Managerial Accounting Report: Budgeting, Income Statement - Amani Gold

VerifiedAdded on 2023/04/25

|17

|4389

|356

Report

AI Summary

This report provides a comprehensive analysis of managerial accounting principles, focusing on budgeting approaches and income statement evaluation, specifically in the context of Amani Gold. It breaks down the elements of a master budget, compares top-down and bottom-up budgeting approaches, and suggests the bottom-up approach for Amani Gold. The report also evaluates Amani Gold's income statement, predicting changes in revenue, cost of consultancy, and expenses. A comparison between the budgeted income statement for 2019 and the actual income statement for 2018 reveals that despite increased revenue, higher costs and expenses contribute to greater losses. Desklib offers a wealth of similar solved assignments and study tools to aid students in their academic pursuits.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Managerial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary

The given study has covered the elements prevalent in a master budget and made a

comparison based on bottom-up and top-down approach of budgeting. The report has also

suggested the appropriate budgeting approach for Amani Gold. Some of the other sections of

the study has evaluated the income statement of Amani Gold. This is done by predicting several

changes in budget related to revenue, cost of consultancy and expenses. The overall findings

have revealed that the main components of master budget include an amalgamation of lower

level budget such as sales budget, capital budget, general and administrative expense budget,

direct material budget and directly labour budget. It has been further discussed that the

appropriate budgeting approach for Amani Gold is suggested with proceeding bottom-up

approach. This will allow the company to take budgeting cost estimates of individual items such

as consultancy cost, occupancy expenses, travel expenses and depreciation expenses. A

comparative study on the budgeted income statement of 2019 and actual income statement of

2018 shows that despite of significant increase in the revenue, the cost of goods sold and

expenses has only contributed to more loss. The projected changes are not favourable for the

company.

Executive Summary

The given study has covered the elements prevalent in a master budget and made a

comparison based on bottom-up and top-down approach of budgeting. The report has also

suggested the appropriate budgeting approach for Amani Gold. Some of the other sections of

the study has evaluated the income statement of Amani Gold. This is done by predicting several

changes in budget related to revenue, cost of consultancy and expenses. The overall findings

have revealed that the main components of master budget include an amalgamation of lower

level budget such as sales budget, capital budget, general and administrative expense budget,

direct material budget and directly labour budget. It has been further discussed that the

appropriate budgeting approach for Amani Gold is suggested with proceeding bottom-up

approach. This will allow the company to take budgeting cost estimates of individual items such

as consultancy cost, occupancy expenses, travel expenses and depreciation expenses. A

comparative study on the budgeted income statement of 2019 and actual income statement of

2018 shows that despite of significant increase in the revenue, the cost of goods sold and

expenses has only contributed to more loss. The projected changes are not favourable for the

company.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction.........................................................................................................................3

a. Breaking down the main elements in Master Budget.....................................................3

b. Comparison of top-down and bottom-up approach and applicable approach for

Amani Gold......................................................................................................................................8

c. Budgeted income statement 2019................................................................................10

d. Opinion on the comparison of Budgeted Income Statement and actual statement....11

Conclusion..........................................................................................................................14

References.........................................................................................................................15

Table of Contents

Introduction.........................................................................................................................3

a. Breaking down the main elements in Master Budget.....................................................3

b. Comparison of top-down and bottom-up approach and applicable approach for

Amani Gold......................................................................................................................................8

c. Budgeted income statement 2019................................................................................10

d. Opinion on the comparison of Budgeted Income Statement and actual statement....11

Conclusion..........................................................................................................................14

References.........................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction

Master budget acts as a documented strategy rulebook of expected future sales, capital

investment, purchases and production level which can be referred by a company for making

future predictions on decision making. Therefore, master budget can be identified as an

amalgamation of various types of other bodies such as sales budget, capital budget, general and

administrative expense budget, direct material budget and directly labour budget. The

discussions of the study have not only covered the elements prevalent in a master budget but

also discussed about the comparison based on bottom-up and top-down approach of

budgeting. Some of the other sections of the study has evaluated the income statement of

Amani Gold (listed in ASX) which conducts exploration on flagship projects such as Giro Gold

Project. The report has evaluated the income statement of the company based on several

changes in budget predictions related to revenue, cost of consultancy and expenses. The overall

projections in terms of revenue cost of consultancy and expenses has been identified with a

growth rate of 10%, 8% and 2% respectively. The study has also enumerated on comparison of

actual income and budgeted income of Amani Gold (Kuroki, Hirose and Motokawa 2018).

a. Breaking down the main elements in Master Budget

The general definition of master budget needs to be understood with combination of

lower level budget such as sales budget, capital budget, general and administrative expense

budget, direct material budget and directly labour budget. The presentation of such positive

information is typically published both quarterly or monthly and covers the full fiscal year of a

company. The conceptualisation of such a budgeting practice acts as a guide for the companies

to provide strategic direction for how such a budget will be conducive in accomplishing certain

Introduction

Master budget acts as a documented strategy rulebook of expected future sales, capital

investment, purchases and production level which can be referred by a company for making

future predictions on decision making. Therefore, master budget can be identified as an

amalgamation of various types of other bodies such as sales budget, capital budget, general and

administrative expense budget, direct material budget and directly labour budget. The

discussions of the study have not only covered the elements prevalent in a master budget but

also discussed about the comparison based on bottom-up and top-down approach of

budgeting. Some of the other sections of the study has evaluated the income statement of

Amani Gold (listed in ASX) which conducts exploration on flagship projects such as Giro Gold

Project. The report has evaluated the income statement of the company based on several

changes in budget predictions related to revenue, cost of consultancy and expenses. The overall

projections in terms of revenue cost of consultancy and expenses has been identified with a

growth rate of 10%, 8% and 2% respectively. The study has also enumerated on comparison of

actual income and budgeted income of Amani Gold (Kuroki, Hirose and Motokawa 2018).

a. Breaking down the main elements in Master Budget

The general definition of master budget needs to be understood with combination of

lower level budget such as sales budget, capital budget, general and administrative expense

budget, direct material budget and directly labour budget. The presentation of such positive

information is typically published both quarterly or monthly and covers the full fiscal year of a

company. The conceptualisation of such a budgeting practice acts as a guide for the companies

to provide strategic direction for how such a budget will be conducive in accomplishing certain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

goals which were desired by the managers of the company. Such a budget may also include

necessary provision for inclusion or exclusion of items to attain the required budget (Islam et al.

2016).

The master budget can therefore act as the integral tool for planning which is used by

the management team to judge the performance of different responsibility centres of an entity.

It is the role of senior management to review various iterations which are to be included in the

master budget and maybe the alterations before arriving at the desired result. It is customary

for participative budgeting in arriving at the final budget after prior recommendation of senior

management (Johnson and Pfeiffer 2016). The amalgamation of different budget heads under a

master budget can be noted with the following types of budget.

1. “Sales budget”

2. “Direct labour budget”

3. “Direct materials budget”

4. “Manufacturing overhead budget”

5. “Cash budget”

6. “Ending finished goods budget”

7. “Selling and administrative expense budget”

8. “Production budget”

A sales budget under a master budget would include the segregation of itemised

category for sales expectation during a budgeting period. This can be recorded in both currency

and units. In case a business entity deals with wide variety of products, generally such a budget

aggregates the overall expected sales into smaller number of categories or geographic region.

goals which were desired by the managers of the company. Such a budget may also include

necessary provision for inclusion or exclusion of items to attain the required budget (Islam et al.

2016).

The master budget can therefore act as the integral tool for planning which is used by

the management team to judge the performance of different responsibility centres of an entity.

It is the role of senior management to review various iterations which are to be included in the

master budget and maybe the alterations before arriving at the desired result. It is customary

for participative budgeting in arriving at the final budget after prior recommendation of senior

management (Johnson and Pfeiffer 2016). The amalgamation of different budget heads under a

master budget can be noted with the following types of budget.

1. “Sales budget”

2. “Direct labour budget”

3. “Direct materials budget”

4. “Manufacturing overhead budget”

5. “Cash budget”

6. “Ending finished goods budget”

7. “Selling and administrative expense budget”

8. “Production budget”

A sales budget under a master budget would include the segregation of itemised

category for sales expectation during a budgeting period. This can be recorded in both currency

and units. In case a business entity deals with wide variety of products, generally such a budget

aggregates the overall expected sales into smaller number of categories or geographic region.

5MANAGERIAL ACCOUNTING

The information under such a budget will identify the sources from which sales are coming into

business. This type of budget is conducive for deciding future strategies such as sales promotion

and monitoring the relevant sale of subsidiaries or product lines during a particular financial

year (Miller 2018).

Direct labour budget is with the calculation of total labour hours which are necessary in

producing itemised category of production budget. The more intricate direct labour budget will

include the breakdown of category of labour used by the company. The main advantage for

using this type of budget can be identified with anticipating total number of staffs which is

required in the manufacturing area. The anticipation benefits can be therefore depicted with

hiring needs, layoffs and scheduling overtimes. However, it needs to be noted that such a

budget provides information on an aggregate level and does not typically provide information

on requirement of hiring and layoffs. This form of budget can be produced either quarterly or

monthly basis (Trenovski and Nikolov 2015).

Direct materials budget computes the purchasing requirements of the material in a

certain period for the purpose of attaining the budgetary requirements of production budget.

This form of information is typically presented either in quarterly or monthly overhead in the

annual budget. Such a budget is prepared as per taking aggregate of raw material and planned

ending inventory for computing total raw material required. The total raw material required is

then subtracted with opening balance of raw material inventory to arrive at the Value of raw

material which is to be purchased by a business. In order to accurately computing such a

budget several software packages utilising the concept of material requirements planning is

used (Miller-Nobles, Mattison and Matsumura 2016).

The information under such a budget will identify the sources from which sales are coming into

business. This type of budget is conducive for deciding future strategies such as sales promotion

and monitoring the relevant sale of subsidiaries or product lines during a particular financial

year (Miller 2018).

Direct labour budget is with the calculation of total labour hours which are necessary in

producing itemised category of production budget. The more intricate direct labour budget will

include the breakdown of category of labour used by the company. The main advantage for

using this type of budget can be identified with anticipating total number of staffs which is

required in the manufacturing area. The anticipation benefits can be therefore depicted with

hiring needs, layoffs and scheduling overtimes. However, it needs to be noted that such a

budget provides information on an aggregate level and does not typically provide information

on requirement of hiring and layoffs. This form of budget can be produced either quarterly or

monthly basis (Trenovski and Nikolov 2015).

Direct materials budget computes the purchasing requirements of the material in a

certain period for the purpose of attaining the budgetary requirements of production budget.

This form of information is typically presented either in quarterly or monthly overhead in the

annual budget. Such a budget is prepared as per taking aggregate of raw material and planned

ending inventory for computing total raw material required. The total raw material required is

then subtracted with opening balance of raw material inventory to arrive at the Value of raw

material which is to be purchased by a business. In order to accurately computing such a

budget several software packages utilising the concept of material requirements planning is

used (Miller-Nobles, Mattison and Matsumura 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

Manufacturing overhead budget encompasses different types of cost associated with

manufacturing a product. This typically includes direct material and direct labour to arrive at

the final value. The inclusion of manufacturing overhead budget is also essential element of

COGS line item in the master budget. The computation of total cost based on this budget uses

conversion of per unit overhead allocation which is able to derive the total cost of finished

goods inventory. After the diversion of total cost this is shown in the budgeted balance sheet.

The presentation of information in such a budget is conducive for various types of

departmental budgeting models as it consists of vast proportion of data on company’s

expenditures. The presentation of manufacturing budget can be done both in a monthly or

quarterly format (Weygandt, Kimmel and Kieso D2015).

“Cash budgets” are essential in planning of the advertisements related to expected cash

receipt or planned cash receipt. These budgets are seen to consider outflows and inflows of

expenses paid, revenues and receipts pertaining to loans. Therefore, cash budget is an

estimation of future prediction of company’s cash. The management team usually develops

cash budget after preparation of capital expenditure, purchases and sales budgets. The

aforementioned budgets should be put to use before cash budget in order to get an accurate

estimation of how cash can be impacted. The overall depictions revealed that management can

use such a budget to manage the cash flows of the company and areas of shortfalls in cash

balance (Wright 2017).

“Ending finished goods budget” is concerned with computing the cost of finished goods

inventory during closure of a budgeting period. Such a budget usually incorporates the unit

Manufacturing overhead budget encompasses different types of cost associated with

manufacturing a product. This typically includes direct material and direct labour to arrive at

the final value. The inclusion of manufacturing overhead budget is also essential element of

COGS line item in the master budget. The computation of total cost based on this budget uses

conversion of per unit overhead allocation which is able to derive the total cost of finished

goods inventory. After the diversion of total cost this is shown in the budgeted balance sheet.

The presentation of information in such a budget is conducive for various types of

departmental budgeting models as it consists of vast proportion of data on company’s

expenditures. The presentation of manufacturing budget can be done both in a monthly or

quarterly format (Weygandt, Kimmel and Kieso D2015).

“Cash budgets” are essential in planning of the advertisements related to expected cash

receipt or planned cash receipt. These budgets are seen to consider outflows and inflows of

expenses paid, revenues and receipts pertaining to loans. Therefore, cash budget is an

estimation of future prediction of company’s cash. The management team usually develops

cash budget after preparation of capital expenditure, purchases and sales budgets. The

aforementioned budgets should be put to use before cash budget in order to get an accurate

estimation of how cash can be impacted. The overall depictions revealed that management can

use such a budget to manage the cash flows of the company and areas of shortfalls in cash

balance (Wright 2017).

“Ending finished goods budget” is concerned with computing the cost of finished goods

inventory during closure of a budgeting period. Such a budget usually incorporates the unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

quantity for finished goods at the end of each budgeting period. However, the real source of

certain information is found in production budget. The primary reason of preparing such a

budget is to provide an estimate of inventory asset which usually appears under the budgeted

balance sheet. The company uses such information about the total amount of cash required for

the investing activities in an asset. Henceforth, in case there is no intention to create a

budgeted balance sheet then ending finished goods budget also need not be prepared. Such a

budget is conducive for closely monitoring the balance of cash on an ongoing basis. The basic

components included under such a budget can be identified with direct material is, overhead

allocation and direct labour (Vallero et al. 2018).

“Selling and administrative expense budget” encompasses various aspects of budgeting

for nonmanufacturing activities such as engineering, facilities, marketing, accounting and sales.

The overall use of such a budget can be compared with the production budget. This typically

comprises of preparation of financial report based on quarterly or monthly basis. In many cases,

such a budget requires splitting of the cost into different segments like marketing budget,

separate sales budget and administration budget. The information under such a budget cannot

be directly derived from any other budget. Instead, the management team can incorporate

general level of organisational activities for ascertaining the exact level of expenditures. These

expenditures can involve analyses based on activity based costing and different types of other

activities which require change in capital spending. This budget may also include some

instances of bottleneck operations which includes amount of expenditures in a specific time

period (Timonen et al. 2017).

“Production budget” is used for computing total units of products which are to be

derived and manufactured as a result of combination of sales forecast and amount of finished

quantity for finished goods at the end of each budgeting period. However, the real source of

certain information is found in production budget. The primary reason of preparing such a

budget is to provide an estimate of inventory asset which usually appears under the budgeted

balance sheet. The company uses such information about the total amount of cash required for

the investing activities in an asset. Henceforth, in case there is no intention to create a

budgeted balance sheet then ending finished goods budget also need not be prepared. Such a

budget is conducive for closely monitoring the balance of cash on an ongoing basis. The basic

components included under such a budget can be identified with direct material is, overhead

allocation and direct labour (Vallero et al. 2018).

“Selling and administrative expense budget” encompasses various aspects of budgeting

for nonmanufacturing activities such as engineering, facilities, marketing, accounting and sales.

The overall use of such a budget can be compared with the production budget. This typically

comprises of preparation of financial report based on quarterly or monthly basis. In many cases,

such a budget requires splitting of the cost into different segments like marketing budget,

separate sales budget and administration budget. The information under such a budget cannot

be directly derived from any other budget. Instead, the management team can incorporate

general level of organisational activities for ascertaining the exact level of expenditures. These

expenditures can involve analyses based on activity based costing and different types of other

activities which require change in capital spending. This budget may also include some

instances of bottleneck operations which includes amount of expenditures in a specific time

period (Timonen et al. 2017).

“Production budget” is used for computing total units of products which are to be

derived and manufactured as a result of combination of sales forecast and amount of finished

8MANAGERIAL ACCOUNTING

goods inventory on hand. The typical elements of production budget are also inclusive of push

manufacturing system which is an integral part of MRP environment. This is typically presented

in both monthly or quarterly format. The evaluation of such a budget is based on aggregation of

forecasted unit sales and planned finished goods ending inventory balance to arrive at the

value of total production requirement. The total production required is then subtracted with

beginning finished goods inventory to arrive at the value of products to be manufactured. In

general, the management may face several difficulties in creating comprehensive production

budget as it involves forecasting of variation of individual activities which the company plans to

produce and sell. Therefore, it is customary for a business organisation to forecast such an

information based on similar characteristics (Callen 2016).

b. Comparison of top-down and bottom-up approach and applicable approach for Amani Gold

A top-down Budgeting approach is considered as that budgeting approach in which the

ultimate budget holder does not have the opportunity to participate in the budgeting process.

On the contrary, a bottom-up approach in budgeting is depicted as that system of budgeting in

which budget holders have greater flexibility of participating in the budget process and

providing estimates about their own budget to the senior management. Such a budgeting

system is also defined as participatory budgeting process (Demski 2017).

The use of bottom-up approach usually instigates motivation among the employees due

to control and ownership of the budget. However, there is a possibility of senior management

resenting on the loss of control. It is also regarded that bottom of budgeting approach provides

a better estimation of budgeting requirements as the employees are familiar with departmental

costs involved in a budget. On the contrary, this may also create dysfunctional behaviour

goods inventory on hand. The typical elements of production budget are also inclusive of push

manufacturing system which is an integral part of MRP environment. This is typically presented

in both monthly or quarterly format. The evaluation of such a budget is based on aggregation of

forecasted unit sales and planned finished goods ending inventory balance to arrive at the

value of total production requirement. The total production required is then subtracted with

beginning finished goods inventory to arrive at the value of products to be manufactured. In

general, the management may face several difficulties in creating comprehensive production

budget as it involves forecasting of variation of individual activities which the company plans to

produce and sell. Therefore, it is customary for a business organisation to forecast such an

information based on similar characteristics (Callen 2016).

b. Comparison of top-down and bottom-up approach and applicable approach for Amani Gold

A top-down Budgeting approach is considered as that budgeting approach in which the

ultimate budget holder does not have the opportunity to participate in the budgeting process.

On the contrary, a bottom-up approach in budgeting is depicted as that system of budgeting in

which budget holders have greater flexibility of participating in the budget process and

providing estimates about their own budget to the senior management. Such a budgeting

system is also defined as participatory budgeting process (Demski 2017).

The use of bottom-up approach usually instigates motivation among the employees due

to control and ownership of the budget. However, there is a possibility of senior management

resenting on the loss of control. It is also regarded that bottom of budgeting approach provides

a better estimation of budgeting requirements as the employees are familiar with departmental

costs involved in a budget. On the contrary, this may also create dysfunctional behaviour

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

among the senior management as there is a possibility that such objectives are not in line with

the corporate objectives. This calls for the need of top-down approach which focuses on

divisional concerns along with corporate objectives. Some of the other points in favour of

bottom-up budgeting approach can be considered with increased understanding of manager’s

commitment. It needs to be also noted bottom-up budgeting approach can lead to poor

decision-making by the involvement of inexperienced managers. The bottom budgeting

approach also drives better communication between departments and provides opportunity for

the senior management to concentrate on the main strategy (Magnan, Wang and Shi 2016).

The appropriate budgeting approach for Amani Gold is suggested with proceeding

bottom-up approach. This will allow the company to take budgeting cost estimates of individual

items such as consultancy cost, occupancy expenses, travel expenses and depreciation

expenses. On the other hand, the use of top-down approach will allow the company to get a

better estimation of cost associated to employee benefits expenses, foreign exchange loss and

share-based payments expenses. Despite of this fact, as the expenses such as consultancy cost,

occupancy expenses, travel expenses and depreciation expenses have a greater share in the

income statement, it is more feasible to adopt bottom-up budgeting approach. Some of the

main advantages for Amani Gold will be instantly seen in estimating the cost of projects such as

Giro Gold Project, Kebigada and Satellite Project and the project of Douze Match. The overall

benefits of consideration of participatory budget will allow flexibility of participating and

providing estimates about their own budget to the senior management. Additionally, the

employees will be more aware of the budgeted estimates of the project such as Giro Gold

Project, Kebigada and Satellite Project and the project of Douze Match. However, in order to

ensure that bottom of budgeting approach is most effectively applied, it needs to be

among the senior management as there is a possibility that such objectives are not in line with

the corporate objectives. This calls for the need of top-down approach which focuses on

divisional concerns along with corporate objectives. Some of the other points in favour of

bottom-up budgeting approach can be considered with increased understanding of manager’s

commitment. It needs to be also noted bottom-up budgeting approach can lead to poor

decision-making by the involvement of inexperienced managers. The bottom budgeting

approach also drives better communication between departments and provides opportunity for

the senior management to concentrate on the main strategy (Magnan, Wang and Shi 2016).

The appropriate budgeting approach for Amani Gold is suggested with proceeding

bottom-up approach. This will allow the company to take budgeting cost estimates of individual

items such as consultancy cost, occupancy expenses, travel expenses and depreciation

expenses. On the other hand, the use of top-down approach will allow the company to get a

better estimation of cost associated to employee benefits expenses, foreign exchange loss and

share-based payments expenses. Despite of this fact, as the expenses such as consultancy cost,

occupancy expenses, travel expenses and depreciation expenses have a greater share in the

income statement, it is more feasible to adopt bottom-up budgeting approach. Some of the

main advantages for Amani Gold will be instantly seen in estimating the cost of projects such as

Giro Gold Project, Kebigada and Satellite Project and the project of Douze Match. The overall

benefits of consideration of participatory budget will allow flexibility of participating and

providing estimates about their own budget to the senior management. Additionally, the

employees will be more aware of the budgeted estimates of the project such as Giro Gold

Project, Kebigada and Satellite Project and the project of Douze Match. However, in order to

ensure that bottom of budgeting approach is most effectively applied, it needs to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

ascertained by the Departmental managers to ensure that this type of budgeting practices is

following the commitments made in the corporate objectives. Moreover, the consideration of

day to day activities in the bottom of approach will be conducive in getting a better estimate of

the line items (Koijen and Yogo 2015).

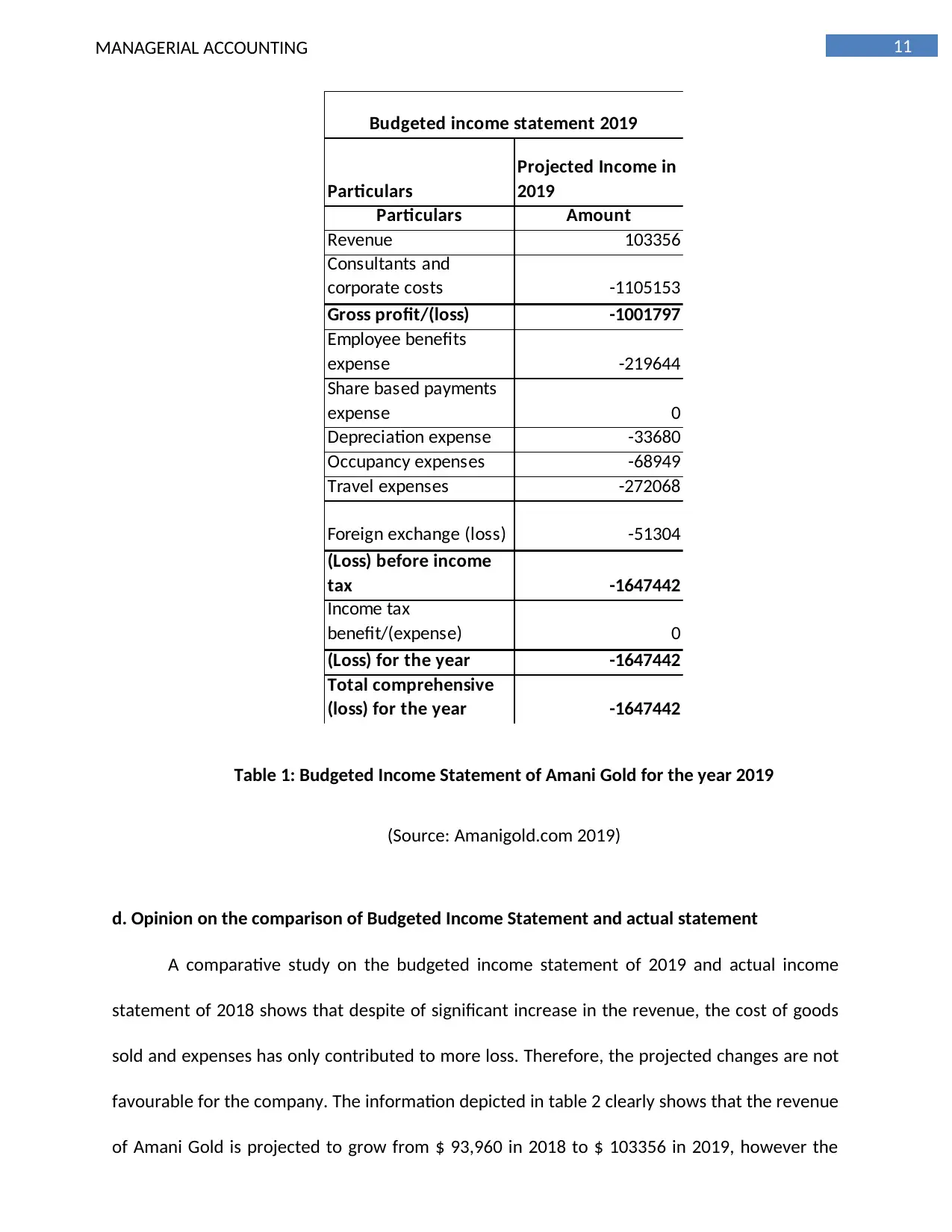

c. Budgeted income statement 2019

The preparation of budgeted income statement for Amani Gold is based on budget

predictions related to revenue, cost of consultancy and expenses. The overall projections in

terms of revenue cost of consultancy and expenses has been identified with a growth rate of

10%, 8% and 2% respectively. The revenue of the company is projected to grow from $ 93,960

in 2018 to $ 103356 in 2019 pertaining to 10% increase. As the company does not manufacture

any goods the main cost for providing services adding to the revenue is considered with

consultants and corporate costs. This cost increased from $ -10,23,290 in 2018 to $ -1105153 in

2019 as a result of 8% increase of projected changes (Konchitchki 2016).

The main items of expenses from the table 1 can be identified with “Employee benefits

expense”, “Share based payments expense”, “Depreciation expense”, “Occupancy expenses”,

“Travel expenses” and “Foreign exchange (loss)”. The 2% increase in all the heads of expenses

has led to a significant increase in losses generated before income tax and total comprehensive

loss for the year. It can be seen that the total loss incurred by the company has increased from

$ -15,62,315 in 2018 to $ -16,47,442 in 2019. This is due to the increasing nature of expenses

such as employee benefits expense which increased from $ -2,15,337 in 2018 to $ -219644 in

2019. Similarly, the occupancy expenses also increased from $ -67,597 in 2018 to $ -68949 in

2019 (Shah 2018).

ascertained by the Departmental managers to ensure that this type of budgeting practices is

following the commitments made in the corporate objectives. Moreover, the consideration of

day to day activities in the bottom of approach will be conducive in getting a better estimate of

the line items (Koijen and Yogo 2015).

c. Budgeted income statement 2019

The preparation of budgeted income statement for Amani Gold is based on budget

predictions related to revenue, cost of consultancy and expenses. The overall projections in

terms of revenue cost of consultancy and expenses has been identified with a growth rate of

10%, 8% and 2% respectively. The revenue of the company is projected to grow from $ 93,960

in 2018 to $ 103356 in 2019 pertaining to 10% increase. As the company does not manufacture

any goods the main cost for providing services adding to the revenue is considered with

consultants and corporate costs. This cost increased from $ -10,23,290 in 2018 to $ -1105153 in

2019 as a result of 8% increase of projected changes (Konchitchki 2016).

The main items of expenses from the table 1 can be identified with “Employee benefits

expense”, “Share based payments expense”, “Depreciation expense”, “Occupancy expenses”,

“Travel expenses” and “Foreign exchange (loss)”. The 2% increase in all the heads of expenses

has led to a significant increase in losses generated before income tax and total comprehensive

loss for the year. It can be seen that the total loss incurred by the company has increased from

$ -15,62,315 in 2018 to $ -16,47,442 in 2019. This is due to the increasing nature of expenses

such as employee benefits expense which increased from $ -2,15,337 in 2018 to $ -219644 in

2019. Similarly, the occupancy expenses also increased from $ -67,597 in 2018 to $ -68949 in

2019 (Shah 2018).

11MANAGERIAL ACCOUNTING

Particulars

Projected Income in

2019

Particulars Amount

Revenue 103356

Consultants and

corporate costs -1105153

Gross profit/(loss) -1001797

Employee benefits

expense -219644

Share based payments

expense 0

Depreciation expense -33680

Occupancy expenses -68949

Travel expenses -272068

Foreign exchange (loss) -51304

(Loss) before income

tax -1647442

Income tax

benefit/(expense) 0

(Loss) for the year -1647442

Total comprehensive

(loss) for the year -1647442

Budgeted income statement 2019

Table 1: Budgeted Income Statement of Amani Gold for the year 2019

(Source: Amanigold.com 2019)

d. Opinion on the comparison of Budgeted Income Statement and actual statement

A comparative study on the budgeted income statement of 2019 and actual income

statement of 2018 shows that despite of significant increase in the revenue, the cost of goods

sold and expenses has only contributed to more loss. Therefore, the projected changes are not

favourable for the company. The information depicted in table 2 clearly shows that the revenue

of Amani Gold is projected to grow from $ 93,960 in 2018 to $ 103356 in 2019, however the

Particulars

Projected Income in

2019

Particulars Amount

Revenue 103356

Consultants and

corporate costs -1105153

Gross profit/(loss) -1001797

Employee benefits

expense -219644

Share based payments

expense 0

Depreciation expense -33680

Occupancy expenses -68949

Travel expenses -272068

Foreign exchange (loss) -51304

(Loss) before income

tax -1647442

Income tax

benefit/(expense) 0

(Loss) for the year -1647442

Total comprehensive

(loss) for the year -1647442

Budgeted income statement 2019

Table 1: Budgeted Income Statement of Amani Gold for the year 2019

(Source: Amanigold.com 2019)

d. Opinion on the comparison of Budgeted Income Statement and actual statement

A comparative study on the budgeted income statement of 2019 and actual income

statement of 2018 shows that despite of significant increase in the revenue, the cost of goods

sold and expenses has only contributed to more loss. Therefore, the projected changes are not

favourable for the company. The information depicted in table 2 clearly shows that the revenue

of Amani Gold is projected to grow from $ 93,960 in 2018 to $ 103356 in 2019, however the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.