Comprehensive Report: Budgeting Techniques and Business Finance

VerifiedAdded on 2020/01/15

|12

|3743

|150

Report

AI Summary

This report delves into the significance of budgeting as a crucial tool for controlling expenses and measuring performance in the business environment. It explores the purpose of budgets, emphasizing their roles in planning, coordination, motivation, control, and evaluation. The report provides detailed calculations and interpretations of cash, sales, and production budgets, illustrating their practical application. It further discusses the relevance of traditional budgeting systems in dynamic business environments and analyzes alternative budgeting techniques, including zero-based and rolling budgeting, highlighting their advantages, disadvantages, and industry applications. The report provides a comprehensive overview of budgeting practices and their impact on financial management.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INDEX OF TABLES

Table 1: Cash budget.......................................................................................................................5

Table 2: Calculation for sales budget...............................................................................................5

Table 3: Production budget..............................................................................................................6

Table 1: Cash budget.......................................................................................................................5

Table 2: Calculation for sales budget...............................................................................................5

Table 3: Production budget..............................................................................................................6

INTRODUCTION

In today era, budget is used as an important tool in controlling expenses and performance

measurement. Without using this tool it is not possible to control cost. In this report purpose due

to which budget is used is described in detail. Along with this role of budget in cost control and

coordination among departments is also explained in detail. After that various budgets like cash,

sales and production budget are calculated and mad available in the report. Along with this there

results are also interpreted in the report. After that brief discussion is carried out on relevance of

traditional budget system to the dynamic business environment. At the end of the report various

budgeting techniques are discussed in detail. These techniques are activity based and rolling

budgeting. Along with their advantages and disadvantages are also described in detail. Finally,

industry in which these techniques are used is also mentioned in the report.

TASK 1

Purpose of budget

In business, lots of operations are performed and for that, money is required. But this

resource cannot be arranged overnight at an exact value. For this, estimation of funds

requirement is necessary. This estimation can be made by envisaging cash inflows and outflows.

On the basis of this estimation for appropriate sources, funds can be raised. These estimations are

prepared in the form of budget. Purpose of budgets is given as below:

Planning- In budget, cash inflows and outflows are determined. On the basis of cash

outflow, value resources required to perform a specific task is determined (Benavides and

Chapman, 2005). Here, planning is required and under this, allocation of entire cash outflow is

done in the proportion among various resources. For example, Aquapet wants to open new

business and for this, it prepares a budget in which there is a head land. This is an aggregate

amount and for acquisition of land, purchase will be made and legal fee will be paid. Thus,

budgeted amount in specific proportion will be divided among land purchase value and legal

charges.

Coordination- Budget promotes coordination among several departments. Finance

department has to divide entire budget among various departments. All these departments make

an attempt to perform their activities in a budgeted amount (Shapiro, 2005). Activities of all

departments are interlinked to each other. Hence, in order to make expenses within a set limit by

In today era, budget is used as an important tool in controlling expenses and performance

measurement. Without using this tool it is not possible to control cost. In this report purpose due

to which budget is used is described in detail. Along with this role of budget in cost control and

coordination among departments is also explained in detail. After that various budgets like cash,

sales and production budget are calculated and mad available in the report. Along with this there

results are also interpreted in the report. After that brief discussion is carried out on relevance of

traditional budget system to the dynamic business environment. At the end of the report various

budgeting techniques are discussed in detail. These techniques are activity based and rolling

budgeting. Along with their advantages and disadvantages are also described in detail. Finally,

industry in which these techniques are used is also mentioned in the report.

TASK 1

Purpose of budget

In business, lots of operations are performed and for that, money is required. But this

resource cannot be arranged overnight at an exact value. For this, estimation of funds

requirement is necessary. This estimation can be made by envisaging cash inflows and outflows.

On the basis of this estimation for appropriate sources, funds can be raised. These estimations are

prepared in the form of budget. Purpose of budgets is given as below:

Planning- In budget, cash inflows and outflows are determined. On the basis of cash

outflow, value resources required to perform a specific task is determined (Benavides and

Chapman, 2005). Here, planning is required and under this, allocation of entire cash outflow is

done in the proportion among various resources. For example, Aquapet wants to open new

business and for this, it prepares a budget in which there is a head land. This is an aggregate

amount and for acquisition of land, purchase will be made and legal fee will be paid. Thus,

budgeted amount in specific proportion will be divided among land purchase value and legal

charges.

Coordination- Budget promotes coordination among several departments. Finance

department has to divide entire budget among various departments. All these departments make

an attempt to perform their activities in a budgeted amount (Shapiro, 2005). Activities of all

departments are interlinked to each other. Hence, in order to make expenses within a set limit by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the budget, all departments cooperate with each other. This promotes coordination between

them.

Motivation- In budget, target is determined for the departments. For managers, it is

always a challenging task to keep expenses below the budgeted value. This challenging factor

motivates them to made extra efforts and tactics at the workplace that generate economies of

scale. Hence, it is an important motivating tool that is used by the managers in business.

Control- The main purpose of budget is to control expenses and to prevent the situation

of extravagance (Berger and Black, 2011). By doing this, employees help management in

fulfilling their objective of profit maximization. Hence, it is a great motivating and controlling

tool that is used by the managers in the present era.

Evaluation- Evaluating a business performance and its direction is another purpose of

budget (Peirson and et.al, 2014). By comparing actual performance with the budgeted figures,

company’s performance is evaluated and it is determined that whether organization is going in

the right direction or not. Hence, if it is find out that company is not performing well then by

taking immediate action, firm’s performance can be improved.

Role of budget/ budget process

Following are the roles of process of budget: Determination of standard- In this stage, standards are determined which will be used in

the later stage to check whether company is performing well or not (Bierman and Smidt,

2012). This stage plays a key role in the entire control process because this is the only

component of the budget that is used to evaluate company’s performance. These

standards are determined by considering lots of factors like economic condition of the

country and firm’s previous budgets and performance regarding the same. Hence, this

stage plays a key role in making cost control attempts of the managers to be successful at

the workplace. Measurement of performance- In this stage, performance is measured in terms of units

and values. Measurement of performance is done by the specially appointed employees.

Hence, firm needs to make sure that only efficient employees are selected for this task.

Control- In this stage, actual results are compared with the budgeted figures. By doing

this, deviation in performance is identified (Midgley and Burns, 2011). If performance is

in line to expectation then there is no issue. But if inverse happens then corrective actions

them.

Motivation- In budget, target is determined for the departments. For managers, it is

always a challenging task to keep expenses below the budgeted value. This challenging factor

motivates them to made extra efforts and tactics at the workplace that generate economies of

scale. Hence, it is an important motivating tool that is used by the managers in business.

Control- The main purpose of budget is to control expenses and to prevent the situation

of extravagance (Berger and Black, 2011). By doing this, employees help management in

fulfilling their objective of profit maximization. Hence, it is a great motivating and controlling

tool that is used by the managers in the present era.

Evaluation- Evaluating a business performance and its direction is another purpose of

budget (Peirson and et.al, 2014). By comparing actual performance with the budgeted figures,

company’s performance is evaluated and it is determined that whether organization is going in

the right direction or not. Hence, if it is find out that company is not performing well then by

taking immediate action, firm’s performance can be improved.

Role of budget/ budget process

Following are the roles of process of budget: Determination of standard- In this stage, standards are determined which will be used in

the later stage to check whether company is performing well or not (Bierman and Smidt,

2012). This stage plays a key role in the entire control process because this is the only

component of the budget that is used to evaluate company’s performance. These

standards are determined by considering lots of factors like economic condition of the

country and firm’s previous budgets and performance regarding the same. Hence, this

stage plays a key role in making cost control attempts of the managers to be successful at

the workplace. Measurement of performance- In this stage, performance is measured in terms of units

and values. Measurement of performance is done by the specially appointed employees.

Hence, firm needs to make sure that only efficient employees are selected for this task.

Control- In this stage, actual results are compared with the budgeted figures. By doing

this, deviation in performance is identified (Midgley and Burns, 2011). If performance is

in line to expectation then there is no issue. But if inverse happens then corrective actions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are taken to improve the firm’s performance. Hence, budget plays a great role in

improving the management of activities in an organization.

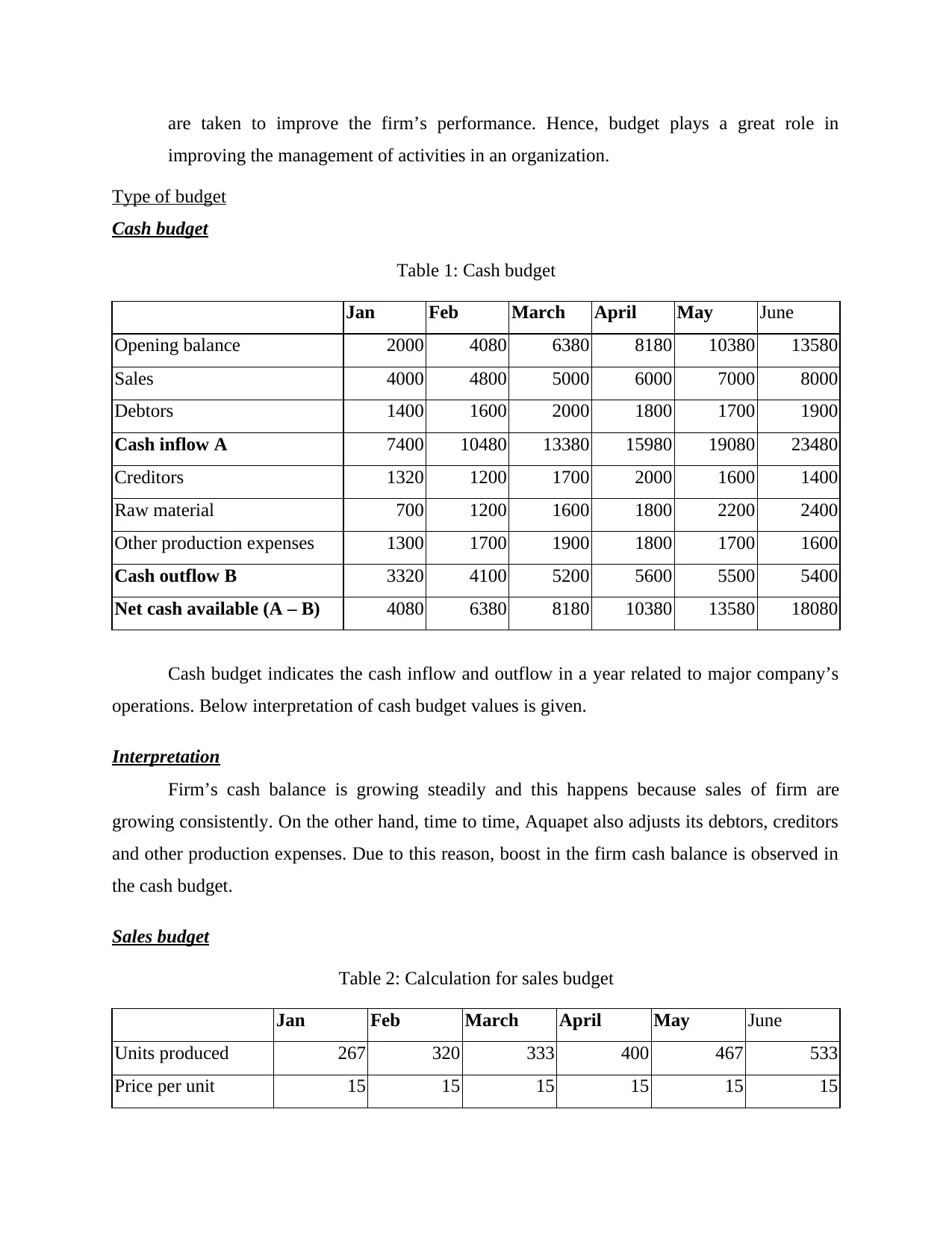

Type of budget

Cash budget

Table 1: Cash budget

Jan Feb March April May June

Opening balance 2000 4080 6380 8180 10380 13580

Sales 4000 4800 5000 6000 7000 8000

Debtors 1400 1600 2000 1800 1700 1900

Cash inflow A 7400 10480 13380 15980 19080 23480

Creditors 1320 1200 1700 2000 1600 1400

Raw material 700 1200 1600 1800 2200 2400

Other production expenses 1300 1700 1900 1800 1700 1600

Cash outflow B 3320 4100 5200 5600 5500 5400

Net cash available (A – B) 4080 6380 8180 10380 13580 18080

Cash budget indicates the cash inflow and outflow in a year related to major company’s

operations. Below interpretation of cash budget values is given.

Interpretation

Firm’s cash balance is growing steadily and this happens because sales of firm are

growing consistently. On the other hand, time to time, Aquapet also adjusts its debtors, creditors

and other production expenses. Due to this reason, boost in the firm cash balance is observed in

the cash budget.

Sales budget

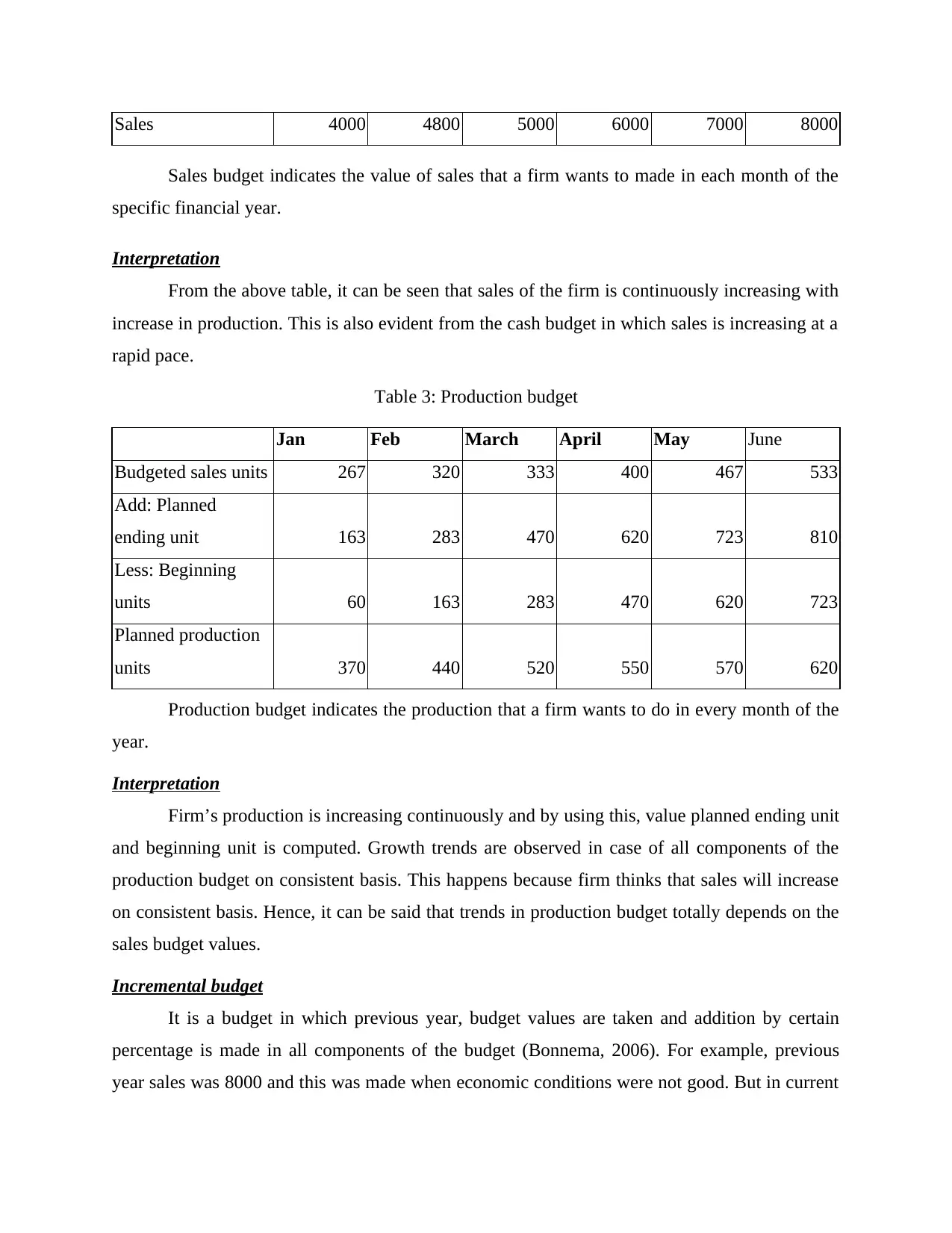

Table 2: Calculation for sales budget

Jan Feb March April May June

Units produced 267 320 333 400 467 533

Price per unit 15 15 15 15 15 15

improving the management of activities in an organization.

Type of budget

Cash budget

Table 1: Cash budget

Jan Feb March April May June

Opening balance 2000 4080 6380 8180 10380 13580

Sales 4000 4800 5000 6000 7000 8000

Debtors 1400 1600 2000 1800 1700 1900

Cash inflow A 7400 10480 13380 15980 19080 23480

Creditors 1320 1200 1700 2000 1600 1400

Raw material 700 1200 1600 1800 2200 2400

Other production expenses 1300 1700 1900 1800 1700 1600

Cash outflow B 3320 4100 5200 5600 5500 5400

Net cash available (A – B) 4080 6380 8180 10380 13580 18080

Cash budget indicates the cash inflow and outflow in a year related to major company’s

operations. Below interpretation of cash budget values is given.

Interpretation

Firm’s cash balance is growing steadily and this happens because sales of firm are

growing consistently. On the other hand, time to time, Aquapet also adjusts its debtors, creditors

and other production expenses. Due to this reason, boost in the firm cash balance is observed in

the cash budget.

Sales budget

Table 2: Calculation for sales budget

Jan Feb March April May June

Units produced 267 320 333 400 467 533

Price per unit 15 15 15 15 15 15

Sales 4000 4800 5000 6000 7000 8000

Sales budget indicates the value of sales that a firm wants to made in each month of the

specific financial year.

Interpretation

From the above table, it can be seen that sales of the firm is continuously increasing with

increase in production. This is also evident from the cash budget in which sales is increasing at a

rapid pace.

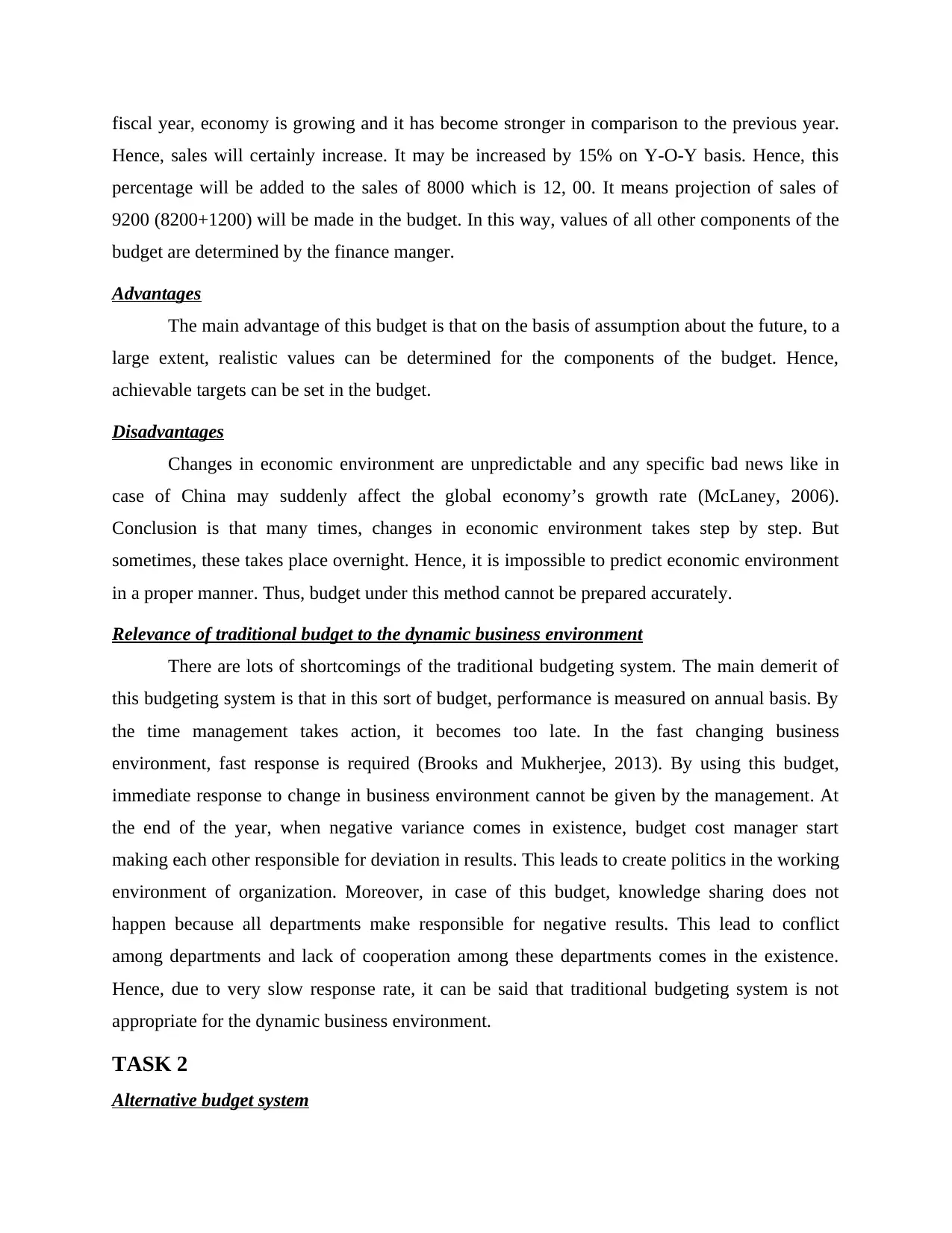

Table 3: Production budget

Jan Feb March April May June

Budgeted sales units 267 320 333 400 467 533

Add: Planned

ending unit 163 283 470 620 723 810

Less: Beginning

units 60 163 283 470 620 723

Planned production

units 370 440 520 550 570 620

Production budget indicates the production that a firm wants to do in every month of the

year.

Interpretation

Firm’s production is increasing continuously and by using this, value planned ending unit

and beginning unit is computed. Growth trends are observed in case of all components of the

production budget on consistent basis. This happens because firm thinks that sales will increase

on consistent basis. Hence, it can be said that trends in production budget totally depends on the

sales budget values.

Incremental budget

It is a budget in which previous year, budget values are taken and addition by certain

percentage is made in all components of the budget (Bonnema, 2006). For example, previous

year sales was 8000 and this was made when economic conditions were not good. But in current

Sales budget indicates the value of sales that a firm wants to made in each month of the

specific financial year.

Interpretation

From the above table, it can be seen that sales of the firm is continuously increasing with

increase in production. This is also evident from the cash budget in which sales is increasing at a

rapid pace.

Table 3: Production budget

Jan Feb March April May June

Budgeted sales units 267 320 333 400 467 533

Add: Planned

ending unit 163 283 470 620 723 810

Less: Beginning

units 60 163 283 470 620 723

Planned production

units 370 440 520 550 570 620

Production budget indicates the production that a firm wants to do in every month of the

year.

Interpretation

Firm’s production is increasing continuously and by using this, value planned ending unit

and beginning unit is computed. Growth trends are observed in case of all components of the

production budget on consistent basis. This happens because firm thinks that sales will increase

on consistent basis. Hence, it can be said that trends in production budget totally depends on the

sales budget values.

Incremental budget

It is a budget in which previous year, budget values are taken and addition by certain

percentage is made in all components of the budget (Bonnema, 2006). For example, previous

year sales was 8000 and this was made when economic conditions were not good. But in current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fiscal year, economy is growing and it has become stronger in comparison to the previous year.

Hence, sales will certainly increase. It may be increased by 15% on Y-O-Y basis. Hence, this

percentage will be added to the sales of 8000 which is 12, 00. It means projection of sales of

9200 (8200+1200) will be made in the budget. In this way, values of all other components of the

budget are determined by the finance manger.

Advantages

The main advantage of this budget is that on the basis of assumption about the future, to a

large extent, realistic values can be determined for the components of the budget. Hence,

achievable targets can be set in the budget.

Disadvantages

Changes in economic environment are unpredictable and any specific bad news like in

case of China may suddenly affect the global economy’s growth rate (McLaney, 2006).

Conclusion is that many times, changes in economic environment takes step by step. But

sometimes, these takes place overnight. Hence, it is impossible to predict economic environment

in a proper manner. Thus, budget under this method cannot be prepared accurately.

Relevance of traditional budget to the dynamic business environment

There are lots of shortcomings of the traditional budgeting system. The main demerit of

this budgeting system is that in this sort of budget, performance is measured on annual basis. By

the time management takes action, it becomes too late. In the fast changing business

environment, fast response is required (Brooks and Mukherjee, 2013). By using this budget,

immediate response to change in business environment cannot be given by the management. At

the end of the year, when negative variance comes in existence, budget cost manager start

making each other responsible for deviation in results. This leads to create politics in the working

environment of organization. Moreover, in case of this budget, knowledge sharing does not

happen because all departments make responsible for negative results. This lead to conflict

among departments and lack of cooperation among these departments comes in the existence.

Hence, due to very slow response rate, it can be said that traditional budgeting system is not

appropriate for the dynamic business environment.

TASK 2

Alternative budget system

Hence, sales will certainly increase. It may be increased by 15% on Y-O-Y basis. Hence, this

percentage will be added to the sales of 8000 which is 12, 00. It means projection of sales of

9200 (8200+1200) will be made in the budget. In this way, values of all other components of the

budget are determined by the finance manger.

Advantages

The main advantage of this budget is that on the basis of assumption about the future, to a

large extent, realistic values can be determined for the components of the budget. Hence,

achievable targets can be set in the budget.

Disadvantages

Changes in economic environment are unpredictable and any specific bad news like in

case of China may suddenly affect the global economy’s growth rate (McLaney, 2006).

Conclusion is that many times, changes in economic environment takes step by step. But

sometimes, these takes place overnight. Hence, it is impossible to predict economic environment

in a proper manner. Thus, budget under this method cannot be prepared accurately.

Relevance of traditional budget to the dynamic business environment

There are lots of shortcomings of the traditional budgeting system. The main demerit of

this budgeting system is that in this sort of budget, performance is measured on annual basis. By

the time management takes action, it becomes too late. In the fast changing business

environment, fast response is required (Brooks and Mukherjee, 2013). By using this budget,

immediate response to change in business environment cannot be given by the management. At

the end of the year, when negative variance comes in existence, budget cost manager start

making each other responsible for deviation in results. This leads to create politics in the working

environment of organization. Moreover, in case of this budget, knowledge sharing does not

happen because all departments make responsible for negative results. This lead to conflict

among departments and lack of cooperation among these departments comes in the existence.

Hence, due to very slow response rate, it can be said that traditional budgeting system is not

appropriate for the dynamic business environment.

TASK 2

Alternative budget system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Alternative budget system is a process in which company uses various types of budgeting

methods in order to determine the various activities which are performed by in the functional

areas of the organization (Caceres and et.al, 2007). Under this system there are normally three

types of budgeting techniques which are used by the different in order to prepare various budgets

(i.e. Zero based budgeting, Activity based budgeting an Rolling budgeting). These budgets are

also used by the company to manage all its activities. And at the same time it is also used to

compare the various month budgets with that of next month. Thus, at least one budgeting method

is used by every organization to manage its activities.

Zero based budgeting

It is a method of budgeting in which each and every department of an organization needs

to determine an activity which will be performed in its functional area (Eiteman, Stonehill, and

Moffett, 2007). Along with this, these departments also need to provide information about the

resources that they will need in order to perform their department operations. Until this

information is not provided to the department’s budget of the specific department will be zero.

Due to this reason this budgeting technique is known as zero based budgeting. There are several

advantages and disadvantages of this technique and some of them are as follows.

Advantages

In zero based budgeting previous year resource allocations is not taken in to account

because with change in year level of operations of the departments also get changed (Chen,

Ctory budget system). Due to this reason whatever allocation was done in previous year not used

for preparing a budget for current year. This is main advantage of this technique.

Disadvantages

Many times department managers do not have proper knowledge about the resource

requirements of their departments (Udell, 2009). Due to this reason they provide wrong

information to prepare a budget. Due to this reason appropriate allocation of funds does not takes

place among various departments. Hence, it is a major disadvantage of zero based budgeting.

Used in

Zero based budgeting is used in hospitality industry. Because in this method of budgeting each

and every department need to define the various activities performed by all departments

(Eiteman, Stonehill and Moffett, 2007). This method is used in hospitality industry in order to

properly allocate the available resources to each and every department to achieve the desired

methods in order to determine the various activities which are performed by in the functional

areas of the organization (Caceres and et.al, 2007). Under this system there are normally three

types of budgeting techniques which are used by the different in order to prepare various budgets

(i.e. Zero based budgeting, Activity based budgeting an Rolling budgeting). These budgets are

also used by the company to manage all its activities. And at the same time it is also used to

compare the various month budgets with that of next month. Thus, at least one budgeting method

is used by every organization to manage its activities.

Zero based budgeting

It is a method of budgeting in which each and every department of an organization needs

to determine an activity which will be performed in its functional area (Eiteman, Stonehill, and

Moffett, 2007). Along with this, these departments also need to provide information about the

resources that they will need in order to perform their department operations. Until this

information is not provided to the department’s budget of the specific department will be zero.

Due to this reason this budgeting technique is known as zero based budgeting. There are several

advantages and disadvantages of this technique and some of them are as follows.

Advantages

In zero based budgeting previous year resource allocations is not taken in to account

because with change in year level of operations of the departments also get changed (Chen,

Ctory budget system). Due to this reason whatever allocation was done in previous year not used

for preparing a budget for current year. This is main advantage of this technique.

Disadvantages

Many times department managers do not have proper knowledge about the resource

requirements of their departments (Udell, 2009). Due to this reason they provide wrong

information to prepare a budget. Due to this reason appropriate allocation of funds does not takes

place among various departments. Hence, it is a major disadvantage of zero based budgeting.

Used in

Zero based budgeting is used in hospitality industry. Because in this method of budgeting each

and every department need to define the various activities performed by all departments

(Eiteman, Stonehill and Moffett, 2007). This method is used in hospitality industry in order to

properly allocate the available resources to each and every department to achieve the desired

target. Use of this method of budgeting is used in hospitality industry because high rate of

management is required in this industry only.

Activity based budgeting

Under this method on the basis of activity budget is prepared. Means that first of all

information about activities that will be performed in an organization is determined. After that

cost drivers are determined (Fielden, Dawe and Woolnough, 2006). Under this cost in units that

will be incurred to perform an activity is determined by the management. There are various

advantages and disadvantages of activity based costing. Some of them are described below.

Advantages

The main advantage of activity based budgeting is that is that it draw attention of

management towards activity and costs that are related to them (Fölscher, 2007). This concept

state that cost can be controlled if volume of activity is controlled. On other hand, this technique

gives an overview of all activities and cost that are incurred to produce products. Hence,

management can identify costs that can be reduced. Thus, this technique helps in generating

economies of scale for the firm.

Disadvantages

With change in business conditions cost of production also get changed. Hence, when

budget is prepared m manager needs to make huge efforts in identifying activities and cost

drivers. In many Companies materials like zinc, lead and aluminum are used (Gordon and Loeb,

2006). These are those materials whose value keeps on changing with change in the economic

conditions of major developed and developing economies. Hence, it is very difficult to determine

cost for each activity in upcoming months. Thus, values of activities may prove unrealistic in

future. This problem is a major limitation of Activity based budgeting.

Used in

Activity based budgeting is used in mining industry (Hope and Fraser, 2013). In this method of

budgeting all the information related to the various activities are determined in order to decide

which cost drive will be best to use. Thus, this method is used in mining industry to in order to

manage all the activities which are going to be performed in advance. Use of various cost drivers

aid the industries to easily analyses the availability of different types of resources.

Rolling budgeting

management is required in this industry only.

Activity based budgeting

Under this method on the basis of activity budget is prepared. Means that first of all

information about activities that will be performed in an organization is determined. After that

cost drivers are determined (Fielden, Dawe and Woolnough, 2006). Under this cost in units that

will be incurred to perform an activity is determined by the management. There are various

advantages and disadvantages of activity based costing. Some of them are described below.

Advantages

The main advantage of activity based budgeting is that is that it draw attention of

management towards activity and costs that are related to them (Fölscher, 2007). This concept

state that cost can be controlled if volume of activity is controlled. On other hand, this technique

gives an overview of all activities and cost that are incurred to produce products. Hence,

management can identify costs that can be reduced. Thus, this technique helps in generating

economies of scale for the firm.

Disadvantages

With change in business conditions cost of production also get changed. Hence, when

budget is prepared m manager needs to make huge efforts in identifying activities and cost

drivers. In many Companies materials like zinc, lead and aluminum are used (Gordon and Loeb,

2006). These are those materials whose value keeps on changing with change in the economic

conditions of major developed and developing economies. Hence, it is very difficult to determine

cost for each activity in upcoming months. Thus, values of activities may prove unrealistic in

future. This problem is a major limitation of Activity based budgeting.

Used in

Activity based budgeting is used in mining industry (Hope and Fraser, 2013). In this method of

budgeting all the information related to the various activities are determined in order to decide

which cost drive will be best to use. Thus, this method is used in mining industry to in order to

manage all the activities which are going to be performed in advance. Use of various cost drivers

aid the industries to easily analyses the availability of different types of resources.

Rolling budgeting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under this budget a firm follows a cautious approach. In this method of budgeting

increment is made to the previous budget values frequently (Kaplan and IQ Consulting, 2006).

Means that in order to prepare budget for the month of February managers will take budget of

January month. They will make increase in the components of the budget as per change in the

business environment in the month of February. Following are the advantages and disadvantage

of this budgeting technique.

Advantages

The main advantage of this budget is that with change in business conditions immediately

changes can be made in the budget. In other words, it can be said that by using this budget action

can be taken on time and as per change in situation budget can be update (Lee, Johnson, and

Joyce, 2012). This budget also prevent clash between management and employees. Normally,

management held employees responsible for negative deviation in the budget figures. But in this

technique this problem is completely eliminated. With change in business conditions if cost

increases then managers easily cannot make employees responsible for deviation in the budget

values. This is because this deviation may happen due to their wrong forecasting done by the

managers about the change in the business environment. Hence, managers cannot easily prove

employees culprit for non achievement of budget objectives.

Disadvantages

In case of rolling budget new budget is created every time. In this economic factors are

considered for determining values of the components of the budget (Linn, 2007). Hence, for

preparing rolling budget in proper manner a set of skilled analysts is required by a firm. For

employing such kind of employee firm will need to pay heavy amount and this will elevate firm

employee cost. So, this is major limitation of rolling budget.

CONCLUSION

On the basis of above discussion it is concluded that use of budget is very important for

the business organizations. Without it is not possible to control cost of production. But there are

many serious issues with preparation of budget and estimation of figures of budget is one of

them. Hence, due care must be taken while preparing estimates for the budget. For this a

procedure can be prepared under which budget will be reviewed by the multiple managers. This

will ensure that perfect estimates are made in the budget. Each budget technique has some merits

and limitations. So, there are numerous factors with which manager requires to deal while

increment is made to the previous budget values frequently (Kaplan and IQ Consulting, 2006).

Means that in order to prepare budget for the month of February managers will take budget of

January month. They will make increase in the components of the budget as per change in the

business environment in the month of February. Following are the advantages and disadvantage

of this budgeting technique.

Advantages

The main advantage of this budget is that with change in business conditions immediately

changes can be made in the budget. In other words, it can be said that by using this budget action

can be taken on time and as per change in situation budget can be update (Lee, Johnson, and

Joyce, 2012). This budget also prevent clash between management and employees. Normally,

management held employees responsible for negative deviation in the budget figures. But in this

technique this problem is completely eliminated. With change in business conditions if cost

increases then managers easily cannot make employees responsible for deviation in the budget

values. This is because this deviation may happen due to their wrong forecasting done by the

managers about the change in the business environment. Hence, managers cannot easily prove

employees culprit for non achievement of budget objectives.

Disadvantages

In case of rolling budget new budget is created every time. In this economic factors are

considered for determining values of the components of the budget (Linn, 2007). Hence, for

preparing rolling budget in proper manner a set of skilled analysts is required by a firm. For

employing such kind of employee firm will need to pay heavy amount and this will elevate firm

employee cost. So, this is major limitation of rolling budget.

CONCLUSION

On the basis of above discussion it is concluded that use of budget is very important for

the business organizations. Without it is not possible to control cost of production. But there are

many serious issues with preparation of budget and estimation of figures of budget is one of

them. Hence, due care must be taken while preparing estimates for the budget. For this a

procedure can be prepared under which budget will be reviewed by the multiple managers. This

will ensure that perfect estimates are made in the budget. Each budget technique has some merits

and limitations. So, there are numerous factors with which manager requires to deal while

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

preparing budget and they must with due attention must prepare a budget. On front of selection

of budget technique managers with due care must select an appropriate budget technique.

of budget technique managers with due care must select an appropriate budget technique.

References

Benavides, N.D. and Chapman, P.L., 2005. Power budgeting of a multiple-input buck-boost

converter. Power Electronics, IEEE Transactions on. 20(6). pp.1303-1309.

Berger, A.N. and Black, L.K., 2011. Bank size, lending technologies, and small business

finance. Journal of Banking & Finance. 35(3). pp.724-735.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Bonnema, M., 2006. Function and budget based system architecting..H. and Yucesan, E., 2005.

An alternative simulation budget allocation scheme for efficient simulation. International

Journal of Simulation and Process Modelling. 1(1-2). pp.49-57.

Brooks, R. and Mukherjee, A.K., 2013. Financial management: core concepts. Pearson.

Caceres, P. and et.al., 2007. Improving usability in e-democracy systems: systematic

development of navigation in an e-participatory budget system. International Journal of

Technology, Policy and Management. 7(2). pp.151-166.

Chen, Ctory budget system. International Journal of Technology, Policy and Management. 7(2).

pp.151-166.

Eiteman, D.K., Stonehill, A.I. and Moffett, M.H., 2007. Multinational business finance.

Pearson/Addison-Wesley.

Fielden, S.L., Dawe, A.J. and Woolnough, H., 2006. UK government small business finance

initiatives: Social inclusion or gender discrimination?. Equal Opportunities International.

25(1). pp.25-37.

Fölscher, A., 2007. Budget Methods and Practices‖. Budgeting and budgetary institutions.

Fölscher, A., 2007. Budget Methods and Practices‖. Budgeting and budgetary institutions.

Gordon, L.A. and Loeb, M.P., 2006. Budgeting process for information security expenditures.

Communications of the ACM. 49(1). pp.121-125.

Hope, J. and Fraser, R., 2013. Beyond budgeting: how managers can break free from the annual

performance trap. Harvard Business Press.

Kaplan, C.A., IQ Consulting, Inc., 2006. Method and system for asynchronous online distributed

problem solving including problems in education, business, finance, and technology. U.S.

Patent 7, 155,157.

Benavides, N.D. and Chapman, P.L., 2005. Power budgeting of a multiple-input buck-boost

converter. Power Electronics, IEEE Transactions on. 20(6). pp.1303-1309.

Berger, A.N. and Black, L.K., 2011. Bank size, lending technologies, and small business

finance. Journal of Banking & Finance. 35(3). pp.724-735.

Bierman Jr, H. and Smidt, S., 2012. The capital budgeting decision: economic analysis of

investment projects. Routledge.

Bonnema, M., 2006. Function and budget based system architecting..H. and Yucesan, E., 2005.

An alternative simulation budget allocation scheme for efficient simulation. International

Journal of Simulation and Process Modelling. 1(1-2). pp.49-57.

Brooks, R. and Mukherjee, A.K., 2013. Financial management: core concepts. Pearson.

Caceres, P. and et.al., 2007. Improving usability in e-democracy systems: systematic

development of navigation in an e-participatory budget system. International Journal of

Technology, Policy and Management. 7(2). pp.151-166.

Chen, Ctory budget system. International Journal of Technology, Policy and Management. 7(2).

pp.151-166.

Eiteman, D.K., Stonehill, A.I. and Moffett, M.H., 2007. Multinational business finance.

Pearson/Addison-Wesley.

Fielden, S.L., Dawe, A.J. and Woolnough, H., 2006. UK government small business finance

initiatives: Social inclusion or gender discrimination?. Equal Opportunities International.

25(1). pp.25-37.

Fölscher, A., 2007. Budget Methods and Practices‖. Budgeting and budgetary institutions.

Fölscher, A., 2007. Budget Methods and Practices‖. Budgeting and budgetary institutions.

Gordon, L.A. and Loeb, M.P., 2006. Budgeting process for information security expenditures.

Communications of the ACM. 49(1). pp.121-125.

Hope, J. and Fraser, R., 2013. Beyond budgeting: how managers can break free from the annual

performance trap. Harvard Business Press.

Kaplan, C.A., IQ Consulting, Inc., 2006. Method and system for asynchronous online distributed

problem solving including problems in education, business, finance, and technology. U.S.

Patent 7, 155,157.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.