BUACC5936: Financial Management - Time Value of Money & Investment

VerifiedAdded on 2023/03/23

|14

|2101

|97

Homework Assignment

AI Summary

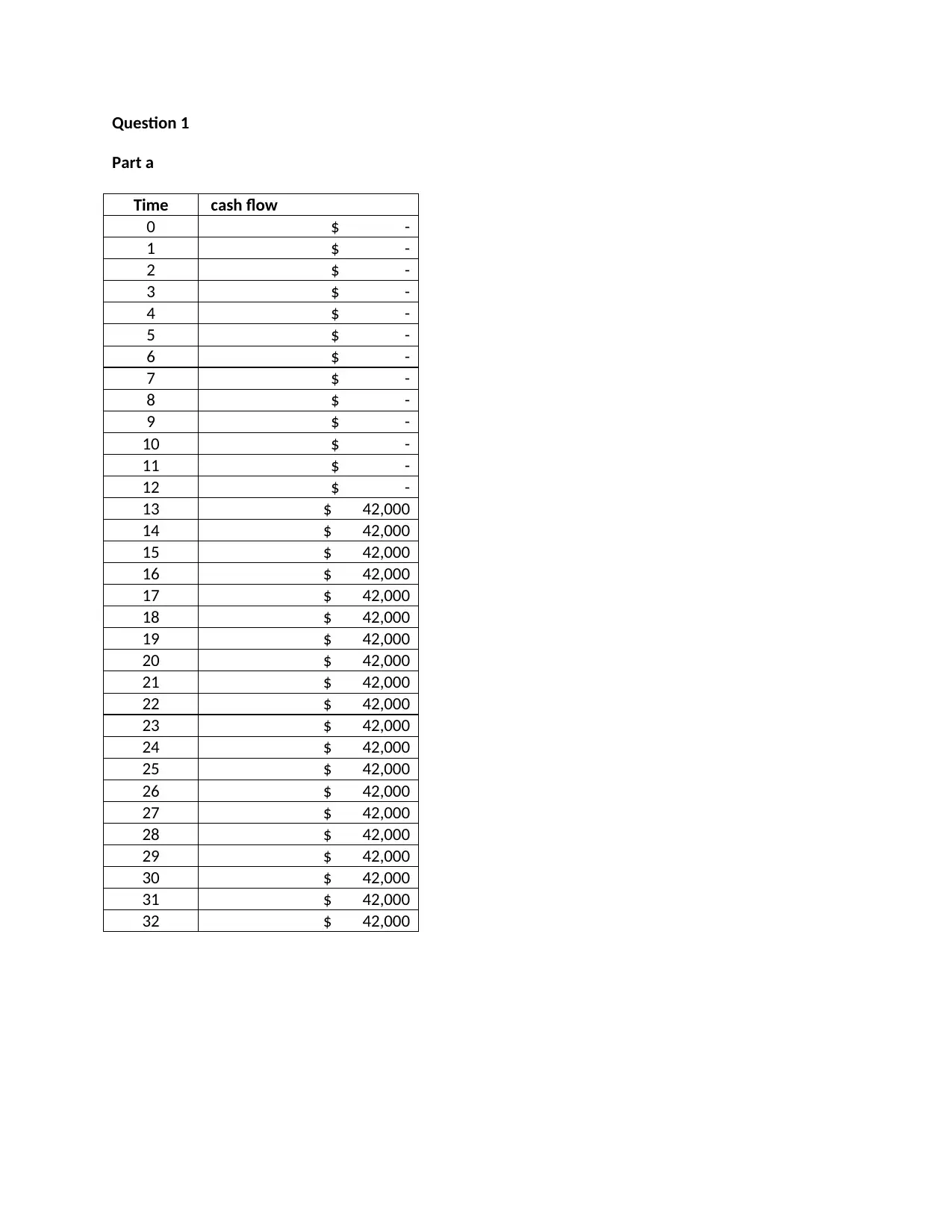

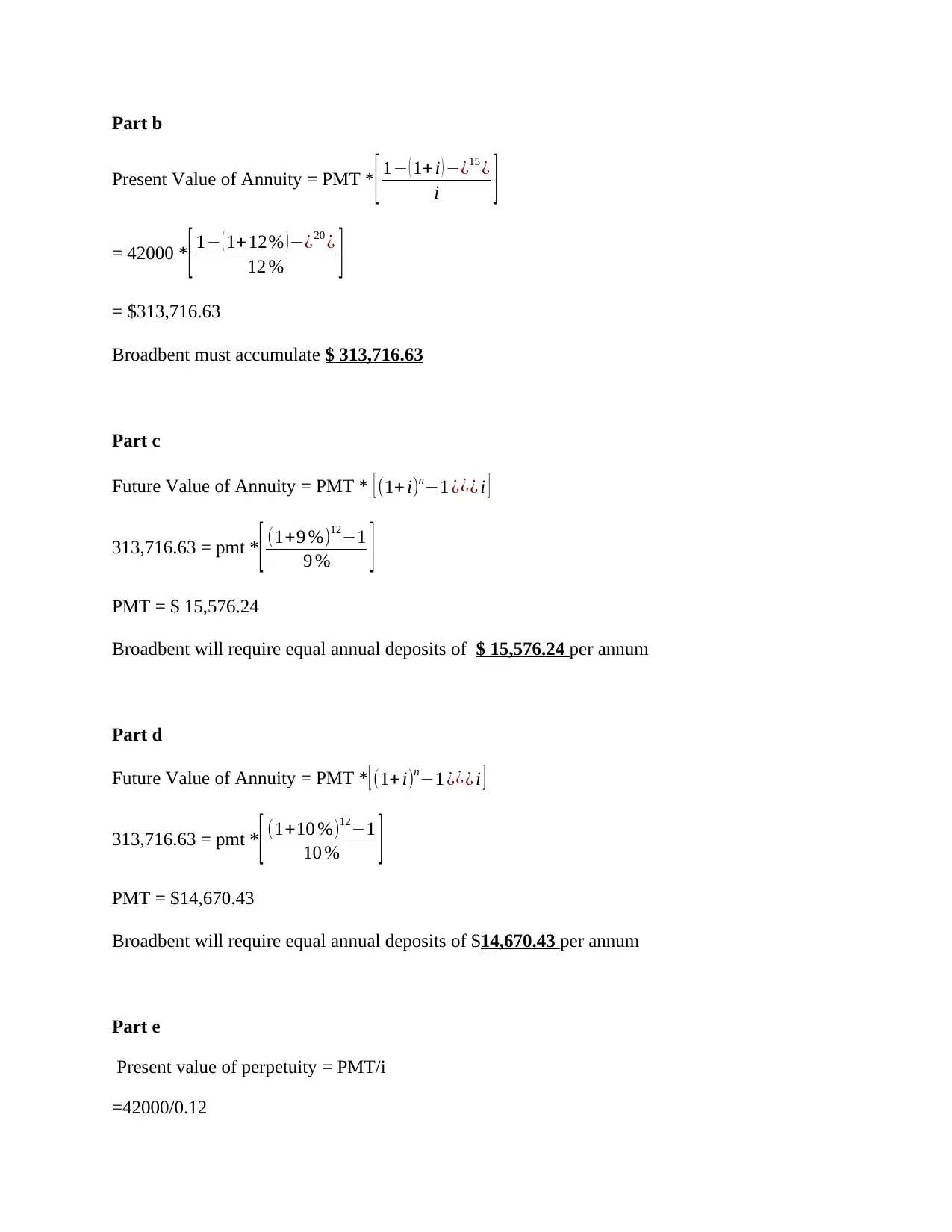

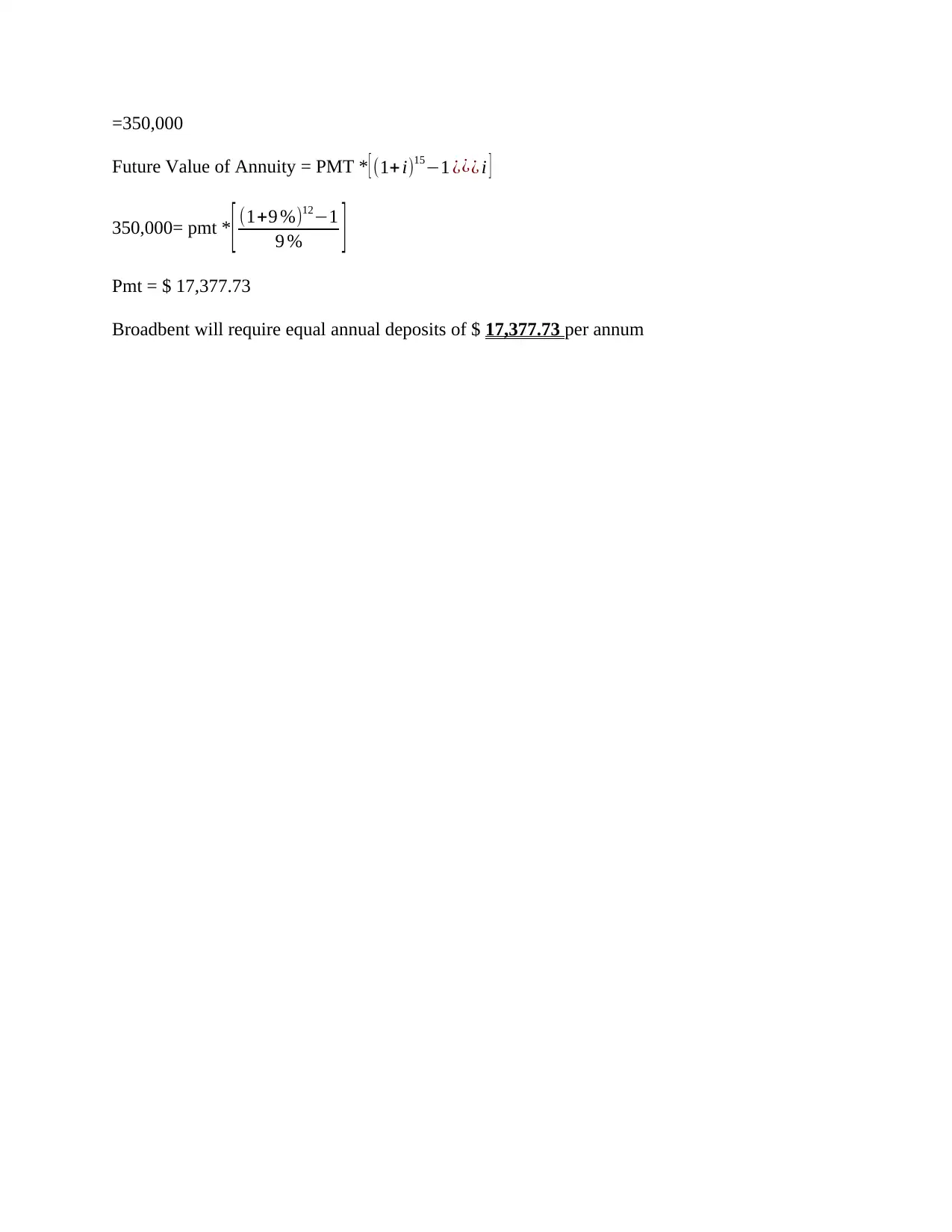

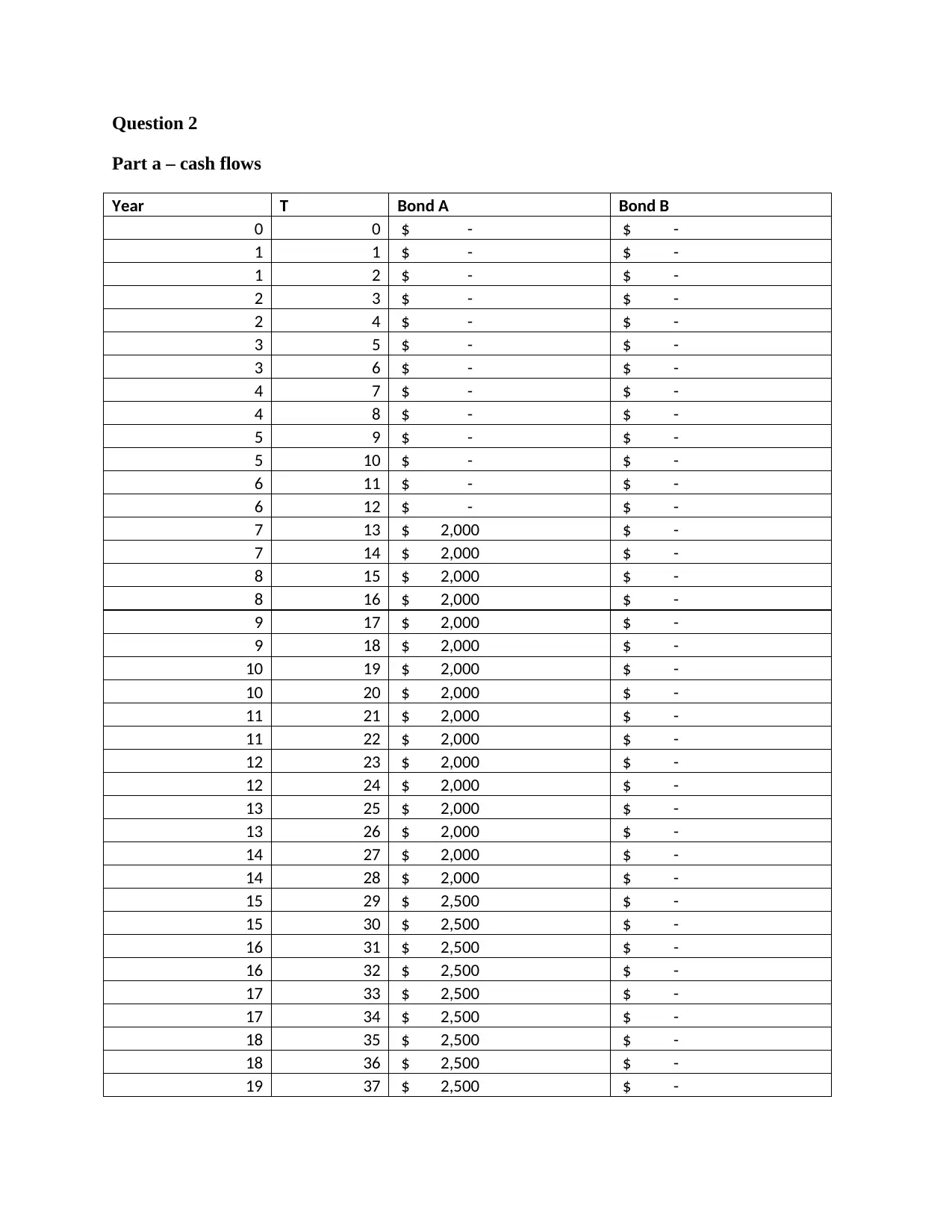

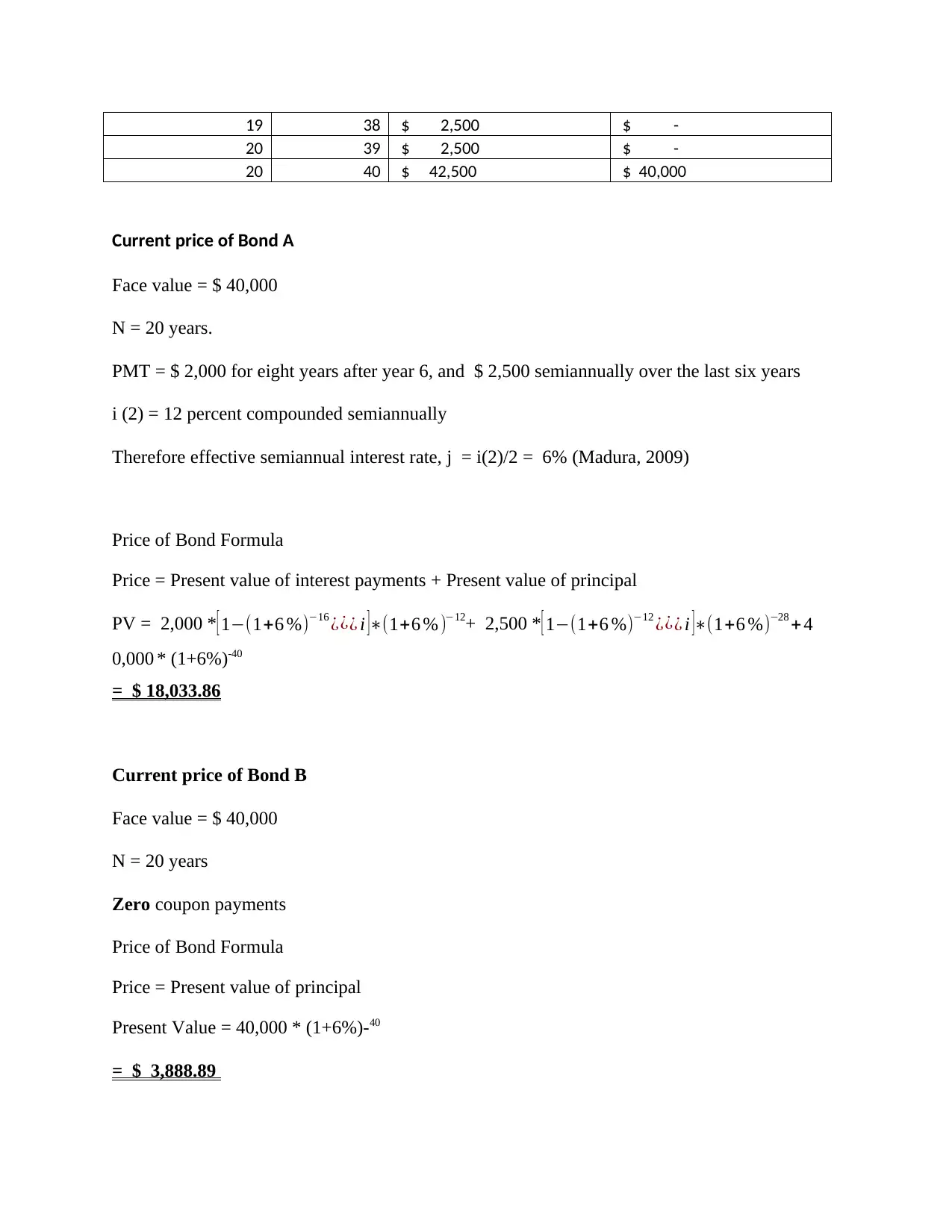

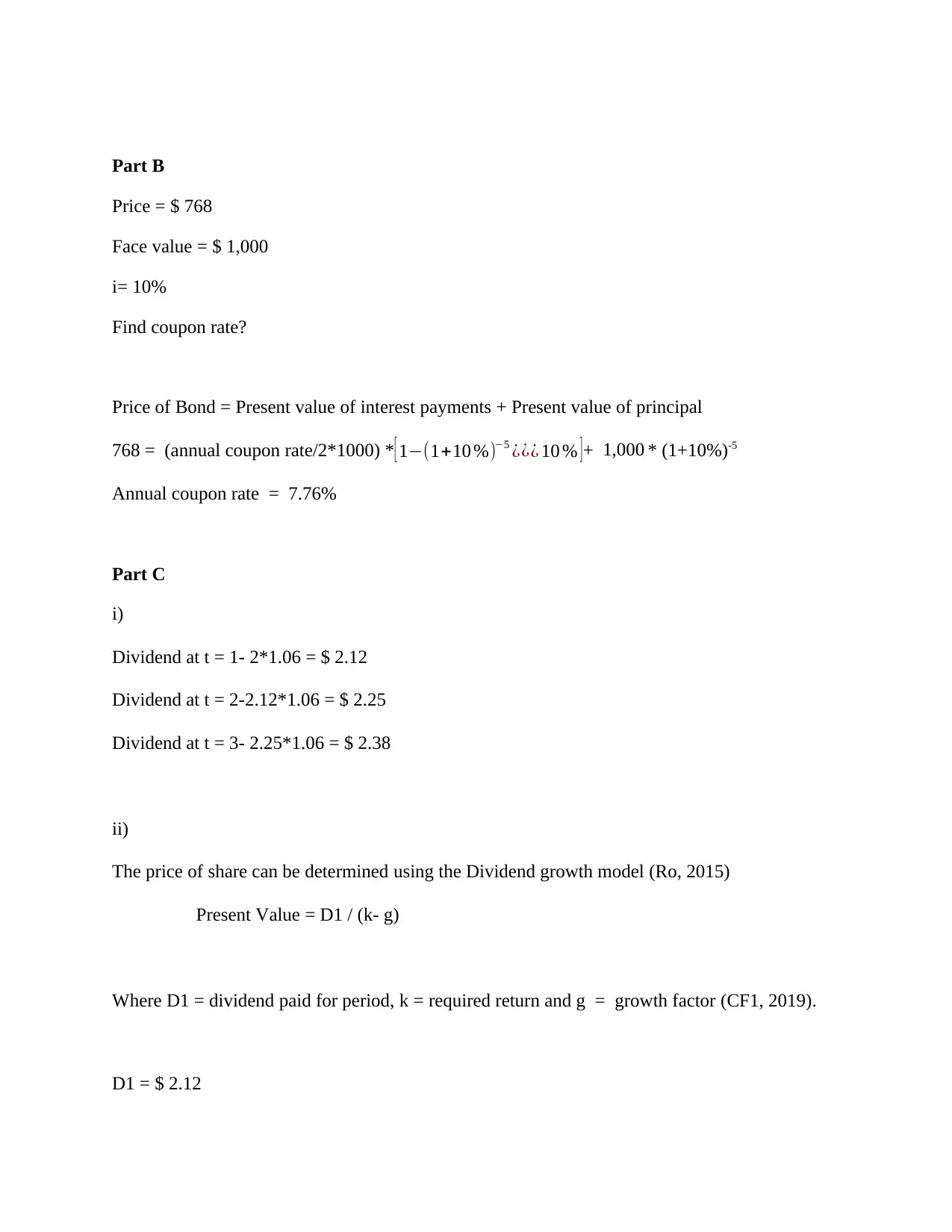

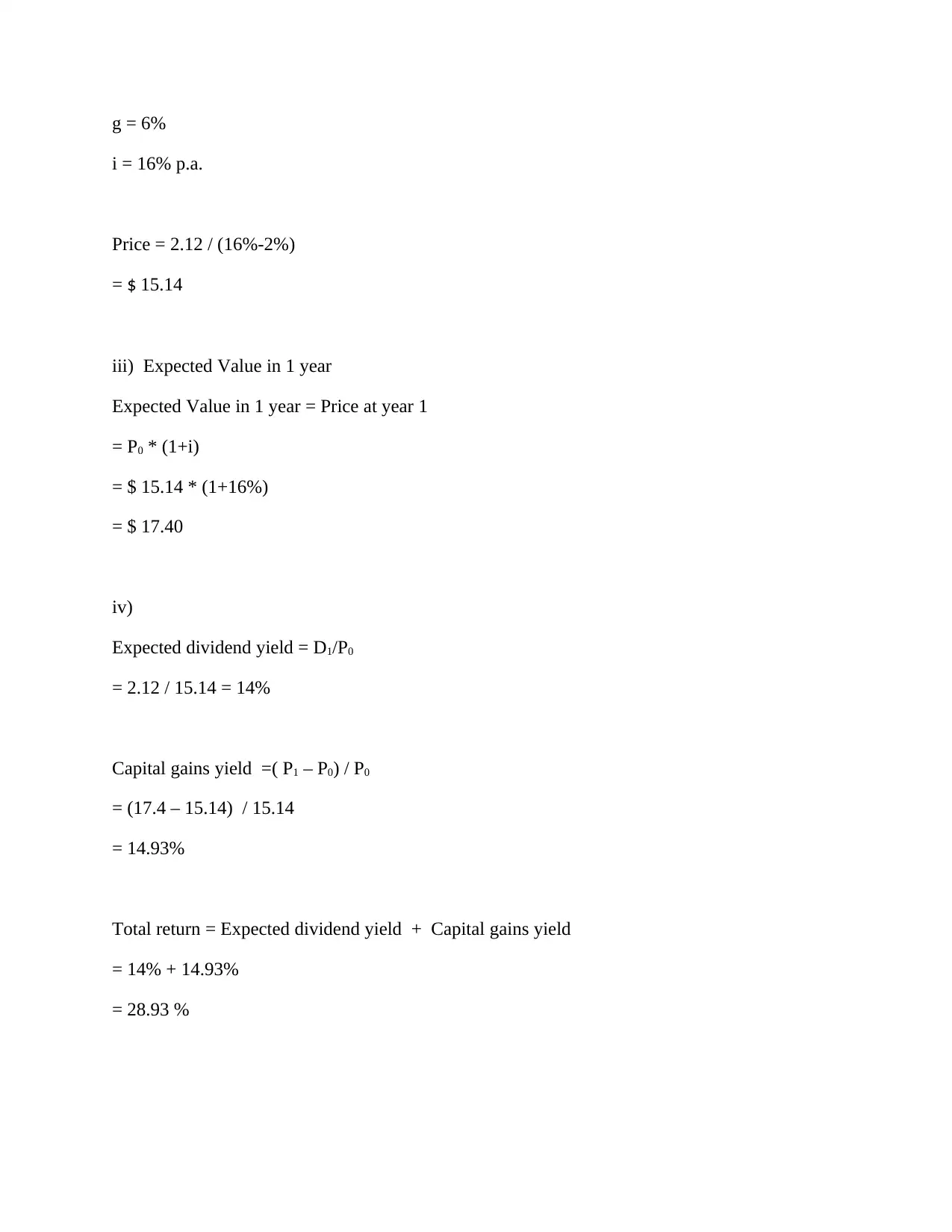

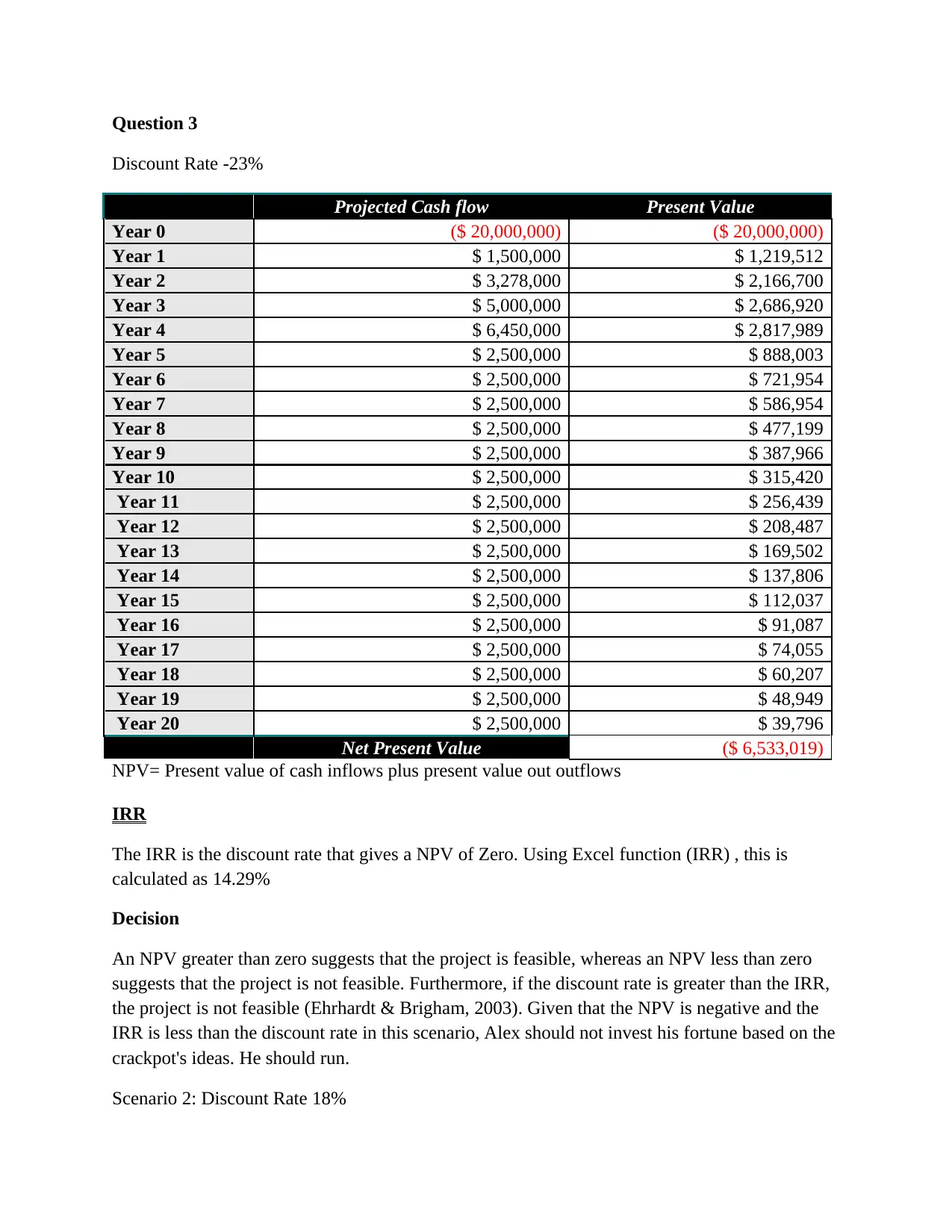

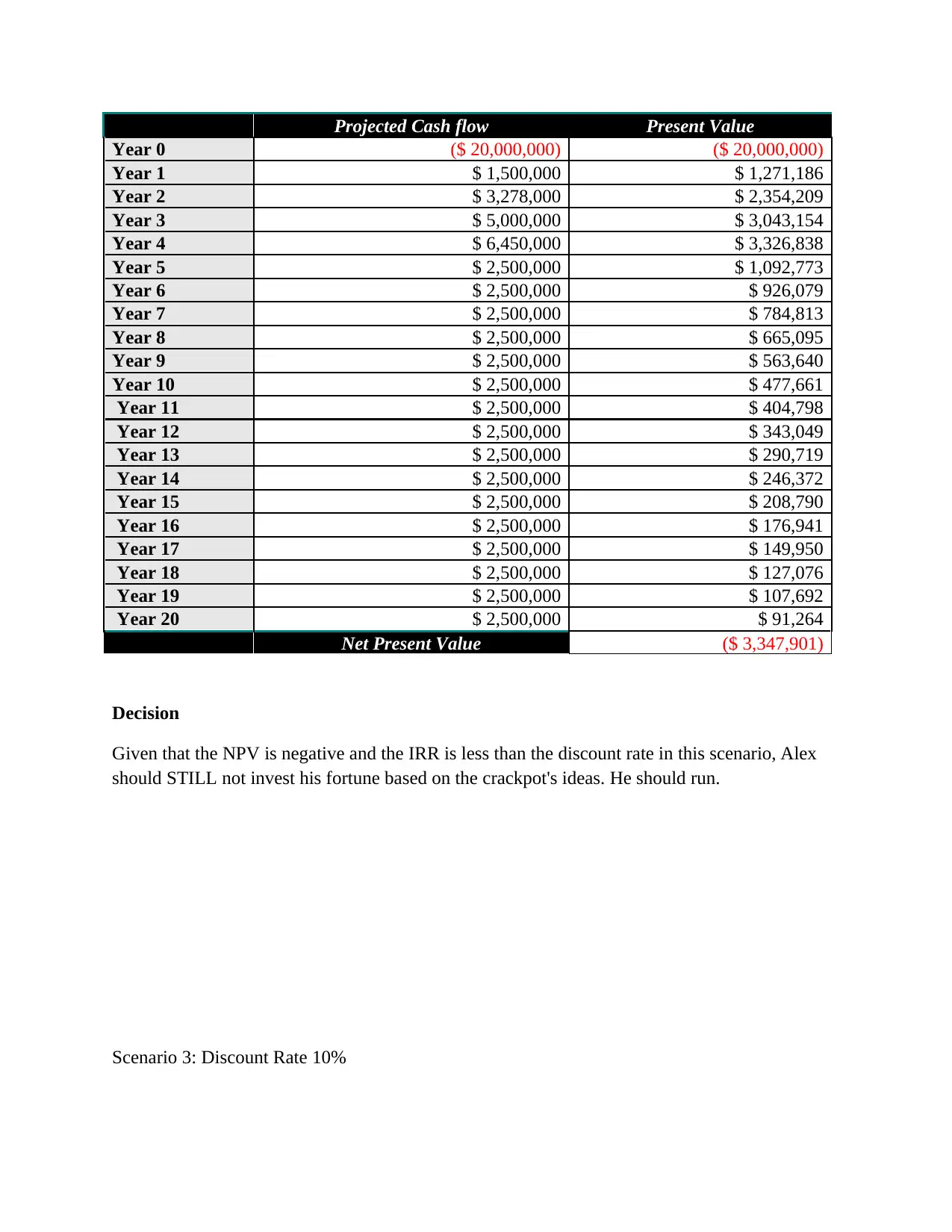

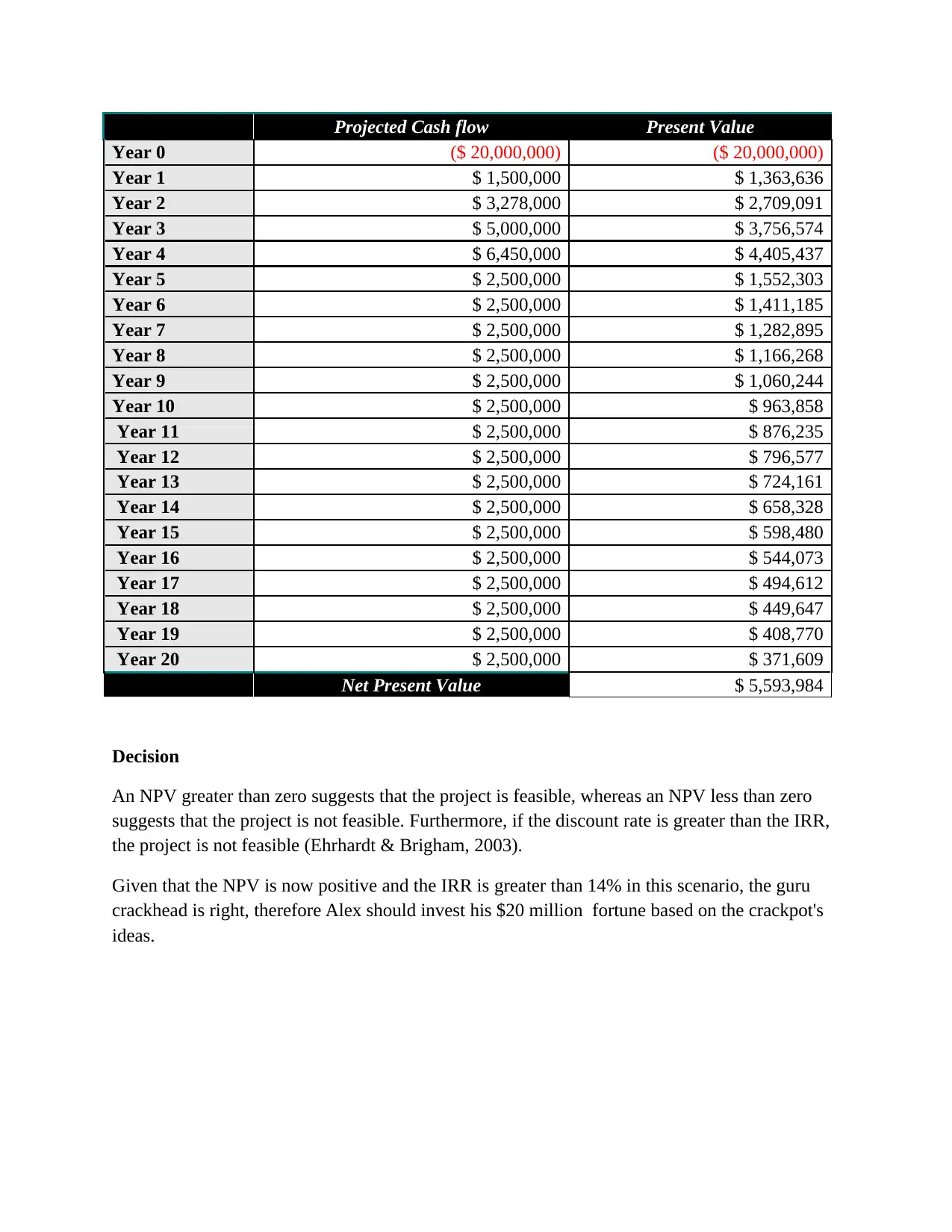

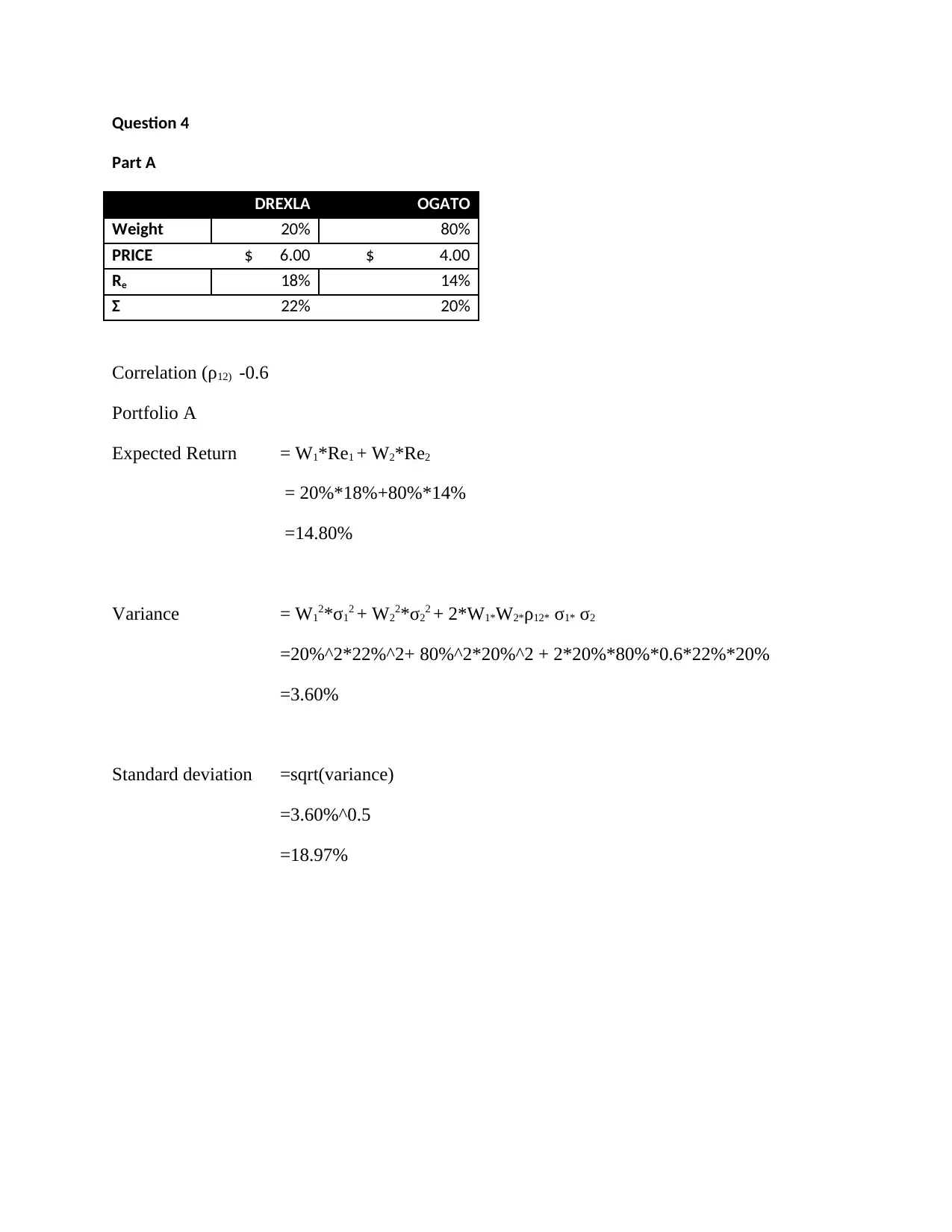

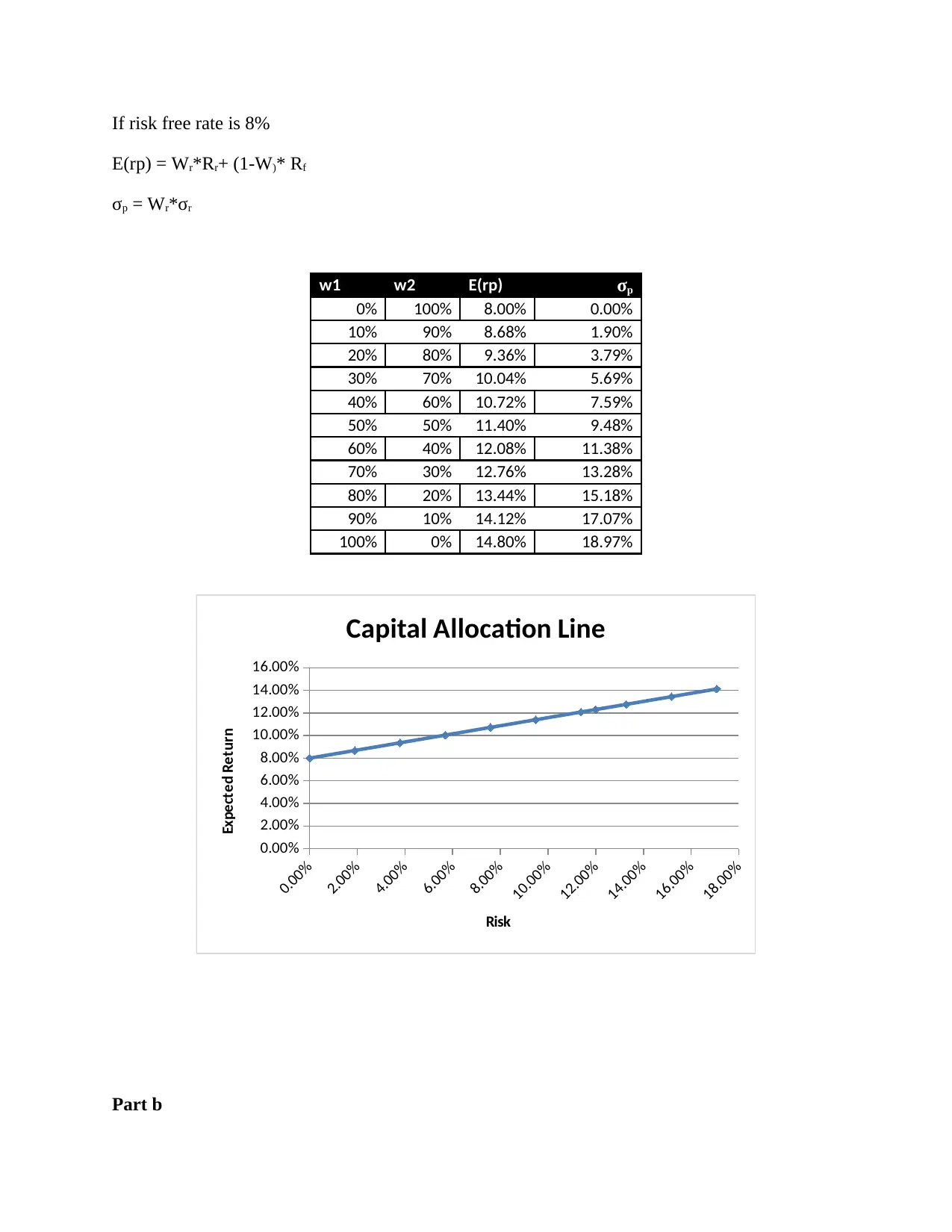

This assignment provides solutions to financial management problems, including time value of money calculations for retirement annuities, bond valuation, investment analysis using Net Present Value (NPV) and Internal Rate of Return (IRR), and portfolio analysis. It covers topics such as calculating the present value of an annuity, future value of an annuity, determining required annual deposits, bond pricing with varying coupon payments, zero-coupon bond pricing, calculating coupon rates, and using the dividend growth model to determine share prices. The assignment also analyzes investment decisions based on NPV and IRR under different discount rate scenarios and provides portfolio analysis with risk-free rate considerations. The document is available on Desklib, a platform offering a wide range of study resources for students.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.