Budget Variance Report Analysis

VerifiedAdded on 2019/10/31

|7

|1927

|157

Report

AI Summary

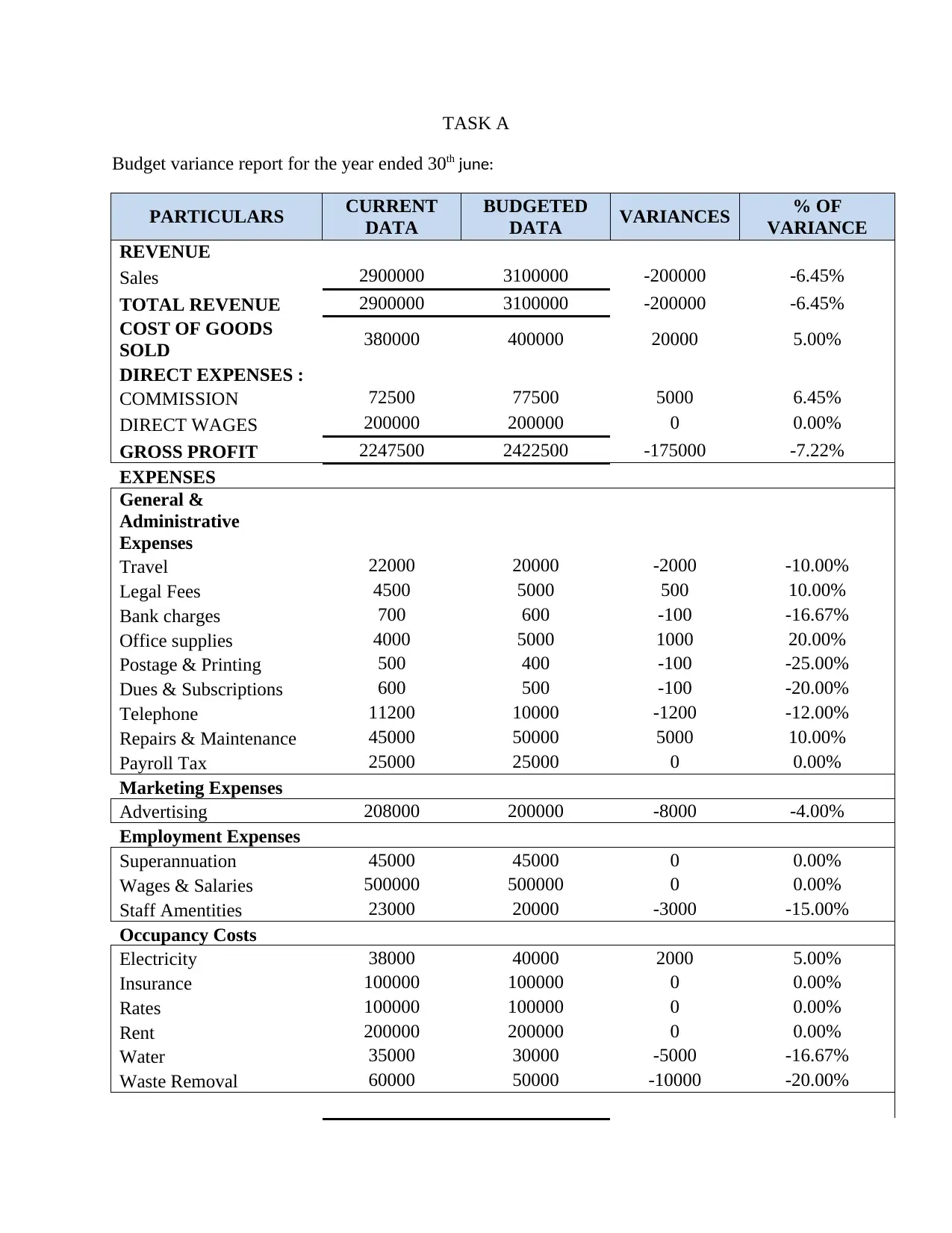

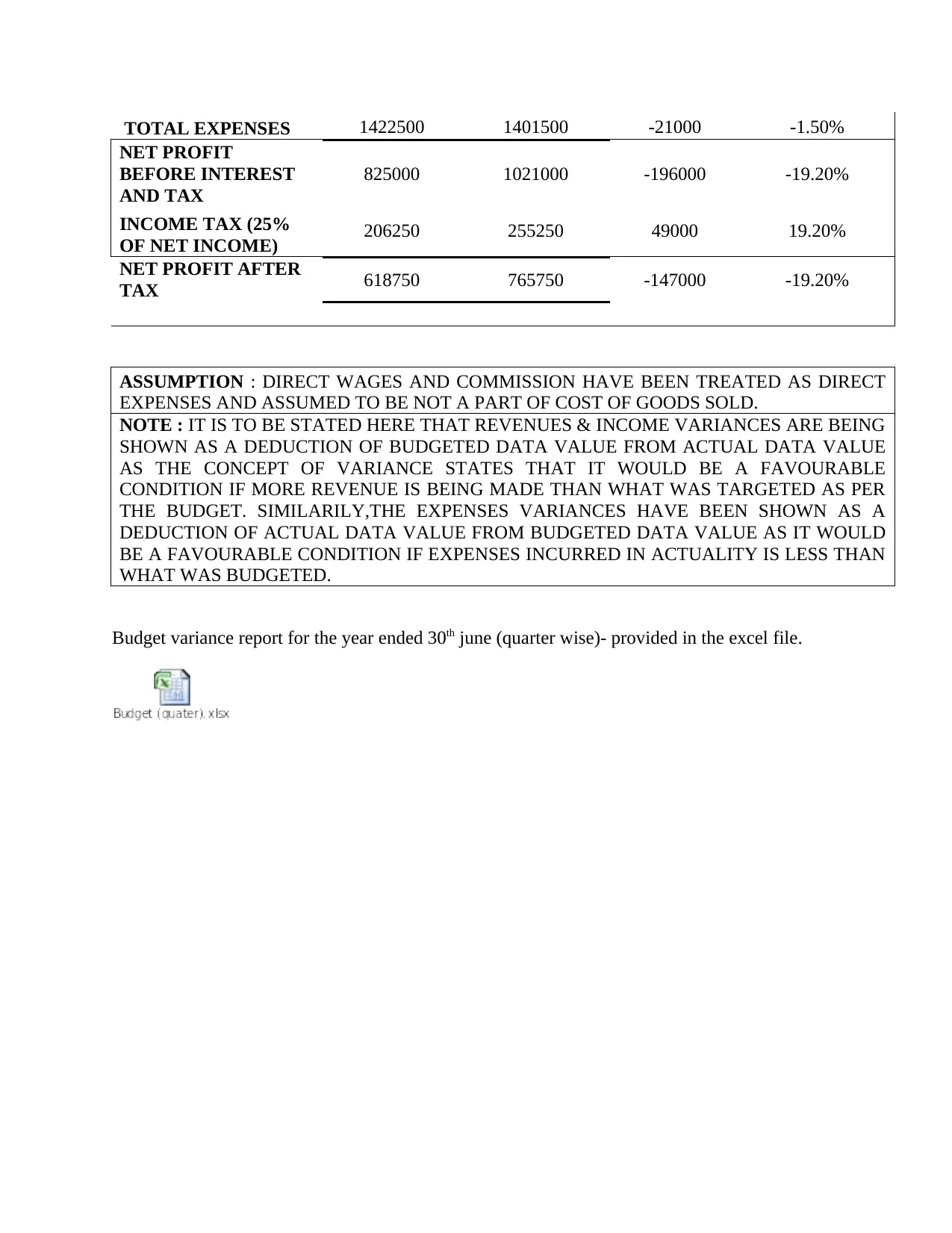

This report analyzes a budget variance report for Big Red Bicycle Pty Ltd. for the year ended June 30th. The report details significant variances in revenue, cost of goods sold, and various expenses, resulting in a negative net profit variance. A key finding is the inconsistency in gross profit across quarters, with significant negative variances in three quarters and a positive variance in the third. The analysis identifies several internal issues contributing to the negative variances, including employee loyalty, material wastage, and the impact of communication styles on sales team morale. A contingency plan is proposed to address these issues, focusing on improved employee training and motivation, stricter adherence to company policies, increased employee involvement in decision-making, and sales commission adjustments. The plan also includes strategies to mitigate the impact of anticipated economic downturn and sales volume reduction, such as product diversification and exploring overseas manufacturing options. The overall goal is to improve profitability and meet company targets by addressing internal weaknesses and adapting to external market conditions.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.