000 52,000 52,000 2,08,000 -8000 -4% Favourable

11,250 11,250 11,250 11,250 45,000 11,250 11,250 11,250 11,250 45,000 0 0% Favourable

1,25,000 1,25,000 1,25,000 1,25,000 5,00,000 1,25,000 1,25,000 1,25,000 1,25,000 5,00,000 0 0% Favourable

5,000 5,000 5,000 5,000 20,000 5,750 5,750 5,750 5,750 23,000 -3000 -15% Favourable

10,000 10,000 10,000 10,000 40,000 9,500 9,500 9,500 9,500 38,000 2000 5% Favourable

25,000 25,000 25,000 25,000 1,00,000 25,000 25,000 25,000 25,000 1,00,000 0 0% Favourable

25,000 25,000 25,000 25,000 1,00,000 25,000 25,000 25,000 25,000 1,00,000 0 0% Favourable

50,000 50,000 50,000 50,000 2,00,000 50,000 50,000 50,000 50,000 2,00,000 0 0% Favourable

7,500 7,500 7,500 7,500 30,000 8,750 8,750 8,750 8,750 35,000 -5000 -17% Favourable

12,500 12,500 12,500 12,500 50,000 15,000 15,000 15,000 15,000 60,000 -10000 -20% Favourable

3,50,375 3,50,375 3,50,375 3,50,375 14,01,500 3,55,625 3,55,625 3,55,625 3,55,625 14,22,500 -21000 -1% Favourable

2,34,625 2,34,625 2,34,625 2,34,625 9,38,500 83,750 3,77,750 2,79,750 83,750 8,25,000 113500 12% Unfavourable

58,656 58,656 58,656 58,656 2,34,625 20,938 94,438 69,938 20,938 2,06,250 28375 12% Favourable

1,75,969 1,75,969 1,75,969 1,75,969 7,03,875 62,813 2,83,313 2,09,813 62,813 6,18,750 85125 12% Unfavourable

NET PROFIT (BEFORE

INTEREST & TAX)

Income Tax Expense

(25%Net)

NET PROFIT AFTER TAX

General & Administrative Expenses

Accounting fees

Legal fees

Bank charges

Office supplies

Postage & printing

Dues & subscriptions

Advertising

Occupancy Costs

TOTAL EXPENSES

Telephone

Repairs & maintenance

Payroll tax

Water

Waste removal

Actual FY 2011/2012

Marketing Expenses

Employment Expenses

Superannuation

Wages & salaries

Staff amenities

Electricity

Insurance

Rates

EXPENSES

REVENUE

Gross Profit

Commissions (2% sales)

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Variance FY 2011/2012Master Budget FY 2011/2012

Rent

Direct wages fixed

Cost of Goods Sold

Sales

Figure 1: (Image Showing Budget estimates of the business)

Source: (Created by Author)

As per the budgeted estimates of the business, the financial information shows

unfavourable gross profit which is due to the facts that the business is facing economic crisis and

the management expects a variance of 10%. Similarly, the net profit will also be low as per

management’s estimate and the result shown is unfavourable as per the budget (Mikes and

Kaplan 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGING BUDGETS AND FINANCIAL PLANS

Changes in budget

The changes which can be recommended are given below in details:

1. The overall commission of the business is kept same for every center and this is not

realistic as it is clear that the such needs to be changed (Mutanov 2016). The company

needs to incorporate a new plan where in the center with production is given more

compensation as this way more motivation can be provided and in addition the company

also needs to provide more wages to the employee of Sales Center A

2. The management needs to change the recording criteria from repairs as such expenses

cannot be given for every quarter and thus such looks unrealistic in nature.

3. As per the master budget the sales of the company are evenly placed for each quarter

which is unrealistic and the management needs to change the same (Popesko and Socova

2016).

Assessment 2

As per the budget of the company, the different sales employee of the business needs to

be communicated the different targets of sales which the management of the company wants to

pursue. The sales employees need to be clear about the sales target of the business and also the

various changes which are to be incorporated in the budget (Kerzner and Kerzner 2017). The

sales of the company as per the budget during the second quarter is more than the sales figure of

all other quarter. The budget also makes it clear that the expenses of the company needs to be

maintained. The cost which will be incurred by the company is estimated to be fixed through the

quarters.

The financial objective of the management is to generate a net profit of $ 1,000,000. In

order to achieve this the management in its budget has estimated costs to be reduced. The

MANAGING BUDGETS AND FINANCIAL PLANS

Changes in budget

The changes which can be recommended are given below in details:

1. The overall commission of the business is kept same for every center and this is not

realistic as it is clear that the such needs to be changed (Mutanov 2016). The company

needs to incorporate a new plan where in the center with production is given more

compensation as this way more motivation can be provided and in addition the company

also needs to provide more wages to the employee of Sales Center A

2. The management needs to change the recording criteria from repairs as such expenses

cannot be given for every quarter and thus such looks unrealistic in nature.

3. As per the master budget the sales of the company are evenly placed for each quarter

which is unrealistic and the management needs to change the same (Popesko and Socova

2016).

Assessment 2

As per the budget of the company, the different sales employee of the business needs to

be communicated the different targets of sales which the management of the company wants to

pursue. The sales employees need to be clear about the sales target of the business and also the

various changes which are to be incorporated in the budget (Kerzner and Kerzner 2017). The

sales of the company as per the budget during the second quarter is more than the sales figure of

all other quarter. The budget also makes it clear that the expenses of the company needs to be

maintained. The cost which will be incurred by the company is estimated to be fixed through the

quarters.

The financial objective of the management is to generate a net profit of $ 1,000,000. In

order to achieve this the management in its budget has estimated costs to be reduced. The

8

MANAGING BUDGETS AND FINANCIAL PLANS

different sales center which are Sales Center A, B and C respectively have also been allocated

their targets of the sales estimate which are to be achieved by them. The wages which have been

allocated to each sales center as per the budget shows $ 1,00,000 is allocated to each center and

in addition to this, supplies worth $ 1,000 is allocated to all the centers. The commission which

allowable to different employee for each center’s totals to about $ 20,000. The sales manager of

Center A needs to communicate the various allocations which are made.

Financial Policies of the Company

In order to achieve the targets which are set by the budget the management of the

company needs to formulate an effective training plan for the employee so that they are able to

manage different resources of the business effectively. The training plan of the company will be

including handling petty cash of the business, tracking of expenses with the help of spreadsheets,

financial policies of the company (Gamayuni 2015).

As per the case which is provided in the question, an individual Bill has been selected to

handle the petty cash for the business. Bill needs to be trained in handling spreadsheet in order to

keep track of the expenses which are incurred by the management of the company. The financial

policies of the business focuses on handling of petty cash expense and tracking of expenses

which is the responsibility which is given to Bill. The business has the policy of reimbursing

expenses which are made by the employees of the organization on behalf of the organization.

The only condition is that the expenses should be a genuine one and appropriate for the business.

However certain expenses will not be reimbursed for example, late fines, amount which are

recoverable from third parties. In addition to this Bill also needs to learn how to use spreadsheet

and implement changes in them. The spreadsheet will be useful in order to keep track of the

expenses which are incurred by the business (Slezà et al. 2014).

MANAGING BUDGETS AND FINANCIAL PLANS

different sales center which are Sales Center A, B and C respectively have also been allocated

their targets of the sales estimate which are to be achieved by them. The wages which have been

allocated to each sales center as per the budget shows $ 1,00,000 is allocated to each center and

in addition to this, supplies worth $ 1,000 is allocated to all the centers. The commission which

allowable to different employee for each center’s totals to about $ 20,000. The sales manager of

Center A needs to communicate the various allocations which are made.

Financial Policies of the Company

In order to achieve the targets which are set by the budget the management of the

company needs to formulate an effective training plan for the employee so that they are able to

manage different resources of the business effectively. The training plan of the company will be

including handling petty cash of the business, tracking of expenses with the help of spreadsheets,

financial policies of the company (Gamayuni 2015).

As per the case which is provided in the question, an individual Bill has been selected to

handle the petty cash for the business. Bill needs to be trained in handling spreadsheet in order to

keep track of the expenses which are incurred by the management of the company. The financial

policies of the business focuses on handling of petty cash expense and tracking of expenses

which is the responsibility which is given to Bill. The business has the policy of reimbursing

expenses which are made by the employees of the organization on behalf of the organization.

The only condition is that the expenses should be a genuine one and appropriate for the business.

However certain expenses will not be reimbursed for example, late fines, amount which are

recoverable from third parties. In addition to this Bill also needs to learn how to use spreadsheet

and implement changes in them. The spreadsheet will be useful in order to keep track of the

expenses which are incurred by the business (Slezà et al. 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGING BUDGETS AND FINANCIAL PLANS

In case of Petty cash handling, the cash ill be handled by an individual who will have a

replacement in case the former is sick. In addition to this an amount which is in excess of $ 800

needs to be banked as soon as possible. The petty cash balance is to be kept in a safe and will be

used to reimburse employees who have incurred expenses on behalf of the company (Hailu,

Awash and Teshome 2014).

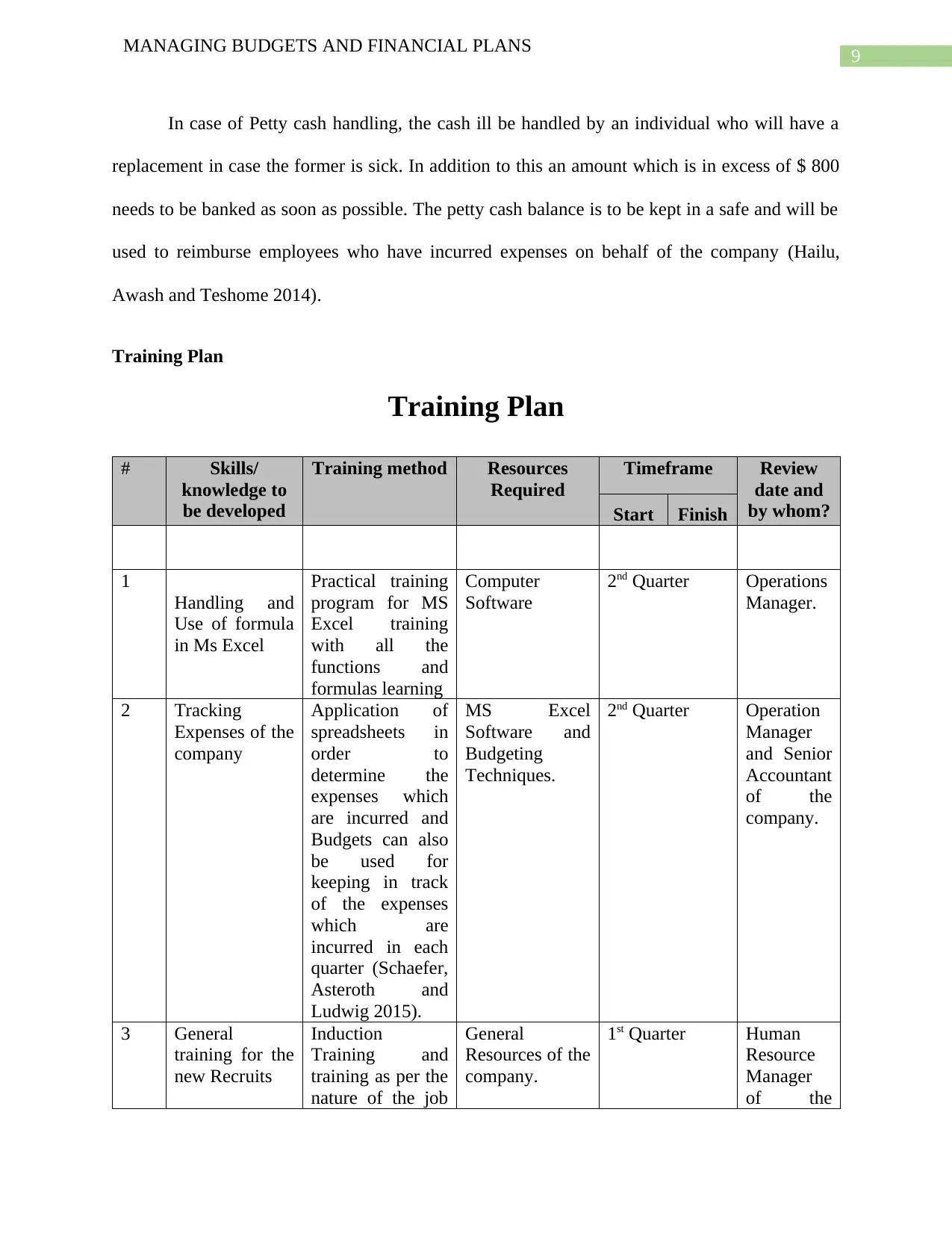

Training Plan

Training Plan

# Skills/

knowledge to

be developed

Training method Resources

Required

Timeframe Review

date and

by whom?Start Finish

1

Handling and

Use of formula

in Ms Excel

Practical training

program for MS

Excel training

with all the

functions and

formulas learning

Computer

Software

2nd Quarter Operations

Manager.

2 Tracking

Expenses of the

company

Application of

spreadsheets in

order to

determine the

expenses which

are incurred and

Budgets can also

be used for

keeping in track

of the expenses

which are

incurred in each

quarter (Schaefer,

Asteroth and

Ludwig 2015).

MS Excel

Software and

Budgeting

Techniques.

2nd Quarter Operation

Manager

and Senior

Accountant

of the

company.

3 General

training for the

new Recruits

Induction

Training and

training as per the

nature of the job

General

Resources of the

company.

1st Quarter Human

Resource

Manager

of the

MANAGING BUDGETS AND FINANCIAL PLANS

In case of Petty cash handling, the cash ill be handled by an individual who will have a

replacement in case the former is sick. In addition to this an amount which is in excess of $ 800

needs to be banked as soon as possible. The petty cash balance is to be kept in a safe and will be

used to reimburse employees who have incurred expenses on behalf of the company (Hailu,

Awash and Teshome 2014).

Training Plan

Training Plan

# Skills/

knowledge to

be developed

Training method Resources

Required

Timeframe Review

date and

by whom?Start Finish

1

Handling and

Use of formula

in Ms Excel

Practical training

program for MS

Excel training

with all the

functions and

formulas learning

Computer

Software

2nd Quarter Operations

Manager.

2 Tracking

Expenses of the

company

Application of

spreadsheets in

order to

determine the

expenses which

are incurred and

Budgets can also

be used for

keeping in track

of the expenses

which are

incurred in each

quarter (Schaefer,

Asteroth and

Ludwig 2015).

MS Excel

Software and

Budgeting

Techniques.

2nd Quarter Operation

Manager

and Senior

Accountant

of the

company.

3 General

training for the

new Recruits

Induction

Training and

training as per the

nature of the job

General

Resources of the

company.

1st Quarter Human

Resource

Manager

of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGING BUDGETS AND FINANCIAL PLANS

applied by every

individual

company.

4

Sales

operations

Communication

skills

development,

sales records

handling.

Vocational

training, ledger

of sales records

for maintaining

sales of the

business

1st Quarter Sales

Manager

of the

company

5 Motivational

and Induction

training

Presentation and

Surveys are used

Companies past

performance

and positioning

of the business

in the market

surveys,

records, charts

and graphs.

1st Quarter CEO and

Managing

Director of

the

company.

The various financial resources which are used by the management of the different

departments can be done with the help of budgets which can help the management to keep track

of the performance of the business.

Assessment 3

Budget Preparation

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Master Budget FY 2011/2012 Actual FY 2011/2012

Variance FY

2011/2012

Q1 Q2 Q3 Q4

Full

Yea

r

Q1 Q2 Q3 Q4

Full

Yea

r

Var

ian

ce

Var

ian

ce

%

Favor

able

or

unfav

ourab

le

REVEN

UE

Sales 7,5

0,0

7,5

0,0

7,5

0,0

7,5

0,0

30,0

0,00

6,0

0,0

9,0

0,0

8,0

0,0

6,0

0,0

29,0

0,00

1,00

,000

3% Unfav

ourabl

MANAGING BUDGETS AND FINANCIAL PLANS

applied by every

individual

company.

4

Sales

operations

Communication

skills

development,

sales records

handling.

Vocational

training, ledger

of sales records

for maintaining

sales of the

business

1st Quarter Sales

Manager

of the

company

5 Motivational

and Induction

training

Presentation and

Surveys are used

Companies past

performance

and positioning

of the business

in the market

surveys,

records, charts

and graphs.

1st Quarter CEO and

Managing

Director of

the

company.

The various financial resources which are used by the management of the different

departments can be done with the help of budgets which can help the management to keep track

of the performance of the business.

Assessment 3

Budget Preparation

Big Red Bicycle Pty Ltd

variance Report for the Year 2011/2012

Master Budget FY 2011/2012 Actual FY 2011/2012

Variance FY

2011/2012

Q1 Q2 Q3 Q4

Full

Yea

r

Q1 Q2 Q3 Q4

Full

Yea

r

Var

ian

ce

Var

ian

ce

%

Favor

able

or

unfav

ourab

le

REVEN

UE

Sales 7,5

0,0

7,5

0,0

7,5

0,0

7,5

0,0

30,0

0,00

6,0

0,0

9,0

0,0

8,0

0,0

6,0

0,0

29,0

0,00

1,00

,000

3% Unfav

ourabl

11

MANAGING BUDGETS AND FINANCIAL PLANS

00 00 00 00 0 00 00 00 00 0 e

Commi

ssions

(2%

sales)

15,

000

15,

000

15,

000

15,

000

60,0

00

12,

000

18,

000

16,

000

12,

000

58,0

00 2,00

0 3%

Favou

rable

Direct

wages

fixed

50,

000

50,

000

50,

000

50,

000

2,00

,000

53,

625

53,

625

53,

625

53,

625

2,14

,500

-

14,5

00 -7%

Unfav

ourabl

e

Cost of

Goods

Sold

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

4,00

,000

95,

000

95,

000

95,

000

95,

000

3,80

,000 20,0

00 5%

Favou

rable

Gross

Profit

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

23,4

0,00

0

4,3

9,3

75

7,3

3,3

75

6,3

5,3

75

4,3

9,3

75

22,4

7,50

0

92,5

00 4%

Unfav

ourabl

e

EXPEN

SES

General & Administrative

Expenses

Accou

nting

fees

5,0

00

5,0

00

5,0

00

5,0

00

20,0

00

5,5

00

5,5

00

5,5

00

5,5

00

22,0

00

-

2,00

0

-

10%

Favou

rable

Legal

fees

1,2

50

1,2

50

1,2

50

1,2

50

5,00

0

1,1

25

1,1

25

1,1

25

1,1

25

4,50

0 500 10%

Favou

rable

Bank

charge

s

150 150 150 150 600 175 175 175 175 700 -

100

-

17%

Favou

rable

Office

supplie

s

1,2

50

1,2

50

1,2

50

1,2

50

5,00

0

1,0

00

1,0

00

1,0

00

1,0

00

4,00

0 1,00

0 20%

Favou

rable

Postag

e &

printin

g

100 100 100 100 400 125 125 125 125 500 -

100

-

25%

Favou

rable

Dues &

subscri

ptions

125 125 125 125 500 150 150 150 150 600 -

100

-

20%

Favou

rable

Teleph

one

2,5

00

2,5

00

2,5

00

2,5

00

10,0

00

2,8

00

2,8

00

2,8

00

2,8

00

11,2

00

-

120

0

-

12%

Favou

rable

Repair

s &

mainte

nance

12,

500

12,

500

12,

500

12,

500

50,0

00

11,

250

11,

250

11,

250

11,

250

45,0

00 500

0 10%

Favou

rable

MANAGING BUDGETS AND FINANCIAL PLANS

00 00 00 00 0 00 00 00 00 0 e

Commi

ssions

(2%

sales)

15,

000

15,

000

15,

000

15,

000

60,0

00

12,

000

18,

000

16,

000

12,

000

58,0

00 2,00

0 3%

Favou

rable

Direct

wages

fixed

50,

000

50,

000

50,

000

50,

000

2,00

,000

53,

625

53,

625

53,

625

53,

625

2,14

,500

-

14,5

00 -7%

Unfav

ourabl

e

Cost of

Goods

Sold

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

1,0

0,0

00

4,00

,000

95,

000

95,

000

95,

000

95,

000

3,80

,000 20,0

00 5%

Favou

rable

Gross

Profit

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

5,8

5,0

00

23,4

0,00

0

4,3

9,3

75

7,3

3,3

75

6,3

5,3

75

4,3

9,3

75

22,4

7,50

0

92,5

00 4%

Unfav

ourabl

e

EXPEN

SES

General & Administrative

Expenses

Accou

nting

fees

5,0

00

5,0

00

5,0

00

5,0

00

20,0

00

5,5

00

5,5

00

5,5

00

5,5

00

22,0

00

-

2,00

0

-

10%

Favou

rable

Legal

fees

1,2

50

1,2

50

1,2

50

1,2

50

5,00

0

1,1

25

1,1

25

1,1

25

1,1

25

4,50

0 500 10%

Favou

rable

Bank

charge

s

150 150 150 150 600 175 175 175 175 700 -

100

-

17%

Favou

rable

Office

supplie

s

1,2

50

1,2

50

1,2

50

1,2

50

5,00

0

1,0

00

1,0

00

1,0

00

1,0

00

4,00

0 1,00

0 20%

Favou

rable

Postag

e &

printin

g

100 100 100 100 400 125 125 125 125 500 -

100

-

25%

Favou

rable

Dues &

subscri

ptions

125 125 125 125 500 150 150 150 150 600 -

100

-

20%

Favou

rable

Teleph

one

2,5

00

2,5

00

2,5

00

2,5

00

10,0

00

2,8

00

2,8

00

2,8

00

2,8

00

11,2

00

-

120

0

-

12%

Favou

rable

Repair

s &

mainte

nance

12,

500

12,

500

12,

500

12,

500

50,0

00

11,

250

11,

250

11,

250

11,

250

45,0

00 500

0 10%

Favou

rable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.