EBUS614: Analysis of Budgeting and Scheduling in Project Management

VerifiedAdded on 2020/11/30

|44

|2950

|305

Report

AI Summary

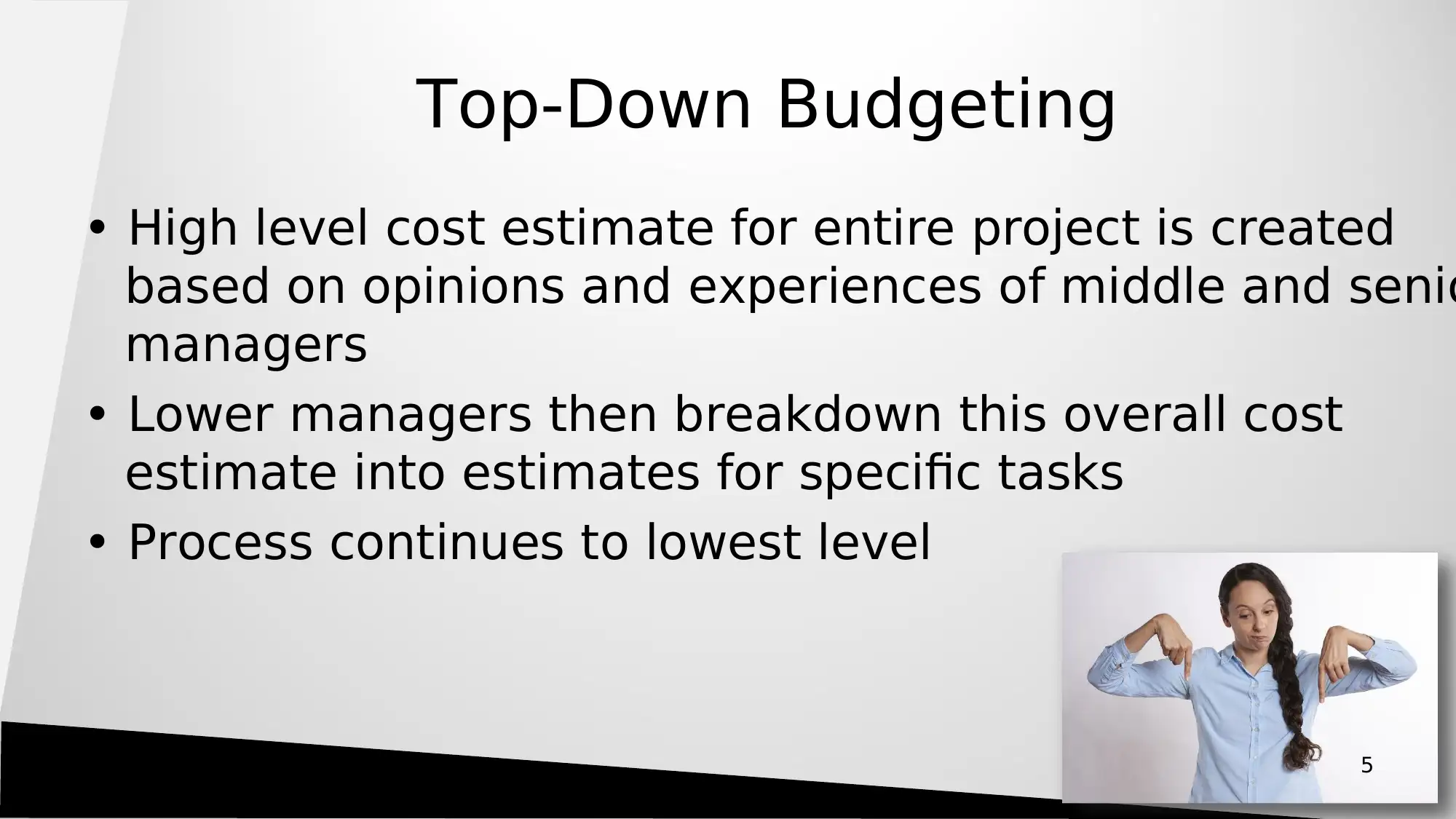

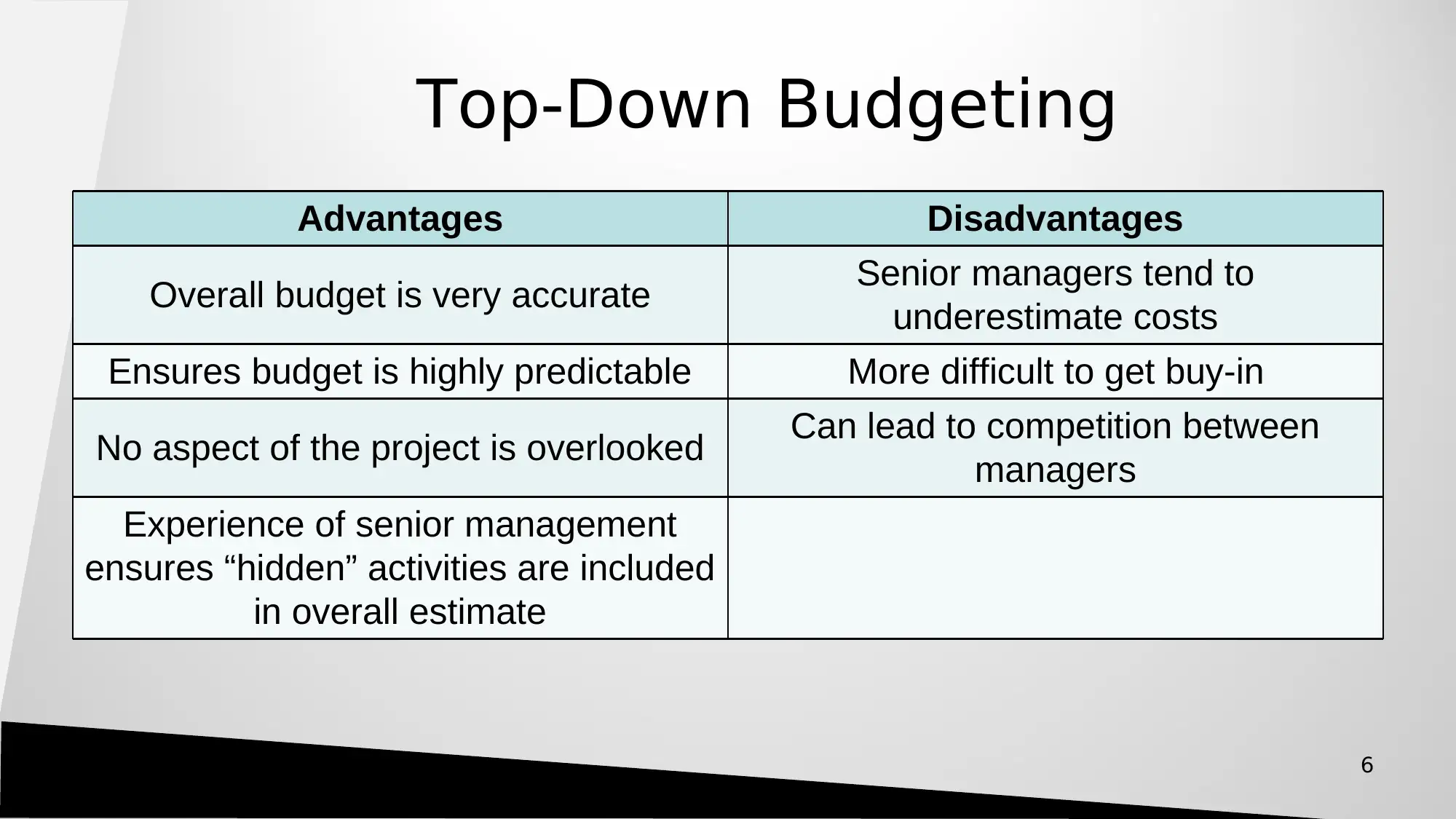

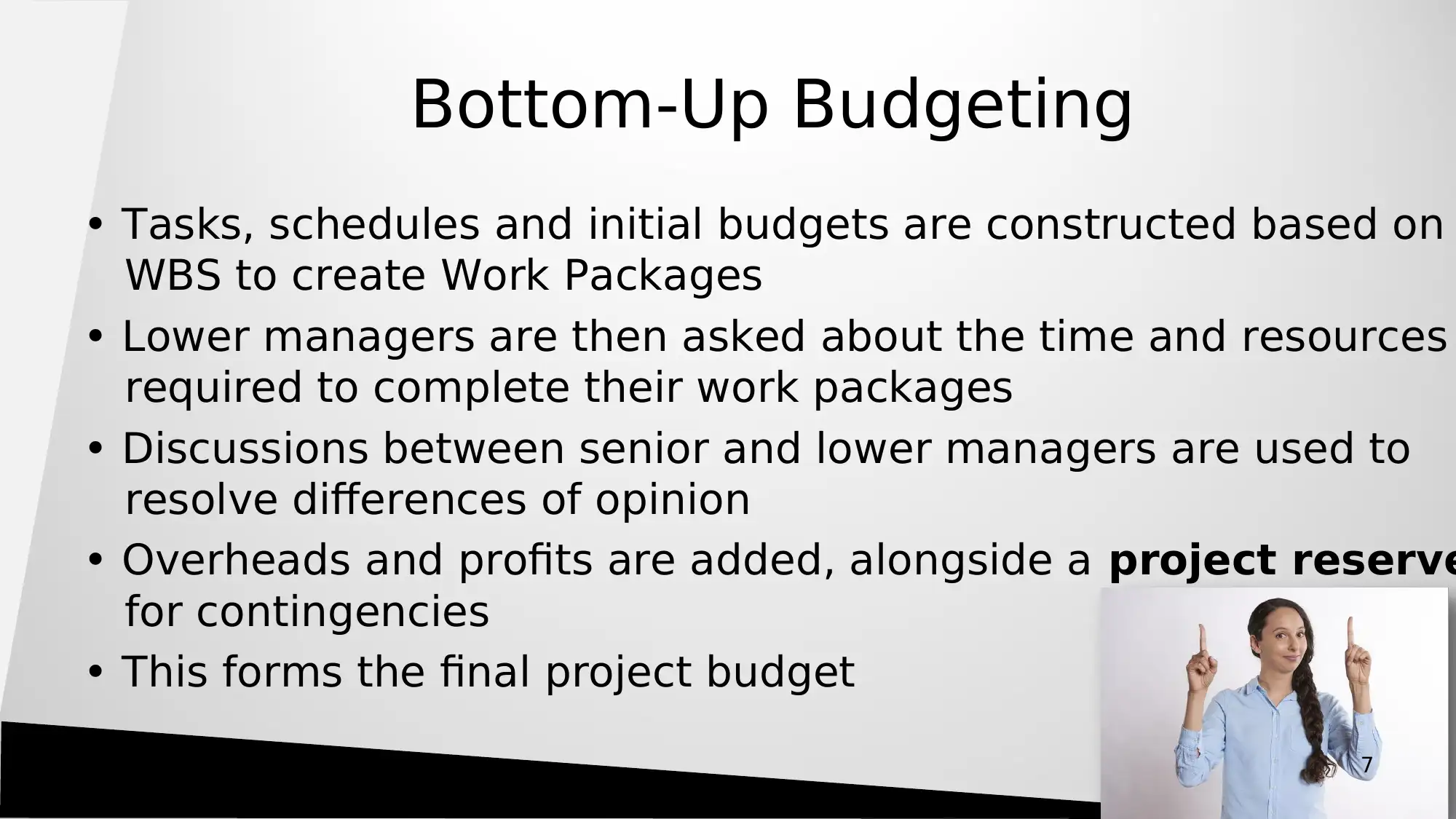

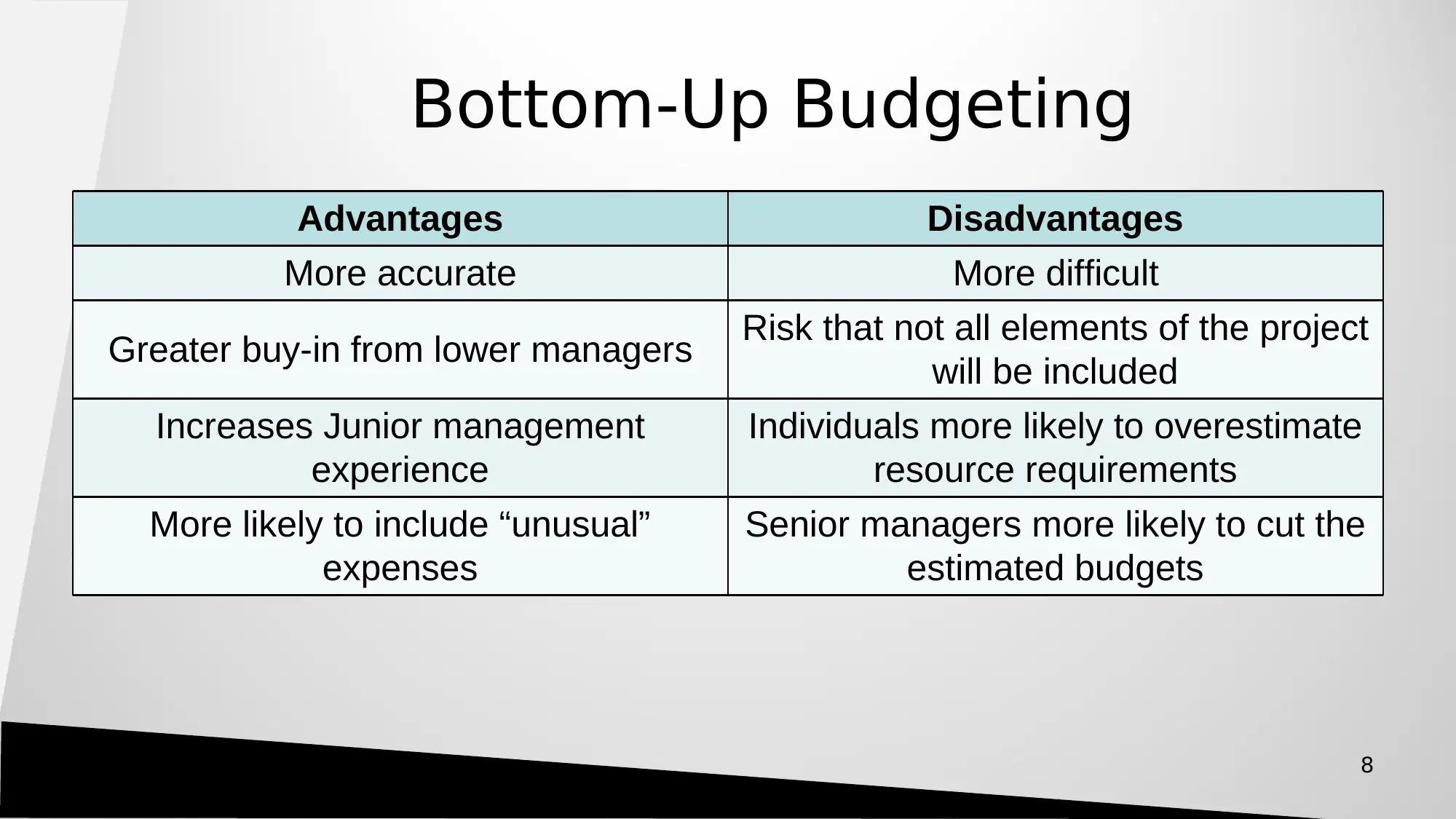

This report provides a comprehensive overview of budgeting and scheduling within project management, drawing from a lecture on the topic. It delves into the core concepts of budgeting, including budget estimation techniques like top-down and bottom-up approaches, work element costing, and the distinction between category and project budgeting. The report then transitions into scheduling, explaining techniques and terminology, such as network diagrams (Activity on Node), expected time calculations, critical path analysis, and the concept of slack. The content covers essential aspects of project planning and control, offering practical insights into resource allocation, time management, and the effective use of scheduling tools to ensure project success. The report also includes quizzes to test the understanding of the concepts.

1 out of 44

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.