Budgeting and Variance Analysis Report for Fleet Highlands Cafe

VerifiedAdded on 2023/01/11

|7

|1837

|50

Report

AI Summary

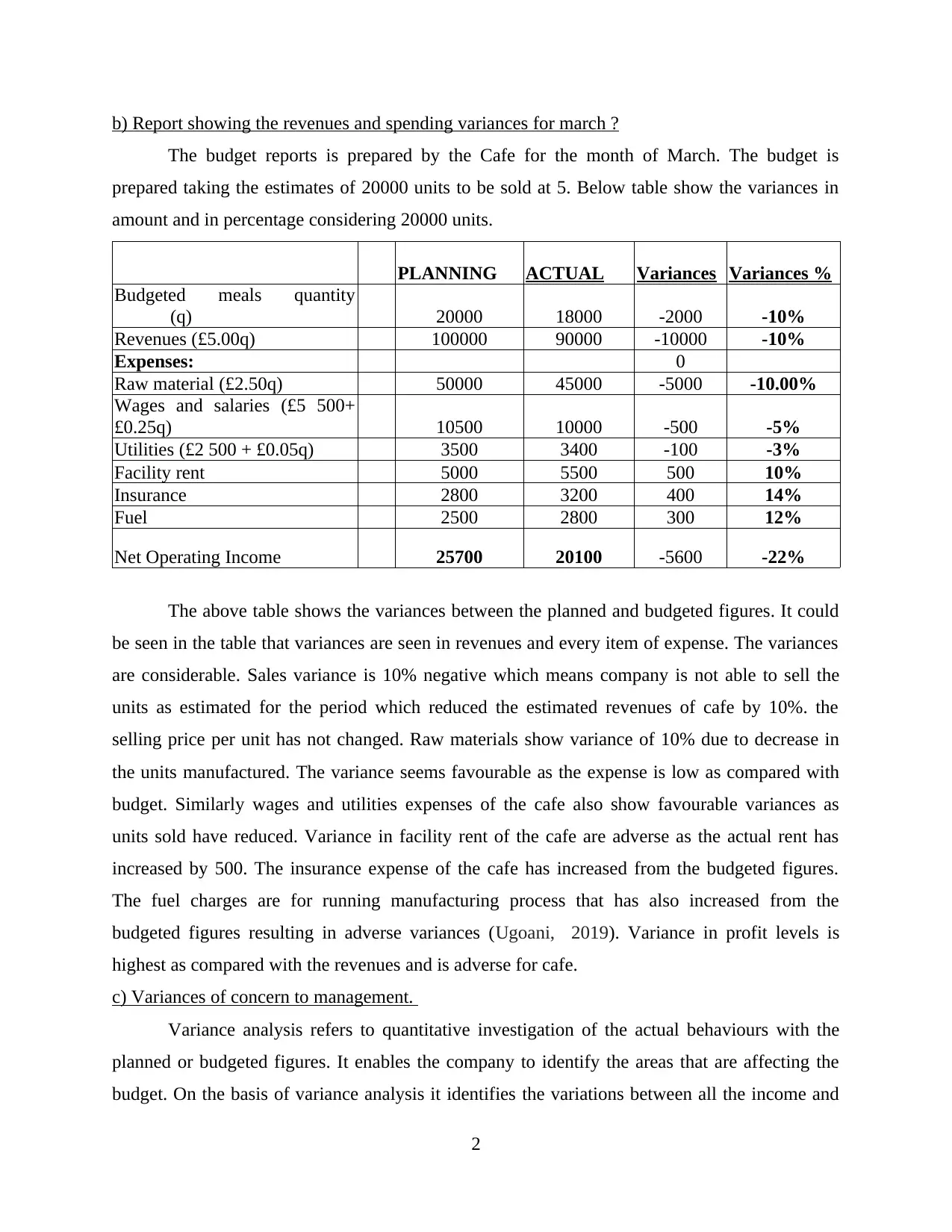

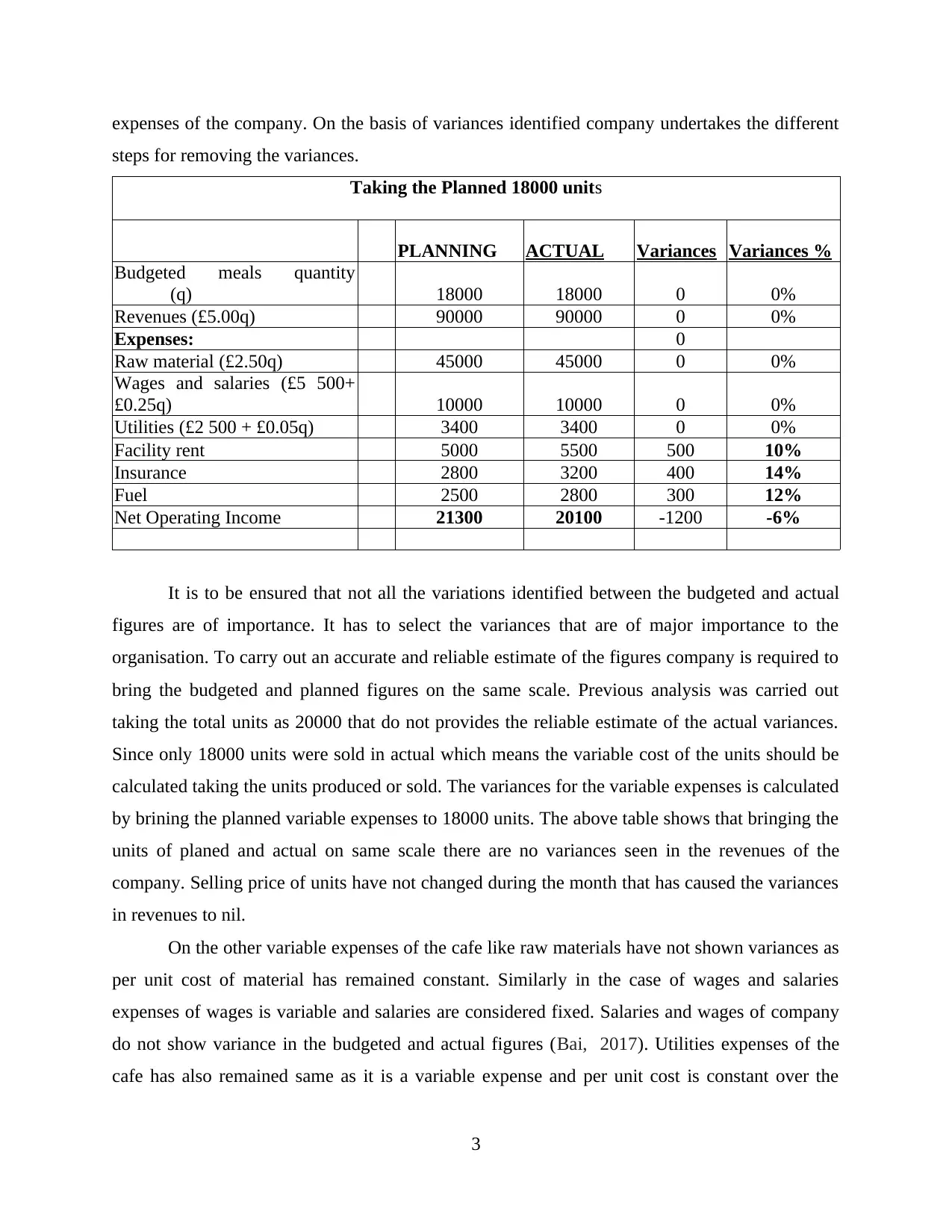

This report provides a comprehensive financial analysis of Fleet Highlands Cafe's budget, focusing on the objectives of budgeting, revenue and spending variances, and measures to maintain profitability and sustainability. The introduction defines budgeting and its role in projecting future income and expenses, emphasizing its importance for managing company expenditures. The report analyzes the budget for March, comparing budgeted and actual figures for revenue, raw materials, wages, utilities, facility rent, insurance, and fuel. It highlights significant variances, such as a 10% decrease in sales and adverse variances in fixed expenses like facility rent, insurance, and fuel. The analysis brings planned and actual figures to the same scale to provide a reliable estimate of variances. The report identifies key variances of concern to management and recommends strategies to address them, including promotion strategies to increase sales, negotiation for lower rent, and exploring cost-effective insurance and fuel-efficient equipment to maintain profitability and sustainability. References to relevant sources support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.