Performance and Knowledge Assessment: BSBFIM501 Manage Budgets

VerifiedAdded on 2022/09/15

|17

|2722

|18

Homework Assignment

AI Summary

This document presents a comprehensive solution for the BSBFIM501 Manage Budgets and Financial Plans assessment. It begins with an overview of the assessment, including its purpose, format, and required resources. The solution provides detailed answers to short answer questions covering key accounting concepts such as the accounting equation, ledger accounts, current liabilities, and the calculation of gross and net profit. The document then includes a completed balance sheet based on provided figures, demonstrating the application of accounting principles. Finally, the solution offers answers to multiple-choice questions, testing the student's understanding of topics such as cash accounting, business ownership, financial statements, budgeting, and variance analysis. The document ensures a thorough understanding of the assessment requirements, providing a complete and accurate solution to help students prepare for and succeed in their assessment.

Course Details

Course Name

Unit(s) of competency

Unit Code (s) and

Names BSBFIM501 Manage Budgets and Financial Plans

Assessment Details

Term and Year Time allowed

Assessment No Assessment Weighting

Assessment

Descriptor

Due Date Extension (if approved)

Re-Assessment Details

Term and Year Time allowed

Assessment No Re-assessment Fee Paid?

Assessment Type

Due Date No Extension

Student Details and Declaration

Student Name

Student ID Trainer/

Assessor’s Name

Student Declaration:

a. I declare that the work submitted is my own and has

not been copied or plagiarised from any person or

source.

b. I have not submitted any part of this assignment

previously as part of another unit/course.

c. I acknowledge that I understand the requirements to

complete the assessment tasks.

d. The assessment process including the provisions

for re-submitting and academic appeals were

explained to me and I understand these processes.

Signature:

_________________________________

_

Date: _______/________/______

Assessment Outcome - To be completed by the Assessor

Assessor’s Name

Results Satisfactory Not

Satisfactory Marks:

Re-assessment

eligibility Yes No Due Date:

This assessment First Attempt 2nd Attempt Late Penalty__________

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 1 of 17

Course Name

Unit(s) of competency

Unit Code (s) and

Names BSBFIM501 Manage Budgets and Financial Plans

Assessment Details

Term and Year Time allowed

Assessment No Assessment Weighting

Assessment

Descriptor

Due Date Extension (if approved)

Re-Assessment Details

Term and Year Time allowed

Assessment No Re-assessment Fee Paid?

Assessment Type

Due Date No Extension

Student Details and Declaration

Student Name

Student ID Trainer/

Assessor’s Name

Student Declaration:

a. I declare that the work submitted is my own and has

not been copied or plagiarised from any person or

source.

b. I have not submitted any part of this assignment

previously as part of another unit/course.

c. I acknowledge that I understand the requirements to

complete the assessment tasks.

d. The assessment process including the provisions

for re-submitting and academic appeals were

explained to me and I understand these processes.

Signature:

_________________________________

_

Date: _______/________/______

Assessment Outcome - To be completed by the Assessor

Assessor’s Name

Results Satisfactory Not

Satisfactory Marks:

Re-assessment

eligibility Yes No Due Date:

This assessment First Attempt 2nd Attempt Late Penalty__________

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 1 of 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FEEDBACK TO STUDENT

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit and I have been advised of my

result. I am also aware of my right to appeal and the

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

FEEDBACK TO STUDENT (FOR REASSESSMENTONLY)

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been re-

assessed in this unit and I have been advised of my

result. I am also aware of my right to appeal.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 2 of 17

Progressive feedback to students, identifying gaps in competency and comments on positive improvements:

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been

assessed in this unit and I have been advised of my

result. I am also aware of my right to appeal and the

reassessment procedure.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

FEEDBACK TO STUDENT (FOR REASSESSMENTONLY)

______________________________________________________________________________________

______________________________________________________________________________________

______________________________________________________________________________________

Student Declaration: I declare that I have been re-

assessed in this unit and I have been advised of my

result. I am also aware of my right to appeal.

Signature: ____________________________

Date: ____/_____/_____

Assessor Declaration: I declare that I have

conducted a fair, valid, reliable and flexible

assessment with this student, and I have provided

appropriate feedback

Student did not attend the feedback session.

Feedback provided on assessment.

Signature: ____________________________

Date: ____/_____/_____

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 2 of 17

Assessment Activity

(Performance and Knowledge)

SITXFIN004

Prepare and monitor budgets

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 3 of 17

(Performance and Knowledge)

SITXFIN004

Prepare and monitor budgets

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 3 of 17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DOCUMENT CONTROL

VERSION DATE COMMENTS

1.0 18th September 2015 Initial

ASSESSOR PRE-ASSESSMENT CHECKLIST

This checklist is to be completed prior to commencing the assessment.

Please discuss this with the learner and circle yes or no for each question.

Is the learner ready for assessment? ☐Yes ☐ No

Have you explained the assessment process and tasks? ☐ Yes ☐No

Does the learner understand which evidence is to be collected and

how?

☐ Yes ☐No

Have the learner’s rights and the appeal system been fully explained? ☐ Yes ☐No

Have you discussed any special needs or reasonable adjustments to be

considered during the assessment?

☐ Yes ☐No

Does the learner have access to all required resources? ☐ Yes ☐No

ASSESSMENT INSTRUCTIONS

PURPOSE OF THE ASSESSMENT TASK

Assessment Tool Performance and Knowledge (Examination)

To demonstrate satisfactory completion of this Assessment

Task the learner must:

Satisfactory

(S)

Not Satisfactory

(NS)

Part A: Short Answer Responses completed ☐ ☐

Part B: Construct a Balance Sheet ☐ ☐

Part C: Multiple Choice Questions ☐ ☐

Overall Assessment Task Performance Satisfactory

(S)

Not Satisfactory

(NS)

Assessment Task: Performance and Knowledge

(Examination) ☐ ☐

Resources required for this Assessment

Trainers and Assessors are required to ensure all learners have access to:

Resources and documentation used in the workplace

Workplace policies and procedures

Workplace budgets and financial plans

Business technology

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 4 of 17

VERSION DATE COMMENTS

1.0 18th September 2015 Initial

ASSESSOR PRE-ASSESSMENT CHECKLIST

This checklist is to be completed prior to commencing the assessment.

Please discuss this with the learner and circle yes or no for each question.

Is the learner ready for assessment? ☐Yes ☐ No

Have you explained the assessment process and tasks? ☐ Yes ☐No

Does the learner understand which evidence is to be collected and

how?

☐ Yes ☐No

Have the learner’s rights and the appeal system been fully explained? ☐ Yes ☐No

Have you discussed any special needs or reasonable adjustments to be

considered during the assessment?

☐ Yes ☐No

Does the learner have access to all required resources? ☐ Yes ☐No

ASSESSMENT INSTRUCTIONS

PURPOSE OF THE ASSESSMENT TASK

Assessment Tool Performance and Knowledge (Examination)

To demonstrate satisfactory completion of this Assessment

Task the learner must:

Satisfactory

(S)

Not Satisfactory

(NS)

Part A: Short Answer Responses completed ☐ ☐

Part B: Construct a Balance Sheet ☐ ☐

Part C: Multiple Choice Questions ☐ ☐

Overall Assessment Task Performance Satisfactory

(S)

Not Satisfactory

(NS)

Assessment Task: Performance and Knowledge

(Examination) ☐ ☐

Resources required for this Assessment

Trainers and Assessors are required to ensure all learners have access to:

Resources and documentation used in the workplace

Workplace policies and procedures

Workplace budgets and financial plans

Business technology

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 4 of 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

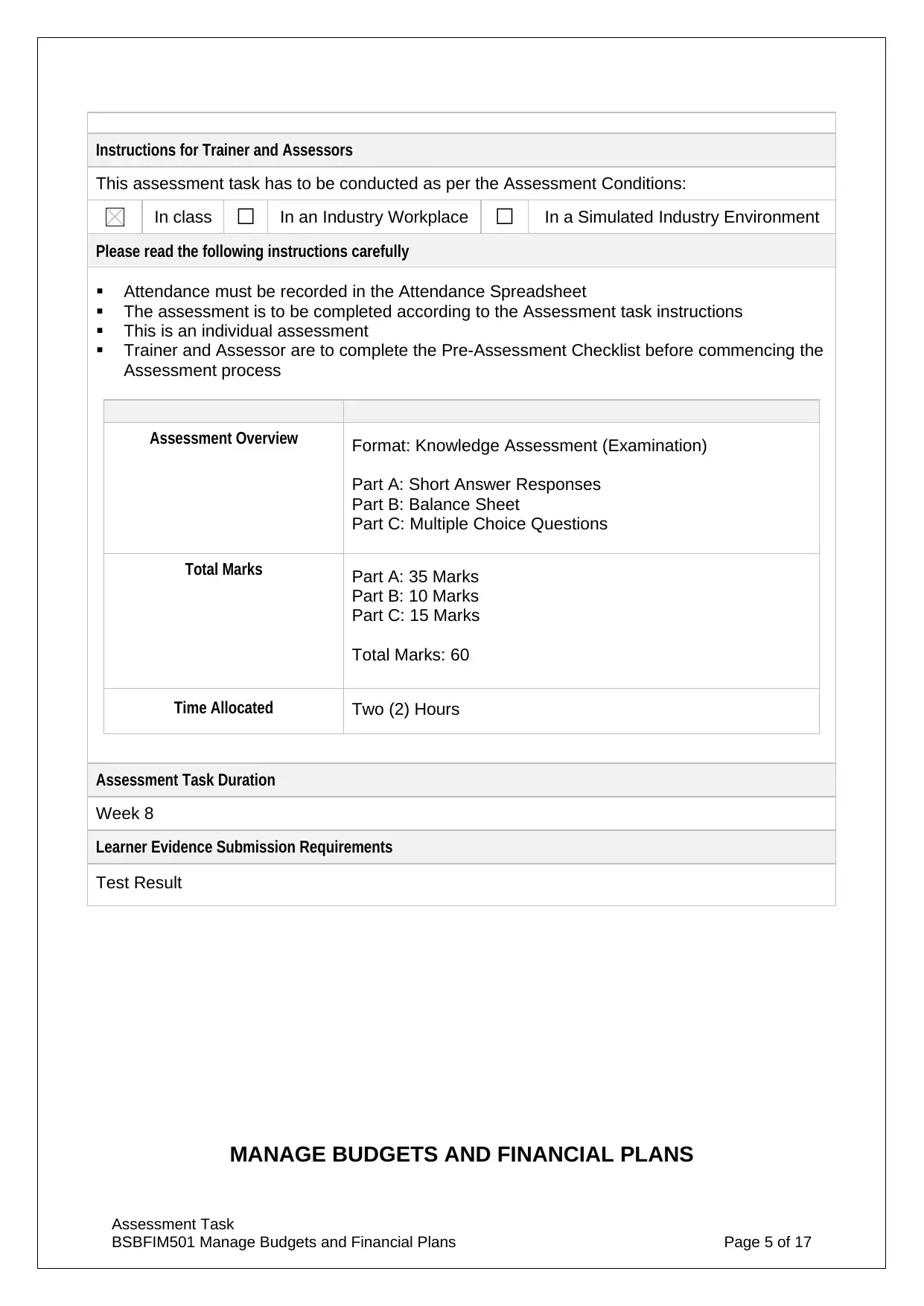

Instructions for Trainer and Assessors

This assessment task has to be conducted as per the Assessment Conditions:

In class ☐ In an Industry Workplace ☐ In a Simulated Industry Environment

Please read the following instructions carefully

Attendance must be recorded in the Attendance Spreadsheet

The assessment is to be completed according to the Assessment task instructions

This is an individual assessment

Trainer and Assessor are to complete the Pre-Assessment Checklist before commencing the

Assessment process

Assessment Overview Format: Knowledge Assessment (Examination)

Part A: Short Answer Responses

Part B: Balance Sheet

Part C: Multiple Choice Questions

Total Marks Part A: 35 Marks

Part B: 10 Marks

Part C: 15 Marks

Total Marks: 60

Time Allocated Two (2) Hours

Assessment Task Duration

Week 8

Learner Evidence Submission Requirements

Test Result

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 5 of 17

This assessment task has to be conducted as per the Assessment Conditions:

In class ☐ In an Industry Workplace ☐ In a Simulated Industry Environment

Please read the following instructions carefully

Attendance must be recorded in the Attendance Spreadsheet

The assessment is to be completed according to the Assessment task instructions

This is an individual assessment

Trainer and Assessor are to complete the Pre-Assessment Checklist before commencing the

Assessment process

Assessment Overview Format: Knowledge Assessment (Examination)

Part A: Short Answer Responses

Part B: Balance Sheet

Part C: Multiple Choice Questions

Total Marks Part A: 35 Marks

Part B: 10 Marks

Part C: 15 Marks

Total Marks: 60

Time Allocated Two (2) Hours

Assessment Task Duration

Week 8

Learner Evidence Submission Requirements

Test Result

MANAGE BUDGETS AND FINANCIAL PLANS

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 5 of 17

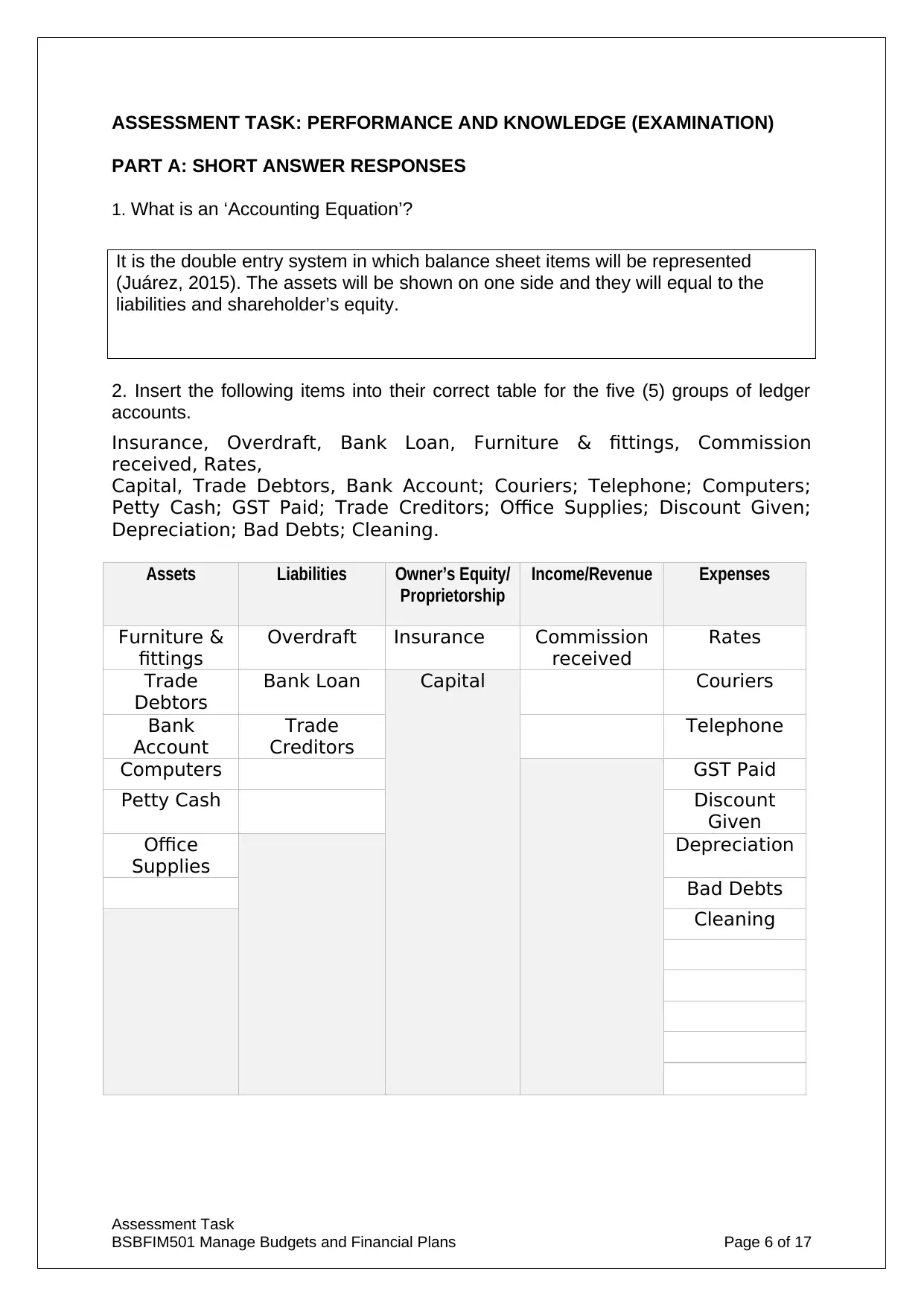

ASSESSMENT TASK: PERFORMANCE AND KNOWLEDGE (EXAMINATION)

PART A: SHORT ANSWER RESPONSES

1. What is an ‘Accounting Equation’?

It is the double entry system in which balance sheet items will be represented

(Juárez, 2015). The assets will be shown on one side and they will equal to the

liabilities and shareholder’s equity.

2. Insert the following items into their correct table for the five (5) groups of ledger

accounts.

Insurance, Overdraft, Bank Loan, Furniture & fittings, Commission

received, Rates,

Capital, Trade Debtors, Bank Account; Couriers; Telephone; Computers;

Petty Cash; GST Paid; Trade Creditors; Office Supplies; Discount Given;

Depreciation; Bad Debts; Cleaning.

Assets Liabilities Owner’s Equity/

Proprietorship

Income/Revenue Expenses

Furniture &

fittings

Overdraft Insurance Commission

received

Rates

Trade

Debtors

Bank Loan Capital Couriers

Bank

Account

Trade

Creditors

Telephone

Computers GST Paid

Petty Cash Discount

Given

Office

Supplies

Depreciation

Bad Debts

Cleaning

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 6 of 17

PART A: SHORT ANSWER RESPONSES

1. What is an ‘Accounting Equation’?

It is the double entry system in which balance sheet items will be represented

(Juárez, 2015). The assets will be shown on one side and they will equal to the

liabilities and shareholder’s equity.

2. Insert the following items into their correct table for the five (5) groups of ledger

accounts.

Insurance, Overdraft, Bank Loan, Furniture & fittings, Commission

received, Rates,

Capital, Trade Debtors, Bank Account; Couriers; Telephone; Computers;

Petty Cash; GST Paid; Trade Creditors; Office Supplies; Discount Given;

Depreciation; Bad Debts; Cleaning.

Assets Liabilities Owner’s Equity/

Proprietorship

Income/Revenue Expenses

Furniture &

fittings

Overdraft Insurance Commission

received

Rates

Trade

Debtors

Bank Loan Capital Couriers

Bank

Account

Trade

Creditors

Telephone

Computers GST Paid

Petty Cash Discount

Given

Office

Supplies

Depreciation

Bad Debts

Cleaning

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 6 of 17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

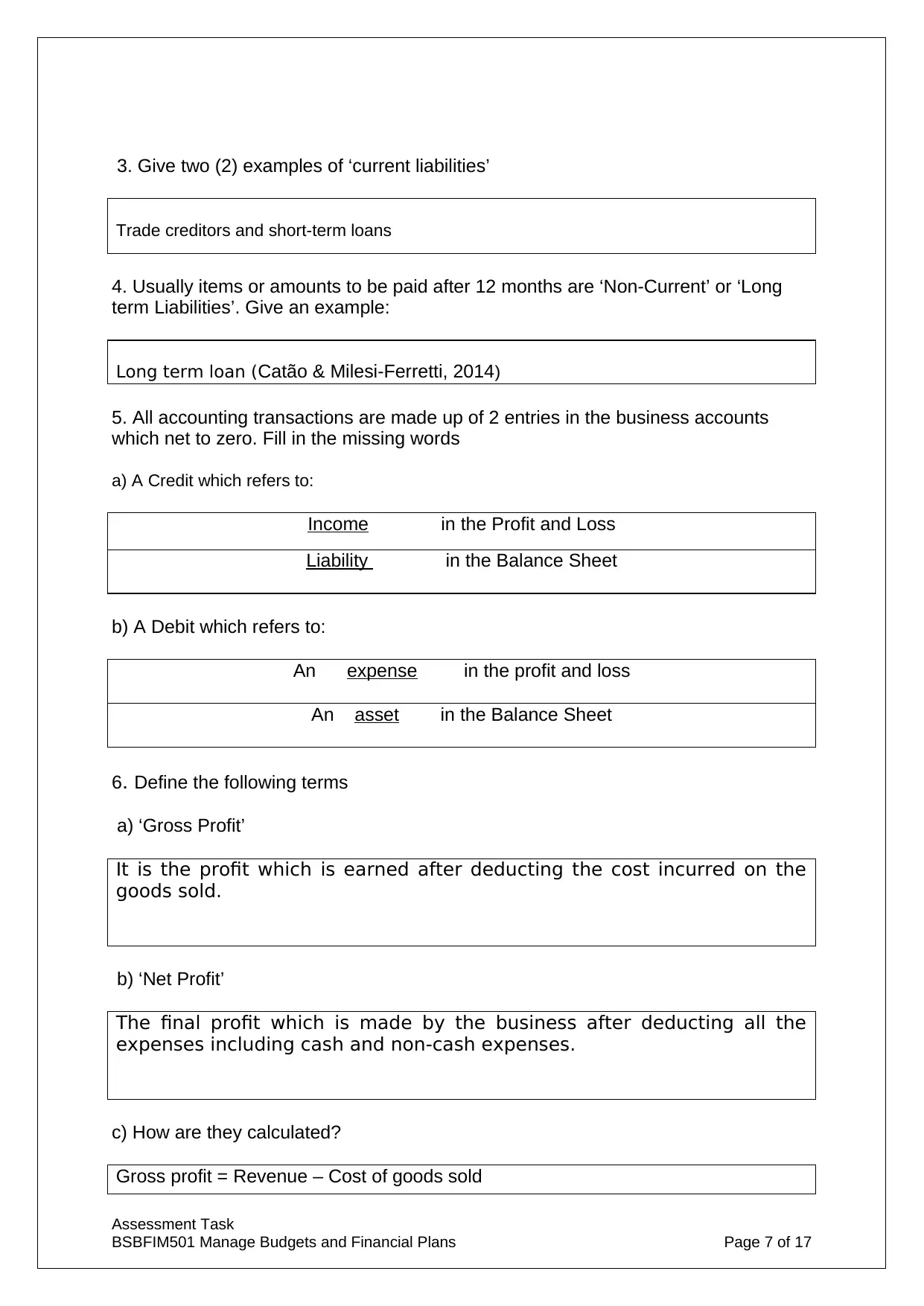

3. Give two (2) examples of ‘current liabilities’

Trade creditors and short-term loans

4. Usually items or amounts to be paid after 12 months are ‘Non-Current’ or ‘Long

term Liabilities’. Give an example:

Long term loan (Catão & Milesi-Ferretti, 2014)

5. All accounting transactions are made up of 2 entries in the business accounts

which net to zero. Fill in the missing words

a) A Credit which refers to:

Income in the Profit and Loss

Liability in the Balance Sheet

b) A Debit which refers to:

An expense in the profit and loss

An asset in the Balance Sheet

6. Define the following terms

a) ‘Gross Profit’

It is the profit which is earned after deducting the cost incurred on the

goods sold.

b) ‘Net Profit’

The final profit which is made by the business after deducting all the

expenses including cash and non-cash expenses.

c) How are they calculated?

Gross profit = Revenue – Cost of goods sold

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 7 of 17

Trade creditors and short-term loans

4. Usually items or amounts to be paid after 12 months are ‘Non-Current’ or ‘Long

term Liabilities’. Give an example:

Long term loan (Catão & Milesi-Ferretti, 2014)

5. All accounting transactions are made up of 2 entries in the business accounts

which net to zero. Fill in the missing words

a) A Credit which refers to:

Income in the Profit and Loss

Liability in the Balance Sheet

b) A Debit which refers to:

An expense in the profit and loss

An asset in the Balance Sheet

6. Define the following terms

a) ‘Gross Profit’

It is the profit which is earned after deducting the cost incurred on the

goods sold.

b) ‘Net Profit’

The final profit which is made by the business after deducting all the

expenses including cash and non-cash expenses.

c) How are they calculated?

Gross profit = Revenue – Cost of goods sold

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 7 of 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

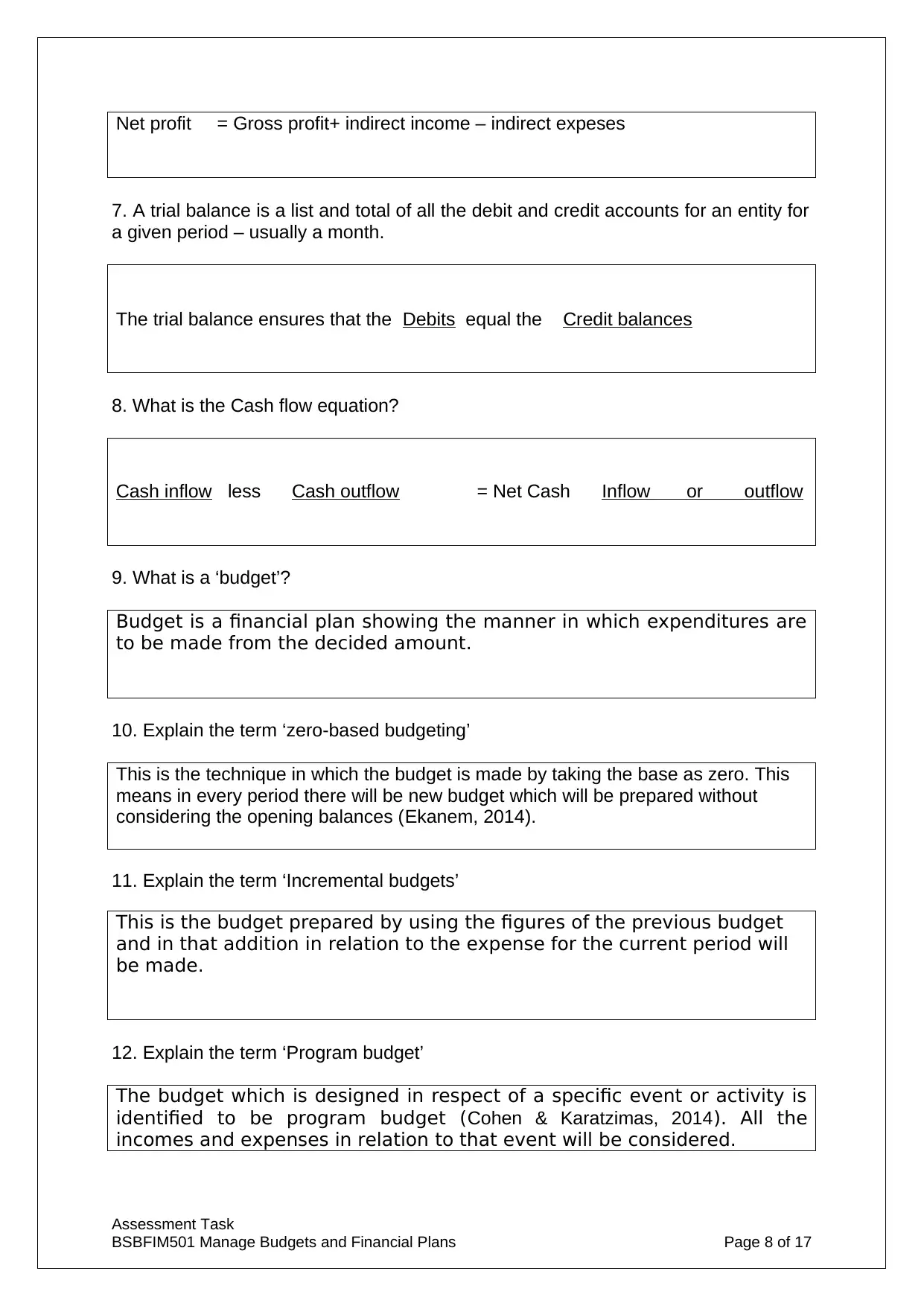

Net profit = Gross profit+ indirect income – indirect expeses

7. A trial balance is a list and total of all the debit and credit accounts for an entity for

a given period – usually a month.

The trial balance ensures that the Debits equal the Credit balances

8. What is the Cash flow equation?

Cash inflow less Cash outflow = Net Cash Inflow or outflow

9. What is a ‘budget’?

Budget is a financial plan showing the manner in which expenditures are

to be made from the decided amount.

10. Explain the term ‘zero-based budgeting’

This is the technique in which the budget is made by taking the base as zero. This

means in every period there will be new budget which will be prepared without

considering the opening balances (Ekanem, 2014).

11. Explain the term ‘Incremental budgets’

This is the budget prepared by using the figures of the previous budget

and in that addition in relation to the expense for the current period will

be made.

12. Explain the term ‘Program budget’

The budget which is designed in respect of a specific event or activity is

identified to be program budget (Cohen & Karatzimas, 2014). All the

incomes and expenses in relation to that event will be considered.

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 8 of 17

7. A trial balance is a list and total of all the debit and credit accounts for an entity for

a given period – usually a month.

The trial balance ensures that the Debits equal the Credit balances

8. What is the Cash flow equation?

Cash inflow less Cash outflow = Net Cash Inflow or outflow

9. What is a ‘budget’?

Budget is a financial plan showing the manner in which expenditures are

to be made from the decided amount.

10. Explain the term ‘zero-based budgeting’

This is the technique in which the budget is made by taking the base as zero. This

means in every period there will be new budget which will be prepared without

considering the opening balances (Ekanem, 2014).

11. Explain the term ‘Incremental budgets’

This is the budget prepared by using the figures of the previous budget

and in that addition in relation to the expense for the current period will

be made.

12. Explain the term ‘Program budget’

The budget which is designed in respect of a specific event or activity is

identified to be program budget (Cohen & Karatzimas, 2014). All the

incomes and expenses in relation to that event will be considered.

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 8 of 17

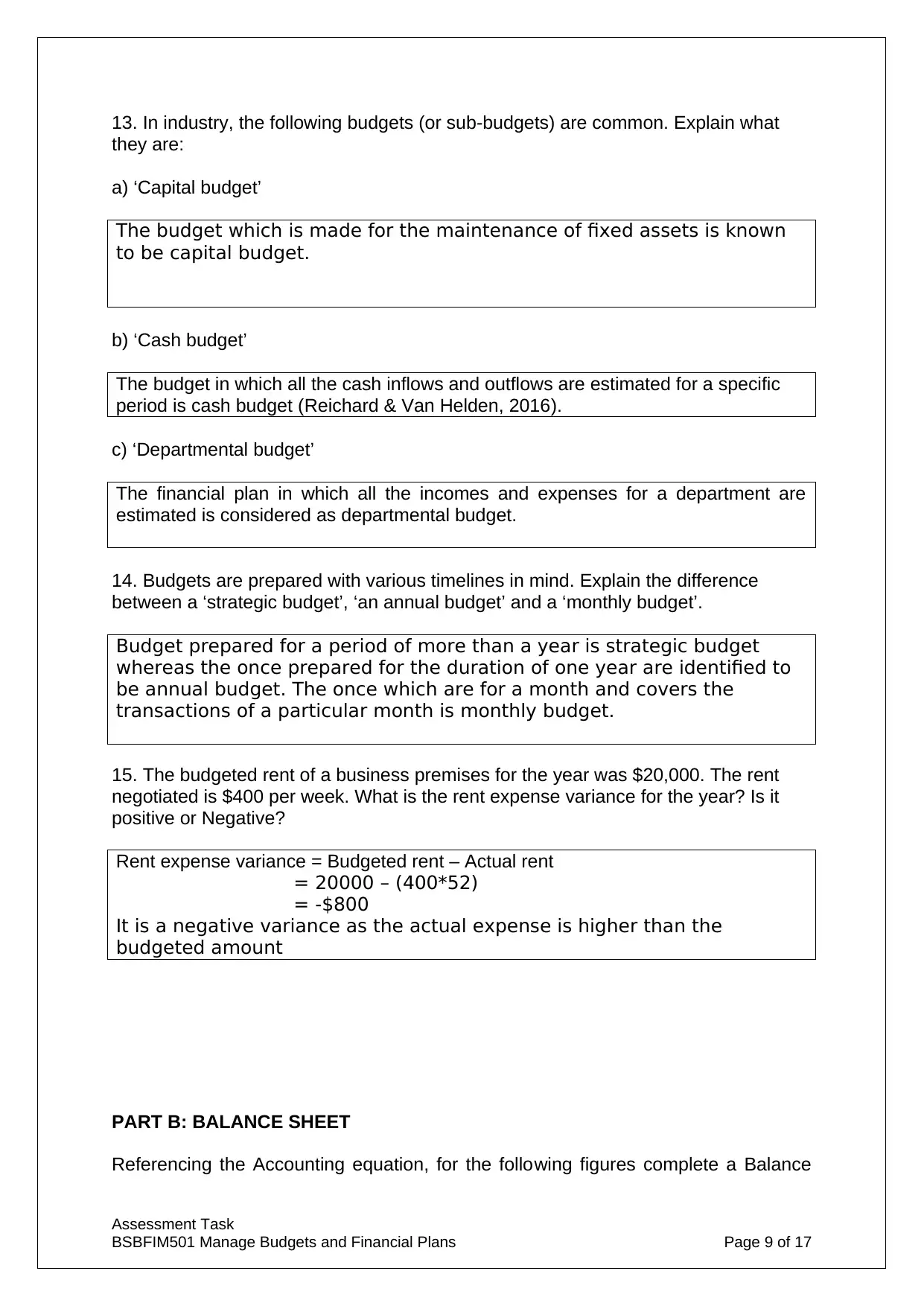

13. In industry, the following budgets (or sub-budgets) are common. Explain what

they are:

a) ‘Capital budget’

The budget which is made for the maintenance of fixed assets is known

to be capital budget.

b) ‘Cash budget’

The budget in which all the cash inflows and outflows are estimated for a specific

period is cash budget (Reichard & Van Helden, 2016).

c) ‘Departmental budget’

The financial plan in which all the incomes and expenses for a department are

estimated is considered as departmental budget.

14. Budgets are prepared with various timelines in mind. Explain the difference

between a ‘strategic budget’, ‘an annual budget’ and a ‘monthly budget’.

Budget prepared for a period of more than a year is strategic budget

whereas the once prepared for the duration of one year are identified to

be annual budget. The once which are for a month and covers the

transactions of a particular month is monthly budget.

15. The budgeted rent of a business premises for the year was $20,000. The rent

negotiated is $400 per week. What is the rent expense variance for the year? Is it

positive or Negative?

Rent expense variance = Budgeted rent – Actual rent

= 20000 – (400*52)

= -$800

It is a negative variance as the actual expense is higher than the

budgeted amount

PART B: BALANCE SHEET

Referencing the Accounting equation, for the following figures complete a Balance

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 9 of 17

they are:

a) ‘Capital budget’

The budget which is made for the maintenance of fixed assets is known

to be capital budget.

b) ‘Cash budget’

The budget in which all the cash inflows and outflows are estimated for a specific

period is cash budget (Reichard & Van Helden, 2016).

c) ‘Departmental budget’

The financial plan in which all the incomes and expenses for a department are

estimated is considered as departmental budget.

14. Budgets are prepared with various timelines in mind. Explain the difference

between a ‘strategic budget’, ‘an annual budget’ and a ‘monthly budget’.

Budget prepared for a period of more than a year is strategic budget

whereas the once prepared for the duration of one year are identified to

be annual budget. The once which are for a month and covers the

transactions of a particular month is monthly budget.

15. The budgeted rent of a business premises for the year was $20,000. The rent

negotiated is $400 per week. What is the rent expense variance for the year? Is it

positive or Negative?

Rent expense variance = Budgeted rent – Actual rent

= 20000 – (400*52)

= -$800

It is a negative variance as the actual expense is higher than the

budgeted amount

PART B: BALANCE SHEET

Referencing the Accounting equation, for the following figures complete a Balance

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 9 of 17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sheet

Inventory: Food $25,000

Inventory: Beverage $23,800

Bank Loan $15,500

Furniture and fittings $12,000

Trade Debtors $18,300

Bank Account $7,500

Computers $8,000

Petty Cash $1,200

GST payable $895

Buildings and Improvements $9,500

Trade Creditors $9,500

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 10 of 17

Inventory: Food $25,000

Inventory: Beverage $23,800

Bank Loan $15,500

Furniture and fittings $12,000

Trade Debtors $18,300

Bank Account $7,500

Computers $8,000

Petty Cash $1,200

GST payable $895

Buildings and Improvements $9,500

Trade Creditors $9,500

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 10 of 17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

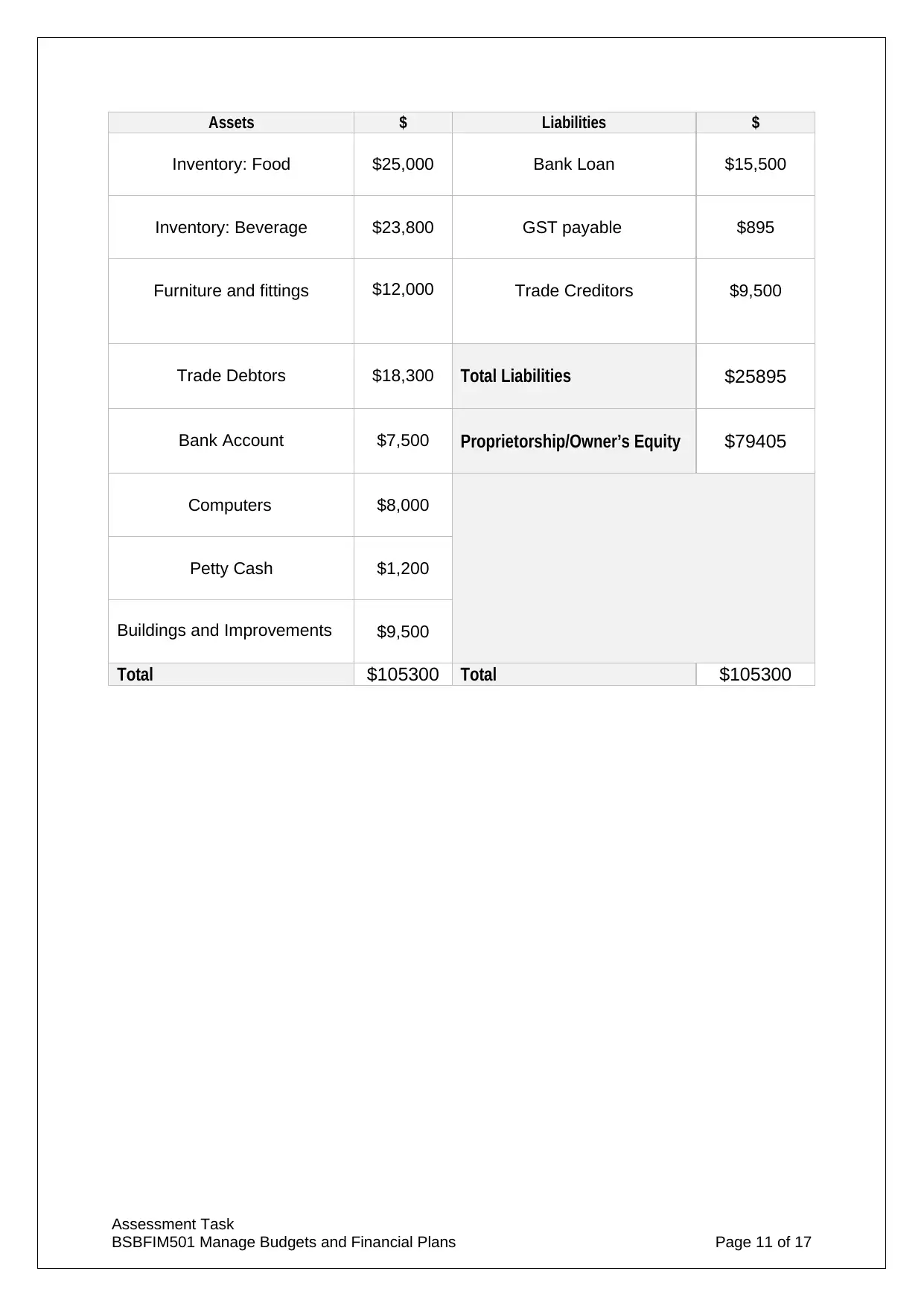

Assets $ Liabilities $

Inventory: Food $25,000 Bank Loan $15,500

Inventory: Beverage $23,800 GST payable $895

Furniture and fittings $12,000 Trade Creditors $9,500

Trade Debtors $18,300 Total Liabilities $25895

Bank Account $7,500 Proprietorship/Owner’s Equity $79405

Computers $8,000

Petty Cash $1,200

Buildings and Improvements $9,500

Total $105300 Total $105300

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 11 of 17

Inventory: Food $25,000 Bank Loan $15,500

Inventory: Beverage $23,800 GST payable $895

Furniture and fittings $12,000 Trade Creditors $9,500

Trade Debtors $18,300 Total Liabilities $25895

Bank Account $7,500 Proprietorship/Owner’s Equity $79405

Computers $8,000

Petty Cash $1,200

Buildings and Improvements $9,500

Total $105300 Total $105300

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 11 of 17

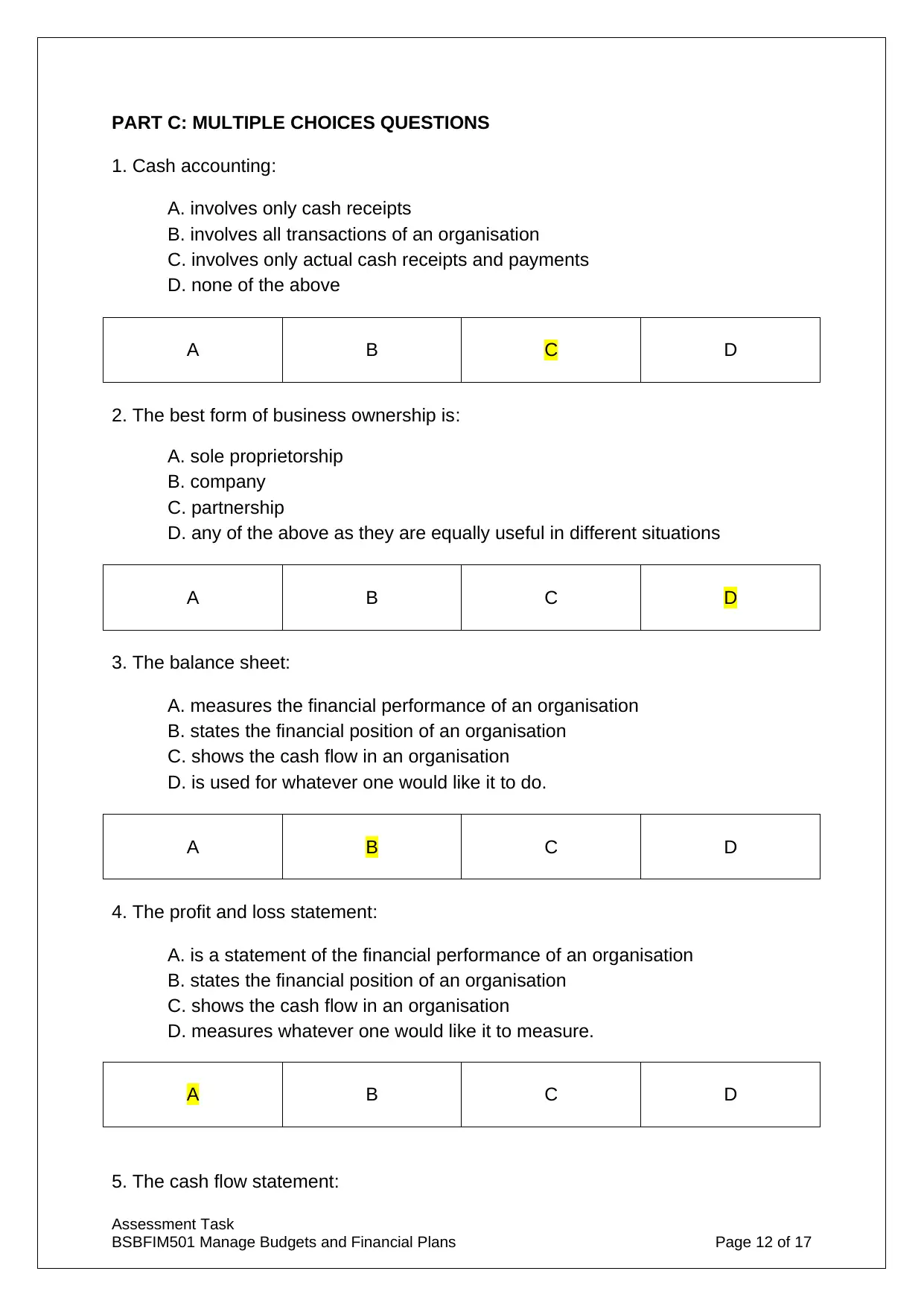

PART C: MULTIPLE CHOICES QUESTIONS

1. Cash accounting:

A. involves only cash receipts

B. involves all transactions of an organisation

C. involves only actual cash receipts and payments

D. none of the above

A B C D

2. The best form of business ownership is:

A. sole proprietorship

B. company

C. partnership

D. any of the above as they are equally useful in different situations

A B C D

3. The balance sheet:

A. measures the financial performance of an organisation

B. states the financial position of an organisation

C. shows the cash flow in an organisation

D. is used for whatever one would like it to do.

A B C D

4. The profit and loss statement:

A. is a statement of the financial performance of an organisation

B. states the financial position of an organisation

C. shows the cash flow in an organisation

D. measures whatever one would like it to measure.

A B C D

5. The cash flow statement:

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 12 of 17

1. Cash accounting:

A. involves only cash receipts

B. involves all transactions of an organisation

C. involves only actual cash receipts and payments

D. none of the above

A B C D

2. The best form of business ownership is:

A. sole proprietorship

B. company

C. partnership

D. any of the above as they are equally useful in different situations

A B C D

3. The balance sheet:

A. measures the financial performance of an organisation

B. states the financial position of an organisation

C. shows the cash flow in an organisation

D. is used for whatever one would like it to do.

A B C D

4. The profit and loss statement:

A. is a statement of the financial performance of an organisation

B. states the financial position of an organisation

C. shows the cash flow in an organisation

D. measures whatever one would like it to measure.

A B C D

5. The cash flow statement:

Assessment Task

BSBFIM501 Manage Budgets and Financial Plans Page 12 of 17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.