Managerial Accounting: A Report on Budgeting Approaches Analysis

VerifiedAdded on 2023/06/03

|17

|4144

|412

Report

AI Summary

This report delves into the concept of budgeting within managerial accounting, providing a literature review and analysis based on two journal articles. The articles explore traditional budgeting methods and newer approaches, including a case study of Mainfreight, which operates without traditional budgeting, and an examination of public budgeting practices. The report discusses the purpose of these studies, highlighting their research questions related to the effectiveness of different budgeting approaches and their alignment with current theories. Similarities and differences between the studies are analyzed, focusing on the role of budgeting in management control systems and public organizations. Finally, the report identifies four key lessons learned from the research findings that could be valuable for management accountants in Australian companies, emphasizing the importance of cost control, financial planning, and strategic resource allocation.

Managerial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING: 1

Executive summary

This report discusses about a concept of a budgeting as an accounting method. It has a

literature review of the topic with the relevant analysis of the topic through journals. These

two articles, which are chosen for the analysis focuses on the concept of traditional budgeting

and new approaches of budgeting.

Executive summary

This report discusses about a concept of a budgeting as an accounting method. It has a

literature review of the topic with the relevant analysis of the topic through journals. These

two articles, which are chosen for the analysis focuses on the concept of traditional budgeting

and new approaches of budgeting.

MANAGERIAL ACCOUNTING: 2

Contents

Introduction...........................................................................................................................................2

Explanation of Budgeting......................................................................................................................2

Explanation of purpose of two studies undertaken to understand budgeting.........................................7

Similarities and differences in two studies............................................................................................8

Four specific outcomes or lessons learned from the two studies’ research findings that will be useful

for management accountants in Australian companies........................................................................10

Conclusion...........................................................................................................................................11

References...........................................................................................................................................13

Contents

Introduction...........................................................................................................................................2

Explanation of Budgeting......................................................................................................................2

Explanation of purpose of two studies undertaken to understand budgeting.........................................7

Similarities and differences in two studies............................................................................................8

Four specific outcomes or lessons learned from the two studies’ research findings that will be useful

for management accountants in Australian companies........................................................................10

Conclusion...........................................................................................................................................11

References...........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING: 3

Introduction

This report brings out the discussion on budgeting based on managerial accounting. A budget

is a pre-determined statement of cost of project. To control the cost of a project, a budget plan

estimates the cash flow associated with the control. A final cost provides a baseline to assess

the financial performance of the project. The extent to which cost is within the detailed cost

estimation, the project is still under the financial control. As soon as the cost overruns, the

possibility of occurring problems become severe. Preparation of budget follows an

organisational pattern of responsibility and authority. Budget provides a control system

through which both feed forward and feedback are connected.

The purpose of using feedback can enable organisation to find out the variation between

executed budget and the actual performance. This report bring out the discussion on two

reviewed articles of renowned journals named Auditing & Accountability Journal. Both

articles have discussed two different viewpoints. First has discussed the case study of Main

freight that layouts and follows non-budgeting method in its management control system. The

another article highlights the public budgeting that determines how public administration

operates with the modern and new approaches of budgeting.

Explanation of Budgeting

According to Leoissac, (2018), Budgeting is a procedure of making a strategic plan that

elaborates how to spend the money. A systematic expenditure plan of money that determine

in advance that how the assigned money to an task will be spent or how the business plan do

the things to use the particular sum of money for a particular task to attain maximum

satisfaction. Budgeting is an inseparable of business operations because it is an economic

concept that resources are always scare. Experts plays an important role in accomplishing

their goals or set objectives through proper planning by applying their knowledge and

experiences to make a plan. Once experts prepare the budget and starts using the scare

Introduction

This report brings out the discussion on budgeting based on managerial accounting. A budget

is a pre-determined statement of cost of project. To control the cost of a project, a budget plan

estimates the cash flow associated with the control. A final cost provides a baseline to assess

the financial performance of the project. The extent to which cost is within the detailed cost

estimation, the project is still under the financial control. As soon as the cost overruns, the

possibility of occurring problems become severe. Preparation of budget follows an

organisational pattern of responsibility and authority. Budget provides a control system

through which both feed forward and feedback are connected.

The purpose of using feedback can enable organisation to find out the variation between

executed budget and the actual performance. This report bring out the discussion on two

reviewed articles of renowned journals named Auditing & Accountability Journal. Both

articles have discussed two different viewpoints. First has discussed the case study of Main

freight that layouts and follows non-budgeting method in its management control system. The

another article highlights the public budgeting that determines how public administration

operates with the modern and new approaches of budgeting.

Explanation of Budgeting

According to Leoissac, (2018), Budgeting is a procedure of making a strategic plan that

elaborates how to spend the money. A systematic expenditure plan of money that determine

in advance that how the assigned money to an task will be spent or how the business plan do

the things to use the particular sum of money for a particular task to attain maximum

satisfaction. Budgeting is an inseparable of business operations because it is an economic

concept that resources are always scare. Experts plays an important role in accomplishing

their goals or set objectives through proper planning by applying their knowledge and

experiences to make a plan. Once experts prepare the budget and starts using the scare

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING: 4

resources accordingly. It gives them a sense of satisfaction after 6 months when they find

them efficiently by following the roadmap. Budget will always give a feeling that you have

an assigned amount of money for a particular task or next task.

According to Andor, Mohanty and Toth, (2015), Following a budget or expenditure plan will

assist the company to form its capital structure whether the operations of the company should

rely on capital and debt or decide the proportion of debt or equity in the budget plan. By

forecasting the future financial expenditure, it gives an overview of which month will be

financially tight once the annual budget report are forecasted. Using a realistic and efficient

budget helps to forecast the spending for a fiscal year that will result in long-term financial

planning. It enables the vision to complex current market situation that can make realistic

assumptions regarding annual income, planning for long term goals, buying the investment,

and recreation property. There is no particular single budget defined for business. Budget

assists the business to track and manage the resources. Business entities use a varied kind of

budget for every department. Budgeting decides the expenditure and form effective strategies

that will maximise the revenue and valuation of assets.

Otley, (2016), Common types of budgets used by the business such as master budget, static

budget, financial budget, cash flow budget, and operating budget. A master budget is

aggregation of the entire individual budget plan of each department from operation,

marketing, sales to finance. A master budget reflects a complete picture of the financial

health of the business. There are several factors that is contained in master budget such as

sales, asset valuation, outstanding payments, operating expenses, and income streams. These

factors allow the entities to establish the objectives and analyse the overall performance as

well as it also includes individual cost centres of the organisation.

resources accordingly. It gives them a sense of satisfaction after 6 months when they find

them efficiently by following the roadmap. Budget will always give a feeling that you have

an assigned amount of money for a particular task or next task.

According to Andor, Mohanty and Toth, (2015), Following a budget or expenditure plan will

assist the company to form its capital structure whether the operations of the company should

rely on capital and debt or decide the proportion of debt or equity in the budget plan. By

forecasting the future financial expenditure, it gives an overview of which month will be

financially tight once the annual budget report are forecasted. Using a realistic and efficient

budget helps to forecast the spending for a fiscal year that will result in long-term financial

planning. It enables the vision to complex current market situation that can make realistic

assumptions regarding annual income, planning for long term goals, buying the investment,

and recreation property. There is no particular single budget defined for business. Budget

assists the business to track and manage the resources. Business entities use a varied kind of

budget for every department. Budgeting decides the expenditure and form effective strategies

that will maximise the revenue and valuation of assets.

Otley, (2016), Common types of budgets used by the business such as master budget, static

budget, financial budget, cash flow budget, and operating budget. A master budget is

aggregation of the entire individual budget plan of each department from operation,

marketing, sales to finance. A master budget reflects a complete picture of the financial

health of the business. There are several factors that is contained in master budget such as

sales, asset valuation, outstanding payments, operating expenses, and income streams. These

factors allow the entities to establish the objectives and analyse the overall performance as

well as it also includes individual cost centres of the organisation.

MANAGERIAL ACCOUNTING: 5

(Source: Leoissac, 2018)

While making business plan, a manager calculates the estimated income and expenses to find

out whether the plan would be profitable or not. Forecasting and estimating income and

expenses help the decision maker to try other business plan trials and alternatives. It enables

the manager to calculate opportunity profit from all the available alternatives and options

(Andor, Mohanty, and Toth, 2015).

According to Uyar, (2009), Cash flow budget is projection of the process how and when cash

comes in and flows out from the business in a specific time period. It helps to maintain ratio

analytical performance of current assets of the company. There is an ideal ratio of current

ratio i.e. 1:1. Current ratio is the ability of the company to payment its outstanding expenses

from its liquid assets (cash and cash equivalents and bank). It enables the company to manage

its cash flow wisely. This type of budget considers several factors such as accounts receivable

and accounts payable that helps the company to assess whether the company has an

appropriate sum of liquid cash to continue its operations. This budget formulates the cash

expenditure plan to spend its cash productively and the ability of the action to generate the

cash in future. For example- An infrastructure company uses the cash flow budget to decide

whether it has the ability or enough liquid cash to start a new construction project before they

are paid for their work (ACCA, 2018).

(Source: Leoissac, 2018)

While making business plan, a manager calculates the estimated income and expenses to find

out whether the plan would be profitable or not. Forecasting and estimating income and

expenses help the decision maker to try other business plan trials and alternatives. It enables

the manager to calculate opportunity profit from all the available alternatives and options

(Andor, Mohanty, and Toth, 2015).

According to Uyar, (2009), Cash flow budget is projection of the process how and when cash

comes in and flows out from the business in a specific time period. It helps to maintain ratio

analytical performance of current assets of the company. There is an ideal ratio of current

ratio i.e. 1:1. Current ratio is the ability of the company to payment its outstanding expenses

from its liquid assets (cash and cash equivalents and bank). It enables the company to manage

its cash flow wisely. This type of budget considers several factors such as accounts receivable

and accounts payable that helps the company to assess whether the company has an

appropriate sum of liquid cash to continue its operations. This budget formulates the cash

expenditure plan to spend its cash productively and the ability of the action to generate the

cash in future. For example- An infrastructure company uses the cash flow budget to decide

whether it has the ability or enough liquid cash to start a new construction project before they

are paid for their work (ACCA, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING: 6

As per the perception of JBlöndal et al., (2008), A financial budget brings out the company`s

strategy to manage the assets, income, expense, and cash flow. This budget is used to

establish and reflect a true picture of organisation`s financial health. Financial budget present

a comprehensive and consolidated overview of relative spending of cash to generate cash

from core operations (principlesofaccounting, 2018). For instance- A software company can

use the financial budget to determine the value in relation to public stock offering or

acquisition. An operational budget forecasts and analysis the projected expense and income

in a particular course of action. To reflect a true picture, operating budget account for several

factors such as material costs, production, overhead, labour cost, overhead, and

administrative costs. This is the most active budget that is prepared most frequently on a

regular basis weekly, monthly or annual basis. An analyst compare the operational activity of

each week or month to ensure that a company overspends on supplies of raw material.

In regards to a business organisation, a budget is a broad overview of financial plan to

achieve financial and operational objectives of an organisation. A budget is an roadmap to

organisation`s strategic plan. While developing a budget, a company plans to achieve the

objective of acquisition of business operations and use of its resources. A budget is a valuable

benchmark to decide how well the procedure steps are taken by the management to ensure

that they can achieve the objectives. Budgets enable to coordinate the business activities

between different departments and aligning these activities to picture or make big strategic

plans.

As per the perception of JBlöndal et al., (2008), A financial budget brings out the company`s

strategy to manage the assets, income, expense, and cash flow. This budget is used to

establish and reflect a true picture of organisation`s financial health. Financial budget present

a comprehensive and consolidated overview of relative spending of cash to generate cash

from core operations (principlesofaccounting, 2018). For instance- A software company can

use the financial budget to determine the value in relation to public stock offering or

acquisition. An operational budget forecasts and analysis the projected expense and income

in a particular course of action. To reflect a true picture, operating budget account for several

factors such as material costs, production, overhead, labour cost, overhead, and

administrative costs. This is the most active budget that is prepared most frequently on a

regular basis weekly, monthly or annual basis. An analyst compare the operational activity of

each week or month to ensure that a company overspends on supplies of raw material.

In regards to a business organisation, a budget is a broad overview of financial plan to

achieve financial and operational objectives of an organisation. A budget is an roadmap to

organisation`s strategic plan. While developing a budget, a company plans to achieve the

objective of acquisition of business operations and use of its resources. A budget is a valuable

benchmark to decide how well the procedure steps are taken by the management to ensure

that they can achieve the objectives. Budgets enable to coordinate the business activities

between different departments and aligning these activities to picture or make big strategic

plans.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING: 7

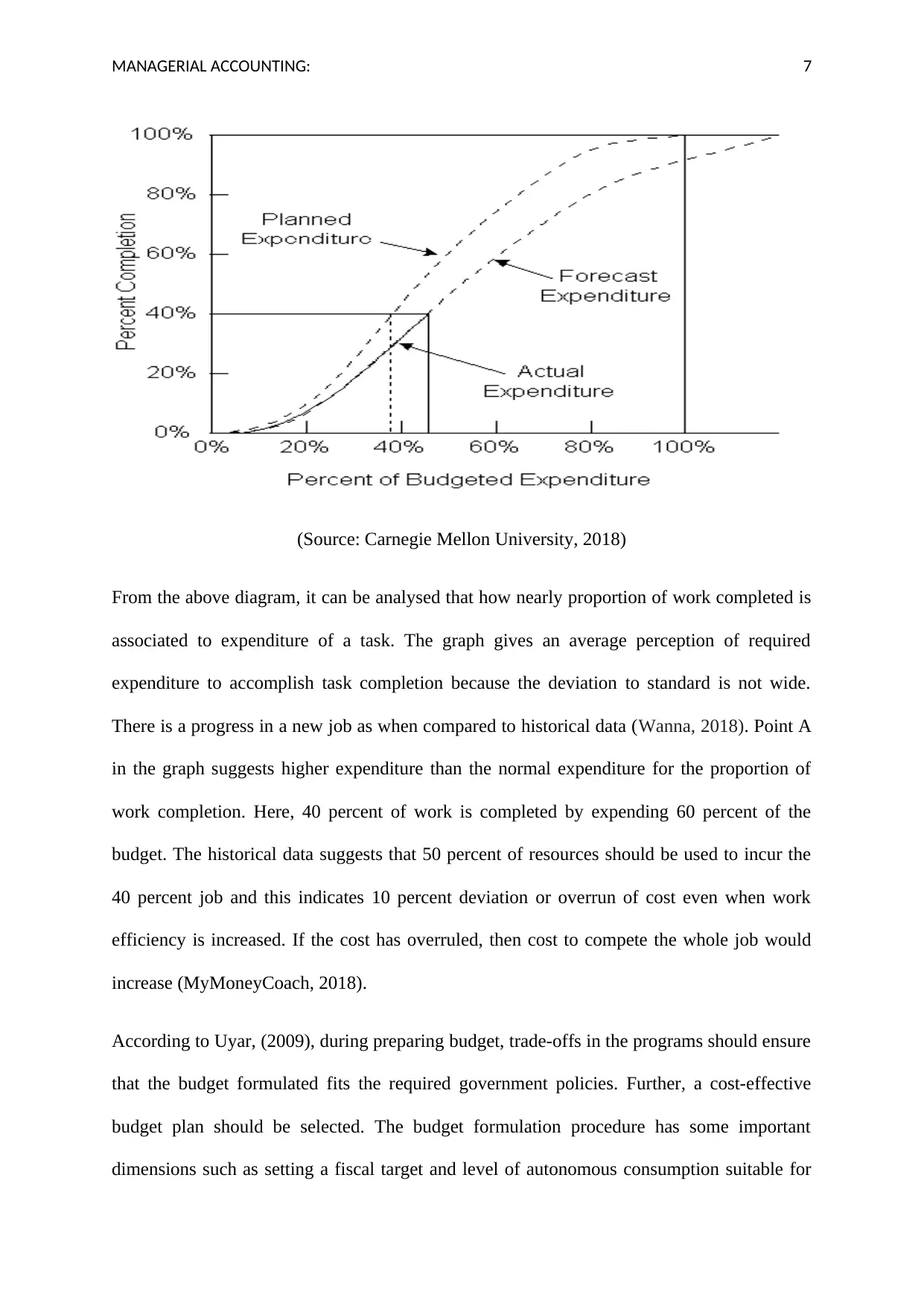

(Source: Carnegie Mellon University, 2018)

From the above diagram, it can be analysed that how nearly proportion of work completed is

associated to expenditure of a task. The graph gives an average perception of required

expenditure to accomplish task completion because the deviation to standard is not wide.

There is a progress in a new job as when compared to historical data (Wanna, 2018). Point A

in the graph suggests higher expenditure than the normal expenditure for the proportion of

work completion. Here, 40 percent of work is completed by expending 60 percent of the

budget. The historical data suggests that 50 percent of resources should be used to incur the

40 percent job and this indicates 10 percent deviation or overrun of cost even when work

efficiency is increased. If the cost has overruled, then cost to compete the whole job would

increase (MyMoneyCoach, 2018).

According to Uyar, (2009), during preparing budget, trade-offs in the programs should ensure

that the budget formulated fits the required government policies. Further, a cost-effective

budget plan should be selected. The budget formulation procedure has some important

dimensions such as setting a fiscal target and level of autonomous consumption suitable for

(Source: Carnegie Mellon University, 2018)

From the above diagram, it can be analysed that how nearly proportion of work completed is

associated to expenditure of a task. The graph gives an average perception of required

expenditure to accomplish task completion because the deviation to standard is not wide.

There is a progress in a new job as when compared to historical data (Wanna, 2018). Point A

in the graph suggests higher expenditure than the normal expenditure for the proportion of

work completion. Here, 40 percent of work is completed by expending 60 percent of the

budget. The historical data suggests that 50 percent of resources should be used to incur the

40 percent job and this indicates 10 percent deviation or overrun of cost even when work

efficiency is increased. If the cost has overruled, then cost to compete the whole job would

increase (MyMoneyCoach, 2018).

According to Uyar, (2009), during preparing budget, trade-offs in the programs should ensure

that the budget formulated fits the required government policies. Further, a cost-effective

budget plan should be selected. The budget formulation procedure has some important

dimensions such as setting a fiscal target and level of autonomous consumption suitable for

MANAGERIAL ACCOUNTING: 8

these targets, which always remained an objective to be achieved in macro-economic

framework. Moreover, there is a need to form a policy regarding the expenditures such as

adequate allocation of resources with confirming both polices and the fiscal targets that

remains the main objective and the core process of preparing budgets. Finally, budget

addresses the operational efficiency and sort the performance issues (Carnegie, Christopher,

and Napier, 2017).

Explanation of purpose of two studies undertaken to understand budgeting

In context to managing a business organisation, there are mainly three purposes to formulate

budget plan such as a forecast of income and expenditure statements. It act as a tool for

decision-making and a mode to check business performance. The purpose of two studies is

based on two different articles based on budgeting. The first article evaluates the budgeting

approaches such as traditional budgeting, improving budgeting system, and making decision

beyond budgeting. The research articles outlays review on case study of Main freight that

was never based on traditional budgeting. Moreover, it also covers the new approaches of

budgeting. This article view budget as a central component of (MCS) management control

systems. This beyond budgeting system opposes that manager should develop employ more

control system to replace budgets. This article examines the MCS (management control

system) which never engaged tradition system of budgeting (Grady and Akroyd, 2016).

Another article from Accounting, Auditing & Accountability Journal purposes budgeting as a

central concept in public organisation. According to the researcher, budgeting is a

multifaceted and knowledge rich topic to research on. The changing institutional, social, and

economic needs, it require assessing the role, and featuring while assessing the accounting

studies with the topic. The purpose is to review the public budgeting that determines how

public management and public administration engage the traditional as well as modern

budgeting theories in contribute a long-term sustainability of business.

these targets, which always remained an objective to be achieved in macro-economic

framework. Moreover, there is a need to form a policy regarding the expenditures such as

adequate allocation of resources with confirming both polices and the fiscal targets that

remains the main objective and the core process of preparing budgets. Finally, budget

addresses the operational efficiency and sort the performance issues (Carnegie, Christopher,

and Napier, 2017).

Explanation of purpose of two studies undertaken to understand budgeting

In context to managing a business organisation, there are mainly three purposes to formulate

budget plan such as a forecast of income and expenditure statements. It act as a tool for

decision-making and a mode to check business performance. The purpose of two studies is

based on two different articles based on budgeting. The first article evaluates the budgeting

approaches such as traditional budgeting, improving budgeting system, and making decision

beyond budgeting. The research articles outlays review on case study of Main freight that

was never based on traditional budgeting. Moreover, it also covers the new approaches of

budgeting. This article view budget as a central component of (MCS) management control

systems. This beyond budgeting system opposes that manager should develop employ more

control system to replace budgets. This article examines the MCS (management control

system) which never engaged tradition system of budgeting (Grady and Akroyd, 2016).

Another article from Accounting, Auditing & Accountability Journal purposes budgeting as a

central concept in public organisation. According to the researcher, budgeting is a

multifaceted and knowledge rich topic to research on. The changing institutional, social, and

economic needs, it require assessing the role, and featuring while assessing the accounting

studies with the topic. The purpose is to review the public budgeting that determines how

public management and public administration engage the traditional as well as modern

budgeting theories in contribute a long-term sustainability of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGERIAL ACCOUNTING: 9

The two research questions in both the articles covers the particular discussion on-

How new budgeting approaches analyses the effectiveness of both approaches in companies?

How far public budgeting is associated with current budgeting theories and practises to analyse

the market?

Similarities and differences in two studies

The major differences between the two studies is that case study of Main freight never

involved traditional budgeting system in management control system. Whereas, the second

article engages both traditional and modern budgeting theory are the major priorities of

public budgeting system. Moreover, the article based on usage of both approaches of

budgetary methods which in return contributes to long-term sustainability (Nielsen, Mitchell

and Nørreklit, 2015).

First article shows how organisations can work without using any traditional budgeting

system and still cope up with and maintain a high level of control. Article 2nd originates how

budgeting plays an important role in public companies and it use the budgeting method to

allocate large share of NNP (net national income) national incomes (Brusca et al., 2016).

The case study of Main freight describes that management control system is designed on the

basis of administrative and cultural system that helped to support planning and reward

systems mangers that have used to monitor the key drivers of short and long-term

performances to focus profitability. This case study has discovered that these findings give

more holistic view of management control system and understand how this control is

accomplished within the organisation that are moved beyond budgeting. There are very

organisation, which cannot work budgets but organisations that never had budgets limits the

opportunities to check how MCS (management control system) plan to function without

The two research questions in both the articles covers the particular discussion on-

How new budgeting approaches analyses the effectiveness of both approaches in companies?

How far public budgeting is associated with current budgeting theories and practises to analyse

the market?

Similarities and differences in two studies

The major differences between the two studies is that case study of Main freight never

involved traditional budgeting system in management control system. Whereas, the second

article engages both traditional and modern budgeting theory are the major priorities of

public budgeting system. Moreover, the article based on usage of both approaches of

budgetary methods which in return contributes to long-term sustainability (Nielsen, Mitchell

and Nørreklit, 2015).

First article shows how organisations can work without using any traditional budgeting

system and still cope up with and maintain a high level of control. Article 2nd originates how

budgeting plays an important role in public companies and it use the budgeting method to

allocate large share of NNP (net national income) national incomes (Brusca et al., 2016).

The case study of Main freight describes that management control system is designed on the

basis of administrative and cultural system that helped to support planning and reward

systems mangers that have used to monitor the key drivers of short and long-term

performances to focus profitability. This case study has discovered that these findings give

more holistic view of management control system and understand how this control is

accomplished within the organisation that are moved beyond budgeting. There are very

organisation, which cannot work budgets but organisations that never had budgets limits the

opportunities to check how MCS (management control system) plan to function without

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGERIAL ACCOUNTING: 10

budgets. This case reveals the design of integrated non-budgeting management control

system (Grady and Akroyd, 2016).

The similarity found in both the articles in every case either non-budgeting system or public

budgeting system is that use of accrual and cash based accounting is used and raises similar

accounting concepts. Every accounting principles and standards has to be followed in the

same way (Schaltegger, and Burritt, 2017). The questioning and filing is based on regulation-

bases approach to implement and execute in policies through budget. Problems encountered

in fusing budgeting and implying different control system, the policy making remains same

despite of implementation side as they can produce different results. Stability and clarity

differs when both organisations follow different management control systems. The entire

request incorporated in budget cycle differs because non-budgetary may have more flexibility

but the typical budgetary system is inbuilt through a highly structured manner. The standard

responses may differ among the budgetary and non-budgetary responses. Any type of control

system is important for organisation; it is not a necessary obligation to accomplish to either

public budgeting or traditional (Blöndal et al., 2008). Every control system result to act as a

tool to manage the costs and cash flows. Any control system is important to make business

decision and long-term business planning process. Management control system estimates and

budgets. This case reveals the design of integrated non-budgeting management control

system (Grady and Akroyd, 2016).

The similarity found in both the articles in every case either non-budgeting system or public

budgeting system is that use of accrual and cash based accounting is used and raises similar

accounting concepts. Every accounting principles and standards has to be followed in the

same way (Schaltegger, and Burritt, 2017). The questioning and filing is based on regulation-

bases approach to implement and execute in policies through budget. Problems encountered

in fusing budgeting and implying different control system, the policy making remains same

despite of implementation side as they can produce different results. Stability and clarity

differs when both organisations follow different management control systems. The entire

request incorporated in budget cycle differs because non-budgetary may have more flexibility

but the typical budgetary system is inbuilt through a highly structured manner. The standard

responses may differ among the budgetary and non-budgetary responses. Any type of control

system is important for organisation; it is not a necessary obligation to accomplish to either

public budgeting or traditional (Blöndal et al., 2008). Every control system result to act as a

tool to manage the costs and cash flows. Any control system is important to make business

decision and long-term business planning process. Management control system estimates and

MANAGERIAL ACCOUNTING: 11

plans a future objective.

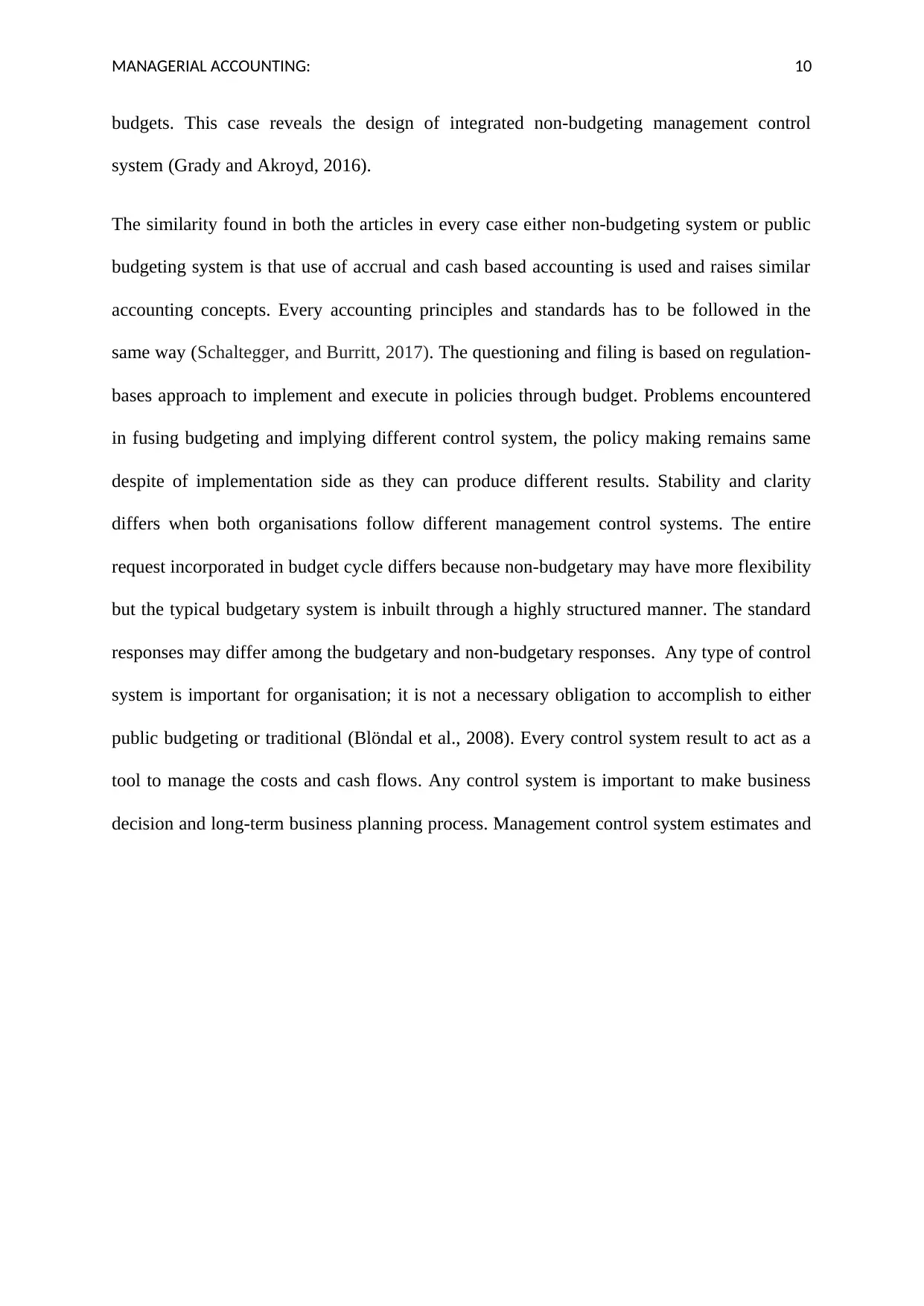

` (Source: Colorado Springs Airport, 2018)

From the above diagram, it is observed that to achieve the pre-decided objective, it has a set

of goals to achieve an overall objective of business. After a particular time, officials’

measures the action executed and performed or the current actions to standard set to find out

the deviation. Every budgeting system set some standards that helps the company to establish

a decision-making. Charts and graphs help the companies to make concise and clear plan and

budget of any project (ACCA, 2018).

Four specific outcomes or lessons learned from the two studies’ research findings that will be

useful for management accountants in Australian companies

By going through both the research articles, it is observed that in any of the case, a manager

has to identify the information regarding awareness of any issue. A better understanding of

issues can lead to better quality decision making. In Australia, Management accountants

employed in hospitals, other non-profit organisation and other local authorities such as clubs

and charities need statistical data and analytical information of several previous years.

Statistical data is derived and calculated through various statistical tools and deviation

plans a future objective.

` (Source: Colorado Springs Airport, 2018)

From the above diagram, it is observed that to achieve the pre-decided objective, it has a set

of goals to achieve an overall objective of business. After a particular time, officials’

measures the action executed and performed or the current actions to standard set to find out

the deviation. Every budgeting system set some standards that helps the company to establish

a decision-making. Charts and graphs help the companies to make concise and clear plan and

budget of any project (ACCA, 2018).

Four specific outcomes or lessons learned from the two studies’ research findings that will be

useful for management accountants in Australian companies

By going through both the research articles, it is observed that in any of the case, a manager

has to identify the information regarding awareness of any issue. A better understanding of

issues can lead to better quality decision making. In Australia, Management accountants

employed in hospitals, other non-profit organisation and other local authorities such as clubs

and charities need statistical data and analytical information of several previous years.

Statistical data is derived and calculated through various statistical tools and deviation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.