ACCY918: Income Statement and Budgeting Analysis Report

VerifiedAdded on 2021/04/16

|8

|923

|42

Report

AI Summary

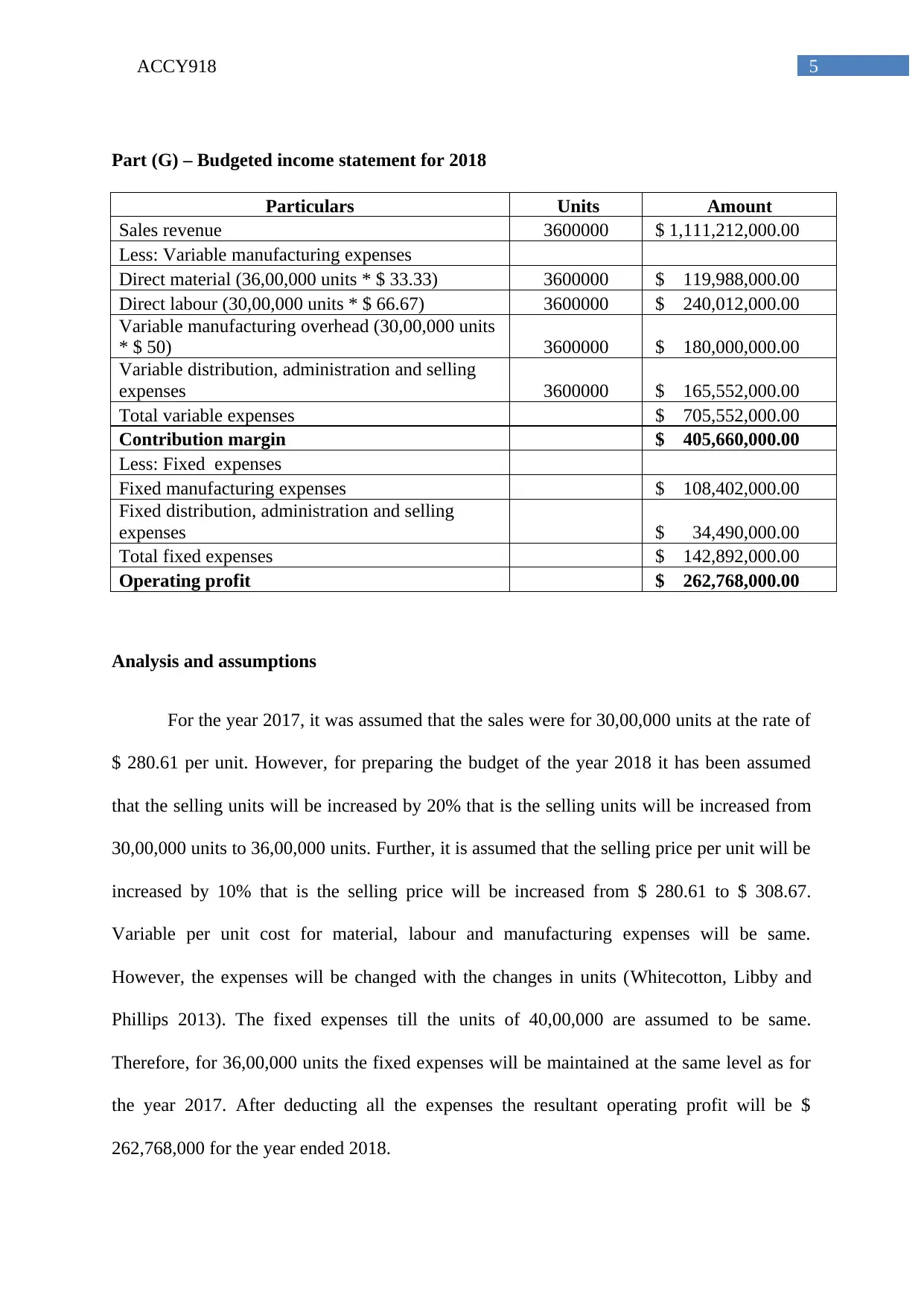

This report, prepared for ACCY918, presents a detailed analysis of income statements using absorption costing and contribution margin methods. It begins by calculating the cost of goods sold and constructing an absorption costing income statement, followed by a contribution margin income statement. The report then provides a budgeted income statement for 2018, projecting sales and costs based on assumptions of increased sales units and selling prices. The analysis includes a breakdown of manufacturing costs, variable and fixed expenses, and a comparison of the two costing methods. The budgeted income statement forecasts an operating profit for 2018. The report concludes with a list of references used in the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.