Budgeting and Variance Analysis in Managerial Accounting

VerifiedAdded on 2023/06/04

|5

|697

|216

Homework Assignment

AI Summary

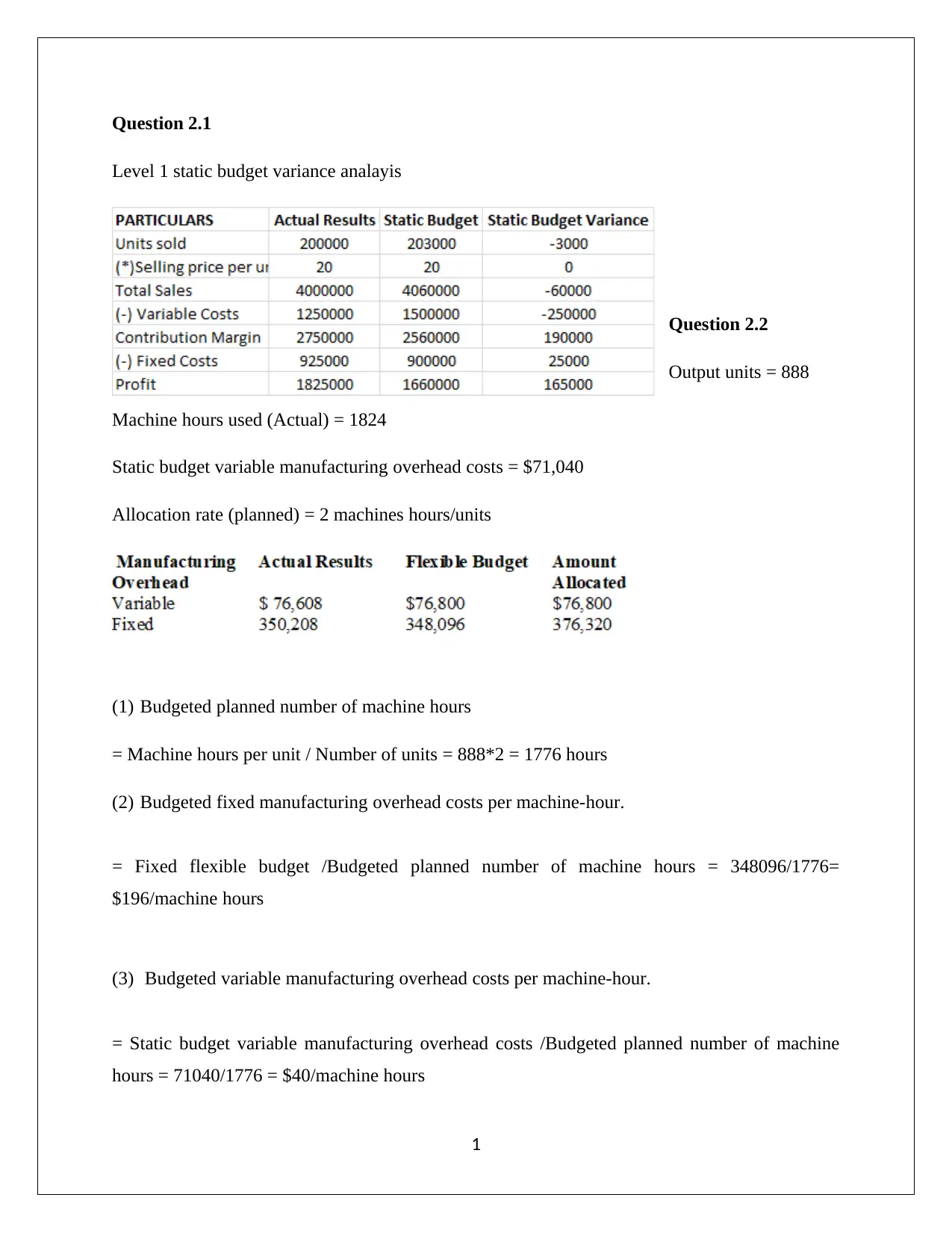

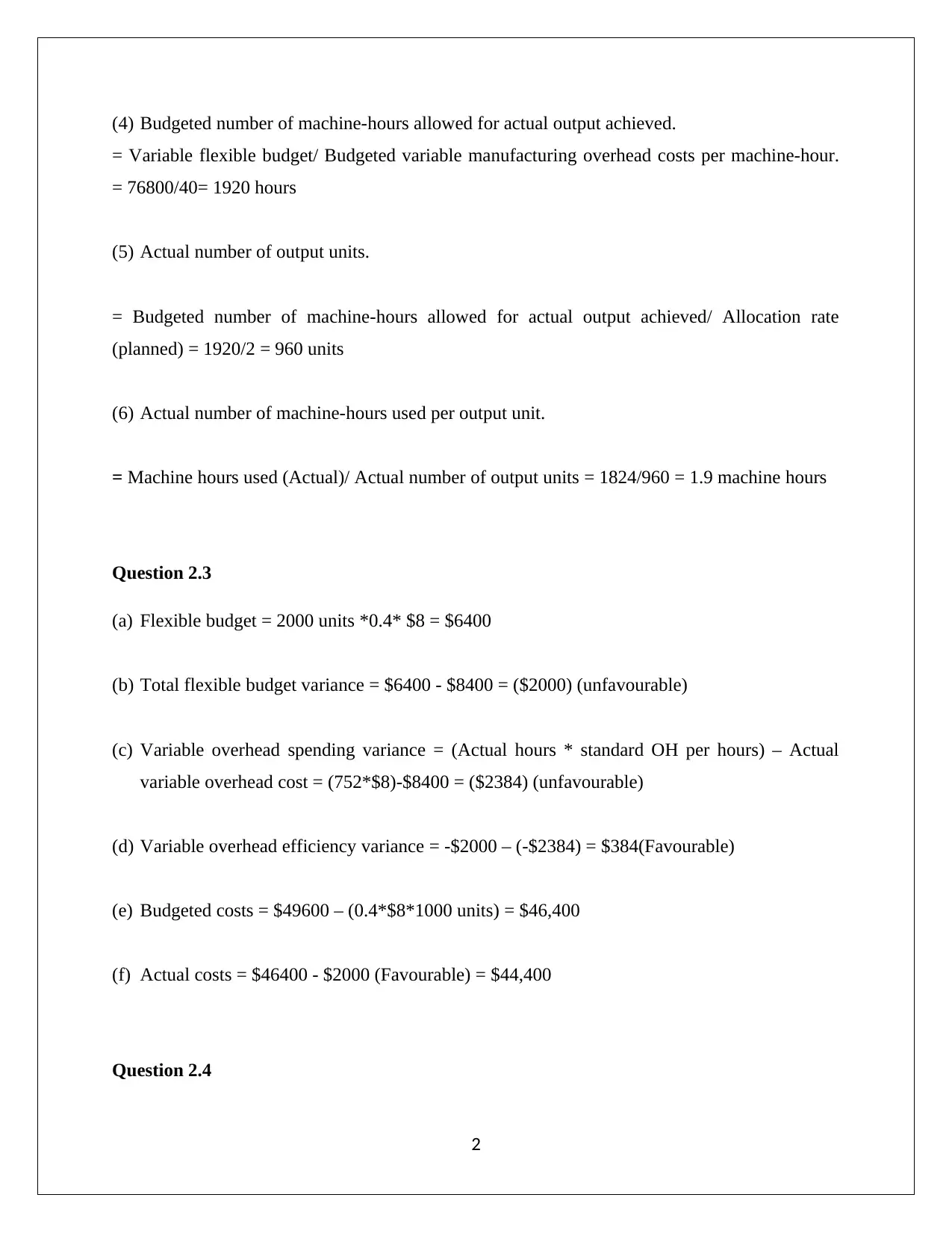

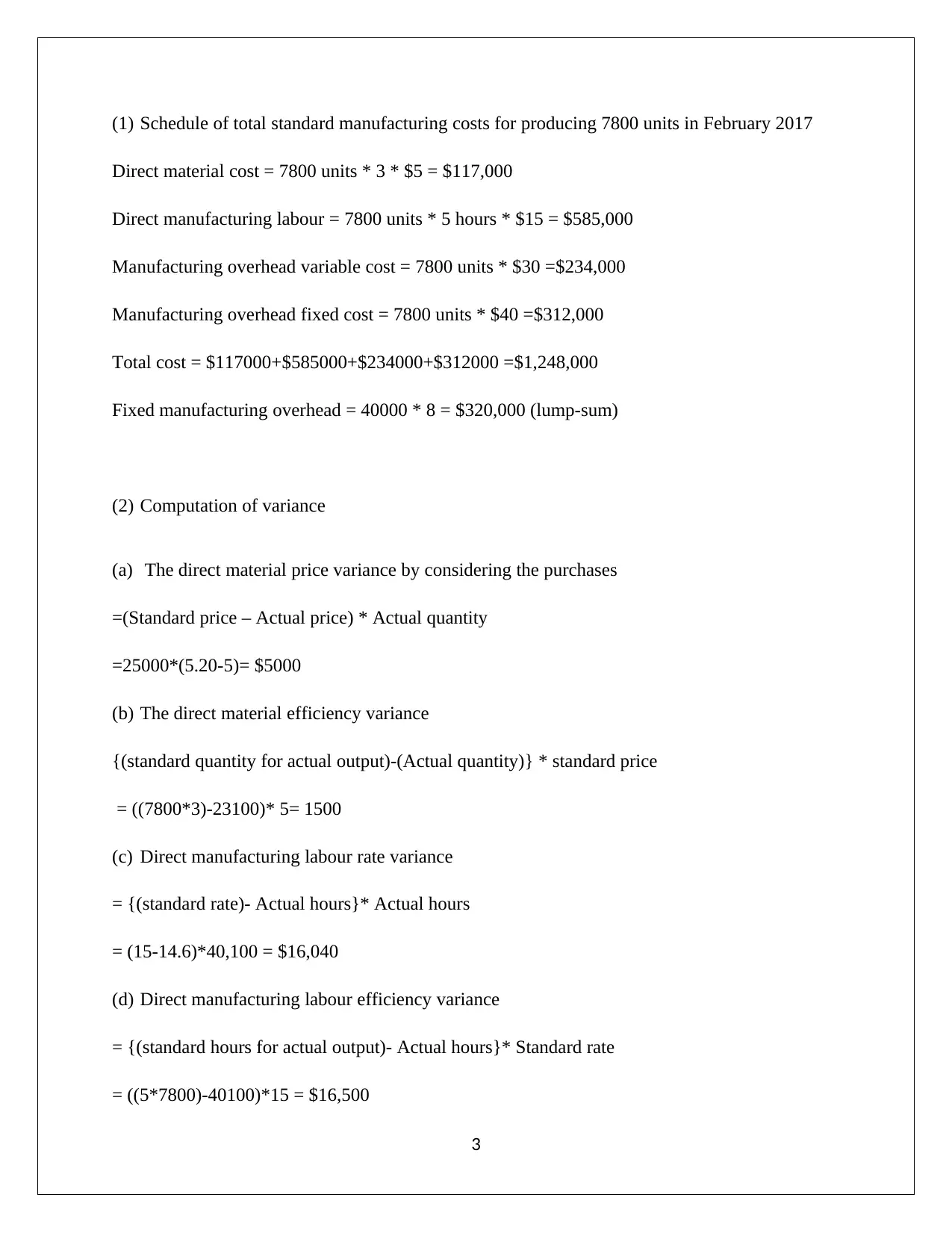

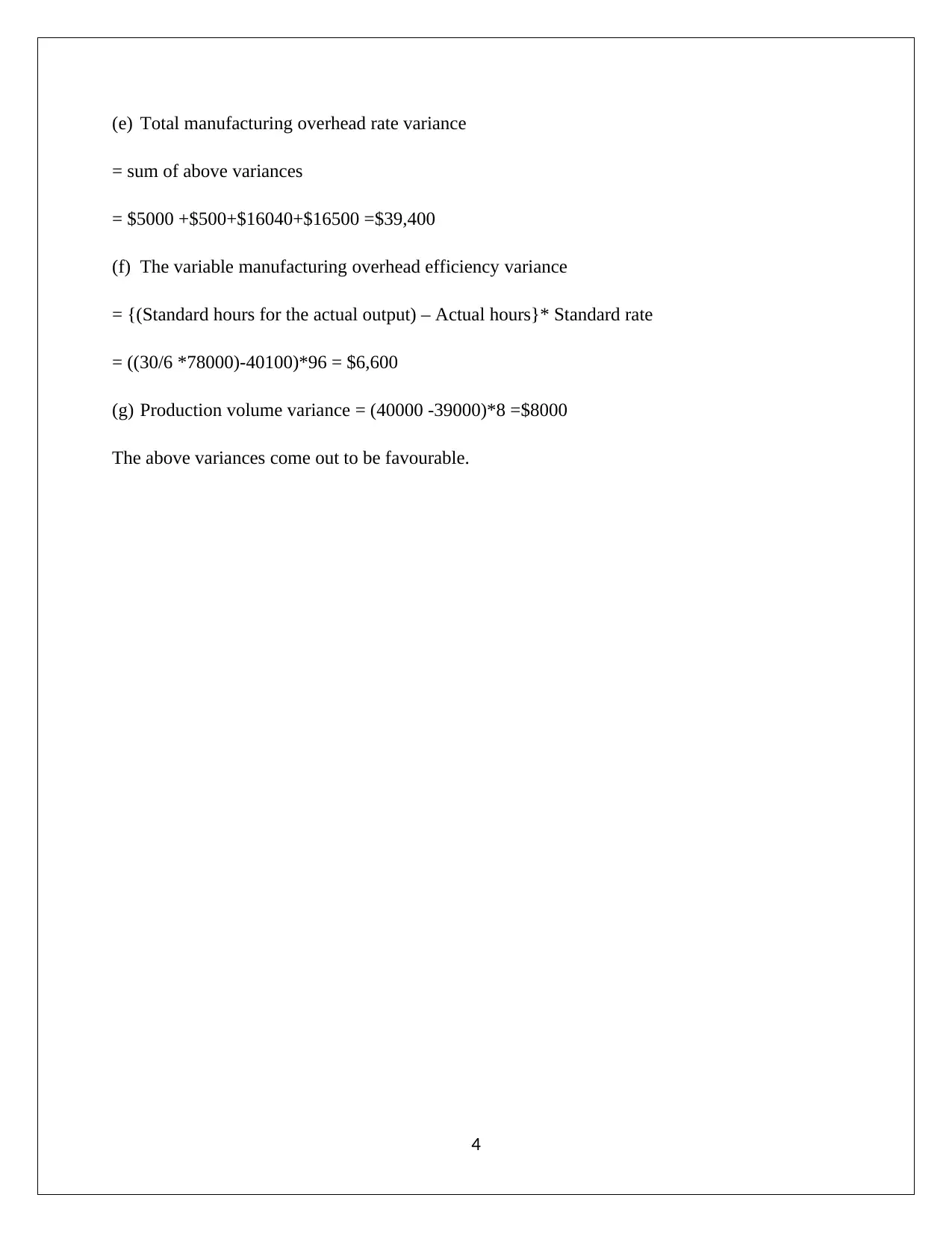

This assignment solution covers various aspects of managerial accounting, including static budget variance analysis, calculation of budgeted machine hours, fixed and variable overhead costs, and flexible budget variances. It also includes the computation of total standard manufacturing costs, direct material and labor variances, and manufacturing overhead rate and efficiency variances. The analysis involves calculating price and efficiency variances for direct materials and labor, as well as variable manufacturing overhead efficiency variance and production volume variance, providing a comprehensive overview of cost control and performance evaluation in a manufacturing setting. Desklib offers more solved assignments and resources for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.