Business Finance Report: Budgeting Methods for TownScape Plc

VerifiedAdded on 2021/06/16

|12

|3249

|22

Report

AI Summary

This report provides a comprehensive analysis of budget preparation, focusing on the case of TownScape Plc, an international manufacturer of street furniture. It begins by outlining the purpose of budget preparation and its importance for business planning, including the steps involved in the process. The report then identifies cost drivers within TownScape Plc and examines the application of traditional budgeting. A significant portion of the report is dedicated to comparing traditional budgetary systems with alternative methods such as rolling budgets, zero-based budgets, and activity-based budgets. It explores the advantages and drawbacks of each method and assesses their potential application for TownScape Plc, ultimately providing recommendations for the most suitable budgeting approach. The analysis considers the company's current challenges, including new contracts and the need for additional manufacturing facilities, and evaluates how different budgeting methods can address these issues effectively. The report emphasizes the importance of selecting the appropriate budgeting system to support the company's future growth and financial goals, considering factors like flexibility, accuracy, and strategic alignment.

1

Business Finance

MOD003319

Business Finance

MOD003319

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Part 1:...............................................................................................................................................3

(i): Purpose of Budget Preparation...............................................................................................3

(ii): Cost Drivers of the TownScape and application of traditional budgeting approach to plan

for the future cost management....................................................................................................5

(iii): Analysis of appropriateness of Traditional Budgetary System............................................6

Part: 2...............................................................................................................................................7

(iv): Understanding of the Alternative Budget Methods and their significant advantages and

drawbacks over traditional approach...........................................................................................7

(v): Potential Application of each Method for the Company.......................................................8

(vi): Recommendations for the Best Budgeting Method for the Company.................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Contents

Introduction......................................................................................................................................3

Part 1:...............................................................................................................................................3

(i): Purpose of Budget Preparation...............................................................................................3

(ii): Cost Drivers of the TownScape and application of traditional budgeting approach to plan

for the future cost management....................................................................................................5

(iii): Analysis of appropriateness of Traditional Budgetary System............................................6

Part: 2...............................................................................................................................................7

(iv): Understanding of the Alternative Budget Methods and their significant advantages and

drawbacks over traditional approach...........................................................................................7

(v): Potential Application of each Method for the Company.......................................................8

(vi): Recommendations for the Best Budgeting Method for the Company.................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

3

Introduction

The present report is developed to provide an adequate understanding of the process of

budget preparation and its significance for promoting the growth and development of a business

entity. The budget preparation enables to develop an expenditure plan that helps in gaining an

estimate of the future needs of the business so that it can implement adequate strategies for

meeting them properly. The report has specifically discussed the case of TownScape Plc that is

regarded as an international manufacturer of street furniture. As analyzed from the case study,

the company adopts the use of traditional technique of budget preparation. However at present

the company is undergoing significant changes with undertaking new and revised contracts of up

to worth £35 million and requires additional plant and manufacturing facility in the year 2018.

The finance director of the company is concerned with the inappropriateness of the current

budgeting system used by the company to meet its future aims and goals. The most significant

problem that the company is facing at present is that the change in the budget approach will

become effective from the year 2019. In this context, the report presents the comparison of the

traditional budgetary system with the alternative budget methods such as rolling budgets, zero

based budgets and activity based budgets. The potential application of these methods to develop

the budget more effectively is also analyzed in the report to identify the best possible method for

developing the budgets for the company in context (Malina, 2017).

Part 1:

(i): Purpose of Budget Preparation

Budgeting can be stated as an important process of business planning by predicting the

potential growth prospects of a company. The purpose of budget is to develop a business model

that helps in providing an overview of potential growth prospects of a company. The budgeting

process enables to forecast the income the expenses and thereby estimating the future

profitability position of a company. It helps in development of a financial framework that detail

out the overall financial activities for facilitating the decision-making of financial managers. It

develops a proposed action plan for planning of future financial needs and also gains an estimate

Introduction

The present report is developed to provide an adequate understanding of the process of

budget preparation and its significance for promoting the growth and development of a business

entity. The budget preparation enables to develop an expenditure plan that helps in gaining an

estimate of the future needs of the business so that it can implement adequate strategies for

meeting them properly. The report has specifically discussed the case of TownScape Plc that is

regarded as an international manufacturer of street furniture. As analyzed from the case study,

the company adopts the use of traditional technique of budget preparation. However at present

the company is undergoing significant changes with undertaking new and revised contracts of up

to worth £35 million and requires additional plant and manufacturing facility in the year 2018.

The finance director of the company is concerned with the inappropriateness of the current

budgeting system used by the company to meet its future aims and goals. The most significant

problem that the company is facing at present is that the change in the budget approach will

become effective from the year 2019. In this context, the report presents the comparison of the

traditional budgetary system with the alternative budget methods such as rolling budgets, zero

based budgets and activity based budgets. The potential application of these methods to develop

the budget more effectively is also analyzed in the report to identify the best possible method for

developing the budgets for the company in context (Malina, 2017).

Part 1:

(i): Purpose of Budget Preparation

Budgeting can be stated as an important process of business planning by predicting the

potential growth prospects of a company. The purpose of budget is to develop a business model

that helps in providing an overview of potential growth prospects of a company. The budgeting

process enables to forecast the income the expenses and thereby estimating the future

profitability position of a company. It helps in development of a financial framework that detail

out the overall financial activities for facilitating the decision-making of financial managers. It

develops a proposed action plan for planning of future financial needs and also gains an estimate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

of the future financial risks that can impact its growth and performance (Moles and Kidwekk,

2011).

It helps in making a comparison between the actual business growth against the

forecasted performance and thus determining the potential chances of its success. The deviations

found in the actual performance as compared to the predicted can help in identification of the

loopholes in the business strategy. As such, the business managers can implement specific

actions for overcoming the issues identified to ensure the long-term growth and development of

the company. The process of budget preparation in the company need to consist of the following

steps:

Stage 1: Development of Budget Policy

o The step involves developing the budgeted period, time table and developing the

budget committee in order to provide a clear direction to the management for

developing the budgets. The budget is prepared for the period of 12 months and

each stage is monitored and evaluated by committee on a regular basis. Stage 2: Communicating the Guidelines of Budget to Relevant Managers

o Budget committee is responsible for disseminating the information obtained from

the process to the relevant managers. This is essential to provide understanding to

the budget managers about the strategic plan that need to be undertaken for

supporting the company’s growth and development (Rasmussen, 2003).

Stage 3: Identification of the Limiting Factors

o The stage consists of identification of the significant problems or issues that can

negatively impact the company plan of future growth and development. Stage 4: Preparation of Budget

o The identification of the limiting factor is followed by determining the overall

impact of the issue identified on the future growth and development of a business

entity. This helps in identification of the issues for which the budget forecast need

to be done for example, sale budget or any other. Stage 5: Developing the draft budgets for all other areas

of the future financial risks that can impact its growth and performance (Moles and Kidwekk,

2011).

It helps in making a comparison between the actual business growth against the

forecasted performance and thus determining the potential chances of its success. The deviations

found in the actual performance as compared to the predicted can help in identification of the

loopholes in the business strategy. As such, the business managers can implement specific

actions for overcoming the issues identified to ensure the long-term growth and development of

the company. The process of budget preparation in the company need to consist of the following

steps:

Stage 1: Development of Budget Policy

o The step involves developing the budgeted period, time table and developing the

budget committee in order to provide a clear direction to the management for

developing the budgets. The budget is prepared for the period of 12 months and

each stage is monitored and evaluated by committee on a regular basis. Stage 2: Communicating the Guidelines of Budget to Relevant Managers

o Budget committee is responsible for disseminating the information obtained from

the process to the relevant managers. This is essential to provide understanding to

the budget managers about the strategic plan that need to be undertaken for

supporting the company’s growth and development (Rasmussen, 2003).

Stage 3: Identification of the Limiting Factors

o The stage consists of identification of the significant problems or issues that can

negatively impact the company plan of future growth and development. Stage 4: Preparation of Budget

o The identification of the limiting factor is followed by determining the overall

impact of the issue identified on the future growth and development of a business

entity. This helps in identification of the issues for which the budget forecast need

to be done for example, sale budget or any other. Stage 5: Developing the draft budgets for all other areas

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

o The drafts of other issues that are identified for developing a budget for the

limiting factor should be prepared by the management so that it can be developed

in the future context on identification of the significant problem or issues. Stage 6: Review and Coordinating the Budgets

o The budget committee needs to monitor the consistency of budgets with one

another in order to identify the issue of lack of co-ordination or any that might

impact the budget preparation process. Stage 7: Developing the Master Budget

o It is prepared by the budget committee and includes the preparation of budgets

such as budgeted income statement or statement of financial position. Stage 8: Communicating the Budgets to the Relevant Parties

o The operating budget prepared is passed to the senior management for review and

is also shared across the other departments so that all business managers attain a

clear direction of what needs to be achieved (Wickramasinghe and Alawattage,

2007). Stage 9: Monitoring the Performance against the Budget Prepared

o The step involves identification of the variance between the actual performances

of the company against the determined targets in the budget prepared.

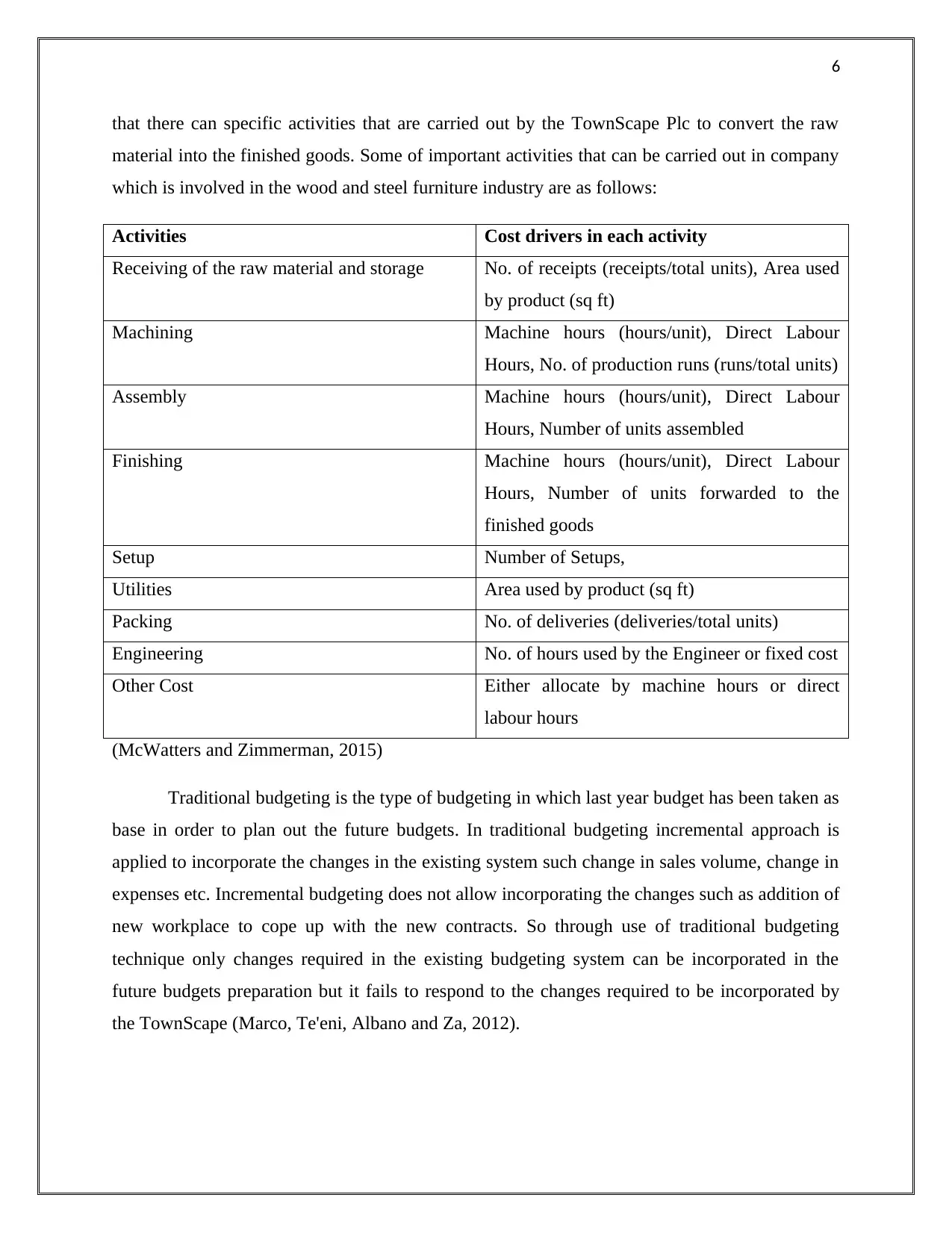

(ii): Cost Drivers of the TownScape and application of traditional budgeting approach to

plan for the future cost management

Cost driver is responsible for the change in the cost of an activity. An activity consist of

more than one cost drivers for example production activity can have cost driver such as machine

hours, labour hours, power unit used, output of inventory, etc. In order to identify the cost driver

for any business it is important to first identify the cost object that is responsible for triggering

the cost in various activities. For example, in case of business that is involved in the regular

material handling has to allocate the total material handling cost to different working units and

for this purpose there is need of cost driver (Adler, 2013).

TownScape Plc is an international company and it is actively involved in the

manufacturing of the street furniture. Some of the important goods manufactured by the

company are benches, litter bins, cycle racks, street bollards and bus shelter. So it can be said

o The drafts of other issues that are identified for developing a budget for the

limiting factor should be prepared by the management so that it can be developed

in the future context on identification of the significant problem or issues. Stage 6: Review and Coordinating the Budgets

o The budget committee needs to monitor the consistency of budgets with one

another in order to identify the issue of lack of co-ordination or any that might

impact the budget preparation process. Stage 7: Developing the Master Budget

o It is prepared by the budget committee and includes the preparation of budgets

such as budgeted income statement or statement of financial position. Stage 8: Communicating the Budgets to the Relevant Parties

o The operating budget prepared is passed to the senior management for review and

is also shared across the other departments so that all business managers attain a

clear direction of what needs to be achieved (Wickramasinghe and Alawattage,

2007). Stage 9: Monitoring the Performance against the Budget Prepared

o The step involves identification of the variance between the actual performances

of the company against the determined targets in the budget prepared.

(ii): Cost Drivers of the TownScape and application of traditional budgeting approach to

plan for the future cost management

Cost driver is responsible for the change in the cost of an activity. An activity consist of

more than one cost drivers for example production activity can have cost driver such as machine

hours, labour hours, power unit used, output of inventory, etc. In order to identify the cost driver

for any business it is important to first identify the cost object that is responsible for triggering

the cost in various activities. For example, in case of business that is involved in the regular

material handling has to allocate the total material handling cost to different working units and

for this purpose there is need of cost driver (Adler, 2013).

TownScape Plc is an international company and it is actively involved in the

manufacturing of the street furniture. Some of the important goods manufactured by the

company are benches, litter bins, cycle racks, street bollards and bus shelter. So it can be said

6

that there can specific activities that are carried out by the TownScape Plc to convert the raw

material into the finished goods. Some of important activities that can be carried out in company

which is involved in the wood and steel furniture industry are as follows:

Activities Cost drivers in each activity

Receiving of the raw material and storage No. of receipts (receipts/total units), Area used

by product (sq ft)

Machining Machine hours (hours/unit), Direct Labour

Hours, No. of production runs (runs/total units)

Assembly Machine hours (hours/unit), Direct Labour

Hours, Number of units assembled

Finishing Machine hours (hours/unit), Direct Labour

Hours, Number of units forwarded to the

finished goods

Setup Number of Setups,

Utilities Area used by product (sq ft)

Packing No. of deliveries (deliveries/total units)

Engineering No. of hours used by the Engineer or fixed cost

Other Cost Either allocate by machine hours or direct

labour hours

(McWatters and Zimmerman, 2015)

Traditional budgeting is the type of budgeting in which last year budget has been taken as

base in order to plan out the future budgets. In traditional budgeting incremental approach is

applied to incorporate the changes in the existing system such change in sales volume, change in

expenses etc. Incremental budgeting does not allow incorporating the changes such as addition of

new workplace to cope up with the new contracts. So through use of traditional budgeting

technique only changes required in the existing budgeting system can be incorporated in the

future budgets preparation but it fails to respond to the changes required to be incorporated by

the TownScape (Marco, Te'eni, Albano and Za, 2012).

that there can specific activities that are carried out by the TownScape Plc to convert the raw

material into the finished goods. Some of important activities that can be carried out in company

which is involved in the wood and steel furniture industry are as follows:

Activities Cost drivers in each activity

Receiving of the raw material and storage No. of receipts (receipts/total units), Area used

by product (sq ft)

Machining Machine hours (hours/unit), Direct Labour

Hours, No. of production runs (runs/total units)

Assembly Machine hours (hours/unit), Direct Labour

Hours, Number of units assembled

Finishing Machine hours (hours/unit), Direct Labour

Hours, Number of units forwarded to the

finished goods

Setup Number of Setups,

Utilities Area used by product (sq ft)

Packing No. of deliveries (deliveries/total units)

Engineering No. of hours used by the Engineer or fixed cost

Other Cost Either allocate by machine hours or direct

labour hours

(McWatters and Zimmerman, 2015)

Traditional budgeting is the type of budgeting in which last year budget has been taken as

base in order to plan out the future budgets. In traditional budgeting incremental approach is

applied to incorporate the changes in the existing system such change in sales volume, change in

expenses etc. Incremental budgeting does not allow incorporating the changes such as addition of

new workplace to cope up with the new contracts. So through use of traditional budgeting

technique only changes required in the existing budgeting system can be incorporated in the

future budgets preparation but it fails to respond to the changes required to be incorporated by

the TownScape (Marco, Te'eni, Albano and Za, 2012).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

(iii): Analysis of appropriateness of Traditional Budgetary System

TownScape is presently adopting the use of traditional budgetary systems for budget

creation and presentation. This system involves developing a budget by taking into consideration

the budget developed for the past year as a base and adjust it for the inflation and the business

changes. It helps in providing an estimate of projected sales and revenue and gain an estimate of

the future profitability position. The company at present is planning to undergo significant

changes for meeting its contractual obligations and as such the use of traditional budgeting

system does not seem to be appropriate in meeting its future business form. This is because it

needs an accurate estimation of plant and manufacturing capacity required in the year 2018 for

meeting its business needs. However, the traditional budgeting system is not a reliable method

for developing accurate estimations as it is often prone to variety if a data entry error as it is

developed with the use of spreadsheets. Also, the budgets prepared with the use of traditional

budgeting system are not reviewed regularly and therefore it is not useful for incorporating the

recent business changes into account. It is not largely useful for developing a strategic plan as the

budget main purpose of creation is cost reduction instead of creating value for the shareholders

and therefore it does not help in development of strategic initiatives for meeting the changes

proposed in business aims and objectives (McWatters and Zimmerman, 2015).

Part: 2

(iv): Understanding of the Alternative Budget Methods and their significant advantages

and drawbacks over traditional approach

The finance director of TownScape need to gain an in-depth understanding of the various

types of alternative budgeting system and their benefits and drawbacks before selecting the best

method for adoption in the company. These can be discussed as follows:

Rolling Budgets

Rolling budget are the budgets that can be updated continually for adding of a new

budgeted period. The budget is subjected to change as per the additional activities to be carried

out a business entity in the coming period of time. The budget involves extending the existing

budget incrementally as per the changes in the business operations. The budget is based on a

(iii): Analysis of appropriateness of Traditional Budgetary System

TownScape is presently adopting the use of traditional budgetary systems for budget

creation and presentation. This system involves developing a budget by taking into consideration

the budget developed for the past year as a base and adjust it for the inflation and the business

changes. It helps in providing an estimate of projected sales and revenue and gain an estimate of

the future profitability position. The company at present is planning to undergo significant

changes for meeting its contractual obligations and as such the use of traditional budgeting

system does not seem to be appropriate in meeting its future business form. This is because it

needs an accurate estimation of plant and manufacturing capacity required in the year 2018 for

meeting its business needs. However, the traditional budgeting system is not a reliable method

for developing accurate estimations as it is often prone to variety if a data entry error as it is

developed with the use of spreadsheets. Also, the budgets prepared with the use of traditional

budgeting system are not reviewed regularly and therefore it is not useful for incorporating the

recent business changes into account. It is not largely useful for developing a strategic plan as the

budget main purpose of creation is cost reduction instead of creating value for the shareholders

and therefore it does not help in development of strategic initiatives for meeting the changes

proposed in business aims and objectives (McWatters and Zimmerman, 2015).

Part: 2

(iv): Understanding of the Alternative Budget Methods and their significant advantages

and drawbacks over traditional approach

The finance director of TownScape need to gain an in-depth understanding of the various

types of alternative budgeting system and their benefits and drawbacks before selecting the best

method for adoption in the company. These can be discussed as follows:

Rolling Budgets

Rolling budget are the budgets that can be updated continually for adding of a new

budgeted period. The budget is subjected to change as per the additional activities to be carried

out a business entity in the coming period of time. The budget involves extending the existing

budget incrementally as per the changes in the business operations. The budget is based on a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

rolling estimate against the forecasted changes in the budgeted activities so that it can be

expanded in future as per the business requirements (Warren, Reeve and Duchac, 2011).

The budget is extremely advantageous for the companies that have high variances in the

economy and commerce. TownScape can gain benefit from this type of budgeting system on

account of its flexibility and incorporates the updated information about the forecasted financial

performance of the company. It will enable the company to become more responsive in respect

of the changes in external environment and also its preparation will not involves nay extra

investment of funds or time by the company. However, the most pertinent drawback with the use

of such budgeting system is that it can adopt the use of unrealistic assumptions such as revenue

forecast that can result in providing large variances (Clowes and Scriven, 2015).

Zero Based Budgets

This method of budgeting adopts the use of Zero Base and all the significant expenses are

recognized for each new period. It involves the preparation of budget from starting point for each

of the line items on the basis of its cost and requirements. Thus, this system of budgeting does

not involve extracting any information from the previous year budget is prepared all fresh.

The significant advantage of this method is that it a flexible type of budget and helps in

overcoming the issues of budget inflation. The potential drawback is that it is subjected to being

manipulated y the managers (Kjerstad, 2003).

Activity Based Budgets

This method of budgeting involves developing budgets as per the cost of each activity

and then involves a compilation of the overall budgeted expenses. It provides an accurate

estimation of the future business expenses and thus improves transparency in the budgeting

process. However, it is associated with the drawback of requiring heavy expenditure and large

consumption of time for its effective implementation and adoption (Tilanus, 2012).

(v): Potential Application of each Method for the Company

TownScape Plc at present is incorporating the use of traditional budgeting system.

However, the company at present is planning for undertaking some major changes for its future

growth and therefore has to adopt some flexibility in its budgeting system to increase its

rolling estimate against the forecasted changes in the budgeted activities so that it can be

expanded in future as per the business requirements (Warren, Reeve and Duchac, 2011).

The budget is extremely advantageous for the companies that have high variances in the

economy and commerce. TownScape can gain benefit from this type of budgeting system on

account of its flexibility and incorporates the updated information about the forecasted financial

performance of the company. It will enable the company to become more responsive in respect

of the changes in external environment and also its preparation will not involves nay extra

investment of funds or time by the company. However, the most pertinent drawback with the use

of such budgeting system is that it can adopt the use of unrealistic assumptions such as revenue

forecast that can result in providing large variances (Clowes and Scriven, 2015).

Zero Based Budgets

This method of budgeting adopts the use of Zero Base and all the significant expenses are

recognized for each new period. It involves the preparation of budget from starting point for each

of the line items on the basis of its cost and requirements. Thus, this system of budgeting does

not involve extracting any information from the previous year budget is prepared all fresh.

The significant advantage of this method is that it a flexible type of budget and helps in

overcoming the issues of budget inflation. The potential drawback is that it is subjected to being

manipulated y the managers (Kjerstad, 2003).

Activity Based Budgets

This method of budgeting involves developing budgets as per the cost of each activity

and then involves a compilation of the overall budgeted expenses. It provides an accurate

estimation of the future business expenses and thus improves transparency in the budgeting

process. However, it is associated with the drawback of requiring heavy expenditure and large

consumption of time for its effective implementation and adoption (Tilanus, 2012).

(v): Potential Application of each Method for the Company

TownScape Plc at present is incorporating the use of traditional budgeting system.

However, the company at present is planning for undertaking some major changes for its future

growth and therefore has to adopt some flexibility in its budgeting system to increase its

9

responsiveness for the future changes. As such, the use of alternative method of accounting

would help in improving the responsiveness and flexibility in the budgeting system of the

company. The rolling budget system can be applied by the company on the basis of expectation

of change in the environment. For example, if there is addition of several new product lines each

year that requires monthly updates. Therefore, the system of rolling budget can be potentially

applied by developing a change management team for determination of how often the business

environment is likely to change. The major impact of rolling budget is on planning element of

budgeting as it helps in developing a specific plan for meeting the uncertainties in future. For

example, the techniques of SWOT analysis, brainstorming and balanced scorecard can help in

identifying the external and internal changes that can impact the company performance

(Scheller-Kreinsen and Geissler, 2009).

The method of zero based budgeting can be applied by the company by detailed

examination of all the previous expenditures to identify the wasteful activities to be removed. It

then starts with the use of blank sheet and develops budgets by redesigning the cost structures as

per the future business changes. It will have a major impact on redesigning the operations and

resources of the company as per the new strategic goals developed. The activity based costing

can be applied by identification of the cost drivers that are responsible for incurring revenue and

expenses for the company in and its significant multiplication by the activity level. It will have a

major impact on the coordination element of budgeting as it involves calculating the overall

expenses after determining the cost of each activity (Shim, Siegel and Shim, 2011).

(vi): Recommendations for the Best Budgeting Method for the Company

The company at present is recommended to adopt the use of rolling based budgeting

system as it will enable the finance director to adjust its budgets as per the future business

changes without having large changes in its structure. The finance director can add a future

period of estimation in the budget that is of a month, quarter or year. However, the company in

addition with his budgeting system is also recommended to adopt activity based costing in the

long-term. This is because it will enable the company to implement material changes in its

budget system. As such, the method is required as the use of rolling budge system will only

simply adjust the previous year budgeted amounts as per the forecasted changes. The cost

involved in various activities for adding plant and manufacturing capacity by TownScape Plc can

responsiveness for the future changes. As such, the use of alternative method of accounting

would help in improving the responsiveness and flexibility in the budgeting system of the

company. The rolling budget system can be applied by the company on the basis of expectation

of change in the environment. For example, if there is addition of several new product lines each

year that requires monthly updates. Therefore, the system of rolling budget can be potentially

applied by developing a change management team for determination of how often the business

environment is likely to change. The major impact of rolling budget is on planning element of

budgeting as it helps in developing a specific plan for meeting the uncertainties in future. For

example, the techniques of SWOT analysis, brainstorming and balanced scorecard can help in

identifying the external and internal changes that can impact the company performance

(Scheller-Kreinsen and Geissler, 2009).

The method of zero based budgeting can be applied by the company by detailed

examination of all the previous expenditures to identify the wasteful activities to be removed. It

then starts with the use of blank sheet and develops budgets by redesigning the cost structures as

per the future business changes. It will have a major impact on redesigning the operations and

resources of the company as per the new strategic goals developed. The activity based costing

can be applied by identification of the cost drivers that are responsible for incurring revenue and

expenses for the company in and its significant multiplication by the activity level. It will have a

major impact on the coordination element of budgeting as it involves calculating the overall

expenses after determining the cost of each activity (Shim, Siegel and Shim, 2011).

(vi): Recommendations for the Best Budgeting Method for the Company

The company at present is recommended to adopt the use of rolling based budgeting

system as it will enable the finance director to adjust its budgets as per the future business

changes without having large changes in its structure. The finance director can add a future

period of estimation in the budget that is of a month, quarter or year. However, the company in

addition with his budgeting system is also recommended to adopt activity based costing in the

long-term. This is because it will enable the company to implement material changes in its

budget system. As such, the method is required as the use of rolling budge system will only

simply adjust the previous year budgeted amounts as per the forecasted changes. The cost

involved in various activities for adding plant and manufacturing capacity by TownScape Plc can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

be identified accurately and this will help in gaining an estimate of the overall expenses (Tănase,

2013).

Conclusion

It can be stated from the overall discussion that the budget preparation enables to develop

an expenditure plan by the company that helps in gaining an estimate of the future needs of the

business so that it can implement adequate strategies for meeting them properly. It has been

identified from the overall case analysis that the method of traditional budgeting is not suitable

for TownScape. It is recommended to adopt the use of alternative method for improving

flexibility in its budgeting system for meeting the future business changes.

be identified accurately and this will help in gaining an estimate of the overall expenses (Tănase,

2013).

Conclusion

It can be stated from the overall discussion that the budget preparation enables to develop

an expenditure plan by the company that helps in gaining an estimate of the future needs of the

business so that it can implement adequate strategies for meeting them properly. It has been

identified from the overall case analysis that the method of traditional budgeting is not suitable

for TownScape. It is recommended to adopt the use of alternative method for improving

flexibility in its budgeting system for meeting the future business changes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Adler, R. 2013. Management Accounting. Routledge.

Clowes, R. and Scriven, V. 2015. Budgeting: A Practical Approach. Pearson Higher Education

AU.

Kjerstad, E. 2003. Prospective Funding of General Hospitals in Norway: Incentives for Higher

Production? International Journal of Health Care Finance and Economics 3(4),pp. 231-251.

Malina, M. 2017. Advances in Management Accounting. Emerald Group Publishing.

Marco, E., Te'eni, D., Albano, V. and Za. S. 2012. Information Systems: Crossroads for

Organization, Management, Accounting and Engineering: ItAIS: The Italian Association for

Information Systems. Springer Science & Business Media.

McWatters, C., and Zimmerman, J. 2015. Management Accounting in a Dynamic Environment.

Routledge.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Rasmussen, N. et al. 2003. Process Improvement for Effective Budgeting and Financial

Reporting. John Wiley & Sons.

Scheller-Kreinsen, D. and Geissler, A. 2009. The ABC of DRGs. Euro Observer 11(4), pp. 1-5.

Shim, J.K., Siegel, J.G. and Shim, A.L. 2011. Budgeting Basics and Beyond. John Wiley & Sons.

Tănase, G.L. 2013. An Overall Analysis of Participatory Budgeting: Advantages and Essential

Factors for an Effective Implementation in Economic Entities. Journal of Eastern Europe

Research in Business and Economics.

Tilanus, C.B. 2012. Quantitative methods in budgeting. Springer Science & Business Media.

Warren, C., Reeve, J. and Duchac, J. 2011. Financial & Managerial Accounting. Cengage

Learning.

References

Adler, R. 2013. Management Accounting. Routledge.

Clowes, R. and Scriven, V. 2015. Budgeting: A Practical Approach. Pearson Higher Education

AU.

Kjerstad, E. 2003. Prospective Funding of General Hospitals in Norway: Incentives for Higher

Production? International Journal of Health Care Finance and Economics 3(4),pp. 231-251.

Malina, M. 2017. Advances in Management Accounting. Emerald Group Publishing.

Marco, E., Te'eni, D., Albano, V. and Za. S. 2012. Information Systems: Crossroads for

Organization, Management, Accounting and Engineering: ItAIS: The Italian Association for

Information Systems. Springer Science & Business Media.

McWatters, C., and Zimmerman, J. 2015. Management Accounting in a Dynamic Environment.

Routledge.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Rasmussen, N. et al. 2003. Process Improvement for Effective Budgeting and Financial

Reporting. John Wiley & Sons.

Scheller-Kreinsen, D. and Geissler, A. 2009. The ABC of DRGs. Euro Observer 11(4), pp. 1-5.

Shim, J.K., Siegel, J.G. and Shim, A.L. 2011. Budgeting Basics and Beyond. John Wiley & Sons.

Tănase, G.L. 2013. An Overall Analysis of Participatory Budgeting: Advantages and Essential

Factors for an Effective Implementation in Economic Entities. Journal of Eastern Europe

Research in Business and Economics.

Tilanus, C.B. 2012. Quantitative methods in budgeting. Springer Science & Business Media.

Warren, C., Reeve, J. and Duchac, J. 2011. Financial & Managerial Accounting. Cengage

Learning.

12

Wickramasinghe, D. and Alawattage, C. 2007. Management accounting change: approaches

and perspectives. London and New York: Routledge. Taylor & Francis Group.

Wickramasinghe, D. and Alawattage, C. 2007. Management accounting change: approaches

and perspectives. London and New York: Routledge. Taylor & Francis Group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.