UGB253 Management Accounting for Business A: Budgeting Analysis Report

VerifiedAdded on 2023/06/01

|8

|3068

|152

Report

AI Summary

This report provides a comprehensive analysis of fixed and flexible budgets in management accounting. It begins by defining and differentiating between fixed and flexible budgets, outlining their respective advantages and disadvantages. The report then delves into the behavioral aspects of budgeting, discussing symbolism, goal congruence, participatory budgeting, and budgetary discrepancies. A case study is presented, analyzing a scenario involving Citrus Grove and a potential contract, evaluating whether the company should accept or reject the offer from Borges, and subsequently, if it should outsource production to an English supplier. Finally, the report considers the impact of management accounting choices on external reputation, labor relations, creditor effects, and product quality, offering insights into how these factors influence decision-making. The report combines theoretical concepts with practical applications, providing a thorough understanding of budgeting and its implications in a business context.

UGB253 Management Accounting for

Business

A 1

A.

Flexible Budget vs Fixed Budget

Fixed budget

It is necessary to grasp what the terms "fixed budget" and "budget" mean before you can

comprehend the phrase "fixed budget." Budget refers to an estimate of the company's economic

activity, while "fixed" refers to anything that is "solid" or "stable." When profits and expenditures

are predetermined in advance, they are referred to as a "Fixed Budget" in this context since they stay

constant regardless of changes in activity levels. When it comes to budgeting, this kind of budget is

referred to as a Static Budget. Providing the company's conditions are stable and forecasting is

straightforward, fixed budgets are an ideal option for businesses that are not at danger of

unanticipated changes in their existing circumstances or external influences, which is the case in

most cases. It's also a good method to keep track of your spending. The management of a

corporation benefits from having a predetermined budget, but it lacks precision since it is hard to

accurately predict future demands and requirements in advance. Aside from that, it only operates on

a single level of activity at a time, which is quite restrictive. When the fixed budget was developed,

it was assumed that the current conditions would not alter in the foreseeable future; nevertheless,

this proved to be erroneous. As a result, it is possible that measures of efficiency and capacity may

be troublesome.

Flexible budget

Having a flexible budget indicates that an organization's financial operations may be readily

adjusted if the budget is kept flexible. In this way, a flexible budget is one that is capable of

accommodating a broad variety of activity levels. It may be possible to simply change or recast the

conclusion, depending on the situation. Because the expenses associated with different levels of

activity can be simply calculated, this is a reasonable and practical option. In the first stage of the

analysis, expenses are divided into three broad categories: fixed, variable, and semi-variable. Semi-

variable costs are further subdivided into fixed and variable costs, respectively. The budget is then

created in accordance with this information. In order to demonstrate how much money will be spent

at each step of the project's development, budgets for different production levels are prepared. They

are particularly appropriate for businesses that have a high degree of unpredictability in sales and

production, sectors that are quickly impacted by external variables or industries that see significant

variations in market circumstances, and so on.

1 | P a g e

Business

A 1

A.

Flexible Budget vs Fixed Budget

Fixed budget

It is necessary to grasp what the terms "fixed budget" and "budget" mean before you can

comprehend the phrase "fixed budget." Budget refers to an estimate of the company's economic

activity, while "fixed" refers to anything that is "solid" or "stable." When profits and expenditures

are predetermined in advance, they are referred to as a "Fixed Budget" in this context since they stay

constant regardless of changes in activity levels. When it comes to budgeting, this kind of budget is

referred to as a Static Budget. Providing the company's conditions are stable and forecasting is

straightforward, fixed budgets are an ideal option for businesses that are not at danger of

unanticipated changes in their existing circumstances or external influences, which is the case in

most cases. It's also a good method to keep track of your spending. The management of a

corporation benefits from having a predetermined budget, but it lacks precision since it is hard to

accurately predict future demands and requirements in advance. Aside from that, it only operates on

a single level of activity at a time, which is quite restrictive. When the fixed budget was developed,

it was assumed that the current conditions would not alter in the foreseeable future; nevertheless,

this proved to be erroneous. As a result, it is possible that measures of efficiency and capacity may

be troublesome.

Flexible budget

Having a flexible budget indicates that an organization's financial operations may be readily

adjusted if the budget is kept flexible. In this way, a flexible budget is one that is capable of

accommodating a broad variety of activity levels. It may be possible to simply change or recast the

conclusion, depending on the situation. Because the expenses associated with different levels of

activity can be simply calculated, this is a reasonable and practical option. In the first stage of the

analysis, expenses are divided into three broad categories: fixed, variable, and semi-variable. Semi-

variable costs are further subdivided into fixed and variable costs, respectively. The budget is then

created in accordance with this information. In order to demonstrate how much money will be spent

at each step of the project's development, budgets for different production levels are prepared. They

are particularly appropriate for businesses that have a high degree of unpredictability in sales and

production, sectors that are quickly impacted by external variables or industries that see significant

variations in market circumstances, and so on.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

What is the difference between Fixed Budget and Flexible Budget?

In accordance with the following characteristics, budgets may be divided into two categories:

"fixed" and "flexible."

In finance, a fixed budget is a budget that does not vary in response to actual production.

The term "flexible budget" refers to a budget that may be quickly altered in response to

changes in production levels.

• A fixed budget remains static, whereas a flexible budget is constantly changing.

In contrast to a set budget, a flexible budget is capable of operating at a variety of different

levels of output.

Flexibility in budgeting is based on real facts, while rigidity in budgeting is based on

estimates.

Due to the inability to recast fixed budgets in light of actual production, they are unable to be

made flexible. Flexible budgets are elastic because they may be altered quickly in response

to changes in production levels.

B.

Flexible Budget Pros:

1. Being able to adjust budgets as your business grows and income rises is more realistic than

having rigid budgets in place.

2. In the event of increasing demand or other external circumstances, this budget model may be

used to explain major deviations from the norm that may have happened.

3. If your spending and revenues are exactly equal to one another, you can automate your

budgeting process.

4. Do you have concerns about what the future may hold? With a flexible budget, it is possible

to account for the unexpected and the unplanned.

5. In the event that you are unclear of how much money you will generate, a flexible budget

model enables you to compare and contrast numerous different options.

Flexible Budget Cons:

1. Budgeting is difficult since there is not always a 1:1 relationship between income and

variable expenses.

2 This approach of budgeting will be ineffective for you if your expenditure is not precisely

proportional to your income.

C.

Behavioral aspects of budgeting

Symbolism: A firm's budget serves as a symbol of the goals and objectives that the organization has

established for itself. It is possible that achieving it will serve as a source of inspiration for other

people's efforts. Employees may underperform if their expectations are set too low, which may

result in a lack of motivation on the part of the organization. Underperformance may stem from

2 | P a g e

In accordance with the following characteristics, budgets may be divided into two categories:

"fixed" and "flexible."

In finance, a fixed budget is a budget that does not vary in response to actual production.

The term "flexible budget" refers to a budget that may be quickly altered in response to

changes in production levels.

• A fixed budget remains static, whereas a flexible budget is constantly changing.

In contrast to a set budget, a flexible budget is capable of operating at a variety of different

levels of output.

Flexibility in budgeting is based on real facts, while rigidity in budgeting is based on

estimates.

Due to the inability to recast fixed budgets in light of actual production, they are unable to be

made flexible. Flexible budgets are elastic because they may be altered quickly in response

to changes in production levels.

B.

Flexible Budget Pros:

1. Being able to adjust budgets as your business grows and income rises is more realistic than

having rigid budgets in place.

2. In the event of increasing demand or other external circumstances, this budget model may be

used to explain major deviations from the norm that may have happened.

3. If your spending and revenues are exactly equal to one another, you can automate your

budgeting process.

4. Do you have concerns about what the future may hold? With a flexible budget, it is possible

to account for the unexpected and the unplanned.

5. In the event that you are unclear of how much money you will generate, a flexible budget

model enables you to compare and contrast numerous different options.

Flexible Budget Cons:

1. Budgeting is difficult since there is not always a 1:1 relationship between income and

variable expenses.

2 This approach of budgeting will be ineffective for you if your expenditure is not precisely

proportional to your income.

C.

Behavioral aspects of budgeting

Symbolism: A firm's budget serves as a symbol of the goals and objectives that the organization has

established for itself. It is possible that achieving it will serve as a source of inspiration for other

people's efforts. Employees may underperform if their expectations are set too low, which may

result in a lack of motivation on the part of the organization. Underperformance may stem from

2 | P a g e

setting unrealistically high goals. If the objectives are seen by the personnel to be unreasonable and

unachievable, they may have given up on them. The belief that budget objectives are achievable will

increase employee motivation to strive toward meeting them, according to the study. The more

sophisticated a budget is, the more difficult it is to evaluate its effectiveness. If the budget is set too

low, it is possible that real performance may suffer. Employees may have low expectations as a

result of a lack of motivation. When a budget is set too high, real performance suffers as a result.

Employees who feel the budget is both unachievable and doable may give up on the project

altogether. They do not intend to participate in this activity in order to prevent squandering their

time or effort in any way.

Conduct that is out of whack If the budget and management goals are matched, actual performance

will be in line with or even better than anticipated. The phrase "goal congruence" is used to

characterize this phenomenon. This refers to the consistency and alignment between individual goals

and the aims of the company as a whole. The achievement of the company's objectives will pave the

way for managers to pursue their own personal aspirations. Inconsistency in goal setting has a

detrimental impact on the motivation of managers. The fact that they may put in little (or no) effort

toward the budget may have a detrimental influence on actual performance.

People who are participating in the process of distributing resources are involved in Participatory

Budgeting (also known as IBB). It is possible to construct a budget from the top down or from the

bottom up depending on the situation. The budget is developed from the top down by management,

and then communicated to all workers at the same time. Participants and communicators on the team

aren't doing their jobs well. Workers are more involved in budgeting when they have a say in it, as

research has shown. Incorporating them was a key part of the entire plan. A sense of responsibility

and a connection to the budget are instilled in them as a result. People are more likely to persevere in

the pursuit of their objectives if they have a sense of control over the process. It may be possible to

boost morale and reduce resistance to budget cutbacks by encouraging worker engagement. It's also

possible that it'll help to lessen tensions inside a company. This approach improves the overall

motivation, productivity, and efficiency of the workforce.

Budgetary Discrepancy When the allocated resources do not meet the demands of the situation,

there is financial slack. Throughout the budget formulation process, managers inject financial slack,

which is referred to as "padding the budget." Their expenditures and expenses will be overstated,

while their income will be understated If they make such a request, the organization may feel

obligated to provide them with more resources. The inclination for managers in practically any

business, regardless of sector, to participate in this conduct may be seen. When it comes to putting

up the budget, the management will depend on their previous expertise. Despite their budgetary

requests, they were allocated less money than they had sought. A 5 percent markup is typical of

what they'll add to their estimate in order to cover their costs. To put it another way, even if they cut

down on their spending, they will still get the same amount of money that they had originally

intended to receive. When managers underestimate income and overestimate costs, they create

financial slack in the organization.

A 2

Data

3 | P a g e

unachievable, they may have given up on them. The belief that budget objectives are achievable will

increase employee motivation to strive toward meeting them, according to the study. The more

sophisticated a budget is, the more difficult it is to evaluate its effectiveness. If the budget is set too

low, it is possible that real performance may suffer. Employees may have low expectations as a

result of a lack of motivation. When a budget is set too high, real performance suffers as a result.

Employees who feel the budget is both unachievable and doable may give up on the project

altogether. They do not intend to participate in this activity in order to prevent squandering their

time or effort in any way.

Conduct that is out of whack If the budget and management goals are matched, actual performance

will be in line with or even better than anticipated. The phrase "goal congruence" is used to

characterize this phenomenon. This refers to the consistency and alignment between individual goals

and the aims of the company as a whole. The achievement of the company's objectives will pave the

way for managers to pursue their own personal aspirations. Inconsistency in goal setting has a

detrimental impact on the motivation of managers. The fact that they may put in little (or no) effort

toward the budget may have a detrimental influence on actual performance.

People who are participating in the process of distributing resources are involved in Participatory

Budgeting (also known as IBB). It is possible to construct a budget from the top down or from the

bottom up depending on the situation. The budget is developed from the top down by management,

and then communicated to all workers at the same time. Participants and communicators on the team

aren't doing their jobs well. Workers are more involved in budgeting when they have a say in it, as

research has shown. Incorporating them was a key part of the entire plan. A sense of responsibility

and a connection to the budget are instilled in them as a result. People are more likely to persevere in

the pursuit of their objectives if they have a sense of control over the process. It may be possible to

boost morale and reduce resistance to budget cutbacks by encouraging worker engagement. It's also

possible that it'll help to lessen tensions inside a company. This approach improves the overall

motivation, productivity, and efficiency of the workforce.

Budgetary Discrepancy When the allocated resources do not meet the demands of the situation,

there is financial slack. Throughout the budget formulation process, managers inject financial slack,

which is referred to as "padding the budget." Their expenditures and expenses will be overstated,

while their income will be understated If they make such a request, the organization may feel

obligated to provide them with more resources. The inclination for managers in practically any

business, regardless of sector, to participate in this conduct may be seen. When it comes to putting

up the budget, the management will depend on their previous expertise. Despite their budgetary

requests, they were allocated less money than they had sought. A 5 percent markup is typical of

what they'll add to their estimate in order to cover their costs. To put it another way, even if they cut

down on their spending, they will still get the same amount of money that they had originally

intended to receive. When managers underestimate income and overestimate costs, they create

financial slack in the organization.

A 2

Data

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

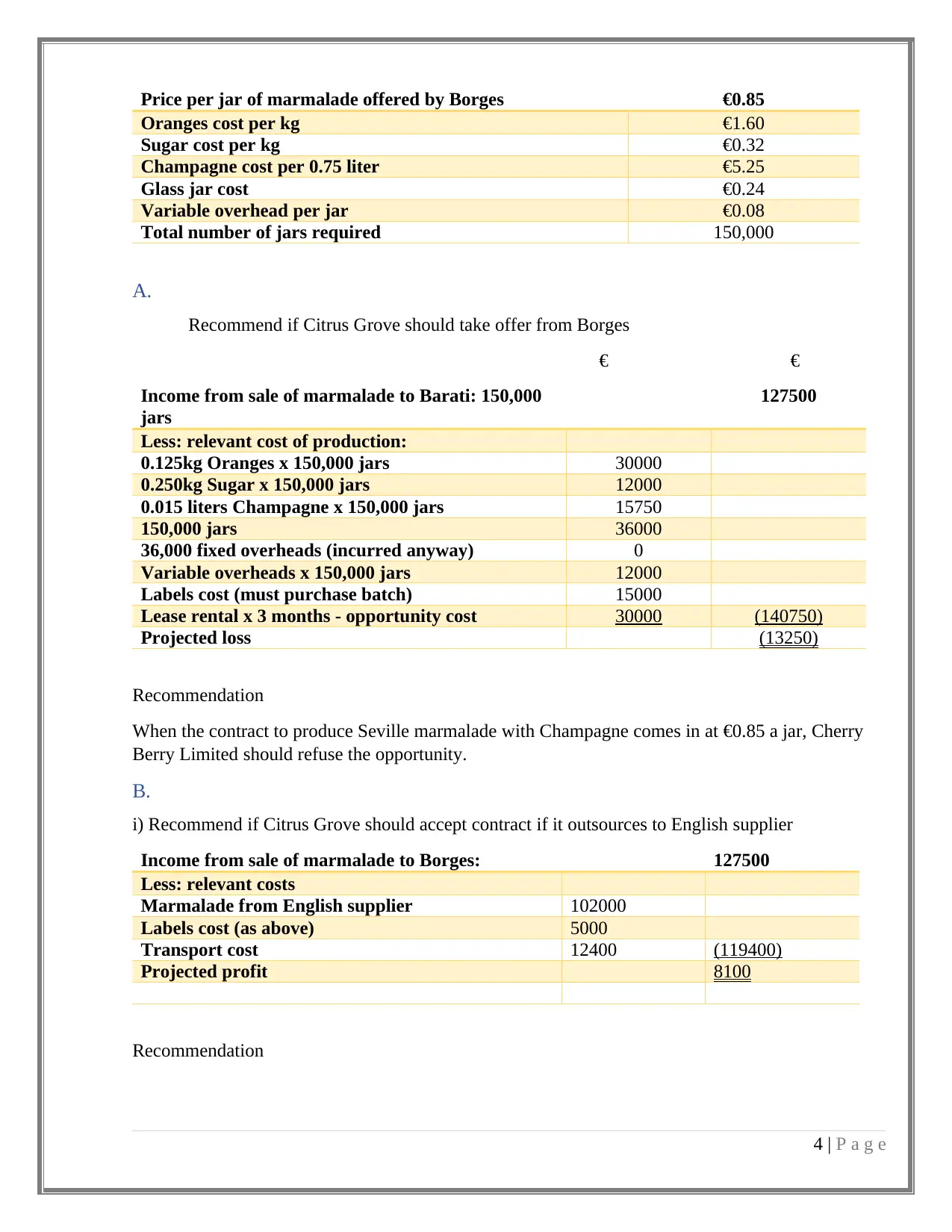

Price per jar of marmalade offered by Borges €0.85

Oranges cost per kg €1.60

Sugar cost per kg €0.32

Champagne cost per 0.75 liter €5.25

Glass jar cost €0.24

Variable overhead per jar €0.08

Total number of jars required 150,000

A.

Recommend if Citrus Grove should take offer from Borges

€ €

Income from sale of marmalade to Barati: 150,000

jars

127500

Less: relevant cost of production:

0.125kg Oranges x 150,000 jars 30000

0.250kg Sugar x 150,000 jars 12000

0.015 liters Champagne x 150,000 jars 15750

150,000 jars 36000

36,000 fixed overheads (incurred anyway) 0

Variable overheads x 150,000 jars 12000

Labels cost (must purchase batch) 15000

Lease rental x 3 months - opportunity cost 30000 (140750)

Projected loss (13250)

Recommendation

When the contract to produce Seville marmalade with Champagne comes in at €0.85 a jar, Cherry

Berry Limited should refuse the opportunity.

B.

i) Recommend if Citrus Grove should accept contract if it outsources to English supplier

Income from sale of marmalade to Borges: 127500

Less: relevant costs

Marmalade from English supplier 102000

Labels cost (as above) 5000

Transport cost 12400 (119400)

Projected profit 8100

Recommendation

4 | P a g e

Oranges cost per kg €1.60

Sugar cost per kg €0.32

Champagne cost per 0.75 liter €5.25

Glass jar cost €0.24

Variable overhead per jar €0.08

Total number of jars required 150,000

A.

Recommend if Citrus Grove should take offer from Borges

€ €

Income from sale of marmalade to Barati: 150,000

jars

127500

Less: relevant cost of production:

0.125kg Oranges x 150,000 jars 30000

0.250kg Sugar x 150,000 jars 12000

0.015 liters Champagne x 150,000 jars 15750

150,000 jars 36000

36,000 fixed overheads (incurred anyway) 0

Variable overheads x 150,000 jars 12000

Labels cost (must purchase batch) 15000

Lease rental x 3 months - opportunity cost 30000 (140750)

Projected loss (13250)

Recommendation

When the contract to produce Seville marmalade with Champagne comes in at €0.85 a jar, Cherry

Berry Limited should refuse the opportunity.

B.

i) Recommend if Citrus Grove should accept contract if it outsources to English supplier

Income from sale of marmalade to Borges: 127500

Less: relevant costs

Marmalade from English supplier 102000

Labels cost (as above) 5000

Transport cost 12400 (119400)

Projected profit 8100

Recommendation

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If production is outsourced to an English supplier, financial data indicates that Cherry Berry Limited

should accept the contract to manufacture Seville marmalade with Champagne since it will earn a

profit of €8,100 if the contract is accepted.

C.

External Reputation

Management accounting choices have a direct impact on how a small firm is seen by the general

public. In many circumstances, quantitative analysis may assist in narrowing down the options when

faced with a decision between two possibilities. However, this kind of study does not always take

into account all of the factors that are present in a particular case. For example, the assembly of

electronic components may be outsourced to a third-party manufacturing company. The research did

not evaluate the impact on consumers of the company's choice to shift its headquarters to a location

outside of the United States, even though future income statements indicate an increase in

profitability.

Labor Relations

Almost every quantitative study will indicate that spending less on personnel results in higher profit

margins. Despite the fact that it is possible that this is a mistake, quantitative decision-making

criteria are seldom employed in labor relations. When it comes to conserving money, organizations

may elect to remove an annual Christmas bonus that they have paid out for the previous 20 years.

Employees may see this as harsh or insensitive, despite the fact that it would surely save money.

Other techniques of cost-cutting are available to small-business owners as well. It's possible that it

would be preferable to reduce yearly pay increases by a few percentage points, or perhaps eliminate

the bonus entirely.

Creditor Effects

Some qualitative facts about a company's operations may be revealed to creditors by accident, but

the vast majority of management accounting data is kept confidential. This report contains

information on the opening and shutting of factories and retail locations, as well as changes in

management and speculations regarding new product introductions. For a variety of reasons,

predicting how qualitative information may effect a creditor's image of a firm can be challenging.

Accepting that some impact may occur and being forthright with other parties in the event that

adverse quality information is made public may be in the best interests of the property's owner.

Issues that Impact Quality Issues that Impact Product Quality

It is common for the quantitative parts of business analysis to fall short when it comes to the process

of completing business analysis. In addition, according to CPA Ireland, difficulties with product or

service quality might arise as a result of qualitative management accounting concerns. In firms that

are logically attempting to reduce expenditures, it is important not to sacrifice the long-term value of

being associated with high-quality goods and services for the short-term quantitative benefit of cost-

cutting. Obtaining denim that is thinner and less costly for the fabrication of jeans, for example, may

be possible for a garment manufacturer to achieve. When purchasers become aware of the

company's association with lower-quality items, it has the potential to harm the company's brand.

5 | P a g e

should accept the contract to manufacture Seville marmalade with Champagne since it will earn a

profit of €8,100 if the contract is accepted.

C.

External Reputation

Management accounting choices have a direct impact on how a small firm is seen by the general

public. In many circumstances, quantitative analysis may assist in narrowing down the options when

faced with a decision between two possibilities. However, this kind of study does not always take

into account all of the factors that are present in a particular case. For example, the assembly of

electronic components may be outsourced to a third-party manufacturing company. The research did

not evaluate the impact on consumers of the company's choice to shift its headquarters to a location

outside of the United States, even though future income statements indicate an increase in

profitability.

Labor Relations

Almost every quantitative study will indicate that spending less on personnel results in higher profit

margins. Despite the fact that it is possible that this is a mistake, quantitative decision-making

criteria are seldom employed in labor relations. When it comes to conserving money, organizations

may elect to remove an annual Christmas bonus that they have paid out for the previous 20 years.

Employees may see this as harsh or insensitive, despite the fact that it would surely save money.

Other techniques of cost-cutting are available to small-business owners as well. It's possible that it

would be preferable to reduce yearly pay increases by a few percentage points, or perhaps eliminate

the bonus entirely.

Creditor Effects

Some qualitative facts about a company's operations may be revealed to creditors by accident, but

the vast majority of management accounting data is kept confidential. This report contains

information on the opening and shutting of factories and retail locations, as well as changes in

management and speculations regarding new product introductions. For a variety of reasons,

predicting how qualitative information may effect a creditor's image of a firm can be challenging.

Accepting that some impact may occur and being forthright with other parties in the event that

adverse quality information is made public may be in the best interests of the property's owner.

Issues that Impact Quality Issues that Impact Product Quality

It is common for the quantitative parts of business analysis to fall short when it comes to the process

of completing business analysis. In addition, according to CPA Ireland, difficulties with product or

service quality might arise as a result of qualitative management accounting concerns. In firms that

are logically attempting to reduce expenditures, it is important not to sacrifice the long-term value of

being associated with high-quality goods and services for the short-term quantitative benefit of cost-

cutting. Obtaining denim that is thinner and less costly for the fabrication of jeans, for example, may

be possible for a garment manufacturer to achieve. When purchasers become aware of the

company's association with lower-quality items, it has the potential to harm the company's brand.

5 | P a g e

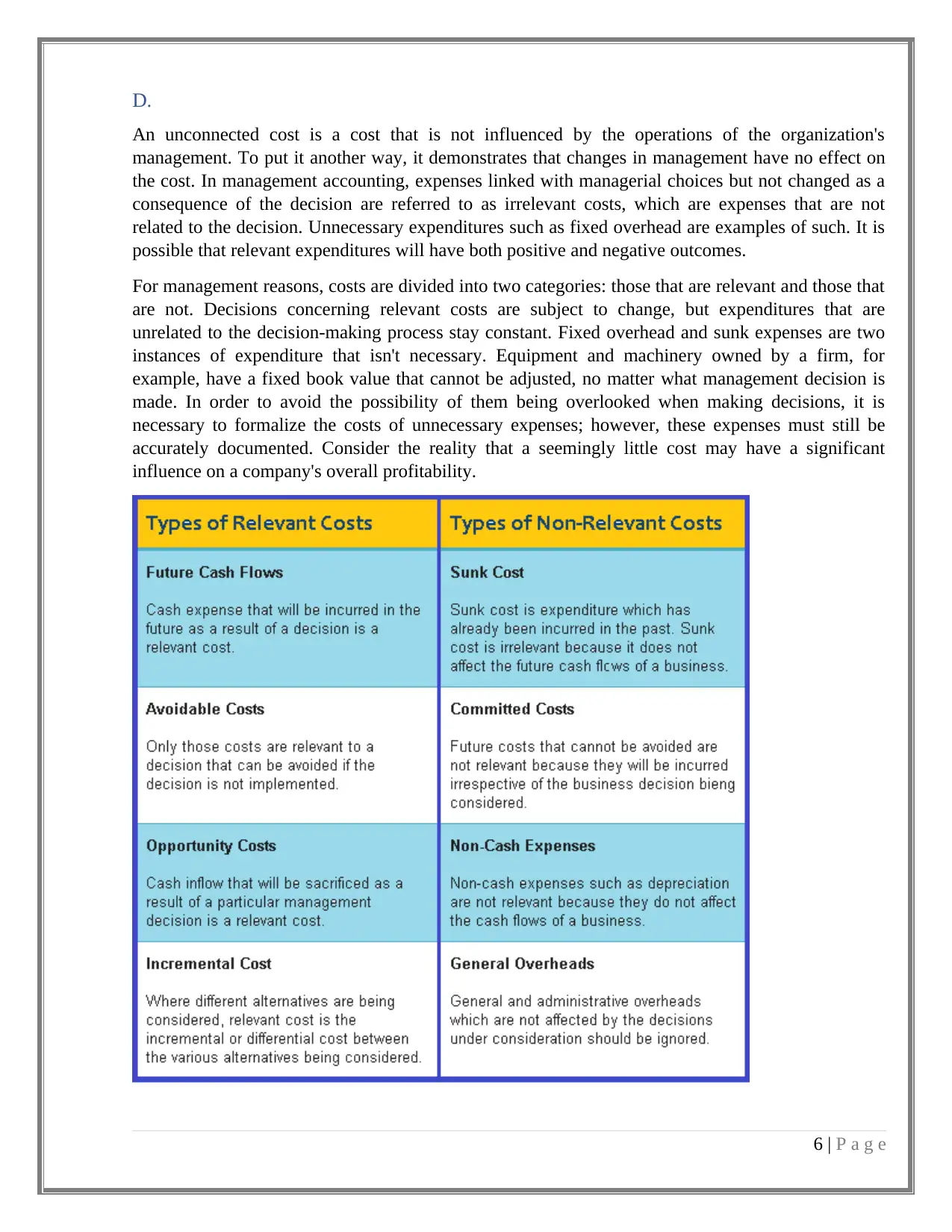

D.

An unconnected cost is a cost that is not influenced by the operations of the organization's

management. To put it another way, it demonstrates that changes in management have no effect on

the cost. In management accounting, expenses linked with managerial choices but not changed as a

consequence of the decision are referred to as irrelevant costs, which are expenses that are not

related to the decision. Unnecessary expenditures such as fixed overhead are examples of such. It is

possible that relevant expenditures will have both positive and negative outcomes.

For management reasons, costs are divided into two categories: those that are relevant and those that

are not. Decisions concerning relevant costs are subject to change, but expenditures that are

unrelated to the decision-making process stay constant. Fixed overhead and sunk expenses are two

instances of expenditure that isn't necessary. Equipment and machinery owned by a firm, for

example, have a fixed book value that cannot be adjusted, no matter what management decision is

made. In order to avoid the possibility of them being overlooked when making decisions, it is

necessary to formalize the costs of unnecessary expenses; however, these expenses must still be

accurately documented. Consider the reality that a seemingly little cost may have a significant

influence on a company's overall profitability.

6 | P a g e

An unconnected cost is a cost that is not influenced by the operations of the organization's

management. To put it another way, it demonstrates that changes in management have no effect on

the cost. In management accounting, expenses linked with managerial choices but not changed as a

consequence of the decision are referred to as irrelevant costs, which are expenses that are not

related to the decision. Unnecessary expenditures such as fixed overhead are examples of such. It is

possible that relevant expenditures will have both positive and negative outcomes.

For management reasons, costs are divided into two categories: those that are relevant and those that

are not. Decisions concerning relevant costs are subject to change, but expenditures that are

unrelated to the decision-making process stay constant. Fixed overhead and sunk expenses are two

instances of expenditure that isn't necessary. Equipment and machinery owned by a firm, for

example, have a fixed book value that cannot be adjusted, no matter what management decision is

made. In order to avoid the possibility of them being overlooked when making decisions, it is

necessary to formalize the costs of unnecessary expenses; however, these expenses must still be

accurately documented. Consider the reality that a seemingly little cost may have a significant

influence on a company's overall profitability.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Relevant costs: A variety of factors will be assessed and taken into account when selecting the best

future course for the firm. Since it is a price that may be required depending on the way employed to

attain the goal, incentives tax is a substantial charge, believes that the level of production generated

by your firm over the next 12 months will enable him to gain more money from you.

Irrelevant (or Sunk) spending is defined as follows: To begin, it's crucial to understand that after a

project has been agreed on and money has been spent on it, sunk costs are no longer considered.

Research and feasibility studies, on the other hand, are regarded sunk expenses, regardless of

whether or not the study is successful.

Suppose your manager asks you to be more aggressive in recruiting new staff the next week, and

you agree.

Summary – Relevant Cost vs Irrelevant Cost

The distinction between relevant and irrelevant charges is determined by whether or not a new

business choice will result in an increase or an extra payment. Choosing to go with a new option for

a highly complicated and large-scale organization may be tough since it is difficult to determine the

amount to which particular expenditures will effect the firm. When assessing whether or not a new

option is preferable, the usage of relevant and irrelevant expenditures becomes critical in these

cases.

7 | P a g e

future course for the firm. Since it is a price that may be required depending on the way employed to

attain the goal, incentives tax is a substantial charge, believes that the level of production generated

by your firm over the next 12 months will enable him to gain more money from you.

Irrelevant (or Sunk) spending is defined as follows: To begin, it's crucial to understand that after a

project has been agreed on and money has been spent on it, sunk costs are no longer considered.

Research and feasibility studies, on the other hand, are regarded sunk expenses, regardless of

whether or not the study is successful.

Suppose your manager asks you to be more aggressive in recruiting new staff the next week, and

you agree.

Summary – Relevant Cost vs Irrelevant Cost

The distinction between relevant and irrelevant charges is determined by whether or not a new

business choice will result in an increase or an extra payment. Choosing to go with a new option for

a highly complicated and large-scale organization may be tough since it is difficult to determine the

amount to which particular expenditures will effect the firm. When assessing whether or not a new

option is preferable, the usage of relevant and irrelevant expenditures becomes critical in these

cases.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Reference

Dili (2017). Difference Between Relevant and Irrelevant Cost. [online]

DifferenceBetween.com. Available at: https://www.differencebetween.com/difference-

between-relevant-and-vs-irrelevant-cost/.

accountingverse.com. (n.d.). Relevant Costing - Accountingverse. [online] Available at:

https://www.accountingverse.com/managerial-accounting/relevant-costing/ [Accessed 30

Apr. 2022].

Quora. (2021). What are the qualitative and quantitative decision making tools? [online]

Available at: https://www.quora.com/What-are-the-qualitative-and-quantitative-decision-

making-tools [Accessed 30 Apr. 2022].

Graybeal, P., Franklin, M. and Cooper, D. (2018). Identify Relevant Information for

Decision-Making. [online] opentextbc.ca. Available at:

https://opentextbc.ca/principlesofaccountingv2openstax/chapter/identify-relevant-

information-for-decision-making/.

Anon, (n.d.). Make or Buy Decision | Explanation with Solved Example | Factors. [online]

Available at: https://www.financialaccountancy.org/marginal-costing/make-or-buy-decision/.

Caili, T. and Singapore, A. (2017). BEHAVIORAL ASPECTS OF

BUDGETING. International Journal of Development Research, [online] 07, pp.16318–

16322. Available at: https://www.journalijdr.com/sites/default/files/issue-pdf/10684.pdf.

Bar-Haim Aviad 2002. Participation Programs in Work Organizations: past, present and

scenarios for the future, 1st edition, Greenwood Publishing Group Inc., Westport,

Connecticut.

Bonner E. Sarah. 2008. Judgment and Decision Making in Accounting, Pearson Education

Inc., Upper Saddle River, New Jersey.

8 | P a g e

Dili (2017). Difference Between Relevant and Irrelevant Cost. [online]

DifferenceBetween.com. Available at: https://www.differencebetween.com/difference-

between-relevant-and-vs-irrelevant-cost/.

accountingverse.com. (n.d.). Relevant Costing - Accountingverse. [online] Available at:

https://www.accountingverse.com/managerial-accounting/relevant-costing/ [Accessed 30

Apr. 2022].

Quora. (2021). What are the qualitative and quantitative decision making tools? [online]

Available at: https://www.quora.com/What-are-the-qualitative-and-quantitative-decision-

making-tools [Accessed 30 Apr. 2022].

Graybeal, P., Franklin, M. and Cooper, D. (2018). Identify Relevant Information for

Decision-Making. [online] opentextbc.ca. Available at:

https://opentextbc.ca/principlesofaccountingv2openstax/chapter/identify-relevant-

information-for-decision-making/.

Anon, (n.d.). Make or Buy Decision | Explanation with Solved Example | Factors. [online]

Available at: https://www.financialaccountancy.org/marginal-costing/make-or-buy-decision/.

Caili, T. and Singapore, A. (2017). BEHAVIORAL ASPECTS OF

BUDGETING. International Journal of Development Research, [online] 07, pp.16318–

16322. Available at: https://www.journalijdr.com/sites/default/files/issue-pdf/10684.pdf.

Bar-Haim Aviad 2002. Participation Programs in Work Organizations: past, present and

scenarios for the future, 1st edition, Greenwood Publishing Group Inc., Westport,

Connecticut.

Bonner E. Sarah. 2008. Judgment and Decision Making in Accounting, Pearson Education

Inc., Upper Saddle River, New Jersey.

8 | P a g e

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.