Management Accounting Application in Wider Business Environment HNC

VerifiedAdded on 2022/08/09

|22

|4000

|31

Report

AI Summary

This report provides a comprehensive overview of management accounting and its application within the broader business environment. It covers various aspects, starting with an information booklet explaining the concept of a management accounting system and report, including different management accounting systems like inventory, cost, job costing, and price optimization. The report then delves into management accounting techniques, highlighting their use in productivity analysis, sales trend prediction, and financial planning. Furthermore, it evaluates different planning tools and their application in budget preparation and forecasting. Finally, the report compares and contrasts two management accounting systems to solve financial problems, providing a holistic understanding of how management accounting contributes to effective business management. Desklib offers a platform to explore similar solved assignments and past papers for students.

Running head: MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

Name of the University

Name of the student

Author notes

MANAGEMENT ACCOUNTING

Name of the University

Name of the student

Author notes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Task 1........................................................................................................................................2

Information booklet useful for understanding the concept of management

accounting system and management accounting report..............................................2

Task 2........................................................................................................................................9

Management accounting techniques...............................................................................9

Task 3......................................................................................................................................12

Evaluation of different planning tools and their application in budget preparation

and forecasting..................................................................................................................12

Task 4......................................................................................................................................14

Comparison and use of two management accounting systems to solve financial

problems.............................................................................................................................14

References.............................................................................................................................17

Appendix..................................................................................................................................19

MANAGEMENT ACCOUNTING

Table of Contents

Task 1........................................................................................................................................2

Information booklet useful for understanding the concept of management

accounting system and management accounting report..............................................2

Task 2........................................................................................................................................9

Management accounting techniques...............................................................................9

Task 3......................................................................................................................................12

Evaluation of different planning tools and their application in budget preparation

and forecasting..................................................................................................................12

Task 4......................................................................................................................................14

Comparison and use of two management accounting systems to solve financial

problems.............................................................................................................................14

References.............................................................................................................................17

Appendix..................................................................................................................................19

2

MANAGEMENT ACCOUNTING

Task 1

Information booklet useful for understanding the concept of management

accounting system and management accounting report

The quantitative and qualitative information that is required for evaluating the

operational and financial performance is gathered from the managerial accounting

techniques. The managerial accounting is a sub division of the accounting system

which is used to make plans and strategy to control the usage of funds by the

managers. It supports in the decision making process by the application of budgeting

and after that it is used to control the budget by making comparison the budgeted

figures with the actual figures, and from the result of the difference between the

actual and the budgeted figures it can be possible to calculate the variances of the

budgeted and the decisions can be taken based on the outcome of such variances.

The managerial accounting techniques as a resource management tool give

emphasis on the estimation of the future and on the other hand as a technique for

controlling the resources it concentrates on the present situations.

Assisting the management to make improvements continuously

The management accounting helps the management to continuously monitor

the results of the budgets and that can help in continuous improvement of the

effectiveness of processes and systems and expand the superiority of the goods and

facilities provided by them. The improvement is to be made on continuous basis to

eliminate the adverse effect of abnormal waste of materials, time and efforts of the

labours, and increase the productivity (Otley 2016).

The management accounting is related with the methods of measurement,

identification, explanation, and communication of the financial data to the

management. The various management accounting system which is utilised by the

organizations are:

Inventory management system

MANAGEMENT ACCOUNTING

Task 1

Information booklet useful for understanding the concept of management

accounting system and management accounting report

The quantitative and qualitative information that is required for evaluating the

operational and financial performance is gathered from the managerial accounting

techniques. The managerial accounting is a sub division of the accounting system

which is used to make plans and strategy to control the usage of funds by the

managers. It supports in the decision making process by the application of budgeting

and after that it is used to control the budget by making comparison the budgeted

figures with the actual figures, and from the result of the difference between the

actual and the budgeted figures it can be possible to calculate the variances of the

budgeted and the decisions can be taken based on the outcome of such variances.

The managerial accounting techniques as a resource management tool give

emphasis on the estimation of the future and on the other hand as a technique for

controlling the resources it concentrates on the present situations.

Assisting the management to make improvements continuously

The management accounting helps the management to continuously monitor

the results of the budgets and that can help in continuous improvement of the

effectiveness of processes and systems and expand the superiority of the goods and

facilities provided by them. The improvement is to be made on continuous basis to

eliminate the adverse effect of abnormal waste of materials, time and efforts of the

labours, and increase the productivity (Otley 2016).

The management accounting is related with the methods of measurement,

identification, explanation, and communication of the financial data to the

management. The various management accounting system which is utilised by the

organizations are:

Inventory management system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

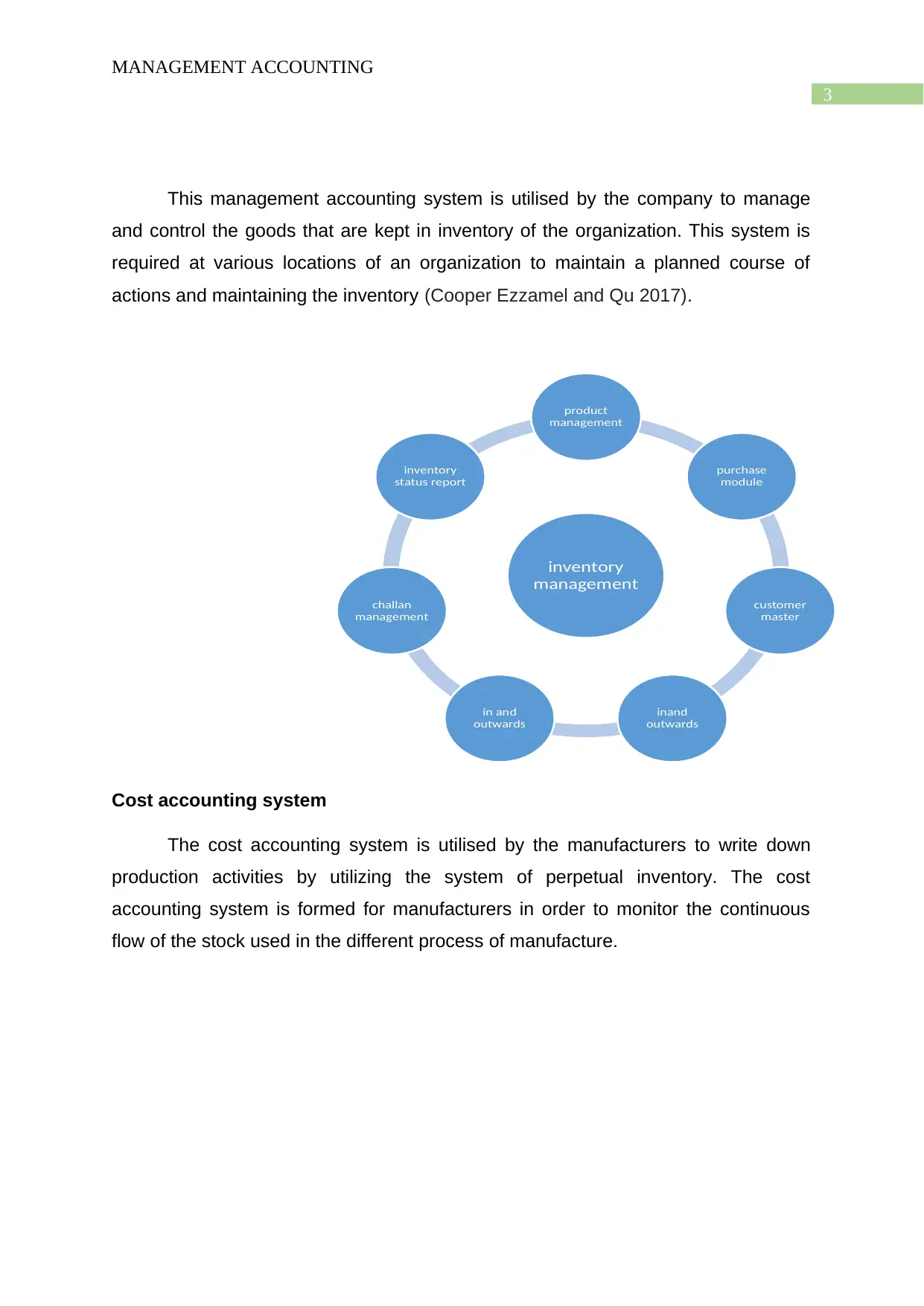

This management accounting system is utilised by the company to manage

and control the goods that are kept in inventory of the organization. This system is

required at various locations of an organization to maintain a planned course of

actions and maintaining the inventory (Cooper Ezzamel and Qu 2017).

Cost accounting system

The cost accounting system is utilised by the manufacturers to write down

production activities by utilizing the system of perpetual inventory. The cost

accounting system is formed for manufacturers in order to monitor the continuous

flow of the stock used in the different process of manufacture.

inventory

management

product

management

purchase

module

customer

master

inand

outwards

in and

outwards

challan

management

inventory

status report

MANAGEMENT ACCOUNTING

This management accounting system is utilised by the company to manage

and control the goods that are kept in inventory of the organization. This system is

required at various locations of an organization to maintain a planned course of

actions and maintaining the inventory (Cooper Ezzamel and Qu 2017).

Cost accounting system

The cost accounting system is utilised by the manufacturers to write down

production activities by utilizing the system of perpetual inventory. The cost

accounting system is formed for manufacturers in order to monitor the continuous

flow of the stock used in the different process of manufacture.

inventory

management

product

management

purchase

module

customer

master

inand

outwards

in and

outwards

challan

management

inventory

status report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

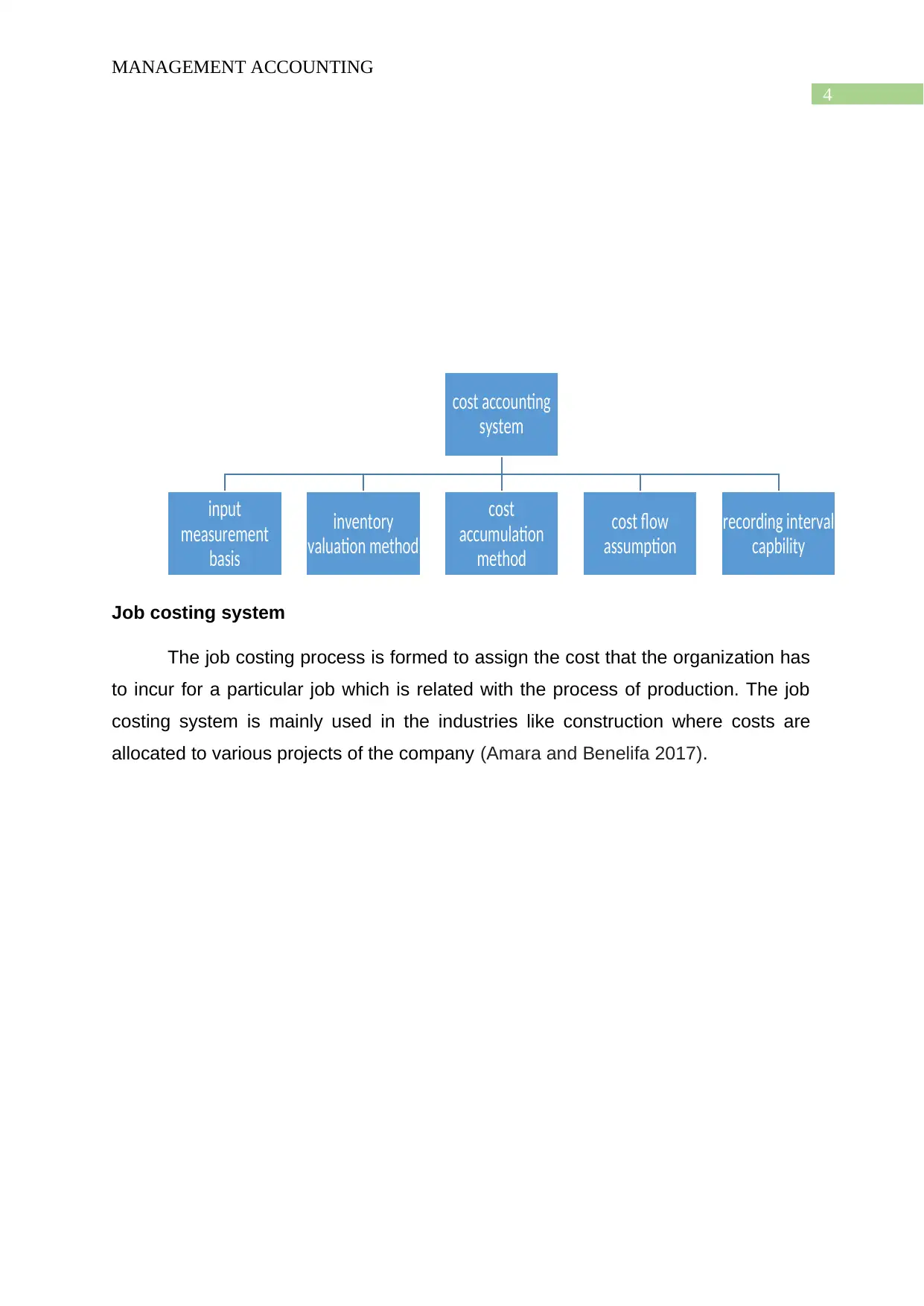

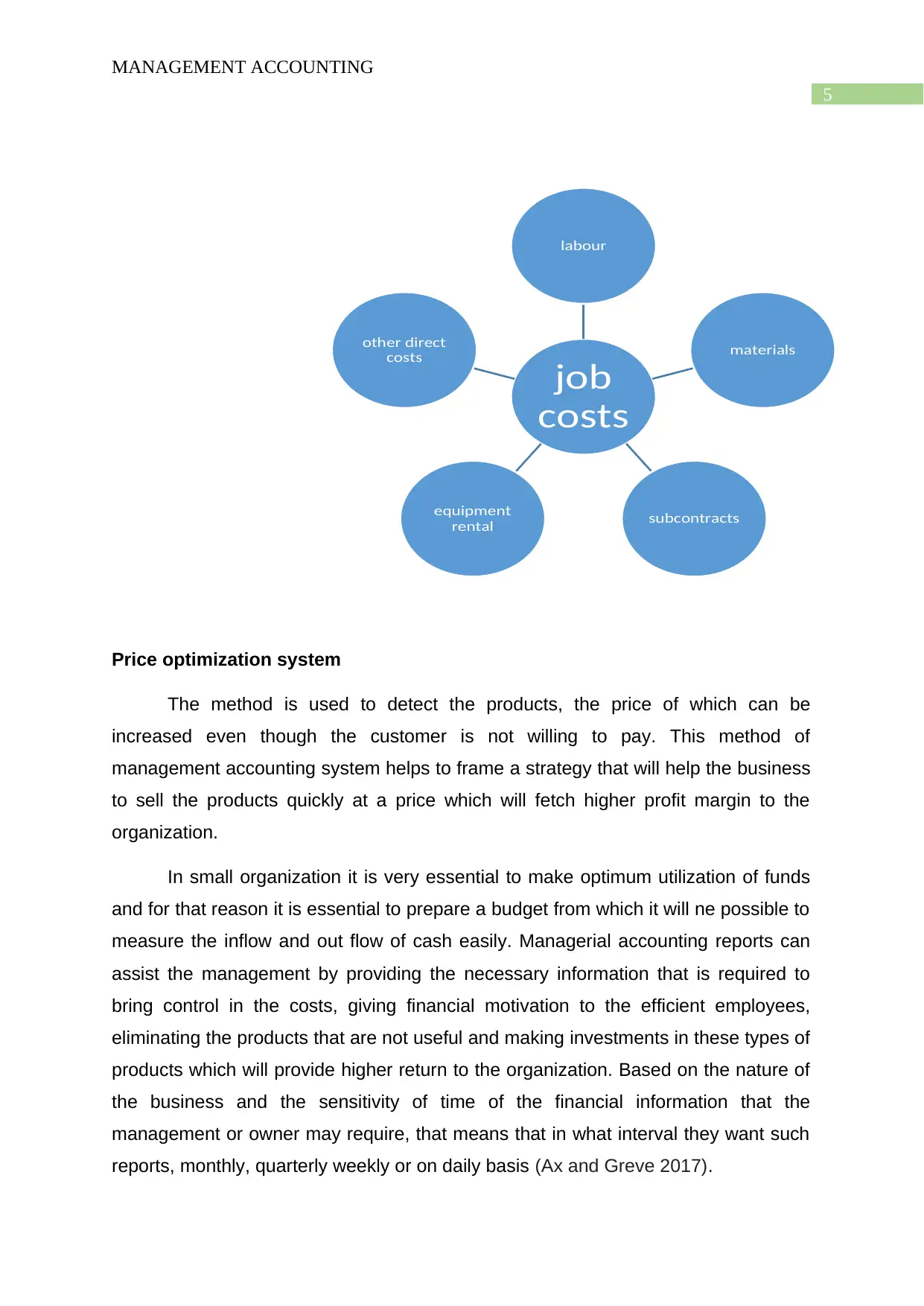

Job costing system

The job costing process is formed to assign the cost that the organization has

to incur for a particular job which is related with the process of production. The job

costing system is mainly used in the industries like construction where costs are

allocated to various projects of the company (Amara and Benelifa 2017).

cost accounting

system

input

measurement

basis

inventory

valuation method

cost

accumulation

method

cost flow

assumption

recording interval

capbility

MANAGEMENT ACCOUNTING

Job costing system

The job costing process is formed to assign the cost that the organization has

to incur for a particular job which is related with the process of production. The job

costing system is mainly used in the industries like construction where costs are

allocated to various projects of the company (Amara and Benelifa 2017).

cost accounting

system

input

measurement

basis

inventory

valuation method

cost

accumulation

method

cost flow

assumption

recording interval

capbility

5

MANAGEMENT ACCOUNTING

Price optimization system

The method is used to detect the products, the price of which can be

increased even though the customer is not willing to pay. This method of

management accounting system helps to frame a strategy that will help the business

to sell the products quickly at a price which will fetch higher profit margin to the

organization.

In small organization it is very essential to make optimum utilization of funds

and for that reason it is essential to prepare a budget from which it will ne possible to

measure the inflow and out flow of cash easily. Managerial accounting reports can

assist the management by providing the necessary information that is required to

bring control in the costs, giving financial motivation to the efficient employees,

eliminating the products that are not useful and making investments in these types of

products which will provide higher return to the organization. Based on the nature of

the business and the sensitivity of time of the financial information that the

management or owner may require, that means that in what interval they want such

reports, monthly, quarterly weekly or on daily basis (Ax and Greve 2017).

job

costs

labour

materials

subcontracts

equipment

rental

other direct

costs

MANAGEMENT ACCOUNTING

Price optimization system

The method is used to detect the products, the price of which can be

increased even though the customer is not willing to pay. This method of

management accounting system helps to frame a strategy that will help the business

to sell the products quickly at a price which will fetch higher profit margin to the

organization.

In small organization it is very essential to make optimum utilization of funds

and for that reason it is essential to prepare a budget from which it will ne possible to

measure the inflow and out flow of cash easily. Managerial accounting reports can

assist the management by providing the necessary information that is required to

bring control in the costs, giving financial motivation to the efficient employees,

eliminating the products that are not useful and making investments in these types of

products which will provide higher return to the organization. Based on the nature of

the business and the sensitivity of time of the financial information that the

management or owner may require, that means that in what interval they want such

reports, monthly, quarterly weekly or on daily basis (Ax and Greve 2017).

job

costs

labour

materials

subcontracts

equipment

rental

other direct

costs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

System produced quote

Quote recommendation

Optimised quote

Budget reports to monitor the performance of the business

This kind of reports provide assistance to small organizations to monitor the

output of the organization and bring control over the costs incurred for running the

operation of the business. The budget is made to make an estimation of the cost of

production of the coming days on the basis of the trend of the actual expenses made

in the past years. In case the organization in the previous year exceeded the

budgeted figure and fail to bring control over the increasing trend of costs then it may

be required to increase the fund to a more correct level (Nitzl 2016).

The budget reports may be utilised by the entrepreneurs to calculate the

inducements that is to be paid to the efficient employees. The budgeted funds are

given out as bonus to the employees as they have been able to achieve the goal

with an amount which is less than the budgeted amount.

Budget allocation

Client request code

Rule 1

Rule 2

Rule 3

MANAGEMENT ACCOUNTING

System produced quote

Quote recommendation

Optimised quote

Budget reports to monitor the performance of the business

This kind of reports provide assistance to small organizations to monitor the

output of the organization and bring control over the costs incurred for running the

operation of the business. The budget is made to make an estimation of the cost of

production of the coming days on the basis of the trend of the actual expenses made

in the past years. In case the organization in the previous year exceeded the

budgeted figure and fail to bring control over the increasing trend of costs then it may

be required to increase the fund to a more correct level (Nitzl 2016).

The budget reports may be utilised by the entrepreneurs to calculate the

inducements that is to be paid to the efficient employees. The budgeted funds are

given out as bonus to the employees as they have been able to achieve the goal

with an amount which is less than the budgeted amount.

Budget allocation

Client request code

Rule 1

Rule 2

Rule 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

Receivable aging reports

The aging report is an important tool used by the management to control the

flow of cash in case the organization want to extend the period of credit that is

allowed to the customers. This report helps to categories the customers in

accordance to the period of credit allowed by them. In general, the aging reports

consists of separate columns in the bills, under three categories 30 days late, late for

60 days and the late for 90 days. The ageing report can be used by the managers to

identify the competence of the collection process of the firm.

There are many customers which are not capable to reimburse their balances,

then in that case the organizations may need to bring more control on the credit

policy. On analysing the accounts receivable balances on a periodic basis will help

the management from neglecting any debts that has not been paid by the customers

(Hopper and Bui 2016).

adminstrative costs

directs cost

overhead

MANAGEMENT ACCOUNTING

Receivable aging reports

The aging report is an important tool used by the management to control the

flow of cash in case the organization want to extend the period of credit that is

allowed to the customers. This report helps to categories the customers in

accordance to the period of credit allowed by them. In general, the aging reports

consists of separate columns in the bills, under three categories 30 days late, late for

60 days and the late for 90 days. The ageing report can be used by the managers to

identify the competence of the collection process of the firm.

There are many customers which are not capable to reimburse their balances,

then in that case the organizations may need to bring more control on the credit

policy. On analysing the accounts receivable balances on a periodic basis will help

the management from neglecting any debts that has not been paid by the customers

(Hopper and Bui 2016).

adminstrative costs

directs cost

overhead

8

MANAGEMENT ACCOUNTING

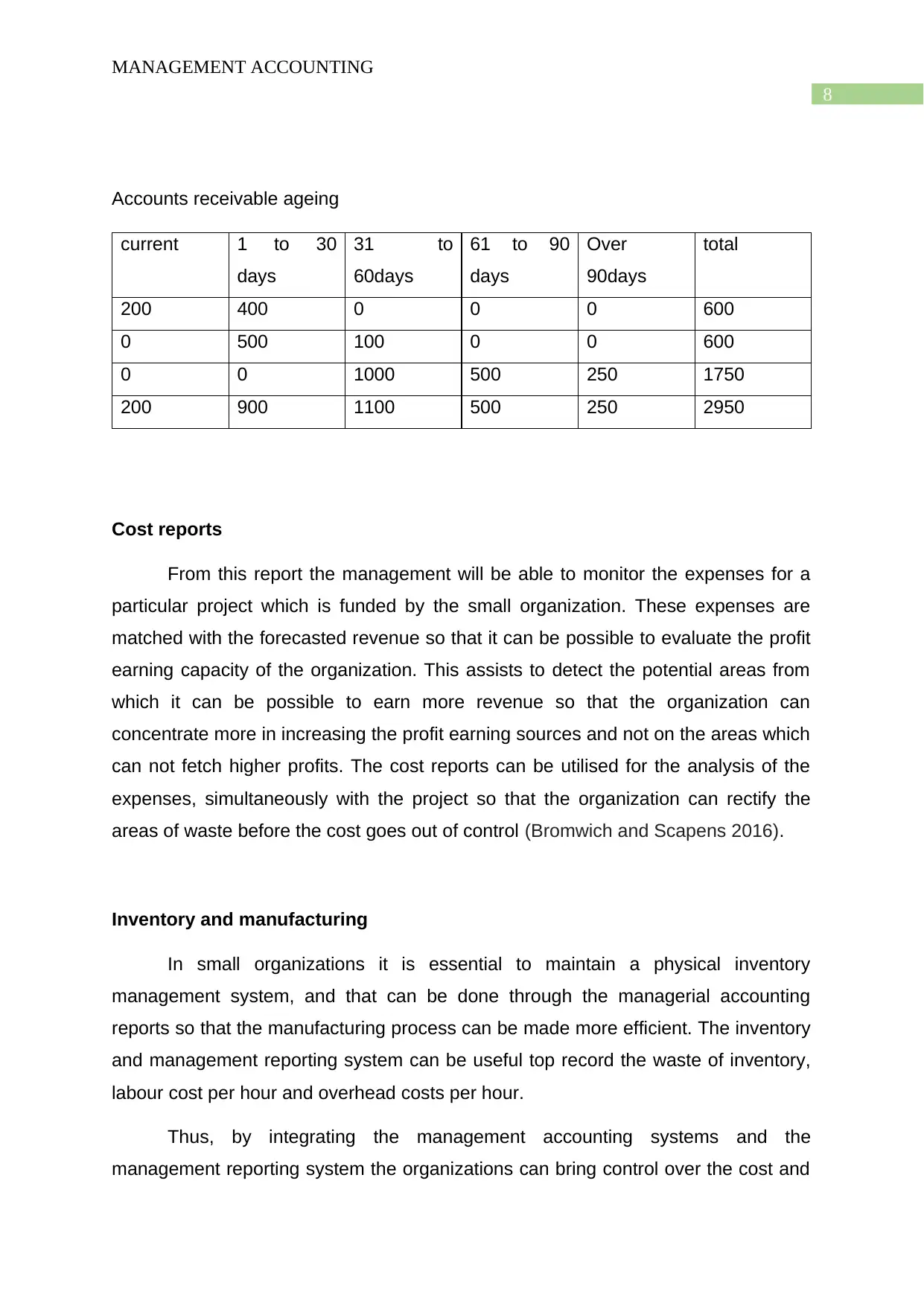

Accounts receivable ageing

current 1 to 30

days

31 to

60days

61 to 90

days

Over

90days

total

200 400 0 0 0 600

0 500 100 0 0 600

0 0 1000 500 250 1750

200 900 1100 500 250 2950

Cost reports

From this report the management will be able to monitor the expenses for a

particular project which is funded by the small organization. These expenses are

matched with the forecasted revenue so that it can be possible to evaluate the profit

earning capacity of the organization. This assists to detect the potential areas from

which it can be possible to earn more revenue so that the organization can

concentrate more in increasing the profit earning sources and not on the areas which

can not fetch higher profits. The cost reports can be utilised for the analysis of the

expenses, simultaneously with the project so that the organization can rectify the

areas of waste before the cost goes out of control (Bromwich and Scapens 2016).

Inventory and manufacturing

In small organizations it is essential to maintain a physical inventory

management system, and that can be done through the managerial accounting

reports so that the manufacturing process can be made more efficient. The inventory

and management reporting system can be useful top record the waste of inventory,

labour cost per hour and overhead costs per hour.

Thus, by integrating the management accounting systems and the

management reporting system the organizations can bring control over the cost and

MANAGEMENT ACCOUNTING

Accounts receivable ageing

current 1 to 30

days

31 to

60days

61 to 90

days

Over

90days

total

200 400 0 0 0 600

0 500 100 0 0 600

0 0 1000 500 250 1750

200 900 1100 500 250 2950

Cost reports

From this report the management will be able to monitor the expenses for a

particular project which is funded by the small organization. These expenses are

matched with the forecasted revenue so that it can be possible to evaluate the profit

earning capacity of the organization. This assists to detect the potential areas from

which it can be possible to earn more revenue so that the organization can

concentrate more in increasing the profit earning sources and not on the areas which

can not fetch higher profits. The cost reports can be utilised for the analysis of the

expenses, simultaneously with the project so that the organization can rectify the

areas of waste before the cost goes out of control (Bromwich and Scapens 2016).

Inventory and manufacturing

In small organizations it is essential to maintain a physical inventory

management system, and that can be done through the managerial accounting

reports so that the manufacturing process can be made more efficient. The inventory

and management reporting system can be useful top record the waste of inventory,

labour cost per hour and overhead costs per hour.

Thus, by integrating the management accounting systems and the

management reporting system the organizations can bring control over the cost and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

can increase the profit margin and bring more efficiency in the production process

(Wen and Mao 2019).

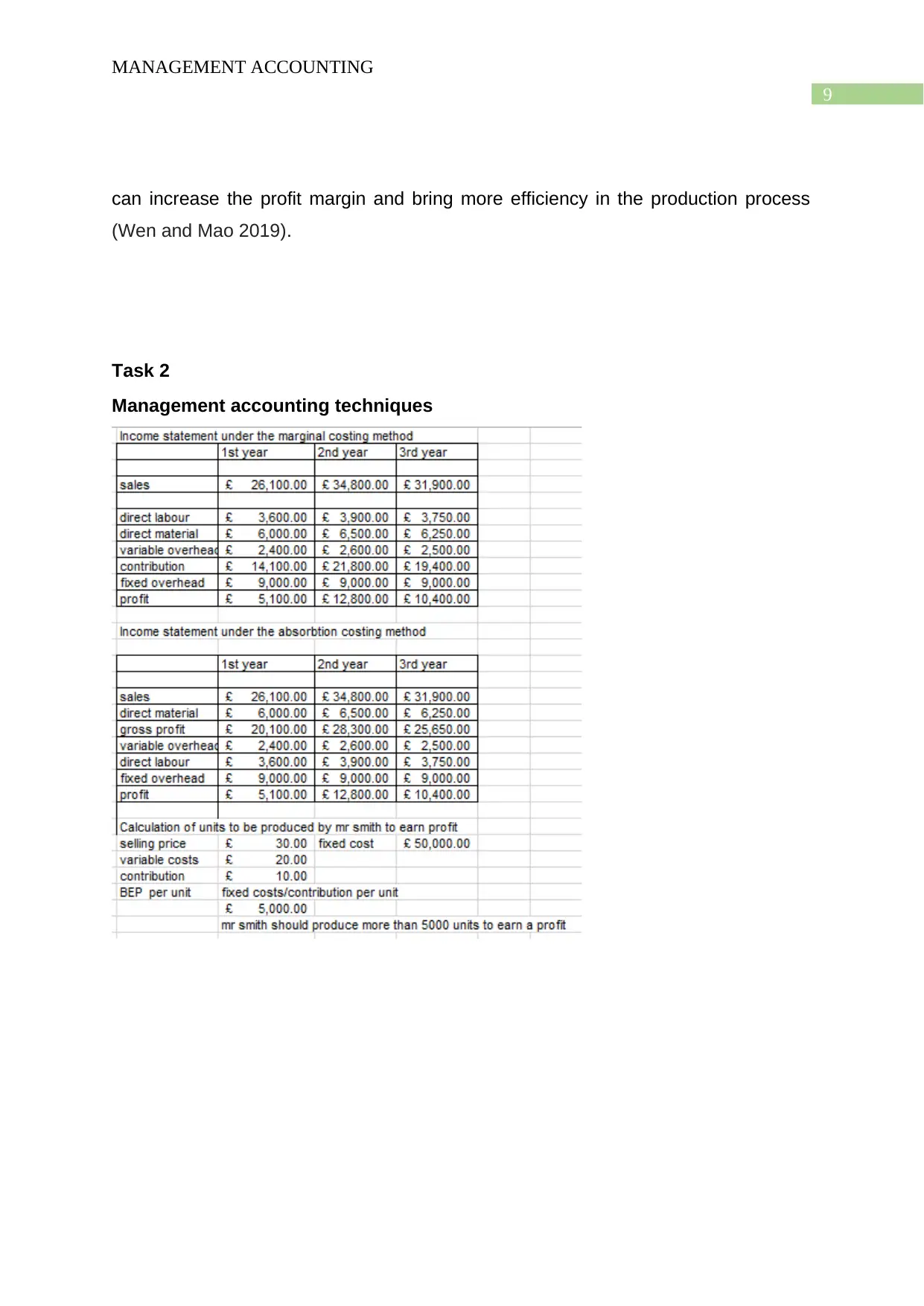

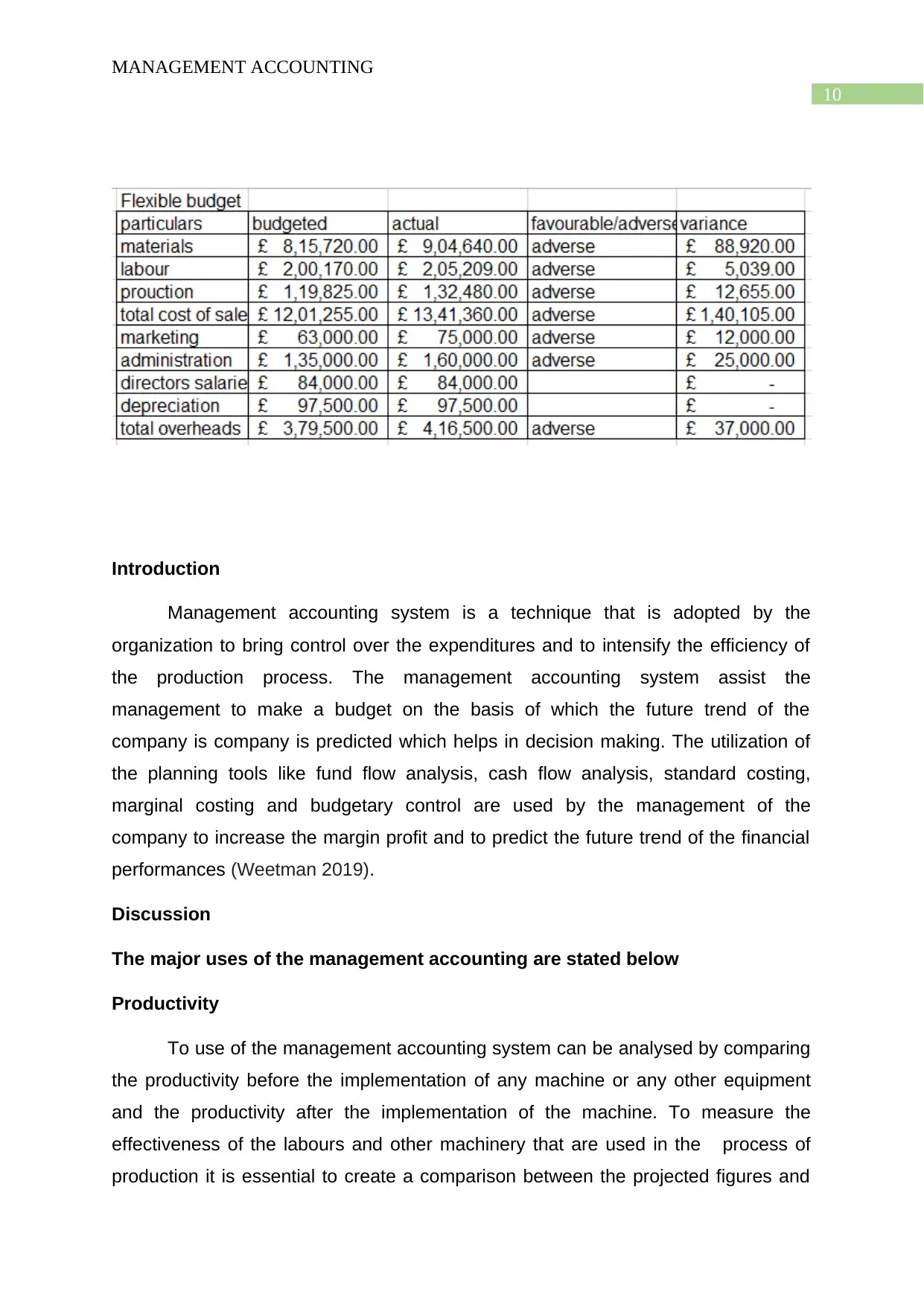

Task 2

Management accounting techniques

MANAGEMENT ACCOUNTING

can increase the profit margin and bring more efficiency in the production process

(Wen and Mao 2019).

Task 2

Management accounting techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

Introduction

Management accounting system is a technique that is adopted by the

organization to bring control over the expenditures and to intensify the efficiency of

the production process. The management accounting system assist the

management to make a budget on the basis of which the future trend of the

company is company is predicted which helps in decision making. The utilization of

the planning tools like fund flow analysis, cash flow analysis, standard costing,

marginal costing and budgetary control are used by the management of the

company to increase the margin profit and to predict the future trend of the financial

performances (Weetman 2019).

Discussion

The major uses of the management accounting are stated below

Productivity

To use of the management accounting system can be analysed by comparing

the productivity before the implementation of any machine or any other equipment

and the productivity after the implementation of the machine. To measure the

effectiveness of the labours and other machinery that are used in the process of

production it is essential to create a comparison between the projected figures and

MANAGEMENT ACCOUNTING

Introduction

Management accounting system is a technique that is adopted by the

organization to bring control over the expenditures and to intensify the efficiency of

the production process. The management accounting system assist the

management to make a budget on the basis of which the future trend of the

company is company is predicted which helps in decision making. The utilization of

the planning tools like fund flow analysis, cash flow analysis, standard costing,

marginal costing and budgetary control are used by the management of the

company to increase the margin profit and to predict the future trend of the financial

performances (Weetman 2019).

Discussion

The major uses of the management accounting are stated below

Productivity

To use of the management accounting system can be analysed by comparing

the productivity before the implementation of any machine or any other equipment

and the productivity after the implementation of the machine. To measure the

effectiveness of the labours and other machinery that are used in the process of

production it is essential to create a comparison between the projected figures and

11

MANAGEMENT ACCOUNTING

the real one. If the actual production is more than the estimated one then it can be

said that the process of production is efficient and that can assist the management to

fulfil the objective of the organization (Dearman Lechner and Shanklin 2018).

Sales trends

The tools for planning of the management accounting also used to predict the

trend of the sales and take necessary actions as per the requirement to implement

any strategy to improve the sales figures as set by the organization. The

management accounting tool is also used to assess that which products are capable

to bring more revenue. The analysis can also help to identify the nature of the

products and also toe assess the present market demand of the products and if the

demand is falling then what necessary changes are to be implemented so that it can

be possible to capture more market and attract more customers. The information that

can be gathered from management accounting will help the organizations to identify

the target market and to set the amount of units that is essential to sale to increase

the margin of profit (Jin 2017).

Financial planning

Management accounting can also used as a financial planning tool as it helps

to deliver data concerning the management of the expenditures, which includes the

process of making plan based on the fund available and how much funds the

organization can raise in the future, the organization can prepare a strategic plan

regarding the time when it may be required to take loan from the market and when to

go for long term investments. Financial planning can help the organization to

manage its working capital requirement and can save from the payment of

unnecessary penalties or late fees (Taylor and Scapens 2016).

Thus management accounting provide the necessary information from which

it can be possible for the management to identify the areas which are providing

revenue and help o improve the financial condition of the company and also

simultaneously help to detect the areas where more improvements will be required

so that the organization can increase its financial strength.

MANAGEMENT ACCOUNTING

the real one. If the actual production is more than the estimated one then it can be

said that the process of production is efficient and that can assist the management to

fulfil the objective of the organization (Dearman Lechner and Shanklin 2018).

Sales trends

The tools for planning of the management accounting also used to predict the

trend of the sales and take necessary actions as per the requirement to implement

any strategy to improve the sales figures as set by the organization. The

management accounting tool is also used to assess that which products are capable

to bring more revenue. The analysis can also help to identify the nature of the

products and also toe assess the present market demand of the products and if the

demand is falling then what necessary changes are to be implemented so that it can

be possible to capture more market and attract more customers. The information that

can be gathered from management accounting will help the organizations to identify

the target market and to set the amount of units that is essential to sale to increase

the margin of profit (Jin 2017).

Financial planning

Management accounting can also used as a financial planning tool as it helps

to deliver data concerning the management of the expenditures, which includes the

process of making plan based on the fund available and how much funds the

organization can raise in the future, the organization can prepare a strategic plan

regarding the time when it may be required to take loan from the market and when to

go for long term investments. Financial planning can help the organization to

manage its working capital requirement and can save from the payment of

unnecessary penalties or late fees (Taylor and Scapens 2016).

Thus management accounting provide the necessary information from which

it can be possible for the management to identify the areas which are providing

revenue and help o improve the financial condition of the company and also

simultaneously help to detect the areas where more improvements will be required

so that the organization can increase its financial strength.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.