Cash Flow and Profit Budget Analysis: Westport Leisure Investments

VerifiedAdded on 2023/01/06

|12

|2982

|86

Report

AI Summary

This report presents a detailed budgetary forecast for Westport Leisure Investments Limited, a hotel business in Wales and south-east England. The report focuses on two key components: a cash budget and a profit budget. The cash budget, covering January to June 2020, analyzes cash inflows (sales, food and beverage, rent) and outflows (purchasing, salaries, marketing) to assess the company's liquidity and cash management. The profit budget estimates revenue, expenses, and profit before and after depreciation, providing insights into the company's profitability. The analysis uses the receipt and payment method for the cash budget and includes interpretations of the financial data, highlighting trends and key financial metrics. The report aims to provide a comprehensive financial overview, aiding in decision-making and financial planning for the company.

BUDGETARY

FORECASTS

FORECASTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Cash budget of Westport Leisure Investments Limited ..............................................................1

TASK 2............................................................................................................................................5

Profit budget of Westport Leisure Investments Limited .............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Cash budget of Westport Leisure Investments Limited ..............................................................1

TASK 2............................................................................................................................................5

Profit budget of Westport Leisure Investments Limited .............................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Budget forecast can be define as the tool of financial management which showcase

quantitative expected estimation of cash inflow and outflow as well as expected monetary

revenue generated from various trade activities. In order to understand the concept of budgetary

forecast in brief manner Westport Leisure Investments Limited has been taken. It is a medium

size business organization which run their business trade in hotel industry and provides various

hotel facilities to their customers in Wales and south-east England. The entity provides various

hospitality services to their customers including food and beverage also provides rental facility .

This report is describe the upcoming forecast cash as well as profit budget of the organization.

Through which manager can understand and analysis activities of generating cash inflow as well

as outflow of given time period. This report also show the profit budget which explain the future

profit estimation of the business entity.

TASK 1

Cash budget of Westport Leisure Investments Limited

Cash budget: It is a measurement technique of financial management which help in

defining the estimated and budgeted cash inflow and outflow estimation of any business entity

for a particular time period generality for a financial year which is started wit January to

December or for many organization it is started with April to march. Cash budget is the

statement of showing the future expected cash related activities of the business organization for

specific time period. The main purpose of preparation of this budget is to identify that whenever

organization has the capacity to run their business organization and able to fulfil their day to day

needs and liabilities as well as requirement of cash for fulling short as well as long term needs of

business organization (Ríos, Guillamón, Benito and Bastida, 2018).

Business organization for preparation of the cash budget use various techniques through which

they are able to formulated their statement of cash budget (DeFranco and Schmidgall, 2020). For

this purpose financial manager use to forecast expected sales revenue from their business

activities as well as they also considered those business activities through which cash outflow

has been generated they considered all the relevant expenses which are necessary for running

business organization (Mukherjee Al Rahahleh and Lane, 2016). It considered all the relent

factors which help in defining the essential cash relevant activities. With the use of business cash

1

Budget forecast can be define as the tool of financial management which showcase

quantitative expected estimation of cash inflow and outflow as well as expected monetary

revenue generated from various trade activities. In order to understand the concept of budgetary

forecast in brief manner Westport Leisure Investments Limited has been taken. It is a medium

size business organization which run their business trade in hotel industry and provides various

hotel facilities to their customers in Wales and south-east England. The entity provides various

hospitality services to their customers including food and beverage also provides rental facility .

This report is describe the upcoming forecast cash as well as profit budget of the organization.

Through which manager can understand and analysis activities of generating cash inflow as well

as outflow of given time period. This report also show the profit budget which explain the future

profit estimation of the business entity.

TASK 1

Cash budget of Westport Leisure Investments Limited

Cash budget: It is a measurement technique of financial management which help in

defining the estimated and budgeted cash inflow and outflow estimation of any business entity

for a particular time period generality for a financial year which is started wit January to

December or for many organization it is started with April to march. Cash budget is the

statement of showing the future expected cash related activities of the business organization for

specific time period. The main purpose of preparation of this budget is to identify that whenever

organization has the capacity to run their business organization and able to fulfil their day to day

needs and liabilities as well as requirement of cash for fulling short as well as long term needs of

business organization (Ríos, Guillamón, Benito and Bastida, 2018).

Business organization for preparation of the cash budget use various techniques through which

they are able to formulated their statement of cash budget (DeFranco and Schmidgall, 2020). For

this purpose financial manager use to forecast expected sales revenue from their business

activities as well as they also considered those business activities through which cash outflow

has been generated they considered all the relevant expenses which are necessary for running

business organization (Mukherjee Al Rahahleh and Lane, 2016). It considered all the relent

factors which help in defining the essential cash relevant activities. With the use of business cash

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budget manager able to find out capacity of their organization to assess trade business activities.

With the use of cash budget financial manger can easily interpret that if they do not have relevant

cash capital then they need to raise it by the use of issuing shares or granting loans from financial

institution to run their day to day business activity in an effective manner (Zhou, Mukonza, and

Zvoushe, 2016).

Cash budget play essential part of every Organization whatever it was small or larger or sole

proprietorship as everyone needs to estimate their future cash flow requirement .It is the base of

all the other budget of the entities.

This is essential measurement technique of performance of the business organization as

managing cash and the availability of cash capital the strong position of any business. It is really

essential for maintain liquidity of cash it provide competitive business advantage .It also use to

compare the performance of the organization from past years performance (Mohan and Narwal,

2017).

With the use of cash budget mangers also recognize the timing of shortage of cash and

transaction which require higher availability of cash for run business activities (Goncharenko and

Rassokhina, 2018).

They can control their cash access activities to control wastage spending. By preparation of the

cash budget Westport Leisure Investments Limited will be able to manage their cash capital and

user it only for purposeful business activities. It also useful for the preparation of effective

borrow spending statement for the organization. (Mussari and et.al. 2016).

There will be many methods through which manager of Westport Leisure Investments Limited

use to prepare their budget, it includes, payment and receipt method, profit and loss method, as

well as method of using balance sheet. All theses methods have their own benefits and drawback.

In this report receipt and payment method has been used for the preparation of cash budget. This

cash budget will help the organization to find out there expense regarding proving hotel

facilities, expenses of rent, beverage, food facility , essential items require for competing

marketing needs for run the hospitality business (Reichard and Küchler-Stahn 2019). Manager of

Westport Leisure Investments Limited organization will be able to analysis and understand all

the relent factors that effect their cash business as well as they identify the problems arise and

activities winch require higher cash requirement for the organization. Manager of Westport

Leisure Investments Limited can easily made their future plan regarding expansion of their

2

With the use of cash budget financial manger can easily interpret that if they do not have relevant

cash capital then they need to raise it by the use of issuing shares or granting loans from financial

institution to run their day to day business activity in an effective manner (Zhou, Mukonza, and

Zvoushe, 2016).

Cash budget play essential part of every Organization whatever it was small or larger or sole

proprietorship as everyone needs to estimate their future cash flow requirement .It is the base of

all the other budget of the entities.

This is essential measurement technique of performance of the business organization as

managing cash and the availability of cash capital the strong position of any business. It is really

essential for maintain liquidity of cash it provide competitive business advantage .It also use to

compare the performance of the organization from past years performance (Mohan and Narwal,

2017).

With the use of cash budget mangers also recognize the timing of shortage of cash and

transaction which require higher availability of cash for run business activities (Goncharenko and

Rassokhina, 2018).

They can control their cash access activities to control wastage spending. By preparation of the

cash budget Westport Leisure Investments Limited will be able to manage their cash capital and

user it only for purposeful business activities. It also useful for the preparation of effective

borrow spending statement for the organization. (Mussari and et.al. 2016).

There will be many methods through which manager of Westport Leisure Investments Limited

use to prepare their budget, it includes, payment and receipt method, profit and loss method, as

well as method of using balance sheet. All theses methods have their own benefits and drawback.

In this report receipt and payment method has been used for the preparation of cash budget. This

cash budget will help the organization to find out there expense regarding proving hotel

facilities, expenses of rent, beverage, food facility , essential items require for competing

marketing needs for run the hospitality business (Reichard and Küchler-Stahn 2019). Manager of

Westport Leisure Investments Limited organization will be able to analysis and understand all

the relent factors that effect their cash business as well as they identify the problems arise and

activities winch require higher cash requirement for the organization. Manager of Westport

Leisure Investments Limited can easily made their future plan regarding expansion of their

2

business as well as they understand the effect of various outcomes and relevant business

transactions on business organization. Cash budget helps them to track their January to June

track forecast through which they can prepare other budgets on the basis of their cash budget

(Eulner and Waldbauer,2018).

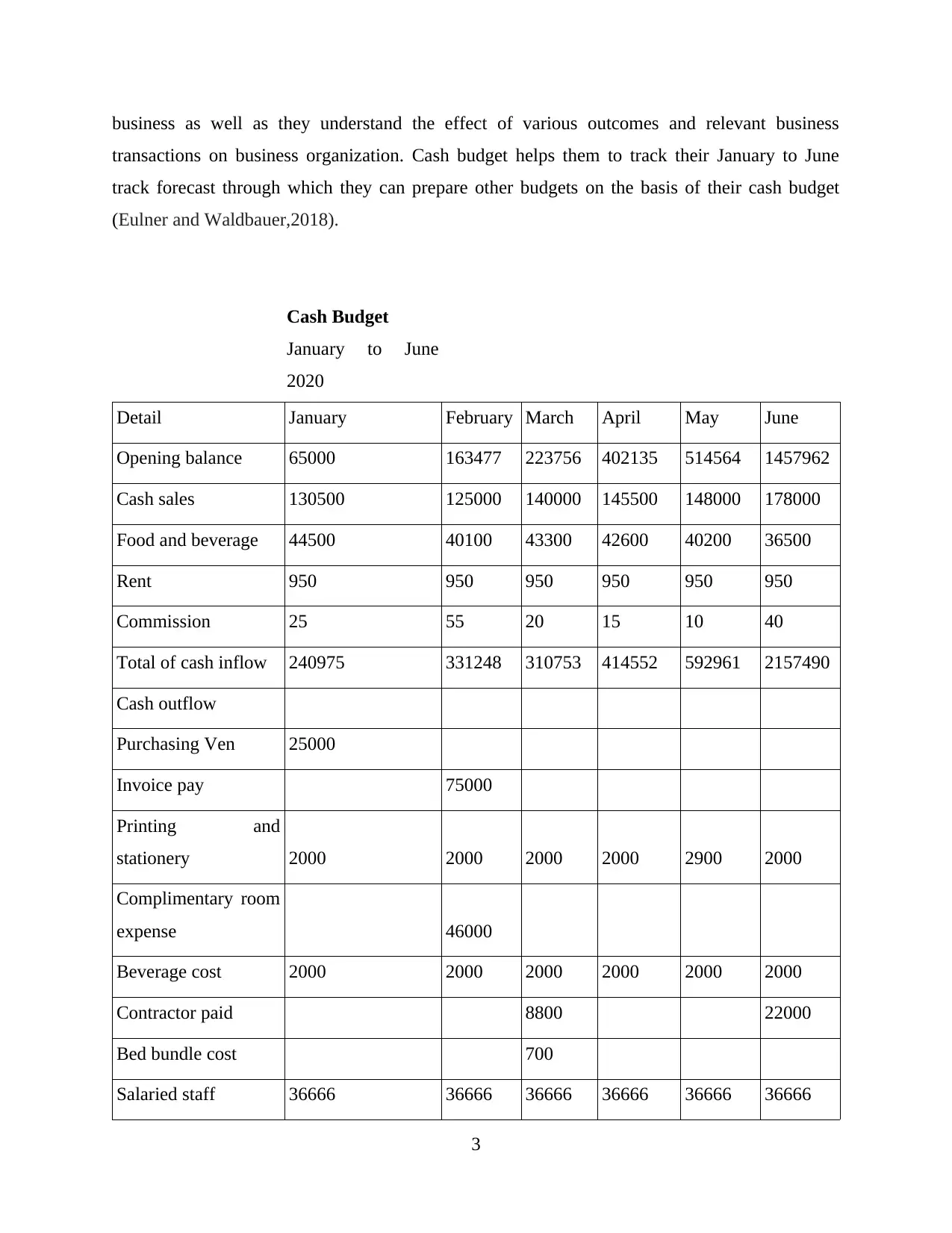

Cash Budget

January to June

2020

Detail January February March April May June

Opening balance 65000 163477 223756 402135 514564 1457962

Cash sales 130500 125000 140000 145500 148000 178000

Food and beverage 44500 40100 43300 42600 40200 36500

Rent 950 950 950 950 950 950

Commission 25 55 20 15 10 40

Total of cash inflow 240975 331248 310753 414552 592961 2157490

Cash outflow

Purchasing Ven 25000

Invoice pay 75000

Printing and

stationery 2000 2000 2000 2000 2900 2000

Complimentary room

expense 46000

Beverage cost 2000 2000 2000 2000 2000 2000

Contractor paid 8800 22000

Bed bundle cost 700

Salaried staff 36666 36666 36666 36666 36666 36666

3

transactions on business organization. Cash budget helps them to track their January to June

track forecast through which they can prepare other budgets on the basis of their cash budget

(Eulner and Waldbauer,2018).

Cash Budget

January to June

2020

Detail January February March April May June

Opening balance 65000 163477 223756 402135 514564 1457962

Cash sales 130500 125000 140000 145500 148000 178000

Food and beverage 44500 40100 43300 42600 40200 36500

Rent 950 950 950 950 950 950

Commission 25 55 20 15 10 40

Total of cash inflow 240975 331248 310753 414552 592961 2157490

Cash outflow

Purchasing Ven 25000

Invoice pay 75000

Printing and

stationery 2000 2000 2000 2000 2900 2000

Complimentary room

expense 46000

Beverage cost 2000 2000 2000 2000 2000 2000

Contractor paid 8800 22000

Bed bundle cost 700

Salaried staff 36666 36666 36666 36666 36666 36666

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

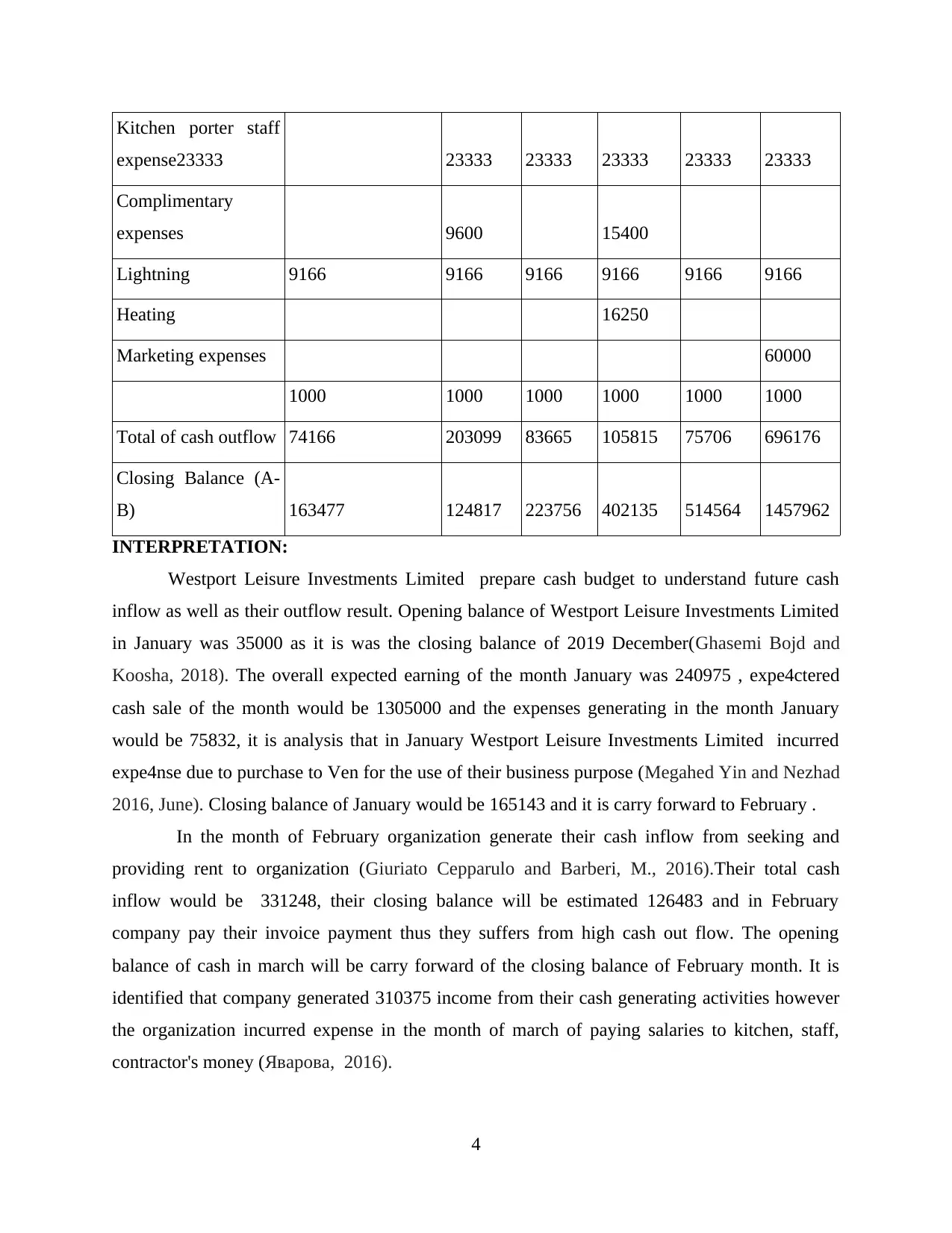

Kitchen porter staff

expense23333 23333 23333 23333 23333 23333

Complimentary

expenses 9600 15400

Lightning 9166 9166 9166 9166 9166 9166

Heating 16250

Marketing expenses 60000

1000 1000 1000 1000 1000 1000

Total of cash outflow 74166 203099 83665 105815 75706 696176

Closing Balance (A-

B) 163477 124817 223756 402135 514564 1457962

INTERPRETATION:

Westport Leisure Investments Limited prepare cash budget to understand future cash

inflow as well as their outflow result. Opening balance of Westport Leisure Investments Limited

in January was 35000 as it is was the closing balance of 2019 December(Ghasemi Bojd and

Koosha, 2018). The overall expected earning of the month January was 240975 , expe4ctered

cash sale of the month would be 1305000 and the expenses generating in the month January

would be 75832, it is analysis that in January Westport Leisure Investments Limited incurred

expe4nse due to purchase to Ven for the use of their business purpose (Megahed Yin and Nezhad

2016, June). Closing balance of January would be 165143 and it is carry forward to February .

In the month of February organization generate their cash inflow from seeking and

providing rent to organization (Giuriato Cepparulo and Barberi, M., 2016).Their total cash

inflow would be 331248, their closing balance will be estimated 126483 and in February

company pay their invoice payment thus they suffers from high cash out flow. The opening

balance of cash in march will be carry forward of the closing balance of February month. It is

identified that company generated 310375 income from their cash generating activities however

the organization incurred expense in the month of march of paying salaries to kitchen, staff,

contractor's money (Яварова, 2016).

4

expense23333 23333 23333 23333 23333 23333

Complimentary

expenses 9600 15400

Lightning 9166 9166 9166 9166 9166 9166

Heating 16250

Marketing expenses 60000

1000 1000 1000 1000 1000 1000

Total of cash outflow 74166 203099 83665 105815 75706 696176

Closing Balance (A-

B) 163477 124817 223756 402135 514564 1457962

INTERPRETATION:

Westport Leisure Investments Limited prepare cash budget to understand future cash

inflow as well as their outflow result. Opening balance of Westport Leisure Investments Limited

in January was 35000 as it is was the closing balance of 2019 December(Ghasemi Bojd and

Koosha, 2018). The overall expected earning of the month January was 240975 , expe4ctered

cash sale of the month would be 1305000 and the expenses generating in the month January

would be 75832, it is analysis that in January Westport Leisure Investments Limited incurred

expe4nse due to purchase to Ven for the use of their business purpose (Megahed Yin and Nezhad

2016, June). Closing balance of January would be 165143 and it is carry forward to February .

In the month of February organization generate their cash inflow from seeking and

providing rent to organization (Giuriato Cepparulo and Barberi, M., 2016).Their total cash

inflow would be 331248, their closing balance will be estimated 126483 and in February

company pay their invoice payment thus they suffers from high cash out flow. The opening

balance of cash in march will be carry forward of the closing balance of February month. It is

identified that company generated 310375 income from their cash generating activities however

the organization incurred expense in the month of march of paying salaries to kitchen, staff,

contractor's money (Яварова, 2016).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The opening balance of April would be estimated 225422 it was identified that

organization generate 414552 income and their outflow in the month of April is estimated

107481 organization paid marke4ting heating and lighting expenses to run their business

activities. In May it will be estimated that Westport Leisure Investments Limited generated their

revenue 592961 for running their business act5ivties and they need to pay expenses. Thus their

balancing value is estimated 516232 and organization also generating their cash inflows from the

moth June is 2157490 the financial manger identified that organization need to pay expense of

salaries paid to their workers and contract's paid (Themsen, T.N., 2019).

Cash flow help manager of Westport Leisure Investments Limited to estimate budget

cash activities through which they can easily identify and recognize the value of all the essential

activities through which help manager to run business in effective and relevant manner. Cash

flow budget use by the manager to develop understating to the manager regarding the estimated

cash generating values of various business activities (Nikulina, 2019).

TASK 2

Profit budget of Westport Leisure Investments Limited

This is the part of financial management tools it also considered as essential budget of the

organization (Nikitina, Litovskaya and Ponomareva, 2018). Profit budget is a numerical

statement through which organization is able to identify the relevant estimation of revenue as

well as expense generated during specific time period and the amount of estimated profit

business organization will be able to generated by performance relevant effective trade functions.

It help Westport Leisure Investments Limited to understand the value of income as well as profit

generated (Mukherjee Al Rahahleh, and Lane 2016). It also estimate the effect of various

business transaction on profit and also useful in comparing the past period profit with estimated

case well as identify the reason and barriers which may effect on the decreasing value of profit.

Profit budget is prepared by Westport Leisure Investments Limited to determine their future

profit which help in comparing and useful for performance management of the entity. In other

words it is relevant and systematic statement which define the net income generated by

organization in specific future time period.

5

organization generate 414552 income and their outflow in the month of April is estimated

107481 organization paid marke4ting heating and lighting expenses to run their business

activities. In May it will be estimated that Westport Leisure Investments Limited generated their

revenue 592961 for running their business act5ivties and they need to pay expenses. Thus their

balancing value is estimated 516232 and organization also generating their cash inflows from the

moth June is 2157490 the financial manger identified that organization need to pay expense of

salaries paid to their workers and contract's paid (Themsen, T.N., 2019).

Cash flow help manager of Westport Leisure Investments Limited to estimate budget

cash activities through which they can easily identify and recognize the value of all the essential

activities through which help manager to run business in effective and relevant manner. Cash

flow budget use by the manager to develop understating to the manager regarding the estimated

cash generating values of various business activities (Nikulina, 2019).

TASK 2

Profit budget of Westport Leisure Investments Limited

This is the part of financial management tools it also considered as essential budget of the

organization (Nikitina, Litovskaya and Ponomareva, 2018). Profit budget is a numerical

statement through which organization is able to identify the relevant estimation of revenue as

well as expense generated during specific time period and the amount of estimated profit

business organization will be able to generated by performance relevant effective trade functions.

It help Westport Leisure Investments Limited to understand the value of income as well as profit

generated (Mukherjee Al Rahahleh, and Lane 2016). It also estimate the effect of various

business transaction on profit and also useful in comparing the past period profit with estimated

case well as identify the reason and barriers which may effect on the decreasing value of profit.

Profit budget is prepared by Westport Leisure Investments Limited to determine their future

profit which help in comparing and useful for performance management of the entity. In other

words it is relevant and systematic statement which define the net income generated by

organization in specific future time period.

5

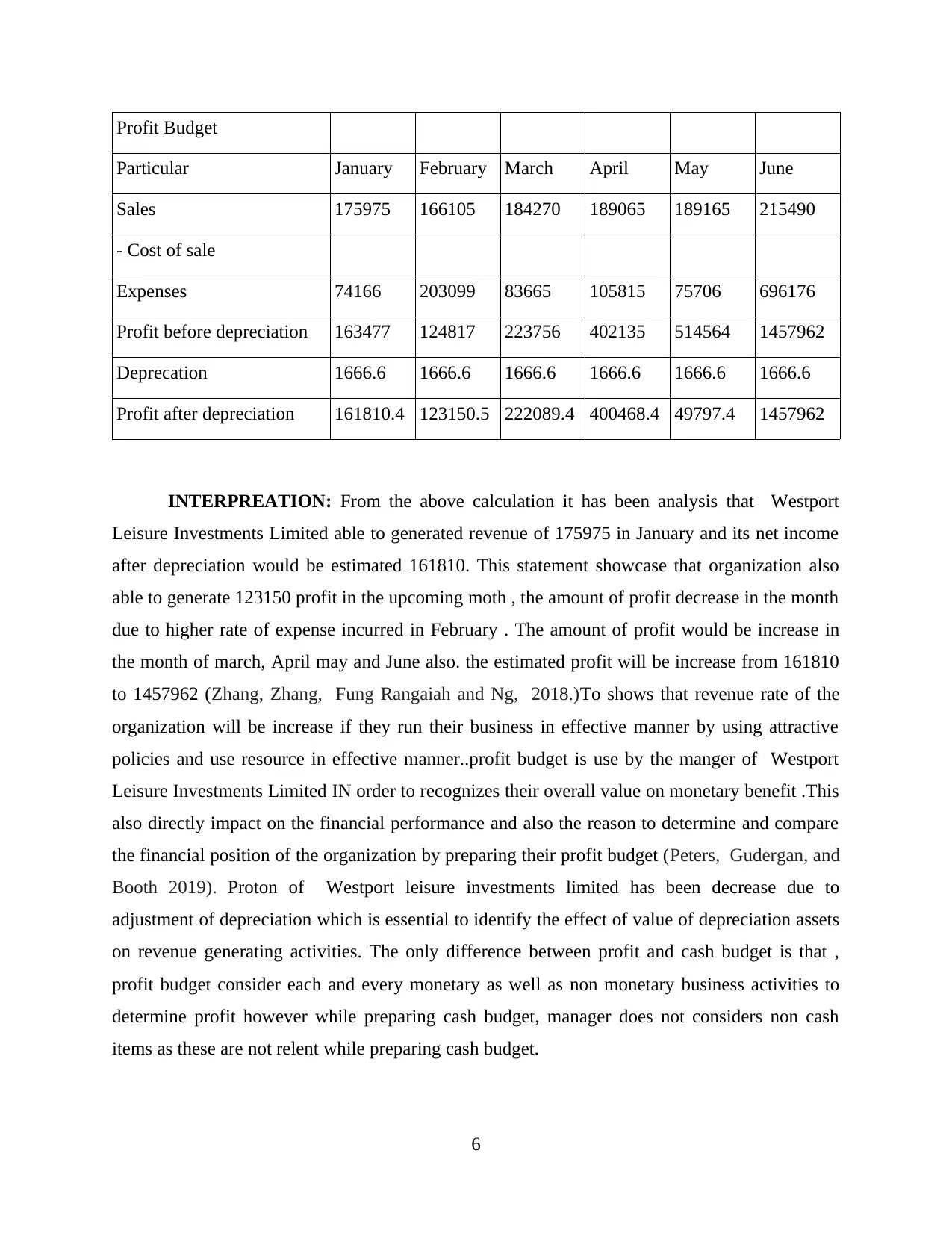

Profit Budget

Particular January February March April May June

Sales 175975 166105 184270 189065 189165 215490

- Cost of sale

Expenses 74166 203099 83665 105815 75706 696176

Profit before depreciation 163477 124817 223756 402135 514564 1457962

Deprecation 1666.6 1666.6 1666.6 1666.6 1666.6 1666.6

Profit after depreciation 161810.4 123150.5 222089.4 400468.4 49797.4 1457962

INTERPREATION: From the above calculation it has been analysis that Westport

Leisure Investments Limited able to generated revenue of 175975 in January and its net income

after depreciation would be estimated 161810. This statement showcase that organization also

able to generate 123150 profit in the upcoming moth , the amount of profit decrease in the month

due to higher rate of expense incurred in February . The amount of profit would be increase in

the month of march, April may and June also. the estimated profit will be increase from 161810

to 1457962 (Zhang, Zhang, Fung Rangaiah and Ng, 2018.)To shows that revenue rate of the

organization will be increase if they run their business in effective manner by using attractive

policies and use resource in effective manner..profit budget is use by the manger of Westport

Leisure Investments Limited IN order to recognizes their overall value on monetary benefit .This

also directly impact on the financial performance and also the reason to determine and compare

the financial position of the organization by preparing their profit budget (Peters, Gudergan, and

Booth 2019). Proton of Westport leisure investments limited has been decrease due to

adjustment of depreciation which is essential to identify the effect of value of depreciation assets

on revenue generating activities. The only difference between profit and cash budget is that ,

profit budget consider each and every monetary as well as non monetary business activities to

determine profit however while preparing cash budget, manager does not considers non cash

items as these are not relent while preparing cash budget.

6

Particular January February March April May June

Sales 175975 166105 184270 189065 189165 215490

- Cost of sale

Expenses 74166 203099 83665 105815 75706 696176

Profit before depreciation 163477 124817 223756 402135 514564 1457962

Deprecation 1666.6 1666.6 1666.6 1666.6 1666.6 1666.6

Profit after depreciation 161810.4 123150.5 222089.4 400468.4 49797.4 1457962

INTERPREATION: From the above calculation it has been analysis that Westport

Leisure Investments Limited able to generated revenue of 175975 in January and its net income

after depreciation would be estimated 161810. This statement showcase that organization also

able to generate 123150 profit in the upcoming moth , the amount of profit decrease in the month

due to higher rate of expense incurred in February . The amount of profit would be increase in

the month of march, April may and June also. the estimated profit will be increase from 161810

to 1457962 (Zhang, Zhang, Fung Rangaiah and Ng, 2018.)To shows that revenue rate of the

organization will be increase if they run their business in effective manner by using attractive

policies and use resource in effective manner..profit budget is use by the manger of Westport

Leisure Investments Limited IN order to recognizes their overall value on monetary benefit .This

also directly impact on the financial performance and also the reason to determine and compare

the financial position of the organization by preparing their profit budget (Peters, Gudergan, and

Booth 2019). Proton of Westport leisure investments limited has been decrease due to

adjustment of depreciation which is essential to identify the effect of value of depreciation assets

on revenue generating activities. The only difference between profit and cash budget is that ,

profit budget consider each and every monetary as well as non monetary business activities to

determine profit however while preparing cash budget, manager does not considers non cash

items as these are not relent while preparing cash budget.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above analysis it has been identified that budgetary forecast is reliable

measurement tool use by financial manager to estimate future cash balance ans well as value of

monetary benefit in terms of profit. Cash budget is estimated tabular statement which show the

cash inflow and cash out flow activities of Westport Leisure Investments Limited . It also useful

in planning and making policies and strategies regarding future business activities in order to

increase cash inflow activities . Manager of Westport Leisure Investments Limited use profit

budget through which they identified that their profit rate has been increase by run business

activities in effective manner.

7

From the above analysis it has been identified that budgetary forecast is reliable

measurement tool use by financial manager to estimate future cash balance ans well as value of

monetary benefit in terms of profit. Cash budget is estimated tabular statement which show the

cash inflow and cash out flow activities of Westport Leisure Investments Limited . It also useful

in planning and making policies and strategies regarding future business activities in order to

increase cash inflow activities . Manager of Westport Leisure Investments Limited use profit

budget through which they identified that their profit rate has been increase by run business

activities in effective manner.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Ríos, A. M., Guillamón, M. D., Benito, B. and Bastida, F., 2018. The influence of transparency

on budget forecast deviations in municipal governments. Journal of Forecasting, 37(4),

pp.457-474.

DeFranco, A. L. and Schmidgall, R. S., 2020. Are We Keeping Our Cash in Our

Hotels?. Journal of Hospitality Financial Management, 28(1), p.7.

Mukherjee, T., Al Rahahleh, N. and Lane, W., 2016. The capital budgeting process of healthcare

organizations: A review of surveys. Journal of Healthcare Management, 61(1), pp.58-

76.

Zhou, G., Mukonza, R.M. and Zvoushe, H., 2016. 10 Public Budgeting in Zimbabwe: Trends,

Processes, and Practices. Public Budgeting in African Nations: Fiscal Analysis in

Development Management, p.234.

Mohan, V. and Narwal, K.P., 2017. Capital budgeting practices: State of the art. Asian Journal

of Research in Banking and Finance, 7(4), pp.57-74.

Goncharenko, O.N. and Rassokhina, Y.G., 2018. PAYMENT SCHEDULE OF CASH FLOWS

AS A BUDGETING TOOL. Modern Science, (11), pp.68-71.

Mussari, R., Tranfaglia, A.E., Reichard, C., Bjørnå, H., Nakrošis, V. and Bankauskaitė-

Grigaliūnienė, S., 2016. Design, trajectories of reform, and implementation of

performance budgeting in local governments: A comparative study of Germany, Italy,

Lithuania, and Norway. In Local public sector reforms in times of crisis (pp. 101-119).

Palgrave Macmillan, London.

Reichard, C. and Küchler-Stahn, N., 2019. Performance budgeting in Germany, Austria and

Switzerland. In Performance-Based Budgeting in the Public Sector (pp. 101-124).

Palgrave Macmillan, Cham.

Eulner, V. and Waldbauer, G., 2018. New development: Cash versus accrual accounting for the

public sector—EPSAS. Public Money & Management, pp.1-4.

Ghasemi Bojd, F. and Koosha, H., 2018. A robust goal programming model for the capital

budgeting problem. Journal of the operational research society, 69(7), pp.1105-1113.

Megahed, A., Yin, P. and Nezhad, H.R.M., 2016, June. An optimization approach to services

sales forecasting in a multi-staged sales pipeline. In 2016 IEEE International

Conference on Services Computing (SCC) (pp. 713-719). IEEE.

Яварова, И.Д., 2016. FINANCIAL PLANNING, FORECASTING, BUDGETING AND

FACTORS AFFECTING THEIR QUALITY. In НАЧАЛО В НАУКЕ (pp. 168-170).

Giuriato, L., Cepparulo, A. and Barberi, M., 2016. Fiscal forecasts and political systems: a

legislative budgeting perspective. Public Choice, 168(1-2), pp.1-22.

Themsen, T.N., 2019. The processes of public megaproject cost estimation: The inaccuracy of

reference class forecasting. Financial Accountability & Management, 35(4), pp.337-

352.

Nikulina, S.N., 2019. Innovative Direction of the Budgeting System Development. In Paper

Materials of the 1st China and CIS Countries Scientific Readings" Urbaniza-tion Level,

Rural Labor Transfer and Economic Growth in the XXI-st Century: Economic Models,

8

Books and journals:

Ríos, A. M., Guillamón, M. D., Benito, B. and Bastida, F., 2018. The influence of transparency

on budget forecast deviations in municipal governments. Journal of Forecasting, 37(4),

pp.457-474.

DeFranco, A. L. and Schmidgall, R. S., 2020. Are We Keeping Our Cash in Our

Hotels?. Journal of Hospitality Financial Management, 28(1), p.7.

Mukherjee, T., Al Rahahleh, N. and Lane, W., 2016. The capital budgeting process of healthcare

organizations: A review of surveys. Journal of Healthcare Management, 61(1), pp.58-

76.

Zhou, G., Mukonza, R.M. and Zvoushe, H., 2016. 10 Public Budgeting in Zimbabwe: Trends,

Processes, and Practices. Public Budgeting in African Nations: Fiscal Analysis in

Development Management, p.234.

Mohan, V. and Narwal, K.P., 2017. Capital budgeting practices: State of the art. Asian Journal

of Research in Banking and Finance, 7(4), pp.57-74.

Goncharenko, O.N. and Rassokhina, Y.G., 2018. PAYMENT SCHEDULE OF CASH FLOWS

AS A BUDGETING TOOL. Modern Science, (11), pp.68-71.

Mussari, R., Tranfaglia, A.E., Reichard, C., Bjørnå, H., Nakrošis, V. and Bankauskaitė-

Grigaliūnienė, S., 2016. Design, trajectories of reform, and implementation of

performance budgeting in local governments: A comparative study of Germany, Italy,

Lithuania, and Norway. In Local public sector reforms in times of crisis (pp. 101-119).

Palgrave Macmillan, London.

Reichard, C. and Küchler-Stahn, N., 2019. Performance budgeting in Germany, Austria and

Switzerland. In Performance-Based Budgeting in the Public Sector (pp. 101-124).

Palgrave Macmillan, Cham.

Eulner, V. and Waldbauer, G., 2018. New development: Cash versus accrual accounting for the

public sector—EPSAS. Public Money & Management, pp.1-4.

Ghasemi Bojd, F. and Koosha, H., 2018. A robust goal programming model for the capital

budgeting problem. Journal of the operational research society, 69(7), pp.1105-1113.

Megahed, A., Yin, P. and Nezhad, H.R.M., 2016, June. An optimization approach to services

sales forecasting in a multi-staged sales pipeline. In 2016 IEEE International

Conference on Services Computing (SCC) (pp. 713-719). IEEE.

Яварова, И.Д., 2016. FINANCIAL PLANNING, FORECASTING, BUDGETING AND

FACTORS AFFECTING THEIR QUALITY. In НАЧАЛО В НАУКЕ (pp. 168-170).

Giuriato, L., Cepparulo, A. and Barberi, M., 2016. Fiscal forecasts and political systems: a

legislative budgeting perspective. Public Choice, 168(1-2), pp.1-22.

Themsen, T.N., 2019. The processes of public megaproject cost estimation: The inaccuracy of

reference class forecasting. Financial Accountability & Management, 35(4), pp.337-

352.

Nikulina, S.N., 2019. Innovative Direction of the Budgeting System Development. In Paper

Materials of the 1st China and CIS Countries Scientific Readings" Urbaniza-tion Level,

Rural Labor Transfer and Economic Growth in the XXI-st Century: Economic Models,

8

New Technologies, Management & Marketing Practices and Mutual

Collaboration" (pp. 404-418).

Nikitina, O.A., Litovskaya, Y.V. and Ponomareva, O.S., 2018. Development of the cost

management mechanism for metal products manufacturing based on budgeting

method. Academy of Strategic Management Journal, 17(5), pp.1-17.

Mukherjee, T., Al Rahahleh, N. and Lane, W., 2016. The capital budgeting process of healthcare

organizations: A review of surveys. Journal of Healthcare Management, 61(1), pp.58-

76.

Zhang, X., Zhang, L., Fung, K.Y., Rangaiah, G.P. and Ng, K.M., 2018. Product design: Impact

of government policy and consumer preference on company profit and corporate social

responsibility. Computers & Chemical Engineering, 118, pp.118-131.

Peters, M.D., Gudergan, S. and Booth, P., 2019. Interactive profit-planning systems and market

turbulence: A dynamic capabilities perspective. Long Range Planning, 52(3), pp.386-

405.

9

Collaboration" (pp. 404-418).

Nikitina, O.A., Litovskaya, Y.V. and Ponomareva, O.S., 2018. Development of the cost

management mechanism for metal products manufacturing based on budgeting

method. Academy of Strategic Management Journal, 17(5), pp.1-17.

Mukherjee, T., Al Rahahleh, N. and Lane, W., 2016. The capital budgeting process of healthcare

organizations: A review of surveys. Journal of Healthcare Management, 61(1), pp.58-

76.

Zhang, X., Zhang, L., Fung, K.Y., Rangaiah, G.P. and Ng, K.M., 2018. Product design: Impact

of government policy and consumer preference on company profit and corporate social

responsibility. Computers & Chemical Engineering, 118, pp.118-131.

Peters, M.D., Gudergan, S. and Booth, P., 2019. Interactive profit-planning systems and market

turbulence: A dynamic capabilities perspective. Long Range Planning, 52(3), pp.386-

405.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.