Budgeting Report: Types, Benefits, and Investment Risk Analysis

VerifiedAdded on 2023/04/21

|13

|2943

|130

Report

AI Summary

This report provides a comprehensive overview of budgeting, examining its core concepts, objectives, and the steps involved in the budgeting process. It delves into the advantages and disadvantages of budgeting, highlighting its role in financial planning, expenditure control, and resource allocation while also acknowledging its limitations. The report further explores various types of budgets, including sales, production, capital, operating, and master budgets, detailing their key characteristics and functions within an organization. A significant portion of the report is dedicated to illustrating how budgeting minimizes investment risks by providing a clear understanding of financial situations and enabling informed decision-making. The report emphasizes the importance of budgeting in forecasting, coordinating activities, and fostering financial stability within organizations. This report aims to educate and inform the reader about the importance of budgeting.

Running head: BUDGETING

BUDGETING

Name of the student

Name of the university

Author note

BUDGETING

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1BUDGETING

Executive Summary

Budgeting is identified as one of the major approach for the corporate organisations to

evaluate its financial situation. In this regard, the purpose of this report is to discuss and

highlight different aspects of the budget and facilitates better understanding of different

attributes of budget in terms of the advantages and disadvantages of the budget in an

organisation. Moreover, there are also different types of budgets and its key characteristics

are also illustrated in course of the discussion. Further, the discussion also cares to develop a

perception regarding the role of budget in reducing the risks in investments.

Executive Summary

Budgeting is identified as one of the major approach for the corporate organisations to

evaluate its financial situation. In this regard, the purpose of this report is to discuss and

highlight different aspects of the budget and facilitates better understanding of different

attributes of budget in terms of the advantages and disadvantages of the budget in an

organisation. Moreover, there are also different types of budgets and its key characteristics

are also illustrated in course of the discussion. Further, the discussion also cares to develop a

perception regarding the role of budget in reducing the risks in investments.

2BUDGETING

Table of Contents

Introduction................................................................................................................................4

Objectives of budgeting.............................................................................................................4

Steps involved in budgeting.......................................................................................................5

Benefits and limitations of budgeting........................................................................................7

Discuss the different types of budgets.......................................................................................9

Sales budget...........................................................................................................................9

Production budget..................................................................................................................9

Capital budget........................................................................................................................9

Operating budget..................................................................................................................10

Master budget.......................................................................................................................10

How budgeting minimizes risk in investments........................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Introduction................................................................................................................................4

Objectives of budgeting.............................................................................................................4

Steps involved in budgeting.......................................................................................................5

Benefits and limitations of budgeting........................................................................................7

Discuss the different types of budgets.......................................................................................9

Sales budget...........................................................................................................................9

Production budget..................................................................................................................9

Capital budget........................................................................................................................9

Operating budget..................................................................................................................10

Master budget.......................................................................................................................10

How budgeting minimizes risk in investments........................................................................10

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3BUDGETING

Introduction

This report has aimed to evaluate and highlight the different aspect of budgeting. The

report will describe the main purpose and objective of performing budgeting. It will also

describe in detail the steps involved in developing a budget. The different advantages and

disadvantages of forming a budget will also be described along with the diverse types of

budget. The process of risk minimization by using budgeting will also be highlighted.

Budgeting is the process of operating, designing and implementing budgets. This is a

managerial process consisting of budget control, preparation, planning and other related

processes. It is used in majority of the managerial policies consisting of cash flow, project

management, capital expenditure and long-range planning.

Objectives of budgeting

The overall purpose of budgeting is to strategize the diverse stages of operation in

business. It also makes sure that there is effective control over all the organizational activities

and coordinate the diverse activities in the departments (Vlaicu et al., 2014). In order to

achieve the above mentioned purposes of budgeting, followings objectives are developed to

fulfill the budget aims:

To predict the future expenses, production cost and sales in order to reach the optimal

amount of sales based by minimizing the chances of losses in business

To forestall the future financial needs and condition of the organization so that

necessary funds can be employed to maintain solvency of the firm

To analyze and develop the composition of the capitalization required so that funds

can be gathered at reasonable costs

To ensure that actions taken from different departments are coordinated so that

common objectives can be obtained

Introduction

This report has aimed to evaluate and highlight the different aspect of budgeting. The

report will describe the main purpose and objective of performing budgeting. It will also

describe in detail the steps involved in developing a budget. The different advantages and

disadvantages of forming a budget will also be described along with the diverse types of

budget. The process of risk minimization by using budgeting will also be highlighted.

Budgeting is the process of operating, designing and implementing budgets. This is a

managerial process consisting of budget control, preparation, planning and other related

processes. It is used in majority of the managerial policies consisting of cash flow, project

management, capital expenditure and long-range planning.

Objectives of budgeting

The overall purpose of budgeting is to strategize the diverse stages of operation in

business. It also makes sure that there is effective control over all the organizational activities

and coordinate the diverse activities in the departments (Vlaicu et al., 2014). In order to

achieve the above mentioned purposes of budgeting, followings objectives are developed to

fulfill the budget aims:

To predict the future expenses, production cost and sales in order to reach the optimal

amount of sales based by minimizing the chances of losses in business

To forestall the future financial needs and condition of the organization so that

necessary funds can be employed to maintain solvency of the firm

To analyze and develop the composition of the capitalization required so that funds

can be gathered at reasonable costs

To ensure that actions taken from different departments are coordinated so that

common objectives can be obtained

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4BUDGETING

To hasten the efficiency of processes in diverse departments, cost centers and

divisions of the organization

To provide fixed responsibilities to all the departmental heads

To make sure that there is efficient control on inventory, sales and cash of the

business entity

To assist in developing centralized control by using effective budgetary systems

Steps involved in budgeting

The budgeting process initiates when they receive objectives of a new project for

upcoming years. The budget is prepared based on the objectives and the time table developed

by the top level of management. These act as a guideline for preparing budget for each of the

department in the industry. The initial step of budgeting is estimating the sales of the

organization as other activities of the business entity is dependent on the sales of the

organization (McNulty, 2015). This will require analysis of the current situation in the

market and projection of the position that the organization wants to stay in the market based

on the objective. This consists of evaluation of external and internal factors that would affect

the market position of the organization.

The marketing manager would then submit the sales estimate prepared to the budget

committee for approval. The budget consists of the top level of management that evaluates

the proposed budget keeping in mind the past results and the future recommendations made

by the analysts (Rossi, 2014). They would provide recommendations for making changes the

budget based on their evaluation. They can recommend a complete revision in the proposed

budget or slight alteration based on their evaluation. The approval and recommendation of

the budget committee is sent to the president of the business entity (Bas, 2014). The president

approves the budget which then officially becomes the sales budget. The sales budget

To hasten the efficiency of processes in diverse departments, cost centers and

divisions of the organization

To provide fixed responsibilities to all the departmental heads

To make sure that there is efficient control on inventory, sales and cash of the

business entity

To assist in developing centralized control by using effective budgetary systems

Steps involved in budgeting

The budgeting process initiates when they receive objectives of a new project for

upcoming years. The budget is prepared based on the objectives and the time table developed

by the top level of management. These act as a guideline for preparing budget for each of the

department in the industry. The initial step of budgeting is estimating the sales of the

organization as other activities of the business entity is dependent on the sales of the

organization (McNulty, 2015). This will require analysis of the current situation in the

market and projection of the position that the organization wants to stay in the market based

on the objective. This consists of evaluation of external and internal factors that would affect

the market position of the organization.

The marketing manager would then submit the sales estimate prepared to the budget

committee for approval. The budget consists of the top level of management that evaluates

the proposed budget keeping in mind the past results and the future recommendations made

by the analysts (Rossi, 2014). They would provide recommendations for making changes the

budget based on their evaluation. They can recommend a complete revision in the proposed

budget or slight alteration based on their evaluation. The approval and recommendation of

the budget committee is sent to the president of the business entity (Bas, 2014). The president

approves the budget which then officially becomes the sales budget. The sales budget

5BUDGETING

includes budget for expenses in distribution and selling which when combined provides the

estimate of the net sales revenue for the next year.

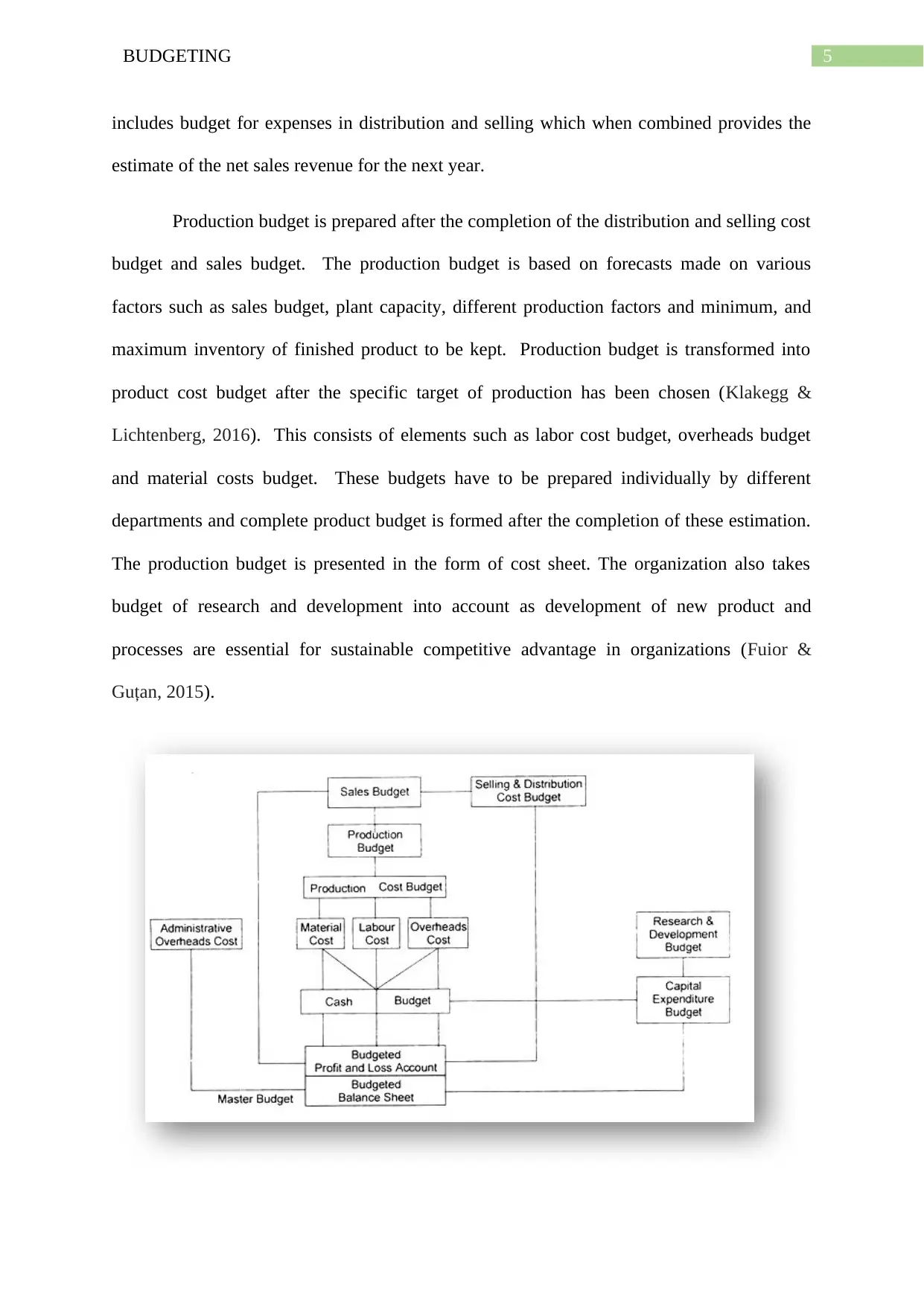

Production budget is prepared after the completion of the distribution and selling cost

budget and sales budget. The production budget is based on forecasts made on various

factors such as sales budget, plant capacity, different production factors and minimum, and

maximum inventory of finished product to be kept. Production budget is transformed into

product cost budget after the specific target of production has been chosen (Klakegg &

Lichtenberg, 2016). This consists of elements such as labor cost budget, overheads budget

and material costs budget. These budgets have to be prepared individually by different

departments and complete product budget is formed after the completion of these estimation.

The production budget is presented in the form of cost sheet. The organization also takes

budget of research and development into account as development of new product and

processes are essential for sustainable competitive advantage in organizations (Fuior &

Guțan, 2015).

includes budget for expenses in distribution and selling which when combined provides the

estimate of the net sales revenue for the next year.

Production budget is prepared after the completion of the distribution and selling cost

budget and sales budget. The production budget is based on forecasts made on various

factors such as sales budget, plant capacity, different production factors and minimum, and

maximum inventory of finished product to be kept. Production budget is transformed into

product cost budget after the specific target of production has been chosen (Klakegg &

Lichtenberg, 2016). This consists of elements such as labor cost budget, overheads budget

and material costs budget. These budgets have to be prepared individually by different

departments and complete product budget is formed after the completion of these estimation.

The production budget is presented in the form of cost sheet. The organization also takes

budget of research and development into account as development of new product and

processes are essential for sustainable competitive advantage in organizations (Fuior &

Guțan, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6BUDGETING

Figure 1: Budgeting Framework

Source: Created by the author

Benefits and limitations of budgeting

Budgeting is one of the key activities of different organization in each fiscal year

which promotes the effective use of resources to achieve the goals of the organization. The

major benefits of using budgeting are as follows:

The management is motivated and forced to make timely and early analysis of the

issues faced by the firm. This facilitates in developing a sense of care and causation

among the managers which assists in effective decision making (Dudin et al., 2015).

It also facilitates in controlling expenditure and income

It is used as a tool for testing and evaluating managerial goals and policies which

forms the guidelines for carrying out different activities within the organization

It also assists in leading resources and capital to the channels that is most profitable

for the business entity (Asogwa & Etim, 2017).

The management can easily decentralize responsibilities by using budgeting and at

the same time keep an effective control over the system. The deviations,

inefficiencies and weaknesses can easily be identified and corrected so that goals can

be achieved in a timely manner

It facilitates in developing norms and scales for effective measurement of

performances of individuals and departments in firms. Managers can also improve

their own decisions and performance by setting benchmarks based on the budget

Cost consciousness is a mindset effectively developed using budgeting which

stimulates effective use of organizational resources and develops profit-mindedness in

the organization. This emphasizes on effective spending to achieve the set goals

Figure 1: Budgeting Framework

Source: Created by the author

Benefits and limitations of budgeting

Budgeting is one of the key activities of different organization in each fiscal year

which promotes the effective use of resources to achieve the goals of the organization. The

major benefits of using budgeting are as follows:

The management is motivated and forced to make timely and early analysis of the

issues faced by the firm. This facilitates in developing a sense of care and causation

among the managers which assists in effective decision making (Dudin et al., 2015).

It also facilitates in controlling expenditure and income

It is used as a tool for testing and evaluating managerial goals and policies which

forms the guidelines for carrying out different activities within the organization

It also assists in leading resources and capital to the channels that is most profitable

for the business entity (Asogwa & Etim, 2017).

The management can easily decentralize responsibilities by using budgeting and at

the same time keep an effective control over the system. The deviations,

inefficiencies and weaknesses can easily be identified and corrected so that goals can

be achieved in a timely manner

It facilitates in developing norms and scales for effective measurement of

performances of individuals and departments in firms. Managers can also improve

their own decisions and performance by setting benchmarks based on the budget

Cost consciousness is a mindset effectively developed using budgeting which

stimulates effective use of organizational resources and develops profit-mindedness in

the organization. This emphasizes on effective spending to achieve the set goals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7BUDGETING

It also facilitates in developing competition, perform effectively and sense of purpose

to the individuals working in the organization. This improves the overall productivity

and output of the employees

It also assists in developing systematic approach to solving problems within

organizations

It also facilitates in effective management to waste and stability to all aspects in

organizational processes

Even though there are multiple advantages of using budgeting but there are certain

limitations which needs to be considered while developing the budget and they are as

follows:

Forecasting, budgeting and planning is based on assumptions, judgment and

approximations which is not fully accurate. Budget is only a process of estimation so

precise forecasting is not possible as it is not a scientific method

The management and its members needs to cooperate and participate effectively as

the utility and success depends on it. This means that efforts need to be directed based

on the plan and cooperation of the top management to achieve success. The process of

budgeting fails multiple times due to the faulty execution from the executive

management team (Shaw, 2016).

Budgeting process is time consuming in nature and as it is based on estimation, often

budgets does not fulfill the expectation of the internal stakeholders. This results in

conflict within the organization. In order to develop an effective budget program it is

crucial to comprehend the objective, essentials and philosophy of the organization

Companies emphasizing on budgeting too much will result in bucking of the system

due to the inappropriate estimates of future revenue and costs (Shaw, 2016).

It also facilitates in developing competition, perform effectively and sense of purpose

to the individuals working in the organization. This improves the overall productivity

and output of the employees

It also assists in developing systematic approach to solving problems within

organizations

It also facilitates in effective management to waste and stability to all aspects in

organizational processes

Even though there are multiple advantages of using budgeting but there are certain

limitations which needs to be considered while developing the budget and they are as

follows:

Forecasting, budgeting and planning is based on assumptions, judgment and

approximations which is not fully accurate. Budget is only a process of estimation so

precise forecasting is not possible as it is not a scientific method

The management and its members needs to cooperate and participate effectively as

the utility and success depends on it. This means that efforts need to be directed based

on the plan and cooperation of the top management to achieve success. The process of

budgeting fails multiple times due to the faulty execution from the executive

management team (Shaw, 2016).

Budgeting process is time consuming in nature and as it is based on estimation, often

budgets does not fulfill the expectation of the internal stakeholders. This results in

conflict within the organization. In order to develop an effective budget program it is

crucial to comprehend the objective, essentials and philosophy of the organization

Companies emphasizing on budgeting too much will result in bucking of the system

due to the inappropriate estimates of future revenue and costs (Shaw, 2016).

8BUDGETING

Discuss the different types of budgets

Sales budget

Sales budget is referred as the estimation of sales by the management for a financial

period. The futuristic feature of the sales budget makes it more effective to set goals for the

business departments and forecasting the earnings and product requirements. From that point

of view, it can be argued that the sales budget provides a strategic advantage to the business

orientation of a company by estimating the expenses and managing profits effectively

(Mohamad & Karbhari, 2016).

Production budget

The concept of production budget is associated with a financial plan that comprised of

number of units in a single period of time. In this regard, the purpose of the managers is to

estimate the way units will be requires in a production process accompanied with the time

and scheduling. As a matter of fact, the managers intends to make a budget estimation based

on the estimated sales number in future (Nakata et al., 2015). However, the costs will not be

shown in the production budget. Instead, the number of production units are incorporated into

the production budget.

Capital budget

As far as the capital budget is concerned, it can be stated that there are the capital

receipts and payments that are identified as the capital budget. The capital receipts can be

identified as loans raised by the government for the public whereas the capital payments are

resembled with the perception of capital expenditure on assets like land, buildings, equipment

Discuss the different types of budgets

Sales budget

Sales budget is referred as the estimation of sales by the management for a financial

period. The futuristic feature of the sales budget makes it more effective to set goals for the

business departments and forecasting the earnings and product requirements. From that point

of view, it can be argued that the sales budget provides a strategic advantage to the business

orientation of a company by estimating the expenses and managing profits effectively

(Mohamad & Karbhari, 2016).

Production budget

The concept of production budget is associated with a financial plan that comprised of

number of units in a single period of time. In this regard, the purpose of the managers is to

estimate the way units will be requires in a production process accompanied with the time

and scheduling. As a matter of fact, the managers intends to make a budget estimation based

on the estimated sales number in future (Nakata et al., 2015). However, the costs will not be

shown in the production budget. Instead, the number of production units are incorporated into

the production budget.

Capital budget

As far as the capital budget is concerned, it can be stated that there are the capital

receipts and payments that are identified as the capital budget. The capital receipts can be

identified as loans raised by the government for the public whereas the capital payments are

resembled with the perception of capital expenditure on assets like land, buildings, equipment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9BUDGETING

and machinery (Ogujiuba & Ehigiamusoe, 2014). Moreover, it can be argued that the role of

the capital budget is to portray the financial transactions in the public accounts.

Operating budget

It can be argued that the operating budget is a detailed projection of the overall

income and expenses on the basis of the sales revenue. However, it is important to know that

the operating budget is relied on a given period of time and includes the sub-budgets, sales

budget. Moreover, it is associated with the goals and objectives of a company and dedicated

to facilitate strategic advantage for the organisation in course of the progress in business.

Master budget

As far as the master budget is concerned, the components of future sales, purchases,

future expenses, production levels and the capital investments are considered to be the part of

the master budget. It is also identified as an expensive business strategy in association with

the income statement and the balance sheet as well (Cox, 2014). It is generally presented in a

monthly or yearly basis and covers the entire fiscal year of a company.

How budgeting minimizes risk in investments

It can be stated that there is a direct correlation between budget and financial

investment. Based on the empirical studies it can be stated that the primary task of the budget

is to highlight the real case scenario of the financial situation for an individual or a company.

As a result of that it becomes a core competency of the budgeting to illustrate the achievable

objectives and goals. As a matter of fact, it can be stated that there are income and expense

overview of the company or an individual that facilitate a better understanding of different

investment techniques and possibilities resembled with the financial condition. Moreover,

one of the major factors of budgeting is to highlight the financial matters and possibilities of

further investment. Therefore, having a clear understanding about different aspects of the

and machinery (Ogujiuba & Ehigiamusoe, 2014). Moreover, it can be argued that the role of

the capital budget is to portray the financial transactions in the public accounts.

Operating budget

It can be argued that the operating budget is a detailed projection of the overall

income and expenses on the basis of the sales revenue. However, it is important to know that

the operating budget is relied on a given period of time and includes the sub-budgets, sales

budget. Moreover, it is associated with the goals and objectives of a company and dedicated

to facilitate strategic advantage for the organisation in course of the progress in business.

Master budget

As far as the master budget is concerned, the components of future sales, purchases,

future expenses, production levels and the capital investments are considered to be the part of

the master budget. It is also identified as an expensive business strategy in association with

the income statement and the balance sheet as well (Cox, 2014). It is generally presented in a

monthly or yearly basis and covers the entire fiscal year of a company.

How budgeting minimizes risk in investments

It can be stated that there is a direct correlation between budget and financial

investment. Based on the empirical studies it can be stated that the primary task of the budget

is to highlight the real case scenario of the financial situation for an individual or a company.

As a result of that it becomes a core competency of the budgeting to illustrate the achievable

objectives and goals. As a matter of fact, it can be stated that there are income and expense

overview of the company or an individual that facilitate a better understanding of different

investment techniques and possibilities resembled with the financial condition. Moreover,

one of the major factors of budgeting is to highlight the financial matters and possibilities of

further investment. Therefore, having a clear understanding about different aspects of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10BUDGETING

financial details provides a strategic advantage for the organisation to measure and set its

investments. In addition to this, it can be seen that there is always a risk in procuring big

investments because the organisation does not have clear idea about the market fluctuation.

They can only anticipate the possible outcome of the market. However, the role of budget in

this process is to deliver a better framework for the organisation in accordance with the

financial situation of the organisation. It may also include the loss and gain for the

organisation so that the company can maneuver its investment.

Conclusion

Based on the above discussion, it can be argued that the report tries to put emphasis

on different aspects and attributes of the budget for a corporate organisation. In this regard,

the objectives and investment risk reducing practices are incorporated into the discussion.

Moreover, the report also discusses different steps of budget that can formulate an effective

and efficient budget for the organisation. In addition to this, various types of budget are

taking into the discussion with the purpose to highlight distinctive purposes and objectives of

budgeting. The advantages and disadvantages of budgeting signifies the competencies and

drawbacks that a budget can create in the business orientation of an organisation. From that

point of view, it can be argued that the report is highly relevant and contextual.

financial details provides a strategic advantage for the organisation to measure and set its

investments. In addition to this, it can be seen that there is always a risk in procuring big

investments because the organisation does not have clear idea about the market fluctuation.

They can only anticipate the possible outcome of the market. However, the role of budget in

this process is to deliver a better framework for the organisation in accordance with the

financial situation of the organisation. It may also include the loss and gain for the

organisation so that the company can maneuver its investment.

Conclusion

Based on the above discussion, it can be argued that the report tries to put emphasis

on different aspects and attributes of the budget for a corporate organisation. In this regard,

the objectives and investment risk reducing practices are incorporated into the discussion.

Moreover, the report also discusses different steps of budget that can formulate an effective

and efficient budget for the organisation. In addition to this, various types of budget are

taking into the discussion with the purpose to highlight distinctive purposes and objectives of

budgeting. The advantages and disadvantages of budgeting signifies the competencies and

drawbacks that a budget can create in the business orientation of an organisation. From that

point of view, it can be argued that the report is highly relevant and contextual.

11BUDGETING

Reference

Asogwa, I. E., & Etim, O. E. (2017). Traditional Budgeting in Today's Business

Environment. Journal of Applied Finance and Banking, 7(3), 111.

Bas, E. (2014). An integrated quality function deployment and capital budgeting

methodology for occupational safety and health as a systems thinking approach: The

case of the construction industry. Accident Analysis & Prevention, 68, 42-56.

Cox, P. (2014). Master budget project: analysis of cash budget report. Strategic

Finance, 19(3), 52-54.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S., & Namitulina, A. (2015). The innovative

business model canvas in the system of effective budgeting. Asian Social

Science, 11(7), 290-296.

Fuior, E., & GUȚAN, V. (2015). The Budgeting based on the Performance: Conceptual

Framework and Implementation Details. Economy Transdisciplinarity

Cognition, 18(1).

Klakegg, O. J., & Lichtenberg, S. (2016). Successive cost estimation–successful budgeting of

major projects. Procedia-Social and Behavioral Sciences, 226, 176-183.

McNulty, S. L. (2015). Barriers to participation: Exploring gender in Peru’s participatory

budget process. The Journal of Development Studies, 51(11), 1429-1443.

Mohamad, M. H. S., & Karbhari, Y. (2016). The NPFM in emerging economies: The

modified budgeting system (mbs) in malaysian government. Indonesian Management

and Accounting Research (IMAR), 9(1), 1-26.

Reference

Asogwa, I. E., & Etim, O. E. (2017). Traditional Budgeting in Today's Business

Environment. Journal of Applied Finance and Banking, 7(3), 111.

Bas, E. (2014). An integrated quality function deployment and capital budgeting

methodology for occupational safety and health as a systems thinking approach: The

case of the construction industry. Accident Analysis & Prevention, 68, 42-56.

Cox, P. (2014). Master budget project: analysis of cash budget report. Strategic

Finance, 19(3), 52-54.

Dudin, M., Kucuri, G., Fedorova, I., Dzusova, S., & Namitulina, A. (2015). The innovative

business model canvas in the system of effective budgeting. Asian Social

Science, 11(7), 290-296.

Fuior, E., & GUȚAN, V. (2015). The Budgeting based on the Performance: Conceptual

Framework and Implementation Details. Economy Transdisciplinarity

Cognition, 18(1).

Klakegg, O. J., & Lichtenberg, S. (2016). Successive cost estimation–successful budgeting of

major projects. Procedia-Social and Behavioral Sciences, 226, 176-183.

McNulty, S. L. (2015). Barriers to participation: Exploring gender in Peru’s participatory

budget process. The Journal of Development Studies, 51(11), 1429-1443.

Mohamad, M. H. S., & Karbhari, Y. (2016). The NPFM in emerging economies: The

modified budgeting system (mbs) in malaysian government. Indonesian Management

and Accounting Research (IMAR), 9(1), 1-26.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.