University Microeconomics Assignment Solution, BUECO5903

VerifiedAdded on 2022/09/07

|13

|1825

|20

Homework Assignment

AI Summary

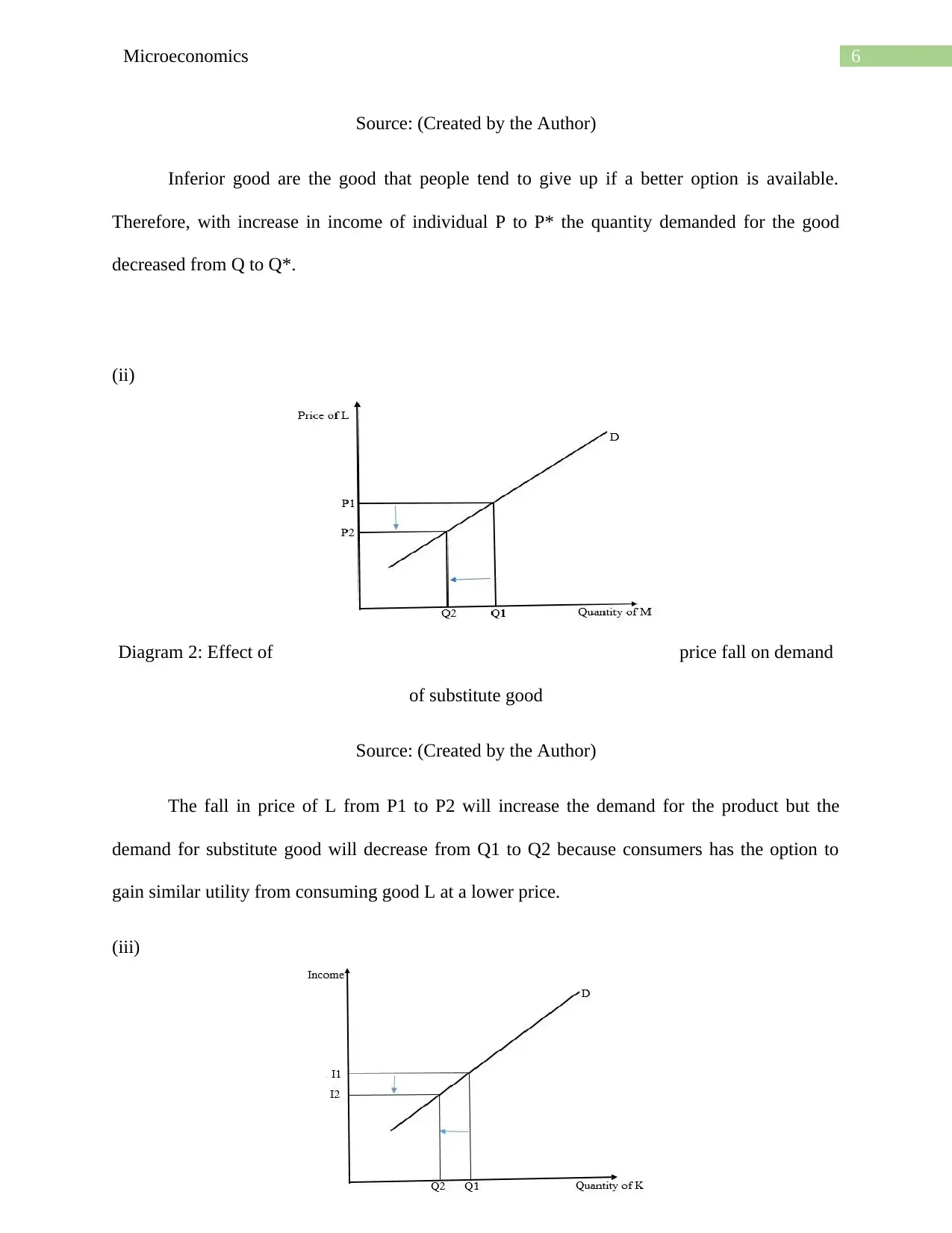

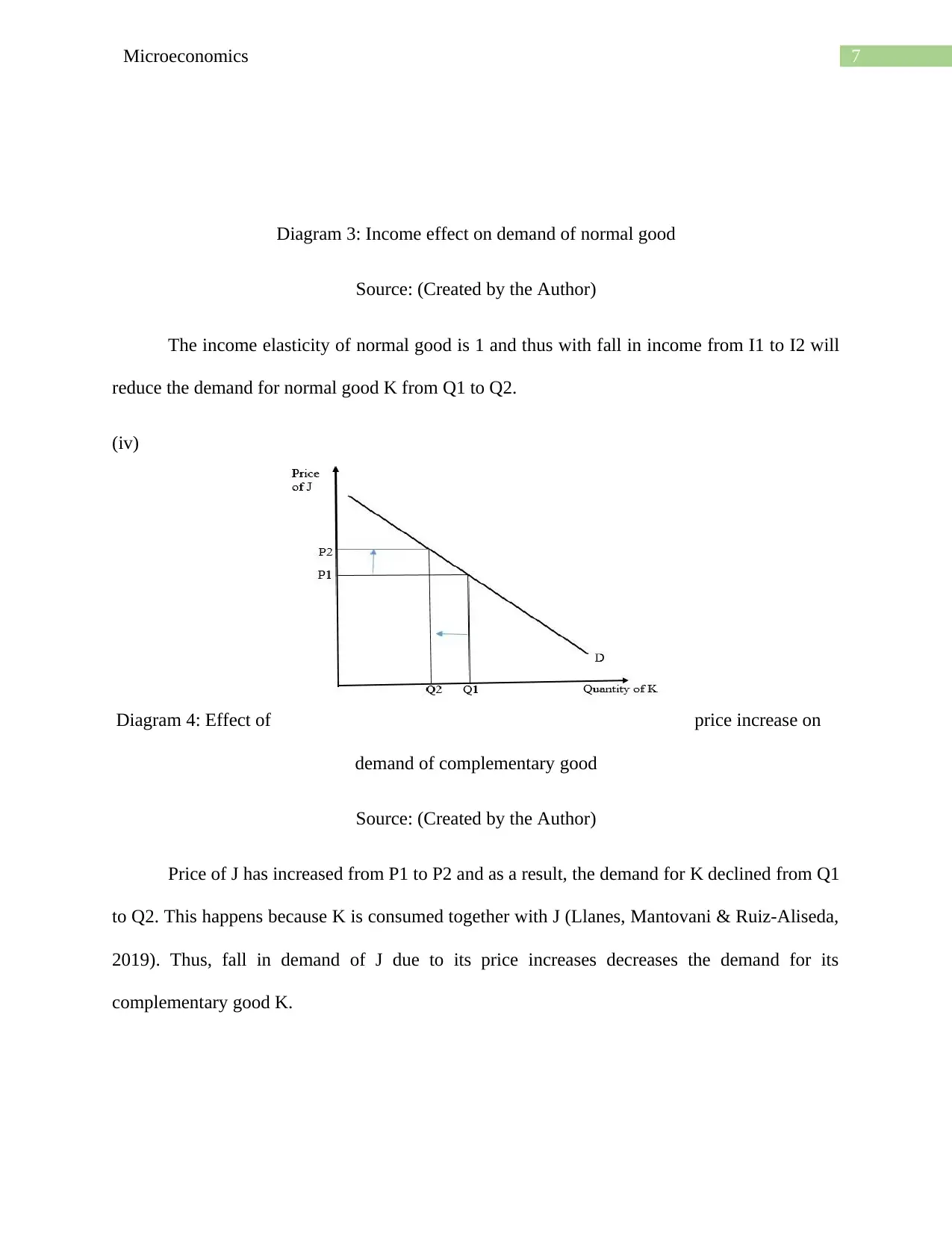

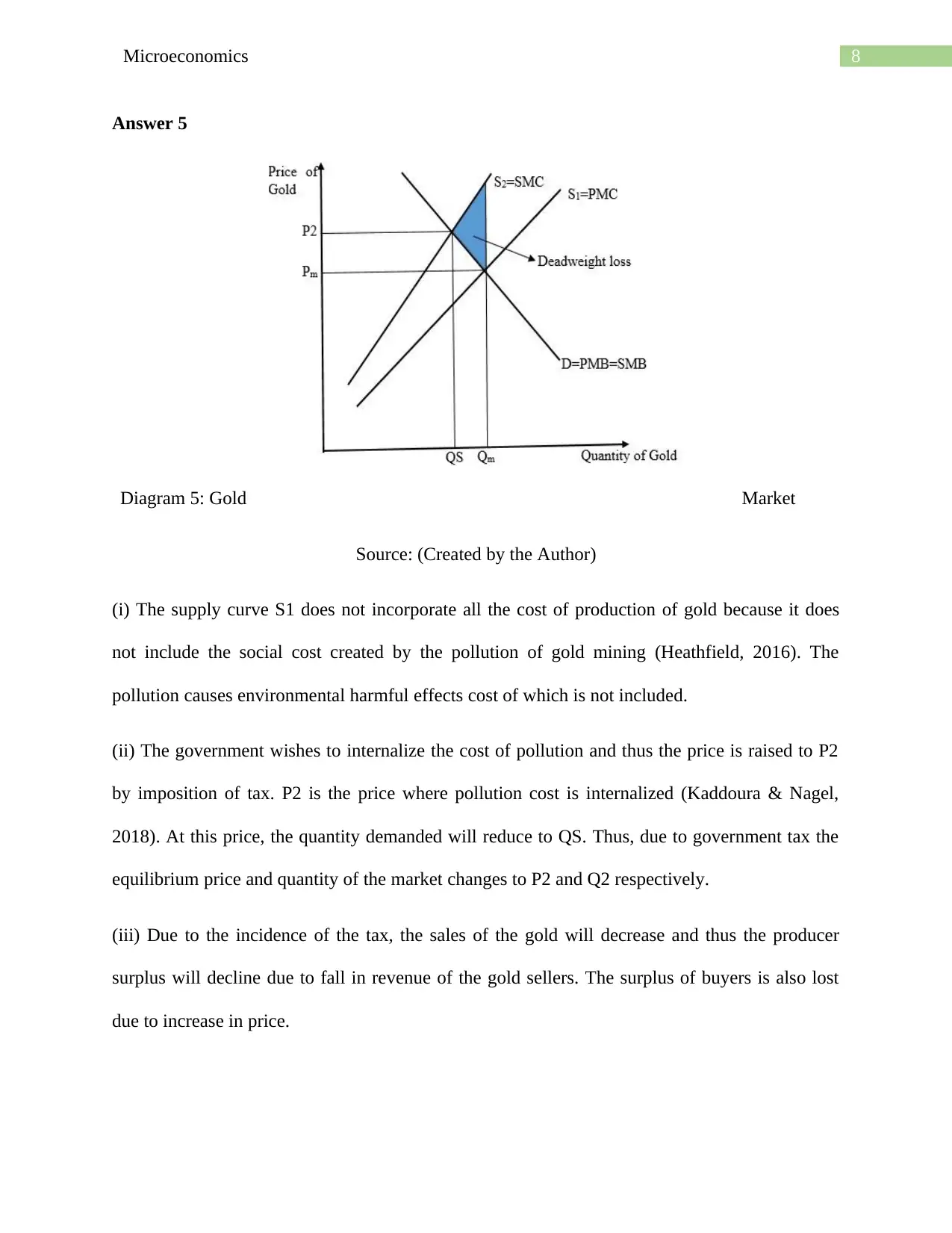

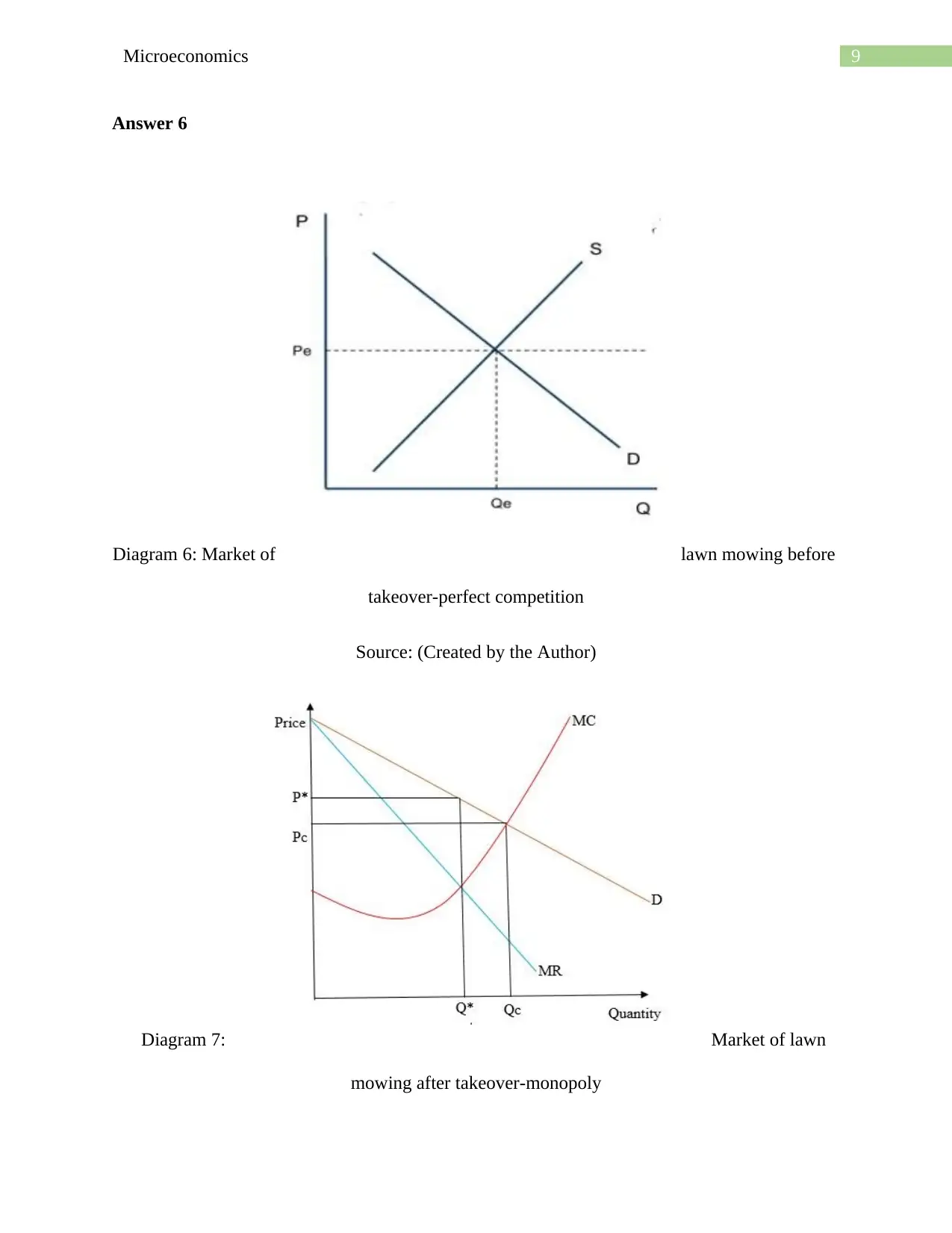

This document presents a comprehensive solution to a microeconomics assignment, addressing key concepts such as elasticity of demand, market structures (perfect competition, monopoly, monopolistic competition, and oligopoly), scarcity, and the impact of government intervention through taxation. The assignment analyzes the cross-price elasticity of demand between substitute products, the implications of price changes on revenue, and the determination of optimal pricing strategies. It also delves into the differences between accounting, economic, and normal profits, and explores the effects of changing demand and supply conditions on market equilibrium. The solution incorporates diagrams to illustrate concepts like income effects on inferior and normal goods, the impact of price changes on complementary and substitute goods, and the effects of pollution costs and taxes in the gold market. Furthermore, the assignment examines the characteristics of monopolistic competition and oligopolistic markets, including collusion incentives. The solution provides detailed explanations and reasoning for each answer, making it a valuable resource for students studying microeconomics.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.