Detailed Budgeting Report: Restaurant Financial Analysis and Planning

VerifiedAdded on 2020/03/16

|17

|3170

|85

Report

AI Summary

This report analyzes the budgeting practices of two local food businesses, Daniells’ Café and Café Waterside. The report begins with research tasks, including average cheque values and daily sales data, which are then used to create a budgeted monthly income statement for each business. Part B of the report addresses issues related to data sources and the necessary documentation for financial components like rent, wages, and asset purchases. The report includes a balance sheet and definitions of key accounting terminology, such as cash receipts, sales, and journals. Additionally, various financial ratios are calculated and explained, including current ratio, return on assets, and profit margins. The report also provides answers to multiple-choice questions and covers concepts such as trial balance, cash flow equations, and the differences between budgets and variances. Finally, the report examines different types of budgets, including zero-based and rolling budgets.

Running head: BUDGETING

Budgeting

Name of the Student:

Name of the University:

Author Note

Budgeting

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUDGETING

Table of Contents

Part A: Research Task.....................................................................................................................4

Answer to Question 1..................................................................................................................4

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................4

Answer to Question 4..................................................................................................................5

Part B...............................................................................................................................................6

Answer to Question 1..................................................................................................................6

Answer to Question 2..................................................................................................................6

Balance Sheet...............................................................................................................................6

Answer to Question 8..................................................................................................................7

Answer to Question 9..................................................................................................................7

Answer to Question 10................................................................................................................7

Answer to Question 11................................................................................................................8

Answer to Question 12................................................................................................................8

Answer to Question 13................................................................................................................8

Answer to Question 17................................................................................................................8

Answer to Question 18................................................................................................................8

Multiple Choice Questions..............................................................................................................9

Answer to Question 2..................................................................................................................9

Answer to Question 3..................................................................................................................9

Answer to Question 4..................................................................................................................9

Answer to Question 5..................................................................................................................9

Table of Contents

Part A: Research Task.....................................................................................................................4

Answer to Question 1..................................................................................................................4

Answer to Question 2..................................................................................................................4

Answer to Question 3..................................................................................................................4

Answer to Question 4..................................................................................................................5

Part B...............................................................................................................................................6

Answer to Question 1..................................................................................................................6

Answer to Question 2..................................................................................................................6

Balance Sheet...............................................................................................................................6

Answer to Question 8..................................................................................................................7

Answer to Question 9..................................................................................................................7

Answer to Question 10................................................................................................................7

Answer to Question 11................................................................................................................8

Answer to Question 12................................................................................................................8

Answer to Question 13................................................................................................................8

Answer to Question 17................................................................................................................8

Answer to Question 18................................................................................................................8

Multiple Choice Questions..............................................................................................................9

Answer to Question 2..................................................................................................................9

Answer to Question 3..................................................................................................................9

Answer to Question 4..................................................................................................................9

Answer to Question 5..................................................................................................................9

2BUDGETING

Answer to Question 6..................................................................................................................9

Answer to Question 7..................................................................................................................9

Answer to Question 8..................................................................................................................9

Answer to Question 9..................................................................................................................9

Answer to Question 10................................................................................................................9

Answer to Question 11................................................................................................................9

Answer to Question 12................................................................................................................9

Answer to Question 13..............................................................................................................10

Answer to Question 14..............................................................................................................10

Answer to Question 15..............................................................................................................10

Trial Balance..................................................................................................................................10

Profit and Loss Statement..............................................................................................................10

Balance Sheet.................................................................................................................................11

Assessment Activity: Accounting Terminology............................................................................11

Cash Receipts.............................................................................................................................11

Cash Sales..................................................................................................................................11

Petty Cash..................................................................................................................................12

Purchase Journal........................................................................................................................12

Payroll Journal...........................................................................................................................12

Current ratio...............................................................................................................................12

Acid test ratio.............................................................................................................................12

Accounts receivable as a percentage of total revenue...............................................................12

Accounts receivable turnover ratio............................................................................................12

Return on Assets........................................................................................................................12

Net return on asset.....................................................................................................................13

Answer to Question 6..................................................................................................................9

Answer to Question 7..................................................................................................................9

Answer to Question 8..................................................................................................................9

Answer to Question 9..................................................................................................................9

Answer to Question 10................................................................................................................9

Answer to Question 11................................................................................................................9

Answer to Question 12................................................................................................................9

Answer to Question 13..............................................................................................................10

Answer to Question 14..............................................................................................................10

Answer to Question 15..............................................................................................................10

Trial Balance..................................................................................................................................10

Profit and Loss Statement..............................................................................................................10

Balance Sheet.................................................................................................................................11

Assessment Activity: Accounting Terminology............................................................................11

Cash Receipts.............................................................................................................................11

Cash Sales..................................................................................................................................11

Petty Cash..................................................................................................................................12

Purchase Journal........................................................................................................................12

Payroll Journal...........................................................................................................................12

Current ratio...............................................................................................................................12

Acid test ratio.............................................................................................................................12

Accounts receivable as a percentage of total revenue...............................................................12

Accounts receivable turnover ratio............................................................................................12

Return on Assets........................................................................................................................12

Net return on asset.....................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUDGETING

Return on stockholder’s equity..................................................................................................13

Inventory turnover.....................................................................................................................13

Working Capital turnover..........................................................................................................13

Gross profit margin....................................................................................................................13

Net profit margin.......................................................................................................................13

Asset turnover ratio....................................................................................................................13

Contribution margin ratio..........................................................................................................13

Margin of safety.........................................................................................................................13

Ownership ratio.........................................................................................................................14

Breakeven point.........................................................................................................................14

Sales increase.............................................................................................................................14

Cost justification........................................................................................................................14

Sales objectives..........................................................................................................................14

Food cost percentage.................................................................................................................14

Gross profit on food...................................................................................................................14

Food stock turn..........................................................................................................................14

Beverage cost percentage..........................................................................................................15

Total payroll...............................................................................................................................15

Cost of Goods sold.....................................................................................................................15

Gross profit margin....................................................................................................................15

Debt to Equity ratio...................................................................................................................15

Overheads..................................................................................................................................15

References and Bibliography.........................................................................................................16

Return on stockholder’s equity..................................................................................................13

Inventory turnover.....................................................................................................................13

Working Capital turnover..........................................................................................................13

Gross profit margin....................................................................................................................13

Net profit margin.......................................................................................................................13

Asset turnover ratio....................................................................................................................13

Contribution margin ratio..........................................................................................................13

Margin of safety.........................................................................................................................13

Ownership ratio.........................................................................................................................14

Breakeven point.........................................................................................................................14

Sales increase.............................................................................................................................14

Cost justification........................................................................................................................14

Sales objectives..........................................................................................................................14

Food cost percentage.................................................................................................................14

Gross profit on food...................................................................................................................14

Food stock turn..........................................................................................................................14

Beverage cost percentage..........................................................................................................15

Total payroll...............................................................................................................................15

Cost of Goods sold.....................................................................................................................15

Gross profit margin....................................................................................................................15

Debt to Equity ratio...................................................................................................................15

Overheads..................................................................................................................................15

References and Bibliography.........................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUDGETING

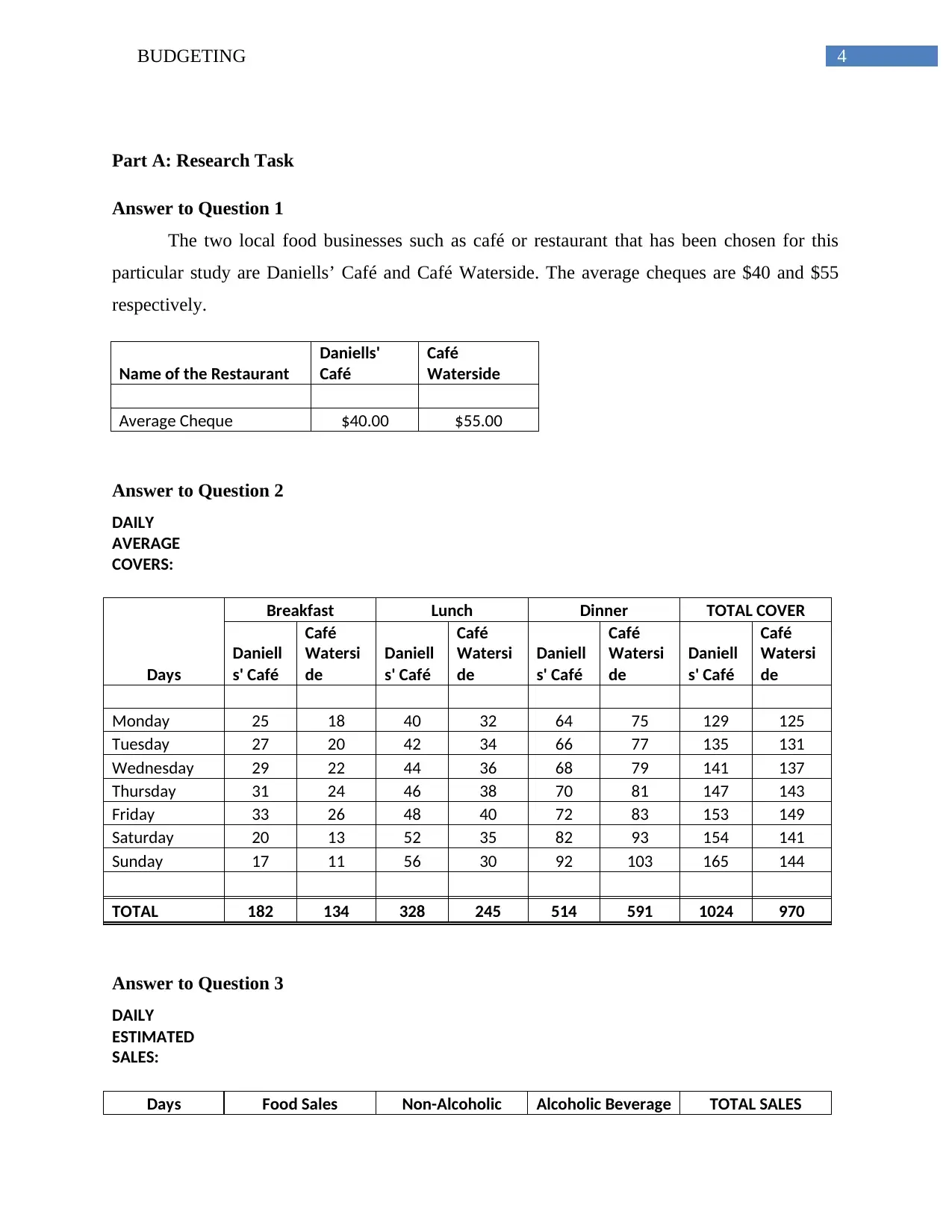

Part A: Research Task

Answer to Question 1

The two local food businesses such as café or restaurant that has been chosen for this

particular study are Daniells’ Café and Café Waterside. The average cheques are $40 and $55

respectively.

Name of the Restaurant

Daniells'

Café

Café

Waterside

Average Cheque $40.00 $55.00

Answer to Question 2

DAILY

AVERAGE

COVERS:

Days

Breakfast Lunch Dinner TOTAL COVER

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Monday 25 18 40 32 64 75 129 125

Tuesday 27 20 42 34 66 77 135 131

Wednesday 29 22 44 36 68 79 141 137

Thursday 31 24 46 38 70 81 147 143

Friday 33 26 48 40 72 83 153 149

Saturday 20 13 52 35 82 93 154 141

Sunday 17 11 56 30 92 103 165 144

TOTAL 182 134 328 245 514 591 1024 970

Answer to Question 3

DAILY

ESTIMATED

SALES:

Days Food Sales Non-Alcoholic Alcoholic Beverage TOTAL SALES

Part A: Research Task

Answer to Question 1

The two local food businesses such as café or restaurant that has been chosen for this

particular study are Daniells’ Café and Café Waterside. The average cheques are $40 and $55

respectively.

Name of the Restaurant

Daniells'

Café

Café

Waterside

Average Cheque $40.00 $55.00

Answer to Question 2

DAILY

AVERAGE

COVERS:

Days

Breakfast Lunch Dinner TOTAL COVER

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Monday 25 18 40 32 64 75 129 125

Tuesday 27 20 42 34 66 77 135 131

Wednesday 29 22 44 36 68 79 141 137

Thursday 31 24 46 38 70 81 147 143

Friday 33 26 48 40 72 83 153 149

Saturday 20 13 52 35 82 93 154 141

Sunday 17 11 56 30 92 103 165 144

TOTAL 182 134 328 245 514 591 1024 970

Answer to Question 3

DAILY

ESTIMATED

SALES:

Days Food Sales Non-Alcoholic Alcoholic Beverage TOTAL SALES

5BUDGETING

Beverage Sales Sales

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

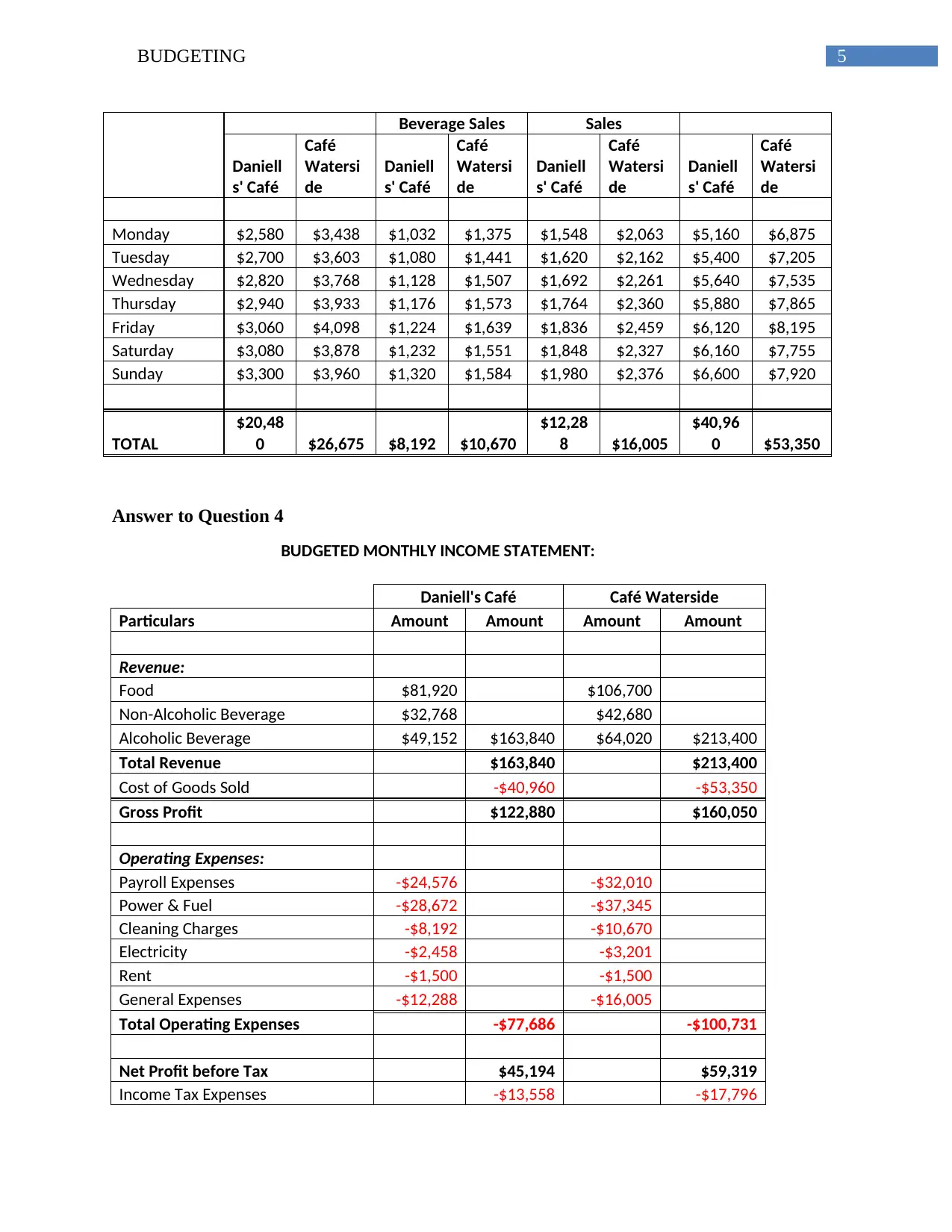

Monday $2,580 $3,438 $1,032 $1,375 $1,548 $2,063 $5,160 $6,875

Tuesday $2,700 $3,603 $1,080 $1,441 $1,620 $2,162 $5,400 $7,205

Wednesday $2,820 $3,768 $1,128 $1,507 $1,692 $2,261 $5,640 $7,535

Thursday $2,940 $3,933 $1,176 $1,573 $1,764 $2,360 $5,880 $7,865

Friday $3,060 $4,098 $1,224 $1,639 $1,836 $2,459 $6,120 $8,195

Saturday $3,080 $3,878 $1,232 $1,551 $1,848 $2,327 $6,160 $7,755

Sunday $3,300 $3,960 $1,320 $1,584 $1,980 $2,376 $6,600 $7,920

TOTAL

$20,48

0 $26,675 $8,192 $10,670

$12,28

8 $16,005

$40,96

0 $53,350

Answer to Question 4

BUDGETED MONTHLY INCOME STATEMENT:

Daniell's Café Café Waterside

Particulars Amount Amount Amount Amount

Revenue:

Food $81,920 $106,700

Non-Alcoholic Beverage $32,768 $42,680

Alcoholic Beverage $49,152 $163,840 $64,020 $213,400

Total Revenue $163,840 $213,400

Cost of Goods Sold -$40,960 -$53,350

Gross Profit $122,880 $160,050

Operating Expenses:

Payroll Expenses -$24,576 -$32,010

Power & Fuel -$28,672 -$37,345

Cleaning Charges -$8,192 -$10,670

Electricity -$2,458 -$3,201

Rent -$1,500 -$1,500

General Expenses -$12,288 -$16,005

Total Operating Expenses -$77,686 -$100,731

Net Profit before Tax $45,194 $59,319

Income Tax Expenses -$13,558 -$17,796

Beverage Sales Sales

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Daniell

s' Café

Café

Watersi

de

Monday $2,580 $3,438 $1,032 $1,375 $1,548 $2,063 $5,160 $6,875

Tuesday $2,700 $3,603 $1,080 $1,441 $1,620 $2,162 $5,400 $7,205

Wednesday $2,820 $3,768 $1,128 $1,507 $1,692 $2,261 $5,640 $7,535

Thursday $2,940 $3,933 $1,176 $1,573 $1,764 $2,360 $5,880 $7,865

Friday $3,060 $4,098 $1,224 $1,639 $1,836 $2,459 $6,120 $8,195

Saturday $3,080 $3,878 $1,232 $1,551 $1,848 $2,327 $6,160 $7,755

Sunday $3,300 $3,960 $1,320 $1,584 $1,980 $2,376 $6,600 $7,920

TOTAL

$20,48

0 $26,675 $8,192 $10,670

$12,28

8 $16,005

$40,96

0 $53,350

Answer to Question 4

BUDGETED MONTHLY INCOME STATEMENT:

Daniell's Café Café Waterside

Particulars Amount Amount Amount Amount

Revenue:

Food $81,920 $106,700

Non-Alcoholic Beverage $32,768 $42,680

Alcoholic Beverage $49,152 $163,840 $64,020 $213,400

Total Revenue $163,840 $213,400

Cost of Goods Sold -$40,960 -$53,350

Gross Profit $122,880 $160,050

Operating Expenses:

Payroll Expenses -$24,576 -$32,010

Power & Fuel -$28,672 -$37,345

Cleaning Charges -$8,192 -$10,670

Electricity -$2,458 -$3,201

Rent -$1,500 -$1,500

General Expenses -$12,288 -$16,005

Total Operating Expenses -$77,686 -$100,731

Net Profit before Tax $45,194 $59,319

Income Tax Expenses -$13,558 -$17,796

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUDGETING

Net Profit for the month $31,636 $41,523

Part B

Answer to Question 1

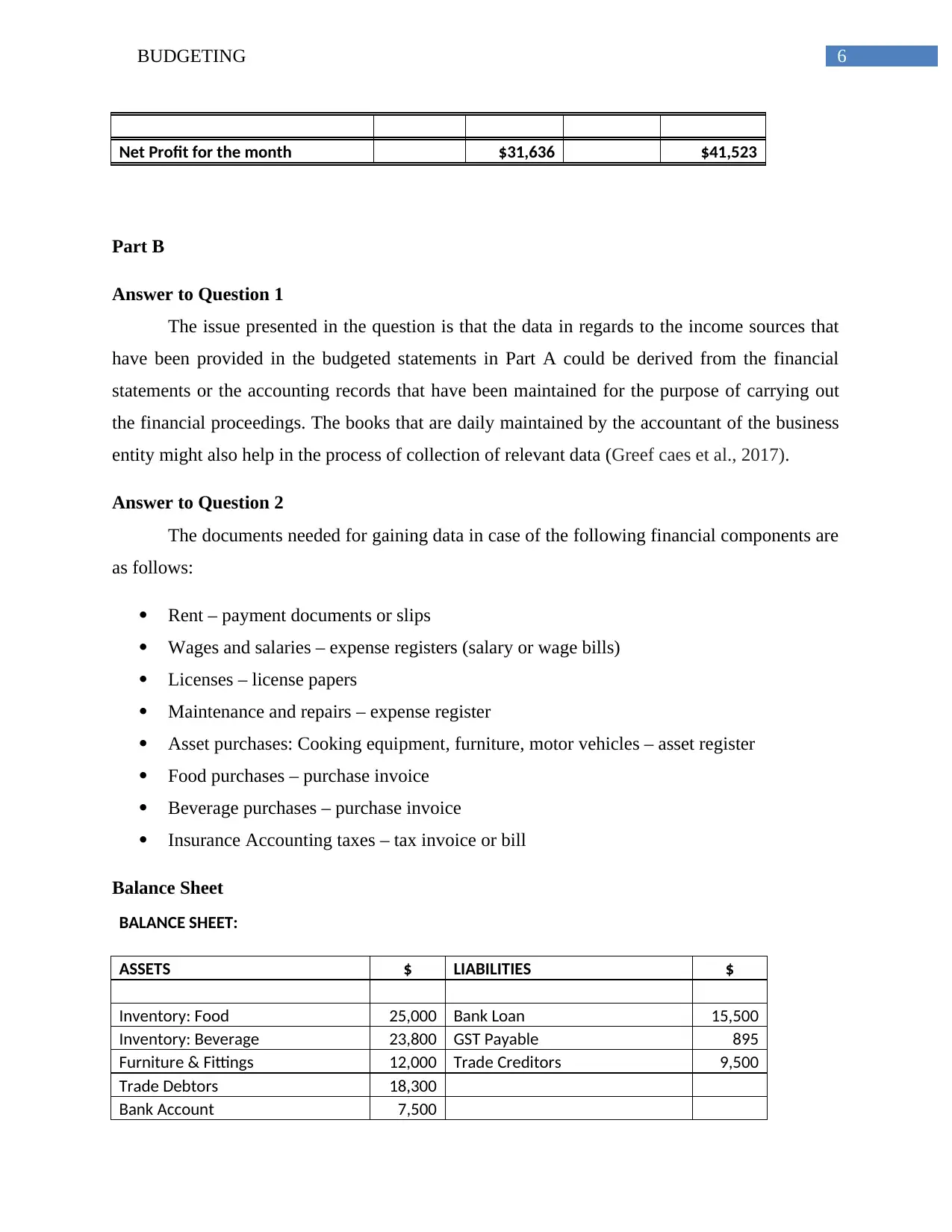

The issue presented in the question is that the data in regards to the income sources that

have been provided in the budgeted statements in Part A could be derived from the financial

statements or the accounting records that have been maintained for the purpose of carrying out

the financial proceedings. The books that are daily maintained by the accountant of the business

entity might also help in the process of collection of relevant data (Greef caes et al., 2017).

Answer to Question 2

The documents needed for gaining data in case of the following financial components are

as follows:

Rent – payment documents or slips

Wages and salaries – expense registers (salary or wage bills)

Licenses – license papers

Maintenance and repairs – expense register

Asset purchases: Cooking equipment, furniture, motor vehicles – asset register

Food purchases – purchase invoice

Beverage purchases – purchase invoice

Insurance Accounting taxes – tax invoice or bill

Balance Sheet

BALANCE SHEET:

ASSETS $ LIABILITIES $

Inventory: Food 25,000 Bank Loan 15,500

Inventory: Beverage 23,800 GST Payable 895

Furniture & Fittings 12,000 Trade Creditors 9,500

Trade Debtors 18,300

Bank Account 7,500

Net Profit for the month $31,636 $41,523

Part B

Answer to Question 1

The issue presented in the question is that the data in regards to the income sources that

have been provided in the budgeted statements in Part A could be derived from the financial

statements or the accounting records that have been maintained for the purpose of carrying out

the financial proceedings. The books that are daily maintained by the accountant of the business

entity might also help in the process of collection of relevant data (Greef caes et al., 2017).

Answer to Question 2

The documents needed for gaining data in case of the following financial components are

as follows:

Rent – payment documents or slips

Wages and salaries – expense registers (salary or wage bills)

Licenses – license papers

Maintenance and repairs – expense register

Asset purchases: Cooking equipment, furniture, motor vehicles – asset register

Food purchases – purchase invoice

Beverage purchases – purchase invoice

Insurance Accounting taxes – tax invoice or bill

Balance Sheet

BALANCE SHEET:

ASSETS $ LIABILITIES $

Inventory: Food 25,000 Bank Loan 15,500

Inventory: Beverage 23,800 GST Payable 895

Furniture & Fittings 12,000 Trade Creditors 9,500

Trade Debtors 18,300

Bank Account 7,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUDGETING

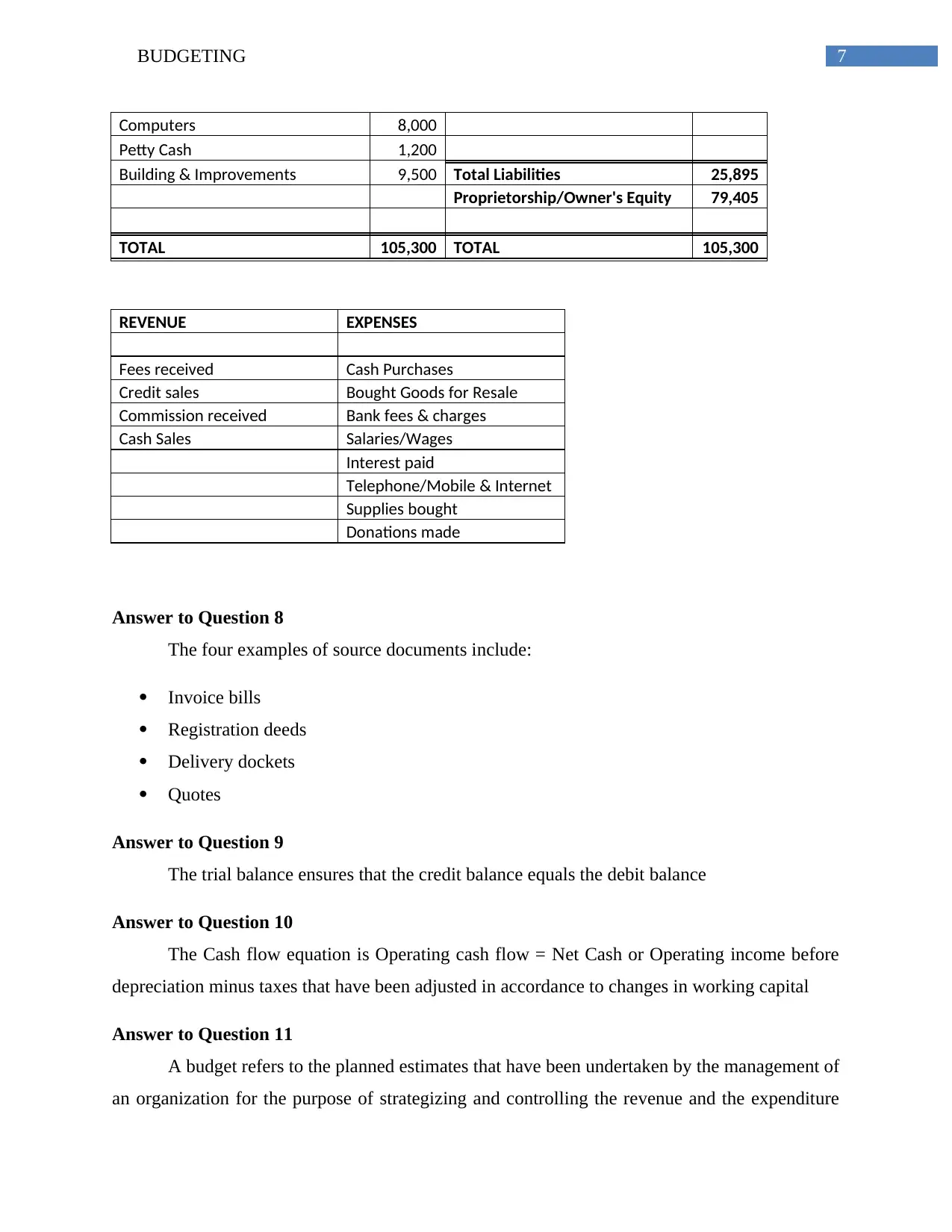

Computers 8,000

Petty Cash 1,200

Building & Improvements 9,500 Total Liabilities 25,895

Proprietorship/Owner's Equity 79,405

TOTAL 105,300 TOTAL 105,300

REVENUE EXPENSES

Fees received Cash Purchases

Credit sales Bought Goods for Resale

Commission received Bank fees & charges

Cash Sales Salaries/Wages

Interest paid

Telephone/Mobile & Internet

Supplies bought

Donations made

Answer to Question 8

The four examples of source documents include:

Invoice bills

Registration deeds

Delivery dockets

Quotes

Answer to Question 9

The trial balance ensures that the credit balance equals the debit balance

Answer to Question 10

The Cash flow equation is Operating cash flow = Net Cash or Operating income before

depreciation minus taxes that have been adjusted in accordance to changes in working capital

Answer to Question 11

A budget refers to the planned estimates that have been undertaken by the management of

an organization for the purpose of strategizing and controlling the revenue and the expenditure

Computers 8,000

Petty Cash 1,200

Building & Improvements 9,500 Total Liabilities 25,895

Proprietorship/Owner's Equity 79,405

TOTAL 105,300 TOTAL 105,300

REVENUE EXPENSES

Fees received Cash Purchases

Credit sales Bought Goods for Resale

Commission received Bank fees & charges

Cash Sales Salaries/Wages

Interest paid

Telephone/Mobile & Internet

Supplies bought

Donations made

Answer to Question 8

The four examples of source documents include:

Invoice bills

Registration deeds

Delivery dockets

Quotes

Answer to Question 9

The trial balance ensures that the credit balance equals the debit balance

Answer to Question 10

The Cash flow equation is Operating cash flow = Net Cash or Operating income before

depreciation minus taxes that have been adjusted in accordance to changes in working capital

Answer to Question 11

A budget refers to the planned estimates that have been undertaken by the management of

an organization for the purpose of strategizing and controlling the revenue and the expenditure

8BUDGETING

for a specific time period in the future. A budget helps in providing a projected view into the

future estimates of business along with forecasting the profits or losses for business that can be

incurred via the estimates (Brown caes et al., 2016).

Answer to Question 12

A zero based budgeting refers to that method of budgeting that leads to the justification

of each of the new expenses that have been incurred. The essential process that a zero based

budgeting follows is that it starts from a zero base. This means that the total inflow of cash in

business minus total outflow of cash must be equal to zero. This will facilitate the allocation of

each and every monetary component of business (Brown caes et al., 2016).

Answer to Question 13

A rolling budget refers to that budget which is updated on a continuous basis for the

purpose of addition of a new budget with the completion of the current budgeted period. The

rolling budget facilitates the extension of the current thus making sure that the business is

continuously supported by a financial budget (Brown caes et al., 2016).

Answer to Question 17

The term variance refers to the difference between the two financial components.

However, the term budget is a relevant concept in case of the budgets. In case of the budgets,

relevance refers to the difference between the budgeted estimates and the actual estimates. A

variance can be favorable in nature indicating that the budgeted estimated has been more or less

accurate in comparison to the real expense or income that has been incurred by business.

However, in case of an unfavorable variance the estimated income does not match with the real

scenario. A variance analysis is essentially drawn in order to measure the effectiveness of a

prepared budget.

Answer to Question 18

Budgets (estimated income) – financial budget

Budgets ( estimated of costs) – overhead budget; material budget; labor budget;

Budgets (expected financing activities and summary results of the coming period) –

revenue budget

for a specific time period in the future. A budget helps in providing a projected view into the

future estimates of business along with forecasting the profits or losses for business that can be

incurred via the estimates (Brown caes et al., 2016).

Answer to Question 12

A zero based budgeting refers to that method of budgeting that leads to the justification

of each of the new expenses that have been incurred. The essential process that a zero based

budgeting follows is that it starts from a zero base. This means that the total inflow of cash in

business minus total outflow of cash must be equal to zero. This will facilitate the allocation of

each and every monetary component of business (Brown caes et al., 2016).

Answer to Question 13

A rolling budget refers to that budget which is updated on a continuous basis for the

purpose of addition of a new budget with the completion of the current budgeted period. The

rolling budget facilitates the extension of the current thus making sure that the business is

continuously supported by a financial budget (Brown caes et al., 2016).

Answer to Question 17

The term variance refers to the difference between the two financial components.

However, the term budget is a relevant concept in case of the budgets. In case of the budgets,

relevance refers to the difference between the budgeted estimates and the actual estimates. A

variance can be favorable in nature indicating that the budgeted estimated has been more or less

accurate in comparison to the real expense or income that has been incurred by business.

However, in case of an unfavorable variance the estimated income does not match with the real

scenario. A variance analysis is essentially drawn in order to measure the effectiveness of a

prepared budget.

Answer to Question 18

Budgets (estimated income) – financial budget

Budgets ( estimated of costs) – overhead budget; material budget; labor budget;

Budgets (expected financing activities and summary results of the coming period) –

revenue budget

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUDGETING

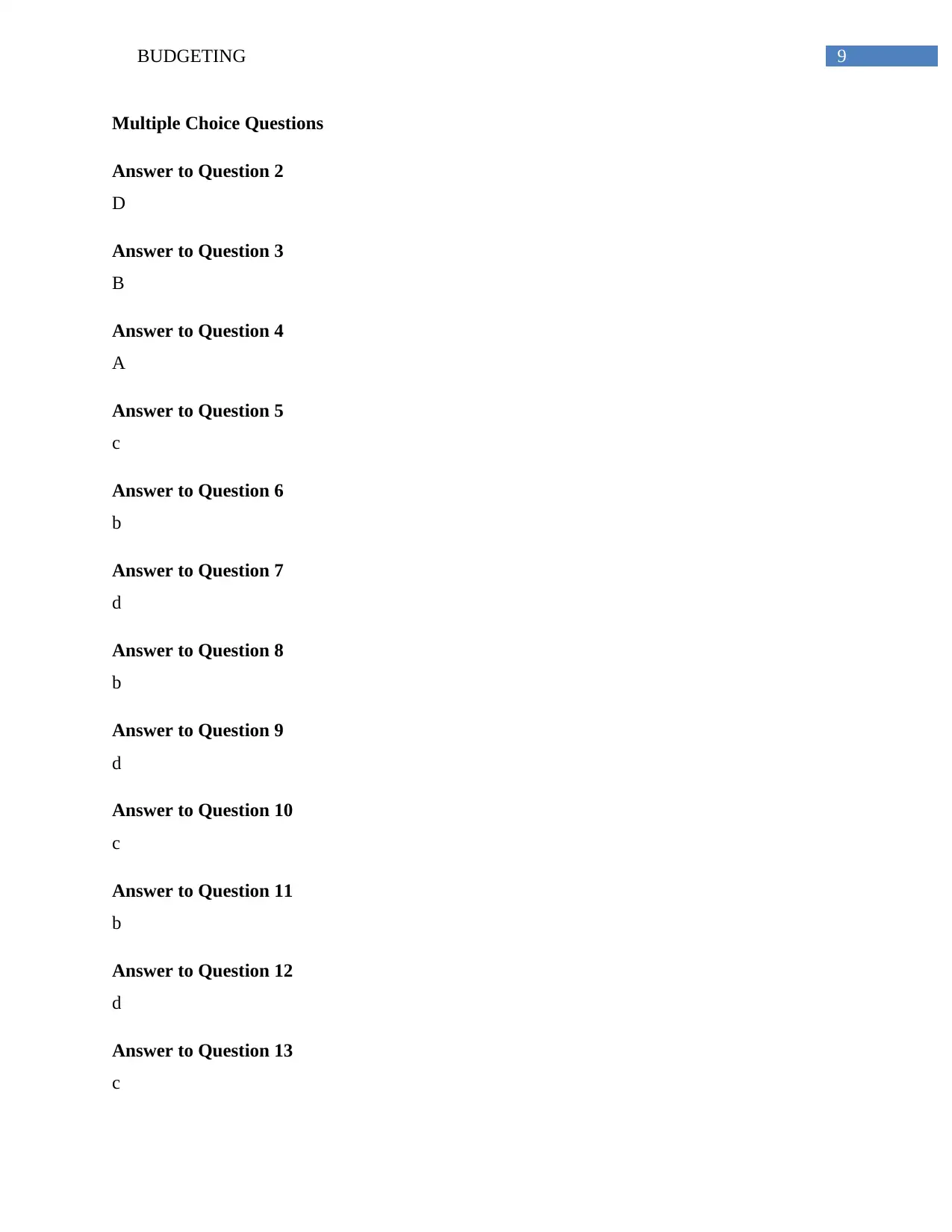

Multiple Choice Questions

Answer to Question 2

D

Answer to Question 3

B

Answer to Question 4

A

Answer to Question 5

c

Answer to Question 6

b

Answer to Question 7

d

Answer to Question 8

b

Answer to Question 9

d

Answer to Question 10

c

Answer to Question 11

b

Answer to Question 12

d

Answer to Question 13

c

Multiple Choice Questions

Answer to Question 2

D

Answer to Question 3

B

Answer to Question 4

A

Answer to Question 5

c

Answer to Question 6

b

Answer to Question 7

d

Answer to Question 8

b

Answer to Question 9

d

Answer to Question 10

c

Answer to Question 11

b

Answer to Question 12

d

Answer to Question 13

c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUDGETING

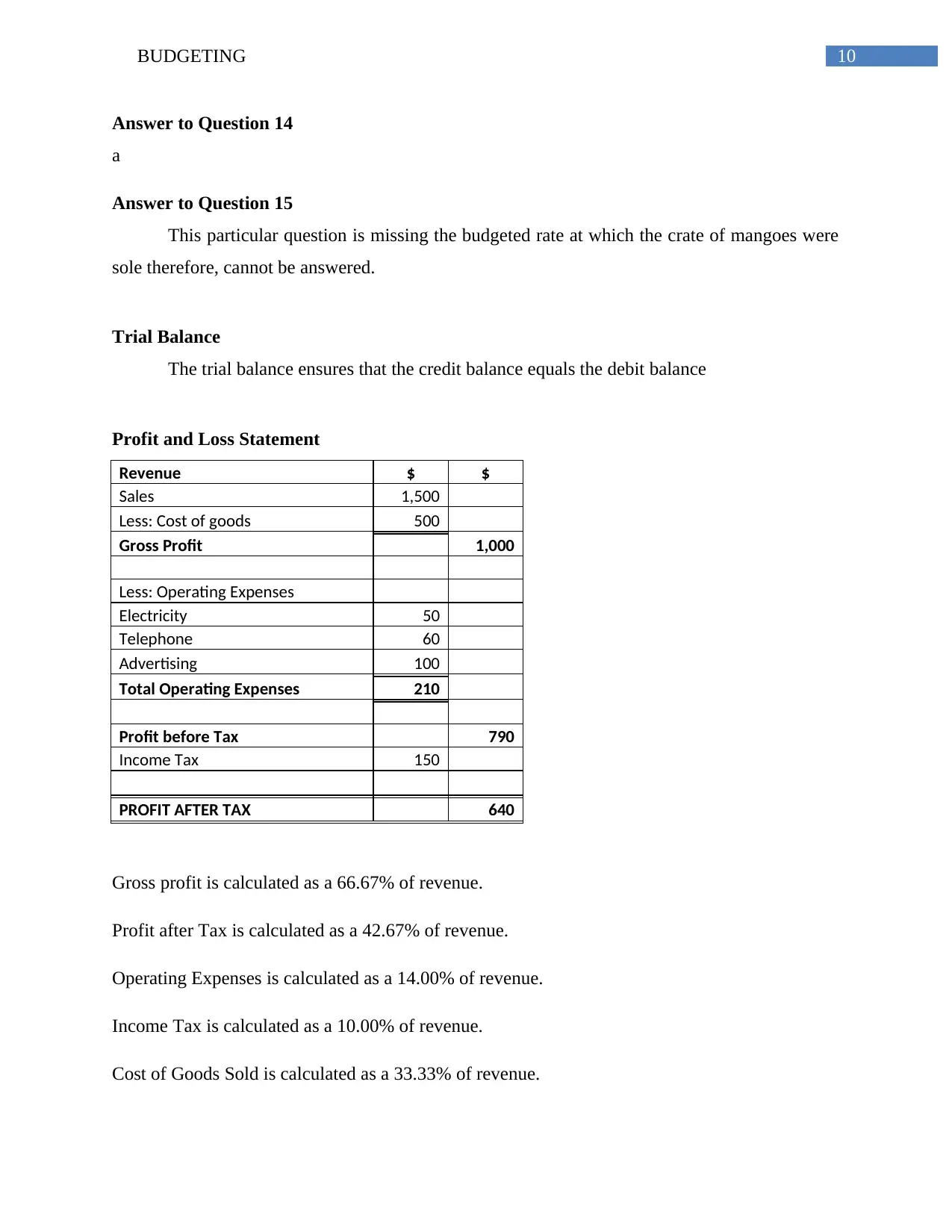

Answer to Question 14

a

Answer to Question 15

This particular question is missing the budgeted rate at which the crate of mangoes were

sole therefore, cannot be answered.

Trial Balance

The trial balance ensures that the credit balance equals the debit balance

Profit and Loss Statement

Revenue $ $

Sales 1,500

Less: Cost of goods 500

Gross Profit 1,000

Less: Operating Expenses

Electricity 50

Telephone 60

Advertising 100

Total Operating Expenses 210

Profit before Tax 790

Income Tax 150

PROFIT AFTER TAX 640

Gross profit is calculated as a 66.67% of revenue.

Profit after Tax is calculated as a 42.67% of revenue.

Operating Expenses is calculated as a 14.00% of revenue.

Income Tax is calculated as a 10.00% of revenue.

Cost of Goods Sold is calculated as a 33.33% of revenue.

Answer to Question 14

a

Answer to Question 15

This particular question is missing the budgeted rate at which the crate of mangoes were

sole therefore, cannot be answered.

Trial Balance

The trial balance ensures that the credit balance equals the debit balance

Profit and Loss Statement

Revenue $ $

Sales 1,500

Less: Cost of goods 500

Gross Profit 1,000

Less: Operating Expenses

Electricity 50

Telephone 60

Advertising 100

Total Operating Expenses 210

Profit before Tax 790

Income Tax 150

PROFIT AFTER TAX 640

Gross profit is calculated as a 66.67% of revenue.

Profit after Tax is calculated as a 42.67% of revenue.

Operating Expenses is calculated as a 14.00% of revenue.

Income Tax is calculated as a 10.00% of revenue.

Cost of Goods Sold is calculated as a 33.33% of revenue.

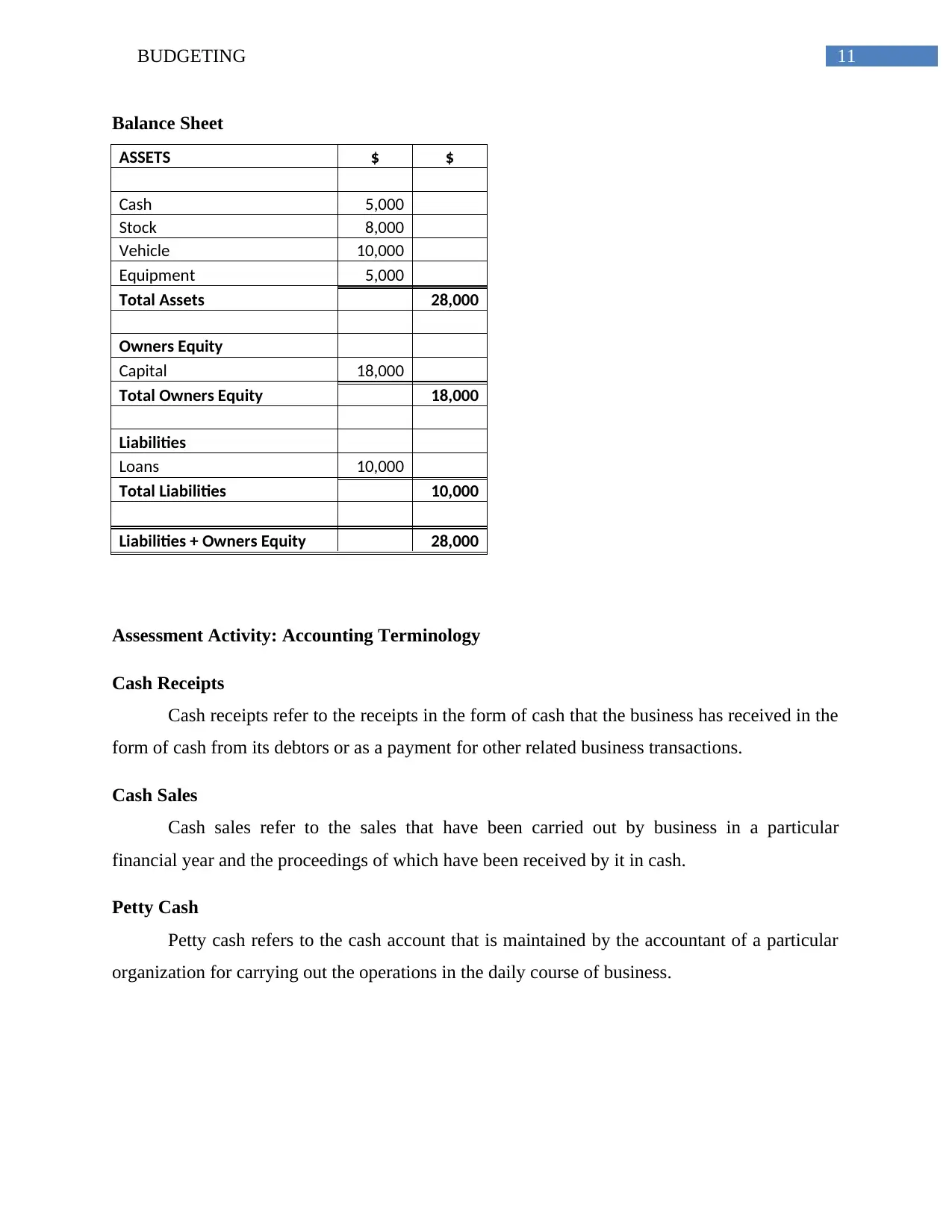

11BUDGETING

Balance Sheet

ASSETS $ $

Cash 5,000

Stock 8,000

Vehicle 10,000

Equipment 5,000

Total Assets 28,000

Owners Equity

Capital 18,000

Total Owners Equity 18,000

Liabilities

Loans 10,000

Total Liabilities 10,000

Liabilities + Owners Equity 28,000

Assessment Activity: Accounting Terminology

Cash Receipts

Cash receipts refer to the receipts in the form of cash that the business has received in the

form of cash from its debtors or as a payment for other related business transactions.

Cash Sales

Cash sales refer to the sales that have been carried out by business in a particular

financial year and the proceedings of which have been received by it in cash.

Petty Cash

Petty cash refers to the cash account that is maintained by the accountant of a particular

organization for carrying out the operations in the daily course of business.

Balance Sheet

ASSETS $ $

Cash 5,000

Stock 8,000

Vehicle 10,000

Equipment 5,000

Total Assets 28,000

Owners Equity

Capital 18,000

Total Owners Equity 18,000

Liabilities

Loans 10,000

Total Liabilities 10,000

Liabilities + Owners Equity 28,000

Assessment Activity: Accounting Terminology

Cash Receipts

Cash receipts refer to the receipts in the form of cash that the business has received in the

form of cash from its debtors or as a payment for other related business transactions.

Cash Sales

Cash sales refer to the sales that have been carried out by business in a particular

financial year and the proceedings of which have been received by it in cash.

Petty Cash

Petty cash refers to the cash account that is maintained by the accountant of a particular

organization for carrying out the operations in the daily course of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.