Budgetary Planning & Control: Zero-Based Budgeting and Performance

VerifiedAdded on 2023/06/18

|13

|3391

|195

Report

AI Summary

This assignment delves into various aspects of budgetary planning and control, contrasting zero-based budgeting with traditional methods and exploring the advantages and disadvantages of activity-based budgeting in a manufacturing context. It addresses the reluctance of managers to participate in budget setting and the potential side effects of top-down budget imposition. The report includes the preparation of an incremental budget, discusses its applicability to different expense types, and compares top-down and bottom-up budgeting approaches. Furthermore, it covers the preparation of a rolling budget and highlights difficulties in changing budgetary systems. The assignment also emphasizes the need for performance measurement, considering both financial and non-financial factors, and provides solutions to address these factors, ultimately aiming to enhance financial performance through improved budgetary practices.

Budgetary Planning and

Control

Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

How Zero-based budgeting techniques differ from the traditional budgeting?......................................3

How Zero-Based budgeting may assist in planning and controlling discretionary costs?........................4

How Zero-based will help to control any inefficiencies?.........................................................................4

QUESTION 2.................................................................................................................................................5

Suggest reasons why managers may be reluctant to participate fully in setting budgets and suggest

also unwanted side effects which may arise from the imposition of budgets by senior management.. .5

QUESTION 3.................................................................................................................................................6

Discuss advantages and disadvantages of adopting activity-based budgets to fixed budget in

manufacturing company..........................................................................................................................6

Explain the need for the measurement or company and department performance giving examples of

the range of financial & non-financial factors which impact the performance and providing solutions

to the factors mentioned.........................................................................................................................7

QUESTION 4.................................................................................................................................................8

Prepare incremental budget....................................................................................................................8

Can incremental budget be used for rent (of premises) and what about advertising expenses?............9

Explain the top down and bottom up approach and explain the advantage and disadvantage of each

approach.................................................................................................................................................9

QUESTION 5...............................................................................................................................................10

Prepare rolling budget...........................................................................................................................10

Examples on difficulties a company must face when changing budgetary systems..............................11

REFERENCES..............................................................................................................................................12

INTRODUCTION...........................................................................................................................................3

QUESTION 1.................................................................................................................................................3

How Zero-based budgeting techniques differ from the traditional budgeting?......................................3

How Zero-Based budgeting may assist in planning and controlling discretionary costs?........................4

How Zero-based will help to control any inefficiencies?.........................................................................4

QUESTION 2.................................................................................................................................................5

Suggest reasons why managers may be reluctant to participate fully in setting budgets and suggest

also unwanted side effects which may arise from the imposition of budgets by senior management.. .5

QUESTION 3.................................................................................................................................................6

Discuss advantages and disadvantages of adopting activity-based budgets to fixed budget in

manufacturing company..........................................................................................................................6

Explain the need for the measurement or company and department performance giving examples of

the range of financial & non-financial factors which impact the performance and providing solutions

to the factors mentioned.........................................................................................................................7

QUESTION 4.................................................................................................................................................8

Prepare incremental budget....................................................................................................................8

Can incremental budget be used for rent (of premises) and what about advertising expenses?............9

Explain the top down and bottom up approach and explain the advantage and disadvantage of each

approach.................................................................................................................................................9

QUESTION 5...............................................................................................................................................10

Prepare rolling budget...........................................................................................................................10

Examples on difficulties a company must face when changing budgetary systems..............................11

REFERENCES..............................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The method of constructing a budget and then using it to manage a daily finances is known

as budget preparation. The goal of budgeting is to reduce the chance that a company's monetary

performance will be less than ideal. Constructing a budget will be the first process in terms of

financing. Budgeting is the process of converting lengthy business vision into brief new

initiatives. A budget is a document that outlines a company's short-term goals and how

stimulates business to obtain, utilize, and regulate funds to satisfy those goals. A company's

spending plan should be thorough and well-planned. The budget is an important component of

planning and scheduling, as well as a key tool for performance evaluations (Velte, 2019). The

budget is a plan used to evaluate revenue and spending over a length of time, generally the

preceding quarter, and to make adjustments to account for any predictable changes. A budget, in

the broadest sense, is an estimate of revenue and spending for a certain predefined timeframe. In

this report consist of different types of budget questions that based on the rolling, zero based and

activity based budgets.

QUESTION 1

How Zero-based budgeting techniques differ from the traditional budgeting?

As the name implies, zero-based planning is a spending approach that involves the

development and justification of every budget from the ground up. Every time the budget is

prepared, it is a technique where all of the operations are reviewed. It is constructed with no

reference to the previous expenditures or real events. Simply said, it's a planning approach in

which each expense element requires particular explanation, like the budget's actions were being

performed in for the first moment. As a result, the management has the weight of proof in

explaining why money is being spent on a specific activity but also what would happen if the

suggested activity is not carried out and no money is being spent. The budget allotment is zero if

permission is not granted.

Traditional budgeting is a method of budget planning wherein the prior year's

expenditure is used as a starting point. Zero-based planning, on either extreme, is a

The method of constructing a budget and then using it to manage a daily finances is known

as budget preparation. The goal of budgeting is to reduce the chance that a company's monetary

performance will be less than ideal. Constructing a budget will be the first process in terms of

financing. Budgeting is the process of converting lengthy business vision into brief new

initiatives. A budget is a document that outlines a company's short-term goals and how

stimulates business to obtain, utilize, and regulate funds to satisfy those goals. A company's

spending plan should be thorough and well-planned. The budget is an important component of

planning and scheduling, as well as a key tool for performance evaluations (Velte, 2019). The

budget is a plan used to evaluate revenue and spending over a length of time, generally the

preceding quarter, and to make adjustments to account for any predictable changes. A budget, in

the broadest sense, is an estimate of revenue and spending for a certain predefined timeframe. In

this report consist of different types of budget questions that based on the rolling, zero based and

activity based budgets.

QUESTION 1

How Zero-based budgeting techniques differ from the traditional budgeting?

As the name implies, zero-based planning is a spending approach that involves the

development and justification of every budget from the ground up. Every time the budget is

prepared, it is a technique where all of the operations are reviewed. It is constructed with no

reference to the previous expenditures or real events. Simply said, it's a planning approach in

which each expense element requires particular explanation, like the budget's actions were being

performed in for the first moment. As a result, the management has the weight of proof in

explaining why money is being spent on a specific activity but also what would happen if the

suggested activity is not carried out and no money is being spent. The budget allotment is zero if

permission is not granted.

Traditional budgeting is a method of budget planning wherein the prior year's

expenditure is used as a starting point. Zero-based planning, on either extreme, is a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

budgetary approach in which the operations are re-evaluated and therefore begun from

the beginning every year the budget is generated.

Traditional budgeting places a premium on the previous spending amount. Zero-based

planning, on the other hand, focuses on creating a fresh financial proposition when the

price is balanced.

Planning in the conventional sense is bookkeeping, as it is based on cost accounting

concepts. The zero-based method of budgeting, on the other hand, is judgment.

Explanation of the current project is not necessary in the typical budget formulation. In

zero-based planning, on the other hand, the current and planned projects must be

justified, taking into consideration the expenses and advantages.

Upper executives make the choice on why a certain amount is spend on a decision unit in

conventional budgeting. With zero-based planning, management decides whether or not

to spend a certain amount on a judgment item.

How Zero-Based budgeting may assist in planning and controlling discretionary costs?

Zero-based budgeting (ZBB) is a budgeting method that contributes directly sustainable

development and environmental and demand instead than previous forecasting. Administration

creates a budget from the base up that only comprises processes and costs that are crucial to

maintain the firm; no expenditures are usually attached to the budgeted. Peter A. Pyhor defines

ZBB as a "operational budget preparation procedure, which demands every management to

explain his whole expenditure in full starting start and puts the burden of evidence to each

manager to demonstrate that he should spend the cash in anyway." All actions must be

recognized in "decision elements," which must then be reviewed and rated in order of

significance using a systematic methodology. ZBB is a methodology that supplements and

connects current strategy, costing, and reviewing procedures by identifying alternate effective

means of employing limited funds in order to effectively achieve specified outcomes. It's an

appropriate organizational technique that focuses on a detailed evaluation and explanation of

existing programme or activity financing and system performance, providing a convincing

reason for shifting resources.

the beginning every year the budget is generated.

Traditional budgeting places a premium on the previous spending amount. Zero-based

planning, on the other hand, focuses on creating a fresh financial proposition when the

price is balanced.

Planning in the conventional sense is bookkeeping, as it is based on cost accounting

concepts. The zero-based method of budgeting, on the other hand, is judgment.

Explanation of the current project is not necessary in the typical budget formulation. In

zero-based planning, on the other hand, the current and planned projects must be

justified, taking into consideration the expenses and advantages.

Upper executives make the choice on why a certain amount is spend on a decision unit in

conventional budgeting. With zero-based planning, management decides whether or not

to spend a certain amount on a judgment item.

How Zero-Based budgeting may assist in planning and controlling discretionary costs?

Zero-based budgeting (ZBB) is a budgeting method that contributes directly sustainable

development and environmental and demand instead than previous forecasting. Administration

creates a budget from the base up that only comprises processes and costs that are crucial to

maintain the firm; no expenditures are usually attached to the budgeted. Peter A. Pyhor defines

ZBB as a "operational budget preparation procedure, which demands every management to

explain his whole expenditure in full starting start and puts the burden of evidence to each

manager to demonstrate that he should spend the cash in anyway." All actions must be

recognized in "decision elements," which must then be reviewed and rated in order of

significance using a systematic methodology. ZBB is a methodology that supplements and

connects current strategy, costing, and reviewing procedures by identifying alternate effective

means of employing limited funds in order to effectively achieve specified outcomes. It's an

appropriate organizational technique that focuses on a detailed evaluation and explanation of

existing programme or activity financing and system performance, providing a convincing

reason for shifting resources.

How Zero-based will help to control any inefficiencies?

Every cycle in a firm's calender is scheduled fully based on the expenditures and demands for

that term, which might be for a monthly, a quarter, or a year, beginning from a zero base with no

spending or debts left forward (whatever works best for a business). Regardless of whether

company' budget was greater or lower even during prior months, the justifiable costs and income

commitments are considered as the major elements for the current period's budget. Start from

zero base and continue the cycle whenever the next session starts.

QUESTION 2

Suggest reasons why managers may be reluctant to participate fully in setting budgets and

suggest also unwanted side effects which may arise from the imposition of budgets by

senior management.

For a variety of reasons, supervisors may be hesitant to participate actively in budgeting. To

begin with, supervisors may believe that they are not genuinely participating in the budgeting

process if they have little impact over the budget. This is due to managers' believing that their

suggestions and ideas will most likely be rejected by their senior executives. Since they dislike

discussing money, a few supervisors are reluctant to take part in financial planning. They may

also believe that creating a budget limits a firm's versatility. A few really people want

unrestricted access to all of the money. The budget resolution can be disconcerting and

demoralizing in the wrong context. It is beneficial to have as much input as possible from

reduced ranks in terms of spending subject matter and variables. They also have to understand

how the spending plan is progressing during the year.

Managers are hesitant to participate in the budget preparation since they can't make a

difference in the budgets while they can't make a difference in the plan. Like a result, they

receive formal approval of the predetermined objective levels, allowing them to be considered

high management. Another cause for executives' apprehension is a lack of knowledge of the

budgetary process. Whereas if management doesn’t understand the financial plan, they won't be

able to meet the budgets objectives and the plan will be rejected. When they have a strained

Every cycle in a firm's calender is scheduled fully based on the expenditures and demands for

that term, which might be for a monthly, a quarter, or a year, beginning from a zero base with no

spending or debts left forward (whatever works best for a business). Regardless of whether

company' budget was greater or lower even during prior months, the justifiable costs and income

commitments are considered as the major elements for the current period's budget. Start from

zero base and continue the cycle whenever the next session starts.

QUESTION 2

Suggest reasons why managers may be reluctant to participate fully in setting budgets and

suggest also unwanted side effects which may arise from the imposition of budgets by

senior management.

For a variety of reasons, supervisors may be hesitant to participate actively in budgeting. To

begin with, supervisors may believe that they are not genuinely participating in the budgeting

process if they have little impact over the budget. This is due to managers' believing that their

suggestions and ideas will most likely be rejected by their senior executives. Since they dislike

discussing money, a few supervisors are reluctant to take part in financial planning. They may

also believe that creating a budget limits a firm's versatility. A few really people want

unrestricted access to all of the money. The budget resolution can be disconcerting and

demoralizing in the wrong context. It is beneficial to have as much input as possible from

reduced ranks in terms of spending subject matter and variables. They also have to understand

how the spending plan is progressing during the year.

Managers are hesitant to participate in the budget preparation since they can't make a

difference in the budgets while they can't make a difference in the plan. Like a result, they

receive formal approval of the predetermined objective levels, allowing them to be considered

high management. Another cause for executives' apprehension is a lack of knowledge of the

budgetary process. Whereas if management doesn’t understand the financial plan, they won't be

able to meet the budgets objectives and the plan will be rejected. When they have a strained

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

connection with their bosses, lower management is expected to be hesitant. Managers will be less

motivated to engage in the government's budget and will have a poor opinion about their

supervisors unless the connection is unfavorable, finding it challenging to meet budget targets.

Managerial character is crucial in the budgetary control. Whereas if executives' supervisors

believe they have a good personality, they will be hesitant to participate in the budgetary process

because they are frightened of being judged.

QUESTION 3

Discuss advantages and disadvantages of adopting activity-based budgets to fixed budget in

manufacturing company

The most common application of activity-based budgeting is in costing system. Budgets

and expenditure proposals are prepared by administrators derived from previous production

process. To put it another way, managers should look at the expenses of executing specific tasks,

such as folding a vehicle fender, in order to budget the entire expenses of manufacturing a

product. The firm may be able to earn costs by expanding batch output, lowering manufacturing

time, or even merging the two tasks, based on two main operations. Activity-based planning not

only saves money for the firm, but it also compels managers to scrutinize each action. This

allows managers to have a thorough understanding of the entire process of production.

Information like this may lead to a lot more than just cost savings. Knowing and comprehending

the production process is frequently the source of development and manufacturing development.

It just means that the company needs to change their perspective on the process. Every

manufacturer should priorities activity-based budgeting.

Advantage:

Control: ABB gives more power over finances. They estimate depending on operations that are

aligned with corporate goals, giving them the flexibility to spend cash according to what

corporate requires to develop.

Cost-cutting: They aren't overspending on activities that the company doesn't require. The goal

of ABB is to expend the rest of the money in the right locations that may save a lot of money.

motivated to engage in the government's budget and will have a poor opinion about their

supervisors unless the connection is unfavorable, finding it challenging to meet budget targets.

Managerial character is crucial in the budgetary control. Whereas if executives' supervisors

believe they have a good personality, they will be hesitant to participate in the budgetary process

because they are frightened of being judged.

QUESTION 3

Discuss advantages and disadvantages of adopting activity-based budgets to fixed budget in

manufacturing company

The most common application of activity-based budgeting is in costing system. Budgets

and expenditure proposals are prepared by administrators derived from previous production

process. To put it another way, managers should look at the expenses of executing specific tasks,

such as folding a vehicle fender, in order to budget the entire expenses of manufacturing a

product. The firm may be able to earn costs by expanding batch output, lowering manufacturing

time, or even merging the two tasks, based on two main operations. Activity-based planning not

only saves money for the firm, but it also compels managers to scrutinize each action. This

allows managers to have a thorough understanding of the entire process of production.

Information like this may lead to a lot more than just cost savings. Knowing and comprehending

the production process is frequently the source of development and manufacturing development.

It just means that the company needs to change their perspective on the process. Every

manufacturer should priorities activity-based budgeting.

Advantage:

Control: ABB gives more power over finances. They estimate depending on operations that are

aligned with corporate goals, giving them the flexibility to spend cash according to what

corporate requires to develop.

Cost-cutting: They aren't overspending on activities that the company doesn't require. The goal

of ABB is to expend the rest of the money in the right locations that may save a lot of money.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Simplifying: They're getting rid of all tasks that aren't directly related to earning income. By

eliminating these constraints, operations may operate perfectly, efficiently, and cost-effectively.

Administrative coherence is required by ABB, which demands a holistic view of the company

centered on activities rather than specific divisions. This gives a more holistic feeling of financial

cohesion.

Disadvantage: Every action is researched, evaluated, and analysed separately by ABB, which

requires a lot of money and time. This type of investigation is time-consuming and expensive. It

takes time and money to accomplish, and management must have a thorough grasp of the many

aspects of the firm. Additionally, incorrectly doing ABB research can lead to budgeting errors,

which can be particularly troublesome for firms with little profit margin.

In many situations, ABB is also more concerned with the ability to pay short objectives.

That doesn't always take very long goals and budgets into account. In addition for ABB to

function successfully, it's critical to evaluate how each operation fits into the larger scope of the

company.

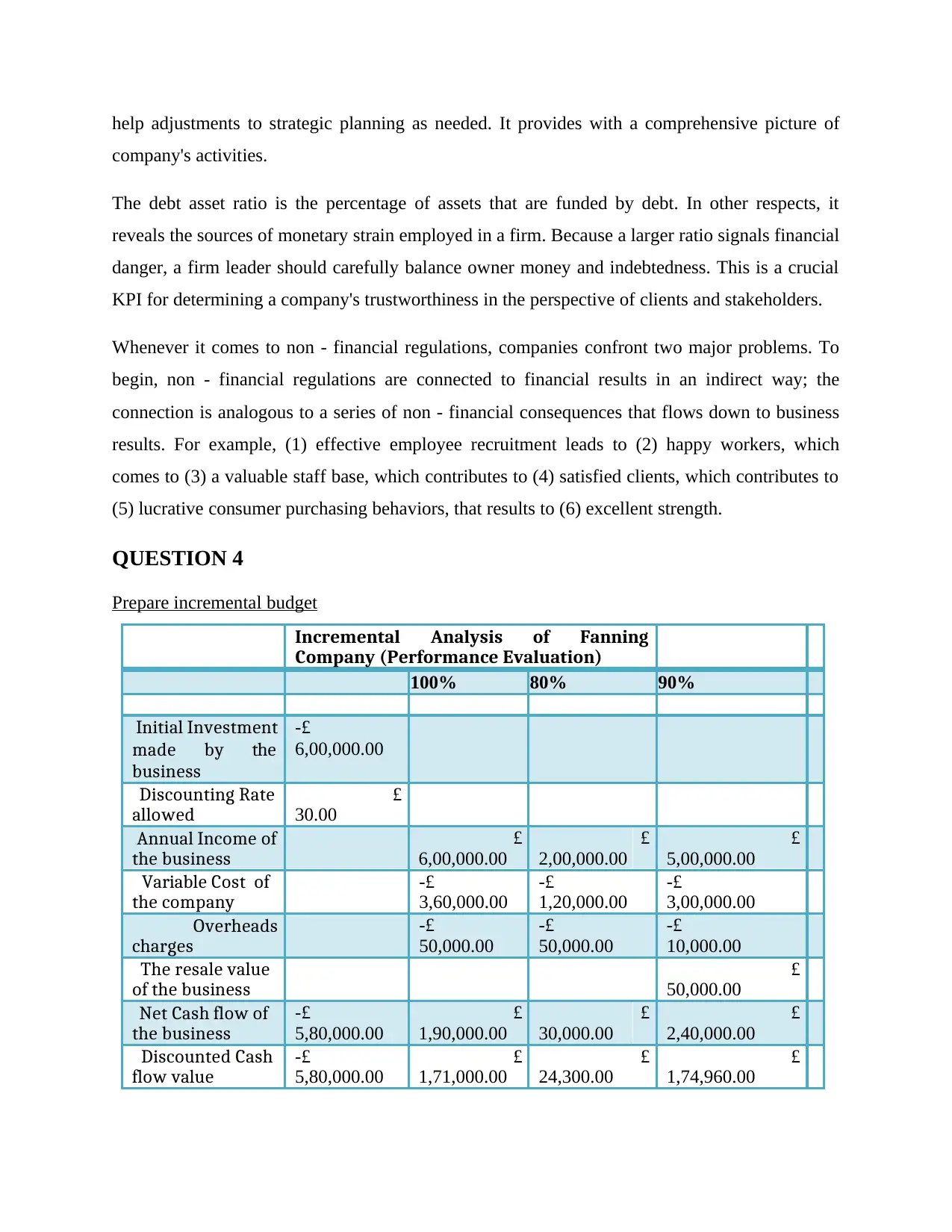

Explain the need for the measurement or company and department performance giving examples

of the range of financial & non-financial factors which impact the performance and

providing solutions to the factors mentioned.

Non financial factor: Non-financial KPIs aren't presented in money units other phrases; they're

not linked to dollar signs. They are generally leadership (forward-looking) indicators that focus

on other sectors of the economy, while financial KPIs are trailing measurements.

Enhance staff input on how to achieve specific priorities. Non-financial KPIs are particular,

quantifiable, and scale up to the group's big-picture plan when correctly established. Members of

the team can see specifically everything they need to accomplish to meet their objectives, as well

as why they ought to run the same analysis every week or how their participation rates slow

down the process. The everyday duties and future plan are inextricably linked.

Financial factors: Maintaining a frequent check on the economic condition of a firm is not only

important, but also vital. They establish a key performance metrics (KPIs) to track quality and

eliminating these constraints, operations may operate perfectly, efficiently, and cost-effectively.

Administrative coherence is required by ABB, which demands a holistic view of the company

centered on activities rather than specific divisions. This gives a more holistic feeling of financial

cohesion.

Disadvantage: Every action is researched, evaluated, and analysed separately by ABB, which

requires a lot of money and time. This type of investigation is time-consuming and expensive. It

takes time and money to accomplish, and management must have a thorough grasp of the many

aspects of the firm. Additionally, incorrectly doing ABB research can lead to budgeting errors,

which can be particularly troublesome for firms with little profit margin.

In many situations, ABB is also more concerned with the ability to pay short objectives.

That doesn't always take very long goals and budgets into account. In addition for ABB to

function successfully, it's critical to evaluate how each operation fits into the larger scope of the

company.

Explain the need for the measurement or company and department performance giving examples

of the range of financial & non-financial factors which impact the performance and

providing solutions to the factors mentioned.

Non financial factor: Non-financial KPIs aren't presented in money units other phrases; they're

not linked to dollar signs. They are generally leadership (forward-looking) indicators that focus

on other sectors of the economy, while financial KPIs are trailing measurements.

Enhance staff input on how to achieve specific priorities. Non-financial KPIs are particular,

quantifiable, and scale up to the group's big-picture plan when correctly established. Members of

the team can see specifically everything they need to accomplish to meet their objectives, as well

as why they ought to run the same analysis every week or how their participation rates slow

down the process. The everyday duties and future plan are inextricably linked.

Financial factors: Maintaining a frequent check on the economic condition of a firm is not only

important, but also vital. They establish a key performance metrics (KPIs) to track quality and

help adjustments to strategic planning as needed. It provides with a comprehensive picture of

company's activities.

The debt asset ratio is the percentage of assets that are funded by debt. In other respects, it

reveals the sources of monetary strain employed in a firm. Because a larger ratio signals financial

danger, a firm leader should carefully balance owner money and indebtedness. This is a crucial

KPI for determining a company's trustworthiness in the perspective of clients and stakeholders.

Whenever it comes to non - financial regulations, companies confront two major problems. To

begin, non - financial regulations are connected to financial results in an indirect way; the

connection is analogous to a series of non - financial consequences that flows down to business

results. For example, (1) effective employee recruitment leads to (2) happy workers, which

comes to (3) a valuable staff base, which contributes to (4) satisfied clients, which contributes to

(5) lucrative consumer purchasing behaviors, that results to (6) excellent strength.

QUESTION 4

Prepare incremental budget

Incremental Analysis of Fanning

Company (Performance Evaluation)

100% 80% 90%

Initial Investment

made by the

business

-£

6,00,000.00

Discounting Rate

allowed 30.00

£

Annual Income of

the business 6,00,000.00

£

2,00,000.00

£

5,00,000.00

£

Variable Cost of

the company

-£

3,60,000.00

-£

1,20,000.00

-£

3,00,000.00

Overheads

charges

-£

50,000.00

-£

50,000.00

-£

10,000.00

The resale value

of the business 50,000.00

£

Net Cash flow of

the business

-£

5,80,000.00 1,90,000.00

£

30,000.00

£

2,40,000.00

£

Discounted Cash

flow value

-£

5,80,000.00 1,71,000.00

£

24,300.00

£

1,74,960.00

£

company's activities.

The debt asset ratio is the percentage of assets that are funded by debt. In other respects, it

reveals the sources of monetary strain employed in a firm. Because a larger ratio signals financial

danger, a firm leader should carefully balance owner money and indebtedness. This is a crucial

KPI for determining a company's trustworthiness in the perspective of clients and stakeholders.

Whenever it comes to non - financial regulations, companies confront two major problems. To

begin, non - financial regulations are connected to financial results in an indirect way; the

connection is analogous to a series of non - financial consequences that flows down to business

results. For example, (1) effective employee recruitment leads to (2) happy workers, which

comes to (3) a valuable staff base, which contributes to (4) satisfied clients, which contributes to

(5) lucrative consumer purchasing behaviors, that results to (6) excellent strength.

QUESTION 4

Prepare incremental budget

Incremental Analysis of Fanning

Company (Performance Evaluation)

100% 80% 90%

Initial Investment

made by the

business

-£

6,00,000.00

Discounting Rate

allowed 30.00

£

Annual Income of

the business 6,00,000.00

£

2,00,000.00

£

5,00,000.00

£

Variable Cost of

the company

-£

3,60,000.00

-£

1,20,000.00

-£

3,00,000.00

Overheads

charges

-£

50,000.00

-£

50,000.00

-£

10,000.00

The resale value

of the business 50,000.00

£

Net Cash flow of

the business

-£

5,80,000.00 1,90,000.00

£

30,000.00

£

2,40,000.00

£

Discounted Cash

flow value

-£

5,80,000.00 1,71,000.00

£

24,300.00

£

1,74,960.00

£

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

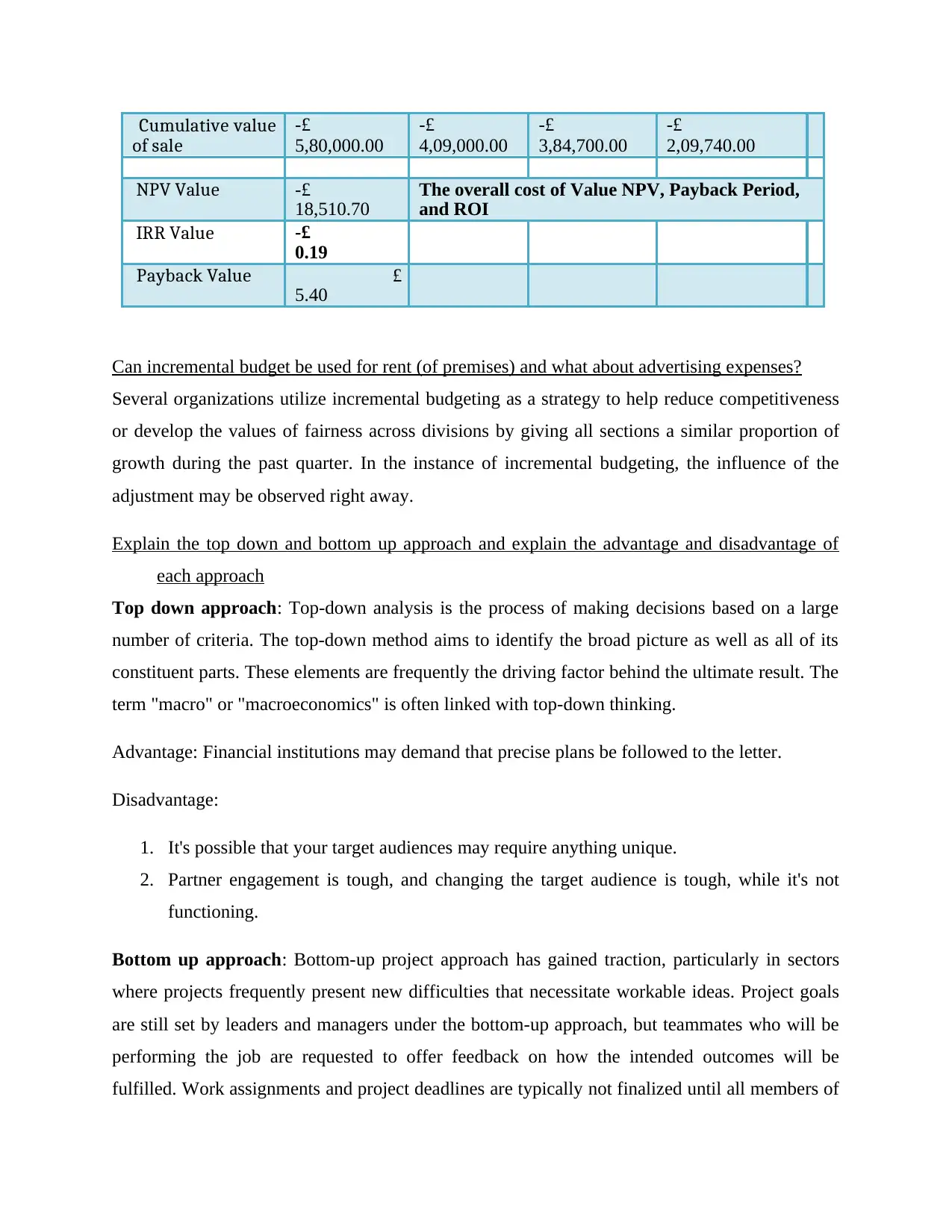

Cumulative value

of sale

-£

5,80,000.00

-£

4,09,000.00

-£

3,84,700.00

-£

2,09,740.00

NPV Value -£

18,510.70

The overall cost of Value NPV, Payback Period,

and ROI

IRR Value -£

0.19

Payback Value

5.40

£

Can incremental budget be used for rent (of premises) and what about advertising expenses?

Several organizations utilize incremental budgeting as a strategy to help reduce competitiveness

or develop the values of fairness across divisions by giving all sections a similar proportion of

growth during the past quarter. In the instance of incremental budgeting, the influence of the

adjustment may be observed right away.

Explain the top down and bottom up approach and explain the advantage and disadvantage of

each approach

Top down approach: Top-down analysis is the process of making decisions based on a large

number of criteria. The top-down method aims to identify the broad picture as well as all of its

constituent parts. These elements are frequently the driving factor behind the ultimate result. The

term "macro" or "macroeconomics" is often linked with top-down thinking.

Advantage: Financial institutions may demand that precise plans be followed to the letter.

Disadvantage:

1. It's possible that your target audiences may require anything unique.

2. Partner engagement is tough, and changing the target audience is tough, while it's not

functioning.

Bottom up approach: Bottom-up project approach has gained traction, particularly in sectors

where projects frequently present new difficulties that necessitate workable ideas. Project goals

are still set by leaders and managers under the bottom-up approach, but teammates who will be

performing the job are requested to offer feedback on how the intended outcomes will be

fulfilled. Work assignments and project deadlines are typically not finalized until all members of

of sale

-£

5,80,000.00

-£

4,09,000.00

-£

3,84,700.00

-£

2,09,740.00

NPV Value -£

18,510.70

The overall cost of Value NPV, Payback Period,

and ROI

IRR Value -£

0.19

Payback Value

5.40

£

Can incremental budget be used for rent (of premises) and what about advertising expenses?

Several organizations utilize incremental budgeting as a strategy to help reduce competitiveness

or develop the values of fairness across divisions by giving all sections a similar proportion of

growth during the past quarter. In the instance of incremental budgeting, the influence of the

adjustment may be observed right away.

Explain the top down and bottom up approach and explain the advantage and disadvantage of

each approach

Top down approach: Top-down analysis is the process of making decisions based on a large

number of criteria. The top-down method aims to identify the broad picture as well as all of its

constituent parts. These elements are frequently the driving factor behind the ultimate result. The

term "macro" or "macroeconomics" is often linked with top-down thinking.

Advantage: Financial institutions may demand that precise plans be followed to the letter.

Disadvantage:

1. It's possible that your target audiences may require anything unique.

2. Partner engagement is tough, and changing the target audience is tough, while it's not

functioning.

Bottom up approach: Bottom-up project approach has gained traction, particularly in sectors

where projects frequently present new difficulties that necessitate workable ideas. Project goals

are still set by leaders and managers under the bottom-up approach, but teammates who will be

performing the job are requested to offer feedback on how the intended outcomes will be

fulfilled. Work assignments and project deadlines are typically not finalized until all members of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the team have given their input, resulting in more reasonable timetables and less disappointments

down the track (Suprunova, 2018).

Advantage:

It's a lot simpler to attract colleagues and get things moving.

Simpler to connect intended audience faster to adjust to various requirements by using

‘free' resource via connecting

Networks of ‘natural' interaction

Disadvantage:

1. Connecting may be costly in terms of money and employee time per targeted party

member contacted.

2. They won't be able to maintain complete control if they allow members to engage and

impact on programme,

3. Making it harder to analyze and genuine in the eyes of funding organizations.

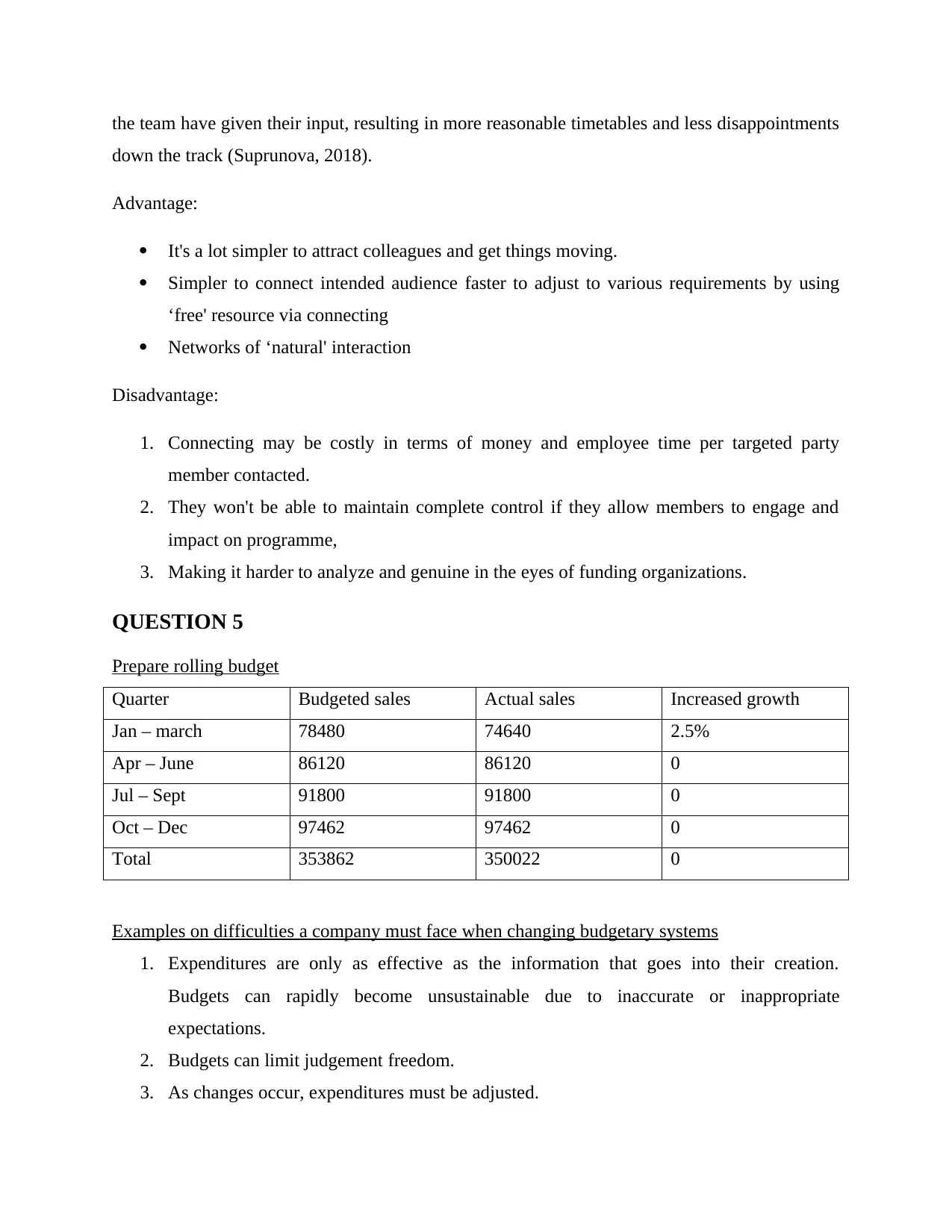

QUESTION 5

Prepare rolling budget

Quarter Budgeted sales Actual sales Increased growth

Jan – march 78480 74640 2.5%

Apr – June 86120 86120 0

Jul – Sept 91800 91800 0

Oct – Dec 97462 97462 0

Total 353862 350022 0

Examples on difficulties a company must face when changing budgetary systems

1. Expenditures are only as effective as the information that goes into their creation.

Budgets can rapidly become unsustainable due to inaccurate or inappropriate

expectations.

2. Budgets can limit judgement freedom.

3. As changes occur, expenditures must be adjusted.

down the track (Suprunova, 2018).

Advantage:

It's a lot simpler to attract colleagues and get things moving.

Simpler to connect intended audience faster to adjust to various requirements by using

‘free' resource via connecting

Networks of ‘natural' interaction

Disadvantage:

1. Connecting may be costly in terms of money and employee time per targeted party

member contacted.

2. They won't be able to maintain complete control if they allow members to engage and

impact on programme,

3. Making it harder to analyze and genuine in the eyes of funding organizations.

QUESTION 5

Prepare rolling budget

Quarter Budgeted sales Actual sales Increased growth

Jan – march 78480 74640 2.5%

Apr – June 86120 86120 0

Jul – Sept 91800 91800 0

Oct – Dec 97462 97462 0

Total 353862 350022 0

Examples on difficulties a company must face when changing budgetary systems

1. Expenditures are only as effective as the information that goes into their creation.

Budgets can rapidly become unsustainable due to inaccurate or inappropriate

expectations.

2. Budgets can limit judgement freedom.

3. As changes occur, expenditures must be adjusted.

4. Budgeting is a day when procedure; in large corporations, whole divisions may be

devoted to planning and management.

5. Budgets might lead to rash short-term judgments in order to stay inside the cost instead of

making the best long-term option that goes beyond the budget.

6. Managers might become obsessed with creating and evaluating budgets, losing sight of

the actual challenges of gaining consumers (Rajagukguk, 2018).

devoted to planning and management.

5. Budgets might lead to rash short-term judgments in order to stay inside the cost instead of

making the best long-term option that goes beyond the budget.

6. Managers might become obsessed with creating and evaluating budgets, losing sight of

the actual challenges of gaining consumers (Rajagukguk, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.