Financial Management Assignment: BUACC3701, Semester 2, 2018 Analysis

VerifiedAdded on 2023/06/05

|14

|2374

|120

Report

AI Summary

This report presents a comprehensive analysis of a financial management assignment, covering key concepts such as capital structure, flotation costs, and the Capital Asset Pricing Model (CAPM) to determine the cost of equity. The report calculates the weighted average cost of capital (WACC) under different financing scenarios, including debt, preference shares, and equity, and evaluates the impact of these choices. It also explores breakeven points and the effects of funding options on Earnings Per Share (EPS). Furthermore, the report delves into investment decisions, analyzing projects based on Internal Rate of Return (IRR) and marginal investment principles, and addresses behavioral finance concepts like representativeness and probability matching through case studies, providing a complete overview of financial decision-making processes.

BUACC3701 FINANCIAL

MANAGEMENT

ASSIGNMENT

SEMESTER 2, 2018

MANAGEMENT

ASSIGNMENT

SEMESTER 2, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

1..............................................................................................................................................3

2..............................................................................................................................................3

3..............................................................................................................................................3

4..............................................................................................................................................3

5..............................................................................................................................................3

6..............................................................................................................................................3

7..............................................................................................................................................3

8..............................................................................................................................................3

9..............................................................................................................................................3

10............................................................................................................................................3

11............................................................................................................................................3

12............................................................................................................................................3

13............................................................................................................................................3

Question 2..................................................................................................................................4

(i)............................................................................................................................................4

Part A.................................................................................................................................4

Part B..................................................................................................................................4

(ii)...........................................................................................................................................4

Part A.................................................................................................................................4

Part B..................................................................................................................................4

Part C..................................................................................................................................4

Question 3..................................................................................................................................5

Part B......................................................................................................................................5

Part D.....................................................................................................................................5

Question 1..................................................................................................................................3

1..............................................................................................................................................3

2..............................................................................................................................................3

3..............................................................................................................................................3

4..............................................................................................................................................3

5..............................................................................................................................................3

6..............................................................................................................................................3

7..............................................................................................................................................3

8..............................................................................................................................................3

9..............................................................................................................................................3

10............................................................................................................................................3

11............................................................................................................................................3

12............................................................................................................................................3

13............................................................................................................................................3

Question 2..................................................................................................................................4

(i)............................................................................................................................................4

Part A.................................................................................................................................4

Part B..................................................................................................................................4

(ii)...........................................................................................................................................4

Part A.................................................................................................................................4

Part B..................................................................................................................................4

Part C..................................................................................................................................4

Question 3..................................................................................................................................5

Part B......................................................................................................................................5

Part D.....................................................................................................................................5

Part E......................................................................................................................................5

References..................................................................................................................................6

References..................................................................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

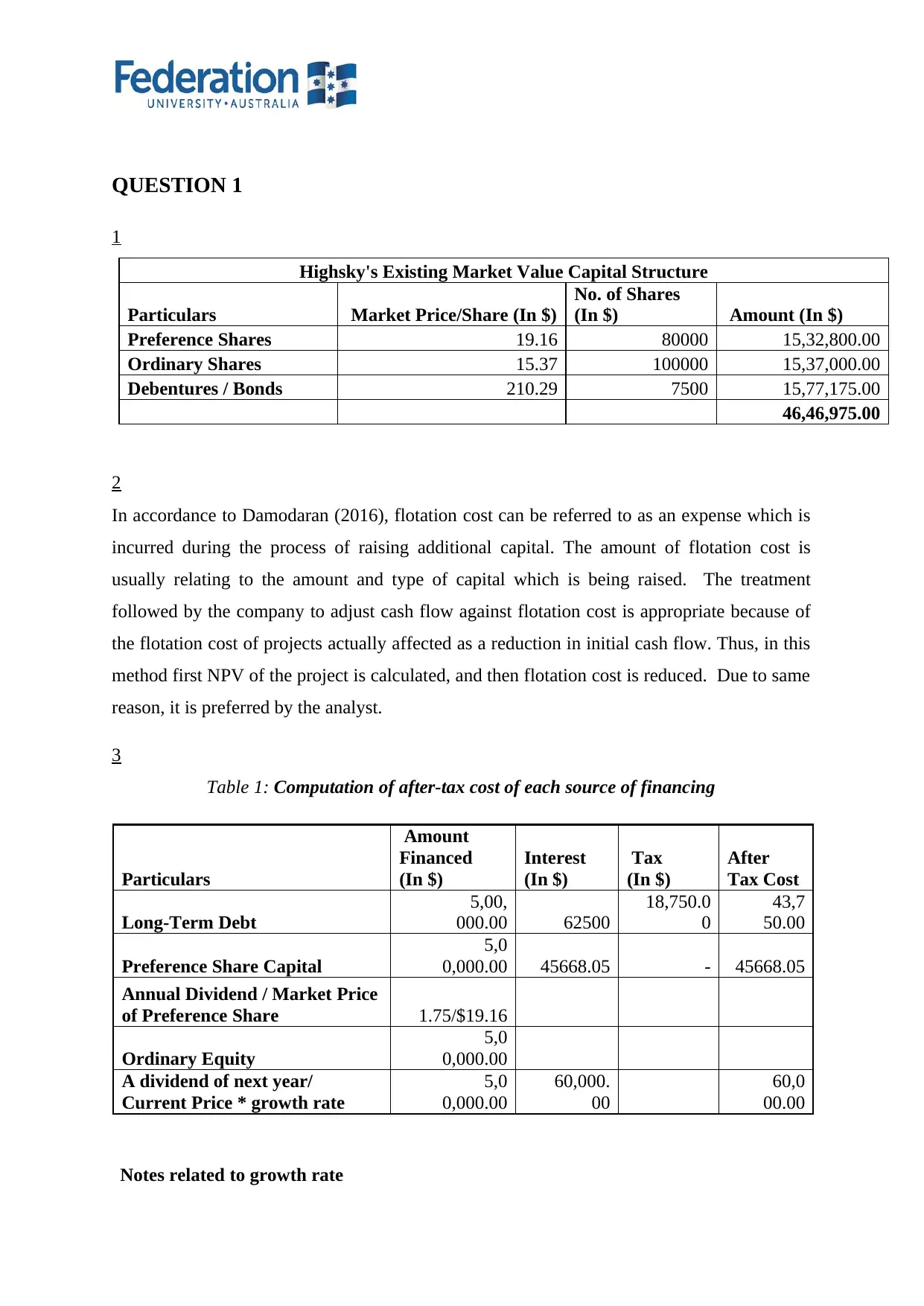

1

Highsky's Existing Market Value Capital Structure

Particulars Market Price/Share (In $)

No. of Shares

(In $) Amount (In $)

Preference Shares 19.16 80000 15,32,800.00

Ordinary Shares 15.37 100000 15,37,000.00

Debentures / Bonds 210.29 7500 15,77,175.00

46,46,975.00

2

In accordance to Damodaran (2016), flotation cost can be referred to as an expense which is

incurred during the process of raising additional capital. The amount of flotation cost is

usually relating to the amount and type of capital which is being raised. The treatment

followed by the company to adjust cash flow against flotation cost is appropriate because of

the flotation cost of projects actually affected as a reduction in initial cash flow. Thus, in this

method first NPV of the project is calculated, and then flotation cost is reduced. Due to same

reason, it is preferred by the analyst.

3

Table 1: Computation of after-tax cost of each source of financing

Particulars

Amount

Financed

(In $)

Interest

(In $)

Tax

(In $)

After

Tax Cost

Long-Term Debt

5,00,

000.00 62500

18,750.0

0

43,7

50.00

Preference Share Capital

5,0

0,000.00 45668.05 - 45668.05

Annual Dividend / Market Price

of Preference Share 1.75/$19.16

Ordinary Equity

5,0

0,000.00

A dividend of next year/

Current Price * growth rate

5,0

0,000.00

60,000.

00

60,0

00.00

Notes related to growth rate

1

Highsky's Existing Market Value Capital Structure

Particulars Market Price/Share (In $)

No. of Shares

(In $) Amount (In $)

Preference Shares 19.16 80000 15,32,800.00

Ordinary Shares 15.37 100000 15,37,000.00

Debentures / Bonds 210.29 7500 15,77,175.00

46,46,975.00

2

In accordance to Damodaran (2016), flotation cost can be referred to as an expense which is

incurred during the process of raising additional capital. The amount of flotation cost is

usually relating to the amount and type of capital which is being raised. The treatment

followed by the company to adjust cash flow against flotation cost is appropriate because of

the flotation cost of projects actually affected as a reduction in initial cash flow. Thus, in this

method first NPV of the project is calculated, and then flotation cost is reduced. Due to same

reason, it is preferred by the analyst.

3

Table 1: Computation of after-tax cost of each source of financing

Particulars

Amount

Financed

(In $)

Interest

(In $)

Tax

(In $)

After

Tax Cost

Long-Term Debt

5,00,

000.00 62500

18,750.0

0

43,7

50.00

Preference Share Capital

5,0

0,000.00 45668.05 - 45668.05

Annual Dividend / Market Price

of Preference Share 1.75/$19.16

Ordinary Equity

5,0

0,000.00

A dividend of next year/

Current Price * growth rate

5,0

0,000.00

60,000.

00

60,0

00.00

Notes related to growth rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

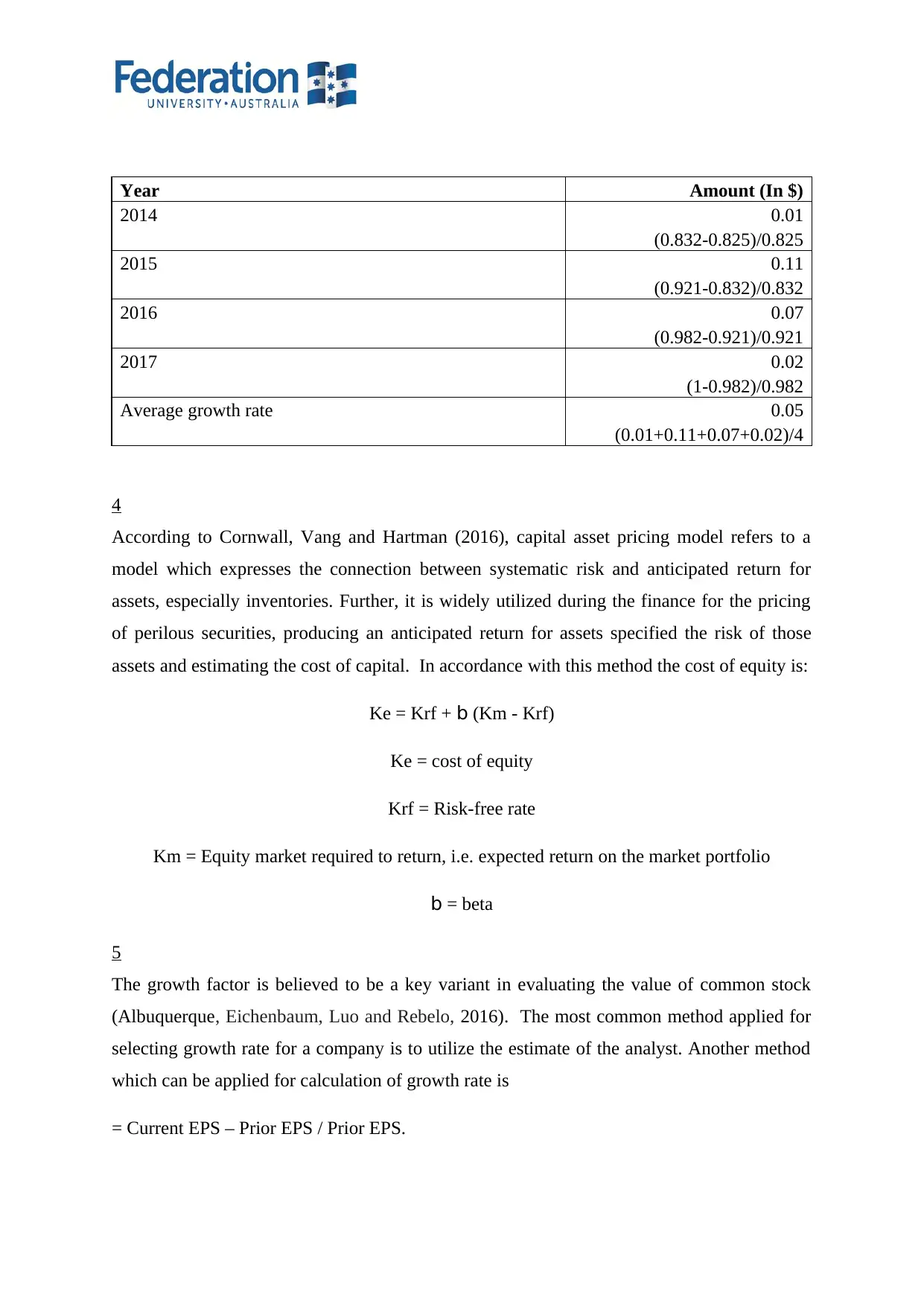

Year Amount (In $)

2014 0.01

(0.832-0.825)/0.825

2015 0.11

(0.921-0.832)/0.832

2016 0.07

(0.982-0.921)/0.921

2017 0.02

(1-0.982)/0.982

Average growth rate 0.05

(0.01+0.11+0.07+0.02)/4

4

According to Cornwall, Vang and Hartman (2016), capital asset pricing model refers to a

model which expresses the connection between systematic risk and anticipated return for

assets, especially inventories. Further, it is widely utilized during the finance for the pricing

of perilous securities, producing an anticipated return for assets specified the risk of those

assets and estimating the cost of capital. In accordance with this method the cost of equity is:

Ke = Krf + b (Km - Krf)

Ke = cost of equity

Krf = Risk-free rate

Km = Equity market required to return, i.e. expected return on the market portfolio

b = beta

5

The growth factor is believed to be a key variant in evaluating the value of common stock

(Albuquerque, Eichenbaum, Luo and Rebelo, 2016). The most common method applied for

selecting growth rate for a company is to utilize the estimate of the analyst. Another method

which can be applied for calculation of growth rate is

= Current EPS – Prior EPS / Prior EPS.

2014 0.01

(0.832-0.825)/0.825

2015 0.11

(0.921-0.832)/0.832

2016 0.07

(0.982-0.921)/0.921

2017 0.02

(1-0.982)/0.982

Average growth rate 0.05

(0.01+0.11+0.07+0.02)/4

4

According to Cornwall, Vang and Hartman (2016), capital asset pricing model refers to a

model which expresses the connection between systematic risk and anticipated return for

assets, especially inventories. Further, it is widely utilized during the finance for the pricing

of perilous securities, producing an anticipated return for assets specified the risk of those

assets and estimating the cost of capital. In accordance with this method the cost of equity is:

Ke = Krf + b (Km - Krf)

Ke = cost of equity

Krf = Risk-free rate

Km = Equity market required to return, i.e. expected return on the market portfolio

b = beta

5

The growth factor is believed to be a key variant in evaluating the value of common stock

(Albuquerque, Eichenbaum, Luo and Rebelo, 2016). The most common method applied for

selecting growth rate for a company is to utilize the estimate of the analyst. Another method

which can be applied for calculation of growth rate is

= Current EPS – Prior EPS / Prior EPS.

In order to apply this method in a case when data of more than two years are available than

taking growth in earning from the first year to last year and then divide same with no. of

years. Every method has its own limitation thus in the present method is wide fluctuation in

annual EPS, and the impact of compounding effect of the growth rate of EPS is not

considered while calculating growth rate.

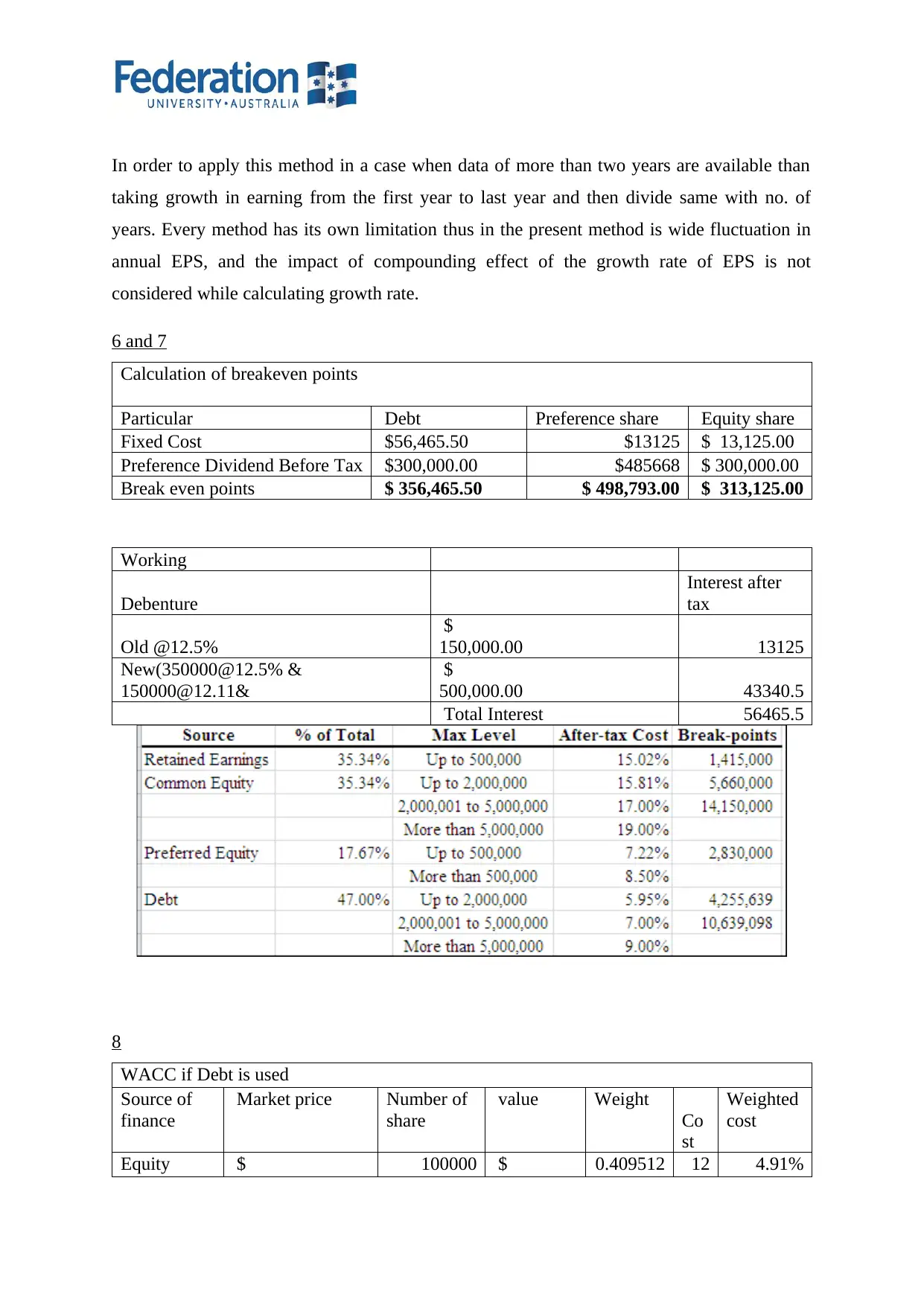

6 and 7

Calculation of breakeven points

Particular Debt Preference share Equity share

Fixed Cost $56,465.50 $13125 $ 13,125.00

Preference Dividend Before Tax $300,000.00 $485668 $ 300,000.00

Break even points $ 356,465.50 $ 498,793.00 $ 313,125.00

Working

Debenture

Interest after

tax

Old @12.5%

$

150,000.00 13125

New(350000@12.5% &

150000@12.11&

$

500,000.00 43340.5

Total Interest 56465.5

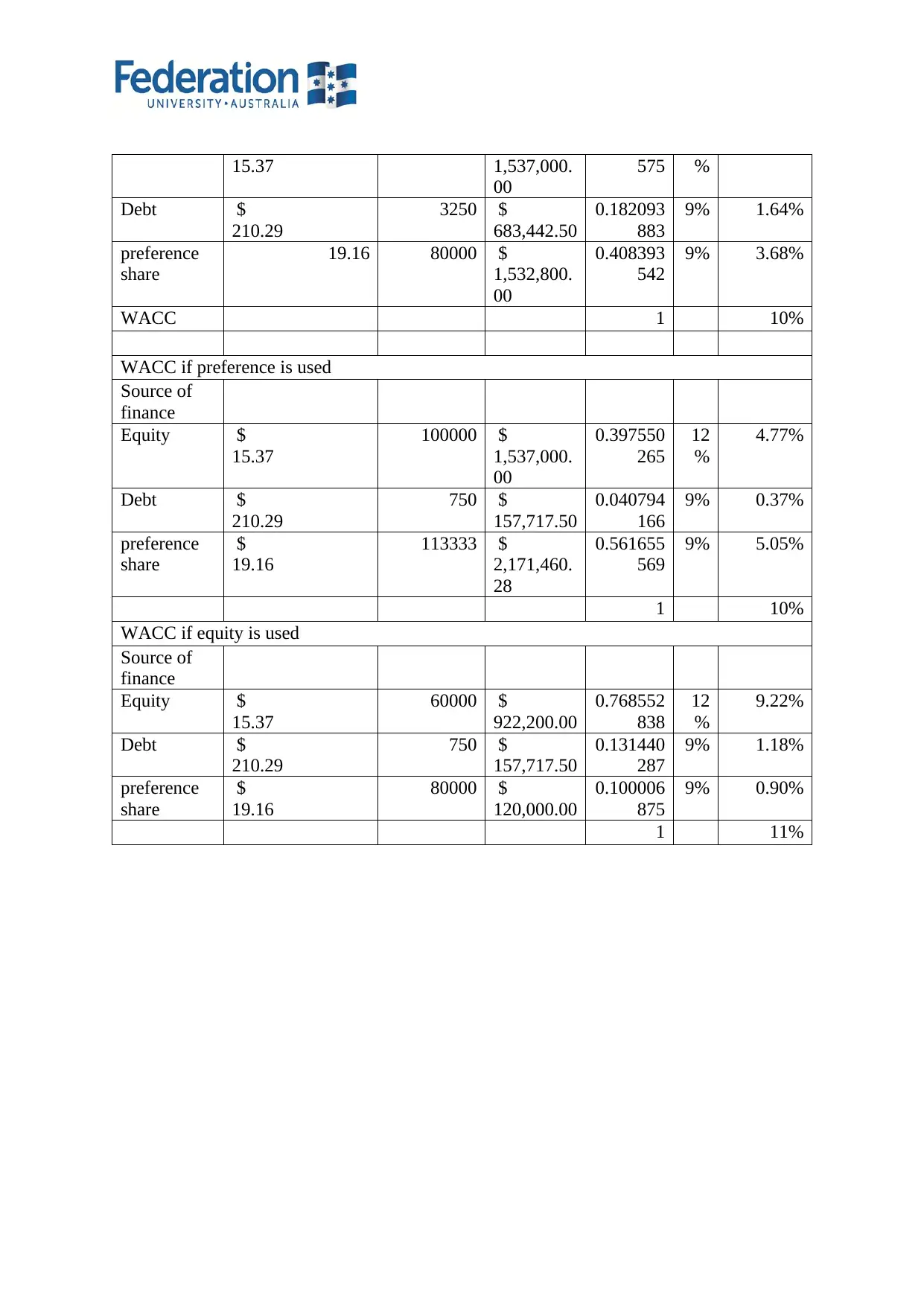

8

WACC if Debt is used

Source of

finance

Market price Number of

share

value Weight

Co

st

Weighted

cost

Equity $ 100000 $ 0.409512 12 4.91%

taking growth in earning from the first year to last year and then divide same with no. of

years. Every method has its own limitation thus in the present method is wide fluctuation in

annual EPS, and the impact of compounding effect of the growth rate of EPS is not

considered while calculating growth rate.

6 and 7

Calculation of breakeven points

Particular Debt Preference share Equity share

Fixed Cost $56,465.50 $13125 $ 13,125.00

Preference Dividend Before Tax $300,000.00 $485668 $ 300,000.00

Break even points $ 356,465.50 $ 498,793.00 $ 313,125.00

Working

Debenture

Interest after

tax

Old @12.5%

$

150,000.00 13125

New(350000@12.5% &

150000@12.11&

$

500,000.00 43340.5

Total Interest 56465.5

8

WACC if Debt is used

Source of

finance

Market price Number of

share

value Weight

Co

st

Weighted

cost

Equity $ 100000 $ 0.409512 12 4.91%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15.37 1,537,000.

00

575 %

Debt $

210.29

3250 $

683,442.50

0.182093

883

9% 1.64%

preference

share

19.16 80000 $

1,532,800.

00

0.408393

542

9% 3.68%

WACC 1 10%

WACC if preference is used

Source of

finance

Equity $

15.37

100000 $

1,537,000.

00

0.397550

265

12

%

4.77%

Debt $

210.29

750 $

157,717.50

0.040794

166

9% 0.37%

preference

share

$

19.16

113333 $

2,171,460.

28

0.561655

569

9% 5.05%

1 10%

WACC if equity is used

Source of

finance

Equity $

15.37

60000 $

922,200.00

0.768552

838

12

%

9.22%

Debt $

210.29

750 $

157,717.50

0.131440

287

9% 1.18%

preference

share

$

19.16

80000 $

120,000.00

0.100006

875

9% 0.90%

1 11%

00

575 %

Debt $

210.29

3250 $

683,442.50

0.182093

883

9% 1.64%

preference

share

19.16 80000 $

1,532,800.

00

0.408393

542

9% 3.68%

WACC 1 10%

WACC if preference is used

Source of

finance

Equity $

15.37

100000 $

1,537,000.

00

0.397550

265

12

%

4.77%

Debt $

210.29

750 $

157,717.50

0.040794

166

9% 0.37%

preference

share

$

19.16

113333 $

2,171,460.

28

0.561655

569

9% 5.05%

1 10%

WACC if equity is used

Source of

finance

Equity $

15.37

60000 $

922,200.00

0.768552

838

12

%

9.22%

Debt $

210.29

750 $

157,717.50

0.131440

287

9% 1.18%

preference

share

$

19.16

80000 $

120,000.00

0.100006

875

9% 0.90%

1 11%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

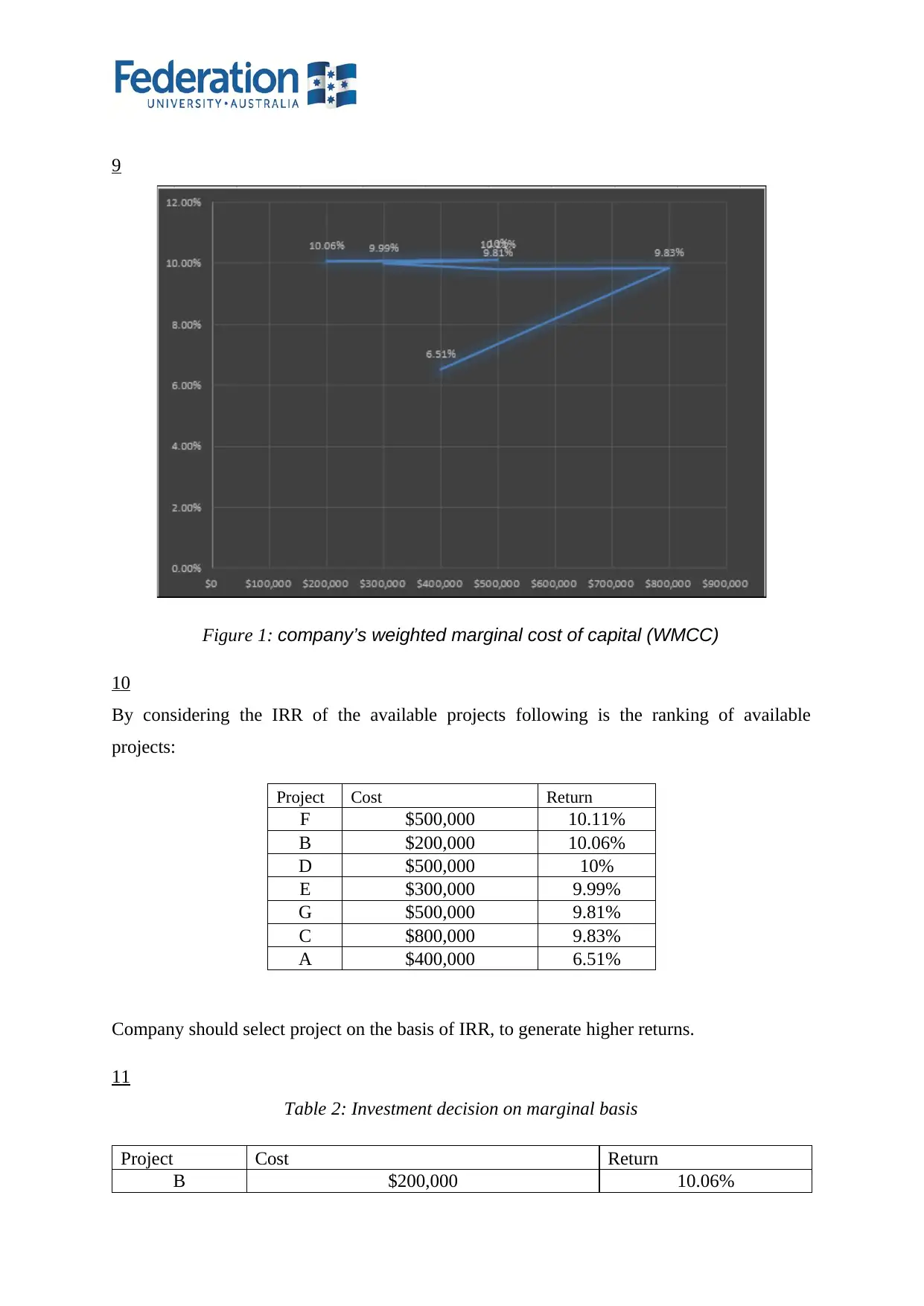

9

Figure 1: company’s weighted marginal cost of capital (WMCC)

10

By considering the IRR of the available projects following is the ranking of available

projects:

Project Cost Return

F $500,000 10.11%

B $200,000 10.06%

D $500,000 10%

E $300,000 9.99%

G $500,000 9.81%

C $800,000 9.83%

A $400,000 6.51%

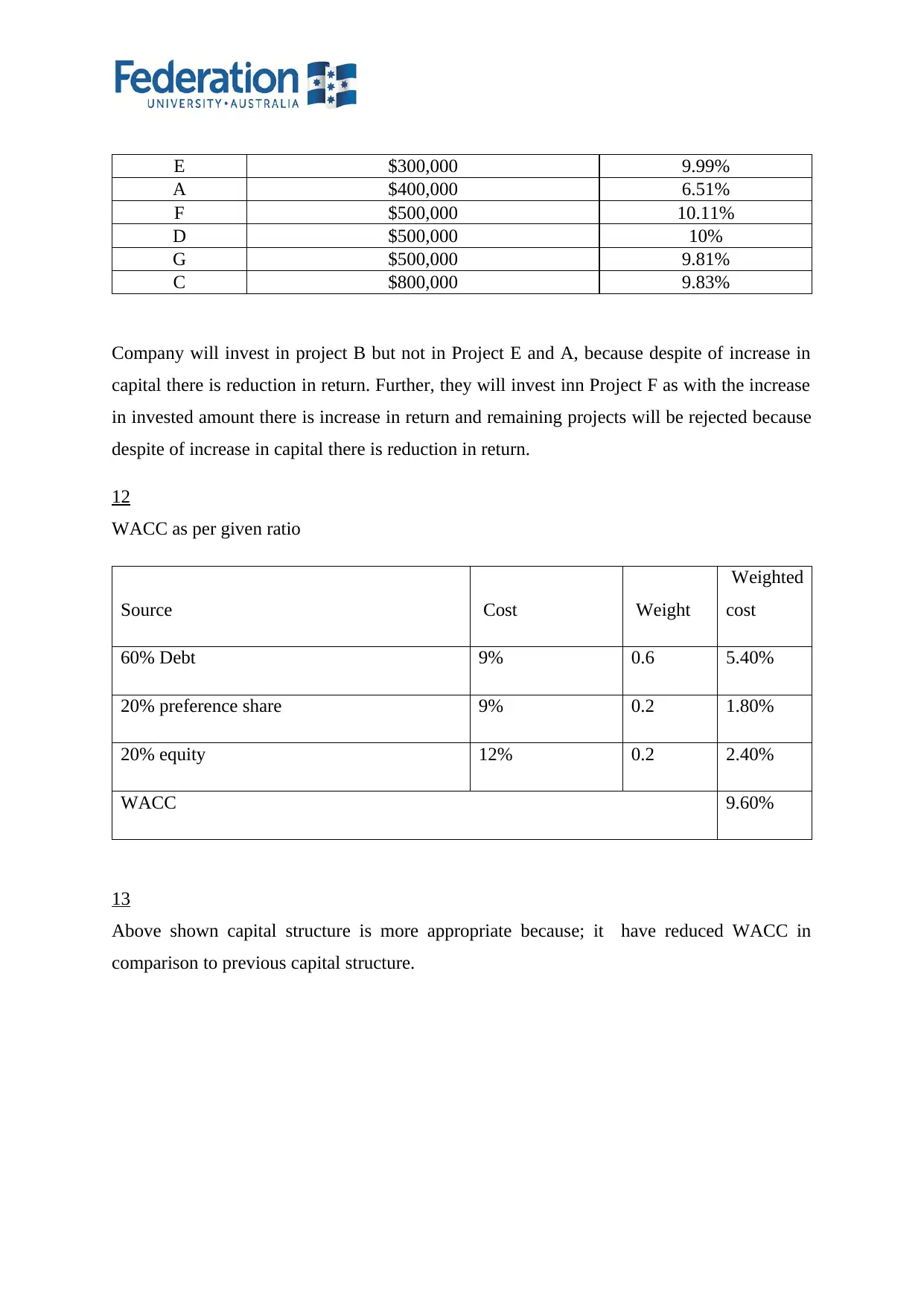

Company should select project on the basis of IRR, to generate higher returns.

11

Table 2: Investment decision on marginal basis

Project Cost Return

B $200,000 10.06%

Figure 1: company’s weighted marginal cost of capital (WMCC)

10

By considering the IRR of the available projects following is the ranking of available

projects:

Project Cost Return

F $500,000 10.11%

B $200,000 10.06%

D $500,000 10%

E $300,000 9.99%

G $500,000 9.81%

C $800,000 9.83%

A $400,000 6.51%

Company should select project on the basis of IRR, to generate higher returns.

11

Table 2: Investment decision on marginal basis

Project Cost Return

B $200,000 10.06%

E $300,000 9.99%

A $400,000 6.51%

F $500,000 10.11%

D $500,000 10%

G $500,000 9.81%

C $800,000 9.83%

Company will invest in project B but not in Project E and A, because despite of increase in

capital there is reduction in return. Further, they will invest inn Project F as with the increase

in invested amount there is increase in return and remaining projects will be rejected because

despite of increase in capital there is reduction in return.

12

WACC as per given ratio

Source Cost Weight

Weighted

cost

60% Debt 9% 0.6 5.40%

20% preference share 9% 0.2 1.80%

20% equity 12% 0.2 2.40%

WACC 9.60%

13

Above shown capital structure is more appropriate because; it have reduced WACC in

comparison to previous capital structure.

A $400,000 6.51%

F $500,000 10.11%

D $500,000 10%

G $500,000 9.81%

C $800,000 9.83%

Company will invest in project B but not in Project E and A, because despite of increase in

capital there is reduction in return. Further, they will invest inn Project F as with the increase

in invested amount there is increase in return and remaining projects will be rejected because

despite of increase in capital there is reduction in return.

12

WACC as per given ratio

Source Cost Weight

Weighted

cost

60% Debt 9% 0.6 5.40%

20% preference share 9% 0.2 1.80%

20% equity 12% 0.2 2.40%

WACC 9.60%

13

Above shown capital structure is more appropriate because; it have reduced WACC in

comparison to previous capital structure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

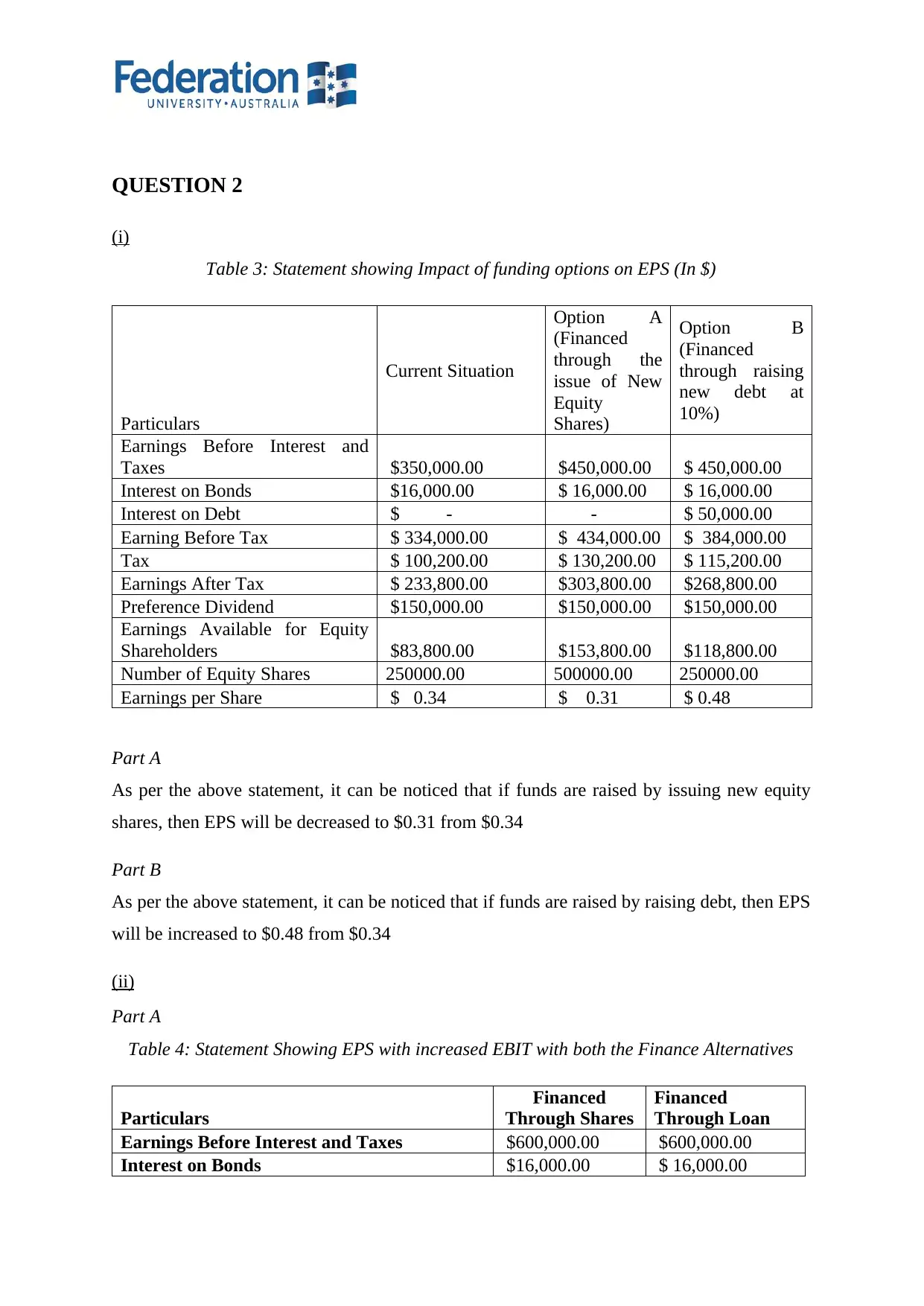

QUESTION 2

(i)

Table 3: Statement showing Impact of funding options on EPS (In $)

Particulars

Current Situation

Option A

(Financed

through the

issue of New

Equity

Shares)

Option B

(Financed

through raising

new debt at

10%)

Earnings Before Interest and

Taxes $350,000.00 $450,000.00 $ 450,000.00

Interest on Bonds $16,000.00 $ 16,000.00 $ 16,000.00

Interest on Debt $ - - $ 50,000.00

Earning Before Tax $ 334,000.00 $ 434,000.00 $ 384,000.00

Tax $ 100,200.00 $ 130,200.00 $ 115,200.00

Earnings After Tax $ 233,800.00 $303,800.00 $268,800.00

Preference Dividend $150,000.00 $150,000.00 $150,000.00

Earnings Available for Equity

Shareholders $83,800.00 $153,800.00 $118,800.00

Number of Equity Shares 250000.00 500000.00 250000.00

Earnings per Share $ 0.34 $ 0.31 $ 0.48

Part A

As per the above statement, it can be noticed that if funds are raised by issuing new equity

shares, then EPS will be decreased to $0.31 from $0.34

Part B

As per the above statement, it can be noticed that if funds are raised by raising debt, then EPS

will be increased to $0.48 from $0.34

(ii)

Part A

Table 4: Statement Showing EPS with increased EBIT with both the Finance Alternatives

Particulars

Financed

Through Shares

Financed

Through Loan

Earnings Before Interest and Taxes $600,000.00 $600,000.00

Interest on Bonds $16,000.00 $ 16,000.00

(i)

Table 3: Statement showing Impact of funding options on EPS (In $)

Particulars

Current Situation

Option A

(Financed

through the

issue of New

Equity

Shares)

Option B

(Financed

through raising

new debt at

10%)

Earnings Before Interest and

Taxes $350,000.00 $450,000.00 $ 450,000.00

Interest on Bonds $16,000.00 $ 16,000.00 $ 16,000.00

Interest on Debt $ - - $ 50,000.00

Earning Before Tax $ 334,000.00 $ 434,000.00 $ 384,000.00

Tax $ 100,200.00 $ 130,200.00 $ 115,200.00

Earnings After Tax $ 233,800.00 $303,800.00 $268,800.00

Preference Dividend $150,000.00 $150,000.00 $150,000.00

Earnings Available for Equity

Shareholders $83,800.00 $153,800.00 $118,800.00

Number of Equity Shares 250000.00 500000.00 250000.00

Earnings per Share $ 0.34 $ 0.31 $ 0.48

Part A

As per the above statement, it can be noticed that if funds are raised by issuing new equity

shares, then EPS will be decreased to $0.31 from $0.34

Part B

As per the above statement, it can be noticed that if funds are raised by raising debt, then EPS

will be increased to $0.48 from $0.34

(ii)

Part A

Table 4: Statement Showing EPS with increased EBIT with both the Finance Alternatives

Particulars

Financed

Through Shares

Financed

Through Loan

Earnings Before Interest and Taxes $600,000.00 $600,000.00

Interest on Bonds $16,000.00 $ 16,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

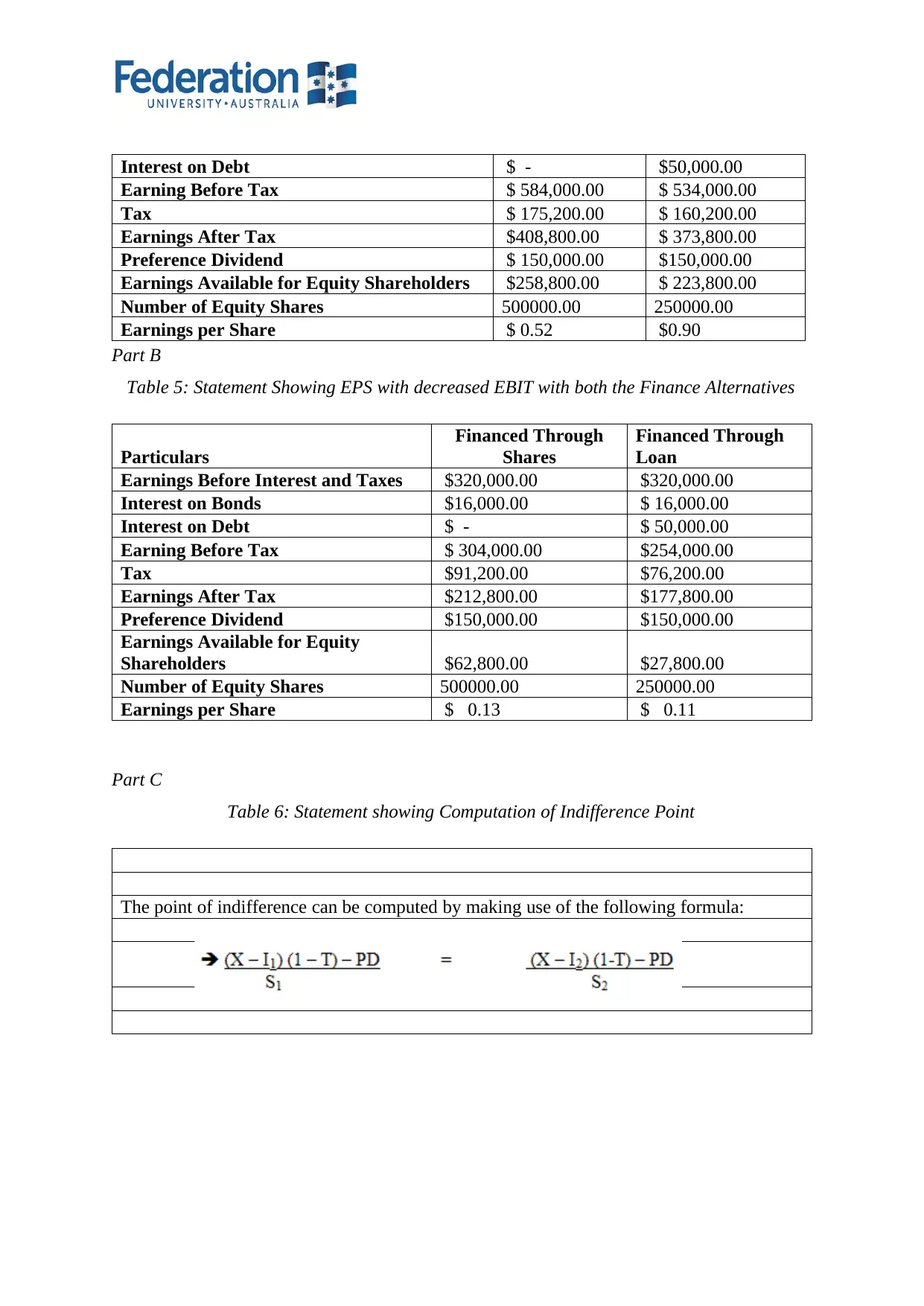

Interest on Debt $ - $50,000.00

Earning Before Tax $ 584,000.00 $ 534,000.00

Tax $ 175,200.00 $ 160,200.00

Earnings After Tax $408,800.00 $ 373,800.00

Preference Dividend $ 150,000.00 $150,000.00

Earnings Available for Equity Shareholders $258,800.00 $ 223,800.00

Number of Equity Shares 500000.00 250000.00

Earnings per Share $ 0.52 $0.90

Part B

Table 5: Statement Showing EPS with decreased EBIT with both the Finance Alternatives

Particulars

Financed Through

Shares

Financed Through

Loan

Earnings Before Interest and Taxes $320,000.00 $320,000.00

Interest on Bonds $16,000.00 $ 16,000.00

Interest on Debt $ - $ 50,000.00

Earning Before Tax $ 304,000.00 $254,000.00

Tax $91,200.00 $76,200.00

Earnings After Tax $212,800.00 $177,800.00

Preference Dividend $150,000.00 $150,000.00

Earnings Available for Equity

Shareholders $62,800.00 $27,800.00

Number of Equity Shares 500000.00 250000.00

Earnings per Share $ 0.13 $ 0.11

Part C

Table 6: Statement showing Computation of Indifference Point

The point of indifference can be computed by making use of the following formula:

Earning Before Tax $ 584,000.00 $ 534,000.00

Tax $ 175,200.00 $ 160,200.00

Earnings After Tax $408,800.00 $ 373,800.00

Preference Dividend $ 150,000.00 $150,000.00

Earnings Available for Equity Shareholders $258,800.00 $ 223,800.00

Number of Equity Shares 500000.00 250000.00

Earnings per Share $ 0.52 $0.90

Part B

Table 5: Statement Showing EPS with decreased EBIT with both the Finance Alternatives

Particulars

Financed Through

Shares

Financed Through

Loan

Earnings Before Interest and Taxes $320,000.00 $320,000.00

Interest on Bonds $16,000.00 $ 16,000.00

Interest on Debt $ - $ 50,000.00

Earning Before Tax $ 304,000.00 $254,000.00

Tax $91,200.00 $76,200.00

Earnings After Tax $212,800.00 $177,800.00

Preference Dividend $150,000.00 $150,000.00

Earnings Available for Equity

Shareholders $62,800.00 $27,800.00

Number of Equity Shares 500000.00 250000.00

Earnings per Share $ 0.13 $ 0.11

Part C

Table 6: Statement showing Computation of Indifference Point

The point of indifference can be computed by making use of the following formula:

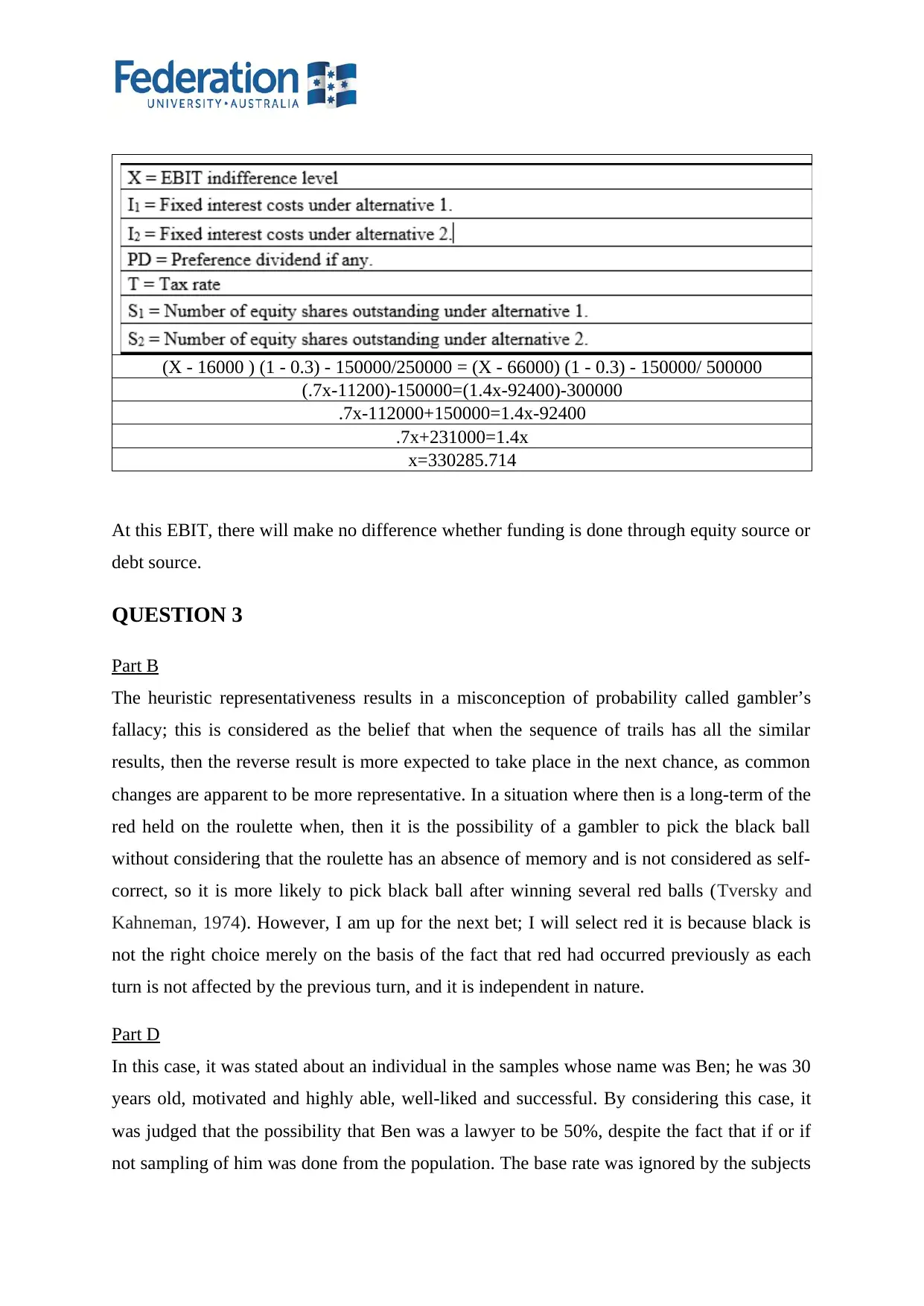

(X - 16000 ) (1 - 0.3) - 150000/250000 = (X - 66000) (1 - 0.3) - 150000/ 500000

(.7x-11200)-150000=(1.4x-92400)-300000

.7x-112000+150000=1.4x-92400

.7x+231000=1.4x

x=330285.714

At this EBIT, there will make no difference whether funding is done through equity source or

debt source.

QUESTION 3

Part B

The heuristic representativeness results in a misconception of probability called gambler’s

fallacy; this is considered as the belief that when the sequence of trails has all the similar

results, then the reverse result is more expected to take place in the next chance, as common

changes are apparent to be more representative. In a situation where then is a long-term of the

red held on the roulette when, then it is the possibility of a gambler to pick the black ball

without considering that the roulette has an absence of memory and is not considered as self-

correct, so it is more likely to pick black ball after winning several red balls (Tversky and

Kahneman, 1974). However, I am up for the next bet; I will select red it is because black is

not the right choice merely on the basis of the fact that red had occurred previously as each

turn is not affected by the previous turn, and it is independent in nature.

Part D

In this case, it was stated about an individual in the samples whose name was Ben; he was 30

years old, motivated and highly able, well-liked and successful. By considering this case, it

was judged that the possibility that Ben was a lawyer to be 50%, despite the fact that if or if

not sampling of him was done from the population. The base rate was ignored by the subjects

(.7x-11200)-150000=(1.4x-92400)-300000

.7x-112000+150000=1.4x-92400

.7x+231000=1.4x

x=330285.714

At this EBIT, there will make no difference whether funding is done through equity source or

debt source.

QUESTION 3

Part B

The heuristic representativeness results in a misconception of probability called gambler’s

fallacy; this is considered as the belief that when the sequence of trails has all the similar

results, then the reverse result is more expected to take place in the next chance, as common

changes are apparent to be more representative. In a situation where then is a long-term of the

red held on the roulette when, then it is the possibility of a gambler to pick the black ball

without considering that the roulette has an absence of memory and is not considered as self-

correct, so it is more likely to pick black ball after winning several red balls (Tversky and

Kahneman, 1974). However, I am up for the next bet; I will select red it is because black is

not the right choice merely on the basis of the fact that red had occurred previously as each

turn is not affected by the previous turn, and it is independent in nature.

Part D

In this case, it was stated about an individual in the samples whose name was Ben; he was 30

years old, motivated and highly able, well-liked and successful. By considering this case, it

was judged that the possibility that Ben was a lawyer to be 50%, despite the fact that if or if

not sampling of him was done from the population. The base rate was ignored by the subjects

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.