BTEC Level 4 Hospitality Finance: Managing Transactions Report

VerifiedAdded on 2022/01/13

|13

|2917

|29

Report

AI Summary

This report, prepared for a BTEC Level 4 Higher National Certificate in Hospital Management, focuses on managing finance and recording transactions within the hospitality business. It begins with an introduction to accounting principles, defining accounting, its contribution to the hospitality industry, and analyzing key accounting principles like the business entity, going concern, monetary unit, and others. The report then delves into the application of the double-entry bookkeeping system, detailing debit and credit rules and illustrating transactions in a general ledger. It presents trial balances and explores the creation of income statements, comparing different options and offering recommendations. The report covers the accounting equation, financial statements, and offers practical examples of financial transactions. This assignment provides a comprehensive overview of financial management in the hospitality sector, aiding in understanding and applying fundamental accounting concepts.

BTEC Level 4 Higher National Certificate in Hospital Management

UNIT 4 THE HOSPITALITY BUSINESS TOOLKIT

|05 DECEMBER 2021 WORD COUNT: 2548

Managing Finance and

Recording Transactions

STUDENT’S NAME: TRAN LE HA MY

LECTURER’S NAME: MRS. HELEN DO

UNIT 4 THE HOSPITALITY BUSINESS TOOLKIT

|05 DECEMBER 2021 WORD COUNT: 2548

Managing Finance and

Recording Transactions

STUDENT’S NAME: TRAN LE HA MY

LECTURER’S NAME: MRS. HELEN DO

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

Introduction............................................................................................................................2

I. The principles of managing and monitoring financial performance:...........................................3

1. The definition of accounting and the contribution of accounting to the hospitality industry:3

2. Analysing the Accounting principles and its definition:..........................................................3

3. The basic Accounting Equation and the Financial Statement:................................................4

II. Applying the double entry book-keeping system of debits and credits to record sales and

purchases transactions in a general ledger:.....................................................................................6

1. Definition of double entry accounting and debit/credit rules:.................................................6

2. Double entry record option 1:..................................................................................................7

3. Producing a basic trial balance applying the use of the balance off rule to complete the

ledger:...............................................................................................................................................8

II. The trial balance with double entry bookkeeping.......................................................................9

III. Recording correctly transactions and an accurate trial balance by completing the balance off

ledger accounts with accepted accounting principles.....................................................................10

1. The income statement and profit and loss statement option 1 and option 2:........................10

2. Comparing the income statement option 1 and option 2 and recommending to the

organization:...................................................................................................................................11

Conclusion............................................................................................................................11

References............................................................................................................................12

1

Introduction............................................................................................................................2

I. The principles of managing and monitoring financial performance:...........................................3

1. The definition of accounting and the contribution of accounting to the hospitality industry:3

2. Analysing the Accounting principles and its definition:..........................................................3

3. The basic Accounting Equation and the Financial Statement:................................................4

II. Applying the double entry book-keeping system of debits and credits to record sales and

purchases transactions in a general ledger:.....................................................................................6

1. Definition of double entry accounting and debit/credit rules:.................................................6

2. Double entry record option 1:..................................................................................................7

3. Producing a basic trial balance applying the use of the balance off rule to complete the

ledger:...............................................................................................................................................8

II. The trial balance with double entry bookkeeping.......................................................................9

III. Recording correctly transactions and an accurate trial balance by completing the balance off

ledger accounts with accepted accounting principles.....................................................................10

1. The income statement and profit and loss statement option 1 and option 2:........................10

2. Comparing the income statement option 1 and option 2 and recommending to the

organization:...................................................................................................................................11

Conclusion............................................................................................................................11

References............................................................................................................................12

1

Introduction

Accounting plays a critical role in all the fields nowadays. Every company now have to

comprises a finance department with multiple related positions such as account payable,

purchasing, account receivable, general cashier… to maintain and control the statistics. By

gaining deeper insight into the financial situation for example the profit, the income and the loss

of the company, the owner can have a better understand of their company situation. Therefore,

based on the accurate statistics and the recommendations from finance department, the owner

boost their profit to the maximum and develop the company.

2

Accounting plays a critical role in all the fields nowadays. Every company now have to

comprises a finance department with multiple related positions such as account payable,

purchasing, account receivable, general cashier… to maintain and control the statistics. By

gaining deeper insight into the financial situation for example the profit, the income and the loss

of the company, the owner can have a better understand of their company situation. Therefore,

based on the accurate statistics and the recommendations from finance department, the owner

boost their profit to the maximum and develop the company.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

I. The principles of managing and monitoring financial performance:

1. The definition of accounting and the contribution of accounting to the hospitality

industry:

1.1. Definition of accounting:

Due to Vietnam Accounting Law in 2003: Accounting is the collection, processing,

examination, analysis and provision of economic and financial information in the form of value,

product and timing. Accounting consists of three fundamental activities:

Identification: Identify economic events (transactions)

Recording: Record, classify and summarize

Communication: Prepare accounting reports, analyze and interpret for users

The accounting process includes the bookkeeping function.

1.2. Both external and internal users take advantage of accounting data:

External users are taxing authorities, labor unions, customers, authorities, investors,

creditors… those are outside the organization who use the financial information to make

decisions or to evaluate an entity’s performance.

Internal users are finance department, human resources department, management,

marketing department…those are within a business organization who utilize financial

information to support their decisions in organizing and running the business.

Accounting plays a vital role in running a business because it helps you track income and

expenditures, ensure statutory compliance, and provide investors, management, and government

with quantitative financial information which can be used in making business decisions.

2. Analysing the Accounting principles and its definition:

2.1. Definition of accounting principles:

Accounting principles are the rules that accountants must follow when preparing

financial statements for a publicly traded organization. The principles have been developed and

modified through common usage by accountants all over the world. They are also what the

complete set of accounting standards were built upon, which are the standards issued by the

Financial Accounting Standards Board and the International Accounting Standards Board.

1) Business Entity principle: An organization created by an individual or individuals to

conduct business, engage in a trade or partake in similar activities. There are various types of

3

1. The definition of accounting and the contribution of accounting to the hospitality

industry:

1.1. Definition of accounting:

Due to Vietnam Accounting Law in 2003: Accounting is the collection, processing,

examination, analysis and provision of economic and financial information in the form of value,

product and timing. Accounting consists of three fundamental activities:

Identification: Identify economic events (transactions)

Recording: Record, classify and summarize

Communication: Prepare accounting reports, analyze and interpret for users

The accounting process includes the bookkeeping function.

1.2. Both external and internal users take advantage of accounting data:

External users are taxing authorities, labor unions, customers, authorities, investors,

creditors… those are outside the organization who use the financial information to make

decisions or to evaluate an entity’s performance.

Internal users are finance department, human resources department, management,

marketing department…those are within a business organization who utilize financial

information to support their decisions in organizing and running the business.

Accounting plays a vital role in running a business because it helps you track income and

expenditures, ensure statutory compliance, and provide investors, management, and government

with quantitative financial information which can be used in making business decisions.

2. Analysing the Accounting principles and its definition:

2.1. Definition of accounting principles:

Accounting principles are the rules that accountants must follow when preparing

financial statements for a publicly traded organization. The principles have been developed and

modified through common usage by accountants all over the world. They are also what the

complete set of accounting standards were built upon, which are the standards issued by the

Financial Accounting Standards Board and the International Accounting Standards Board.

1) Business Entity principle: An organization created by an individual or individuals to

conduct business, engage in a trade or partake in similar activities. There are various types of

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business entities — sole proprietorship, partnership, LLC, corporation, etc. A business's entity

type dictates both the structure of that organization and how that company is taxed.

2) Going Concern principle: It assumes that an entity will continue to operate indefinitely.

In this basis, generally, assets are recorded based on their original cost and not on market value.

Assets are assumed to be held and used for an indefinite period of time or during its estimated

useful life. And that assets are not intended to be sold immediately or liquidated.

3) Monetary Unit principle: The assumption that money itself is treated as a unit of

measurement. The organization record business transactions or events that can be expressed in

monetary terms by a currency.

4) Historical Cost principle: All business resources acquired should be valued and

recorded based on the actual cash equivalent or original cost of acquisition, not the prevailing

market value or future value. Exception to the rule is when the business is in the process of

closure and liquidation.

5) Matching principle: This principle requires that revenue recorded, in a given accounting

period, should have an equivalent expense recorded so as to show the true profit of the business.

6) Accounting period principle: A business report all of its financial information within a

set of time and that the business can divide all of its activities into defined time periods.

7) Conservatism principle: This principle requires company accounts to be prepared with

caution and high degrees of verification. All probable losses are recorded when they are

discovered, while gains can only be registered when they are fully realized.

8) Consistency principle: This principle ensures similar and consistent accounting

procedures is used by the business, year after year, unless change is necessary.

9) Materiality principle: Business transactions will affect the decision-making in an

organization. Therefore, business transactions must be reported properly and accurately. This

principle mentions that errors or mistakes in accounting procedures, that which involves

immaterial or small amount, may not need attention or correction.

10) Objectivity principle: This principle is the concept that the financial statement of an

organization was based on solid evidence, not based on any others third-parties or people.

11) Accrual principle: This principle requires that revenue should be recorded in the period

it is earned, regardless of the time the cash is received. The same is true for expense. Expense

should be recognized and recorded at the time it is incurred, regardless of the time that cash is

paid. This is to show the true picture of the business financial performance.

12) Transparent principle: This principle of transparency in organizing, engagement and

equity work refers to the full and honest accounting of all facts, information, and context

essential to ensuring an informed and equitable decision-making process.

4

type dictates both the structure of that organization and how that company is taxed.

2) Going Concern principle: It assumes that an entity will continue to operate indefinitely.

In this basis, generally, assets are recorded based on their original cost and not on market value.

Assets are assumed to be held and used for an indefinite period of time or during its estimated

useful life. And that assets are not intended to be sold immediately or liquidated.

3) Monetary Unit principle: The assumption that money itself is treated as a unit of

measurement. The organization record business transactions or events that can be expressed in

monetary terms by a currency.

4) Historical Cost principle: All business resources acquired should be valued and

recorded based on the actual cash equivalent or original cost of acquisition, not the prevailing

market value or future value. Exception to the rule is when the business is in the process of

closure and liquidation.

5) Matching principle: This principle requires that revenue recorded, in a given accounting

period, should have an equivalent expense recorded so as to show the true profit of the business.

6) Accounting period principle: A business report all of its financial information within a

set of time and that the business can divide all of its activities into defined time periods.

7) Conservatism principle: This principle requires company accounts to be prepared with

caution and high degrees of verification. All probable losses are recorded when they are

discovered, while gains can only be registered when they are fully realized.

8) Consistency principle: This principle ensures similar and consistent accounting

procedures is used by the business, year after year, unless change is necessary.

9) Materiality principle: Business transactions will affect the decision-making in an

organization. Therefore, business transactions must be reported properly and accurately. This

principle mentions that errors or mistakes in accounting procedures, that which involves

immaterial or small amount, may not need attention or correction.

10) Objectivity principle: This principle is the concept that the financial statement of an

organization was based on solid evidence, not based on any others third-parties or people.

11) Accrual principle: This principle requires that revenue should be recorded in the period

it is earned, regardless of the time the cash is received. The same is true for expense. Expense

should be recognized and recorded at the time it is incurred, regardless of the time that cash is

paid. This is to show the true picture of the business financial performance.

12) Transparent principle: This principle of transparency in organizing, engagement and

equity work refers to the full and honest accounting of all facts, information, and context

essential to ensuring an informed and equitable decision-making process.

4

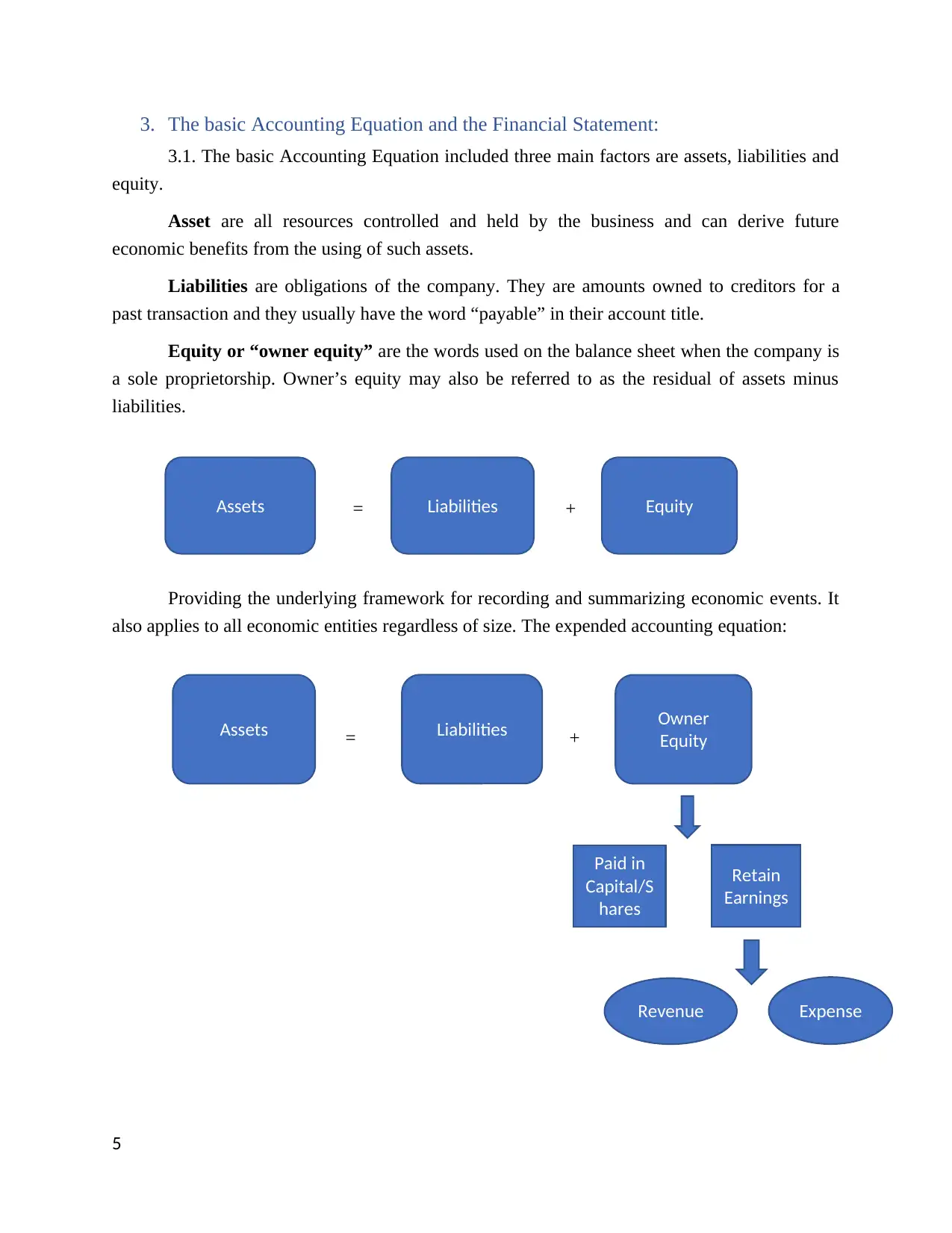

3. The basic Accounting Equation and the Financial Statement:

3.1. The basic Accounting Equation included three main factors are assets, liabilities and

equity.

Asset are all resources controlled and held by the business and can derive future

economic benefits from the using of such assets.

Liabilities are obligations of the company. They are amounts owned to creditors for a

past transaction and they usually have the word “payable” in their account title.

Equity or “owner equity” are the words used on the balance sheet when the company is

a sole proprietorship. Owner’s equity may also be referred to as the residual of assets minus

liabilities.

= +

Providing the underlying framework for recording and summarizing economic events. It

also applies to all economic entities regardless of size. The expended accounting equation:

= +

5

Assets Liabilities Equity

Assets Liabilities Owner

Equity

Paid in

Capital/S

hares

Retain

Earnings

Revenue Expense

3.1. The basic Accounting Equation included three main factors are assets, liabilities and

equity.

Asset are all resources controlled and held by the business and can derive future

economic benefits from the using of such assets.

Liabilities are obligations of the company. They are amounts owned to creditors for a

past transaction and they usually have the word “payable” in their account title.

Equity or “owner equity” are the words used on the balance sheet when the company is

a sole proprietorship. Owner’s equity may also be referred to as the residual of assets minus

liabilities.

= +

Providing the underlying framework for recording and summarizing economic events. It

also applies to all economic entities regardless of size. The expended accounting equation:

= +

5

Assets Liabilities Equity

Assets Liabilities Owner

Equity

Paid in

Capital/S

hares

Retain

Earnings

Revenue Expense

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.2. The Financial Statement are written records that convey the business transactions and

the financial outcomes of the company. Financial statements are audited by government

agencies, accountants, firms… so as to ensure accuracy and for tax, financing or investing

purposes. There are three different kinds of financial statements.

1) Balance Sheet: Providing an overview of a company’s assets, liabilities and

stockholders’equity as a snapshoot in time. The balance sheet identifies how assets are funded,

either with liabilities, such as debt, or stockholders’ equity, such as retained earnings and

additional paid-in capital. There are three items included in the balance sheet: Assets, liabilities

and shareholders’ equity.

2) Income Statement: An income statement is used for reporting a company’s financial

performance over a specific accounting period. Also known as the profit and loss statement or

the statement of revenue and expense, the income statement primarily focuses on a company’s

revenues and expenses during a particular period.

3) Cash Flow: The cash flow is used for measuring the company generates cash to pay its

debt obligations, fund its operating expenses and fund investment. The cash flow can help

investors to gain deeper insight into the operation of a company such as where its money is

coming from, how money is being spent, whether a company is on a solid financial footing.

II. Applying the double entry book-keeping system of debits and credits

to record sales and purchases transactions in a general ledger:

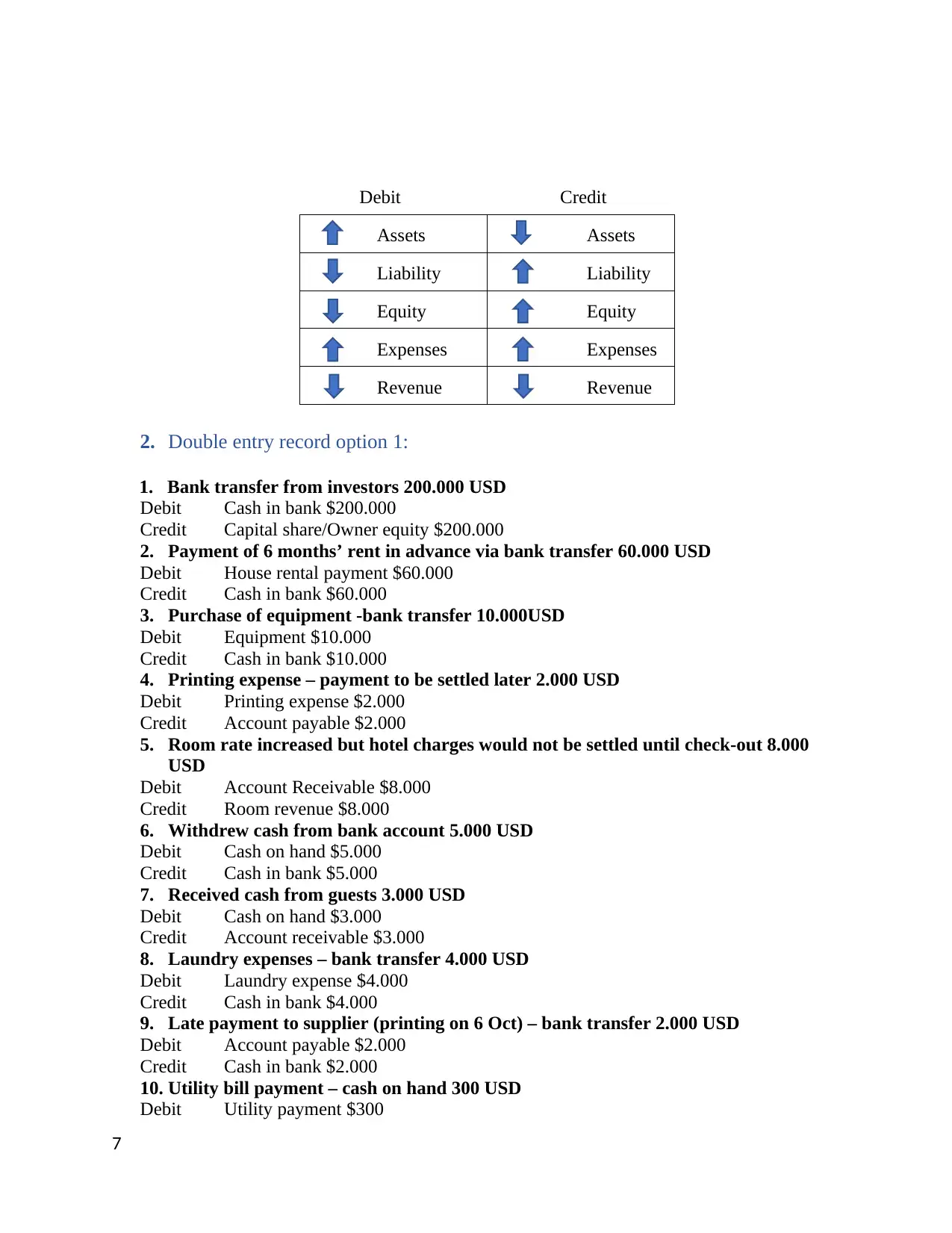

1. Definition of double entry accounting and debit/credit rules:

1.1. Double entry accounting is a system of recording business transactions where each

transaction affects at least two accounts and requires an equal debit and credit. Each transaction

must affect two or more accounts to keep the basic accounting equation in balance. Recording

done by debiting at least one account and crediting another. The total debits and credits in an

accounting system must be equal.

If debit amounts are greater than credit amounts, the account will have a debit balance. If debit

amounts are less than credit amounts, the account will have a credit balance.

1.2. The debit/credit rules:

6

the financial outcomes of the company. Financial statements are audited by government

agencies, accountants, firms… so as to ensure accuracy and for tax, financing or investing

purposes. There are three different kinds of financial statements.

1) Balance Sheet: Providing an overview of a company’s assets, liabilities and

stockholders’equity as a snapshoot in time. The balance sheet identifies how assets are funded,

either with liabilities, such as debt, or stockholders’ equity, such as retained earnings and

additional paid-in capital. There are three items included in the balance sheet: Assets, liabilities

and shareholders’ equity.

2) Income Statement: An income statement is used for reporting a company’s financial

performance over a specific accounting period. Also known as the profit and loss statement or

the statement of revenue and expense, the income statement primarily focuses on a company’s

revenues and expenses during a particular period.

3) Cash Flow: The cash flow is used for measuring the company generates cash to pay its

debt obligations, fund its operating expenses and fund investment. The cash flow can help

investors to gain deeper insight into the operation of a company such as where its money is

coming from, how money is being spent, whether a company is on a solid financial footing.

II. Applying the double entry book-keeping system of debits and credits

to record sales and purchases transactions in a general ledger:

1. Definition of double entry accounting and debit/credit rules:

1.1. Double entry accounting is a system of recording business transactions where each

transaction affects at least two accounts and requires an equal debit and credit. Each transaction

must affect two or more accounts to keep the basic accounting equation in balance. Recording

done by debiting at least one account and crediting another. The total debits and credits in an

accounting system must be equal.

If debit amounts are greater than credit amounts, the account will have a debit balance. If debit

amounts are less than credit amounts, the account will have a credit balance.

1.2. The debit/credit rules:

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debit Credit

Assets Assets

Liability Liability

Equity Equity

Expenses Expenses

Revenue Revenue

2. Double entry record option 1:

1. Bank transfer from investors 200.000 USD

Debit Cash in bank $200.000

Credit Capital share/Owner equity $200.000

2. Payment of 6 months’ rent in advance via bank transfer 60.000 USD

Debit House rental payment $60.000

Credit Cash in bank $60.000

3. Purchase of equipment -bank transfer 10.000USD

Debit Equipment $10.000

Credit Cash in bank $10.000

4. Printing expense – payment to be settled later 2.000 USD

Debit Printing expense $2.000

Credit Account payable $2.000

5. Room rate increased but hotel charges would not be settled until check-out 8.000

USD

Debit Account Receivable $8.000

Credit Room revenue $8.000

6. Withdrew cash from bank account 5.000 USD

Debit Cash on hand $5.000

Credit Cash in bank $5.000

7. Received cash from guests 3.000 USD

Debit Cash on hand $3.000

Credit Account receivable $3.000

8. Laundry expenses – bank transfer 4.000 USD

Debit Laundry expense $4.000

Credit Cash in bank $4.000

9. Late payment to supplier (printing on 6 Oct) – bank transfer 2.000 USD

Debit Account payable $2.000

Credit Cash in bank $2.000

10. Utility bill payment – cash on hand 300 USD

Debit Utility payment $300

7

Assets Assets

Liability Liability

Equity Equity

Expenses Expenses

Revenue Revenue

2. Double entry record option 1:

1. Bank transfer from investors 200.000 USD

Debit Cash in bank $200.000

Credit Capital share/Owner equity $200.000

2. Payment of 6 months’ rent in advance via bank transfer 60.000 USD

Debit House rental payment $60.000

Credit Cash in bank $60.000

3. Purchase of equipment -bank transfer 10.000USD

Debit Equipment $10.000

Credit Cash in bank $10.000

4. Printing expense – payment to be settled later 2.000 USD

Debit Printing expense $2.000

Credit Account payable $2.000

5. Room rate increased but hotel charges would not be settled until check-out 8.000

USD

Debit Account Receivable $8.000

Credit Room revenue $8.000

6. Withdrew cash from bank account 5.000 USD

Debit Cash on hand $5.000

Credit Cash in bank $5.000

7. Received cash from guests 3.000 USD

Debit Cash on hand $3.000

Credit Account receivable $3.000

8. Laundry expenses – bank transfer 4.000 USD

Debit Laundry expense $4.000

Credit Cash in bank $4.000

9. Late payment to supplier (printing on 6 Oct) – bank transfer 2.000 USD

Debit Account payable $2.000

Credit Cash in bank $2.000

10. Utility bill payment – cash on hand 300 USD

Debit Utility payment $300

7

Credit Cash on hand $300

11. Employee salary October settlement – bank transfer 20.000 USD

Debit Employee salary expense $20.000

Credit Cash in bank $20.000

12. Telephone bill payment – cash on hand 350 USD

Debit Telephone expense $350

Credit Cash on hand $350

3. Producing a basic trial balance applying the use of the balance off rule to complete

the ledger:

The Trial Balance Option 1:

GL Account Debit Credit

Cash on hand 7,350

Cash in bank 99,000

Ac Account Receivable 5,000

Ve Equipment 10,000

House rental prepaid 60,000

Account Payable 0

N Owner Equity/ Share Capital 200,000

Revenue 8,000

Utility expense 300

Printing expense 2,000

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

Balance 208000 208000

The Trial Balance Option 2:

GL Account Debit Credit

Cash on hand 9,950

Cash in bank 169,000

Ac Account Receivable 5,000

Ve Equipment 15,000

House rental prepaid 72,000

Account Payable 0

N Owner Equity/ Share Capital 300,000

Revenue 10,000

Utility expense 500

Printing expense 3000

Laundry expense 5000

8

11. Employee salary October settlement – bank transfer 20.000 USD

Debit Employee salary expense $20.000

Credit Cash in bank $20.000

12. Telephone bill payment – cash on hand 350 USD

Debit Telephone expense $350

Credit Cash on hand $350

3. Producing a basic trial balance applying the use of the balance off rule to complete

the ledger:

The Trial Balance Option 1:

GL Account Debit Credit

Cash on hand 7,350

Cash in bank 99,000

Ac Account Receivable 5,000

Ve Equipment 10,000

House rental prepaid 60,000

Account Payable 0

N Owner Equity/ Share Capital 200,000

Revenue 8,000

Utility expense 300

Printing expense 2,000

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

Balance 208000 208000

The Trial Balance Option 2:

GL Account Debit Credit

Cash on hand 9,950

Cash in bank 169,000

Ac Account Receivable 5,000

Ve Equipment 15,000

House rental prepaid 72,000

Account Payable 0

N Owner Equity/ Share Capital 300,000

Revenue 10,000

Utility expense 500

Printing expense 3000

Laundry expense 5000

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

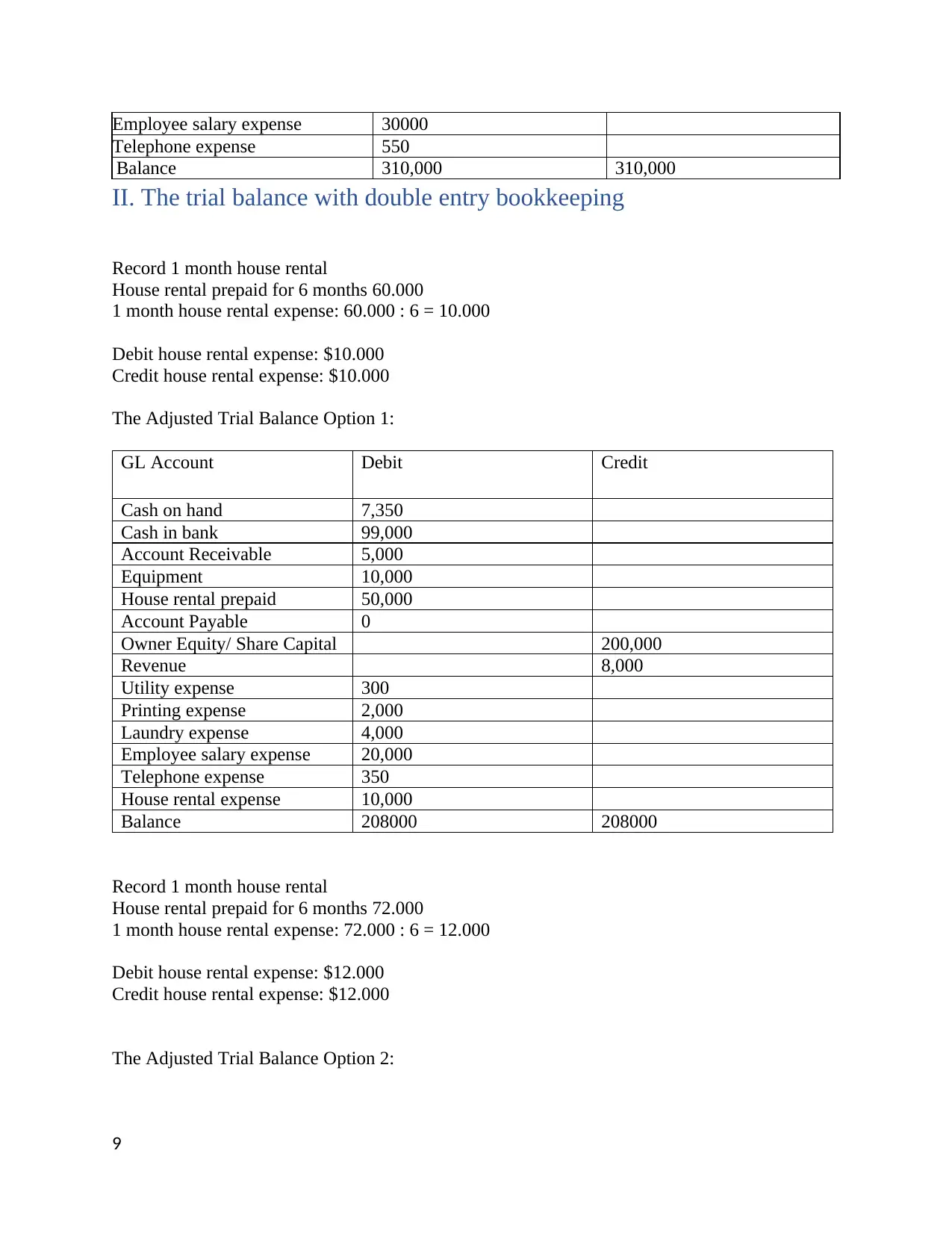

Employee salary expense 30000

Telephone expense 550

Balance 310,000 310,000

II. The trial balance with double entry bookkeeping

Record 1 month house rental

House rental prepaid for 6 months 60.000

1 month house rental expense: 60.000 : 6 = 10.000

Debit house rental expense: $10.000

Credit house rental expense: $10.000

The Adjusted Trial Balance Option 1:

GL Account Debit Credit

Cash on hand 7,350

Cash in bank 99,000

Account Receivable 5,000

Equipment 10,000

House rental prepaid 50,000

Account Payable 0

Owner Equity/ Share Capital 200,000

Revenue 8,000

Utility expense 300

Printing expense 2,000

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

House rental expense 10,000

Balance 208000 208000

Record 1 month house rental

House rental prepaid for 6 months 72.000

1 month house rental expense: 72.000 : 6 = 12.000

Debit house rental expense: $12.000

Credit house rental expense: $12.000

The Adjusted Trial Balance Option 2:

9

Telephone expense 550

Balance 310,000 310,000

II. The trial balance with double entry bookkeeping

Record 1 month house rental

House rental prepaid for 6 months 60.000

1 month house rental expense: 60.000 : 6 = 10.000

Debit house rental expense: $10.000

Credit house rental expense: $10.000

The Adjusted Trial Balance Option 1:

GL Account Debit Credit

Cash on hand 7,350

Cash in bank 99,000

Account Receivable 5,000

Equipment 10,000

House rental prepaid 50,000

Account Payable 0

Owner Equity/ Share Capital 200,000

Revenue 8,000

Utility expense 300

Printing expense 2,000

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

House rental expense 10,000

Balance 208000 208000

Record 1 month house rental

House rental prepaid for 6 months 72.000

1 month house rental expense: 72.000 : 6 = 12.000

Debit house rental expense: $12.000

Credit house rental expense: $12.000

The Adjusted Trial Balance Option 2:

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

GL Account Debit Credit

Cash on hand 9,950

Cash in bank 169,000

Account Receivable 5,000

Equipment 15,000

House rental prepaid 60,000

Account Payable 0

Owner Equity/ Share Capital 300,000

Revenue 10,000

Utility expense 500

Printing expense 3000

Laundry expense 5000

Employee salary expense 30000

Telephone expense 550

House rental expense 12,000

Balance 310,000 310,000

III. Recording correctly transactions and an accurate trial balance by

completing the balance off ledger accounts with accepted accounting

principles.

1. The income statement and profit and loss statement option 1 and option 2:

1.1. The Income Statement Option 1:

Revenue 8,000

Total revenue 8,000

Printing expense 2,000

Utility expense 300

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

House rental expense 10,000

Total expense 36650

Profit (loss) -28650

1.2. The Income Statement Option 2:

Revenue 10,000

Total revenue 10,000

Printing expense 3000

Utility expense 500

Laundry expense 5000

10

Cash on hand 9,950

Cash in bank 169,000

Account Receivable 5,000

Equipment 15,000

House rental prepaid 60,000

Account Payable 0

Owner Equity/ Share Capital 300,000

Revenue 10,000

Utility expense 500

Printing expense 3000

Laundry expense 5000

Employee salary expense 30000

Telephone expense 550

House rental expense 12,000

Balance 310,000 310,000

III. Recording correctly transactions and an accurate trial balance by

completing the balance off ledger accounts with accepted accounting

principles.

1. The income statement and profit and loss statement option 1 and option 2:

1.1. The Income Statement Option 1:

Revenue 8,000

Total revenue 8,000

Printing expense 2,000

Utility expense 300

Laundry expense 4,000

Employee salary expense 20,000

Telephone expense 350

House rental expense 10,000

Total expense 36650

Profit (loss) -28650

1.2. The Income Statement Option 2:

Revenue 10,000

Total revenue 10,000

Printing expense 3000

Utility expense 500

Laundry expense 5000

10

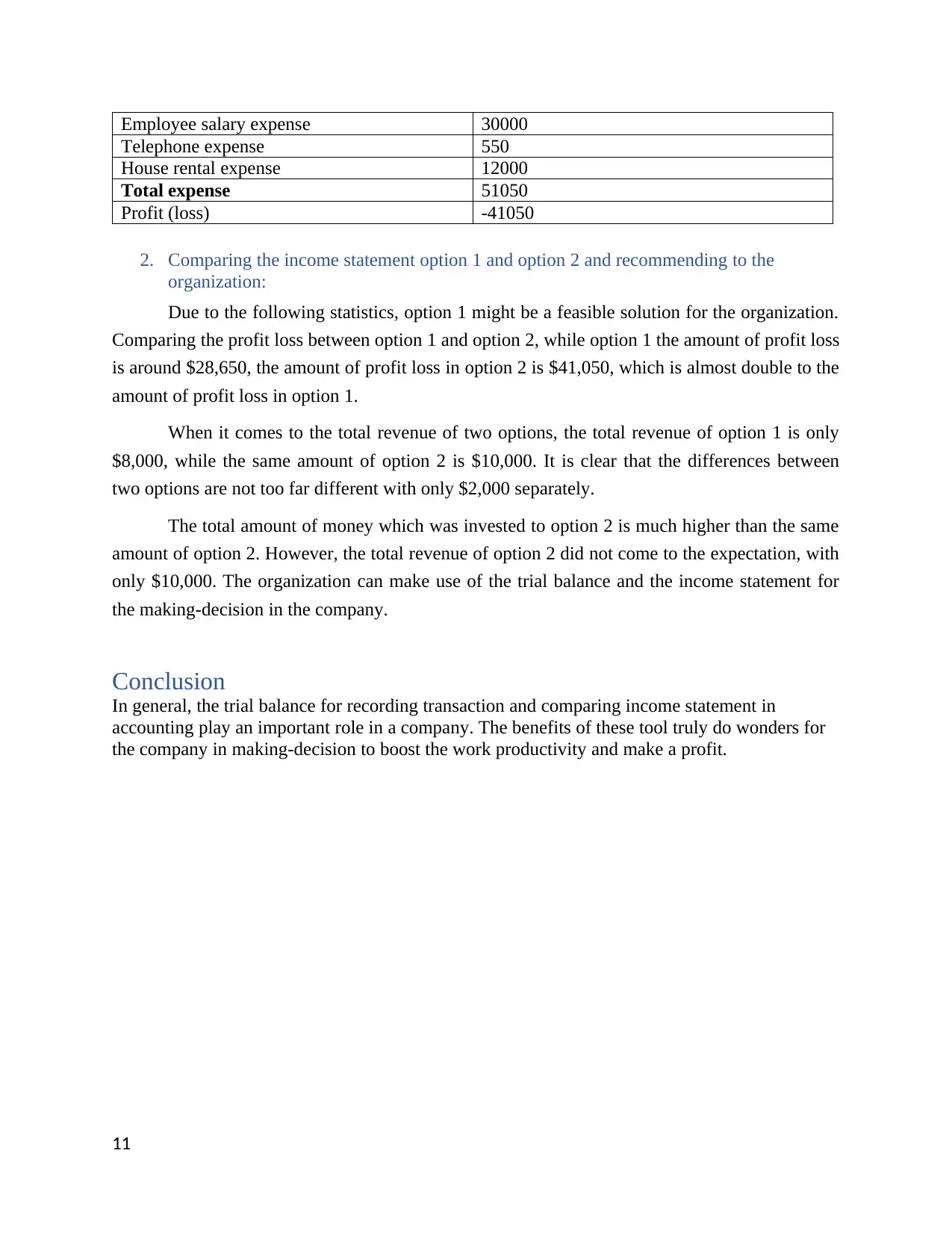

Employee salary expense 30000

Telephone expense 550

House rental expense 12000

Total expense 51050

Profit (loss) -41050

2. Comparing the income statement option 1 and option 2 and recommending to the

organization:

Due to the following statistics, option 1 might be a feasible solution for the organization.

Comparing the profit loss between option 1 and option 2, while option 1 the amount of profit loss

is around $28,650, the amount of profit loss in option 2 is $41,050, which is almost double to the

amount of profit loss in option 1.

When it comes to the total revenue of two options, the total revenue of option 1 is only

$8,000, while the same amount of option 2 is $10,000. It is clear that the differences between

two options are not too far different with only $2,000 separately.

The total amount of money which was invested to option 2 is much higher than the same

amount of option 2. However, the total revenue of option 2 did not come to the expectation, with

only $10,000. The organization can make use of the trial balance and the income statement for

the making-decision in the company.

Conclusion

In general, the trial balance for recording transaction and comparing income statement in

accounting play an important role in a company. The benefits of these tool truly do wonders for

the company in making-decision to boost the work productivity and make a profit.

11

Telephone expense 550

House rental expense 12000

Total expense 51050

Profit (loss) -41050

2. Comparing the income statement option 1 and option 2 and recommending to the

organization:

Due to the following statistics, option 1 might be a feasible solution for the organization.

Comparing the profit loss between option 1 and option 2, while option 1 the amount of profit loss

is around $28,650, the amount of profit loss in option 2 is $41,050, which is almost double to the

amount of profit loss in option 1.

When it comes to the total revenue of two options, the total revenue of option 1 is only

$8,000, while the same amount of option 2 is $10,000. It is clear that the differences between

two options are not too far different with only $2,000 separately.

The total amount of money which was invested to option 2 is much higher than the same

amount of option 2. However, the total revenue of option 2 did not come to the expectation, with

only $10,000. The organization can make use of the trial balance and the income statement for

the making-decision in the company.

Conclusion

In general, the trial balance for recording transaction and comparing income statement in

accounting play an important role in a company. The benefits of these tool truly do wonders for

the company in making-decision to boost the work productivity and make a profit.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.