Unit 13 Financial Reporting: Standards and Global Market Analysis

VerifiedAdded on 2023/06/30

|14

|4033

|487

Report

AI Summary

This report provides a detailed analysis of financial reporting in global markets, focusing on the context, purpose, and evaluation of financial reporting standards. It assesses the role of financial reporting in meeting stakeholder expectations, predicting future performance, and ensuring compliance. The report evaluates the benefits of IAS and IFRS, highlighting their impact on transparency, consistency, and comparability of financial information. It also addresses the differences between IAS and IFRS and their application in global financial reporting practices. This document is available on Desklib, a platform offering a wide range of study tools and resources for students.

Higher Nationals

Assignment Brief – BTEC (RQF)

Higher National Diploma in Business

Student Name DENISA FIRTU ID HE07394

Unit Number and Title Unit 13 Financial Reporting

Academic Year 2019-20 Cohort April 19 Term Block 6

Unit Leader Syed Ahmed Assessor Joseph Olaniyan

Assignment Title Financial reporting in global markets

Issue Date 13.07.2020

Submission Start Date (Formative) 28.09.2020

Submission Summative 10.10.2020

IV Name Seethalakshmy Nagarajan

IV Date 13.07.2020

Learners Declaration: I certify that the work submitted for this unit is my own and the research sources are fully

acknowledged.

Learners Name: DENISA FIRTU Date: 25.09.2020

1

Assignment Brief – BTEC (RQF)

Higher National Diploma in Business

Student Name DENISA FIRTU ID HE07394

Unit Number and Title Unit 13 Financial Reporting

Academic Year 2019-20 Cohort April 19 Term Block 6

Unit Leader Syed Ahmed Assessor Joseph Olaniyan

Assignment Title Financial reporting in global markets

Issue Date 13.07.2020

Submission Start Date (Formative) 28.09.2020

Submission Summative 10.10.2020

IV Name Seethalakshmy Nagarajan

IV Date 13.07.2020

Learners Declaration: I certify that the work submitted for this unit is my own and the research sources are fully

acknowledged.

Learners Name: DENISA FIRTU Date: 25.09.2020

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:................................................................................................................................. 3

LO1: Context and purpose of financial reporting:.........................................................................4

Context of financial reporting:...................................................................................................4

Purpose of financial reporting:..................................................................................................5

LO3 Evaluate financial reporting standards and theoretical models and concepts......................7

IAS and IFRS Benefits:............................................................................................................ 7

Models of financial reporting and auditing:...............................................................................9

LO4 Evaluate international differences in financial reporting.....................................................10

Conclusion:................................................................................................................................ 12

References:............................................................................................................................... 13

2

Introduction:................................................................................................................................. 3

LO1: Context and purpose of financial reporting:.........................................................................4

Context of financial reporting:...................................................................................................4

Purpose of financial reporting:..................................................................................................5

LO3 Evaluate financial reporting standards and theoretical models and concepts......................7

IAS and IFRS Benefits:............................................................................................................ 7

Models of financial reporting and auditing:...............................................................................9

LO4 Evaluate international differences in financial reporting.....................................................10

Conclusion:................................................................................................................................ 12

References:............................................................................................................................... 13

2

Introduction:

The purpose of this research study is to analyze the financial reporting by consigning the

context and purpose of the reporting. It will include the analysis of the different objectives for

which financial reporting is made by the businesses. It will include the assessment of the

difference between the IFRS and IAS that regulates the accounting and reporting practices

within the company. In addition to this, the degree to which the businesses are abiding by the

IFRS and other standards will be analyzed in this report.

3

The purpose of this research study is to analyze the financial reporting by consigning the

context and purpose of the reporting. It will include the analysis of the different objectives for

which financial reporting is made by the businesses. It will include the assessment of the

difference between the IFRS and IAS that regulates the accounting and reporting practices

within the company. In addition to this, the degree to which the businesses are abiding by the

IFRS and other standards will be analyzed in this report.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO1: Context and purpose of financial reporting:

Context of financial reporting:

A report that is used for presenting and revealing the information to the stakeholder of the firm

to make them aware of the performance, financial issues, and other accounting information of

the company (Ankarath et al., 2010). A process of preparing the financial accounts and

developing the statements in the report can be stated as the financial reporting that can be

affected the stakeholder such as shareholders, lenders, management, suppliers, government,

and others. The financial reports must include a statement of the financial position, income

statement, change in equity, and cash flow statement along with financial notes to avail detailed

information to the users (Epstein and Jermakowicz, 2010). The report of the businesses must

be prepared by including the document such as risk management report, report of CEO,

Director’s report, and others. The compliance with guidelines mentioned in the laws and

accounting regulations must be followed by the businesses to prepare a valid report.

The regulations for the reporting are the conceptual framework to govern the process of

preparation of the financial statement and preparing the reports. It creates a strong framework

that is used for preparing the financial stamen in the report and it improves the effectiveness in

the reporting (Ankarath et al., 2010). The regulatory framework includes the law of lend,

conceptual framework, and reporting standards. The regulatory frameworks that have to be

abided by the businesses may include the regulations, guidelines, standards, procedures, code

of conduct, and others.

Law of Land is applied like legislation to govern and regulate the firms for the creation of

recording documents for all the kinds of information and for developing the statements to

publish the information. All the firms incorporated and registered are bound for preparing he

reports for the stakeholder while the firms which are not incorporated are not legally bound that

they must create reports for their self-assessment of financial performance (Louwers et al.,

2015).

Along with this, there are some standards in the compliance framework that has to be

considered by organizations while building up and develop financial reports. These standards

include GAAP, IFRS, IAS, and local accounting standards (Van Greuning et al., 2011). The

functioning and rules in each standard and reporting rules are developed by the IASC and other

4

Context of financial reporting:

A report that is used for presenting and revealing the information to the stakeholder of the firm

to make them aware of the performance, financial issues, and other accounting information of

the company (Ankarath et al., 2010). A process of preparing the financial accounts and

developing the statements in the report can be stated as the financial reporting that can be

affected the stakeholder such as shareholders, lenders, management, suppliers, government,

and others. The financial reports must include a statement of the financial position, income

statement, change in equity, and cash flow statement along with financial notes to avail detailed

information to the users (Epstein and Jermakowicz, 2010). The report of the businesses must

be prepared by including the document such as risk management report, report of CEO,

Director’s report, and others. The compliance with guidelines mentioned in the laws and

accounting regulations must be followed by the businesses to prepare a valid report.

The regulations for the reporting are the conceptual framework to govern the process of

preparation of the financial statement and preparing the reports. It creates a strong framework

that is used for preparing the financial stamen in the report and it improves the effectiveness in

the reporting (Ankarath et al., 2010). The regulatory framework includes the law of lend,

conceptual framework, and reporting standards. The regulatory frameworks that have to be

abided by the businesses may include the regulations, guidelines, standards, procedures, code

of conduct, and others.

Law of Land is applied like legislation to govern and regulate the firms for the creation of

recording documents for all the kinds of information and for developing the statements to

publish the information. All the firms incorporated and registered are bound for preparing he

reports for the stakeholder while the firms which are not incorporated are not legally bound that

they must create reports for their self-assessment of financial performance (Louwers et al.,

2015).

Along with this, there are some standards in the compliance framework that has to be

considered by organizations while building up and develop financial reports. These standards

include GAAP, IFRS, IAS, and local accounting standards (Van Greuning et al., 2011). The

functioning and rules in each standard and reporting rules are developed by the IASC and other

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bodies that involves in process of developing rules in the standards are the IFRSC, IASB, and

others. The objective for creating a regulatory framework in financial reporting are given below:

To enhance the quality of the statements so that they can be used for decision making

To improve the understandability of financial reports of the entities (Ankarath et al.,

2010)

To improve the degree of consistency in the reports for improving the possibility of

comparison

To enhance the degree of transparency in the financial reports

To enhance the reliability, validity, and accuracy of the data in the reports (Van Greuning

et al., 2011)

Purpose of financial reporting:

Stakeholder Expectation:

The financial reports are aimed at meeting the stakeholder expectations by offering user-based

information in the statements and documents. There are many stakeholders of the firm that

require accounting and financial information.

Business

Manager

The manager of business requires detailed information regarding the

business transactions and financial performance for planning actions and

strategies to remove the issues and enhance the performance for

attaining the purpose of the organization (Ankarath et al., 2010).

Financial reports avail the information about the financial performance by

comparing with the past that enables the managers to find the gap and

take effective actions or decision to control the declining performance if it

is.

Business Owner The owner of the business is concerned about the performance of the

firm. Hence, the financial report every year helps them to track the

performance and evaluate whether the company is trending upwards or

not. The analysis of the information in the financial reports aids the owner

to determine whether the firm is acquiring the goals or not (Epstein and

Jermakowicz, 2010)

Government The bodies and agencies of the government require the organization to

5

others. The objective for creating a regulatory framework in financial reporting are given below:

To enhance the quality of the statements so that they can be used for decision making

To improve the understandability of financial reports of the entities (Ankarath et al.,

2010)

To improve the degree of consistency in the reports for improving the possibility of

comparison

To enhance the degree of transparency in the financial reports

To enhance the reliability, validity, and accuracy of the data in the reports (Van Greuning

et al., 2011)

Purpose of financial reporting:

Stakeholder Expectation:

The financial reports are aimed at meeting the stakeholder expectations by offering user-based

information in the statements and documents. There are many stakeholders of the firm that

require accounting and financial information.

Business

Manager

The manager of business requires detailed information regarding the

business transactions and financial performance for planning actions and

strategies to remove the issues and enhance the performance for

attaining the purpose of the organization (Ankarath et al., 2010).

Financial reports avail the information about the financial performance by

comparing with the past that enables the managers to find the gap and

take effective actions or decision to control the declining performance if it

is.

Business Owner The owner of the business is concerned about the performance of the

firm. Hence, the financial report every year helps them to track the

performance and evaluate whether the company is trending upwards or

not. The analysis of the information in the financial reports aids the owner

to determine whether the firm is acquiring the goals or not (Epstein and

Jermakowicz, 2010)

Government The bodies and agencies of the government require the organization to

5

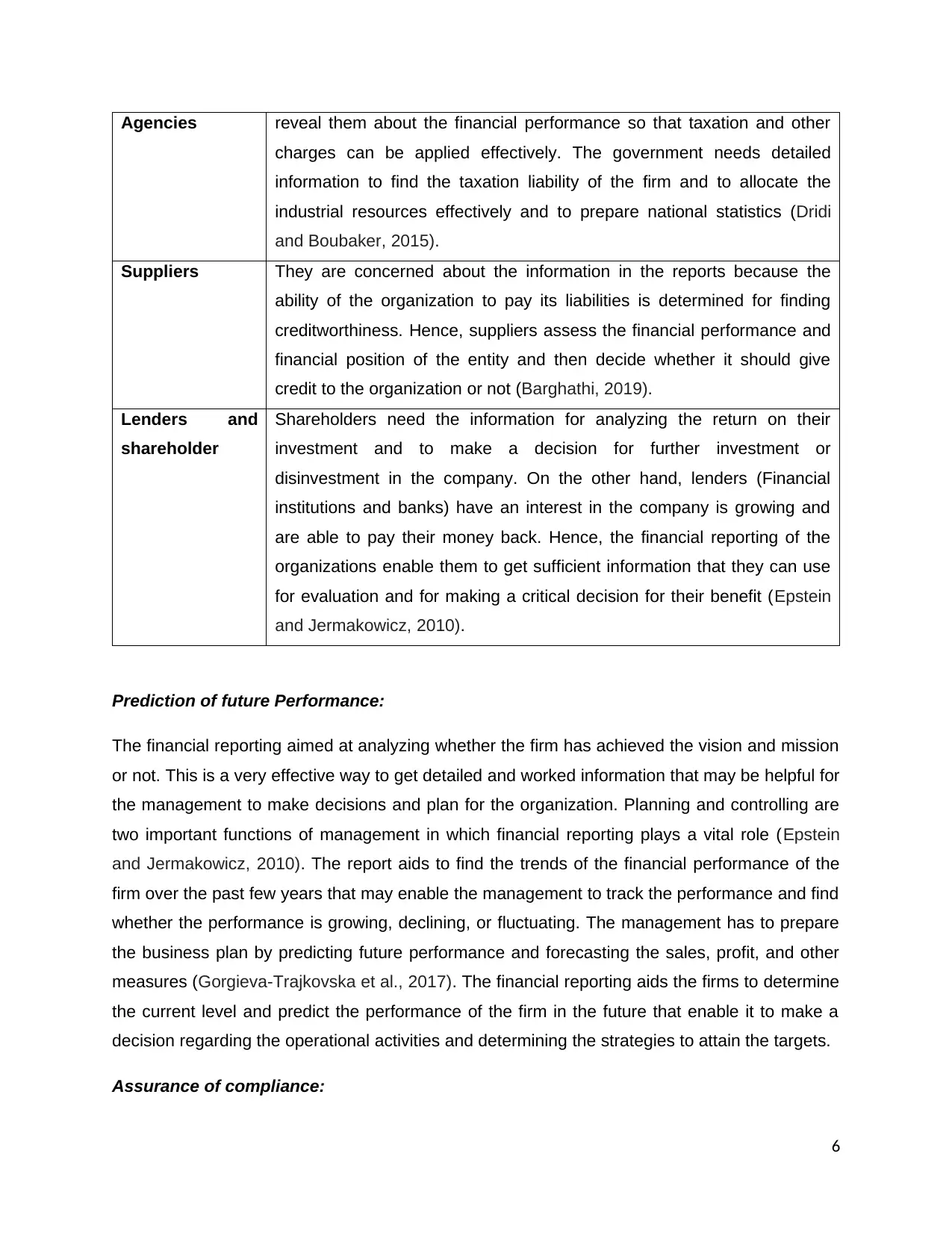

Agencies reveal them about the financial performance so that taxation and other

charges can be applied effectively. The government needs detailed

information to find the taxation liability of the firm and to allocate the

industrial resources effectively and to prepare national statistics (Dridi

and Boubaker, 2015).

Suppliers They are concerned about the information in the reports because the

ability of the organization to pay its liabilities is determined for finding

creditworthiness. Hence, suppliers assess the financial performance and

financial position of the entity and then decide whether it should give

credit to the organization or not (Barghathi, 2019).

Lenders and

shareholder

Shareholders need the information for analyzing the return on their

investment and to make a decision for further investment or

disinvestment in the company. On the other hand, lenders (Financial

institutions and banks) have an interest in the company is growing and

are able to pay their money back. Hence, the financial reporting of the

organizations enable them to get sufficient information that they can use

for evaluation and for making a critical decision for their benefit (Epstein

and Jermakowicz, 2010).

Prediction of future Performance:

The financial reporting aimed at analyzing whether the firm has achieved the vision and mission

or not. This is a very effective way to get detailed and worked information that may be helpful for

the management to make decisions and plan for the organization. Planning and controlling are

two important functions of management in which financial reporting plays a vital role (Epstein

and Jermakowicz, 2010). The report aids to find the trends of the financial performance of the

firm over the past few years that may enable the management to track the performance and find

whether the performance is growing, declining, or fluctuating. The management has to prepare

the business plan by predicting future performance and forecasting the sales, profit, and other

measures (Gorgieva-Trajkovska et al., 2017). The financial reporting aids the firms to determine

the current level and predict the performance of the firm in the future that enable it to make a

decision regarding the operational activities and determining the strategies to attain the targets.

Assurance of compliance:

6

charges can be applied effectively. The government needs detailed

information to find the taxation liability of the firm and to allocate the

industrial resources effectively and to prepare national statistics (Dridi

and Boubaker, 2015).

Suppliers They are concerned about the information in the reports because the

ability of the organization to pay its liabilities is determined for finding

creditworthiness. Hence, suppliers assess the financial performance and

financial position of the entity and then decide whether it should give

credit to the organization or not (Barghathi, 2019).

Lenders and

shareholder

Shareholders need the information for analyzing the return on their

investment and to make a decision for further investment or

disinvestment in the company. On the other hand, lenders (Financial

institutions and banks) have an interest in the company is growing and

are able to pay their money back. Hence, the financial reporting of the

organizations enable them to get sufficient information that they can use

for evaluation and for making a critical decision for their benefit (Epstein

and Jermakowicz, 2010).

Prediction of future Performance:

The financial reporting aimed at analyzing whether the firm has achieved the vision and mission

or not. This is a very effective way to get detailed and worked information that may be helpful for

the management to make decisions and plan for the organization. Planning and controlling are

two important functions of management in which financial reporting plays a vital role (Epstein

and Jermakowicz, 2010). The report aids to find the trends of the financial performance of the

firm over the past few years that may enable the management to track the performance and find

whether the performance is growing, declining, or fluctuating. The management has to prepare

the business plan by predicting future performance and forecasting the sales, profit, and other

measures (Gorgieva-Trajkovska et al., 2017). The financial reporting aids the firms to determine

the current level and predict the performance of the firm in the future that enable it to make a

decision regarding the operational activities and determining the strategies to attain the targets.

Assurance of compliance:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The financial reporting is also conducted for ensuring the availability of the required, valid,

reliable, and accurate information for the managers and other stakeholders. The report may

enable the firms to assure their compliance with the regulations and standards of accounting

and reporting (Van Greuning et al., 2011). The quality of the statements of businesses is

presented through the financial reports. The businesses can present the following

characteristics of the statements:

All the information in the statement are totally relevant to the operation of the firms and

its financial transactions which are required in decision making

All the data in the statements have been demonstrated in a faithful way that increases

the confidence of the stakeholder

All the data are correct, accurate, valid, and reliable for the decision making by

stakeholder

The information is comparative to improve the effectiveness of the reports and to

improve understanding of users (Louwers et al., 2015)

LO3 Evaluate financial reporting standards and theoretical models and concepts

IAS and IFRS Benefits:

IAS and IFRS are two important standards that are applied for governing the financial reporting

practice within the companies.

Evaluation of Benefits of IFRS:

International Financial Reporting Standard governs the reporting of the organization for ensuring

transparency, consistency, comparability, and relevance of the information in the statement and

reports. It is the abided by the international businesses to ensure integration of the financial

performance and consolidation of information of business units operating in different nations

(Kieso et al., 2010).

It may ensure the availability of the information in a comparative manner at one year in

the report that enables the users such as management, lenders, shareholder for

evaluating the information, and making a decision can give maximum benefit (Palepu et

al., 2013). Management of the company may decide strategies as per the information for

gaining sustainable growth of the firm (Palea, 2013).

7

reliable, and accurate information for the managers and other stakeholders. The report may

enable the firms to assure their compliance with the regulations and standards of accounting

and reporting (Van Greuning et al., 2011). The quality of the statements of businesses is

presented through the financial reports. The businesses can present the following

characteristics of the statements:

All the information in the statement are totally relevant to the operation of the firms and

its financial transactions which are required in decision making

All the data in the statements have been demonstrated in a faithful way that increases

the confidence of the stakeholder

All the data are correct, accurate, valid, and reliable for the decision making by

stakeholder

The information is comparative to improve the effectiveness of the reports and to

improve understanding of users (Louwers et al., 2015)

LO3 Evaluate financial reporting standards and theoretical models and concepts

IAS and IFRS Benefits:

IAS and IFRS are two important standards that are applied for governing the financial reporting

practice within the companies.

Evaluation of Benefits of IFRS:

International Financial Reporting Standard governs the reporting of the organization for ensuring

transparency, consistency, comparability, and relevance of the information in the statement and

reports. It is the abided by the international businesses to ensure integration of the financial

performance and consolidation of information of business units operating in different nations

(Kieso et al., 2010).

It may ensure the availability of the information in a comparative manner at one year in

the report that enables the users such as management, lenders, shareholder for

evaluating the information, and making a decision can give maximum benefit (Palepu et

al., 2013). Management of the company may decide strategies as per the information for

gaining sustainable growth of the firm (Palea, 2013).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IFRS ensures the disclosure of valid and reliable information in the reports that are

useful for the organization to find the challenge and to determine the possible issues in

the financial performance. It may improve the effectiveness of future strategies. The

users and stakeholders can improve the effectiveness of their decision to get maximum

return on their investment (Iatridis, 2010).

The transparency in the operation is improved by IFRS by availed information and data

about the operation and performance to the stakeholder and this improves the

relationship of the organization with its stakeholders. Investors would be more involved

in the operation as transparency would encourage them to put money in the organization

(Palea, 2013).

The detailed and complete information is given by the organization to investors by

following IFRS that benefit to investors. They would be in a good position to investigate

the capability of the entity and make the decision for the investment (Palepu et al., 2013)

Benefits of IAS:

IAS is an older standard of accounting and it was introduced by the IASB that is an international

body for setting accounting standards. The purpose of the IAS was to integrate the accounting

practices and the firms operating internationally can use the global financial reporting

framework. This was to improve the governance for effective regulation of the financial reporting

and financial reports (Iatridis, 2010). The biggest benefit of the IAS is that it provides separate

rules and regulation for each item in the statements and this improve the effectiveness of the

reporting. The organization can easily understand the IAS regulations for accounting practices.

IAS enables organizations to easily consolidating the financial statement of the different

divisions and operations of a giant.

Difference between IAS and IFRS:

Technically said IFRS is similar to the IAS. IFRS is the current set of the standard for accounting

while IAS is the older set of accounting. Some of the standards are updated in IFRS but many of

the IASs that are not superseded by the IFRS are still being used for governing the practices of

reporting by the firms (Iatridis, 2010).

IAS IFRS

IAS is known as the International Accounting IFRS is known as International Financial

8

useful for the organization to find the challenge and to determine the possible issues in

the financial performance. It may improve the effectiveness of future strategies. The

users and stakeholders can improve the effectiveness of their decision to get maximum

return on their investment (Iatridis, 2010).

The transparency in the operation is improved by IFRS by availed information and data

about the operation and performance to the stakeholder and this improves the

relationship of the organization with its stakeholders. Investors would be more involved

in the operation as transparency would encourage them to put money in the organization

(Palea, 2013).

The detailed and complete information is given by the organization to investors by

following IFRS that benefit to investors. They would be in a good position to investigate

the capability of the entity and make the decision for the investment (Palepu et al., 2013)

Benefits of IAS:

IAS is an older standard of accounting and it was introduced by the IASB that is an international

body for setting accounting standards. The purpose of the IAS was to integrate the accounting

practices and the firms operating internationally can use the global financial reporting

framework. This was to improve the governance for effective regulation of the financial reporting

and financial reports (Iatridis, 2010). The biggest benefit of the IAS is that it provides separate

rules and regulation for each item in the statements and this improve the effectiveness of the

reporting. The organization can easily understand the IAS regulations for accounting practices.

IAS enables organizations to easily consolidating the financial statement of the different

divisions and operations of a giant.

Difference between IAS and IFRS:

Technically said IFRS is similar to the IAS. IFRS is the current set of the standard for accounting

while IAS is the older set of accounting. Some of the standards are updated in IFRS but many of

the IASs that are not superseded by the IFRS are still being used for governing the practices of

reporting by the firms (Iatridis, 2010).

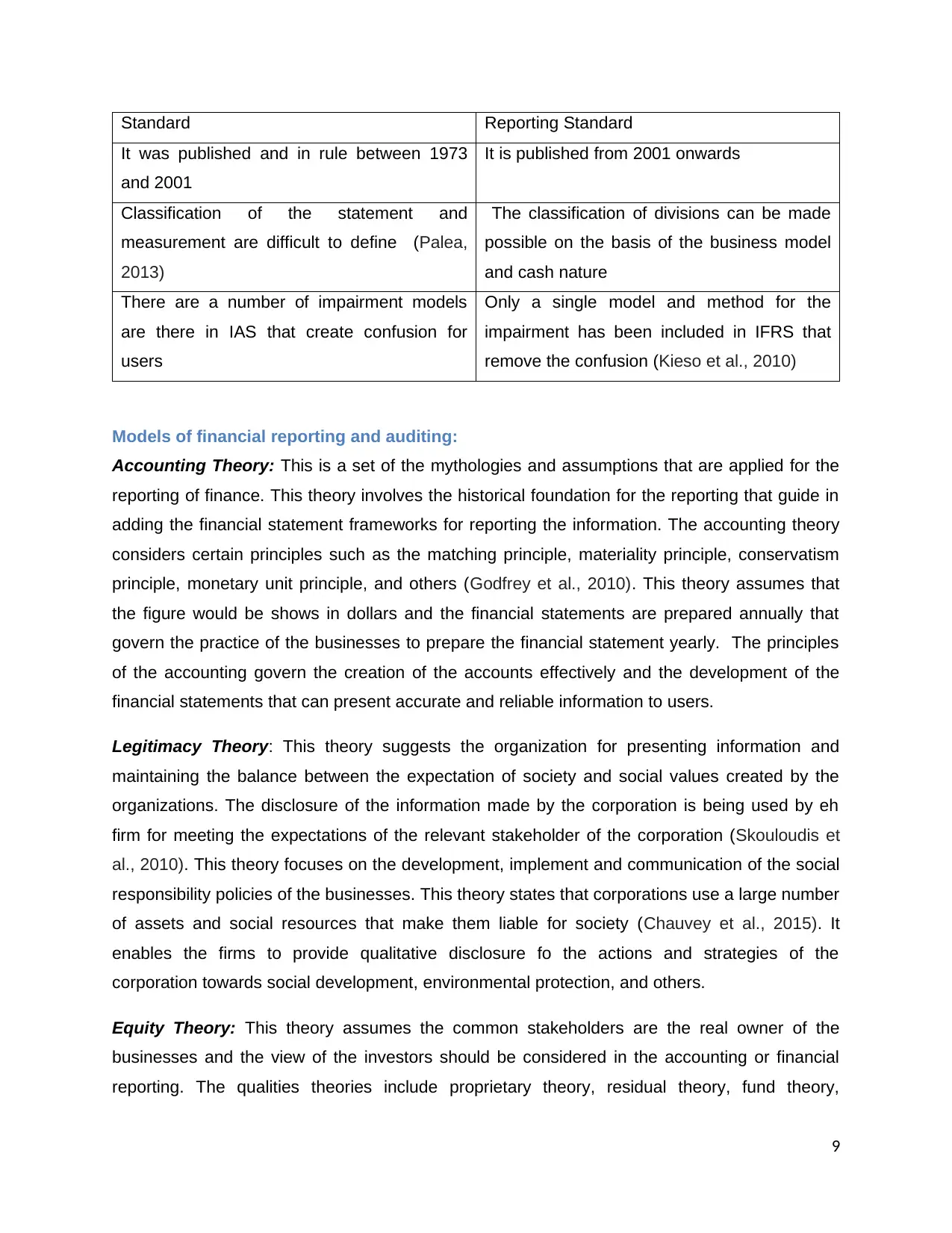

IAS IFRS

IAS is known as the International Accounting IFRS is known as International Financial

8

Standard Reporting Standard

It was published and in rule between 1973

and 2001

It is published from 2001 onwards

Classification of the statement and

measurement are difficult to define (Palea,

2013)

The classification of divisions can be made

possible on the basis of the business model

and cash nature

There are a number of impairment models

are there in IAS that create confusion for

users

Only a single model and method for the

impairment has been included in IFRS that

remove the confusion (Kieso et al., 2010)

Models of financial reporting and auditing:

Accounting Theory: This is a set of the mythologies and assumptions that are applied for the

reporting of finance. This theory involves the historical foundation for the reporting that guide in

adding the financial statement frameworks for reporting the information. The accounting theory

considers certain principles such as the matching principle, materiality principle, conservatism

principle, monetary unit principle, and others (Godfrey et al., 2010). This theory assumes that

the figure would be shows in dollars and the financial statements are prepared annually that

govern the practice of the businesses to prepare the financial statement yearly. The principles

of the accounting govern the creation of the accounts effectively and the development of the

financial statements that can present accurate and reliable information to users.

Legitimacy Theory: This theory suggests the organization for presenting information and

maintaining the balance between the expectation of society and social values created by the

organizations. The disclosure of the information made by the corporation is being used by eh

firm for meeting the expectations of the relevant stakeholder of the corporation (Skouloudis et

al., 2010). This theory focuses on the development, implement and communication of the social

responsibility policies of the businesses. This theory states that corporations use a large number

of assets and social resources that make them liable for society (Chauvey et al., 2015). It

enables the firms to provide qualitative disclosure fo the actions and strategies of the

corporation towards social development, environmental protection, and others.

Equity Theory: This theory assumes the common stakeholders are the real owner of the

businesses and the view of the investors should be considered in the accounting or financial

reporting. The qualities theories include proprietary theory, residual theory, fund theory,

9

It was published and in rule between 1973

and 2001

It is published from 2001 onwards

Classification of the statement and

measurement are difficult to define (Palea,

2013)

The classification of divisions can be made

possible on the basis of the business model

and cash nature

There are a number of impairment models

are there in IAS that create confusion for

users

Only a single model and method for the

impairment has been included in IFRS that

remove the confusion (Kieso et al., 2010)

Models of financial reporting and auditing:

Accounting Theory: This is a set of the mythologies and assumptions that are applied for the

reporting of finance. This theory involves the historical foundation for the reporting that guide in

adding the financial statement frameworks for reporting the information. The accounting theory

considers certain principles such as the matching principle, materiality principle, conservatism

principle, monetary unit principle, and others (Godfrey et al., 2010). This theory assumes that

the figure would be shows in dollars and the financial statements are prepared annually that

govern the practice of the businesses to prepare the financial statement yearly. The principles

of the accounting govern the creation of the accounts effectively and the development of the

financial statements that can present accurate and reliable information to users.

Legitimacy Theory: This theory suggests the organization for presenting information and

maintaining the balance between the expectation of society and social values created by the

organizations. The disclosure of the information made by the corporation is being used by eh

firm for meeting the expectations of the relevant stakeholder of the corporation (Skouloudis et

al., 2010). This theory focuses on the development, implement and communication of the social

responsibility policies of the businesses. This theory states that corporations use a large number

of assets and social resources that make them liable for society (Chauvey et al., 2015). It

enables the firms to provide qualitative disclosure fo the actions and strategies of the

corporation towards social development, environmental protection, and others.

Equity Theory: This theory assumes the common stakeholders are the real owner of the

businesses and the view of the investors should be considered in the accounting or financial

reporting. The qualities theories include proprietary theory, residual theory, fund theory,

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

commander theory, and entity theory (Schroeder et al., 2019). All five theories influence the

items and accounting equation that affect the reporting in the statements of the firms.

Models of reporting and models for auditing:

The financial reports are affected and prested in different ways based on different methods and

models being used and followed by the business. Generally, three statement model is followed

by the businesses for reporting the financial information to the stakeholders. There are different

models such as three statements, consolidation model, the LBO model, the merger model, and

others that may cause an influence on the financial reporting of the businesses. Auditing is an

important activity in the accounting and it is conducted for ensuring quality in the accounts and

accuracy in the statement that is made complying with the certain rules and principles

mentioned in the standards (Godfrey et al., 2010). The audit report is a disclaimer by the

auditing firm that there are no mistakes in the accounts and the reporting by firms is complying

with IFRS and other GAAP. The audit of the organization is conducted by internal, external and

internal revenue service audits.

LO4 Evaluate international differences in financial reporting

The international differences occur when people from different countries use the financial

statement in one country for their decision but the lack of consistency and equity in the

statement may affect the decision. It is very hard for cross border investors to understand the

accounts and financial statements of the foreign companies that generally prepare the reports

considering their nation's accounting standards and principles. IFRS was created for removing

this issue and challenge for meeting the expectations of stakeholders and bringing equity and

consistency in the accounting practices in a comparable manner so that users can easily

understand the statement and can compare the performance for making their decisions (Nobes

and Stadler, 2018). However, there is an international difference before IFRS and financial

reporting. Businesses listed on the stock change must have to comply with the IFRS for

providing consistency and transparency in the statements. Almost 166 countries in the world are

using IFRS ad its principles for the reporting and accounting practices in the organizations.

More than 49000 domestic firms are listed on approx 93 stock exchange houses and approx

29000 of them are complying with IFRS rules and regulations. This is a senior difference before

IFRS. About 85% of the total organizations over the world are complying with the principle of the

10

items and accounting equation that affect the reporting in the statements of the firms.

Models of reporting and models for auditing:

The financial reports are affected and prested in different ways based on different methods and

models being used and followed by the business. Generally, three statement model is followed

by the businesses for reporting the financial information to the stakeholders. There are different

models such as three statements, consolidation model, the LBO model, the merger model, and

others that may cause an influence on the financial reporting of the businesses. Auditing is an

important activity in the accounting and it is conducted for ensuring quality in the accounts and

accuracy in the statement that is made complying with the certain rules and principles

mentioned in the standards (Godfrey et al., 2010). The audit report is a disclaimer by the

auditing firm that there are no mistakes in the accounts and the reporting by firms is complying

with IFRS and other GAAP. The audit of the organization is conducted by internal, external and

internal revenue service audits.

LO4 Evaluate international differences in financial reporting

The international differences occur when people from different countries use the financial

statement in one country for their decision but the lack of consistency and equity in the

statement may affect the decision. It is very hard for cross border investors to understand the

accounts and financial statements of the foreign companies that generally prepare the reports

considering their nation's accounting standards and principles. IFRS was created for removing

this issue and challenge for meeting the expectations of stakeholders and bringing equity and

consistency in the accounting practices in a comparable manner so that users can easily

understand the statement and can compare the performance for making their decisions (Nobes

and Stadler, 2018). However, there is an international difference before IFRS and financial

reporting. Businesses listed on the stock change must have to comply with the IFRS for

providing consistency and transparency in the statements. Almost 166 countries in the world are

using IFRS ad its principles for the reporting and accounting practices in the organizations.

More than 49000 domestic firms are listed on approx 93 stock exchange houses and approx

29000 of them are complying with IFRS rules and regulations. This is a senior difference before

IFRS. About 85% of the total organizations over the world are complying with the principle of the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IFRS in financial reporting and 15% of firms are not following the regulations but they are still

making reports on the basis of older rules and principles (IFRS, 2018). There are some factors

that influences the accounting practice and influence the practices of organization in countries

such as legalization and trade policies of the countries that can cause influence on the practices

of organizations to comply with IFRS. Political parties and decisions influence compliance with

IFRS by firms in the organizations (Chand et al., 2008). For instance, the USA does not permit

the organizations for using the IFRS but it allows them to follow and use GAAP only. IFRS is

facing De Jure and De Facto differences between the accounting practices in the nations. This

difference occurs because of the macro as well as micro factors. IFRS allows principle-based

accounting while certain nations are still focusing on the rule-based accounting that causes a

difference in financial reporting between different nations. Philippines Financial Reporting

Standards is a domestic standard of Philippine and certain modification has been made this

nation in IFRS before its adoption in the accounting practices. It has reduced the segment

reporting, commodity derivative contract, losses from the sale of nonperforming assets and

others in the case of banks and others in IFRS reporting (IAS Plus, 2020).

11

making reports on the basis of older rules and principles (IFRS, 2018). There are some factors

that influences the accounting practice and influence the practices of organization in countries

such as legalization and trade policies of the countries that can cause influence on the practices

of organizations to comply with IFRS. Political parties and decisions influence compliance with

IFRS by firms in the organizations (Chand et al., 2008). For instance, the USA does not permit

the organizations for using the IFRS but it allows them to follow and use GAAP only. IFRS is

facing De Jure and De Facto differences between the accounting practices in the nations. This

difference occurs because of the macro as well as micro factors. IFRS allows principle-based

accounting while certain nations are still focusing on the rule-based accounting that causes a

difference in financial reporting between different nations. Philippines Financial Reporting

Standards is a domestic standard of Philippine and certain modification has been made this

nation in IFRS before its adoption in the accounting practices. It has reduced the segment

reporting, commodity derivative contract, losses from the sale of nonperforming assets and

others in the case of banks and others in IFRS reporting (IAS Plus, 2020).

11

Conclusion:

From the analysis of the report, it can be summarized that this report has achieved the learning

outcomes. It is found that the conceptual framework fo the compliance may govern the reporting

practices in the organization and the purpose of the reporting is to meet the expectation of the

uses and predict the future performance of the firm. Furthermore, it is found that there is no

significant difference between IFRS and IAS. This report has identified that environmental

factors and other causes are there creating the international differences in financial reporting.

12

From the analysis of the report, it can be summarized that this report has achieved the learning

outcomes. It is found that the conceptual framework fo the compliance may govern the reporting

practices in the organization and the purpose of the reporting is to meet the expectation of the

uses and predict the future performance of the firm. Furthermore, it is found that there is no

significant difference between IFRS and IAS. This report has identified that environmental

factors and other causes are there creating the international differences in financial reporting.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.