BSBFIM502: Manage Payroll Assignment - Imagine Education - BSBFIM502

VerifiedAdded on 2023/06/08

|16

|3058

|52

Homework Assignment

AI Summary

This document presents a detailed solution to a Manage Payroll assignment (BSBFIM502), covering key aspects of payroll management. Part A addresses security procedures, employee allowances, gross pay calculation, statutory deductions, tax deductions, payroll reconciliation, and payroll tax. It explains the purpose of establishing security procedures, ensures employee claim substantiation, and lists items required to compute gross pay. Part B analyzes a case study, outlining security procedures and control measures for a school's payroll system. It includes the creation of a tax invoice and a record of vehicle trips. Part C focuses on project elements, emphasizing security and confidentiality of payroll information and substantiation of claims for allowances. The solution provides a comprehensive overview of payroll processes, tax implications, and security measures, making it a valuable resource for students studying payroll management. The assignment references various aspects of Australian tax laws and regulations.

BSBFIM502 MANAGE

PAYROLL

PAYROLL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART A

1.

The three aspects of purpose of establishing security procedures in relation to managing payroll

information are as follows:

It is required to perform background checks on potential payroll employees.

To ensure the confidentiality of payroll data as well as records.

It is also significant for paying employees and filling employment tax (Murphy, 2019).

2.

In order to ensure that employee claim for allowance is substantiated, it is significant to establish

clear policies and procedure in relation to same which are as follows:

The definition of allowance should be clear.

The basis for the allowances are clearly explained such as award, contract etc.

The application of claiming allowances is processed.

Employee submit document required to substantiate claims such as application forms

should have downloaded from intranets.

Proper approval and authorisation of claim.

3.

Payroll records such as wages paid, allowances, bonus etc. for at least three years.

Wage computation record such as time cards, work schedule etc. for at least two years.

Employment tax documents such as forms for at least four years (Morgan and Castelyn,

2018).

4.

List of items required to compute gross pay:

Wages

Allowances

1.

The three aspects of purpose of establishing security procedures in relation to managing payroll

information are as follows:

It is required to perform background checks on potential payroll employees.

To ensure the confidentiality of payroll data as well as records.

It is also significant for paying employees and filling employment tax (Murphy, 2019).

2.

In order to ensure that employee claim for allowance is substantiated, it is significant to establish

clear policies and procedure in relation to same which are as follows:

The definition of allowance should be clear.

The basis for the allowances are clearly explained such as award, contract etc.

The application of claiming allowances is processed.

Employee submit document required to substantiate claims such as application forms

should have downloaded from intranets.

Proper approval and authorisation of claim.

3.

Payroll records such as wages paid, allowances, bonus etc. for at least three years.

Wage computation record such as time cards, work schedule etc. for at least two years.

Employment tax documents such as forms for at least four years (Morgan and Castelyn,

2018).

4.

List of items required to compute gross pay:

Wages

Allowances

Pay leaves

This information would be required to obtain from payroll records, time sheet, rate of pay,

employment contract, person tax file number declaration form (Murphy, 2019).

5.

The two statutory deductions that can apply to a wage or salary earners are as follows:

PAYG withholding for tax: The employer withholds certain amount of employee salary

or wages with themselves at the time of payment. This is further send by employer to

ATO. The employee can take deduction of withholding. The calculation is (Estimated tax

/ instalment income) * 100

Medicare Levy: This is one of the statutory deduction which is determined via 2% of the

employee taxable income (Murphy, 2019).

6.

My current job is Credit manager in reputed bank of Australia. The two allowable tax deduction

that I can claim my overall tax deduction is as follows:

Gift and donation: This is one of the type of expense which I have made in the current

year and I can claim 100% deduction on it.

Travel expenses: The expenses I have incur for the purpose of my work such as meeting

clients are also a type of deduction which I can claim to reduce my overall taxable

income (Fitzpatrick, 2019).

7.

The three checks that an organization need to perform when reconciling payroll are as follows:

Payroll register.

Employee time cards.

General ledger to check wages and deductions.

This information would be required to obtain from payroll records, time sheet, rate of pay,

employment contract, person tax file number declaration form (Murphy, 2019).

5.

The two statutory deductions that can apply to a wage or salary earners are as follows:

PAYG withholding for tax: The employer withholds certain amount of employee salary

or wages with themselves at the time of payment. This is further send by employer to

ATO. The employee can take deduction of withholding. The calculation is (Estimated tax

/ instalment income) * 100

Medicare Levy: This is one of the statutory deduction which is determined via 2% of the

employee taxable income (Murphy, 2019).

6.

My current job is Credit manager in reputed bank of Australia. The two allowable tax deduction

that I can claim my overall tax deduction is as follows:

Gift and donation: This is one of the type of expense which I have made in the current

year and I can claim 100% deduction on it.

Travel expenses: The expenses I have incur for the purpose of my work such as meeting

clients are also a type of deduction which I can claim to reduce my overall taxable

income (Fitzpatrick, 2019).

7.

The three checks that an organization need to perform when reconciling payroll are as follows:

Payroll register.

Employee time cards.

General ledger to check wages and deductions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8.

Tax File Number is an individual personal reference number which is used for the purpose of

Australian tax and superannuation systems. The individual that work in Australia should require

to have TFN number. The purpose of TFN declaration form is the list all the tax saving

investments that an employee proposed to make during that specific year. Further, the time line

takes by ATO to process, complete and lodgement tax return electronically is within 12 business

days (Morgan and Castelyn, 2018).

9.

i. Payroll tax is referred to the amount of tax charged and withheld on the employer’s payroll.

For instance, social security tax, medicare levy, etc. A business is required to pay payroll tax it is

either individually or in a group paying more than $25000 per week in terms of Australian

taxable wages.

ii. If the annual Australian taxable wages are less than $1.3 million, then there is no requirement

to pay payroll tax.

iii. It is 4.75% for employer paying $6.5 million or less in Australian taxable wages while for

those who are paying more than $6.5 million, current payroll tax rate is 4.95%.

iv. On getting registered as an employer in Queensland, the payroll tax return must be lodged

periodically on monthly basis and annual returns annually each year.

v. Period returns are due to payment after the 7 days from the end of return period while annual

returns are due by 21st of July each year.

iv. There were no tax to be calculated for the Australian taxable wages which is below the

exempted threshold of $1.3 million. Accordingly, for $1 million payroll, there would be no

payroll tax.

10.

i. Fringe benefit tax refers to the tax paid by businesses in lieu of the benefits it has offered to its

employees. It is important in PMS as it indicates the various in which employer is committed

towards compensating employees.

Tax File Number is an individual personal reference number which is used for the purpose of

Australian tax and superannuation systems. The individual that work in Australia should require

to have TFN number. The purpose of TFN declaration form is the list all the tax saving

investments that an employee proposed to make during that specific year. Further, the time line

takes by ATO to process, complete and lodgement tax return electronically is within 12 business

days (Morgan and Castelyn, 2018).

9.

i. Payroll tax is referred to the amount of tax charged and withheld on the employer’s payroll.

For instance, social security tax, medicare levy, etc. A business is required to pay payroll tax it is

either individually or in a group paying more than $25000 per week in terms of Australian

taxable wages.

ii. If the annual Australian taxable wages are less than $1.3 million, then there is no requirement

to pay payroll tax.

iii. It is 4.75% for employer paying $6.5 million or less in Australian taxable wages while for

those who are paying more than $6.5 million, current payroll tax rate is 4.95%.

iv. On getting registered as an employer in Queensland, the payroll tax return must be lodged

periodically on monthly basis and annual returns annually each year.

v. Period returns are due to payment after the 7 days from the end of return period while annual

returns are due by 21st of July each year.

iv. There were no tax to be calculated for the Australian taxable wages which is below the

exempted threshold of $1.3 million. Accordingly, for $1 million payroll, there would be no

payroll tax.

10.

i. Fringe benefit tax refers to the tax paid by businesses in lieu of the benefits it has offered to its

employees. It is important in PMS as it indicates the various in which employer is committed

towards compensating employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ii. HECS refers to the loan or contribution made by the employers towards the educational fees

of their employee’s child. It indicates how financial resources have been allocated for different

needs of employees while managing payroll.

iii. Superannuation is the payment made by employee or their employer towards the fund meant

for providing pension post retirement. It is important in PMS as it indicates the retirement

benefits that the employer is providing to its employees.

iv. PAYG refers to the amount of tax withhold by the employer from the payment made to their

employees which is then paid to ATO. It is important in PMS as it indicates the employer’s

liability towards the tax authority.

v. Medicare levy is additional tax levied on taxable income to fund the cost of Australian health

care system. It indicates the employer’s commitment towards fulfilling its obligations towards

the society.

11.

i. Anti discrimination laws are relevant in managing payroll system to ensure that there is no

discrimination made by employer in compensating its employees on the ground of race, sex,

ethnicity and religion.

ii. Ethical principles are relevant in PMS for ensuring that the employer is paying just & fair

benefit to its employees.

iii. These codes of practice are important in PMS to ensure than financial records has been kept

in required order and also there were no frauds taking place within the organization pertaining to

payroll system.

iv. This Act is relevant in PMS to ensure that the employees are getting required support from

their employers in superannuation fund for the security of income post retirement.

v. Privacy laws are relevant in PMS to ensure the security & confidentiality of employee’s

personal records and limiting any kind of unauthorized access to it.

of their employee’s child. It indicates how financial resources have been allocated for different

needs of employees while managing payroll.

iii. Superannuation is the payment made by employee or their employer towards the fund meant

for providing pension post retirement. It is important in PMS as it indicates the retirement

benefits that the employer is providing to its employees.

iv. PAYG refers to the amount of tax withhold by the employer from the payment made to their

employees which is then paid to ATO. It is important in PMS as it indicates the employer’s

liability towards the tax authority.

v. Medicare levy is additional tax levied on taxable income to fund the cost of Australian health

care system. It indicates the employer’s commitment towards fulfilling its obligations towards

the society.

11.

i. Anti discrimination laws are relevant in managing payroll system to ensure that there is no

discrimination made by employer in compensating its employees on the ground of race, sex,

ethnicity and religion.

ii. Ethical principles are relevant in PMS for ensuring that the employer is paying just & fair

benefit to its employees.

iii. These codes of practice are important in PMS to ensure than financial records has been kept

in required order and also there were no frauds taking place within the organization pertaining to

payroll system.

iv. This Act is relevant in PMS to ensure that the employees are getting required support from

their employers in superannuation fund for the security of income post retirement.

v. Privacy laws are relevant in PMS to ensure the security & confidentiality of employee’s

personal records and limiting any kind of unauthorized access to it.

PART B – Case Study

1. Security procedures & control measures to be implemented by school

The payroll register must be audited through the implementation of system to check the

registers either on quarterly or annual basis for searching errors that are potential for the

incidents of using the code of fake employees for transferring the money to personal

account. This is possible through integrating payroll personnel & bookkeepers within the

financial data which allows the payroll department in performing their jobs along with

the requirement of obtaining approvals for payroll from executives. This in turn would be

helpful in ensuring no signs of frauds.

Switching to modern timesheet system allows for having a biometric or 2 step

authentication process while processing payroll instead of considering employee

reporting by themselves for the hours worked. Therefore, there would be no scope for

creating fake employee ids.

Further, the regular audit of taxes paid on payroll must be done internally which in turn

would facilitate hindering the way for any accidental fraud taking place on the part of the

company. Any review done on routine basis is useful in catching mistakes earlier that is,

prior to the occurrence of huge damages or losses.

Installation of CCTV systems and ensuring employees are working in pairs is helpful in

preventing false reports.

Regulation of the behavior of employees working with sensitive data pertaining to payroll

must be done. They must be allowed perform all their tasks during office hours only

along with conducting random audit of the payroll personnel would definitely ensure

everything to be up to date.

2. Creation of Tax invoice

TAX INVOICE

Account to: Bunnings

Moore Parade

1. Security procedures & control measures to be implemented by school

The payroll register must be audited through the implementation of system to check the

registers either on quarterly or annual basis for searching errors that are potential for the

incidents of using the code of fake employees for transferring the money to personal

account. This is possible through integrating payroll personnel & bookkeepers within the

financial data which allows the payroll department in performing their jobs along with

the requirement of obtaining approvals for payroll from executives. This in turn would be

helpful in ensuring no signs of frauds.

Switching to modern timesheet system allows for having a biometric or 2 step

authentication process while processing payroll instead of considering employee

reporting by themselves for the hours worked. Therefore, there would be no scope for

creating fake employee ids.

Further, the regular audit of taxes paid on payroll must be done internally which in turn

would facilitate hindering the way for any accidental fraud taking place on the part of the

company. Any review done on routine basis is useful in catching mistakes earlier that is,

prior to the occurrence of huge damages or losses.

Installation of CCTV systems and ensuring employees are working in pairs is helpful in

preventing false reports.

Regulation of the behavior of employees working with sensitive data pertaining to payroll

must be done. They must be allowed perform all their tasks during office hours only

along with conducting random audit of the payroll personnel would definitely ensure

everything to be up to date.

2. Creation of Tax invoice

TAX INVOICE

Account to: Bunnings

Moore Parade

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

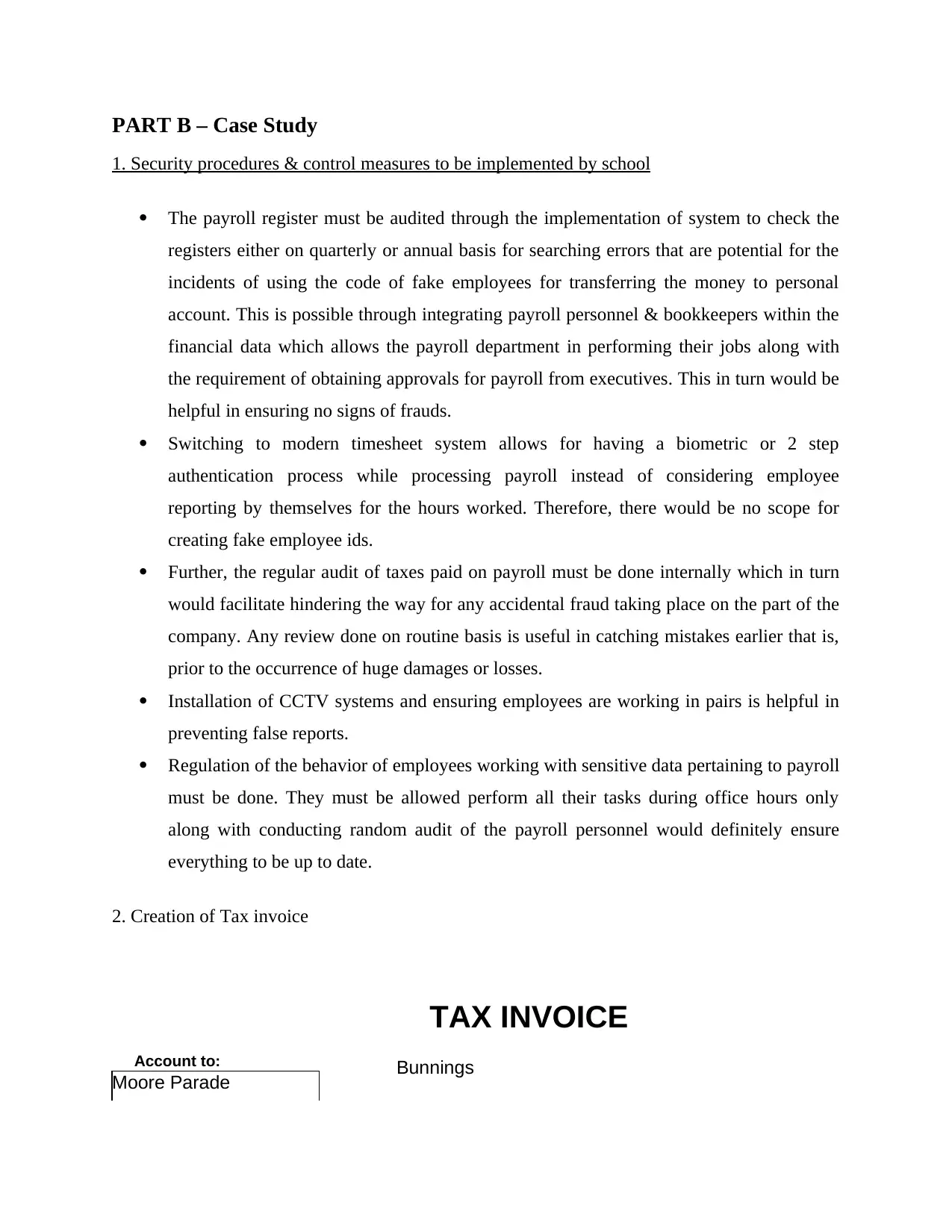

5 Nerang Street, Nerang

Qld 4211

33, Southport,

ABN: 33 987 223 120

Invoice Number: IN - 001

Date: 21st June 2013

Goods or Services provided to:

Moore Parade

33, Southport,

QLD, 4215.

DESCRIPTION AMOUNT

$880

Office Use only POSTAGE, COURIERS, etc

TOTAL (inclusive of GST) $880.00

% indicates GST-free goods/services

Value of GST= $8.80

If you have any questions regarding this invoice, call

Remittance Please return lower portion with payment

Make all cheques payable to:

Qld 4211

33, Southport,

ABN: 33 987 223 120

Invoice Number: IN - 001

Date: 21st June 2013

Goods or Services provided to:

Moore Parade

33, Southport,

QLD, 4215.

DESCRIPTION AMOUNT

$880

Office Use only POSTAGE, COURIERS, etc

TOTAL (inclusive of GST) $880.00

% indicates GST-free goods/services

Value of GST= $8.80

If you have any questions regarding this invoice, call

Remittance Please return lower portion with payment

Make all cheques payable to:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

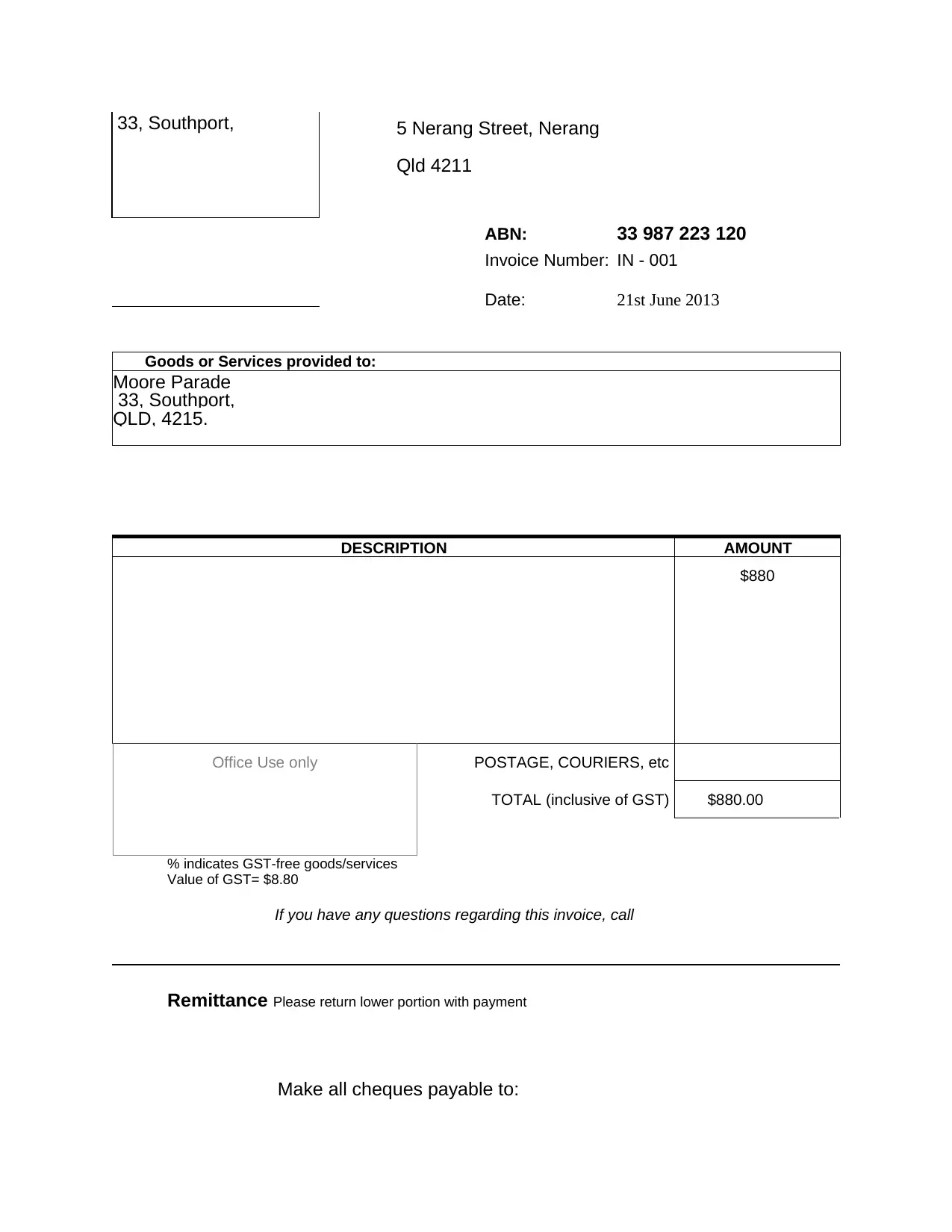

Invoice No IN - 001

Date Paid 21st June

2013Amount Paid $880

Check this box if you need a receipt

3.

Car make Volkswagen Model Transporter Registration number

IDX 812

Date trip

commenced

Date

trip

ended

Odometer

at start

Odometer

at finish

Business

km

Purpose

of trip

Name

of

driver

Signature

18/6/12 18/6/12 33,345 33,375 30 Framing Brett Brett

19/6/12 19/6/12 33,412 33,442 30 Roof Brett Brett

20/6/12 20/6/12 33,501 33,585 84 Cupboards Brett Brett

21/6/12 21/6/12 33,610 33,669 59 Cupboards Brett Brett

22/6/12 22/6/12 33,680 33,725 45

Repairs to

offices in

city

Brett Brett

PART C – Project

1.

Security to ensure the confidentiality and security of payroll information

The basic intention behind this policy is to ensure the security as well as the confidentiality of

information pertaining to the payroll department. This is because the payroll departments usually

held the sensitive information of the employees within the organization. The following three

procedures must be adopted by the management to ensure the confidentiality & security of

payroll information held by the payroll officers.

a. Securing the physical environment of payroll department is key to the security of payroll

information. Any document handled in physical form must be kept in locked up condition all

time. Also, desks must be positioned appropriately in order to ensure that the screens are not

Date Paid 21st June

2013Amount Paid $880

Check this box if you need a receipt

3.

Car make Volkswagen Model Transporter Registration number

IDX 812

Date trip

commenced

Date

trip

ended

Odometer

at start

Odometer

at finish

Business

km

Purpose

of trip

Name

of

driver

Signature

18/6/12 18/6/12 33,345 33,375 30 Framing Brett Brett

19/6/12 19/6/12 33,412 33,442 30 Roof Brett Brett

20/6/12 20/6/12 33,501 33,585 84 Cupboards Brett Brett

21/6/12 21/6/12 33,610 33,669 59 Cupboards Brett Brett

22/6/12 22/6/12 33,680 33,725 45

Repairs to

offices in

city

Brett Brett

PART C – Project

1.

Security to ensure the confidentiality and security of payroll information

The basic intention behind this policy is to ensure the security as well as the confidentiality of

information pertaining to the payroll department. This is because the payroll departments usually

held the sensitive information of the employees within the organization. The following three

procedures must be adopted by the management to ensure the confidentiality & security of

payroll information held by the payroll officers.

a. Securing the physical environment of payroll department is key to the security of payroll

information. Any document handled in physical form must be kept in locked up condition all

time. Also, desks must be positioned appropriately in order to ensure that the screens are not

visible to by others walking nearby. Further, the payroll office’s doors must be kept locked

always with the entry to be allowed to only authorized executives and payroll employees.

b. Limiting the access to payroll information is additionally required along with physical

precautions. For instances, employees could be able to access the information of their own but no

of other employee’s or colleague’s information. Therefore, it is necessarily required to be

determined in advance that who would be having the access to the information containing the

records of employees and how the access would be handled.

c. The third procedure pertaining to security & confidentiality of payroll information is the

choice made for processing payroll along with the company’s electronic security. Therefore, it is

necessary on the part of company to have firewall for the protection of computer databases and

systems.

2. Substantiation of claims for allowances

It refers to validating as well as providing enough proof to support with regards to the claim for

allowances. The intention for framing policies pertaining to the substantiation of claims is to

ensure that potential procedures have been adopted to guarantee the substantiation of claims for

allowances. Therefore, policies & procedures are need to be in place with respect to the payment

of each allowance. Accordingly, the following procedures must be followed:

a. There must be a clear definition of each and every allowances that the company is paying to be

included within company’s documents and also, the same should be given to each employees

through training programs specially designed for making them aware of what allowances they

would get. In addition to this, the explanation must be given with respect to what basis such

allowances are provided to the employees like whether it as award, contract, agreement or

legislative requirement.

b. There must be appropriate procedures applied by the management with regards to claiming as

well as receiving the allowance along with indicating them that what documents they are

required to provide in order substantiate the claim for allowance like the application form

required to be downloaded from intranet.

always with the entry to be allowed to only authorized executives and payroll employees.

b. Limiting the access to payroll information is additionally required along with physical

precautions. For instances, employees could be able to access the information of their own but no

of other employee’s or colleague’s information. Therefore, it is necessarily required to be

determined in advance that who would be having the access to the information containing the

records of employees and how the access would be handled.

c. The third procedure pertaining to security & confidentiality of payroll information is the

choice made for processing payroll along with the company’s electronic security. Therefore, it is

necessary on the part of company to have firewall for the protection of computer databases and

systems.

2. Substantiation of claims for allowances

It refers to validating as well as providing enough proof to support with regards to the claim for

allowances. The intention for framing policies pertaining to the substantiation of claims is to

ensure that potential procedures have been adopted to guarantee the substantiation of claims for

allowances. Therefore, policies & procedures are need to be in place with respect to the payment

of each allowance. Accordingly, the following procedures must be followed:

a. There must be a clear definition of each and every allowances that the company is paying to be

included within company’s documents and also, the same should be given to each employees

through training programs specially designed for making them aware of what allowances they

would get. In addition to this, the explanation must be given with respect to what basis such

allowances are provided to the employees like whether it as award, contract, agreement or

legislative requirement.

b. There must be appropriate procedures applied by the management with regards to claiming as

well as receiving the allowance along with indicating them that what documents they are

required to provide in order substantiate the claim for allowance like the application form

required to be downloaded from intranet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

c. Further, there must be an appropriate procedure in place with regards to the approval &

authorization of claims for allowances like the application must be signed by the employee’s

immediate manager to ensure appropriate substantiation of claims for allowances.

3. Control measures to safeguard the organization’s financial resources in accordance with

legislative and organizational requirements. The purpose of this policy is to ensure that the

financial resources of organization are appropriately safeguarded as per the requirements of both

the organizational as well as the legislative requirements in order to ensure that there is no room

provided for the incident of damages or losses to the company’s financial resources. Therefore,

the following control measures are essential:

a. Timesheets are appropriately supervised and is maintained through the biometric or 2 step

authentication process instead of employees reporting by their own. In addition to this, it must be

checked prior to the same getting processed. This would ensure no payment made to employees

unreasonable on the ground fraudulent reporting of the hours worked.

b. Further, the sign of employees must be obtained after the payment is being received by them

which would ensure that the payment has been collected by the concerned employees and the

same not been lost to the unauthorized hands.

c. Another measure that could be in place as a measure for safeguarding the financial resources

of the company is to ensure that the duties pertaining to the management of payroll is being

segregated among multiple staff members instead of it being handled signal handedly.

4. Checking of payroll and authorization of salaries and wages for payment. It is intended to

provide the payroll officer to outline the policies & procedures of the organization pertaining to

the checking of payroll and authorizing salaries & wages for payment. The following procedure

could be used with this regard:

a. All payroll transactions must be substantiated by the appropriate person by looking into the

employees listed on company’s payroll against those who are physically present within the

company.

authorization of claims for allowances like the application must be signed by the employee’s

immediate manager to ensure appropriate substantiation of claims for allowances.

3. Control measures to safeguard the organization’s financial resources in accordance with

legislative and organizational requirements. The purpose of this policy is to ensure that the

financial resources of organization are appropriately safeguarded as per the requirements of both

the organizational as well as the legislative requirements in order to ensure that there is no room

provided for the incident of damages or losses to the company’s financial resources. Therefore,

the following control measures are essential:

a. Timesheets are appropriately supervised and is maintained through the biometric or 2 step

authentication process instead of employees reporting by their own. In addition to this, it must be

checked prior to the same getting processed. This would ensure no payment made to employees

unreasonable on the ground fraudulent reporting of the hours worked.

b. Further, the sign of employees must be obtained after the payment is being received by them

which would ensure that the payment has been collected by the concerned employees and the

same not been lost to the unauthorized hands.

c. Another measure that could be in place as a measure for safeguarding the financial resources

of the company is to ensure that the duties pertaining to the management of payroll is being

segregated among multiple staff members instead of it being handled signal handedly.

4. Checking of payroll and authorization of salaries and wages for payment. It is intended to

provide the payroll officer to outline the policies & procedures of the organization pertaining to

the checking of payroll and authorizing salaries & wages for payment. The following procedure

could be used with this regard:

a. All payroll transactions must be substantiated by the appropriate person by looking into the

employees listed on company’s payroll against those who are physically present within the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. Duties must be separation of duties pertaining to payroll management where if one is

preparing, then the other employee should be engaged for authorizing the same. It is necessary

for minimizing the risk of payroll thefts.

c. Auditing of payroll transactions must be done by other departments such as the accounting

department to determine any errors or discrepancies against the paycheck for making necessary

adjustments.

5. Reconciliation of salaries, wages and deductions. It is necessary for ensuring everything to be

up to date and free of frauds. The procedures to ensure the same are:

a. Undertaking the review of payroll register and reconciling the amount with that of

paychecks helps in preventing errors & frauds.

b. Checking the working hours entered against the timesheets ensure accuracy in wages

determination.

c. Checking pay rates is equally important for ensuring that the correct rate has been used

for determining the salaries or wages of employees.

6. Employee enquiries related to salaries and wages to ensure the amount has been paid to the

concerned employee. The procedures for the same are:

a. Obtaining employee’s sign on paychecks after making payment for wages or salaries to ensure

that the salaries are received by the concerned employee.

b. Payroll reports must be generated for each individual employees to make them understand the

reasons for gross & net pay.

c. There must be appropriate disaster recovery and back up system in place to fulfill the enquiries

of employees as and when it arises.

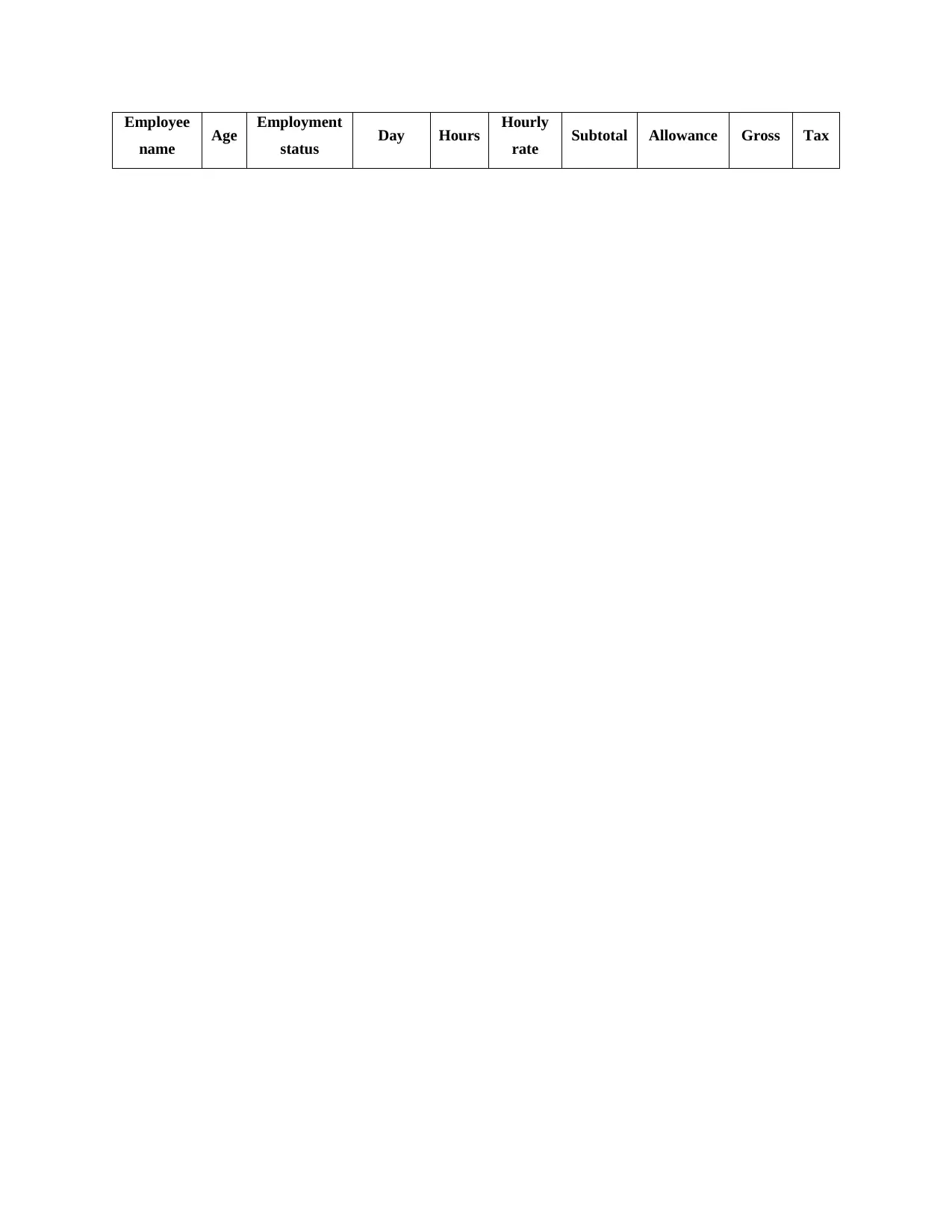

2.

i., ii.

preparing, then the other employee should be engaged for authorizing the same. It is necessary

for minimizing the risk of payroll thefts.

c. Auditing of payroll transactions must be done by other departments such as the accounting

department to determine any errors or discrepancies against the paycheck for making necessary

adjustments.

5. Reconciliation of salaries, wages and deductions. It is necessary for ensuring everything to be

up to date and free of frauds. The procedures to ensure the same are:

a. Undertaking the review of payroll register and reconciling the amount with that of

paychecks helps in preventing errors & frauds.

b. Checking the working hours entered against the timesheets ensure accuracy in wages

determination.

c. Checking pay rates is equally important for ensuring that the correct rate has been used

for determining the salaries or wages of employees.

6. Employee enquiries related to salaries and wages to ensure the amount has been paid to the

concerned employee. The procedures for the same are:

a. Obtaining employee’s sign on paychecks after making payment for wages or salaries to ensure

that the salaries are received by the concerned employee.

b. Payroll reports must be generated for each individual employees to make them understand the

reasons for gross & net pay.

c. There must be appropriate disaster recovery and back up system in place to fulfill the enquiries

of employees as and when it arises.

2.

i., ii.

Employee

name Age Employment

status Day Hours Hourly

rate Subtotal Allowance Gross Tax

name Age Employment

status Day Hours Hourly

rate Subtotal Allowance Gross Tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.