Business Finance Report: Budgeting Methods, Applications and Analysis

VerifiedAdded on 2020/12/09

|12

|3997

|339

Report

AI Summary

This report delves into the realm of business finance, focusing on the purpose and process of budgeting within an organization. It begins by defining budgeting and its significance in financial operations, emphasizing its role in planning, control, and long-term strategy. The report then outlines the budgeting process, including strategic planning, goal setting, revenue projections, cost analysis, and budget review. Part 1 further examines traditional budgeting approaches, including incremental budgeting, and evaluates its applications, such as providing a concrete framework, encouraging decentralization, and impacting organizational culture. Part 2 then introduces alternative budgeting methods, such as rolling budgets and zero-based budgeting, along with their applications. The report concludes by evaluating the suitability of different methods for future business operations, providing a comprehensive analysis of budgeting strategies for effective financial management. The report is designed to provide insights on budgeting methods, applications and analysis.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1. Purpose and process of budgeting ..........................................................................................3

2. Application of traditional budgeting approach.......................................................................5

3. Is Traditional Budget System Is Appropriate For Future Business Operations......................6

PART 2............................................................................................................................................7

4 Different Budgeting Methods..................................................................................................7

5 Application Different Budgeting Method................................................................................8

6. Evaluate which method is appropriate for the company.........................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

PART 1............................................................................................................................................3

1. Purpose and process of budgeting ..........................................................................................3

2. Application of traditional budgeting approach.......................................................................5

3. Is Traditional Budget System Is Appropriate For Future Business Operations......................6

PART 2............................................................................................................................................7

4 Different Budgeting Methods..................................................................................................7

5 Application Different Budgeting Method................................................................................8

6. Evaluate which method is appropriate for the company.........................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Business finance means cash and credit score employed within the organisation. Thus, it's

miles required to buy property, products, raw materials and for the alternative drift of financial

operations. A budget is a formal declaration of expected profits and fees based on destiny plans

and targets. Thus, a price range is a record that administration makes to evaluate the income and

costs for an upcoming duration based on their objectives for the commercial enterprise.

However, the report will highlight the purpose of budgeting and along with that it will outline the

process of budgeting that will be followed by the company (Ylhäinen, 2017). Further, the

assignment will frame the application of traditional budgeting along with that it will comment on

the incremental budgeting which is inclusive of concrete framework, decentralization,

organisational culture etc. Moreover, the report will outline about the different budgeting

methods which is inclusive of rolling budgets, zero-based budgeting and activity based

budgeting. On the other hand, the project will comment on the applications of the above

mentioned method and along with that it will comment on the two methods which are

appropriate for the future operations of the company.

PART 1

1. Purpose and process of budgeting

Budgeting is a method of framing, enforcing and operating budgets. Thus, it's miles the

managerial procedure of planning the budget and implementing them, controlling of expenses

and the related techniques. Budgeting is the advanced level of accountancy for considering the

future context which suggests a precise direction of movement and no longer simply reporting.

Therefore, it is a fundamental part of such managerial guidelines for long term planning, cash

flow, capital outlay and project implementation.

Purpose

The general purpose of budgeting of snappy drinks is to plot specific levels of business

operations, arrange tasks of different sections of the company and to make certain effective

control over it. Further, budget helps to anticipate the company’s future income, production price

and other costs good to earn preferred amount of earnings and decrease the chance of losses.

Moreover, its purpose is to assume the company’s future monetary condition and future need for

budget to be hired in the enterprise which will keeping the company solvent (Bogsnes, 2016).

Business finance means cash and credit score employed within the organisation. Thus, it's

miles required to buy property, products, raw materials and for the alternative drift of financial

operations. A budget is a formal declaration of expected profits and fees based on destiny plans

and targets. Thus, a price range is a record that administration makes to evaluate the income and

costs for an upcoming duration based on their objectives for the commercial enterprise.

However, the report will highlight the purpose of budgeting and along with that it will outline the

process of budgeting that will be followed by the company (Ylhäinen, 2017). Further, the

assignment will frame the application of traditional budgeting along with that it will comment on

the incremental budgeting which is inclusive of concrete framework, decentralization,

organisational culture etc. Moreover, the report will outline about the different budgeting

methods which is inclusive of rolling budgets, zero-based budgeting and activity based

budgeting. On the other hand, the project will comment on the applications of the above

mentioned method and along with that it will comment on the two methods which are

appropriate for the future operations of the company.

PART 1

1. Purpose and process of budgeting

Budgeting is a method of framing, enforcing and operating budgets. Thus, it's miles the

managerial procedure of planning the budget and implementing them, controlling of expenses

and the related techniques. Budgeting is the advanced level of accountancy for considering the

future context which suggests a precise direction of movement and no longer simply reporting.

Therefore, it is a fundamental part of such managerial guidelines for long term planning, cash

flow, capital outlay and project implementation.

Purpose

The general purpose of budgeting of snappy drinks is to plot specific levels of business

operations, arrange tasks of different sections of the company and to make certain effective

control over it. Further, budget helps to anticipate the company’s future income, production price

and other costs good to earn preferred amount of earnings and decrease the chance of losses.

Moreover, its purpose is to assume the company’s future monetary condition and future need for

budget to be hired in the enterprise which will keeping the company solvent (Bogsnes, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, the motive of budgeting is to give a financial framework for the choice making

system i.e. the planned action that the company have got deliberate for or not. Moreover, in

managing a commercial enterprise responsibly, expenses have to be managed properly.

Process of Budgeting

Each company require making the budget in order to keep the track and control the

expenses. Thus, increasing and coping with a price range is how organizations allocate, monitor

and plan financial spending. Further, a proper budgeting structure is the basis for suitable

business control, development and enhancement. Thus, while preparing budget, discipline and

designing should be the basis of a commercial enterprise budgeting structure.

Strategic Plan: A Strategic Plan of the snappy drinks is how the enterprise plans to

accomplish its goals. Thus, the first step within the budgeting method is to prepare a strategic

plan (Wildavsky,2017). Hence, the strategic plan helps to make sure that organizational sources

are used to assist the approach and development of the company. It way budgeting towards the

vision.

Business Goals: snappy drinks need to develop their goals and there objectives to be

responsible for achieving their pre-decided objectives. Thus, that is usually the duty of the

management crew, board or business proprietor. However, the budget will help the company by

providing the financial assets to achieve their objectives. For instance, if the company has fully

grown its facility and there is a goal to develop more space, there desires to be dollar budgeted to

amplify or flow the business operations.

Revenue Projections: revenue anticipation must be based totally on historical economic

performance, as well as proposed boom earnings. However, the planned growth can be linked to

organizational objectives of the snappy drinks and deliberate tasks on the way to provoke

commercial enterprise growth (Miller,2018.).

Fixed and Variable Cost Projections: fixed costs projections is absolutely counted of

searching on the month-to-month predictable prices that do not get change. On the other hand,

variable costs changes on a monthly basis, supply costs etc. Thus, these costs should be properly

planned and managed of the snappy drinks .

system i.e. the planned action that the company have got deliberate for or not. Moreover, in

managing a commercial enterprise responsibly, expenses have to be managed properly.

Process of Budgeting

Each company require making the budget in order to keep the track and control the

expenses. Thus, increasing and coping with a price range is how organizations allocate, monitor

and plan financial spending. Further, a proper budgeting structure is the basis for suitable

business control, development and enhancement. Thus, while preparing budget, discipline and

designing should be the basis of a commercial enterprise budgeting structure.

Strategic Plan: A Strategic Plan of the snappy drinks is how the enterprise plans to

accomplish its goals. Thus, the first step within the budgeting method is to prepare a strategic

plan (Wildavsky,2017). Hence, the strategic plan helps to make sure that organizational sources

are used to assist the approach and development of the company. It way budgeting towards the

vision.

Business Goals: snappy drinks need to develop their goals and there objectives to be

responsible for achieving their pre-decided objectives. Thus, that is usually the duty of the

management crew, board or business proprietor. However, the budget will help the company by

providing the financial assets to achieve their objectives. For instance, if the company has fully

grown its facility and there is a goal to develop more space, there desires to be dollar budgeted to

amplify or flow the business operations.

Revenue Projections: revenue anticipation must be based totally on historical economic

performance, as well as proposed boom earnings. However, the planned growth can be linked to

organizational objectives of the snappy drinks and deliberate tasks on the way to provoke

commercial enterprise growth (Miller,2018.).

Fixed and Variable Cost Projections: fixed costs projections is absolutely counted of

searching on the month-to-month predictable prices that do not get change. On the other hand,

variable costs changes on a monthly basis, supply costs etc. Thus, these costs should be properly

planned and managed of the snappy drinks .

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Annual Goal Expenses: goal related initiatives have to also be given budgets. However,

each initiative ought to have projected fees related to the objectives. Further, that is where the

price of enforcing goals are integrated into the once a year budget. Moreover, Projections of

prices must be recognized, laid out and included into the departmental price range that is

accountable for finishing the intention.

Budget Review: At last after following all the above steps the snappy drinks should

overlook their budget in case they have missed out something, thus by reviewing they can

monitor whether their budget meeting their goals and objectives or not.

Thus, budgeting is the core component of successful implementation of business model

of the snappy drinks and with the help of budgeting process the company can plane their

expenditure and control the cost and expenses of the organisation (Dudin and et.al., 2015).

2. Application of traditional budgeting approach

Traditional Budgeting

A traditional budgeting is defined as a quantitative document and additive tool for an

action plan. However, it usually consists of objectives relating to cash flows, fees, revenues,

belongings, and liabilities for a specific duration. Further, a traditional finance is proposed by

including incremental quantities, along with inflation or preset will lead to increase in income

costs and prices, to present annual budget.

Moreover, traditional budgeting in snappy drinks is mostly executed with a top-down

technique as a result of a hierarchical outlook. Thus, this indicates, significant management

prepares a former price range in keeping with organisation’s method for all departments and then

sub-departments prepare budgets in line with their needs. For example, there is an XYZ ltd. who

prepares their finances through top- down approach. However, the management, to boom the

general profitability of the organisation sets a goal for sales crew to sell 12000 devices at a lower

rate for the 12 months. Moreover, the production unit does no longer have the capability to

produce 12000 gadgets in a year and this may results in a day after day conflicts between income

and production. Further, if the control could have taken inputs from the manufacturing unit too

this situation could now not have been rise up. however income group has if accomplished the

target, they may expect a raise or incentive for their order book even though the same became no

each initiative ought to have projected fees related to the objectives. Further, that is where the

price of enforcing goals are integrated into the once a year budget. Moreover, Projections of

prices must be recognized, laid out and included into the departmental price range that is

accountable for finishing the intention.

Budget Review: At last after following all the above steps the snappy drinks should

overlook their budget in case they have missed out something, thus by reviewing they can

monitor whether their budget meeting their goals and objectives or not.

Thus, budgeting is the core component of successful implementation of business model

of the snappy drinks and with the help of budgeting process the company can plane their

expenditure and control the cost and expenses of the organisation (Dudin and et.al., 2015).

2. Application of traditional budgeting approach

Traditional Budgeting

A traditional budgeting is defined as a quantitative document and additive tool for an

action plan. However, it usually consists of objectives relating to cash flows, fees, revenues,

belongings, and liabilities for a specific duration. Further, a traditional finance is proposed by

including incremental quantities, along with inflation or preset will lead to increase in income

costs and prices, to present annual budget.

Moreover, traditional budgeting in snappy drinks is mostly executed with a top-down

technique as a result of a hierarchical outlook. Thus, this indicates, significant management

prepares a former price range in keeping with organisation’s method for all departments and then

sub-departments prepare budgets in line with their needs. For example, there is an XYZ ltd. who

prepares their finances through top- down approach. However, the management, to boom the

general profitability of the organisation sets a goal for sales crew to sell 12000 devices at a lower

rate for the 12 months. Moreover, the production unit does no longer have the capability to

produce 12000 gadgets in a year and this may results in a day after day conflicts between income

and production. Further, if the control could have taken inputs from the manufacturing unit too

this situation could now not have been rise up. however income group has if accomplished the

target, they may expect a raise or incentive for their order book even though the same became no

longer introduced due to lower manufacturing. Thus, the management might also must bear this

price with none addition inside the top operations (Popesko and et.al., 2017).

Incremental Budgeting

However, Incremental budgeting is a budgeting method of the snappy drinks which is

based totally on moderate adjustments from the previous budgeted outcome or actual

consequences. Further, this is a basic method in corporations where management does not mean

to use up a huge amount of time in developing budgets, or wherein it does no longer understand

any incredible want to conduct an intensive re-evaluation of the commercial enterprise.

Therefore, this mind-set commonly takes place whilst there isn't always an extraordinary deal of

competition in an enterprise, so that earnings have a tendency to be uphold from yearly. For

instance, in an organisation overall remuneration paid to personnel in a particular 12 months is

500,000. while the budget is prepared for the following year the management issue that they

want 5 new personnel who might be paid 30,000 each and additionally an increment of 10 % to

present employees will be given. Consequently, in incremental budgeting the finances for

earnings could be 700,000 that means (500,000 + 10% raise to present personnel + (30,000*5

new employees recruited).

Applications of Traditional Budgeting

Gives A Concrete Framework: seeing that traditional budgeting is primarily based on a

reference factor that is the information points of the preceding year, it becomes convenient to

control the financial operations of the company. As an alternative, this reference factor lets in the

business enterprise to prepare their budget on a stable framework which is simple to implement

and easy to manage.

Encourages Decentralization: According to this application as anyone can look at the

previous years' expenditure and might decide upon the finances for next year, the idea turns into

decentralized and the pinnacle management doesn’t want to think about a way to budget for the

subsequent 12 months. Thus, as an end result, they can give attention to different excessive value

responsibilities (de Campos and Rodrigues, 2016).

Organizational Culture: for the reason that traditional budget is the simplistic method

of budgeting of snappy drinks, quickly it becomes a part of the organizational subculture and

always the approach goes continuously. Thus, if the brand new approach is introduced as an

instance zero-primarily based budgeting then it'd be a risky project for the enterprise.

price with none addition inside the top operations (Popesko and et.al., 2017).

Incremental Budgeting

However, Incremental budgeting is a budgeting method of the snappy drinks which is

based totally on moderate adjustments from the previous budgeted outcome or actual

consequences. Further, this is a basic method in corporations where management does not mean

to use up a huge amount of time in developing budgets, or wherein it does no longer understand

any incredible want to conduct an intensive re-evaluation of the commercial enterprise.

Therefore, this mind-set commonly takes place whilst there isn't always an extraordinary deal of

competition in an enterprise, so that earnings have a tendency to be uphold from yearly. For

instance, in an organisation overall remuneration paid to personnel in a particular 12 months is

500,000. while the budget is prepared for the following year the management issue that they

want 5 new personnel who might be paid 30,000 each and additionally an increment of 10 % to

present employees will be given. Consequently, in incremental budgeting the finances for

earnings could be 700,000 that means (500,000 + 10% raise to present personnel + (30,000*5

new employees recruited).

Applications of Traditional Budgeting

Gives A Concrete Framework: seeing that traditional budgeting is primarily based on a

reference factor that is the information points of the preceding year, it becomes convenient to

control the financial operations of the company. As an alternative, this reference factor lets in the

business enterprise to prepare their budget on a stable framework which is simple to implement

and easy to manage.

Encourages Decentralization: According to this application as anyone can look at the

previous years' expenditure and might decide upon the finances for next year, the idea turns into

decentralized and the pinnacle management doesn’t want to think about a way to budget for the

subsequent 12 months. Thus, as an end result, they can give attention to different excessive value

responsibilities (de Campos and Rodrigues, 2016).

Organizational Culture: for the reason that traditional budget is the simplistic method

of budgeting of snappy drinks, quickly it becomes a part of the organizational subculture and

always the approach goes continuously. Thus, if the brand new approach is introduced as an

instance zero-primarily based budgeting then it'd be a risky project for the enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Is Traditional Budget System Is Appropriate For Future Business Operations

From the above discussion it has been analysed that the traditional budget is made from all

financial factors of a corporation, from particular units to divisions and departments. Thus, it

represents a typical image of the business enterprise’s functional objectives and strategic

objectives.

Further, when higher management evaluates an organisation's overall financial objectives

and analyse the wants to projected sales for a year, it receives a clean image of the way a lot

money it is able to fairly allocate to distinct areas. Thus, this is some predominant benefits of the

traditional budgeting through which can plan their future operations. However, selections are

made approximately where budget will have the maximum effect and members of company are

given guiding on how to perform their activities. This method permits higher managers to

preserve whole financial control over a finance (Clark, Menifield and Stewart, 2018).

PART 2

4 Different Budgeting Methods

Rolling Budgets: A rolling budgeting method is always updated in order to include a

new finances period as the latest budget duration is completed. Consequently, the rolling

finances refer to the additive expansion of the prevailing price range model, thus, via doing so, a

business always has a price range that extends 365 into the future. Thus, a rolling price range

requires substantially greater management interest than is the case whilst an organization

develops a one-year static budget, for the reason that some budgeting tasks should now be

continual every month (Mahieu, Vroman and Calluy, 2015). Thus, this budget will improve

traditional budgeting method by providing the information of the latest budget facts of the

snappy drinks.

Moreover, This approach has the gain of having someone continuously attends to the

price range version and revise finances assumptions for the closing incremental period of the

finances. On the other hand, the disadvantage of this method is that it may now not yield a

finance which is extra workable than the conventional static price range, for the reason that

budgets durations preceding to the additive month just added are not altered.

Zero Based Budgeting: zero based budgeting is a technique that is used by the

companies for making plans and budgeting technique which calls for each manager to confirm

his entire finances request in detail from abrasion and transfers the encumbrance of proof to

From the above discussion it has been analysed that the traditional budget is made from all

financial factors of a corporation, from particular units to divisions and departments. Thus, it

represents a typical image of the business enterprise’s functional objectives and strategic

objectives.

Further, when higher management evaluates an organisation's overall financial objectives

and analyse the wants to projected sales for a year, it receives a clean image of the way a lot

money it is able to fairly allocate to distinct areas. Thus, this is some predominant benefits of the

traditional budgeting through which can plan their future operations. However, selections are

made approximately where budget will have the maximum effect and members of company are

given guiding on how to perform their activities. This method permits higher managers to

preserve whole financial control over a finance (Clark, Menifield and Stewart, 2018).

PART 2

4 Different Budgeting Methods

Rolling Budgets: A rolling budgeting method is always updated in order to include a

new finances period as the latest budget duration is completed. Consequently, the rolling

finances refer to the additive expansion of the prevailing price range model, thus, via doing so, a

business always has a price range that extends 365 into the future. Thus, a rolling price range

requires substantially greater management interest than is the case whilst an organization

develops a one-year static budget, for the reason that some budgeting tasks should now be

continual every month (Mahieu, Vroman and Calluy, 2015). Thus, this budget will improve

traditional budgeting method by providing the information of the latest budget facts of the

snappy drinks.

Moreover, This approach has the gain of having someone continuously attends to the

price range version and revise finances assumptions for the closing incremental period of the

finances. On the other hand, the disadvantage of this method is that it may now not yield a

finance which is extra workable than the conventional static price range, for the reason that

budgets durations preceding to the additive month just added are not altered.

Zero Based Budgeting: zero based budgeting is a technique that is used by the

companies for making plans and budgeting technique which calls for each manager to confirm

his entire finances request in detail from abrasion and transfers the encumbrance of proof to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

every supervisor to justify why he must spend any money in any respect. Further, this method

calls for that each of the tasks be analysed in choice applications which are evaluated through

systematic analysis and graded in order of standing (Brusca and Labrador,2016). However, the

zero based budgeting will improve the traditional method by helping the company to prepare

their expenses with zero budgets and plans, thus company can conduct their business operations

without any tension of budget plan they need to follow.

Moreover, the main advantage of zero based budgeting is that company don’t want to

rely upon any reference factor to assume over the budget of a specific object. for instance, the

company can make more investments their advertising and marketing department, because they

are starting the price range from zero. On the other hand, the major disadvantage of zero based

budgeting is that each budgeting object turns into the direct outcome of whether it generates

income or no longer. for instance, if the human source's department of the company doesn’t

generate plenty income for the previous couple of years, it will get much less investment for the

following year.

Activity Based Budgets: Activity based budgeting (ABB) is a method that provide

information, explore, and evaluate the tasks that result in charges for an organisation. Further,

every activity in an enterprise that incurs a price is examined for ability ways to develop

efficiencies. Budgets are then developed based totally on those consequences. Further, this

method will improve the traditional method by providing proper facts and data which depends on

the operations of the company.

Moreover, activity based budgeting (ABB) structures permit for extra manipulation over

the budgeting process. However, sales and price making plans takes place at a specific degree

that offers beneficial details concerning projections. ABB enables the management of company

to have accelerated control over the budgeting procedure and to line up the finances with overall

corporation goals (Rogulenko and et.al., 2016). On the other hand, Activity based budgeting is

more high-priced to put in force and hold than conventional budgeting techniques and extra time

consuming as well. Furthermore, ABB structures want additive presumptions and insight from

control, that can, now and again, bring about capacity budgeting inaccuracies.

5 Application Different Budgeting Method

Rolling budget: An application of rolling budget in snappy drinks can be explained

through following example, the snappy drinks have followed static budgets. They have been set

calls for that each of the tasks be analysed in choice applications which are evaluated through

systematic analysis and graded in order of standing (Brusca and Labrador,2016). However, the

zero based budgeting will improve the traditional method by helping the company to prepare

their expenses with zero budgets and plans, thus company can conduct their business operations

without any tension of budget plan they need to follow.

Moreover, the main advantage of zero based budgeting is that company don’t want to

rely upon any reference factor to assume over the budget of a specific object. for instance, the

company can make more investments their advertising and marketing department, because they

are starting the price range from zero. On the other hand, the major disadvantage of zero based

budgeting is that each budgeting object turns into the direct outcome of whether it generates

income or no longer. for instance, if the human source's department of the company doesn’t

generate plenty income for the previous couple of years, it will get much less investment for the

following year.

Activity Based Budgets: Activity based budgeting (ABB) is a method that provide

information, explore, and evaluate the tasks that result in charges for an organisation. Further,

every activity in an enterprise that incurs a price is examined for ability ways to develop

efficiencies. Budgets are then developed based totally on those consequences. Further, this

method will improve the traditional method by providing proper facts and data which depends on

the operations of the company.

Moreover, activity based budgeting (ABB) structures permit for extra manipulation over

the budgeting process. However, sales and price making plans takes place at a specific degree

that offers beneficial details concerning projections. ABB enables the management of company

to have accelerated control over the budgeting procedure and to line up the finances with overall

corporation goals (Rogulenko and et.al., 2016). On the other hand, Activity based budgeting is

more high-priced to put in force and hold than conventional budgeting techniques and extra time

consuming as well. Furthermore, ABB structures want additive presumptions and insight from

control, that can, now and again, bring about capacity budgeting inaccuracies.

5 Application Different Budgeting Method

Rolling budget: An application of rolling budget in snappy drinks can be explained

through following example, the snappy drinks have followed static budgets. They have been set

once and secured in for the 12 months. This effect in departments assembly their budgets early

and doing truly not anything the relaxation of the year. Thus, the organization established an 18-

month rolling finances. As we have seen that the agency adopted static finances and evolved a

budget for each of the following 18 months. And every month, actual income figures are

evaluated in opposition to the price range and the model is adjusted (Mahal and Hossain, 2015).

Zero Based Budgeting: This kind of budgeting commonly occurs in the authorities and

non-profit enterprises. However, the application of this budgeting technique in snappy drinks is

that it should be noted it requires common critiques. In zero based Budgeting evaluations of the

company are carried each year due to the fact that it's far a time-ingesting and costly technique.

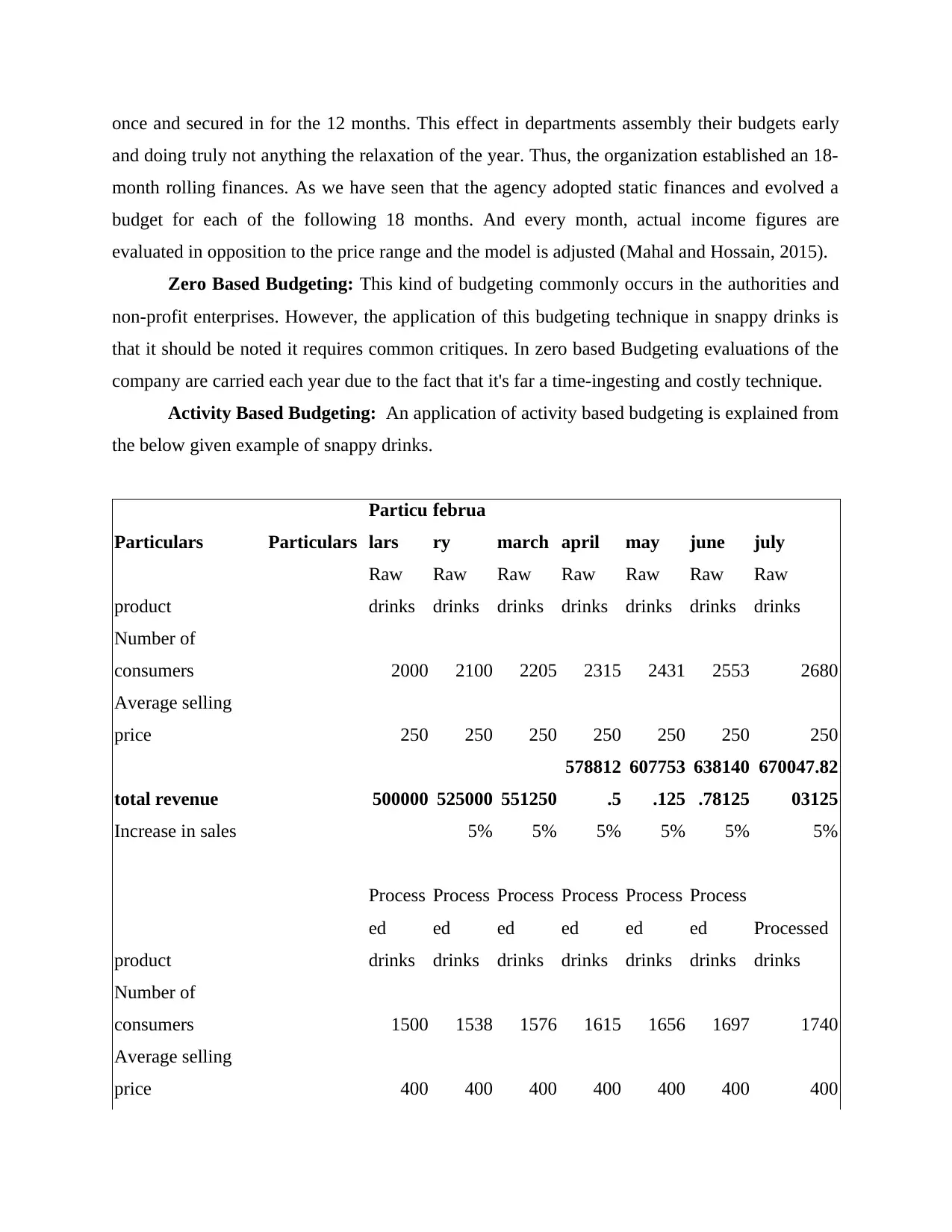

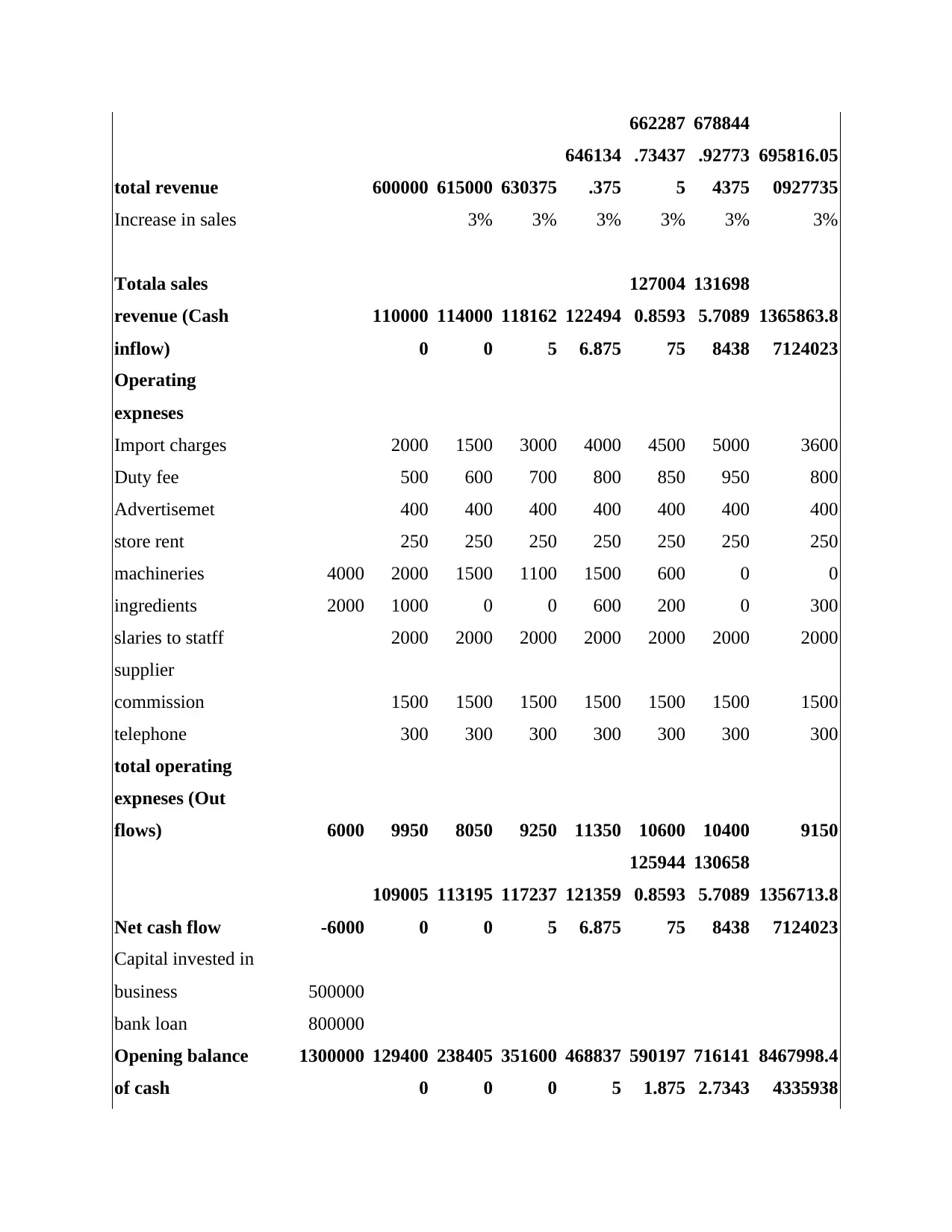

Activity Based Budgeting: An application of activity based budgeting is explained from

the below given example of snappy drinks.

Particulars Particulars

Particu

lars

februa

ry march april may june july

product

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Number of

consumers 2000 2100 2205 2315 2431 2553 2680

Average selling

price 250 250 250 250 250 250 250

total revenue 500000 525000 551250

578812

.5

607753

.125

638140

.78125

670047.82

03125

Increase in sales 5% 5% 5% 5% 5% 5%

product

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Processed

drinks

Number of

consumers 1500 1538 1576 1615 1656 1697 1740

Average selling

price 400 400 400 400 400 400 400

and doing truly not anything the relaxation of the year. Thus, the organization established an 18-

month rolling finances. As we have seen that the agency adopted static finances and evolved a

budget for each of the following 18 months. And every month, actual income figures are

evaluated in opposition to the price range and the model is adjusted (Mahal and Hossain, 2015).

Zero Based Budgeting: This kind of budgeting commonly occurs in the authorities and

non-profit enterprises. However, the application of this budgeting technique in snappy drinks is

that it should be noted it requires common critiques. In zero based Budgeting evaluations of the

company are carried each year due to the fact that it's far a time-ingesting and costly technique.

Activity Based Budgeting: An application of activity based budgeting is explained from

the below given example of snappy drinks.

Particulars Particulars

Particu

lars

februa

ry march april may june july

product

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Raw

drinks

Number of

consumers 2000 2100 2205 2315 2431 2553 2680

Average selling

price 250 250 250 250 250 250 250

total revenue 500000 525000 551250

578812

.5

607753

.125

638140

.78125

670047.82

03125

Increase in sales 5% 5% 5% 5% 5% 5%

product

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Process

ed

drinks

Processed

drinks

Number of

consumers 1500 1538 1576 1615 1656 1697 1740

Average selling

price 400 400 400 400 400 400 400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

total revenue 600000 615000 630375

646134

.375

662287

.73437

5

678844

.92773

4375

695816.05

0927735

Increase in sales 3% 3% 3% 3% 3% 3%

Totala sales

revenue (Cash

inflow)

110000

0

114000

0

118162

5

122494

6.875

127004

0.8593

75

131698

5.7089

8438

1365863.8

7124023

Operating

expneses

Import charges 2000 1500 3000 4000 4500 5000 3600

Duty fee 500 600 700 800 850 950 800

Advertisemet 400 400 400 400 400 400 400

store rent 250 250 250 250 250 250 250

machineries 4000 2000 1500 1100 1500 600 0 0

ingredients 2000 1000 0 0 600 200 0 300

slaries to statff 2000 2000 2000 2000 2000 2000 2000

supplier

commission 1500 1500 1500 1500 1500 1500 1500

telephone 300 300 300 300 300 300 300

total operating

expneses (Out

flows) 6000 9950 8050 9250 11350 10600 10400 9150

Net cash flow -6000

109005

0

113195

0

117237

5

121359

6.875

125944

0.8593

75

130658

5.7089

8438

1356713.8

7124023

Capital invested in

business 500000

bank loan 800000

Opening balance

of cash

1300000 129400

0

238405

0

351600

0

468837

5

590197

1.875

716141

2.7343

8467998.4

4335938

646134

.375

662287

.73437

5

678844

.92773

4375

695816.05

0927735

Increase in sales 3% 3% 3% 3% 3% 3%

Totala sales

revenue (Cash

inflow)

110000

0

114000

0

118162

5

122494

6.875

127004

0.8593

75

131698

5.7089

8438

1365863.8

7124023

Operating

expneses

Import charges 2000 1500 3000 4000 4500 5000 3600

Duty fee 500 600 700 800 850 950 800

Advertisemet 400 400 400 400 400 400 400

store rent 250 250 250 250 250 250 250

machineries 4000 2000 1500 1100 1500 600 0 0

ingredients 2000 1000 0 0 600 200 0 300

slaries to statff 2000 2000 2000 2000 2000 2000 2000

supplier

commission 1500 1500 1500 1500 1500 1500 1500

telephone 300 300 300 300 300 300 300

total operating

expneses (Out

flows) 6000 9950 8050 9250 11350 10600 10400 9150

Net cash flow -6000

109005

0

113195

0

117237

5

121359

6.875

125944

0.8593

75

130658

5.7089

8438

1356713.8

7124023

Capital invested in

business 500000

bank loan 800000

Opening balance

of cash

1300000 129400

0

238405

0

351600

0

468837

5

590197

1.875

716141

2.7343

8467998.4

4335938

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

75

Closing balance of

cash 1294000

238405

0

351600

0

468837

5

590197

1.875

716141

2.7343

75

846799

8.4433

5938

9824712.3

1459961

6. Evaluate which method is appropriate for the company.

There are two methods which are effective for the future operations of the company

namely; zero based budgeting and activity based budgeting due to the fact that zero-based

Budgeting enables the company in the allocation of assets effectively and according the size of

different department because it does now not look at the previous finance's numbers, rather

seems on the real figures. Furthermore, activity based budgeting permits equalization operational

requirements (Ylhäinen, 2017). This technique tries to keep away from calculating the financial

outcomes of unworkable plans. As it generates a budget from tasks and sources, it can frame

assets of imbalances, unskilfulness, and different regions for enhancements with the intention to

then permit managers and personnel to accurate the inefficiencies.

CONCLUSION

This report will briefly summarise about the purpose of budgeting and the process of

budgeting that will be followed by the company. Further, the project has outlined about the

application of tradition budgeting method and along with that it will highlight the incremental

budgeting method. Moreover, the assignment has highlighted about different budgeting methods

which is inclusive of rolling budgets, zero based budgeting and activity based budgeting etc. On

the other hand, the project will frame the application of the above mentioned methods with the

help of an example.

Closing balance of

cash 1294000

238405

0

351600

0

468837

5

590197

1.875

716141

2.7343

75

846799

8.4433

5938

9824712.3

1459961

6. Evaluate which method is appropriate for the company.

There are two methods which are effective for the future operations of the company

namely; zero based budgeting and activity based budgeting due to the fact that zero-based

Budgeting enables the company in the allocation of assets effectively and according the size of

different department because it does now not look at the previous finance's numbers, rather

seems on the real figures. Furthermore, activity based budgeting permits equalization operational

requirements (Ylhäinen, 2017). This technique tries to keep away from calculating the financial

outcomes of unworkable plans. As it generates a budget from tasks and sources, it can frame

assets of imbalances, unskilfulness, and different regions for enhancements with the intention to

then permit managers and personnel to accurate the inefficiencies.

CONCLUSION

This report will briefly summarise about the purpose of budgeting and the process of

budgeting that will be followed by the company. Further, the project has outlined about the

application of tradition budgeting method and along with that it will highlight the incremental

budgeting method. Moreover, the assignment has highlighted about different budgeting methods

which is inclusive of rolling budgets, zero based budgeting and activity based budgeting etc. On

the other hand, the project will frame the application of the above mentioned methods with the

help of an example.

REFERENCES

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance.77.pp.176-196.

Bogsnes, B., 2016. Implementing beyond budgeting: Unlocking the performance potential. John

Wiley & Sons.

Wildavsky, A., 2017. Budgeting and governing. Routledge.

Miller, G., 2018. Performance based budgeting. Routledge.

Dudin, M and et.al., 2015. The innovative business model canvas in the system of effective

budgeting. Asian Social Science.11(7). pp.290-296.

Popesko, B and et.al., 2017. The maturity of a budgeting system and its influence on corporate

performance. Acta Polytechnica Hungarica.14(7).

de Campos, C.M.P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global

Encyclopedia of Public Administration, Public Policy, and Governance, pp.1-10.

Clark, C., Menifield, C.E. and Stewart, L.M., 2018. Policy Diffusion and Performance-based

Budgeting. International Journal of Public Administration.41(7).pp.528-534.

Mahieu, K., Vroman, S. and Calluy, P., 2015. Asset-based Budgeting in Practice. Controlling &

Management Review.59(5). pp.29-37.

Brusca, I. and Labrador, M., 2016. Budgeting in the public sector. Global Encyclopedia of

Public Administration, Public Policy, and Governance, pp.1-13.

Rogulenko, T and et.al., 2016. Budgeting-Based Organization of Internal Control. International

Journal of Environmental and Science Education.11(11). pp.4104-4117.

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting.6(4).pp.66-74.

Ylhäinen, I., 2017. Life-cycle effects in small business finance. Journal of Banking &

Finance.77.pp.176-196.

Bogsnes, B., 2016. Implementing beyond budgeting: Unlocking the performance potential. John

Wiley & Sons.

Wildavsky, A., 2017. Budgeting and governing. Routledge.

Miller, G., 2018. Performance based budgeting. Routledge.

Dudin, M and et.al., 2015. The innovative business model canvas in the system of effective

budgeting. Asian Social Science.11(7). pp.290-296.

Popesko, B and et.al., 2017. The maturity of a budgeting system and its influence on corporate

performance. Acta Polytechnica Hungarica.14(7).

de Campos, C.M.P. and Rodrigues, L.L., 2016. Budgeting Techniques: Incremental Based,

Performance Based, Activity Based, Zero Based, and Priority Based. Global

Encyclopedia of Public Administration, Public Policy, and Governance, pp.1-10.

Clark, C., Menifield, C.E. and Stewart, L.M., 2018. Policy Diffusion and Performance-based

Budgeting. International Journal of Public Administration.41(7).pp.528-534.

Mahieu, K., Vroman, S. and Calluy, P., 2015. Asset-based Budgeting in Practice. Controlling &

Management Review.59(5). pp.29-37.

Brusca, I. and Labrador, M., 2016. Budgeting in the public sector. Global Encyclopedia of

Public Administration, Public Policy, and Governance, pp.1-13.

Rogulenko, T and et.al., 2016. Budgeting-Based Organization of Internal Control. International

Journal of Environmental and Science Education.11(11). pp.4104-4117.

Mahal, I. and Hossain, A., 2015. Activity-Based Costing (ABC)–An Effective Tool for Better

Management. Research Journal of Finance and Accounting.6(4).pp.66-74.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.