BUACC5931: ISO 9000 Adoption and Factors in China's Service Sector

VerifiedAdded on 2023/06/04

|19

|3960

|305

Report

AI Summary

This report investigates the adoption of ISO 9000 and its relationship with various factors in China's service industry. Using data from the National Bureau of Statistics of China, the study reveals that ISO 9000 certified companies demonstrate higher profits and sales compared to their non-certified counterparts. However, the report also highlights that only a small percentage of companies in the study have undergone ISO 9000 certification. Based on these findings, the report recommends a national campaign to promote ISO 9000 certification and stricter government regulations to ensure service quality. The analysis includes descriptive and inferential statistics, hypothesis testing, and managerial advice, while also acknowledging limitations and suggesting directions for future research.

Adoption of ISO9000 and its Relationship with other Factors in

China’s Service Industry

Name:

Date: 4th October 2018

China’s Service Industry

Name:

Date: 4th October 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

The main aim of this study was to identify the relationship between Adoption of ISO9000 with

other factor players in China’s service industry. Analysis of the data from the National Bureau of

Statistics of China gave the following main results;

The profit made by the ISO9000 certified companies was higher than that of the non-

ISO9000 certified companies

The sales made by the ISO9000 certified companies was higher than that of the non-

ISO9000 certified companies

Only a very small proportion (8%, n = 460) of the companies studied have so far

undergone ISO9000 certification.

Based on the above key findings, the following recommendations are made;

There is need for an intensive national drive and sensitization of various companies to

undergo ISO9000 certification.

The government to put strict and adequate measures for companies being registered to

ensure they are ISO9000 certified so as to ensure quality of service offered to the citizens

The main aim of this study was to identify the relationship between Adoption of ISO9000 with

other factor players in China’s service industry. Analysis of the data from the National Bureau of

Statistics of China gave the following main results;

The profit made by the ISO9000 certified companies was higher than that of the non-

ISO9000 certified companies

The sales made by the ISO9000 certified companies was higher than that of the non-

ISO9000 certified companies

Only a very small proportion (8%, n = 460) of the companies studied have so far

undergone ISO9000 certification.

Based on the above key findings, the following recommendations are made;

There is need for an intensive national drive and sensitization of various companies to

undergo ISO9000 certification.

The government to put strict and adequate measures for companies being registered to

ensure they are ISO9000 certified so as to ensure quality of service offered to the citizens

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Literature Review............................................................................................................................5

Motivations for Adoption of ISO Standards................................................................................5

Research Questions..........................................................................................................................6

Research Hypothesis........................................................................................................................7

Description of the methodology......................................................................................................8

Results..............................................................................................................................................8

Descriptive Analysis....................................................................................................................8

Inferential Analysis....................................................................................................................11

Discussion and managerial advises...............................................................................................16

Limitations and directions for future research...............................................................................17

References......................................................................................................................................17

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Literature Review............................................................................................................................5

Motivations for Adoption of ISO Standards................................................................................5

Research Questions..........................................................................................................................6

Research Hypothesis........................................................................................................................7

Description of the methodology......................................................................................................8

Results..............................................................................................................................................8

Descriptive Analysis....................................................................................................................8

Inferential Analysis....................................................................................................................11

Discussion and managerial advises...............................................................................................16

Limitations and directions for future research...............................................................................17

References......................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The ISO 9000 series of quality management systems standard has been widely applied all over

the world since its introduction in 1987. By the end of 2013, ISO 9000 had been adopted by over

1,129,000 facilities in 189 countries. Both academics and practitioners are interested in

understanding the relationship between adoption of ISO 9000, and other factors (Christmann &

Taylor, 2006; Du, Yin, & Zhang, 2016; Fikru, 2014a, 2014b, 2016; Nakamura, Takahashi, &

Vertinsky, 2001; Pekovic, 2010; Wu, Chu, & Liu, 2007).

In 2008, the National Bureau of Statistics of China conducted an Economic Census of the service

firms. The descriptions of variables, the coding are shown in the table. The data is available in

Moodle.

As an indication of universal quality framework, ISO9000 certification has been embraced by an

ever increasing number of business enterprises. In the last few years, there have been over half a

million certified companies in both America and Europe, and China has had an excess of

390,000 certified companies. It has pulled in attention of many scholars as to whether

certification has positive or negative impact on the performance of the companies. This paper

examines the ISO9000 certification impact on company's market performance basing on the

Chinese companies. Considering ISO9000 affirmation as an occasion, a confirmation impact

model will be set up by methods for the occasion ponder strategy, which takes irregular return

rate as a fundamental marker to gauge the ISO9000 accreditation impact on Chinese market

execution in various occasion times.

The ISO 9000 series of quality management systems standard has been widely applied all over

the world since its introduction in 1987. By the end of 2013, ISO 9000 had been adopted by over

1,129,000 facilities in 189 countries. Both academics and practitioners are interested in

understanding the relationship between adoption of ISO 9000, and other factors (Christmann &

Taylor, 2006; Du, Yin, & Zhang, 2016; Fikru, 2014a, 2014b, 2016; Nakamura, Takahashi, &

Vertinsky, 2001; Pekovic, 2010; Wu, Chu, & Liu, 2007).

In 2008, the National Bureau of Statistics of China conducted an Economic Census of the service

firms. The descriptions of variables, the coding are shown in the table. The data is available in

Moodle.

As an indication of universal quality framework, ISO9000 certification has been embraced by an

ever increasing number of business enterprises. In the last few years, there have been over half a

million certified companies in both America and Europe, and China has had an excess of

390,000 certified companies. It has pulled in attention of many scholars as to whether

certification has positive or negative impact on the performance of the companies. This paper

examines the ISO9000 certification impact on company's market performance basing on the

Chinese companies. Considering ISO9000 affirmation as an occasion, a confirmation impact

model will be set up by methods for the occasion ponder strategy, which takes irregular return

rate as a fundamental marker to gauge the ISO9000 accreditation impact on Chinese market

execution in various occasion times.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review

Motivations for Adoption of ISO Standards

Immediately after introduction of the ISO 9000 series sometime back in 1987, an number of

studies touching on motivational factors related to acquiring of ISO certification have been

published, yet the prevalent research approach has taken a gander at these components from the

alleged double perspective, or at the end of the day from the inward/outer inspirations point of

view. In view of this examination approach, the internal factors include desire to make more

profits, improve productivity, reduce on operation costs, and of course to improve on the quality.

The external factors on the other hand include enhanced image, pressure from the suppliers and

clients

(Santos & Millán, Motivation And Benefits Of Implementation And Certification According ISO

9001–The Portuguese Experience, 2013; Santos, Costa, & Leal, Motivation and benefits of

implementation and certification according ISO 9001: The Portuguese experience, 2014)

In general, the ISO 9000 group of principles has turned into a primary necessity for entering the

worldwide market (Sun, 2000; Abraham, Crawford, Carter, & Mazotta, 2000; Almeida, Caten, &

Gutterres, 2009), subsequently some of the past research takes a shot at the reasons behind

getting ISO certification argue that the external factors are better than the internal factors

(Casadesús & Karapetrovic, 2005; Dongmo & Onojaefe, 2013; Heras-Saizarbitoria, Arana, &

San , 2010).

The instance of Japan gives solid proof to the in advance of specified articulation: in the 90s, ISO

9001 accreditation turned into a necessity for exports to Europe. Henceforth, Japan was

compelled to acquire ISO accreditation keeping in mind the end goal to keep up and proceed

Motivations for Adoption of ISO Standards

Immediately after introduction of the ISO 9000 series sometime back in 1987, an number of

studies touching on motivational factors related to acquiring of ISO certification have been

published, yet the prevalent research approach has taken a gander at these components from the

alleged double perspective, or at the end of the day from the inward/outer inspirations point of

view. In view of this examination approach, the internal factors include desire to make more

profits, improve productivity, reduce on operation costs, and of course to improve on the quality.

The external factors on the other hand include enhanced image, pressure from the suppliers and

clients

(Santos & Millán, Motivation And Benefits Of Implementation And Certification According ISO

9001–The Portuguese Experience, 2013; Santos, Costa, & Leal, Motivation and benefits of

implementation and certification according ISO 9001: The Portuguese experience, 2014)

In general, the ISO 9000 group of principles has turned into a primary necessity for entering the

worldwide market (Sun, 2000; Abraham, Crawford, Carter, & Mazotta, 2000; Almeida, Caten, &

Gutterres, 2009), subsequently some of the past research takes a shot at the reasons behind

getting ISO certification argue that the external factors are better than the internal factors

(Casadesús & Karapetrovic, 2005; Dongmo & Onojaefe, 2013; Heras-Saizarbitoria, Arana, &

San , 2010).

The instance of Japan gives solid proof to the in advance of specified articulation: in the 90s, ISO

9001 accreditation turned into a necessity for exports to Europe. Henceforth, Japan was

compelled to acquire ISO accreditation keeping in mind the end goal to keep up and proceed

with the development of its piece of the overall industry abroad (Heras-Saizarbitoria, Arana, &

San , 2010; Kostagiolas & Kitsiou, 2008; Kumar & Balakrishnan, 2011).

Absolutely, there are likewise those (Abraham, Crawford, Carter, & Mazotta, 2000; Llopis &

Tarí, 2003) who contend that the appropriation of gauges, for example, the ISO 9000 series is

driven internally. For this situation, as upheld by Heras-Saizarbitoria et al. (2010), the adoption

would regularly rely upon the organization's particular hierarchical assets. For instance, on

account of organizations which go for TQM usage, ISO 9001 certification is a great beginning

towards reducing cost and quality change (Martínez-Costa, Martínez-Lorente, & Choi, 2008). As

Sun (2000) affirms, ISO 9001 accreditation can be helpful in the event that it is viewed as a route

towards TQM. In any case, for ISO execution requires a generous budgetary asset, which can

change from as meagre as ten thousand dollars to as much as three hundred thousand dollars

(Martínez-Lorente & Martínez-Costa, 2004) and on the grounds that the enhancements yielded

by such accreditation are easy to refute (Almeida, Caten, & Gutterres, 2009).

Research Questions

This study sought to answer the following research questions.

1. Is there is significant difference in the profit made by the ISO certified companies and the

non-ISO certified companies?

2. Is there is significant difference in the profit made by the companies with overseas

investment and those without overseas investment?

3. Is there is significant difference in the sales made by the ISO certified companies and the

non-ISO certified companies?

San , 2010; Kostagiolas & Kitsiou, 2008; Kumar & Balakrishnan, 2011).

Absolutely, there are likewise those (Abraham, Crawford, Carter, & Mazotta, 2000; Llopis &

Tarí, 2003) who contend that the appropriation of gauges, for example, the ISO 9000 series is

driven internally. For this situation, as upheld by Heras-Saizarbitoria et al. (2010), the adoption

would regularly rely upon the organization's particular hierarchical assets. For instance, on

account of organizations which go for TQM usage, ISO 9001 certification is a great beginning

towards reducing cost and quality change (Martínez-Costa, Martínez-Lorente, & Choi, 2008). As

Sun (2000) affirms, ISO 9001 accreditation can be helpful in the event that it is viewed as a route

towards TQM. In any case, for ISO execution requires a generous budgetary asset, which can

change from as meagre as ten thousand dollars to as much as three hundred thousand dollars

(Martínez-Lorente & Martínez-Costa, 2004) and on the grounds that the enhancements yielded

by such accreditation are easy to refute (Almeida, Caten, & Gutterres, 2009).

Research Questions

This study sought to answer the following research questions.

1. Is there is significant difference in the profit made by the ISO certified companies and the

non-ISO certified companies?

2. Is there is significant difference in the profit made by the companies with overseas

investment and those without overseas investment?

3. Is there is significant difference in the sales made by the ISO certified companies and the

non-ISO certified companies?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Is there is significant difference in the sales made by the companies with overseas

investment and those without overseas investment?

5. What factors affect the company profits?

Research Hypothesis

From the above research questions, the following hypothesis were generated and were to be

tested so answer to answer the research questions.

H0: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

H0: There is no significant difference in the average profit made by the companies with overseas

investment and those without overseas investment.

HA: There is significant difference in the average profit made by the companies with overseas

investment and those without overseas investment.

H0: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

H0: There is no significant difference in the average sales made by the companies with overseas

investment and those without overseas investment.

HA: There is significant difference in the average sales made by the companies with overseas

investment and those without overseas investment.

H0: There are no factors that significantly affect the profits of a company

investment and those without overseas investment?

5. What factors affect the company profits?

Research Hypothesis

From the above research questions, the following hypothesis were generated and were to be

tested so answer to answer the research questions.

H0: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

H0: There is no significant difference in the average profit made by the companies with overseas

investment and those without overseas investment.

HA: There is significant difference in the average profit made by the companies with overseas

investment and those without overseas investment.

H0: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

H0: There is no significant difference in the average sales made by the companies with overseas

investment and those without overseas investment.

HA: There is significant difference in the average sales made by the companies with overseas

investment and those without overseas investment.

H0: There are no factors that significantly affect the profits of a company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

HA: There are factors that significantly affect the profits of a company

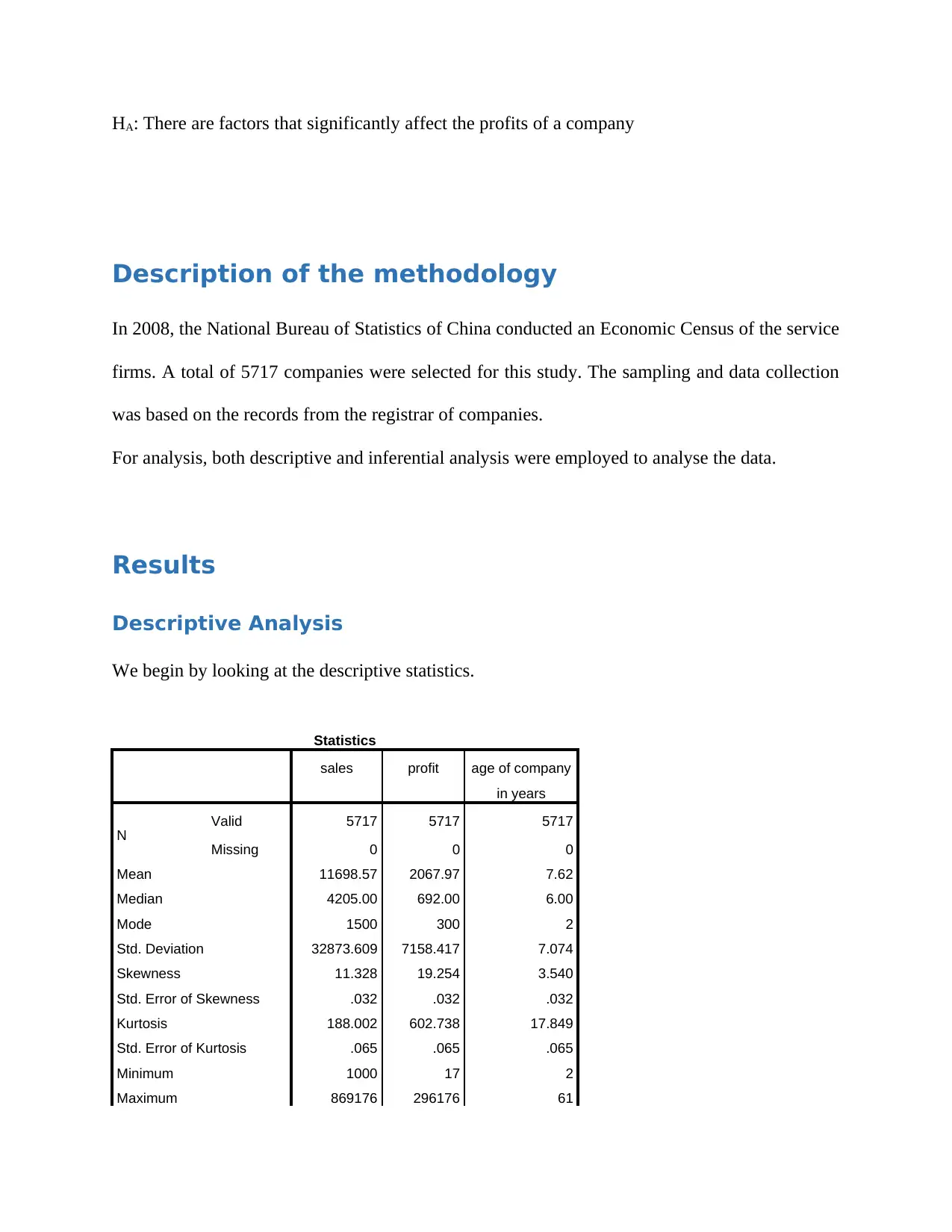

Description of the methodology

In 2008, the National Bureau of Statistics of China conducted an Economic Census of the service

firms. A total of 5717 companies were selected for this study. The sampling and data collection

was based on the records from the registrar of companies.

For analysis, both descriptive and inferential analysis were employed to analyse the data.

Results

Descriptive Analysis

We begin by looking at the descriptive statistics.

Statistics

sales profit age of company

in years

N Valid 5717 5717 5717

Missing 0 0 0

Mean 11698.57 2067.97 7.62

Median 4205.00 692.00 6.00

Mode 1500 300 2

Std. Deviation 32873.609 7158.417 7.074

Skewness 11.328 19.254 3.540

Std. Error of Skewness .032 .032 .032

Kurtosis 188.002 602.738 17.849

Std. Error of Kurtosis .065 .065 .065

Minimum 1000 17 2

Maximum 869176 296176 61

Description of the methodology

In 2008, the National Bureau of Statistics of China conducted an Economic Census of the service

firms. A total of 5717 companies were selected for this study. The sampling and data collection

was based on the records from the registrar of companies.

For analysis, both descriptive and inferential analysis were employed to analyse the data.

Results

Descriptive Analysis

We begin by looking at the descriptive statistics.

Statistics

sales profit age of company

in years

N Valid 5717 5717 5717

Missing 0 0 0

Mean 11698.57 2067.97 7.62

Median 4205.00 692.00 6.00

Mode 1500 300 2

Std. Deviation 32873.609 7158.417 7.074

Skewness 11.328 19.254 3.540

Std. Error of Skewness .032 .032 .032

Kurtosis 188.002 602.738 17.849

Std. Error of Kurtosis .065 .065 .065

Minimum 1000 17 2

Maximum 869176 296176 61

Percentiles

25 2273.50 313.00 3.00

50 4205.00 692.00 6.00

75 8953.50 1542.00 9.00

As can be seen, the average sales for all the companies in the sample was found to be 11698.57

while the average profit was 2067.97. The maximum profit made by the companies was 296176

while the minimum profit was 17. In terms of company age, the average age of the companies

was found to be 7.62 years with the oldest company being 61 years old and the youngest

company being 2 years old.

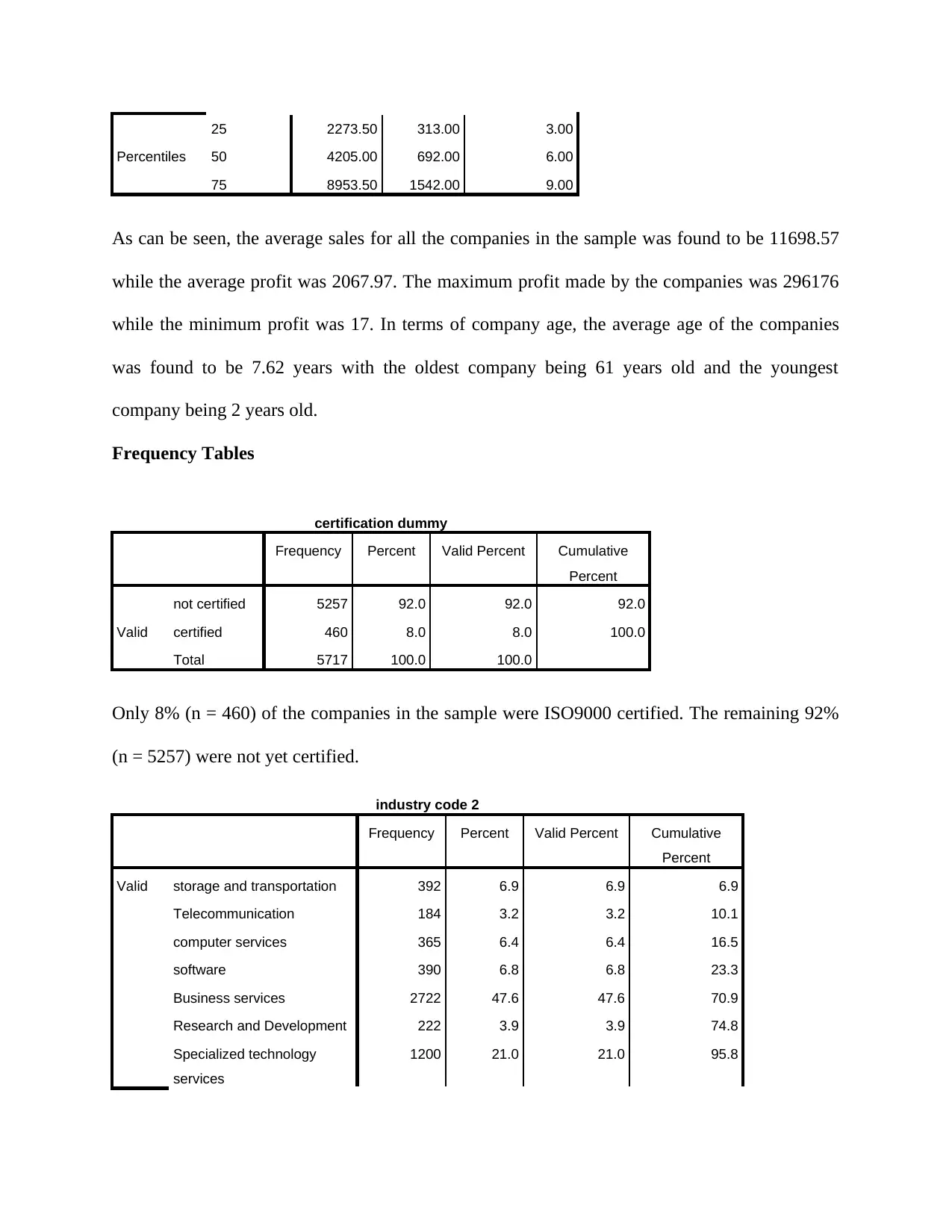

Frequency Tables

certification dummy

Frequency Percent Valid Percent Cumulative

Percent

Valid

not certified 5257 92.0 92.0 92.0

certified 460 8.0 8.0 100.0

Total 5717 100.0 100.0

Only 8% (n = 460) of the companies in the sample were ISO9000 certified. The remaining 92%

(n = 5257) were not yet certified.

industry code 2

Frequency Percent Valid Percent Cumulative

Percent

Valid storage and transportation 392 6.9 6.9 6.9

Telecommunication 184 3.2 3.2 10.1

computer services 365 6.4 6.4 16.5

software 390 6.8 6.8 23.3

Business services 2722 47.6 47.6 70.9

Research and Development 222 3.9 3.9 74.8

Specialized technology

services

1200 21.0 21.0 95.8

25 2273.50 313.00 3.00

50 4205.00 692.00 6.00

75 8953.50 1542.00 9.00

As can be seen, the average sales for all the companies in the sample was found to be 11698.57

while the average profit was 2067.97. The maximum profit made by the companies was 296176

while the minimum profit was 17. In terms of company age, the average age of the companies

was found to be 7.62 years with the oldest company being 61 years old and the youngest

company being 2 years old.

Frequency Tables

certification dummy

Frequency Percent Valid Percent Cumulative

Percent

Valid

not certified 5257 92.0 92.0 92.0

certified 460 8.0 8.0 100.0

Total 5717 100.0 100.0

Only 8% (n = 460) of the companies in the sample were ISO9000 certified. The remaining 92%

(n = 5257) were not yet certified.

industry code 2

Frequency Percent Valid Percent Cumulative

Percent

Valid storage and transportation 392 6.9 6.9 6.9

Telecommunication 184 3.2 3.2 10.1

computer services 365 6.4 6.4 16.5

software 390 6.8 6.8 23.3

Business services 2722 47.6 47.6 70.9

Research and Development 222 3.9 3.9 74.8

Specialized technology

services

1200 21.0 21.0 95.8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Technology exchange and

promotion

242 4.2 4.2 100.0

Total 5717 100.0 100.0

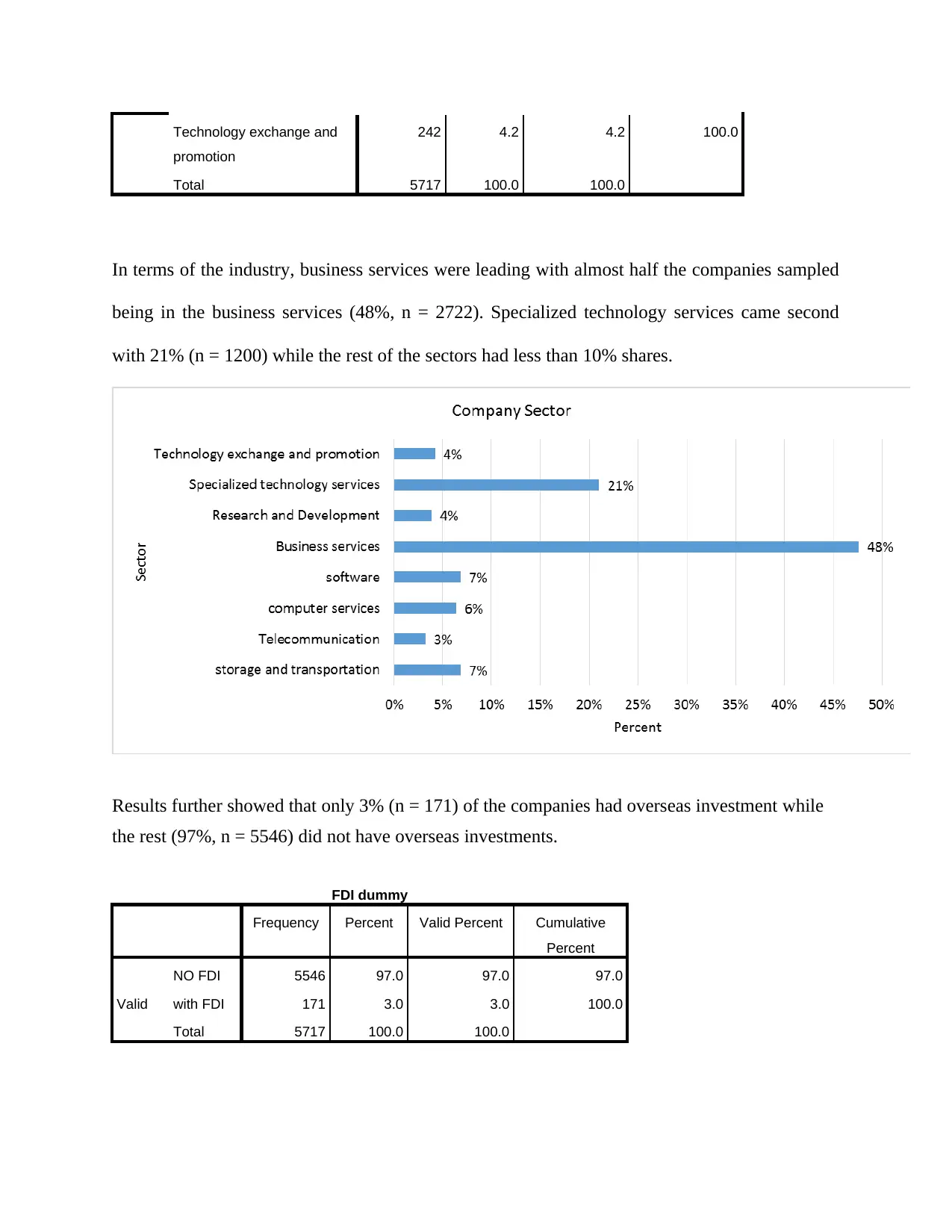

In terms of the industry, business services were leading with almost half the companies sampled

being in the business services (48%, n = 2722). Specialized technology services came second

with 21% (n = 1200) while the rest of the sectors had less than 10% shares.

Results further showed that only 3% (n = 171) of the companies had overseas investment while

the rest (97%, n = 5546) did not have overseas investments.

FDI dummy

Frequency Percent Valid Percent Cumulative

Percent

Valid

NO FDI 5546 97.0 97.0 97.0

with FDI 171 3.0 3.0 100.0

Total 5717 100.0 100.0

promotion

242 4.2 4.2 100.0

Total 5717 100.0 100.0

In terms of the industry, business services were leading with almost half the companies sampled

being in the business services (48%, n = 2722). Specialized technology services came second

with 21% (n = 1200) while the rest of the sectors had less than 10% shares.

Results further showed that only 3% (n = 171) of the companies had overseas investment while

the rest (97%, n = 5546) did not have overseas investments.

FDI dummy

Frequency Percent Valid Percent Cumulative

Percent

Valid

NO FDI 5546 97.0 97.0 97.0

with FDI 171 3.0 3.0 100.0

Total 5717 100.0 100.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inferential Analysis

Hypothesis Tests

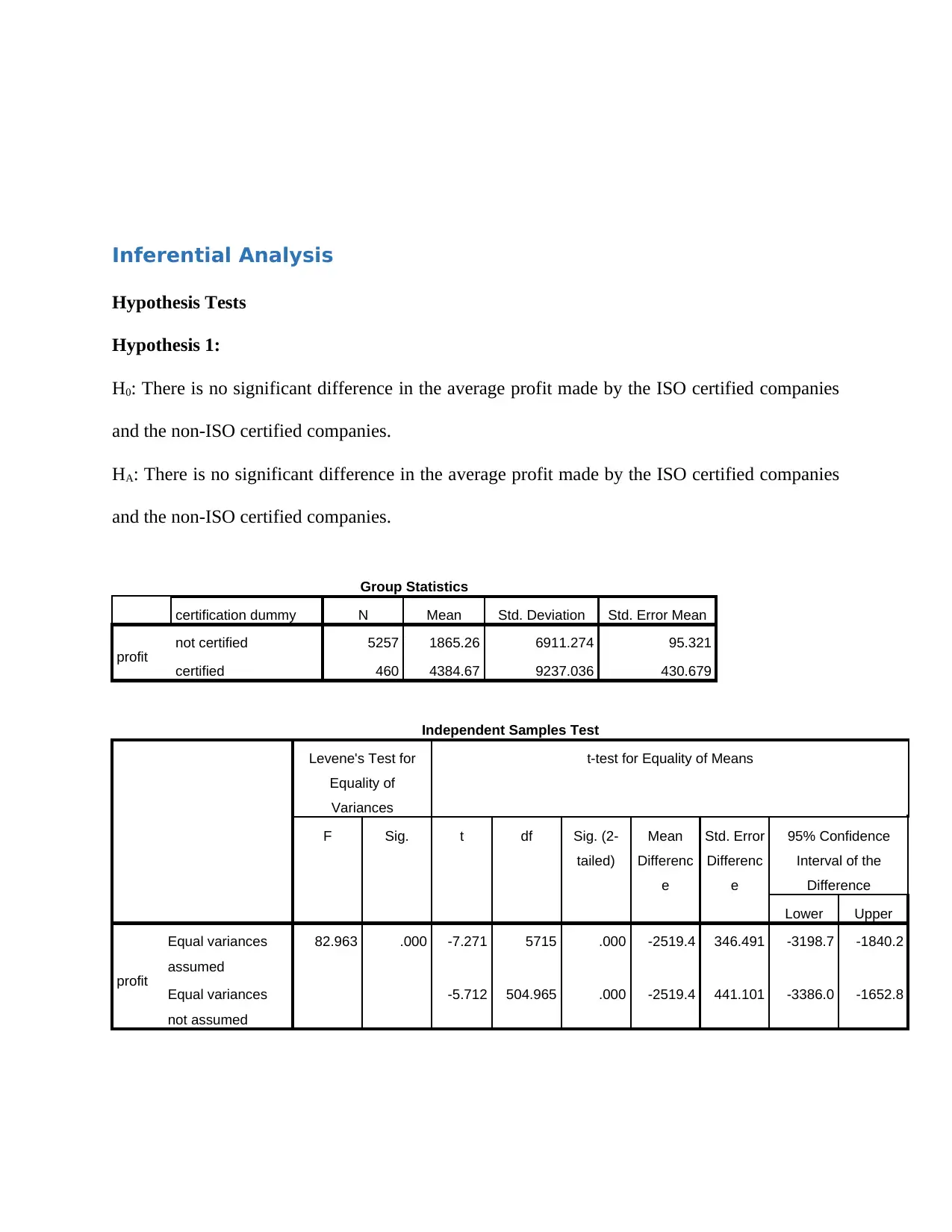

Hypothesis 1:

H0: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

Group Statistics

certification dummy N Mean Std. Deviation Std. Error Mean

profit not certified 5257 1865.26 6911.274 95.321

certified 460 4384.67 9237.036 430.679

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differenc

e

Std. Error

Differenc

e

95% Confidence

Interval of the

Difference

Lower Upper

profit

Equal variances

assumed

82.963 .000 -7.271 5715 .000 -2519.4 346.491 -3198.7 -1840.2

Equal variances

not assumed

-5.712 504.965 .000 -2519.4 441.101 -3386.0 -1652.8

Hypothesis Tests

Hypothesis 1:

H0: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average profit made by the ISO certified companies

and the non-ISO certified companies.

Group Statistics

certification dummy N Mean Std. Deviation Std. Error Mean

profit not certified 5257 1865.26 6911.274 95.321

certified 460 4384.67 9237.036 430.679

Independent Samples Test

Levene's Test for

Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differenc

e

Std. Error

Differenc

e

95% Confidence

Interval of the

Difference

Lower Upper

profit

Equal variances

assumed

82.963 .000 -7.271 5715 .000 -2519.4 346.491 -3198.7 -1840.2

Equal variances

not assumed

-5.712 504.965 .000 -2519.4 441.101 -3386.0 -1652.8

We performed an independent t-test in order to compare the average profits for ISO9000

certified companies and non-ISO9000 certified companies. Results showed that the average

profits for ISO9000 certified companies (M = 4384.67, SD = 9237.04, N = 460) was

significantly different from the average profits for the non-ISO9000 certified companies (M =

1865.26, SD = 6911.27, N = 5257), t (5715) = -7.271, p < .05, two-tailed. Essentially the results

showed that the average profits made by the ISO9000 certified companies was significantly

higher than that of the non-ISO9000 certified companies.

Hypothesis 2:

H0: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

Group Statistics

certification dummy N Mean Std. Deviation Std. Error Mean

sales not certified 5257 10132.88 29617.093 408.482

certified 460 29591.67 55356.924 2581.030

Independent Samples Test

Levene's Test for

Equality of Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differenc

e

Std. Error

Differenc

e

95% Confidence

Interval of the

Difference

Lower Upper

sales Equal variances

assumed

203.848 .000 -12.334 5715 .000 -19458.8 1577.673 -22551.6 -16366.0

certified companies and non-ISO9000 certified companies. Results showed that the average

profits for ISO9000 certified companies (M = 4384.67, SD = 9237.04, N = 460) was

significantly different from the average profits for the non-ISO9000 certified companies (M =

1865.26, SD = 6911.27, N = 5257), t (5715) = -7.271, p < .05, two-tailed. Essentially the results

showed that the average profits made by the ISO9000 certified companies was significantly

higher than that of the non-ISO9000 certified companies.

Hypothesis 2:

H0: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

HA: There is no significant difference in the average sales made by the ISO certified companies

and the non-ISO certified companies.

Group Statistics

certification dummy N Mean Std. Deviation Std. Error Mean

sales not certified 5257 10132.88 29617.093 408.482

certified 460 29591.67 55356.924 2581.030

Independent Samples Test

Levene's Test for

Equality of Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differenc

e

Std. Error

Differenc

e

95% Confidence

Interval of the

Difference

Lower Upper

sales Equal variances

assumed

203.848 .000 -12.334 5715 .000 -19458.8 1577.673 -22551.6 -16366.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.