Budgeting Solved Assignments

VerifiedAdded on 2019/10/30

|5

|820

|342

Homework Assignment

AI Summary

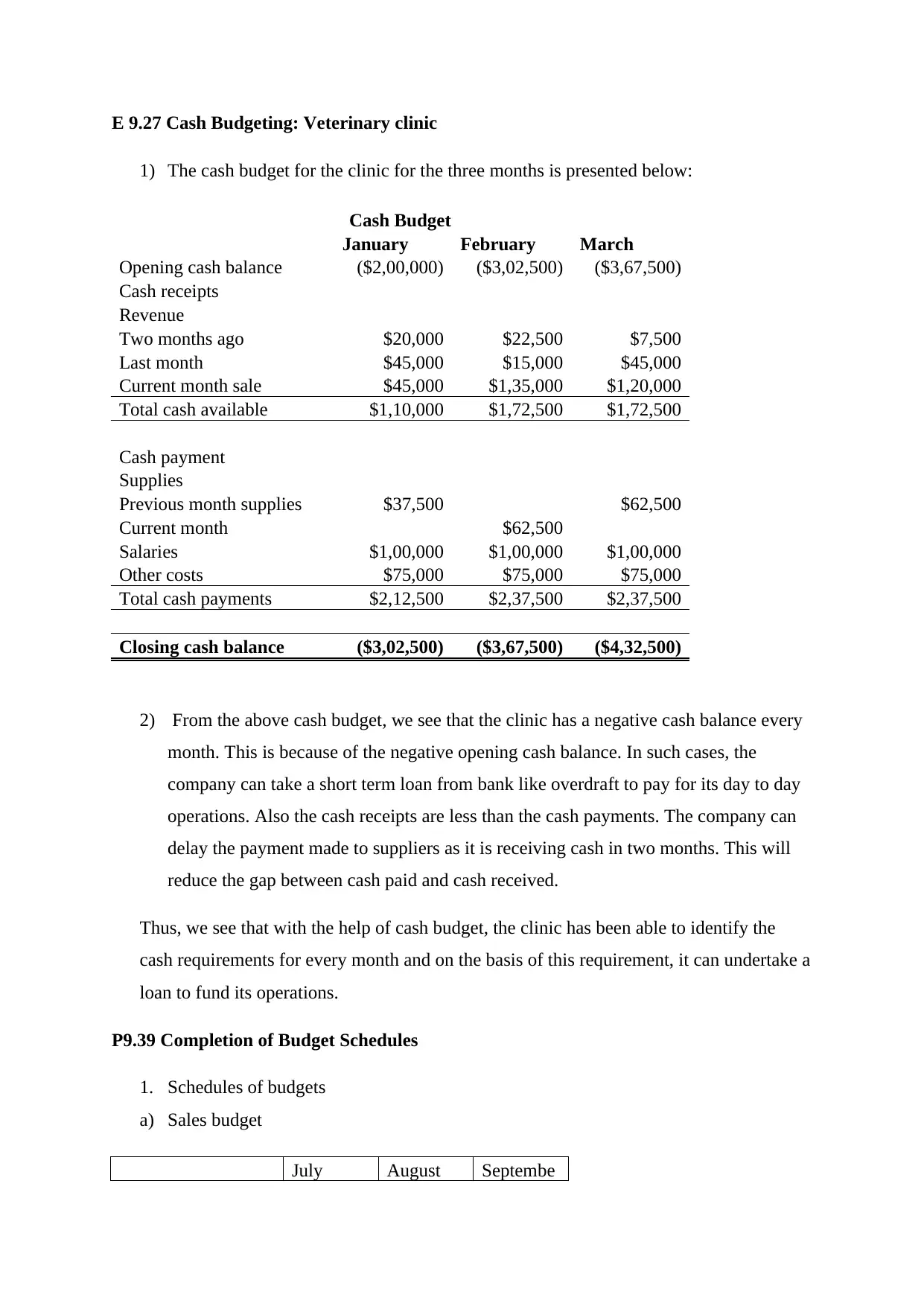

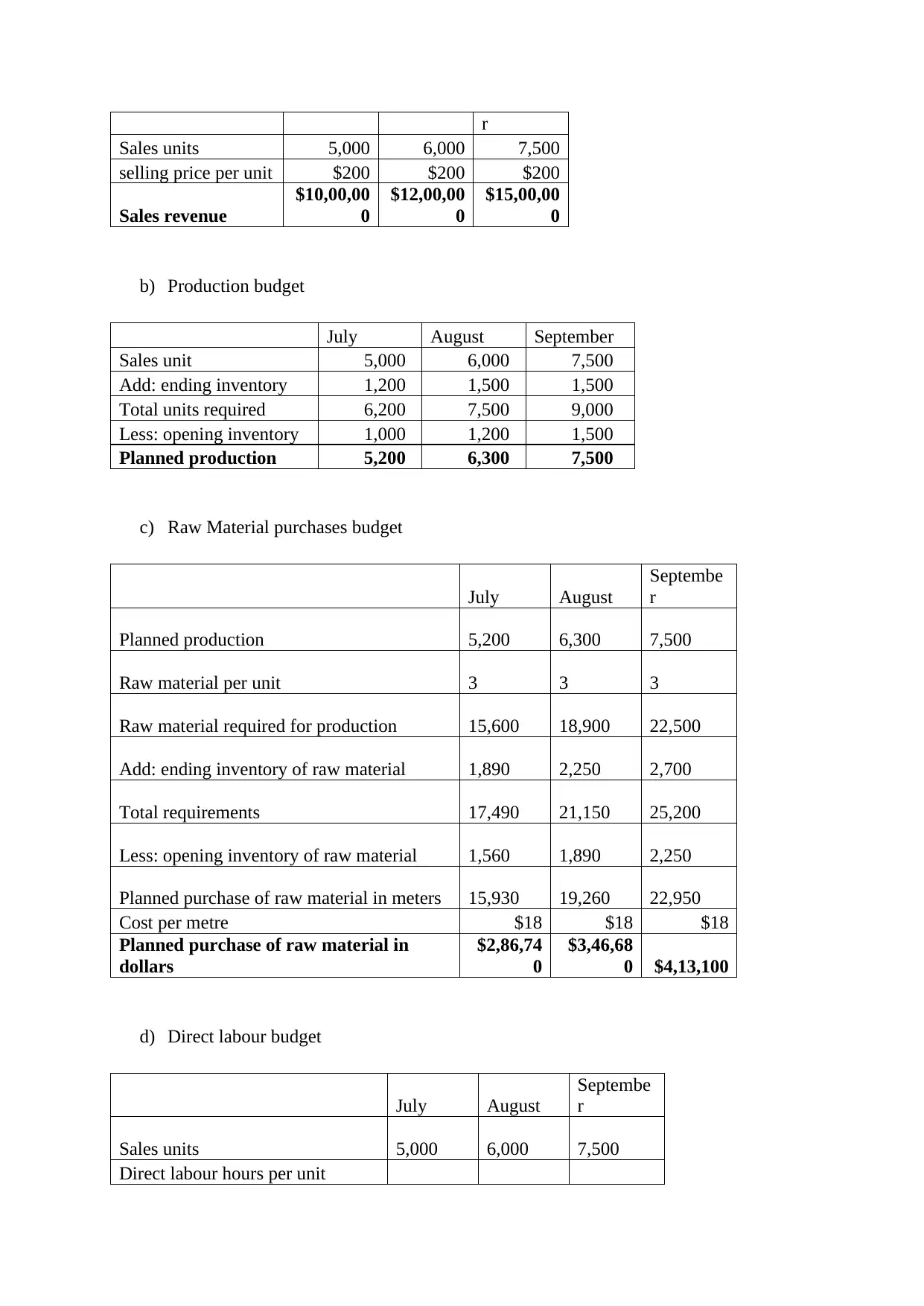

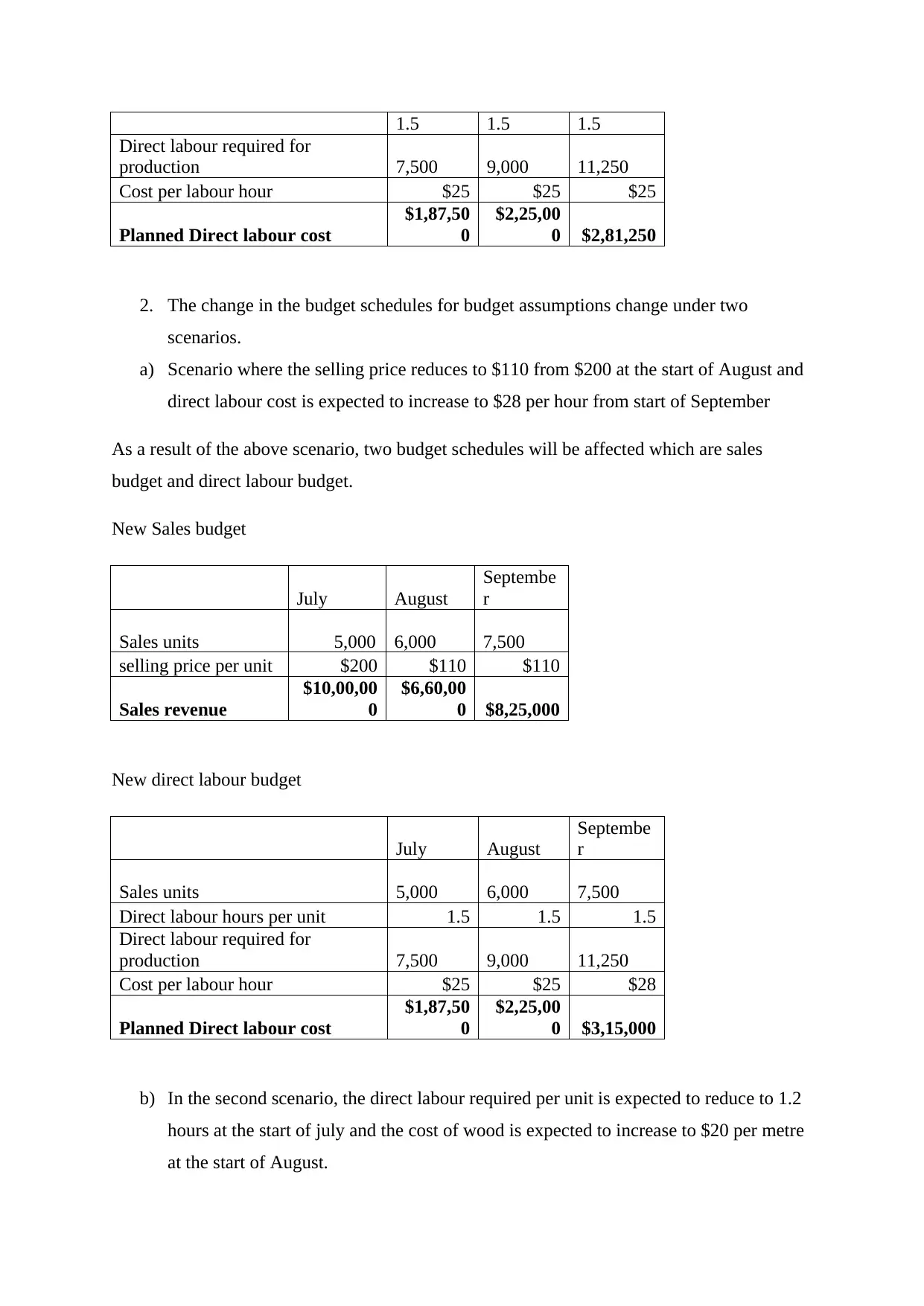

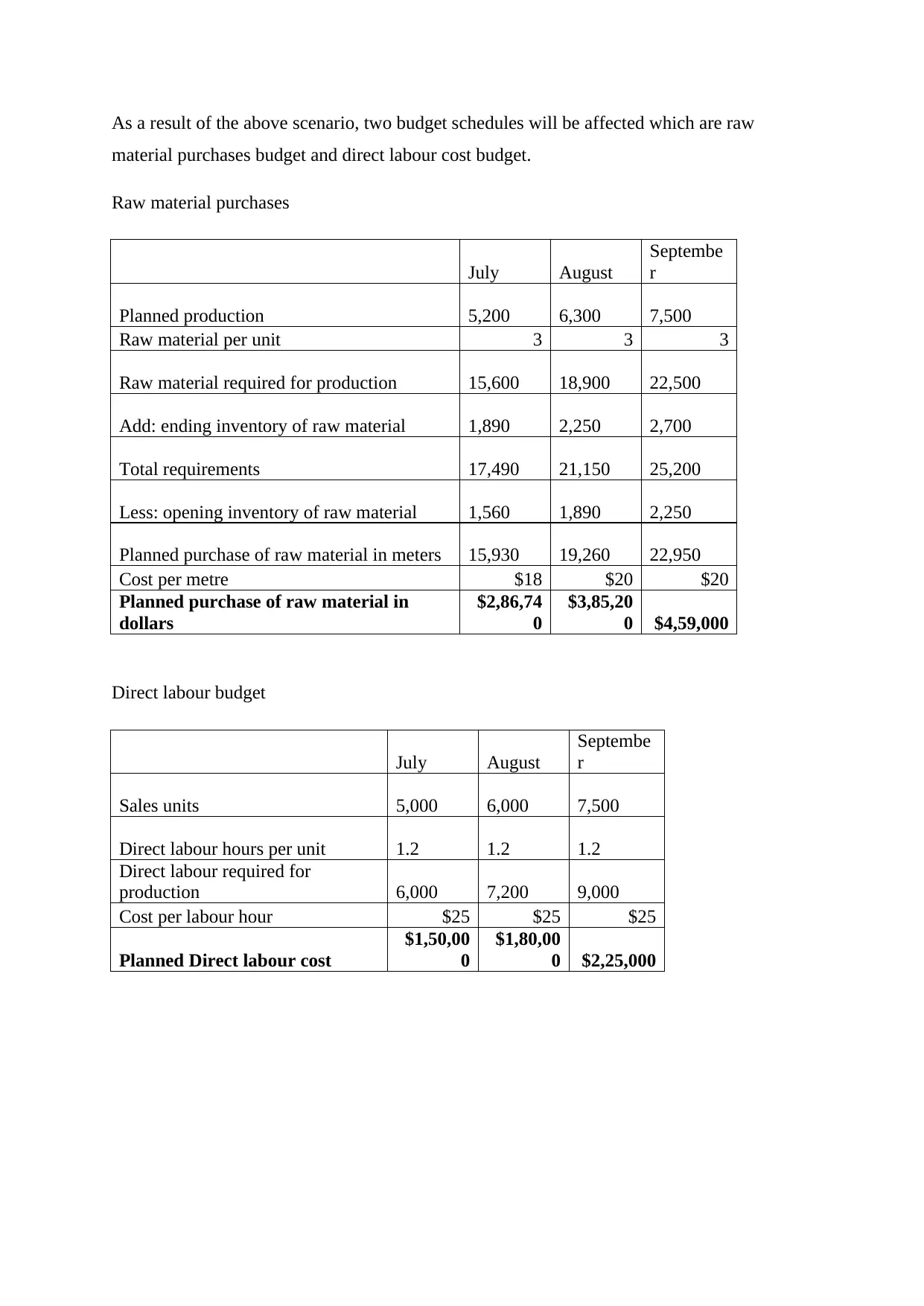

This assignment provides solved examples of budgeting problems. It includes a detailed cash budget for a veterinary clinic, highlighting the clinic's negative cash balance and suggesting solutions like short-term loans. The assignment also demonstrates the creation of several budget schedules: sales budget, production budget, raw material purchases budget, and direct labor budget. It further explores how changes in budget assumptions (selling price, direct labor cost, raw material cost) affect these schedules, presenting revised budgets under two different scenarios. The solutions illustrate the process of adjusting budgets based on changing market conditions and operational factors.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.