Analyzing Budgeting and Cost: Financial Resource Management Report

VerifiedAdded on 2020/12/29

|10

|3113

|59

Report

AI Summary

This report provides a detailed analysis of financial resource management, focusing on budgeting and cost analysis within an organizational context. It explores the alignment of budgets with organizational planning, strategies, and goals, emphasizing the importance of executive-level contribution and long-term perspectives. The report discusses the time frame for preparing budgets, highlighting key costs, variables, and sources of information, including business plans, historical data, and key personnel insights. It also examines various costing models, such as activity-based budgeting, and the requirement for sign-off in the budget process. Furthermore, the report covers measuring and monitoring performance against the budget through benchmarking and key performance indicators (KPIs), and it highlights how budgets facilitate communication across departments, encouraging staff to meet budgetary targets.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

Alignment of budget for organizational planning, strategies and goals......................................1

Time frame in context of preparing budget.................................................................................2

Key costs in budget and variables...............................................................................................2

Sources of information collected for budget...............................................................................3

Costing model used for generating information for budget........................................................4

Requirement of sign-off in budget..............................................................................................4

Measuring and monitoring performance against the budget ......................................................5

Budget facilitate communication within every department........................................................5

Staff encouragement for meeting budget....................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 2............................................................................................................................................1

Alignment of budget for organizational planning, strategies and goals......................................1

Time frame in context of preparing budget.................................................................................2

Key costs in budget and variables...............................................................................................2

Sources of information collected for budget...............................................................................3

Costing model used for generating information for budget........................................................4

Requirement of sign-off in budget..............................................................................................4

Measuring and monitoring performance against the budget ......................................................5

Budget facilitate communication within every department........................................................5

Staff encouragement for meeting budget....................................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Financial resources are very important aspect of each and every organization. Each

organization lays special emphasis on managing those financial resources as they will be giving

better and profitable outcome to the organization. The present report is giving brief discussion

about analysis of budgeting and cost. There is proper critical analysis of preparation of budget

and procedure for monitoring. Further it has given discussion about budget process which has

discussed about alignment of budget with strategic goals and planning. The time frame has been

illustrated in report for preparing budget with major cost and revenue with key variable which

are driving. The sources of information which are required for preparing budget and along with

that different costing models for generating information. Furthermore, it has given discussion

about performance which is directly measured and monitored as well. In the last part, ways for

encouraging staff for meeting budget has been provided.

TASK 2

Alignment of budget for organisational planning, strategies and goals

At execution level, the top discussion is always about strategy, budget and goals. The

stakeholders who prepare budgets without understanding of strategy of organization so this will

directly reflect in allocation of investment and spending (Budget with strategy, 2016). For

aligning budgets with strategy of organisation there are various measures which are as follows:

The budget should be prepared with effective contribution of executive level with respect

to strategy of organization. In the present era, different individual who are responsible for

framing strategy, there vision is not always similar so the responsibility of executive is to

connect management from top to bottom.

The budget should be set according to perspective of long term, usually budget are for 1

year because it can be achievable and quantifiable. But on contrary 1 year objective must

be subset of long term plan so it will ensure all individuals to lay special emphasis on

strategy.

Key performance indicator plays major contribution in financial budget and for achieving

success. The financial and non-financial indicators are included in KPI. They should be

easily identifiable because they only leads to achieve success with accomplishing budget

and strategy (Herath and Lu, 2018).

1

Financial resources are very important aspect of each and every organization. Each

organization lays special emphasis on managing those financial resources as they will be giving

better and profitable outcome to the organization. The present report is giving brief discussion

about analysis of budgeting and cost. There is proper critical analysis of preparation of budget

and procedure for monitoring. Further it has given discussion about budget process which has

discussed about alignment of budget with strategic goals and planning. The time frame has been

illustrated in report for preparing budget with major cost and revenue with key variable which

are driving. The sources of information which are required for preparing budget and along with

that different costing models for generating information. Furthermore, it has given discussion

about performance which is directly measured and monitored as well. In the last part, ways for

encouraging staff for meeting budget has been provided.

TASK 2

Alignment of budget for organisational planning, strategies and goals

At execution level, the top discussion is always about strategy, budget and goals. The

stakeholders who prepare budgets without understanding of strategy of organization so this will

directly reflect in allocation of investment and spending (Budget with strategy, 2016). For

aligning budgets with strategy of organisation there are various measures which are as follows:

The budget should be prepared with effective contribution of executive level with respect

to strategy of organization. In the present era, different individual who are responsible for

framing strategy, there vision is not always similar so the responsibility of executive is to

connect management from top to bottom.

The budget should be set according to perspective of long term, usually budget are for 1

year because it can be achievable and quantifiable. But on contrary 1 year objective must

be subset of long term plan so it will ensure all individuals to lay special emphasis on

strategy.

Key performance indicator plays major contribution in financial budget and for achieving

success. The financial and non-financial indicators are included in KPI. They should be

easily identifiable because they only leads to achieve success with accomplishing budget

and strategy (Herath and Lu, 2018).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Goals must be validated not in favour of major metrics and key data.

The strategy and planning must be revisited, because sometimes in that duration market

conditions are changed and all past plans remain unrealistic according to that. If plans

and strategy are revisited then organization can frame solution to the problems which are

cause in certain duration and it will make information related to budget very relevant and

informative in same context.

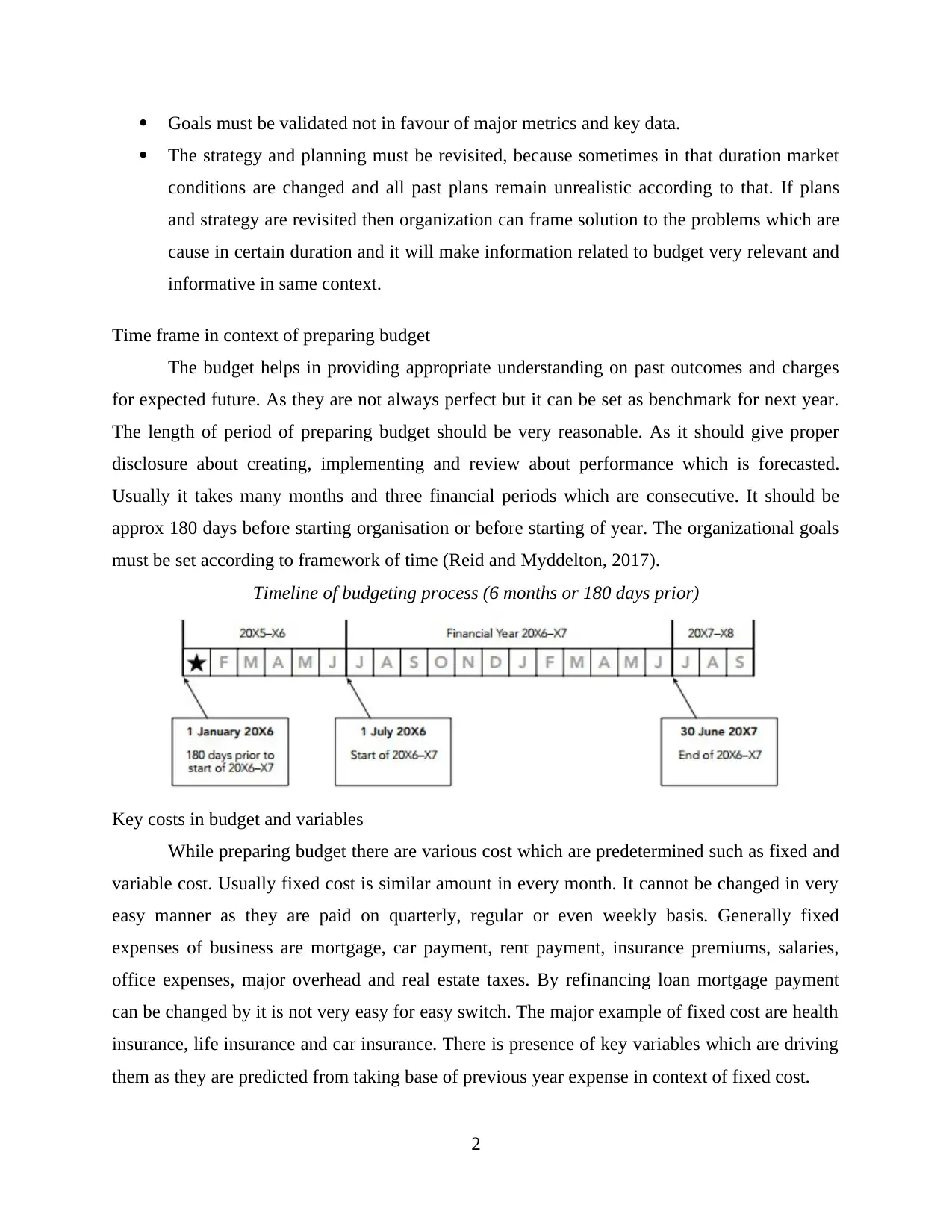

Time frame in context of preparing budget

The budget helps in providing appropriate understanding on past outcomes and charges

for expected future. As they are not always perfect but it can be set as benchmark for next year.

The length of period of preparing budget should be very reasonable. As it should give proper

disclosure about creating, implementing and review about performance which is forecasted.

Usually it takes many months and three financial periods which are consecutive. It should be

approx 180 days before starting organisation or before starting of year. The organizational goals

must be set according to framework of time (Reid and Myddelton, 2017).

Timeline of budgeting process (6 months or 180 days prior)

Key costs in budget and variables

While preparing budget there are various cost which are predetermined such as fixed and

variable cost. Usually fixed cost is similar amount in every month. It cannot be changed in very

easy manner as they are paid on quarterly, regular or even weekly basis. Generally fixed

expenses of business are mortgage, car payment, rent payment, insurance premiums, salaries,

office expenses, major overhead and real estate taxes. By refinancing loan mortgage payment

can be changed by it is not very easy for easy switch. The major example of fixed cost are health

insurance, life insurance and car insurance. There is presence of key variables which are driving

them as they are predicted from taking base of previous year expense in context of fixed cost.

2

The strategy and planning must be revisited, because sometimes in that duration market

conditions are changed and all past plans remain unrealistic according to that. If plans

and strategy are revisited then organization can frame solution to the problems which are

cause in certain duration and it will make information related to budget very relevant and

informative in same context.

Time frame in context of preparing budget

The budget helps in providing appropriate understanding on past outcomes and charges

for expected future. As they are not always perfect but it can be set as benchmark for next year.

The length of period of preparing budget should be very reasonable. As it should give proper

disclosure about creating, implementing and review about performance which is forecasted.

Usually it takes many months and three financial periods which are consecutive. It should be

approx 180 days before starting organisation or before starting of year. The organizational goals

must be set according to framework of time (Reid and Myddelton, 2017).

Timeline of budgeting process (6 months or 180 days prior)

Key costs in budget and variables

While preparing budget there are various cost which are predetermined such as fixed and

variable cost. Usually fixed cost is similar amount in every month. It cannot be changed in very

easy manner as they are paid on quarterly, regular or even weekly basis. Generally fixed

expenses of business are mortgage, car payment, rent payment, insurance premiums, salaries,

office expenses, major overhead and real estate taxes. By refinancing loan mortgage payment

can be changed by it is not very easy for easy switch. The major example of fixed cost are health

insurance, life insurance and car insurance. There is presence of key variables which are driving

them as they are predicted from taking base of previous year expense in context of fixed cost.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The initial expense which is always tried to cut down that is known as variable cost. They

are major contribution of forecasting budget. The variable expense usually reflect daily spending

on purchasing raw material, rebates, loan buy downs and training cost of contractor. These are

also budgeted at initial stage. It helps in decision making, as it varies from direct proportion to

output of quantity. It is in context of production volume of direct function, which is rising when

expansion of production has been presented with falling of contracts. These are usually budgeted

on incremental based of budgeting, which depicts always increasing from previous year.

Sources of information collected for budget

The information should be collected from creating budget are described as statements,

bills, assessment of student loan and even from financial accounts which are audited. These

audited accounts provides information in context of wealth and relative information in context of

financial performance. The system of accounting gives detailed information for sources of

income, gross profit margins, different overheads like electricity, salaries, office costs,

maintenance etc. even it gives detail information about loan repayments and different cost which

can be overlooked very easily. If there is any change in business plan of organisation, the

account of previous year are represented as excellent point for starting and it will be also helpful

for measuring expenditure and income for next year. As total relevance on historical cost, it is

quite dangerous because not always market conditions are same. For budgeting no shortcuts are

applied so in every month there is requirement of considering each and every item. In forming

budget, there are three major sources of information which is essential for developing budget are:

Business plan

Historical information

Knowledge of key personnel

Business plan: It is always altered from year to year and it will be leading to give major

impact on budget. Generally its duration is of 3 to 5 years and it will be giving basic overview of

goals and objectives of organization (Bartov and Mohanram, 2014). It provides very important

aspect for personnel which are involved in budgeting and alterations to level of income and

expenditure of organization from past year. Even it consists of operational plan which helps in

pursuing goals and objectives or organization in context of operation. Operational plan and

budget is interlinked to each other as budget is incomplete without operational plan. Strategies

can be executed by organization which has resources in context of business and operational plan.

3

are major contribution of forecasting budget. The variable expense usually reflect daily spending

on purchasing raw material, rebates, loan buy downs and training cost of contractor. These are

also budgeted at initial stage. It helps in decision making, as it varies from direct proportion to

output of quantity. It is in context of production volume of direct function, which is rising when

expansion of production has been presented with falling of contracts. These are usually budgeted

on incremental based of budgeting, which depicts always increasing from previous year.

Sources of information collected for budget

The information should be collected from creating budget are described as statements,

bills, assessment of student loan and even from financial accounts which are audited. These

audited accounts provides information in context of wealth and relative information in context of

financial performance. The system of accounting gives detailed information for sources of

income, gross profit margins, different overheads like electricity, salaries, office costs,

maintenance etc. even it gives detail information about loan repayments and different cost which

can be overlooked very easily. If there is any change in business plan of organisation, the

account of previous year are represented as excellent point for starting and it will be also helpful

for measuring expenditure and income for next year. As total relevance on historical cost, it is

quite dangerous because not always market conditions are same. For budgeting no shortcuts are

applied so in every month there is requirement of considering each and every item. In forming

budget, there are three major sources of information which is essential for developing budget are:

Business plan

Historical information

Knowledge of key personnel

Business plan: It is always altered from year to year and it will be leading to give major

impact on budget. Generally its duration is of 3 to 5 years and it will be giving basic overview of

goals and objectives of organization (Bartov and Mohanram, 2014). It provides very important

aspect for personnel which are involved in budgeting and alterations to level of income and

expenditure of organization from past year. Even it consists of operational plan which helps in

pursuing goals and objectives or organization in context of operation. Operational plan and

budget is interlinked to each other as budget is incomplete without operational plan. Strategies

can be executed by organization which has resources in context of business and operational plan.

3

Key personnel: The most important strategy is to create team of people who are very

motivating and inspired in business context. The task which estimates revenue and cost for

particular department of firm which has responsibility in same context. All those individuals will

be having capability to give forecast of expenses and income in very appropriate manner. The

people who are involved in process of budgeting will be examining feasibility of finance and

budget will be prepared in such manner which will be accepted by different persons who are

directly or indirectly involved in it.

Costing model used for generating information for budget

Activity based budgeting is replicated as method of budgeting on framework of activity

which uses data of different cost driver in setting budget and processes of variance feedback. The

most essential framework has been identified for cost drivers via activity based costing for

framing budgets (Boardman and et. al., 2017). This activity usually lays special emphasis on

activities instead of functions. These activities are classified in three stages as:

Determining activities with respect to their cost drivers

Number of units are predicted of cost driver at activity level which is required and

Finally, cost per unit of activity is calculated.

Generally, it draws attention of activities of overhead and costs which are associated to

them. It gives special emphasis on controlling cost if volume of that specific activity is controlled

or not. All the irrelevant activities are substituted if it is apart from business. Then cost is saved

and that cost is reflected in production of services and goods at lower cost from its competitors

so while performing this competitive edge has been created. The traditional costing gives

importance to input costs as it takes approach of output based and all activities which drives cost

are recognized. It reviews the activity collection of business and it will be directly linked to

strategy of organization. In this method of budgeting whole business is termed as single business

unit which is not separated in form of departments. The budgets are also prepared in perspective

of business not in department. The relationship has been improved within organizations and even

customers which tends to increase in sales and revenue as well.

Requirement of sign-off in budget

The budget which is prepared should be very ethical and it should be not be very out of

line. It should indicate acceptance or approval of budget by the top authority and board. After

4

motivating and inspired in business context. The task which estimates revenue and cost for

particular department of firm which has responsibility in same context. All those individuals will

be having capability to give forecast of expenses and income in very appropriate manner. The

people who are involved in process of budgeting will be examining feasibility of finance and

budget will be prepared in such manner which will be accepted by different persons who are

directly or indirectly involved in it.

Costing model used for generating information for budget

Activity based budgeting is replicated as method of budgeting on framework of activity

which uses data of different cost driver in setting budget and processes of variance feedback. The

most essential framework has been identified for cost drivers via activity based costing for

framing budgets (Boardman and et. al., 2017). This activity usually lays special emphasis on

activities instead of functions. These activities are classified in three stages as:

Determining activities with respect to their cost drivers

Number of units are predicted of cost driver at activity level which is required and

Finally, cost per unit of activity is calculated.

Generally, it draws attention of activities of overhead and costs which are associated to

them. It gives special emphasis on controlling cost if volume of that specific activity is controlled

or not. All the irrelevant activities are substituted if it is apart from business. Then cost is saved

and that cost is reflected in production of services and goods at lower cost from its competitors

so while performing this competitive edge has been created. The traditional costing gives

importance to input costs as it takes approach of output based and all activities which drives cost

are recognized. It reviews the activity collection of business and it will be directly linked to

strategy of organization. In this method of budgeting whole business is termed as single business

unit which is not separated in form of departments. The budgets are also prepared in perspective

of business not in department. The relationship has been improved within organizations and even

customers which tends to increase in sales and revenue as well.

Requirement of sign-off in budget

The budget which is prepared should be very ethical and it should be not be very out of

line. It should indicate acceptance or approval of budget by the top authority and board. After

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

approving it should be circulated to each and every department with its consequence then its

implementation will be done. The starting of year of business has its initial step is to prepare

budget of their organization and get approved by board. After approval, it should be

communicated and spread properly in organization. The acceptance ensures clear and appropriate

understanding of work which is being performed in the project is successful or not.

Measuring and monitoring performance against the budget

Budget is referred as financial action plan. It is very basic necessity that budgets should

be reviewed regularly being a part of annual planning cycle. Budgets can be served as a specific

indicator of revenue and cost which is directly linked to every activities, it is a way for

supporting and giving information about decision making throughout specific year and it is

medium for controlling and monitoring business and specifically it analyses variations between

budgeted and actual income. It can be monitored against budget by:

Benchmarking performance: It is referred as most important way for increasing the

understanding of performance of business and its potential for proper comparison with business

of similar industry. For performing benchmark, all figures in context of business must be

gathered and in this context most challenging aspect is to collect external information for

comparisons. The data of benchmark must be used in similar context as any other data which

measures performance is generated for improving operating way of business. Usually it sets

targets for reaching benchmark value which has been aspired (Islam and et. al., 2016).

Key performance indicators (KPIs): For increasing performance of business there is

requirement of proper understanding and monitoring key drivers of business which has huge

impact. In this aspect there are several factors which affects each and every business

performance as its special focus is to monitoring it carefully. The specific attribute are

quantifiable and it directly captures business driver. There are two types of KPI that is financial

KPI and non-financial KPI as they both drive future improvements in context of performance.

The key drivers such as sales, working capital and costs. The main objective is to spot

opportunities and problems and other objective is to set goals or target for various departments

and employees as well throughout whole business which will be helping in attaining strategic

goals (Measure performance and set targets, 2018).

5

implementation will be done. The starting of year of business has its initial step is to prepare

budget of their organization and get approved by board. After approval, it should be

communicated and spread properly in organization. The acceptance ensures clear and appropriate

understanding of work which is being performed in the project is successful or not.

Measuring and monitoring performance against the budget

Budget is referred as financial action plan. It is very basic necessity that budgets should

be reviewed regularly being a part of annual planning cycle. Budgets can be served as a specific

indicator of revenue and cost which is directly linked to every activities, it is a way for

supporting and giving information about decision making throughout specific year and it is

medium for controlling and monitoring business and specifically it analyses variations between

budgeted and actual income. It can be monitored against budget by:

Benchmarking performance: It is referred as most important way for increasing the

understanding of performance of business and its potential for proper comparison with business

of similar industry. For performing benchmark, all figures in context of business must be

gathered and in this context most challenging aspect is to collect external information for

comparisons. The data of benchmark must be used in similar context as any other data which

measures performance is generated for improving operating way of business. Usually it sets

targets for reaching benchmark value which has been aspired (Islam and et. al., 2016).

Key performance indicators (KPIs): For increasing performance of business there is

requirement of proper understanding and monitoring key drivers of business which has huge

impact. In this aspect there are several factors which affects each and every business

performance as its special focus is to monitoring it carefully. The specific attribute are

quantifiable and it directly captures business driver. There are two types of KPI that is financial

KPI and non-financial KPI as they both drive future improvements in context of performance.

The key drivers such as sales, working capital and costs. The main objective is to spot

opportunities and problems and other objective is to set goals or target for various departments

and employees as well throughout whole business which will be helping in attaining strategic

goals (Measure performance and set targets, 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget facilitate communication within every department

Budget should be communicated in very efficient manner to every department as it plays

huge contribution in strategy of effective marketing communication. At prior, all resources must

be allocated with proper corporate demand with specific function. Each and every department of

business enterprise gets all financial resources for conducting initiatives in proper manner

(Budgeting communication, 2018). The organization must weigh requirement of every

department and combine this with organization total operating budget.

The budget communication is referred as guide of budget to the marketing head of

communication department with specification of allocation of various communication activities.

It is very important aspect as it allows organization for performing proper analysis and key

comparisons (Mahal and Hossain, 2015). While, preparing budgeting and planning every small

business owner set goals with his team for the coming year which includes productivity goals,

revenue targets and even percentage of gross margin for improving organization visibility in

their community. It is very necessary because CEO will be holding team members who are

accountable for reaching goals. As it should be distributed to every department and if there is

requirement of any alteration then it should be communicated to top management with specific

justification. If it is communicated in common meeting then it will lead to unity or people will

work together for reaching at conclusion.

Staff encouragement for meeting budget

The staff can be encouraged for meeting budget as they are very fiscally minded because

they pay great attention to detail and even they think before performing any activity. While

forming budget employees must be included who have their stake in that are more adhere to their

goals and objectives. They must attain agreement from all the parties in context of budget while

its completion. Each level such as supervisors, employees and top management must be equally

accountable for failure or success as well of budget. For meeting budget they must record the

actual performance in specific duration and in this context information of sales and expense must

be traced monthly or frequently if it is available.

Threshold must be identified for investigating variance of budget and it determines very

consistent threshold for investigation and after that all the budget variances must be calculated.

For achieving consistency budgeted amount must be subtracted from actual amount. It is

unfavourable for expenses and positive variance but on its contrary it is favourable to revenue

6

Budget should be communicated in very efficient manner to every department as it plays

huge contribution in strategy of effective marketing communication. At prior, all resources must

be allocated with proper corporate demand with specific function. Each and every department of

business enterprise gets all financial resources for conducting initiatives in proper manner

(Budgeting communication, 2018). The organization must weigh requirement of every

department and combine this with organization total operating budget.

The budget communication is referred as guide of budget to the marketing head of

communication department with specification of allocation of various communication activities.

It is very important aspect as it allows organization for performing proper analysis and key

comparisons (Mahal and Hossain, 2015). While, preparing budgeting and planning every small

business owner set goals with his team for the coming year which includes productivity goals,

revenue targets and even percentage of gross margin for improving organization visibility in

their community. It is very necessary because CEO will be holding team members who are

accountable for reaching goals. As it should be distributed to every department and if there is

requirement of any alteration then it should be communicated to top management with specific

justification. If it is communicated in common meeting then it will lead to unity or people will

work together for reaching at conclusion.

Staff encouragement for meeting budget

The staff can be encouraged for meeting budget as they are very fiscally minded because

they pay great attention to detail and even they think before performing any activity. While

forming budget employees must be included who have their stake in that are more adhere to their

goals and objectives. They must attain agreement from all the parties in context of budget while

its completion. Each level such as supervisors, employees and top management must be equally

accountable for failure or success as well of budget. For meeting budget they must record the

actual performance in specific duration and in this context information of sales and expense must

be traced monthly or frequently if it is available.

Threshold must be identified for investigating variance of budget and it determines very

consistent threshold for investigation and after that all the budget variances must be calculated.

For achieving consistency budgeted amount must be subtracted from actual amount. It is

unfavourable for expenses and positive variance but on its contrary it is favourable to revenue

6

and positive variances. The variances must be identified and which are greater than threshold

used for investigation and appropriate follow up. Managers must be able to determine causes of

those budget variances which are greater than threshold which is predetermined (Greer and et.

al., 2016).

After specific identification, an action plan has to be created for investigating variances

and these plans addresses all budget variance and its efficacy has been examined with next

period. Finally, the performance must be recognized and budget is also considered as a very

encouraging tool for rewarding employees who are performing and adhering according to

budget. Even this can be applied for correcting employees who are not able to accomplish goals

and objectives.

CONCLUSION

From the above report it has been concluded that budgeting and cost analysis is very

important tool for each and every organisation. It has helped in considering effectiveness of

process of budget with specific mechanism for monitoring cost and performance as well of

organisation. Further this report has shown specific understanding that budget should be aligned

with organization planning, strategies and goals as if it is not aligned it will be representing

negative consequences to organization.

7

used for investigation and appropriate follow up. Managers must be able to determine causes of

those budget variances which are greater than threshold which is predetermined (Greer and et.

al., 2016).

After specific identification, an action plan has to be created for investigating variances

and these plans addresses all budget variance and its efficacy has been examined with next

period. Finally, the performance must be recognized and budget is also considered as a very

encouraging tool for rewarding employees who are performing and adhering according to

budget. Even this can be applied for correcting employees who are not able to accomplish goals

and objectives.

CONCLUSION

From the above report it has been concluded that budgeting and cost analysis is very

important tool for each and every organisation. It has helped in considering effectiveness of

process of budget with specific mechanism for monitoring cost and performance as well of

organisation. Further this report has shown specific understanding that budget should be aligned

with organization planning, strategies and goals as if it is not aligned it will be representing

negative consequences to organization.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bartov, E. and Mohanram, P.S., 2014. Does income statement placement matter to investors?

The case of gains/losses from early debt extinguishment. The Accounting Review. 89(6).

pp.2021-2055.

Boardman, A. E. and et. al., 2017. Cost-benefit analysis: concepts and practice. Cambridge

University Press.

Greer, J. A. and et. al., 2016. Cost analysis of a randomized trial of early palliative care in

patients with metastatic nonsmall-cell lung cancer. Journal of palliative medicine. 19(8).

pp.842-848.

Herath, H. S. and Lu, X., 2018. Inference of economic truth from financial statements for

detecting earnings management: inventory costing methods from an information

economics perspective. Managerial and Decision Economics. 39(4). pp.389-402.

Islam, M. A. and et. al., 2016. Online energy budgeting for cost minimization in virtualized data

center. IEEE Transactions on Services Computing. 9(3). pp.421-432.

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting. 6(4). pp.66-74.

Reid, W. and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Online

Budget with strategy. 2016. [Online]. Available through: <https://blog.carlsonmc.com/aligning-

budget-with-strategy>.

Budgeting communication. 2018. [Online]. Available through: <https://bizfluent.com/info-

7864790-budgeting-communication.html>.

Measure performance and set targets. 2018. [Online]. Available through:

<http://www.infoentrepreneurs.org/en/guides/measure-performance-and-set-targets/>.

8

Books and Journals

Bartov, E. and Mohanram, P.S., 2014. Does income statement placement matter to investors?

The case of gains/losses from early debt extinguishment. The Accounting Review. 89(6).

pp.2021-2055.

Boardman, A. E. and et. al., 2017. Cost-benefit analysis: concepts and practice. Cambridge

University Press.

Greer, J. A. and et. al., 2016. Cost analysis of a randomized trial of early palliative care in

patients with metastatic nonsmall-cell lung cancer. Journal of palliative medicine. 19(8).

pp.842-848.

Herath, H. S. and Lu, X., 2018. Inference of economic truth from financial statements for

detecting earnings management: inventory costing methods from an information

economics perspective. Managerial and Decision Economics. 39(4). pp.389-402.

Islam, M. A. and et. al., 2016. Online energy budgeting for cost minimization in virtualized data

center. IEEE Transactions on Services Computing. 9(3). pp.421-432.

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting. 6(4). pp.66-74.

Reid, W. and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Online

Budget with strategy. 2016. [Online]. Available through: <https://blog.carlsonmc.com/aligning-

budget-with-strategy>.

Budgeting communication. 2018. [Online]. Available through: <https://bizfluent.com/info-

7864790-budgeting-communication.html>.

Measure performance and set targets. 2018. [Online]. Available through:

<http://www.infoentrepreneurs.org/en/guides/measure-performance-and-set-targets/>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.