Budget Incidence of Tax: Impact of Government Expenditure on Economy

VerifiedAdded on 2019/11/26

|10

|1904

|206

Report

AI Summary

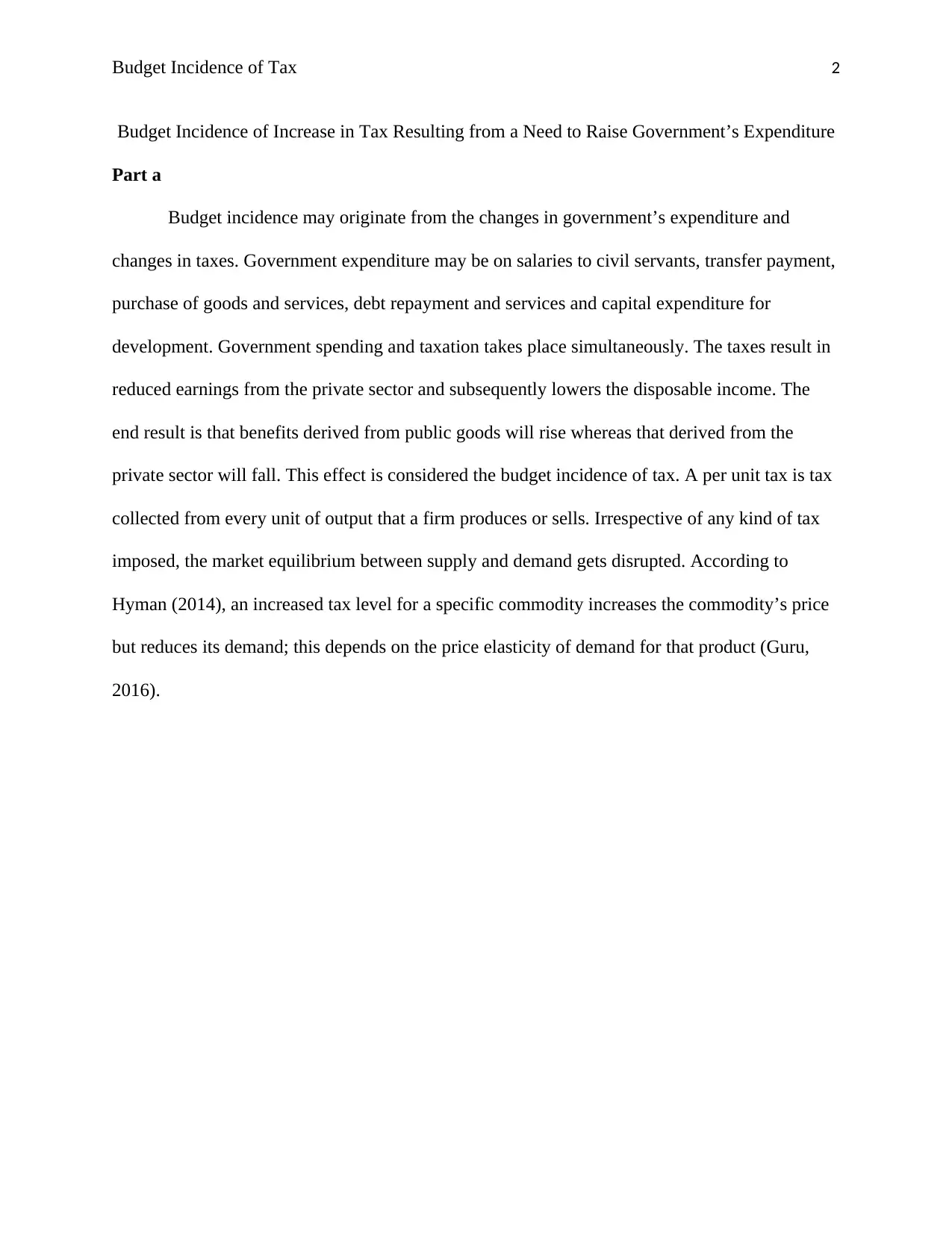

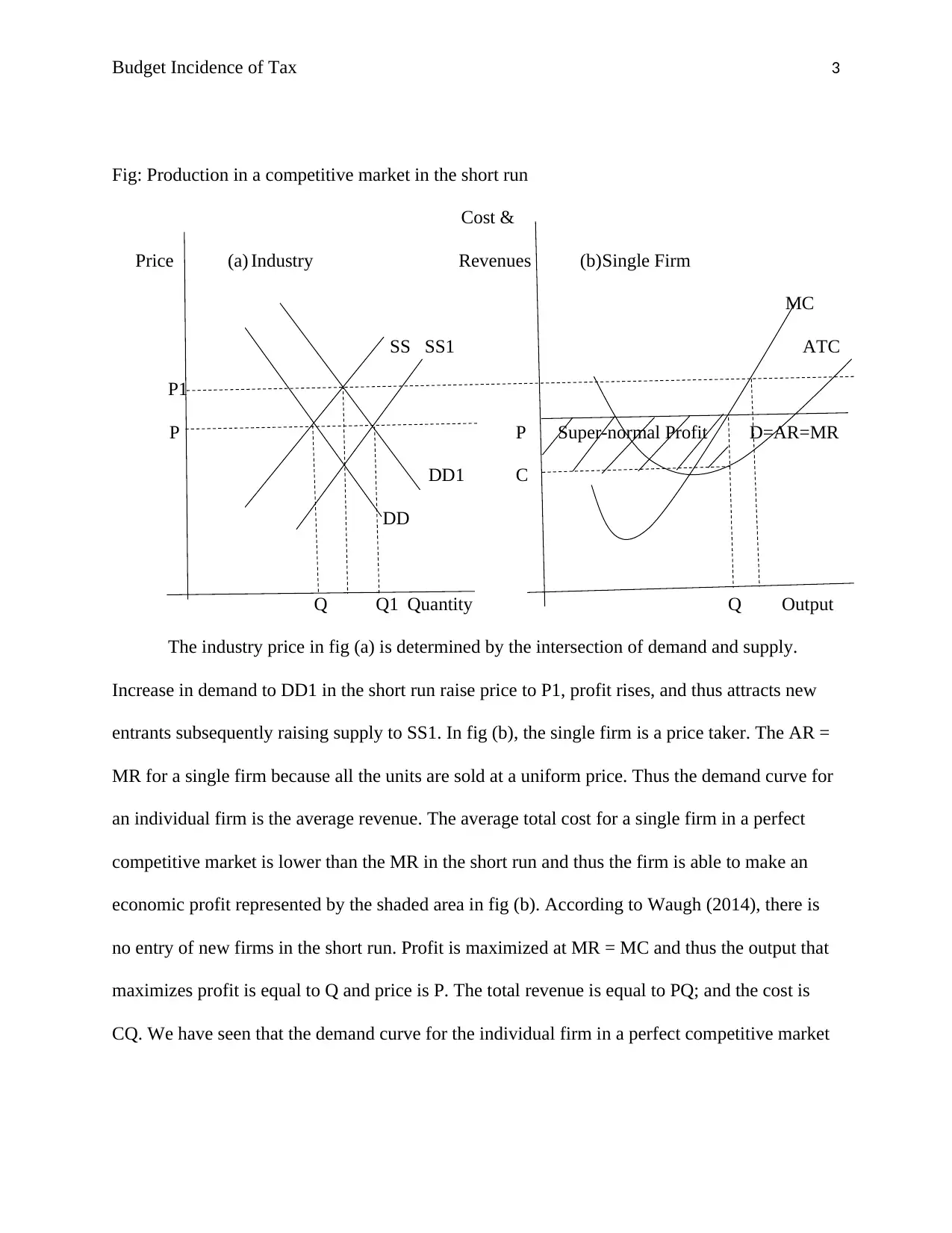

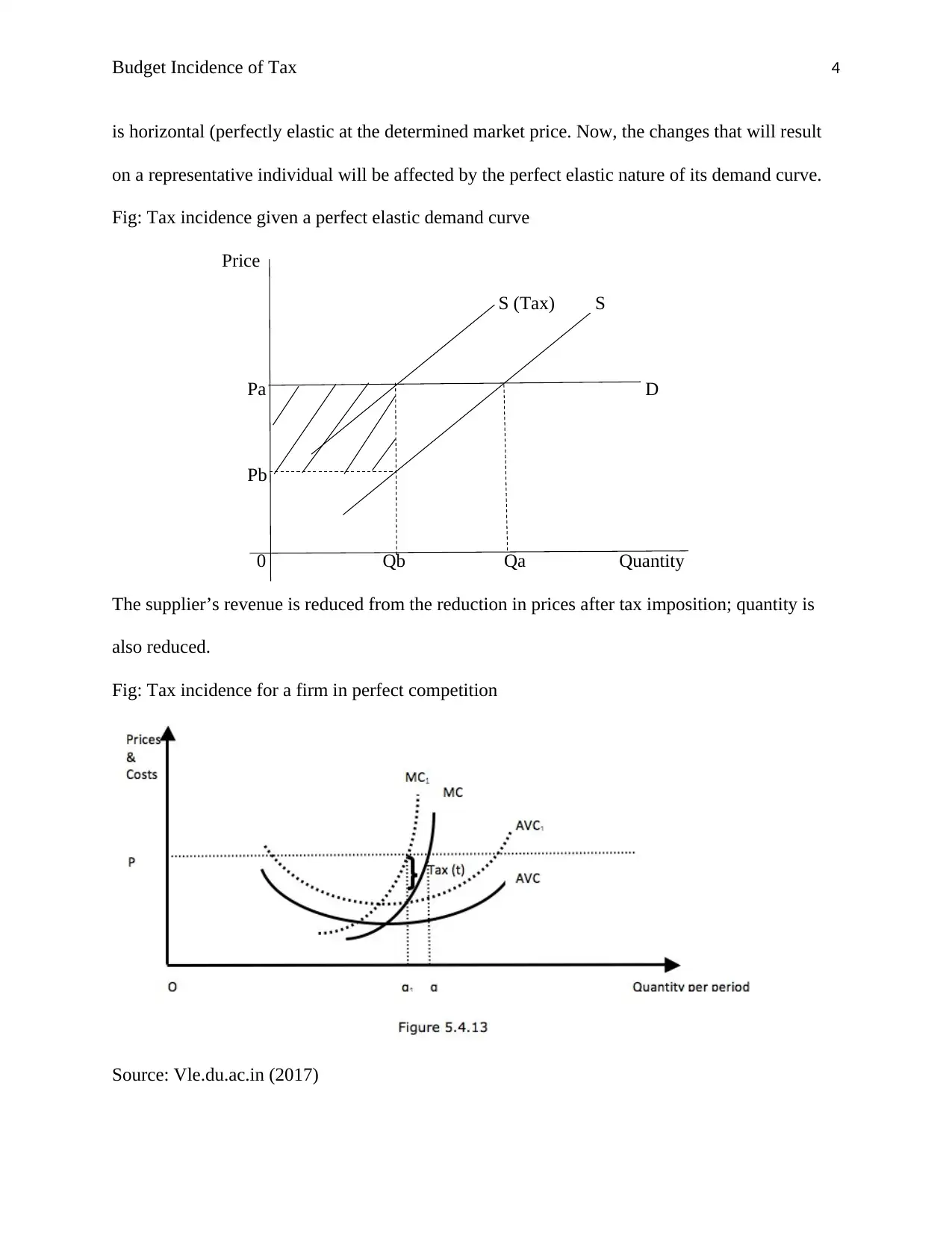

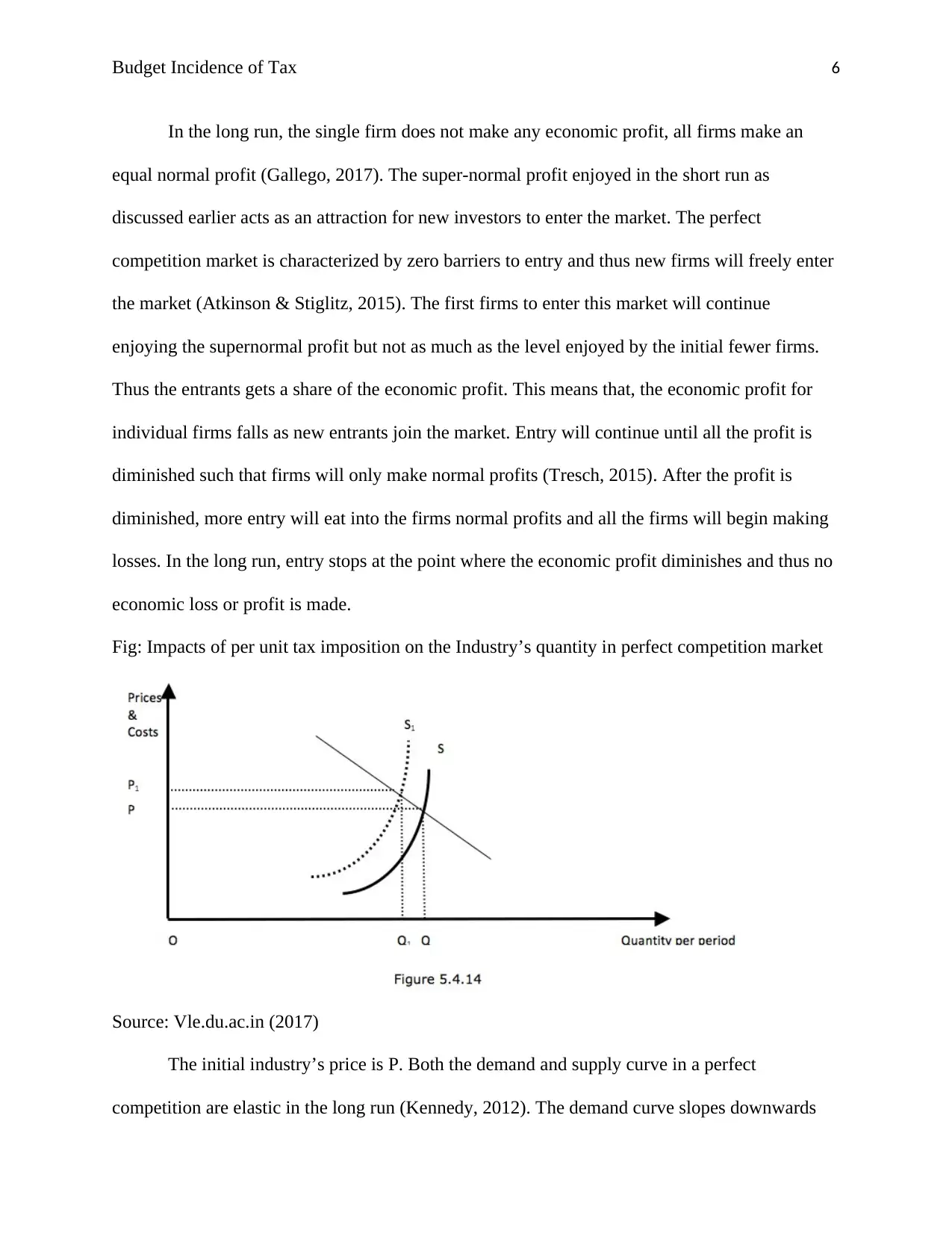

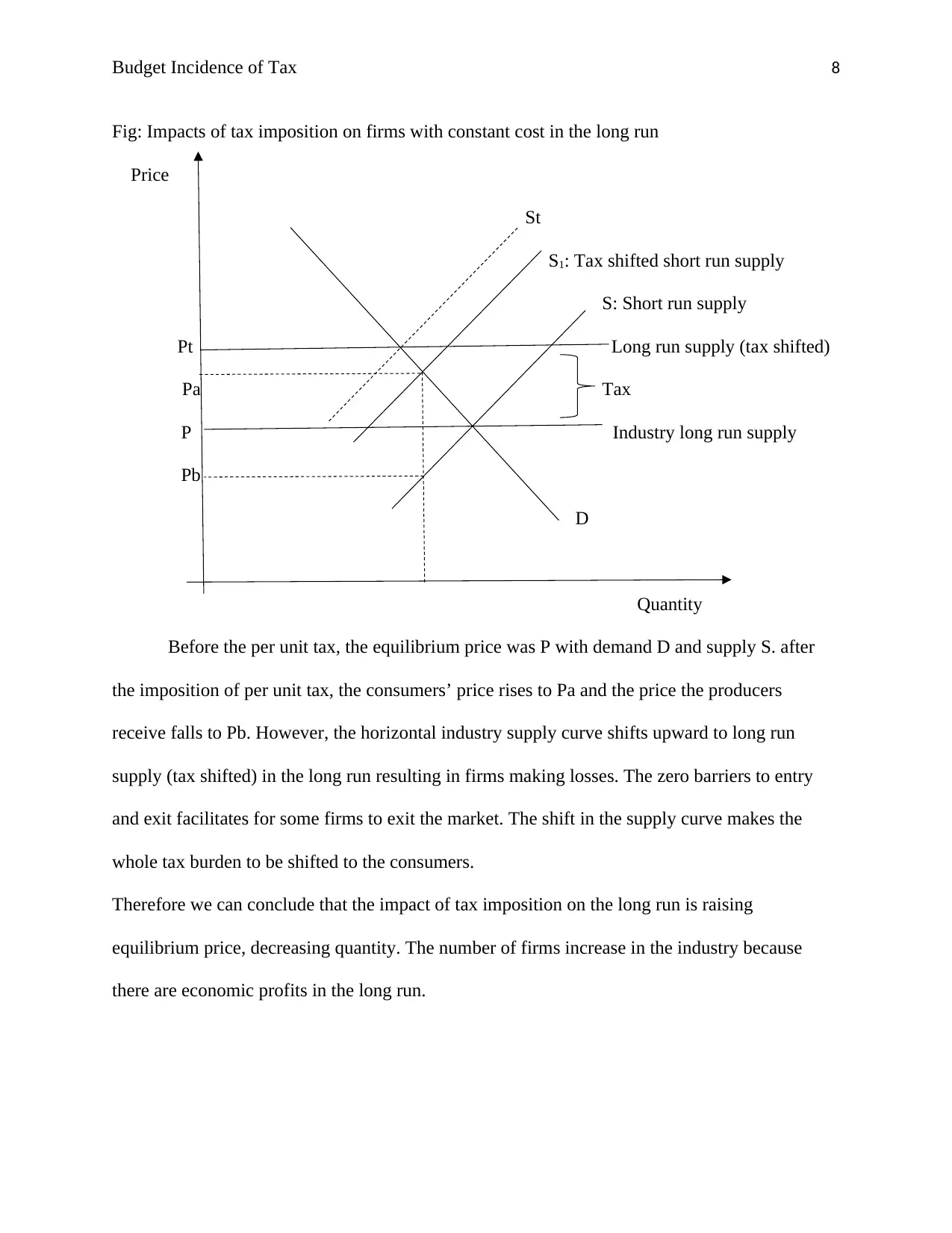

This report examines the budget incidence of tax, focusing on how changes in government expenditure and taxation affect market equilibrium in competitive markets. It explores the impact of per-unit taxes on firms in both the short and long run, analyzing how supply and demand dynamics shift and how economic profits are influenced. The report details how firms respond to tax impositions, considering factors such as price elasticity and the ability to pass the tax burden to consumers. It also discusses the long-run effects, including changes in industry supply, firm entry and exit, and the ultimate distribution of the tax burden between producers and consumers. The analysis includes graphical representations to illustrate the shifts in supply and demand curves, demonstrating how taxes affect market prices and quantities, and ultimately influencing economic outcomes.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.