Understanding Budget Discrepancies in Management Approaches

VerifiedAdded on 2020/05/03

|15

|3290

|157

AI Summary

The document examines two distinct budgeting approaches: imposed and participative. An imposed approach is characterized by a top-down communication flow where decisions are made independently by senior management without input from lower-level staff. This method allows for swift decision-making but may lead to disengagement among employees, who feel less responsible for the outcomes. Conversely, a participative budgetary approach involves all organizational levels in the budgeting process, fostering inclusivity and motivation. This bottom-up communication flow encourages detailed analysis and error reduction due to collective input. However, it can be time-consuming. The analysis highlights how these approaches influence an employee's response to budget discrepancies. In an imposed system, employees like Paulo might address issues without urgency, whereas in a participative environment, they are more likely to proactively seek solutions due to their involvement in the process.

Running head: AN EVALUATION OF BUDGETS

An Evaluation of Budgets

Student’s Name:

University Name:

Author Note

An Evaluation of Budgets

Student’s Name:

University Name:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AN EVALUATION OF BUDGETS

Table of Contents

Part A.........................................................................................................................................2

Answer to Part a.....................................................................................................................2

Answer to Part b.....................................................................................................................2

Answer to Part c.....................................................................................................................2

Answer to Part d.....................................................................................................................3

Answer to Part e.....................................................................................................................3

Answer to Part f.....................................................................................................................4

Answer to Part g.....................................................................................................................5

Answer to Part h.....................................................................................................................5

Answer to Part i......................................................................................................................6

Workings................................................................................................................................7

Part B..........................................................................................................................................8

Part C..........................................................................................................................................9

Part D.......................................................................................................................................12

References................................................................................................................................15

Table of Contents

Part A.........................................................................................................................................2

Answer to Part a.....................................................................................................................2

Answer to Part b.....................................................................................................................2

Answer to Part c.....................................................................................................................2

Answer to Part d.....................................................................................................................3

Answer to Part e.....................................................................................................................3

Answer to Part f.....................................................................................................................4

Answer to Part g.....................................................................................................................5

Answer to Part h.....................................................................................................................5

Answer to Part i......................................................................................................................6

Workings................................................................................................................................7

Part B..........................................................................................................................................8

Part C..........................................................................................................................................9

Part D.......................................................................................................................................12

References................................................................................................................................15

2AN EVALUATION OF BUDGETS

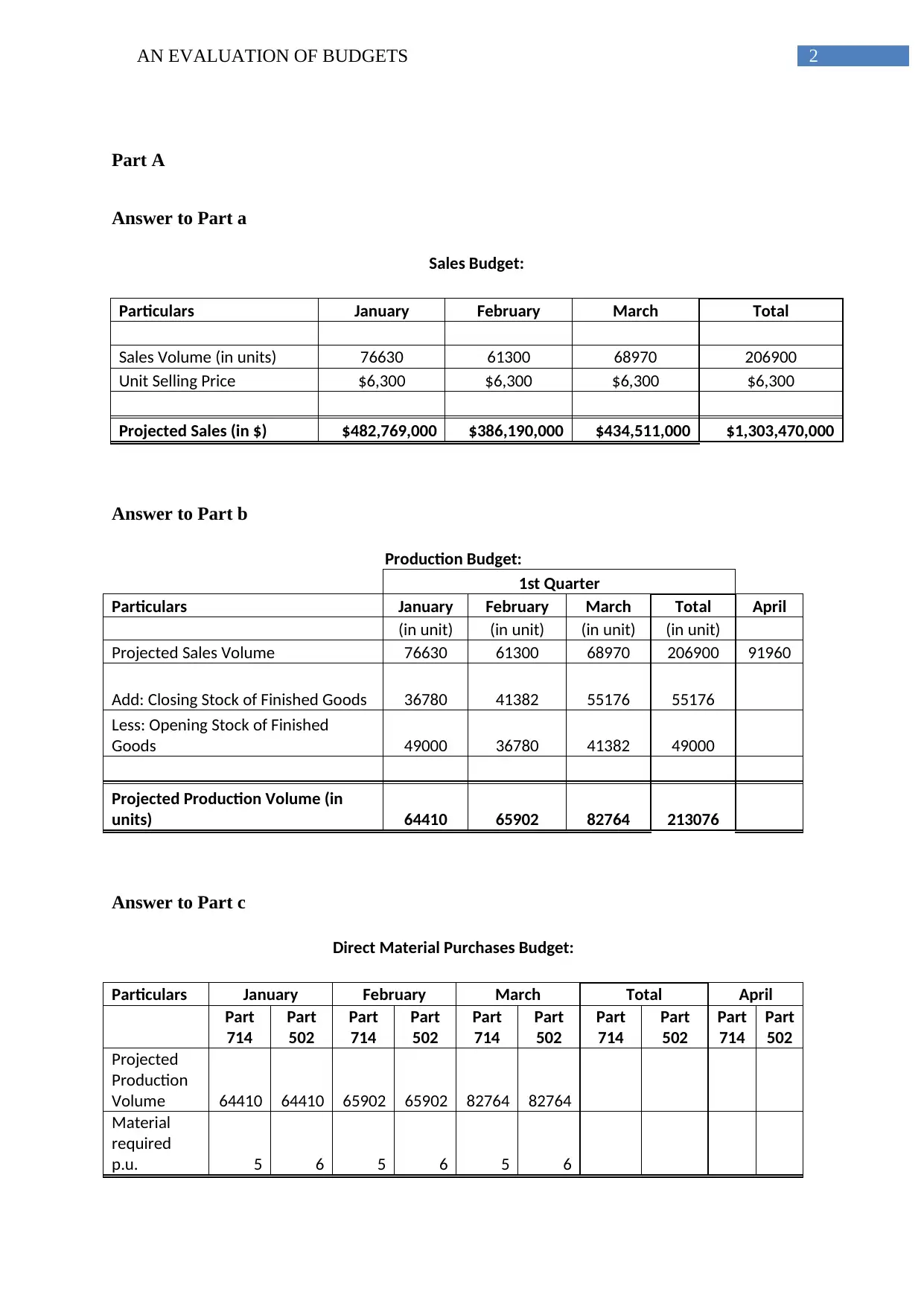

Part A

Answer to Part a

Sales Budget:

Particulars January February March Total

Sales Volume (in units) 76630 61300 68970 206900

Unit Selling Price $6,300 $6,300 $6,300 $6,300

Projected Sales (in $) $482,769,000 $386,190,000 $434,511,000 $1,303,470,000

Answer to Part b

Production Budget:

1st Quarter

Particulars January February March Total April

(in unit) (in unit) (in unit) (in unit)

Projected Sales Volume 76630 61300 68970 206900 91960

Add: Closing Stock of Finished Goods 36780 41382 55176 55176

Less: Opening Stock of Finished

Goods 49000 36780 41382 49000

Projected Production Volume (in

units) 64410 65902 82764 213076

Answer to Part c

Direct Material Purchases Budget:

Particulars January February March Total April

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Projected

Production

Volume 64410 64410 65902 65902 82764 82764

Material

required

p.u. 5 6 5 6 5 6

Part A

Answer to Part a

Sales Budget:

Particulars January February March Total

Sales Volume (in units) 76630 61300 68970 206900

Unit Selling Price $6,300 $6,300 $6,300 $6,300

Projected Sales (in $) $482,769,000 $386,190,000 $434,511,000 $1,303,470,000

Answer to Part b

Production Budget:

1st Quarter

Particulars January February March Total April

(in unit) (in unit) (in unit) (in unit)

Projected Sales Volume 76630 61300 68970 206900 91960

Add: Closing Stock of Finished Goods 36780 41382 55176 55176

Less: Opening Stock of Finished

Goods 49000 36780 41382 49000

Projected Production Volume (in

units) 64410 65902 82764 213076

Answer to Part c

Direct Material Purchases Budget:

Particulars January February March Total April

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Projected

Production

Volume 64410 64410 65902 65902 82764 82764

Material

required

p.u. 5 6 5 6 5 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AN EVALUATION OF BUDGETS

Total

Material

Required

32205

0

38646

0

32951

0

39541

2

41382

0

49658

4

10653

80

12784

56

Add: Closing

Stock of

Raw

Materials 61300 73560 68970 82764 91960

11035

2 91960

11035

2

Less:

Opening

Stock of

Raw

Material 76630 91956 61300 73560 68970 82764 76630 91956

Direct

Material

Purchased

(in units)

30672

0

36806

4

33718

0

40461

6

43681

0

52417

2

10807

10

12968

52

Material

Cost p.u. $92 $123 $92 $123 $92 $123 $92 $123

Projected

Direct

Material

Purchased

$28,2

18,24

0

$45,2

71,87

2

$31,0

20,56

0

$49,7

67,76

8

$40,1

86,52

0

$64,4

73,15

6

$99,4

25,32

0

$159,5

12,796

Answer to Part d

Direct Labor Budget:

1st Quarter

Particulars January February March Total

(in unit) (in unit) (in unit) (in unit)

Projected Production 64410 65902 82764 213076

Direct Labor Hours p.u. 9 9 9 9

Total Direct Labor Hours 579690 593118 744876 1917684

Direct Labor Cost per hour $50 $50 $50 $50

Budgeted Direct Labor Cost $28,984,500 $29,655,900 $37,243,800 $95,884,200

Answer to Part e

Manufacturing Overhead Budget

1st Quarter

Particulars January February March Total

Total

Material

Required

32205

0

38646

0

32951

0

39541

2

41382

0

49658

4

10653

80

12784

56

Add: Closing

Stock of

Raw

Materials 61300 73560 68970 82764 91960

11035

2 91960

11035

2

Less:

Opening

Stock of

Raw

Material 76630 91956 61300 73560 68970 82764 76630 91956

Direct

Material

Purchased

(in units)

30672

0

36806

4

33718

0

40461

6

43681

0

52417

2

10807

10

12968

52

Material

Cost p.u. $92 $123 $92 $123 $92 $123 $92 $123

Projected

Direct

Material

Purchased

$28,2

18,24

0

$45,2

71,87

2

$31,0

20,56

0

$49,7

67,76

8

$40,1

86,52

0

$64,4

73,15

6

$99,4

25,32

0

$159,5

12,796

Answer to Part d

Direct Labor Budget:

1st Quarter

Particulars January February March Total

(in unit) (in unit) (in unit) (in unit)

Projected Production 64410 65902 82764 213076

Direct Labor Hours p.u. 9 9 9 9

Total Direct Labor Hours 579690 593118 744876 1917684

Direct Labor Cost per hour $50 $50 $50 $50

Budgeted Direct Labor Cost $28,984,500 $29,655,900 $37,243,800 $95,884,200

Answer to Part e

Manufacturing Overhead Budget

1st Quarter

Particulars January February March Total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AN EVALUATION OF BUDGETS

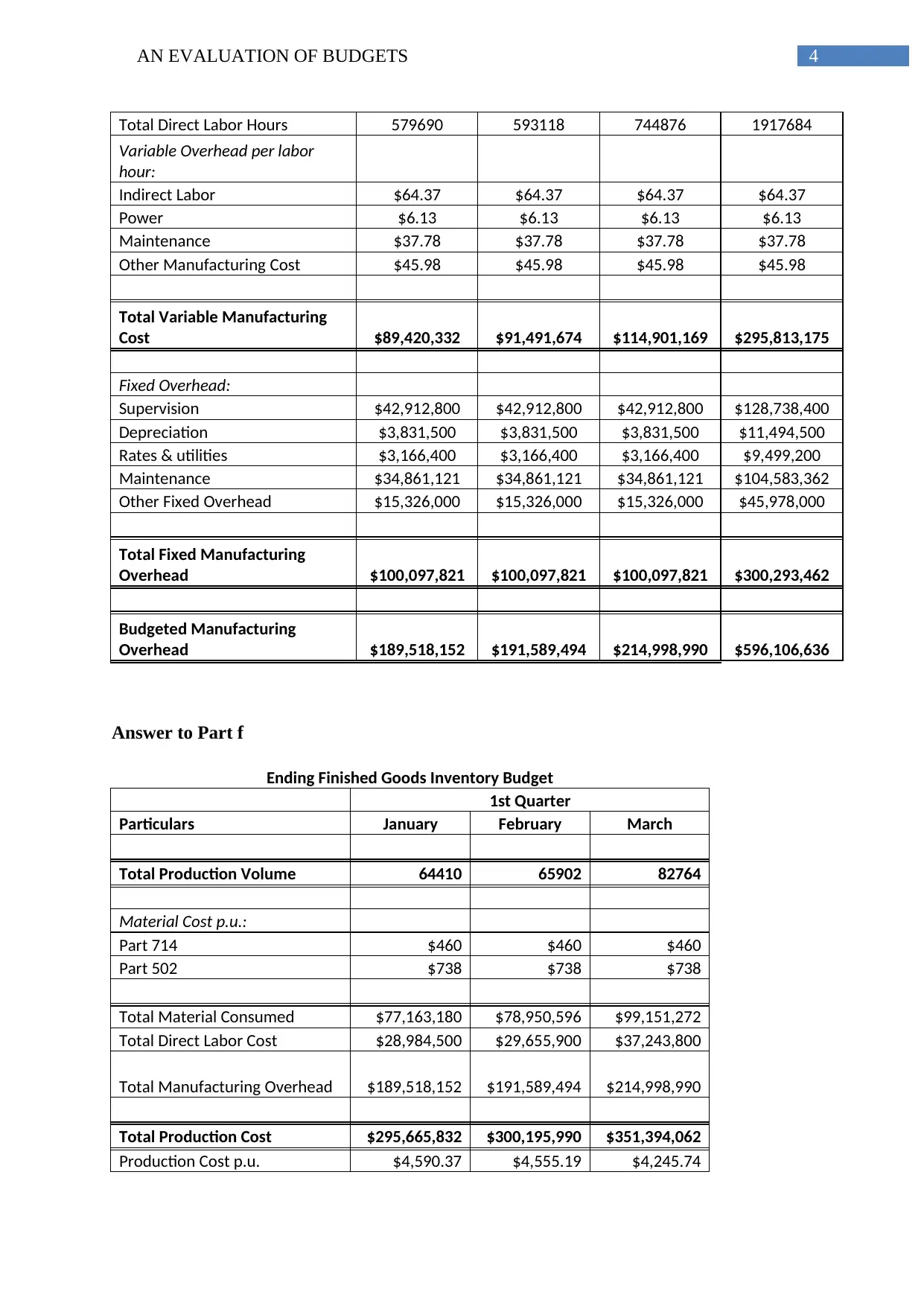

Total Direct Labor Hours 579690 593118 744876 1917684

Variable Overhead per labor

hour:

Indirect Labor $64.37 $64.37 $64.37 $64.37

Power $6.13 $6.13 $6.13 $6.13

Maintenance $37.78 $37.78 $37.78 $37.78

Other Manufacturing Cost $45.98 $45.98 $45.98 $45.98

Total Variable Manufacturing

Cost $89,420,332 $91,491,674 $114,901,169 $295,813,175

Fixed Overhead:

Supervision $42,912,800 $42,912,800 $42,912,800 $128,738,400

Depreciation $3,831,500 $3,831,500 $3,831,500 $11,494,500

Rates & utilities $3,166,400 $3,166,400 $3,166,400 $9,499,200

Maintenance $34,861,121 $34,861,121 $34,861,121 $104,583,362

Other Fixed Overhead $15,326,000 $15,326,000 $15,326,000 $45,978,000

Total Fixed Manufacturing

Overhead $100,097,821 $100,097,821 $100,097,821 $300,293,462

Budgeted Manufacturing

Overhead $189,518,152 $191,589,494 $214,998,990 $596,106,636

Answer to Part f

Ending Finished Goods Inventory Budget

1st Quarter

Particulars January February March

Total Production Volume 64410 65902 82764

Material Cost p.u.:

Part 714 $460 $460 $460

Part 502 $738 $738 $738

Total Material Consumed $77,163,180 $78,950,596 $99,151,272

Total Direct Labor Cost $28,984,500 $29,655,900 $37,243,800

Total Manufacturing Overhead $189,518,152 $191,589,494 $214,998,990

Total Production Cost $295,665,832 $300,195,990 $351,394,062

Production Cost p.u. $4,590.37 $4,555.19 $4,245.74

Total Direct Labor Hours 579690 593118 744876 1917684

Variable Overhead per labor

hour:

Indirect Labor $64.37 $64.37 $64.37 $64.37

Power $6.13 $6.13 $6.13 $6.13

Maintenance $37.78 $37.78 $37.78 $37.78

Other Manufacturing Cost $45.98 $45.98 $45.98 $45.98

Total Variable Manufacturing

Cost $89,420,332 $91,491,674 $114,901,169 $295,813,175

Fixed Overhead:

Supervision $42,912,800 $42,912,800 $42,912,800 $128,738,400

Depreciation $3,831,500 $3,831,500 $3,831,500 $11,494,500

Rates & utilities $3,166,400 $3,166,400 $3,166,400 $9,499,200

Maintenance $34,861,121 $34,861,121 $34,861,121 $104,583,362

Other Fixed Overhead $15,326,000 $15,326,000 $15,326,000 $45,978,000

Total Fixed Manufacturing

Overhead $100,097,821 $100,097,821 $100,097,821 $300,293,462

Budgeted Manufacturing

Overhead $189,518,152 $191,589,494 $214,998,990 $596,106,636

Answer to Part f

Ending Finished Goods Inventory Budget

1st Quarter

Particulars January February March

Total Production Volume 64410 65902 82764

Material Cost p.u.:

Part 714 $460 $460 $460

Part 502 $738 $738 $738

Total Material Consumed $77,163,180 $78,950,596 $99,151,272

Total Direct Labor Cost $28,984,500 $29,655,900 $37,243,800

Total Manufacturing Overhead $189,518,152 $191,589,494 $214,998,990

Total Production Cost $295,665,832 $300,195,990 $351,394,062

Production Cost p.u. $4,590.37 $4,555.19 $4,245.74

5AN EVALUATION OF BUDGETS

Ending Finished Goods

Inventory 36780 41382 55176

Budgeted Finished Goods

Inventory $168,833,866 $188,502,784 $234,262,708

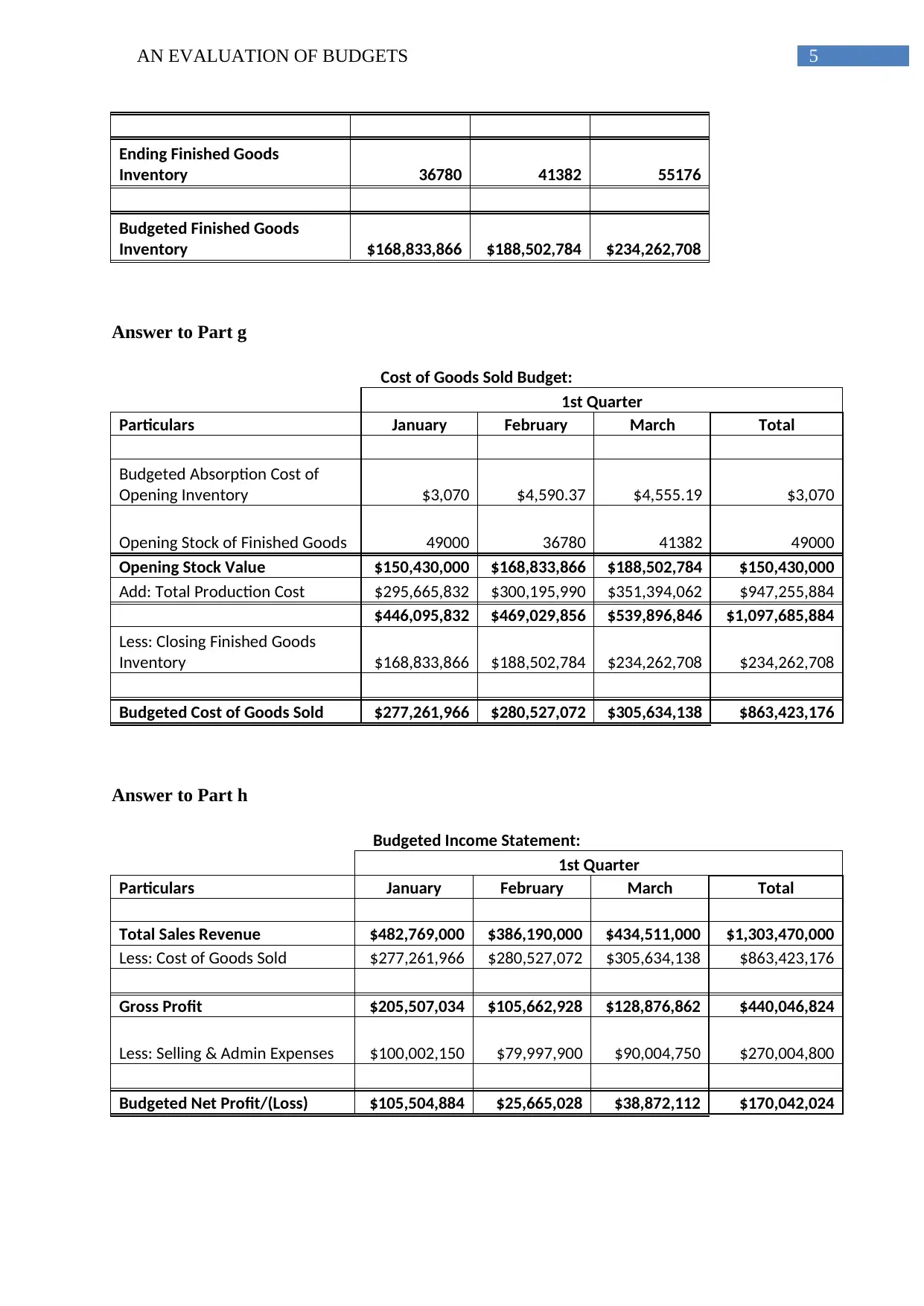

Answer to Part g

Cost of Goods Sold Budget:

1st Quarter

Particulars January February March Total

Budgeted Absorption Cost of

Opening Inventory $3,070 $4,590.37 $4,555.19 $3,070

Opening Stock of Finished Goods 49000 36780 41382 49000

Opening Stock Value $150,430,000 $168,833,866 $188,502,784 $150,430,000

Add: Total Production Cost $295,665,832 $300,195,990 $351,394,062 $947,255,884

$446,095,832 $469,029,856 $539,896,846 $1,097,685,884

Less: Closing Finished Goods

Inventory $168,833,866 $188,502,784 $234,262,708 $234,262,708

Budgeted Cost of Goods Sold $277,261,966 $280,527,072 $305,634,138 $863,423,176

Answer to Part h

Budgeted Income Statement:

1st Quarter

Particulars January February March Total

Total Sales Revenue $482,769,000 $386,190,000 $434,511,000 $1,303,470,000

Less: Cost of Goods Sold $277,261,966 $280,527,072 $305,634,138 $863,423,176

Gross Profit $205,507,034 $105,662,928 $128,876,862 $440,046,824

Less: Selling & Admin Expenses $100,002,150 $79,997,900 $90,004,750 $270,004,800

Budgeted Net Profit/(Loss) $105,504,884 $25,665,028 $38,872,112 $170,042,024

Ending Finished Goods

Inventory 36780 41382 55176

Budgeted Finished Goods

Inventory $168,833,866 $188,502,784 $234,262,708

Answer to Part g

Cost of Goods Sold Budget:

1st Quarter

Particulars January February March Total

Budgeted Absorption Cost of

Opening Inventory $3,070 $4,590.37 $4,555.19 $3,070

Opening Stock of Finished Goods 49000 36780 41382 49000

Opening Stock Value $150,430,000 $168,833,866 $188,502,784 $150,430,000

Add: Total Production Cost $295,665,832 $300,195,990 $351,394,062 $947,255,884

$446,095,832 $469,029,856 $539,896,846 $1,097,685,884

Less: Closing Finished Goods

Inventory $168,833,866 $188,502,784 $234,262,708 $234,262,708

Budgeted Cost of Goods Sold $277,261,966 $280,527,072 $305,634,138 $863,423,176

Answer to Part h

Budgeted Income Statement:

1st Quarter

Particulars January February March Total

Total Sales Revenue $482,769,000 $386,190,000 $434,511,000 $1,303,470,000

Less: Cost of Goods Sold $277,261,966 $280,527,072 $305,634,138 $863,423,176

Gross Profit $205,507,034 $105,662,928 $128,876,862 $440,046,824

Less: Selling & Admin Expenses $100,002,150 $79,997,900 $90,004,750 $270,004,800

Budgeted Net Profit/(Loss) $105,504,884 $25,665,028 $38,872,112 $170,042,024

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AN EVALUATION OF BUDGETS

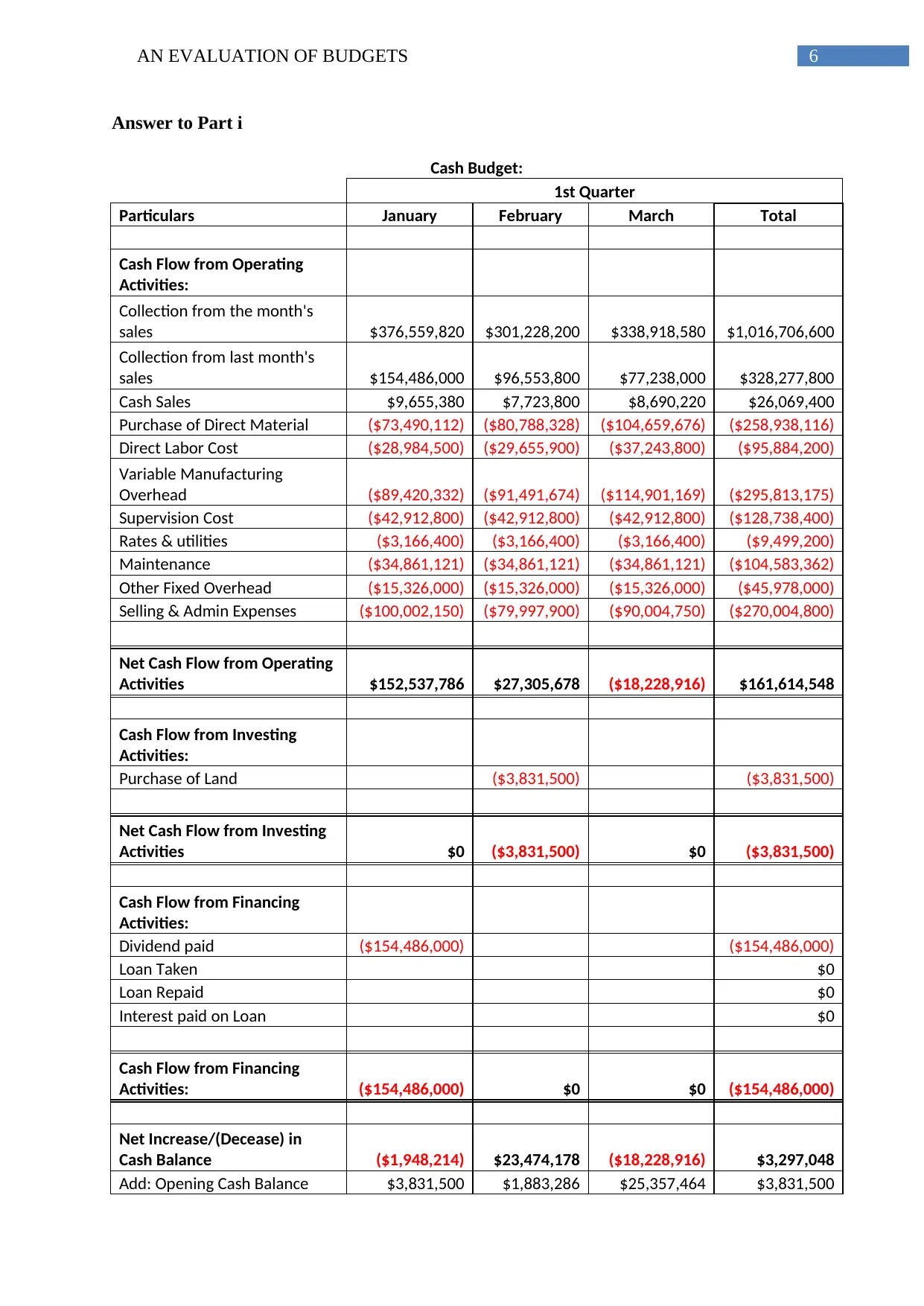

Answer to Part i

Cash Budget:

1st Quarter

Particulars January February March Total

Cash Flow from Operating

Activities:

Collection from the month's

sales $376,559,820 $301,228,200 $338,918,580 $1,016,706,600

Collection from last month's

sales $154,486,000 $96,553,800 $77,238,000 $328,277,800

Cash Sales $9,655,380 $7,723,800 $8,690,220 $26,069,400

Purchase of Direct Material ($73,490,112) ($80,788,328) ($104,659,676) ($258,938,116)

Direct Labor Cost ($28,984,500) ($29,655,900) ($37,243,800) ($95,884,200)

Variable Manufacturing

Overhead ($89,420,332) ($91,491,674) ($114,901,169) ($295,813,175)

Supervision Cost ($42,912,800) ($42,912,800) ($42,912,800) ($128,738,400)

Rates & utilities ($3,166,400) ($3,166,400) ($3,166,400) ($9,499,200)

Maintenance ($34,861,121) ($34,861,121) ($34,861,121) ($104,583,362)

Other Fixed Overhead ($15,326,000) ($15,326,000) ($15,326,000) ($45,978,000)

Selling & Admin Expenses ($100,002,150) ($79,997,900) ($90,004,750) ($270,004,800)

Net Cash Flow from Operating

Activities $152,537,786 $27,305,678 ($18,228,916) $161,614,548

Cash Flow from Investing

Activities:

Purchase of Land ($3,831,500) ($3,831,500)

Net Cash Flow from Investing

Activities $0 ($3,831,500) $0 ($3,831,500)

Cash Flow from Financing

Activities:

Dividend paid ($154,486,000) ($154,486,000)

Loan Taken $0

Loan Repaid $0

Interest paid on Loan $0

Cash Flow from Financing

Activities: ($154,486,000) $0 $0 ($154,486,000)

Net Increase/(Decease) in

Cash Balance ($1,948,214) $23,474,178 ($18,228,916) $3,297,048

Add: Opening Cash Balance $3,831,500 $1,883,286 $25,357,464 $3,831,500

Answer to Part i

Cash Budget:

1st Quarter

Particulars January February March Total

Cash Flow from Operating

Activities:

Collection from the month's

sales $376,559,820 $301,228,200 $338,918,580 $1,016,706,600

Collection from last month's

sales $154,486,000 $96,553,800 $77,238,000 $328,277,800

Cash Sales $9,655,380 $7,723,800 $8,690,220 $26,069,400

Purchase of Direct Material ($73,490,112) ($80,788,328) ($104,659,676) ($258,938,116)

Direct Labor Cost ($28,984,500) ($29,655,900) ($37,243,800) ($95,884,200)

Variable Manufacturing

Overhead ($89,420,332) ($91,491,674) ($114,901,169) ($295,813,175)

Supervision Cost ($42,912,800) ($42,912,800) ($42,912,800) ($128,738,400)

Rates & utilities ($3,166,400) ($3,166,400) ($3,166,400) ($9,499,200)

Maintenance ($34,861,121) ($34,861,121) ($34,861,121) ($104,583,362)

Other Fixed Overhead ($15,326,000) ($15,326,000) ($15,326,000) ($45,978,000)

Selling & Admin Expenses ($100,002,150) ($79,997,900) ($90,004,750) ($270,004,800)

Net Cash Flow from Operating

Activities $152,537,786 $27,305,678 ($18,228,916) $161,614,548

Cash Flow from Investing

Activities:

Purchase of Land ($3,831,500) ($3,831,500)

Net Cash Flow from Investing

Activities $0 ($3,831,500) $0 ($3,831,500)

Cash Flow from Financing

Activities:

Dividend paid ($154,486,000) ($154,486,000)

Loan Taken $0

Loan Repaid $0

Interest paid on Loan $0

Cash Flow from Financing

Activities: ($154,486,000) $0 $0 ($154,486,000)

Net Increase/(Decease) in

Cash Balance ($1,948,214) $23,474,178 ($18,228,916) $3,297,048

Add: Opening Cash Balance $3,831,500 $1,883,286 $25,357,464 $3,831,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AN EVALUATION OF BUDGETS

Closing Balance $1,883,286 $25,357,464 $7,128,548 $7,128,548

Workings

Total Opening & Closing Raw Material Inventory:

Particulars January February March April

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Total Sales Volume 76630 76630 61300 61300 68970 68970 91960 91960

Material Required

p.u. 5 6 5 6 5 6 5 6

Stock Maintaining

Level 20% 20% 20% 20% 20% 20% 20% 20%

Opening Stock 76630 91956 61300 73560 68970 82764 91960

11035

2

Closing Stock 61300 73560 68970 82764 91960

11035

2

Fixed & Variable Maintenance Cost:

Direct Labor Hours

Total

Maintenance

Cost

1479000 $90,729,900

1685900 $98,546,200

1547900 $93,335,300

1410000 $88,124,500

Variable Maintenance Cost

per hour $37.78

Fixed Maintenance Cost $34,861,121

Part B

Particulars

Without New

Facility

% of

Total

Cost

With New

Facility

% of

Total

Cost

Varianc

e Remarks

Closing Balance $1,883,286 $25,357,464 $7,128,548 $7,128,548

Workings

Total Opening & Closing Raw Material Inventory:

Particulars January February March April

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Part

714

Part

502

Total Sales Volume 76630 76630 61300 61300 68970 68970 91960 91960

Material Required

p.u. 5 6 5 6 5 6 5 6

Stock Maintaining

Level 20% 20% 20% 20% 20% 20% 20% 20%

Opening Stock 76630 91956 61300 73560 68970 82764 91960

11035

2

Closing Stock 61300 73560 68970 82764 91960

11035

2

Fixed & Variable Maintenance Cost:

Direct Labor Hours

Total

Maintenance

Cost

1479000 $90,729,900

1685900 $98,546,200

1547900 $93,335,300

1410000 $88,124,500

Variable Maintenance Cost

per hour $37.78

Fixed Maintenance Cost $34,861,121

Part B

Particulars

Without New

Facility

% of

Total

Cost

With New

Facility

% of

Total

Cost

Varianc

e Remarks

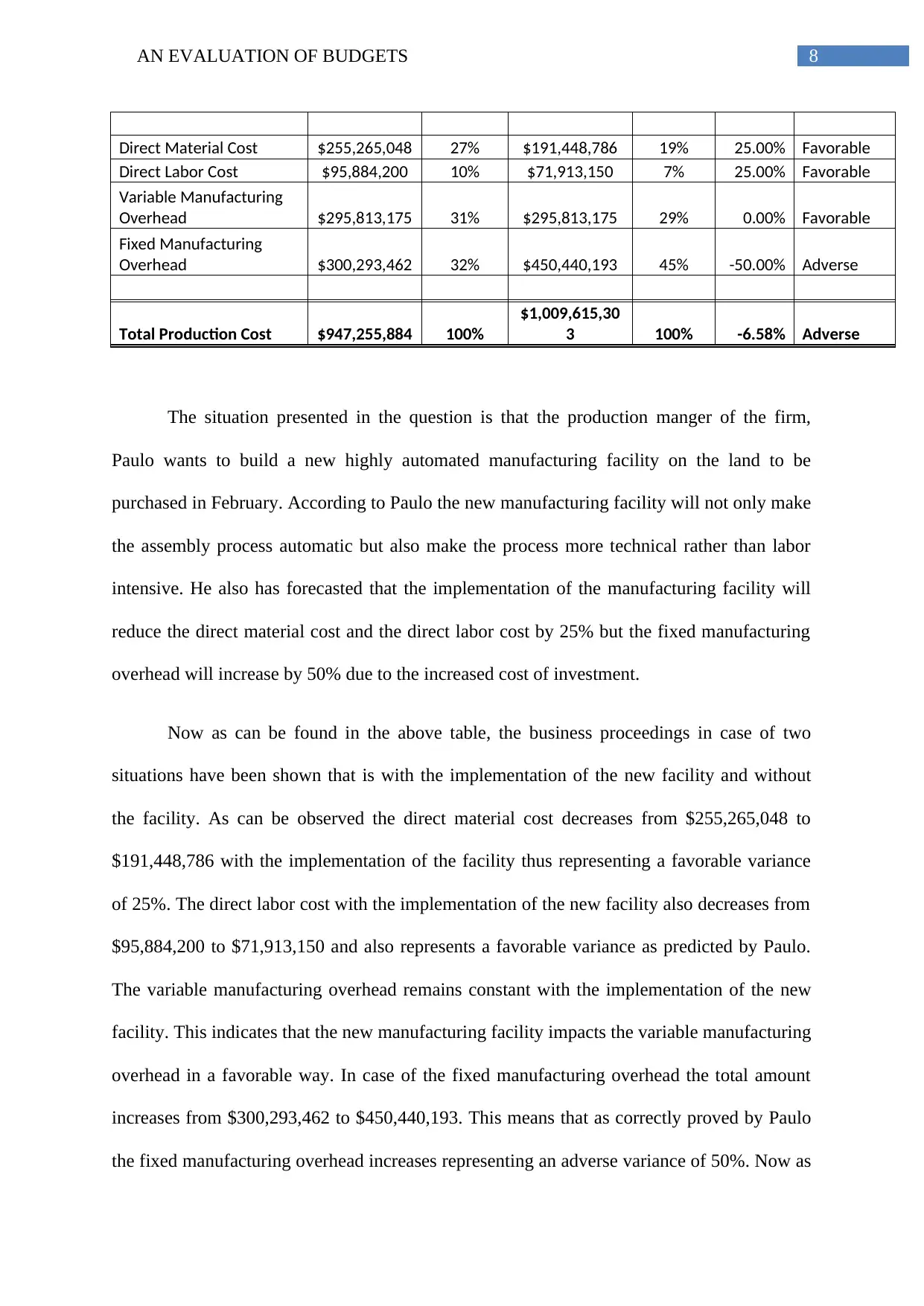

8AN EVALUATION OF BUDGETS

Direct Material Cost $255,265,048 27% $191,448,786 19% 25.00% Favorable

Direct Labor Cost $95,884,200 10% $71,913,150 7% 25.00% Favorable

Variable Manufacturing

Overhead $295,813,175 31% $295,813,175 29% 0.00% Favorable

Fixed Manufacturing

Overhead $300,293,462 32% $450,440,193 45% -50.00% Adverse

Total Production Cost $947,255,884 100%

$1,009,615,30

3 100% -6.58% Adverse

The situation presented in the question is that the production manger of the firm,

Paulo wants to build a new highly automated manufacturing facility on the land to be

purchased in February. According to Paulo the new manufacturing facility will not only make

the assembly process automatic but also make the process more technical rather than labor

intensive. He also has forecasted that the implementation of the manufacturing facility will

reduce the direct material cost and the direct labor cost by 25% but the fixed manufacturing

overhead will increase by 50% due to the increased cost of investment.

Now as can be found in the above table, the business proceedings in case of two

situations have been shown that is with the implementation of the new facility and without

the facility. As can be observed the direct material cost decreases from $255,265,048 to

$191,448,786 with the implementation of the facility thus representing a favorable variance

of 25%. The direct labor cost with the implementation of the new facility also decreases from

$95,884,200 to $71,913,150 and also represents a favorable variance as predicted by Paulo.

The variable manufacturing overhead remains constant with the implementation of the new

facility. This indicates that the new manufacturing facility impacts the variable manufacturing

overhead in a favorable way. In case of the fixed manufacturing overhead the total amount

increases from $300,293,462 to $450,440,193. This means that as correctly proved by Paulo

the fixed manufacturing overhead increases representing an adverse variance of 50%. Now as

Direct Material Cost $255,265,048 27% $191,448,786 19% 25.00% Favorable

Direct Labor Cost $95,884,200 10% $71,913,150 7% 25.00% Favorable

Variable Manufacturing

Overhead $295,813,175 31% $295,813,175 29% 0.00% Favorable

Fixed Manufacturing

Overhead $300,293,462 32% $450,440,193 45% -50.00% Adverse

Total Production Cost $947,255,884 100%

$1,009,615,30

3 100% -6.58% Adverse

The situation presented in the question is that the production manger of the firm,

Paulo wants to build a new highly automated manufacturing facility on the land to be

purchased in February. According to Paulo the new manufacturing facility will not only make

the assembly process automatic but also make the process more technical rather than labor

intensive. He also has forecasted that the implementation of the manufacturing facility will

reduce the direct material cost and the direct labor cost by 25% but the fixed manufacturing

overhead will increase by 50% due to the increased cost of investment.

Now as can be found in the above table, the business proceedings in case of two

situations have been shown that is with the implementation of the new facility and without

the facility. As can be observed the direct material cost decreases from $255,265,048 to

$191,448,786 with the implementation of the facility thus representing a favorable variance

of 25%. The direct labor cost with the implementation of the new facility also decreases from

$95,884,200 to $71,913,150 and also represents a favorable variance as predicted by Paulo.

The variable manufacturing overhead remains constant with the implementation of the new

facility. This indicates that the new manufacturing facility impacts the variable manufacturing

overhead in a favorable way. In case of the fixed manufacturing overhead the total amount

increases from $300,293,462 to $450,440,193. This means that as correctly proved by Paulo

the fixed manufacturing overhead increases representing an adverse variance of 50%. Now as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AN EVALUATION OF BUDGETS

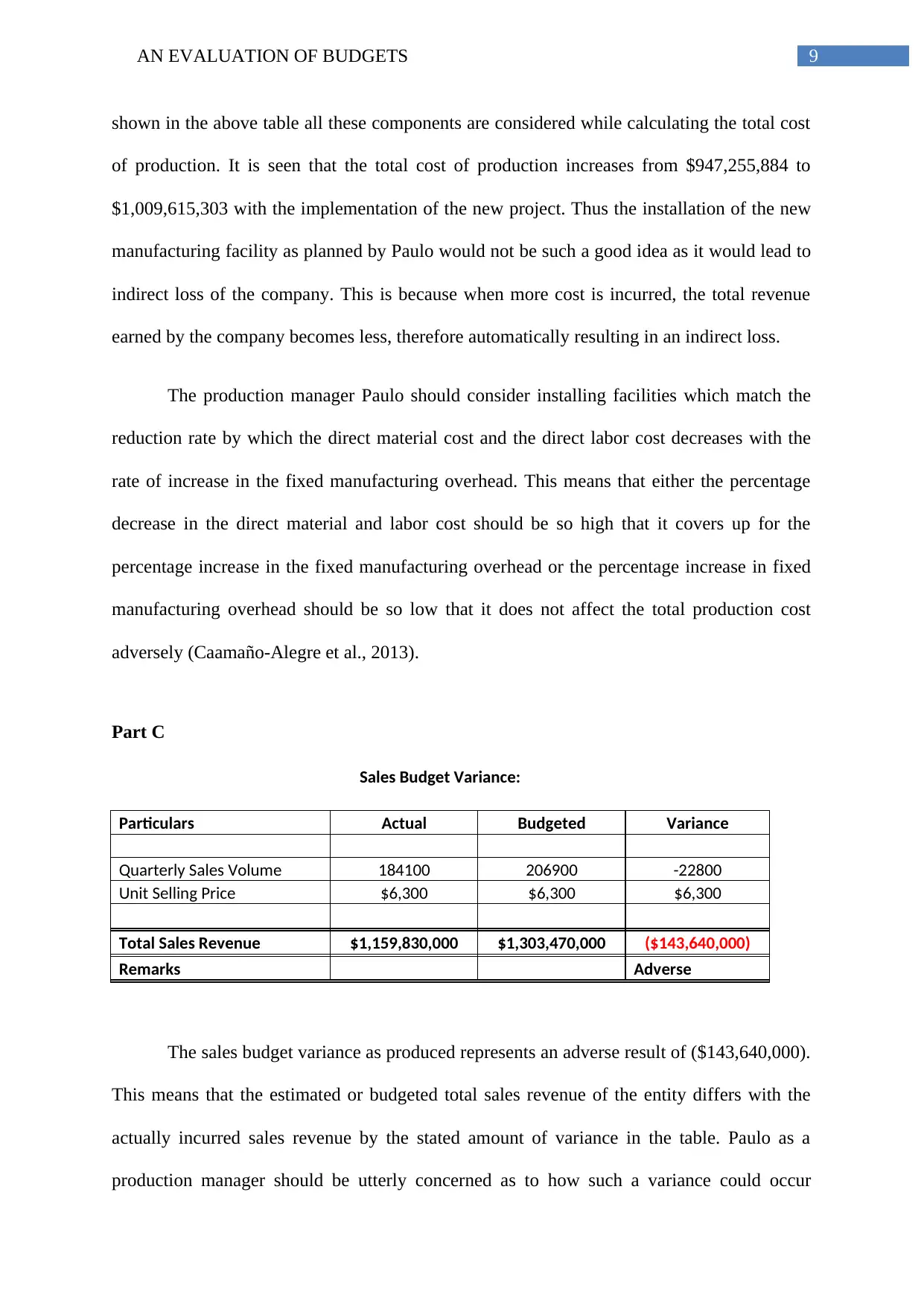

shown in the above table all these components are considered while calculating the total cost

of production. It is seen that the total cost of production increases from $947,255,884 to

$1,009,615,303 with the implementation of the new project. Thus the installation of the new

manufacturing facility as planned by Paulo would not be such a good idea as it would lead to

indirect loss of the company. This is because when more cost is incurred, the total revenue

earned by the company becomes less, therefore automatically resulting in an indirect loss.

The production manager Paulo should consider installing facilities which match the

reduction rate by which the direct material cost and the direct labor cost decreases with the

rate of increase in the fixed manufacturing overhead. This means that either the percentage

decrease in the direct material and labor cost should be so high that it covers up for the

percentage increase in the fixed manufacturing overhead or the percentage increase in fixed

manufacturing overhead should be so low that it does not affect the total production cost

adversely (Caamaño-Alegre et al., 2013).

Part C

Sales Budget Variance:

Particulars Actual Budgeted Variance

Quarterly Sales Volume 184100 206900 -22800

Unit Selling Price $6,300 $6,300 $6,300

Total Sales Revenue $1,159,830,000 $1,303,470,000 ($143,640,000)

Remarks Adverse

The sales budget variance as produced represents an adverse result of ($143,640,000).

This means that the estimated or budgeted total sales revenue of the entity differs with the

actually incurred sales revenue by the stated amount of variance in the table. Paulo as a

production manager should be utterly concerned as to how such a variance could occur

shown in the above table all these components are considered while calculating the total cost

of production. It is seen that the total cost of production increases from $947,255,884 to

$1,009,615,303 with the implementation of the new project. Thus the installation of the new

manufacturing facility as planned by Paulo would not be such a good idea as it would lead to

indirect loss of the company. This is because when more cost is incurred, the total revenue

earned by the company becomes less, therefore automatically resulting in an indirect loss.

The production manager Paulo should consider installing facilities which match the

reduction rate by which the direct material cost and the direct labor cost decreases with the

rate of increase in the fixed manufacturing overhead. This means that either the percentage

decrease in the direct material and labor cost should be so high that it covers up for the

percentage increase in the fixed manufacturing overhead or the percentage increase in fixed

manufacturing overhead should be so low that it does not affect the total production cost

adversely (Caamaño-Alegre et al., 2013).

Part C

Sales Budget Variance:

Particulars Actual Budgeted Variance

Quarterly Sales Volume 184100 206900 -22800

Unit Selling Price $6,300 $6,300 $6,300

Total Sales Revenue $1,159,830,000 $1,303,470,000 ($143,640,000)

Remarks Adverse

The sales budget variance as produced represents an adverse result of ($143,640,000).

This means that the estimated or budgeted total sales revenue of the entity differs with the

actually incurred sales revenue by the stated amount of variance in the table. Paulo as a

production manager should be utterly concerned as to how such a variance could occur

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AN EVALUATION OF BUDGETS

between the predicted and the actual figure incurred. This may be due to reasons like a fall in

the general market price or change in the pattern of the tastes and preferences of the

consumers or sudden increase in the number of competitors in business resulting in fall in the

total amount of sales because the consumers are now provided with a whole lot of choices in

the same domain of products (DRURY 2013).

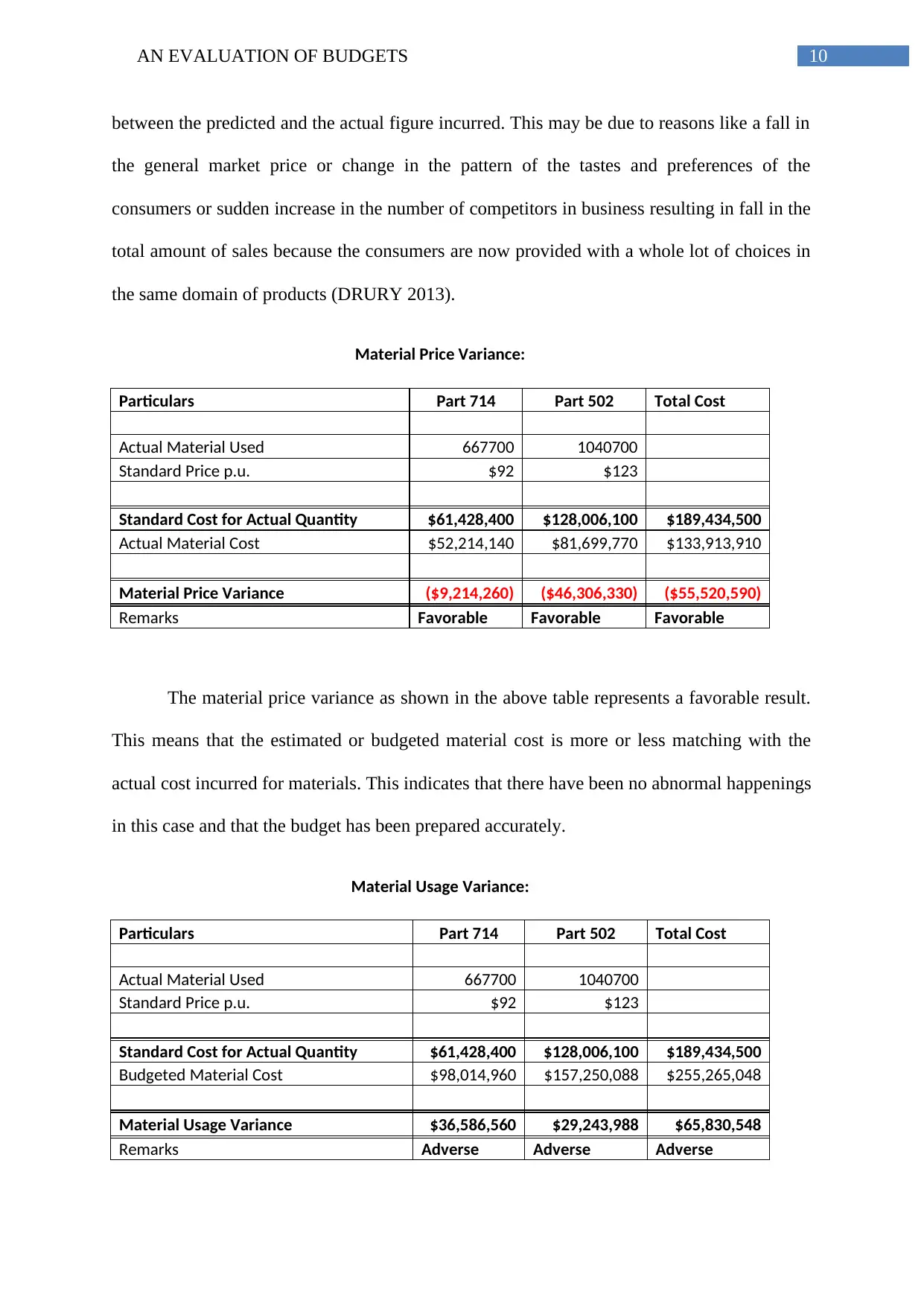

Material Price Variance:

Particulars Part 714 Part 502 Total Cost

Actual Material Used 667700 1040700

Standard Price p.u. $92 $123

Standard Cost for Actual Quantity $61,428,400 $128,006,100 $189,434,500

Actual Material Cost $52,214,140 $81,699,770 $133,913,910

Material Price Variance ($9,214,260) ($46,306,330) ($55,520,590)

Remarks Favorable Favorable Favorable

The material price variance as shown in the above table represents a favorable result.

This means that the estimated or budgeted material cost is more or less matching with the

actual cost incurred for materials. This indicates that there have been no abnormal happenings

in this case and that the budget has been prepared accurately.

Material Usage Variance:

Particulars Part 714 Part 502 Total Cost

Actual Material Used 667700 1040700

Standard Price p.u. $92 $123

Standard Cost for Actual Quantity $61,428,400 $128,006,100 $189,434,500

Budgeted Material Cost $98,014,960 $157,250,088 $255,265,048

Material Usage Variance $36,586,560 $29,243,988 $65,830,548

Remarks Adverse Adverse Adverse

between the predicted and the actual figure incurred. This may be due to reasons like a fall in

the general market price or change in the pattern of the tastes and preferences of the

consumers or sudden increase in the number of competitors in business resulting in fall in the

total amount of sales because the consumers are now provided with a whole lot of choices in

the same domain of products (DRURY 2013).

Material Price Variance:

Particulars Part 714 Part 502 Total Cost

Actual Material Used 667700 1040700

Standard Price p.u. $92 $123

Standard Cost for Actual Quantity $61,428,400 $128,006,100 $189,434,500

Actual Material Cost $52,214,140 $81,699,770 $133,913,910

Material Price Variance ($9,214,260) ($46,306,330) ($55,520,590)

Remarks Favorable Favorable Favorable

The material price variance as shown in the above table represents a favorable result.

This means that the estimated or budgeted material cost is more or less matching with the

actual cost incurred for materials. This indicates that there have been no abnormal happenings

in this case and that the budget has been prepared accurately.

Material Usage Variance:

Particulars Part 714 Part 502 Total Cost

Actual Material Used 667700 1040700

Standard Price p.u. $92 $123

Standard Cost for Actual Quantity $61,428,400 $128,006,100 $189,434,500

Budgeted Material Cost $98,014,960 $157,250,088 $255,265,048

Material Usage Variance $36,586,560 $29,243,988 $65,830,548

Remarks Adverse Adverse Adverse

11AN EVALUATION OF BUDGETS

The material usage variance as shown in the above table represents an adverse

outcome. This means that in case of material usage estimations, there must have been some

error committed on the part of the management. The term material usage refers to the

quantity of materials to be used by the company which has already been stipulated by the

management of the company. Now in case of disparity between the budgeted and the actual

figures, Paulo should investigate and identify as where are the exact points where materials

more than that was stipulated was used and the reasons behind it. He should also check the

budget for any error or disproportions (Hofstede 2012).

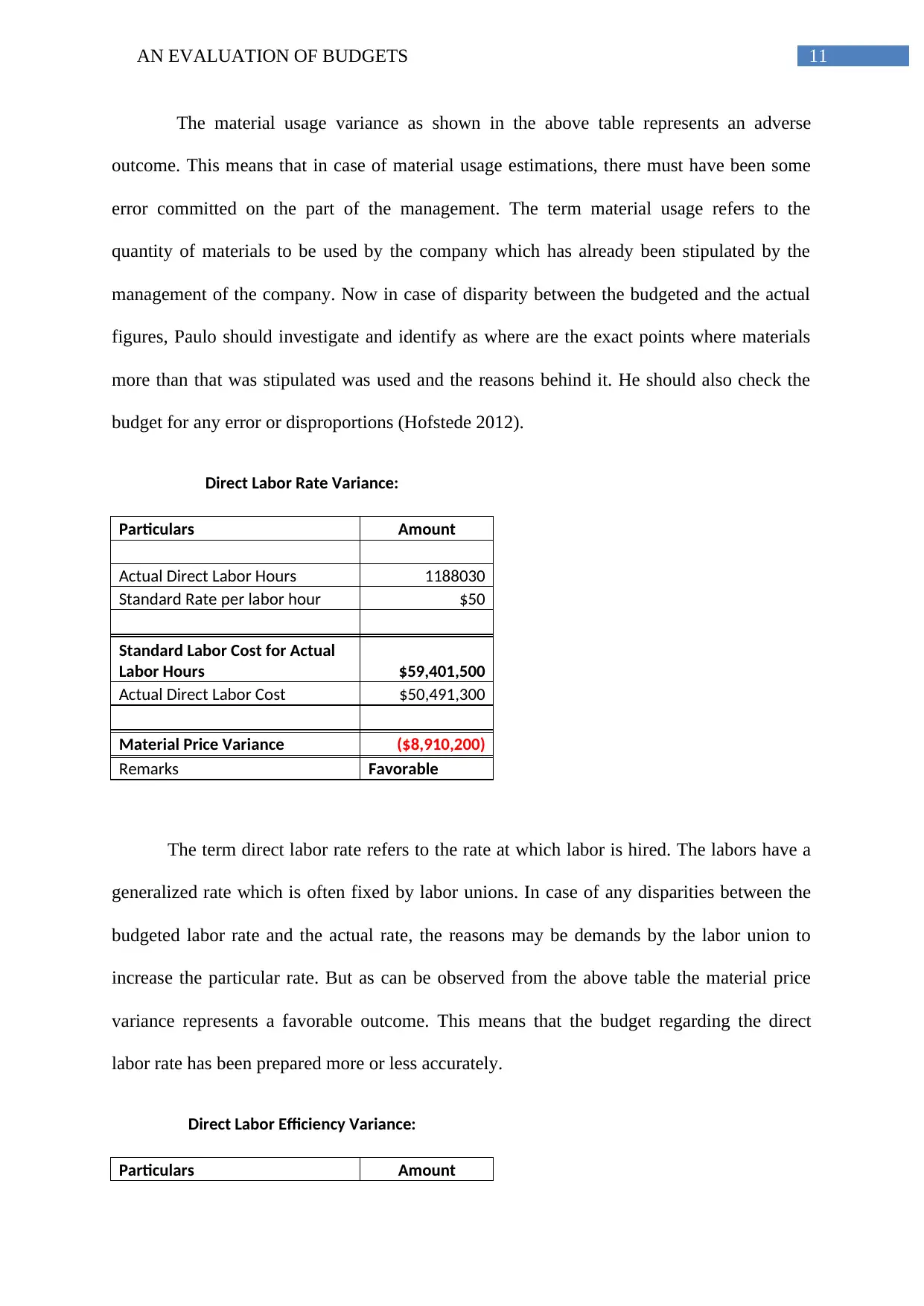

Direct Labor Rate Variance:

Particulars Amount

Actual Direct Labor Hours 1188030

Standard Rate per labor hour $50

Standard Labor Cost for Actual

Labor Hours $59,401,500

Actual Direct Labor Cost $50,491,300

Material Price Variance ($8,910,200)

Remarks Favorable

The term direct labor rate refers to the rate at which labor is hired. The labors have a

generalized rate which is often fixed by labor unions. In case of any disparities between the

budgeted labor rate and the actual rate, the reasons may be demands by the labor union to

increase the particular rate. But as can be observed from the above table the material price

variance represents a favorable outcome. This means that the budget regarding the direct

labor rate has been prepared more or less accurately.

Direct Labor Efficiency Variance:

Particulars Amount

The material usage variance as shown in the above table represents an adverse

outcome. This means that in case of material usage estimations, there must have been some

error committed on the part of the management. The term material usage refers to the

quantity of materials to be used by the company which has already been stipulated by the

management of the company. Now in case of disparity between the budgeted and the actual

figures, Paulo should investigate and identify as where are the exact points where materials

more than that was stipulated was used and the reasons behind it. He should also check the

budget for any error or disproportions (Hofstede 2012).

Direct Labor Rate Variance:

Particulars Amount

Actual Direct Labor Hours 1188030

Standard Rate per labor hour $50

Standard Labor Cost for Actual

Labor Hours $59,401,500

Actual Direct Labor Cost $50,491,300

Material Price Variance ($8,910,200)

Remarks Favorable

The term direct labor rate refers to the rate at which labor is hired. The labors have a

generalized rate which is often fixed by labor unions. In case of any disparities between the

budgeted labor rate and the actual rate, the reasons may be demands by the labor union to

increase the particular rate. But as can be observed from the above table the material price

variance represents a favorable outcome. This means that the budget regarding the direct

labor rate has been prepared more or less accurately.

Direct Labor Efficiency Variance:

Particulars Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.