Management Accounting: Systems, Reporting, and Budgetary Control

VerifiedAdded on 2024/05/17

|24

|4114

|416

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, methods, and systems. It explains different management accounting systems, including cost accounting, job costing, price optimization, and inventory management. The report also discusses various management accounting reporting methods such as cost reports, revenue reports, stock and production reports, budget reports, and performance reports. It evaluates the benefits of management accounting systems and their integration within organizational processes. The report includes a detailed cost analysis using marginal and absorption costing techniques to prepare an income statement. Furthermore, it explains the advantages and disadvantages of different planning tools used in budgetary control and how organizations adapt management accounting systems to respond to financial problems. Desklib provides this and other solved assignments to aid students in their studies.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:....................................................................................................................................3

P1: Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2: Explain different methods used for management accounting reporting................................6

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing........................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools used in

budgetary control.......................................................................................................................15

P5: How organizations are adapting management accounting systems to respond to financial

problems....................................................................................................................................18

Conclusion:....................................................................................................................................22

References:....................................................................................................................................23

2

Introduction:....................................................................................................................................3

P1: Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................4

P2: Explain different methods used for management accounting reporting................................6

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing........................................................................9

P4. Explain the advantages and disadvantages of different types of planning tools used in

budgetary control.......................................................................................................................15

P5: How organizations are adapting management accounting systems to respond to financial

problems....................................................................................................................................18

Conclusion:....................................................................................................................................22

References:....................................................................................................................................23

2

Introduction:

This report is generated to give management an understanding of basic principles of management

accounting. The different methods and approaches of management accounting system are used to

prepare and deliver various useful reports to the managers of company. Management accounting

ensures quality management with organization and the same is necessary to achieve the goal of

sustainable success. Assignment explains the cost accounting system also. Costing tools are

used to control and manage the cost of every business activities. For identifying the cost of

production and to calculate profit marginal and absorption costing techniques can be used by

manager. Planning tools of management accounting helpful to arrange the business process

according to the targets of company and in addition it also provides a base to determinate the

non-financial factors of business for long term growth. Budgetary control techniques are also

helpful for business in numerous ways. It helps to make appropriate future policies for the

development of business organization.

3

This report is generated to give management an understanding of basic principles of management

accounting. The different methods and approaches of management accounting system are used to

prepare and deliver various useful reports to the managers of company. Management accounting

ensures quality management with organization and the same is necessary to achieve the goal of

sustainable success. Assignment explains the cost accounting system also. Costing tools are

used to control and manage the cost of every business activities. For identifying the cost of

production and to calculate profit marginal and absorption costing techniques can be used by

manager. Planning tools of management accounting helpful to arrange the business process

according to the targets of company and in addition it also provides a base to determinate the

non-financial factors of business for long term growth. Budgetary control techniques are also

helpful for business in numerous ways. It helps to make appropriate future policies for the

development of business organization.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

P1: Explain management accounting and give the essential requirements of different types

of management accounting systems.

Management accounting: management Accounting is the procedure of examination,

determination and reporting of financial data compile with the help of monetary accounting and

cost accounting, keeping in mind the ultimate goal to help management during the time decision

making, production of strategy and routine task of a business. Along these lines, it is obvious

from the over that the management accounting depends on accounting and costing (Shen, et.al.,

2016).

Management accounting includes:

Image 1, steps in management accounting

(By Author, 2018)

Various management accounting approaches and their requirement is as follows:

Cost accounting system: The cost accounting framework helps the management in assessing the

cost of each type of product which might be required in income examination, cost control and

stock management. The different necessities of this approach are:

Coordination between different departments is essential for this approach.

Regular stock audit reacquired for the effective use of cist accounting system.

Proper and effective internal stock audit system is necessary under this method

Proper inventory management with the appropriate order and storage system is required

to obtain benefits of cost accounting system (VanBaren, 2017).

4

Planning

Implementation

Controlling

of management accounting systems.

Management accounting: management Accounting is the procedure of examination,

determination and reporting of financial data compile with the help of monetary accounting and

cost accounting, keeping in mind the ultimate goal to help management during the time decision

making, production of strategy and routine task of a business. Along these lines, it is obvious

from the over that the management accounting depends on accounting and costing (Shen, et.al.,

2016).

Management accounting includes:

Image 1, steps in management accounting

(By Author, 2018)

Various management accounting approaches and their requirement is as follows:

Cost accounting system: The cost accounting framework helps the management in assessing the

cost of each type of product which might be required in income examination, cost control and

stock management. The different necessities of this approach are:

Coordination between different departments is essential for this approach.

Regular stock audit reacquired for the effective use of cist accounting system.

Proper and effective internal stock audit system is necessary under this method

Proper inventory management with the appropriate order and storage system is required

to obtain benefits of cost accounting system (VanBaren, 2017).

4

Planning

Implementation

Controlling

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing: job costing framework is a procedure of collecting the data about the cost of a

particular item produced or group of items. This approach basically used to identify the cost

when company producing the products in different groups and groups are different from each

other. Under this method:

It is necessary for cost plus contracts.

Under this method it is necessary that the direct cost of production charged to the product

directly and indirect cost are distributed as per standards.

The approach is suitable in the situations where the products are created after an affirmed

order is gotten.

It is necessary that each job group contains a identification number for proper distribution

of expenses.

Price optimization method: this system includes the study of customer behaviour at different

price level. This approach requires:

Previous year data of sales, prices and other financial data.

Proper policy and planning for regular monitoring of the system.

Proper distribution of responsibility and sound communication structure.

Regular Help of upper level management (Shen, et.al., 2016).

Inventory management: inventory management is related with the appropriate management of

inventory. It includes the management of purchase, storage and use of raw material and goods

produced.

Proper method of stock valuation like FIFO, LIFO, or Weighted average should be

followed in stock valuation.

Effective physical control on stock is required.

An internal stock monitoring system like stock audit is require for effective use of this

system.

5

particular item produced or group of items. This approach basically used to identify the cost

when company producing the products in different groups and groups are different from each

other. Under this method:

It is necessary for cost plus contracts.

Under this method it is necessary that the direct cost of production charged to the product

directly and indirect cost are distributed as per standards.

The approach is suitable in the situations where the products are created after an affirmed

order is gotten.

It is necessary that each job group contains a identification number for proper distribution

of expenses.

Price optimization method: this system includes the study of customer behaviour at different

price level. This approach requires:

Previous year data of sales, prices and other financial data.

Proper policy and planning for regular monitoring of the system.

Proper distribution of responsibility and sound communication structure.

Regular Help of upper level management (Shen, et.al., 2016).

Inventory management: inventory management is related with the appropriate management of

inventory. It includes the management of purchase, storage and use of raw material and goods

produced.

Proper method of stock valuation like FIFO, LIFO, or Weighted average should be

followed in stock valuation.

Effective physical control on stock is required.

An internal stock monitoring system like stock audit is require for effective use of this

system.

5

P2: Explain different methods used for management accounting reporting.

Cost reports: This report contains information about the cost factors like material or labour and

the revenue related factors like sales analysis. With the help of these reports management can

examine the cost of each product and take appropriate decision for long term profitability.

Revenue reports: revenue reports are associated with the sales figures. These reports are used to

conduct the incomes analysis of business. With the help of revenue reports manager can examine

the changes in sales level and take appropriate step for every shortage (VanBaren, 2017).

Stock and production related reports: regular inventory level reports are produced to maintain

the reasonable level of stock as per production needs. Various production processes related

reports are also prepared for identifying the problems in production process. These reports are

helpful for management in numerous ways.

Budget reports: budget techniques tracks expenses, builds wealth for organization and helps in

achieving the goals. This process is used to make comparison between pre -decided standards

and actual results of business operations. It helps in the efficient planning and forecasting of

funding, strategy and decision- making.

Performance reports: various performance reports like department-wise performance report,

employee productivity report are prepared for reporting purpose. With the help of these reports

management can analyse the performance level for every department and take appropriate action

for deficiency.

6

Cost reports: This report contains information about the cost factors like material or labour and

the revenue related factors like sales analysis. With the help of these reports management can

examine the cost of each product and take appropriate decision for long term profitability.

Revenue reports: revenue reports are associated with the sales figures. These reports are used to

conduct the incomes analysis of business. With the help of revenue reports manager can examine

the changes in sales level and take appropriate step for every shortage (VanBaren, 2017).

Stock and production related reports: regular inventory level reports are produced to maintain

the reasonable level of stock as per production needs. Various production processes related

reports are also prepared for identifying the problems in production process. These reports are

helpful for management in numerous ways.

Budget reports: budget techniques tracks expenses, builds wealth for organization and helps in

achieving the goals. This process is used to make comparison between pre -decided standards

and actual results of business operations. It helps in the efficient planning and forecasting of

funding, strategy and decision- making.

Performance reports: various performance reports like department-wise performance report,

employee productivity report are prepared for reporting purpose. With the help of these reports

management can analyse the performance level for every department and take appropriate action

for deficiency.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1: Evaluate the benefits of management accounting systems and their application within

an organizational context.

Increase efficiency: management accounting technique provides detailed performance analysis

reports of each process and department. Management can use these reports to find-out the

reasons of short performance and take decision accordingly.

Cost control: management accounting tools includes various cost control techniques. These

techniques are very useful in analysis of inventory, production and sales related problems.

Management can examine the problems and try to eliminate it.

Provides support in decision making: effective decision making requires detailed information

about financial statement. Management accounting tools can be used for generating the various

reports. Management can take effective decision on the basis of these reports (Shen, et.al., 2016).

Effective fund management: management accounting examines the funds in detail.

Additionally, it helps in keeping up the backup if there should arise an occurrence of any

direness. Further, it likewise helps in dispensing with any source inside the organization that

abuses the store.

Improved profitability: management techniques like budgetary control and capital budgeting

are used to eliminate the extra expenditure of process. This increases the profit level indirectly.

Increase the cash flow: management accounting covers the detailed study of cash inflow and

outflow. This information can be used for maintaining the appropriate level of cash within

organization for emergency situation.

Information system: Availability of accurate information is necessary for every business.

Management accounting techniques generates various reports which contain useful information

about the business. This information can be used by management for strategy planning.

7

an organizational context.

Increase efficiency: management accounting technique provides detailed performance analysis

reports of each process and department. Management can use these reports to find-out the

reasons of short performance and take decision accordingly.

Cost control: management accounting tools includes various cost control techniques. These

techniques are very useful in analysis of inventory, production and sales related problems.

Management can examine the problems and try to eliminate it.

Provides support in decision making: effective decision making requires detailed information

about financial statement. Management accounting tools can be used for generating the various

reports. Management can take effective decision on the basis of these reports (Shen, et.al., 2016).

Effective fund management: management accounting examines the funds in detail.

Additionally, it helps in keeping up the backup if there should arise an occurrence of any

direness. Further, it likewise helps in dispensing with any source inside the organization that

abuses the store.

Improved profitability: management techniques like budgetary control and capital budgeting

are used to eliminate the extra expenditure of process. This increases the profit level indirectly.

Increase the cash flow: management accounting covers the detailed study of cash inflow and

outflow. This information can be used for maintaining the appropriate level of cash within

organization for emergency situation.

Information system: Availability of accurate information is necessary for every business.

Management accounting techniques generates various reports which contain useful information

about the business. This information can be used by management for strategy planning.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1: how management accounting systems and management accounting reporting are

integrated within organizational processes.

Costing system and reports: cost management techniques and reports gives detailed

information about cost factors. Management can make deep study of each cost factor and

take action appropriately. It also ensures that correct selling price is decided for the

product.

Production reports: the establishment of this system within organization helps the

manager to identify the perfect production cost and appropriate level of inventory to be

maintained.

Revenue reports: this system enables the management to determinate the right price of

product. Management can make analysis about the sales and the change in demand

according to price change. This will helpful for the management to eliminate the wrong

steps taken in sales strategy (VanBaren, 2017).

Integration of Performance reports: performance reports are prepared for identifying

the efficiency level of each employee. The same will help the company to take corrective

step on shortage determinate in performance.

8

integrated within organizational processes.

Costing system and reports: cost management techniques and reports gives detailed

information about cost factors. Management can make deep study of each cost factor and

take action appropriately. It also ensures that correct selling price is decided for the

product.

Production reports: the establishment of this system within organization helps the

manager to identify the perfect production cost and appropriate level of inventory to be

maintained.

Revenue reports: this system enables the management to determinate the right price of

product. Management can make analysis about the sales and the change in demand

according to price change. This will helpful for the management to eliminate the wrong

steps taken in sales strategy (VanBaren, 2017).

Integration of Performance reports: performance reports are prepared for identifying

the efficiency level of each employee. The same will help the company to take corrective

step on shortage determinate in performance.

8

P3. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costing.

Marginal costing – The marginal costing technique of cost accounting is associated with

identifying and considering only the variable cost of production in calculation of unit cost of

product for the company and working out the contribution or marginal contribution achieved by

the company form the manufacturing operations. The marginal costing is also known as relevant

costing technique in which fixed costs associated with the production are ignored while

obtaining the contribution achieved and the same will not be considered in taking decision about

various proposals (Guga& Musa, 2015).

The various features of marginal costing are presented below in order to demonstrate this

technique of costing:

Feature Description

Treatment of fixed cost The fixed costs related with the company are

written off form the profit and loss statement

and the same are not used in calculation of unit

cost of production.

Decision making The concept of marginal costing is an

innovative way of accepting or rejecting the

proposals and the fixed cost are treated as sunk

cost and only marginal cost of production is

taken into consideration in decision making

(Anna, 2015).

Contribution The contribution in marginal costing is

calculated by deducting all the variable cost

form the revenues obtained by the company.

9

statement using marginal and absorption costing.

Marginal costing – The marginal costing technique of cost accounting is associated with

identifying and considering only the variable cost of production in calculation of unit cost of

product for the company and working out the contribution or marginal contribution achieved by

the company form the manufacturing operations. The marginal costing is also known as relevant

costing technique in which fixed costs associated with the production are ignored while

obtaining the contribution achieved and the same will not be considered in taking decision about

various proposals (Guga& Musa, 2015).

The various features of marginal costing are presented below in order to demonstrate this

technique of costing:

Feature Description

Treatment of fixed cost The fixed costs related with the company are

written off form the profit and loss statement

and the same are not used in calculation of unit

cost of production.

Decision making The concept of marginal costing is an

innovative way of accepting or rejecting the

proposals and the fixed cost are treated as sunk

cost and only marginal cost of production is

taken into consideration in decision making

(Anna, 2015).

Contribution The contribution in marginal costing is

calculated by deducting all the variable cost

form the revenues obtained by the company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

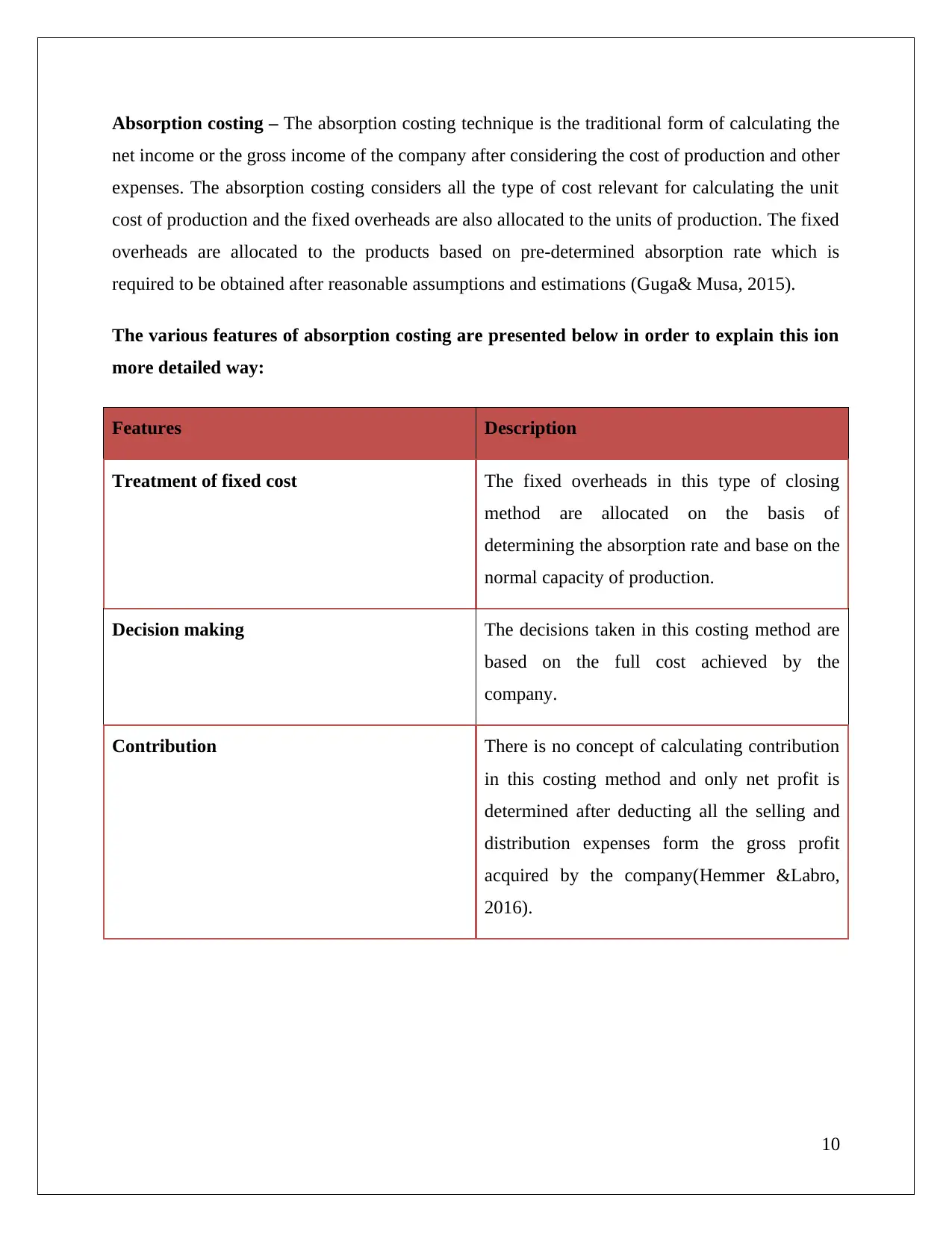

Absorption costing – The absorption costing technique is the traditional form of calculating the

net income or the gross income of the company after considering the cost of production and other

expenses. The absorption costing considers all the type of cost relevant for calculating the unit

cost of production and the fixed overheads are also allocated to the units of production. The fixed

overheads are allocated to the products based on pre-determined absorption rate which is

required to be obtained after reasonable assumptions and estimations (Guga& Musa, 2015).

The various features of absorption costing are presented below in order to explain this ion

more detailed way:

Features Description

Treatment of fixed cost The fixed overheads in this type of closing

method are allocated on the basis of

determining the absorption rate and base on the

normal capacity of production.

Decision making The decisions taken in this costing method are

based on the full cost achieved by the

company.

Contribution There is no concept of calculating contribution

in this costing method and only net profit is

determined after deducting all the selling and

distribution expenses form the gross profit

acquired by the company(Hemmer &Labro,

2016).

10

net income or the gross income of the company after considering the cost of production and other

expenses. The absorption costing considers all the type of cost relevant for calculating the unit

cost of production and the fixed overheads are also allocated to the units of production. The fixed

overheads are allocated to the products based on pre-determined absorption rate which is

required to be obtained after reasonable assumptions and estimations (Guga& Musa, 2015).

The various features of absorption costing are presented below in order to explain this ion

more detailed way:

Features Description

Treatment of fixed cost The fixed overheads in this type of closing

method are allocated on the basis of

determining the absorption rate and base on the

normal capacity of production.

Decision making The decisions taken in this costing method are

based on the full cost achieved by the

company.

Contribution There is no concept of calculating contribution

in this costing method and only net profit is

determined after deducting all the selling and

distribution expenses form the gross profit

acquired by the company(Hemmer &Labro,

2016).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

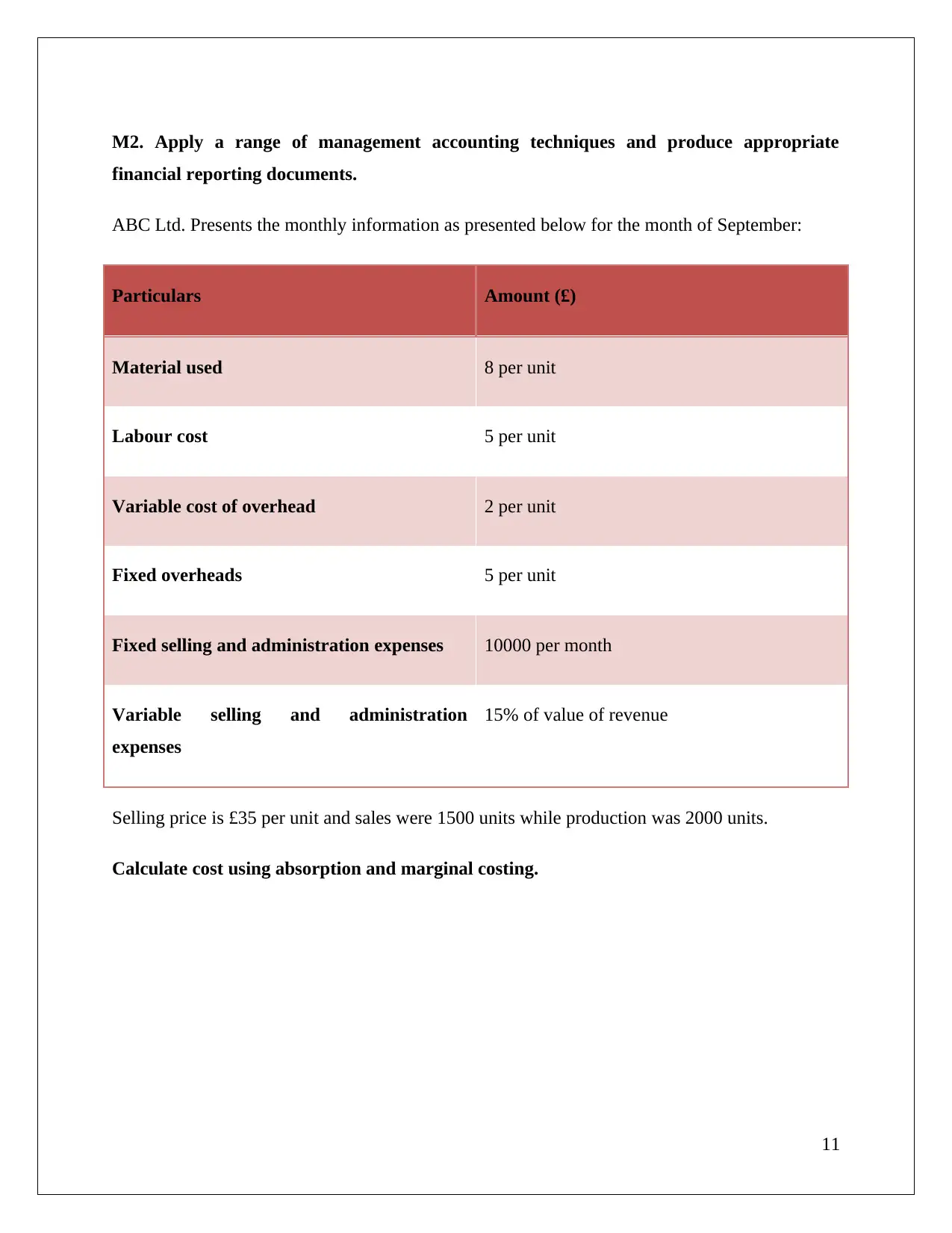

M2. Apply a range of management accounting techniques and produce appropriate

financial reporting documents.

ABC Ltd. Presents the monthly information as presented below for the month of September:

Particulars Amount (£)

Material used 8 per unit

Labour cost 5 per unit

Variable cost of overhead 2 per unit

Fixed overheads 5 per unit

Fixed selling and administration expenses 10000 per month

Variable selling and administration

expenses

15% of value of revenue

Selling price is £35 per unit and sales were 1500 units while production was 2000 units.

Calculate cost using absorption and marginal costing.

11

financial reporting documents.

ABC Ltd. Presents the monthly information as presented below for the month of September:

Particulars Amount (£)

Material used 8 per unit

Labour cost 5 per unit

Variable cost of overhead 2 per unit

Fixed overheads 5 per unit

Fixed selling and administration expenses 10000 per month

Variable selling and administration

expenses

15% of value of revenue

Selling price is £35 per unit and sales were 1500 units while production was 2000 units.

Calculate cost using absorption and marginal costing.

11

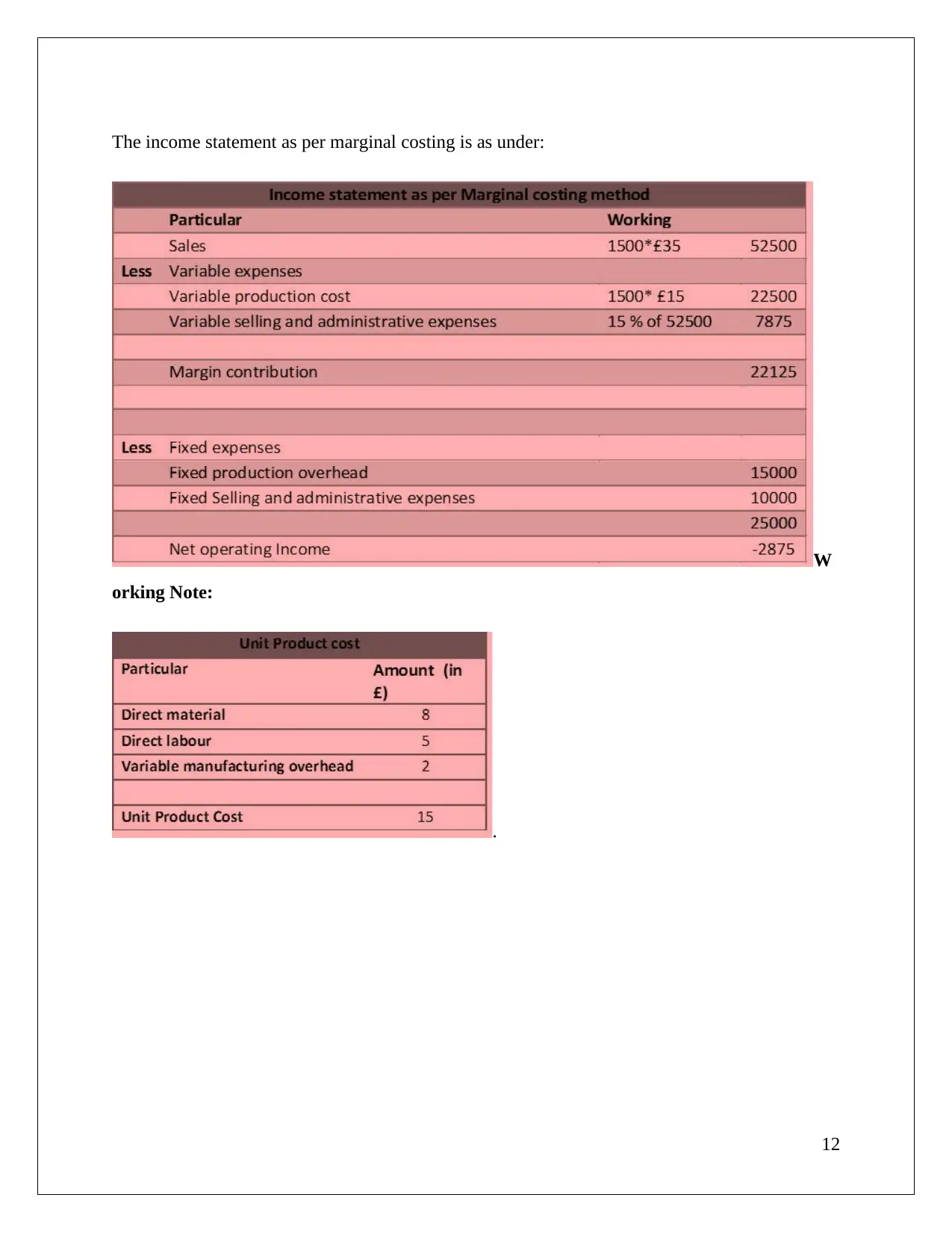

The income statement as per marginal costing is as under:

W

orking Note:

.

12

W

orking Note:

.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.