820 Coursework Assignment 2: Analysis of Bupa Insurance Policies

VerifiedAdded on 2023/01/19

|13

|3776

|44

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of Bupa insurance services, focusing on various aspects of their operations. It begins with an introduction to Bupa, highlighting its structure as a private company and its commitment to customer-centric practices. The assignment delves into the types of insurance offered by Bupa, including health, life, and travel insurance, with an emphasis on underwriting processes and the different types of life insurance policies available. A significant portion of the assignment addresses the trends in claims, particularly the increase in indemnity spend, exploring the factors that contribute to this trend, such as competitive market dynamics and technological advancements. The document identifies drivers of leakage, like coverage determination issues and incomplete investigations, and discusses the causes and implications of these trends. The assignment also touches upon the regulatory aspects, particularly the prohibition of indemnity-based products by life insurers, and suggests methods to improve financial performance by managing indemnity spend. Overall, the assignment provides valuable insights into the operations, challenges, and strategies of Bupa within the insurance industry.

Coursework assignment 2 answer template820Coursework submission rules and important notes

Before you start your assignment, it is essential that you familiarise yourself with the

Coursework assessment guidelines and instructions available on RevisionMate.

This includes the following information:

Important rules relating to referencing all sources including the study text, regulations and

citing statute and case law.

Penalties for contravention of the rules relating to plagiarism and collaboration.

Coursework marking criteria applied by markers to submitted answers.

Deadlines for submission of coursework answers.

There are 80 marks available per coursework assignment. You must obtain a minimum of 40

marks (50%) per coursework assignment to achieve a pass.

Your answer must be submitted on the correct answer template in Arial font, size 11.

Your answer must include a brief context, at the start of your answer, and should be referred

to throughout your answer.

Each assignment submission should be a maximum of 3,200 words.

Do not include your name or CII PIN anywhere in your answer.

Top tips for answering coursework assignments

Read the 820 Specimen coursework assignment and answer, available on RevisionMate.

Read the assignments carefully and ensure you answer all parts of the assignments.

You are encouraged to choose a context that is based on a real organisation or a division of

an organisation.

For assignments relating to regulation and law, knowledge of the UK regulatory framework is

appropriate. However, marks can be awarded for non-UK examples if they are more relevant

to your context.

There is no minimum word requirement, but an answer with fewer than 2,800 words may be

insufficiently comprehensive.

To be completed before submission:

Word count: 2340

Start typing your answer here:

Introduction

This assignment will give theoretical knowledge about Bupa insurance services. Their

product/policies which are underwritten, its significant claim trend that has increased the

indemnity spends cause of the claimed trend, and the various points for improvements of the

indemnity spend. BUPA is a private company limited by the guarantee, which simply means

1

January 2019

Before you start your assignment, it is essential that you familiarise yourself with the

Coursework assessment guidelines and instructions available on RevisionMate.

This includes the following information:

Important rules relating to referencing all sources including the study text, regulations and

citing statute and case law.

Penalties for contravention of the rules relating to plagiarism and collaboration.

Coursework marking criteria applied by markers to submitted answers.

Deadlines for submission of coursework answers.

There are 80 marks available per coursework assignment. You must obtain a minimum of 40

marks (50%) per coursework assignment to achieve a pass.

Your answer must be submitted on the correct answer template in Arial font, size 11.

Your answer must include a brief context, at the start of your answer, and should be referred

to throughout your answer.

Each assignment submission should be a maximum of 3,200 words.

Do not include your name or CII PIN anywhere in your answer.

Top tips for answering coursework assignments

Read the 820 Specimen coursework assignment and answer, available on RevisionMate.

Read the assignments carefully and ensure you answer all parts of the assignments.

You are encouraged to choose a context that is based on a real organisation or a division of

an organisation.

For assignments relating to regulation and law, knowledge of the UK regulatory framework is

appropriate. However, marks can be awarded for non-UK examples if they are more relevant

to your context.

There is no minimum word requirement, but an answer with fewer than 2,800 words may be

insufficiently comprehensive.

To be completed before submission:

Word count: 2340

Start typing your answer here:

Introduction

This assignment will give theoretical knowledge about Bupa insurance services. Their

product/policies which are underwritten, its significant claim trend that has increased the

indemnity spends cause of the claimed trend, and the various points for improvements of the

indemnity spend. BUPA is a private company limited by the guarantee, which simply means

1

January 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

820Coursework assignment 2 answer template

that BUPA does not have any shareholder and not derive by the short-term profit. Therefore,

they focus on their customers. They reinvest their profits in the business to provide more and

better healthcare and life care.

Their long vision is to complete their purpose i.e. longer, healthier, happier lives. In the UK,

they have 5.1 million insurance and provision customers with 52 clinics and 1 hospital and

31 dental centres as well as 288 care homes. BUPA deals in various types of insurance like

car insurance, pet insurance, health insurance, etc. BUPA is a privately owned business

entity which deals in straight national health services (BUPA, 2019).

The NHS is subsidized by taxpayers fund and NHS does not need private insurance in view

to gain admittance. BUPA has its private hospitals that can be retrieved by the population

residing by population living in the UK and have private health insurance strategies or those

who can compete with their costs. Firstly, the company gives private medical assurance but

eventually extended to offer privately run hospitals ( Chang, et al., 2019).

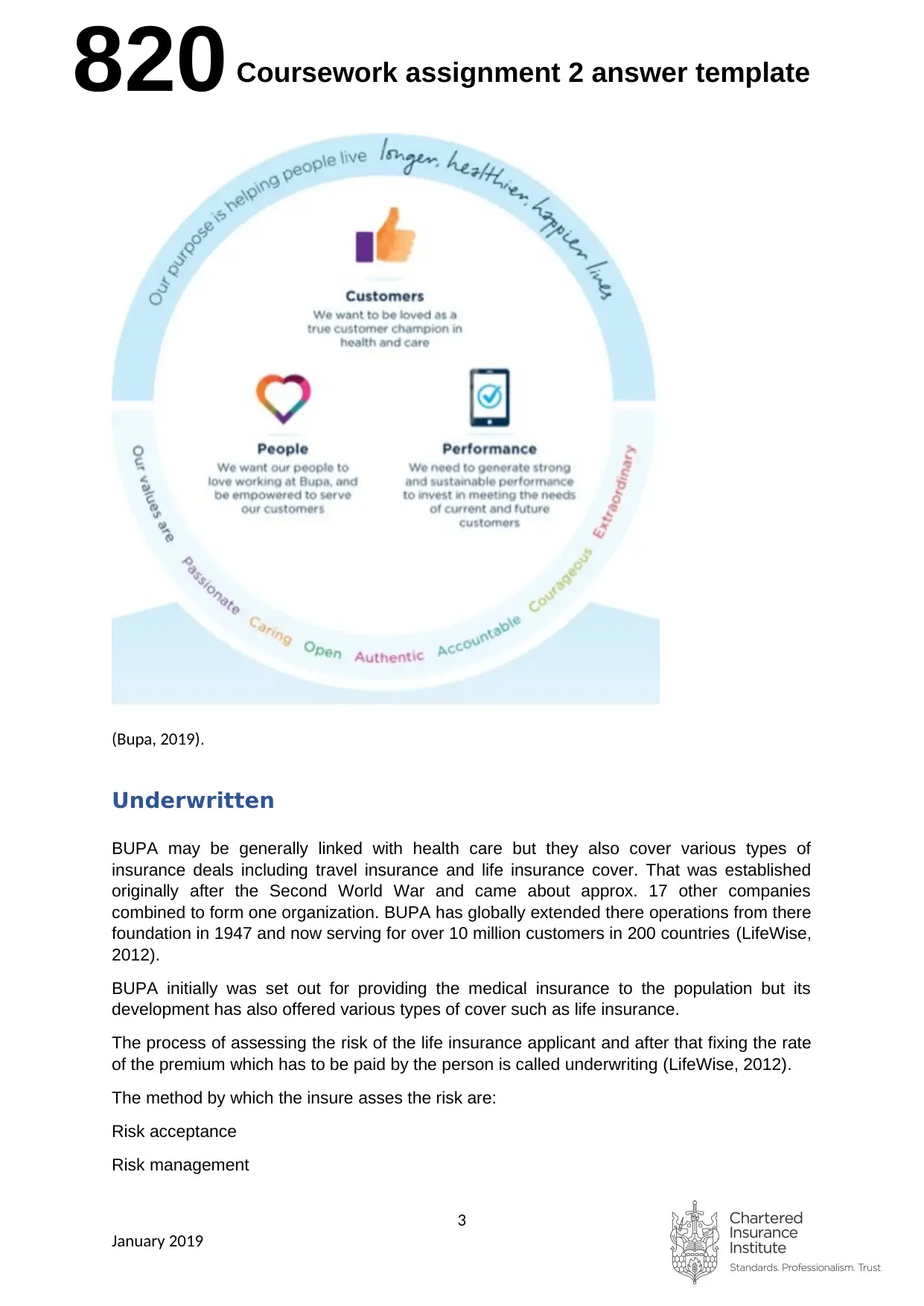

BUPA aims to create values for their customers, peoples, partners, and society. As BUPA

does not have shareholders, their focus remains on customers. BUPA is a service business

everything they do to deliver to their customers is through the peoples. These can be termed

critical to their success. BUPA consists of various worldwide partners, e.g., brokers,

distributors, and health providers. BUPA also takes care of the environment as one of the

responsibilities (Bupa, 2019).

BUPA has been directing business for more than 60 years. BUPA's biggest and unique

business is in the UK where it is the main wellbeing back up plan, however, it has huge tasks

the world over.

BUPA right now utilizes around 40,000 individuals in the UK. BUPA’s principal advantages

are medical coverage, care homes for youthful crippled and more seasoned individuals,

working environment wellbeing administrations, wellbeing appraisals, and unending ailment

the executive's administrations (Bupa, 2019).

Sixty years prior, BUPA was set up to help avoid, ease and fix disorder and sick strength of

each sort. Today, our motivation continues as before. By putting resources into inventive

administrations, such as offering access to the most recent demonstrated medications and

treatment, and their spearheading dementia care, they resolutely keep on helping individuals

live more, more advantageous, more joyful lives.

In the UK BUPA have 3.3 million protected individuals, and over 80% of FTSE 100,

organizations are BUPA clients.

BUPA International is the world's biggest universal wellbeing safety net provider with clients

in more than 190 nations and a system of in excess of 5,500 emergency clinics and facilities

(Bupa, 2017).

2

January 2019

that BUPA does not have any shareholder and not derive by the short-term profit. Therefore,

they focus on their customers. They reinvest their profits in the business to provide more and

better healthcare and life care.

Their long vision is to complete their purpose i.e. longer, healthier, happier lives. In the UK,

they have 5.1 million insurance and provision customers with 52 clinics and 1 hospital and

31 dental centres as well as 288 care homes. BUPA deals in various types of insurance like

car insurance, pet insurance, health insurance, etc. BUPA is a privately owned business

entity which deals in straight national health services (BUPA, 2019).

The NHS is subsidized by taxpayers fund and NHS does not need private insurance in view

to gain admittance. BUPA has its private hospitals that can be retrieved by the population

residing by population living in the UK and have private health insurance strategies or those

who can compete with their costs. Firstly, the company gives private medical assurance but

eventually extended to offer privately run hospitals ( Chang, et al., 2019).

BUPA aims to create values for their customers, peoples, partners, and society. As BUPA

does not have shareholders, their focus remains on customers. BUPA is a service business

everything they do to deliver to their customers is through the peoples. These can be termed

critical to their success. BUPA consists of various worldwide partners, e.g., brokers,

distributors, and health providers. BUPA also takes care of the environment as one of the

responsibilities (Bupa, 2019).

BUPA has been directing business for more than 60 years. BUPA's biggest and unique

business is in the UK where it is the main wellbeing back up plan, however, it has huge tasks

the world over.

BUPA right now utilizes around 40,000 individuals in the UK. BUPA’s principal advantages

are medical coverage, care homes for youthful crippled and more seasoned individuals,

working environment wellbeing administrations, wellbeing appraisals, and unending ailment

the executive's administrations (Bupa, 2019).

Sixty years prior, BUPA was set up to help avoid, ease and fix disorder and sick strength of

each sort. Today, our motivation continues as before. By putting resources into inventive

administrations, such as offering access to the most recent demonstrated medications and

treatment, and their spearheading dementia care, they resolutely keep on helping individuals

live more, more advantageous, more joyful lives.

In the UK BUPA have 3.3 million protected individuals, and over 80% of FTSE 100,

organizations are BUPA clients.

BUPA International is the world's biggest universal wellbeing safety net provider with clients

in more than 190 nations and a system of in excess of 5,500 emergency clinics and facilities

(Bupa, 2017).

2

January 2019

820Coursework assignment 2 answer template

(Bupa, 2019).

Underwritten

BUPA may be generally linked with health care but they also cover various types of

insurance deals including travel insurance and life insurance cover. That was established

originally after the Second World War and came about approx. 17 other companies

combined to form one organization. BUPA has globally extended there operations from there

foundation in 1947 and now serving for over 10 million customers in 200 countries (LifeWise,

2012).

BUPA initially was set out for providing the medical insurance to the population but its

development has also offered various types of cover such as life insurance.

The process of assessing the risk of the life insurance applicant and after that fixing the rate

of the premium which has to be paid by the person is called underwriting (LifeWise, 2012).

The method by which the insure asses the risk are:

Risk acceptance

Risk management

3

January 2019

(Bupa, 2019).

Underwritten

BUPA may be generally linked with health care but they also cover various types of

insurance deals including travel insurance and life insurance cover. That was established

originally after the Second World War and came about approx. 17 other companies

combined to form one organization. BUPA has globally extended there operations from there

foundation in 1947 and now serving for over 10 million customers in 200 countries (LifeWise,

2012).

BUPA initially was set out for providing the medical insurance to the population but its

development has also offered various types of cover such as life insurance.

The process of assessing the risk of the life insurance applicant and after that fixing the rate

of the premium which has to be paid by the person is called underwriting (LifeWise, 2012).

The method by which the insure asses the risk are:

Risk acceptance

Risk management

3

January 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

820Coursework assignment 2 answer template

Risk transfer

Risk avoidance.

BUPA’s offer is very flexible in nature, easily allowing the customers to select the plan

according to their needs. There is the choice, which is given to the customers that they can

pick the type of insurance they need and how much premium each month they want to pay.

There are two types of life insurance in the insurance company:

Permanent insurance; and,

Term insurance

Term insurance covers the set amount of life. There is a fixed term for which amount will be

ceased.

Whereas, in term of permanent insurance, which remains for life.it is very expensive either

pay it at once or in installments.

BUPA also provides them customers 24hrs support on BUPA healthiness support service.

BUPA provides five types so cover to the population such as:

Level Term Cover, Family Income Benefit Cover, Mortgage Protection Term Cover,

Renewable Term Cover and Decreasing Term Cover.

Many clients of BUPA also ought to take Serious illness cover in the link to BUPA life

insurance (Bupa, 2019).

Some of the life policies are underwritten and some are not. Underwriting is the term used by

the insured to the procedure of accessing risk, confirming that the cost of cover taken by the

customer is proportioned to the risk faced by the concern customers. The underwritten

process somehow help the person in their risk. Insurance risk effect only the common

insurance person in the group. It consists of pricing and underwriting risk and reserving risk

(LifeWise, 2012).

With numerous items on offer, it tends to be troublesome picking the correct one. In any

case, it is fundamental to contrast with getting the best arrangement and with many suppliers

working in the UK, this can be very overwhelming. In any case, the inability to investigate

every one of your choices could prompt you paying a lot for your extra security (Bain, 2014).

BUPA life insurance givers various range of insurance products through there various

trusted financial services for e.g., Clear View. They help in underwriting their products and

services, which will help them in mitigating the risk associated. In the event that need to

contrast BUPA Life Insurance and the best, the remainder of the market brings to the table,

at that point come. BUPA analyses many arrangements from suppliers over the UK to locate

the best arrangement for you. All the permanent residing of the UK can apply for the policy

of life insurance although the ages one of the factors which will go to affect the eligibility of

the person. Some personal lifestyle question is been asked by the company just to ensure

which type of cover is too given (Bupa, 2019).

Product difficulty has been steady stress of clients and institutionalization is a positive

development to manufacture further trust, simplify underwriting, claims, operational and

complaint forms in the medical coverage industry for both buyers and insurers.

4

January 2019

Risk transfer

Risk avoidance.

BUPA’s offer is very flexible in nature, easily allowing the customers to select the plan

according to their needs. There is the choice, which is given to the customers that they can

pick the type of insurance they need and how much premium each month they want to pay.

There are two types of life insurance in the insurance company:

Permanent insurance; and,

Term insurance

Term insurance covers the set amount of life. There is a fixed term for which amount will be

ceased.

Whereas, in term of permanent insurance, which remains for life.it is very expensive either

pay it at once or in installments.

BUPA also provides them customers 24hrs support on BUPA healthiness support service.

BUPA provides five types so cover to the population such as:

Level Term Cover, Family Income Benefit Cover, Mortgage Protection Term Cover,

Renewable Term Cover and Decreasing Term Cover.

Many clients of BUPA also ought to take Serious illness cover in the link to BUPA life

insurance (Bupa, 2019).

Some of the life policies are underwritten and some are not. Underwriting is the term used by

the insured to the procedure of accessing risk, confirming that the cost of cover taken by the

customer is proportioned to the risk faced by the concern customers. The underwritten

process somehow help the person in their risk. Insurance risk effect only the common

insurance person in the group. It consists of pricing and underwriting risk and reserving risk

(LifeWise, 2012).

With numerous items on offer, it tends to be troublesome picking the correct one. In any

case, it is fundamental to contrast with getting the best arrangement and with many suppliers

working in the UK, this can be very overwhelming. In any case, the inability to investigate

every one of your choices could prompt you paying a lot for your extra security (Bain, 2014).

BUPA life insurance givers various range of insurance products through there various

trusted financial services for e.g., Clear View. They help in underwriting their products and

services, which will help them in mitigating the risk associated. In the event that need to

contrast BUPA Life Insurance and the best, the remainder of the market brings to the table,

at that point come. BUPA analyses many arrangements from suppliers over the UK to locate

the best arrangement for you. All the permanent residing of the UK can apply for the policy

of life insurance although the ages one of the factors which will go to affect the eligibility of

the person. Some personal lifestyle question is been asked by the company just to ensure

which type of cover is too given (Bupa, 2019).

Product difficulty has been steady stress of clients and institutionalization is a positive

development to manufacture further trust, simplify underwriting, claims, operational and

complaint forms in the medical coverage industry for both buyers and insurers.

4

January 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

820Coursework assignment 2 answer template

Significant claims trend that has increased the

indemnity spend

Many insurers have felt the need to improve the efficiency of their claims management

process.

BUPA is operating in the competitive market with the ability to generate a sufficient return to

the policyholders. Various risk has been developed due to the competitive market which

increases the trend of indemnity spend (Everplans, 2019).

Claims indemnity is the biggest expense of the insurer’s. Various technological changes lead

to an increase in this trend in this modern era. Aiming at reducing this biggest expenses will

going to offer bi8g and material awards to the insurers but it will be going to impact on the

investor returns. As per the recent statistics from the Association of British Insurers (ABI)

indicates ( Deloitte Financial Services Group, 2010):

• For UK general risks, premiums fell by 8.8% and claims rose by 1.2% in 2009;

• A ten-year average return of 4.3% on worldwide general business assets; and

• The 2009 general result being the lowest worldwide insurance trading profit since 2003.

This trend reflects is one of falling the premium and rising claims. This gives a challenging

insurance environment in terms of its capacity to generate adequate threat adjusted yields

for policyholders (ABI, 2018).

Drivers of leakage (indemnity)

Coverage determination

Inability to heighten potential inclusion issues.

No examination of other potential accessible inclusion for the protected furthermore, different

gatherings.

• Failure to address approaching danger exchange demands.

Attorney representation

No time to time contact with the claimant or insured,

Relationship building was very poor.

Liability determination

Incomplete investigation.

Taking decision without any supporting documentation.

Missed subrogation opportunity

Missed referral.

5

January 2019

Significant claims trend that has increased the

indemnity spend

Many insurers have felt the need to improve the efficiency of their claims management

process.

BUPA is operating in the competitive market with the ability to generate a sufficient return to

the policyholders. Various risk has been developed due to the competitive market which

increases the trend of indemnity spend (Everplans, 2019).

Claims indemnity is the biggest expense of the insurer’s. Various technological changes lead

to an increase in this trend in this modern era. Aiming at reducing this biggest expenses will

going to offer bi8g and material awards to the insurers but it will be going to impact on the

investor returns. As per the recent statistics from the Association of British Insurers (ABI)

indicates ( Deloitte Financial Services Group, 2010):

• For UK general risks, premiums fell by 8.8% and claims rose by 1.2% in 2009;

• A ten-year average return of 4.3% on worldwide general business assets; and

• The 2009 general result being the lowest worldwide insurance trading profit since 2003.

This trend reflects is one of falling the premium and rising claims. This gives a challenging

insurance environment in terms of its capacity to generate adequate threat adjusted yields

for policyholders (ABI, 2018).

Drivers of leakage (indemnity)

Coverage determination

Inability to heighten potential inclusion issues.

No examination of other potential accessible inclusion for the protected furthermore, different

gatherings.

• Failure to address approaching danger exchange demands.

Attorney representation

No time to time contact with the claimant or insured,

Relationship building was very poor.

Liability determination

Incomplete investigation.

Taking decision without any supporting documentation.

Missed subrogation opportunity

Missed referral.

5

January 2019

820Coursework assignment 2 answer template

Lack of flow of investigation.

All the insurance providing company where it is life insurance or health insurance can now

have their separate proposal from which they can set out the separate standard and

declarations

Life insurers are not permitted to offer indemnity based products to the public.

This regulation has been made from now onwards that life insurer will not go to be offer

indemnity products. For the existing policy, the holder will, however, have indemnity products

until their policy term comes to end.

Aiming at diminishing the indemnity spend is a method through which insurer can able to

achieve the good improvements in the financial statement of the company and stability in

their performance and can achieve in a providing good return to the policyholders (Sinha,

2013).

Indemnity spend is one of the biggest expense for the company. Even a tiny change in the

claims indemnity will be going to have an important impact on the insurer profit or

profitability.

The competitive market is one of the main significant claim trends that has increased the

indemnity spend (Hobson, 2016).

Causes

Gamification gains traction as a clients engagement device

Gamification is gaining traction between life insurers as a tool to involve with clients as well

as to increase brand awareness and generate new products.

Glamification educates the customers about the benefits of the life insurance that customers

get knowledge about the various minor information about their claims policy and conditions.

It gives the knowledge about minor information of the company to the customers by which

the policyholder know about all and everything and can easily find out the minor loose points

about the policy.

Although it is resulting in risk reduction it can also affect the company in regard to the claims

(Cognizant, 2019).

Use of robot advisors being explored

Although life insurer is discovering the use of robot consultants for greater accessibility and

understanding recommendation it is also creating risk against claims.

In this customers techniques, are personalized which result in increasing claims (Rapid

Value, 2017).

Block chain technology

Block chain technology maintains a focus on maintaining decentralized records.it blocks the

information of the public due which transparency eliminated between the customers and the

6

January 2019

Lack of flow of investigation.

All the insurance providing company where it is life insurance or health insurance can now

have their separate proposal from which they can set out the separate standard and

declarations

Life insurers are not permitted to offer indemnity based products to the public.

This regulation has been made from now onwards that life insurer will not go to be offer

indemnity products. For the existing policy, the holder will, however, have indemnity products

until their policy term comes to end.

Aiming at diminishing the indemnity spend is a method through which insurer can able to

achieve the good improvements in the financial statement of the company and stability in

their performance and can achieve in a providing good return to the policyholders (Sinha,

2013).

Indemnity spend is one of the biggest expense for the company. Even a tiny change in the

claims indemnity will be going to have an important impact on the insurer profit or

profitability.

The competitive market is one of the main significant claim trends that has increased the

indemnity spend (Hobson, 2016).

Causes

Gamification gains traction as a clients engagement device

Gamification is gaining traction between life insurers as a tool to involve with clients as well

as to increase brand awareness and generate new products.

Glamification educates the customers about the benefits of the life insurance that customers

get knowledge about the various minor information about their claims policy and conditions.

It gives the knowledge about minor information of the company to the customers by which

the policyholder know about all and everything and can easily find out the minor loose points

about the policy.

Although it is resulting in risk reduction it can also affect the company in regard to the claims

(Cognizant, 2019).

Use of robot advisors being explored

Although life insurer is discovering the use of robot consultants for greater accessibility and

understanding recommendation it is also creating risk against claims.

In this customers techniques, are personalized which result in increasing claims (Rapid

Value, 2017).

Block chain technology

Block chain technology maintains a focus on maintaining decentralized records.it blocks the

information of the public due which transparency eliminated between the customers and the

6

January 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

820Coursework assignment 2 answer template

insurer. Although it can help in minimizing the operating cost it is not good for the insurance

company (Research brief, 2019).

Recommendation

Recommendation 1

The public hospital should only charge private patients

For the admission which is already booked;

When they have a contract with the health insurer. By doing this there will be a improve on

the internet spend.

Recommendation 2

For reforming pricing arrangement the government should adopt a staged approach:

• as an initial step, costs right now paid by open emergency clinics in Australia ought to be

made open, and utilized as the reason at the costs recorded on the Prostheses List at

whatever point conceivable, with restricted scope for a bigger premium over this open

valuing so that there is never again a 'two-layered advertise'.

• this ought to be trailed by a procedure to universally benchmark all things, prompting

further decreases to costs for open and private patients in Australia.

• at last, yet again reasonable costs have been built up, prostheses ought to be packaged

into installments for systems, as opposed to exclusively charged. Similarly, as packaging

has prompted decreasing lengths of remains in the private area and maintaining a strategic

distance from pointless days in the emergency clinic, so could packaging of prostheses lead

to the selection of prostheses better lined up with post-viability and generally results, and

diminishing a portion of the unreasonable impetuses seen presently (Bupa, 2019).

Recommendation 3

The government should assign the separate provider to separate no. private and public

hospital co-located.

Recommendation 4

The government should create a productivity commission assessment of the health system

to mature a 10-year road map for structural improvement of the health system.

Recommendation 5

The Medicare Levy Surcharge ought to be rebased so it gives a more grounded motivating

force to the individuals who can stand to add to the expenses of their medicinal services to

do as such. This could be accomplished by re-establishing the first proportion between the

MLS and normal private medical coverage costs, accordingly re-establishing the impetus for

high-pay workers to take out private medical coverage

7

January 2019

insurer. Although it can help in minimizing the operating cost it is not good for the insurance

company (Research brief, 2019).

Recommendation

Recommendation 1

The public hospital should only charge private patients

For the admission which is already booked;

When they have a contract with the health insurer. By doing this there will be a improve on

the internet spend.

Recommendation 2

For reforming pricing arrangement the government should adopt a staged approach:

• as an initial step, costs right now paid by open emergency clinics in Australia ought to be

made open, and utilized as the reason at the costs recorded on the Prostheses List at

whatever point conceivable, with restricted scope for a bigger premium over this open

valuing so that there is never again a 'two-layered advertise'.

• this ought to be trailed by a procedure to universally benchmark all things, prompting

further decreases to costs for open and private patients in Australia.

• at last, yet again reasonable costs have been built up, prostheses ought to be packaged

into installments for systems, as opposed to exclusively charged. Similarly, as packaging

has prompted decreasing lengths of remains in the private area and maintaining a strategic

distance from pointless days in the emergency clinic, so could packaging of prostheses lead

to the selection of prostheses better lined up with post-viability and generally results, and

diminishing a portion of the unreasonable impetuses seen presently (Bupa, 2019).

Recommendation 3

The government should assign the separate provider to separate no. private and public

hospital co-located.

Recommendation 4

The government should create a productivity commission assessment of the health system

to mature a 10-year road map for structural improvement of the health system.

Recommendation 5

The Medicare Levy Surcharge ought to be rebased so it gives a more grounded motivating

force to the individuals who can stand to add to the expenses of their medicinal services to

do as such. This could be accomplished by re-establishing the first proportion between the

MLS and normal private medical coverage costs, accordingly re-establishing the impetus for

high-pay workers to take out private medical coverage

7

January 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

820Coursework assignment 2 answer template

Recommendation 6

Should the Government wish to hold 'light touch' value observing, notwithstanding surveying

regardless of whether premium builds raise any dissolvability or prudential concerns, APRA

could likewise evaluate regardless of whether cost builds to meet a concurred set of valuing

standards (which could be created by the Government in an interview with the business).

Conclusion

The Medicare Levy Surcharge ought to be rebased so it gives a more grounded motivating

force to the individuals who can stand to add to the expenses of their medicinal services to

do as such. This could be accomplished by re-establishing the first proportion between the

MLS and normal private medical coverage costs, accordingly re-establishing the impetus for

high-pay workers to take out private medical coverage.

As UK general insurer work to rise their profitability in this difficult working condition, the

speedy successes that can be accomplished by normally leading CFRs give them a savvy

device to expand productivity, while ending up "top tier" safety net providers regarding

overseeing claims spillage. Proactive case taking care of by the organization - including

early case assessment and arrangement with offended party counsel - can diminish the

number of records that go into the suit and in this manner decrease guard costs. In those

occasions where cases do not settle before the case, early and intensive assessment can

result in progressively engaged and effective utilization of lawyer exercises, again alleviating

guard costs.

8

January 2019

Recommendation 6

Should the Government wish to hold 'light touch' value observing, notwithstanding surveying

regardless of whether premium builds raise any dissolvability or prudential concerns, APRA

could likewise evaluate regardless of whether cost builds to meet a concurred set of valuing

standards (which could be created by the Government in an interview with the business).

Conclusion

The Medicare Levy Surcharge ought to be rebased so it gives a more grounded motivating

force to the individuals who can stand to add to the expenses of their medicinal services to

do as such. This could be accomplished by re-establishing the first proportion between the

MLS and normal private medical coverage costs, accordingly re-establishing the impetus for

high-pay workers to take out private medical coverage.

As UK general insurer work to rise their profitability in this difficult working condition, the

speedy successes that can be accomplished by normally leading CFRs give them a savvy

device to expand productivity, while ending up "top tier" safety net providers regarding

overseeing claims spillage. Proactive case taking care of by the organization - including

early case assessment and arrangement with offended party counsel - can diminish the

number of records that go into the suit and in this manner decrease guard costs. In those

occasions where cases do not settle before the case, early and intensive assessment can

result in progressively engaged and effective utilization of lawyer exercises, again alleviating

guard costs.

8

January 2019

820Coursework assignment 2 answer template

Referencing must be completed before submission

All sources must be referenced in the body of your answer as well as in your reference list. See

the 820 Specimen coursework assignment and answer for examples of how to reference

correctly in text and in your reference list.

References

9

January 2019

Referencing must be completed before submission

All sources must be referenced in the body of your answer as well as in your reference list. See

the 820 Specimen coursework assignment and answer for examples of how to reference

correctly in text and in your reference list.

References

9

January 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

820Coursework assignment 2 answer template

Bibliography

Chang, J., Peysakhovich, F., Wang, W. & Zhu, J., 2019. The UK Health Care System.

[Online]

Available at: http://assets.ce.columbia.edu/pdf/actu/actu-uk.pdf

[Accessed 29 April 2019].

Deloitte Financial Services Group, 2010. UK: Insurance Market Update: The Deloitte View

for Non-Life Insurers. [Online]

Available at:

http://www.mondaq.com/uk/x/112152/Financial+Services/Insurance+Market+Update+The+D

eloitte+View+for+NonLife+Insurers+September+2010

[Accessed 29 April 2019].

ABI, 2018. Insurance industry takes action on excessive differences between new customer

premiums and renewals. [Online]

Available at: https://www.abi.org.uk/news/news-articles/2018/05/insurance-industry-takes-

action-on-excessive-differences-between-new-customer-premiums-and-renewals/

[Accessed 29 April 2019].

Bain, T., 2014. What is Life Insurance Underwriting?. [Online]

Available at: https://www.quickquote.com/blog/life-insurance-underwriting/

[Accessed 29 April 2019].

Bupa, 2017. Health: our business. [Online]

Available at: https://www.bupa.com/~/media/files/site-specific-files/our%20purpose/

workplaces/health%20our%20business%20iii.pdf

[Accessed 29 April 2019].

10

January 2019

Bibliography

Chang, J., Peysakhovich, F., Wang, W. & Zhu, J., 2019. The UK Health Care System.

[Online]

Available at: http://assets.ce.columbia.edu/pdf/actu/actu-uk.pdf

[Accessed 29 April 2019].

Deloitte Financial Services Group, 2010. UK: Insurance Market Update: The Deloitte View

for Non-Life Insurers. [Online]

Available at:

http://www.mondaq.com/uk/x/112152/Financial+Services/Insurance+Market+Update+The+D

eloitte+View+for+NonLife+Insurers+September+2010

[Accessed 29 April 2019].

ABI, 2018. Insurance industry takes action on excessive differences between new customer

premiums and renewals. [Online]

Available at: https://www.abi.org.uk/news/news-articles/2018/05/insurance-industry-takes-

action-on-excessive-differences-between-new-customer-premiums-and-renewals/

[Accessed 29 April 2019].

Bain, T., 2014. What is Life Insurance Underwriting?. [Online]

Available at: https://www.quickquote.com/blog/life-insurance-underwriting/

[Accessed 29 April 2019].

Bupa, 2017. Health: our business. [Online]

Available at: https://www.bupa.com/~/media/files/site-specific-files/our%20purpose/

workplaces/health%20our%20business%20iii.pdf

[Accessed 29 April 2019].

10

January 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

820Coursework assignment 2 answer template

Bupa, 2019. Bupa boosts workplace health. [Online]

Available at: https://www.bupa.com/newsroom/news/bupa-boosts-workplace-health

[Accessed 29 April 2019].

Bupa, 2019. Bupa Response. [Online]

Available at: file:///C:/Users/System04127/Downloads/sub43_Bupa%20(1).pdf

[Accessed 29 April 2019].

Bupa, 2019. Feel the support of thousands of healthcare providers. [Online]

Available at: https://www.bupa.com.au/health-insurance

[Accessed 29 April 2019].

Bupa, 2019. Life Insurance - Bupa. [Online]

Available at: https://www.bupa.com.au/vertical-channel/ch.life-insurance.phi

[Accessed 29 April 2019].

BUPA, 2019. Our story. [Online]

Available at: https://www.bupa.com/corporate/who-we-are/our-story

[Accessed 29 April 2019].

Cognizant, 2019. Gamification for Insurers:A Practitioner’s Perspective. [Online]

Available at: https://www.cognizant.com/whitepapers/gamification-for-insurers-a-practitioner-

s-perspective-codex2268.pdf

[Accessed 29 April 2019].

Everplans, 2019. All You Need To Know About Life Insurance. [Online]

Available at: https://www.everplans.com/articles/all-you-need-to-know-about-life-insurance

[Accessed 29 April 2019].

Hobson, T., 2016. The Changing Face of the Insurance Market. [Online]

Available at: https://whoswholegal.com/news/features/article/33130/changing-face-

11

January 2019

Bupa, 2019. Bupa boosts workplace health. [Online]

Available at: https://www.bupa.com/newsroom/news/bupa-boosts-workplace-health

[Accessed 29 April 2019].

Bupa, 2019. Bupa Response. [Online]

Available at: file:///C:/Users/System04127/Downloads/sub43_Bupa%20(1).pdf

[Accessed 29 April 2019].

Bupa, 2019. Feel the support of thousands of healthcare providers. [Online]

Available at: https://www.bupa.com.au/health-insurance

[Accessed 29 April 2019].

Bupa, 2019. Life Insurance - Bupa. [Online]

Available at: https://www.bupa.com.au/vertical-channel/ch.life-insurance.phi

[Accessed 29 April 2019].

BUPA, 2019. Our story. [Online]

Available at: https://www.bupa.com/corporate/who-we-are/our-story

[Accessed 29 April 2019].

Cognizant, 2019. Gamification for Insurers:A Practitioner’s Perspective. [Online]

Available at: https://www.cognizant.com/whitepapers/gamification-for-insurers-a-practitioner-

s-perspective-codex2268.pdf

[Accessed 29 April 2019].

Everplans, 2019. All You Need To Know About Life Insurance. [Online]

Available at: https://www.everplans.com/articles/all-you-need-to-know-about-life-insurance

[Accessed 29 April 2019].

Hobson, T., 2016. The Changing Face of the Insurance Market. [Online]

Available at: https://whoswholegal.com/news/features/article/33130/changing-face-

11

January 2019

820Coursework assignment 2 answer template

insurance-market-means-lawyers

[Accessed 29 April 2019].

LifeWise, 2012. What is underwriting?. [Online]

Available at: http://www.lifewise.org.au/insurance-101/what-is-underwriting

[Accessed 29 April 2019].

Rapid Value, 2017. Rise of Robo-Advice in Insurance Companies. [Online]

Available at: https://www.rapidvaluesolutions.com/the-rise-of-robo-advice-in-insurance-

companies/

[Accessed 29 April 2019].

Research brief, 2019. How Blockchain Could Disrupt Insurance. [Online]

Available at: https://www.cbinsights.com/research/blockchain-insurance-disruption/

[Accessed 29 April 2019].

Sinha, S., 2013. Cover your professional risks with indemnity insurance. [Online]

Available at: https://economictimes.indiatimes.com/wealth/insure/cover-your-professional-

risks-with-indemnity-insurance/articleshow/24600366.cms?from=mdr

[Accessed 29 April 2019].

Glossary of key words

Analyse

Find the relevant facts and examine these in depth. Examine the relationship between

various facts and make conclusions or recommendations.

Construct

To build or make something; construct a table.

Describe

Give an account in words (someone or something) including all relevant characteristics,

qualities or events.

12

January 2019

insurance-market-means-lawyers

[Accessed 29 April 2019].

LifeWise, 2012. What is underwriting?. [Online]

Available at: http://www.lifewise.org.au/insurance-101/what-is-underwriting

[Accessed 29 April 2019].

Rapid Value, 2017. Rise of Robo-Advice in Insurance Companies. [Online]

Available at: https://www.rapidvaluesolutions.com/the-rise-of-robo-advice-in-insurance-

companies/

[Accessed 29 April 2019].

Research brief, 2019. How Blockchain Could Disrupt Insurance. [Online]

Available at: https://www.cbinsights.com/research/blockchain-insurance-disruption/

[Accessed 29 April 2019].

Sinha, S., 2013. Cover your professional risks with indemnity insurance. [Online]

Available at: https://economictimes.indiatimes.com/wealth/insure/cover-your-professional-

risks-with-indemnity-insurance/articleshow/24600366.cms?from=mdr

[Accessed 29 April 2019].

Glossary of key words

Analyse

Find the relevant facts and examine these in depth. Examine the relationship between

various facts and make conclusions or recommendations.

Construct

To build or make something; construct a table.

Describe

Give an account in words (someone or something) including all relevant characteristics,

qualities or events.

12

January 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.