Burberry Plc: Financial Analysis, Revenue, Liabilities & Compensation

VerifiedAdded on 2023/06/14

|18

|4132

|453

Report

AI Summary

This report provides a comprehensive financial analysis of Burberry Plc, covering key aspects such as the accounting information system, financial statement preparation, and closing and reporting activities. It delves into the revenue recognition process, identifying the techniques used by Burberry and the applicable business reasoning. The report also includes an in-depth analysis of the liability side of Burberry's balance sheet, along with relevant ratio analysis and business reasoning. Furthermore, it examines the compensation structure of Burberry, including stock compensation plans and retirement benefits. The analysis incorporates financial data and accounting principles to provide a clear understanding of Burberry's financial performance and strategic decision-making.

Company’s Business

Financial Analysis

Report

Financial Analysis

Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

1.Accounting information system of Burberry along with preparation of financial

statements, closing and reporting activities.......................................................................3

2.Explain revenue recognition process and structure of revenues. Recognize which

technique for revenue recognition is used. Explain which business reasoning is

applicable...............................................................................................................................4

3.Analysis of Liability Side in Balance Sheet of Burberry Plc Along with Ratio Analysis

of Certain Ratios with Business Reasoning:......................................................................5

4. Analysis of compensation structure of Burberry and stock compensation plans with

retirement benefits................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

1.Accounting information system of Burberry along with preparation of financial

statements, closing and reporting activities.......................................................................3

2.Explain revenue recognition process and structure of revenues. Recognize which

technique for revenue recognition is used. Explain which business reasoning is

applicable...............................................................................................................................4

3.Analysis of Liability Side in Balance Sheet of Burberry Plc Along with Ratio Analysis

of Certain Ratios with Business Reasoning:......................................................................5

4. Analysis of compensation structure of Burberry and stock compensation plans with

retirement benefits................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

INTRODUCTION

The report prepared highlights the importance of Accounting information system which

helps in proper functioning of business. It also helps to understand the importance of financial

statements which can be used by company for managing efficiency and proper working of

business (Banker, 2018). It helps to understand usefulness of closing and reporting activities. The

report prepared so far also takes into account recognised revenue and which method must be

used by company. It also helps company to understand Business reasoning that must be chosen

by managers. The report further helps to select which compensation system must be selected by

the company and also explains compensation plans and benefit of post retirement plans.

TASK

1.Accounting information system of Burberry along with preparation of financial

statements, closing and reporting activities.

Accounting information system: It can be explained as a necessary step in every business

which helps supervisor and managers in decision making. It helps Burberry to predict working of

company and guide analyst in collecting essential data and apply it at useful places for carrying

out operational related activities (Clarke and et.al., 2020). It helps Burberry to check reliability

and enhance understanding complex terms and figures. It also provides them to check if the data

collected is relevant and can be used for futuristic plans.

Preparation of financial statements: Financial position of Burberry can be disclosed with the

help of financial statement such as income statements and balance sheet. It helps internal and

external users to get an idea about the working of a company. It also helps to understand

weakness and strengths of Burberry in comparison to competitors. It can be observed that Net

assets accountable for Burberry company can be seen rising in comparison with previous year.

Cash flow reflects Liquidity of Burberry which has also taken a step further in relation to past

performances and has contributed company in positive aspects. It helps company to have an idea

whether decision making process is fruitful for them in long run or not. Financial statement also

helps Burberry to understand which areas are generating profit and what decisions are leading

towards losses and contributing in growth of company. It helps in preparing budgets and

motivate staff for working towards one common goal as a whole.

The report prepared highlights the importance of Accounting information system which

helps in proper functioning of business. It also helps to understand the importance of financial

statements which can be used by company for managing efficiency and proper working of

business (Banker, 2018). It helps to understand usefulness of closing and reporting activities. The

report prepared so far also takes into account recognised revenue and which method must be

used by company. It also helps company to understand Business reasoning that must be chosen

by managers. The report further helps to select which compensation system must be selected by

the company and also explains compensation plans and benefit of post retirement plans.

TASK

1.Accounting information system of Burberry along with preparation of financial

statements, closing and reporting activities.

Accounting information system: It can be explained as a necessary step in every business

which helps supervisor and managers in decision making. It helps Burberry to predict working of

company and guide analyst in collecting essential data and apply it at useful places for carrying

out operational related activities (Clarke and et.al., 2020). It helps Burberry to check reliability

and enhance understanding complex terms and figures. It also provides them to check if the data

collected is relevant and can be used for futuristic plans.

Preparation of financial statements: Financial position of Burberry can be disclosed with the

help of financial statement such as income statements and balance sheet. It helps internal and

external users to get an idea about the working of a company. It also helps to understand

weakness and strengths of Burberry in comparison to competitors. It can be observed that Net

assets accountable for Burberry company can be seen rising in comparison with previous year.

Cash flow reflects Liquidity of Burberry which has also taken a step further in relation to past

performances and has contributed company in positive aspects. It helps company to have an idea

whether decision making process is fruitful for them in long run or not. Financial statement also

helps Burberry to understand which areas are generating profit and what decisions are leading

towards losses and contributing in growth of company. It helps in preparing budgets and

motivate staff for working towards one common goal as a whole.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Closing and reporting activities: These are the reports which are being prepared by Burberry

company on daily basis for having its ground clear for further planning and decision making

process. It helps to calculate and perform analyses which would help them in having a better and

bigger picture in management terms. It helps Burberry to choose best method possible from the

alternatives available which would help to keep records accurate and record the closing balances

at the end of financial year (Ganino, 2020). Closing entries are carried out for transferring data

from temporary accounts to permanent accounts. Closing activities help Burberry company to

enter correct and reliable data so that it helps to prepare finance related reports which would help

managers to control outflow of cash and better management of liquidity funds. Closing activities

helps to close all expense account, revenue accounts, dividend accounts and income related

accounts as well. Settling of funds through closing activities helps company to start next

accounting period and have an idea as what should be done to reduce expenses, increase income

and cash flow.

2.Explain revenue recognition process and structure of revenues. Recognize which

technique for revenue recognition is used. Explain which business reasoning is

applicable.

Revenue recognition: Revenue recognition can be explained as certain conditions where

revenue can be ascertained and it also helps to understand how accounting for the same can be

processed. Burberry company can measure revenue for its business cycle with the help of

different methods such as Completed contract based method and Sales basis method.

Techniques used for revenue recognition by Burberry company:

Completed contract based method: In this type of method revenue earned can only be

considered when contract is completed (Ildarkhanov, 2020). This method helps Burberry

to work in unpredictable environment when it feels there is some unforeseen risk is

prevailing in market. It helps to calculate revenue earned for the year with the help of

profit and loss statement prepared by the company.

Sales base method: This method would help Burberry company to have a record of

revenue earned when product gets delivered to customers. It further explains that

companies realise revenue when it is earned and not when company is paid for the

services rendered. It directly affects the working and financial conditions of a company.

company on daily basis for having its ground clear for further planning and decision making

process. It helps to calculate and perform analyses which would help them in having a better and

bigger picture in management terms. It helps Burberry to choose best method possible from the

alternatives available which would help to keep records accurate and record the closing balances

at the end of financial year (Ganino, 2020). Closing entries are carried out for transferring data

from temporary accounts to permanent accounts. Closing activities help Burberry company to

enter correct and reliable data so that it helps to prepare finance related reports which would help

managers to control outflow of cash and better management of liquidity funds. Closing activities

helps to close all expense account, revenue accounts, dividend accounts and income related

accounts as well. Settling of funds through closing activities helps company to start next

accounting period and have an idea as what should be done to reduce expenses, increase income

and cash flow.

2.Explain revenue recognition process and structure of revenues. Recognize which

technique for revenue recognition is used. Explain which business reasoning is

applicable.

Revenue recognition: Revenue recognition can be explained as certain conditions where

revenue can be ascertained and it also helps to understand how accounting for the same can be

processed. Burberry company can measure revenue for its business cycle with the help of

different methods such as Completed contract based method and Sales basis method.

Techniques used for revenue recognition by Burberry company:

Completed contract based method: In this type of method revenue earned can only be

considered when contract is completed (Ildarkhanov, 2020). This method helps Burberry

to work in unpredictable environment when it feels there is some unforeseen risk is

prevailing in market. It helps to calculate revenue earned for the year with the help of

profit and loss statement prepared by the company.

Sales base method: This method would help Burberry company to have a record of

revenue earned when product gets delivered to customers. It further explains that

companies realise revenue when it is earned and not when company is paid for the

services rendered. It directly affects the working and financial conditions of a company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Structure of revenues: It can be bifurcated in two types which is operating and non-

operating revenues. Operating revenues can be explained as Main business operations

which help to generate business revenues in Burberry company and are directly related to

working of business. Non-operating revenues can be explained as revenues earned

through other related activities which are not directly linked to business operations.

Business reasoning: It helps the company to take important decisions for better functioning of

business and for the long life cycle of business (Jones and Wang, 2019). It also helps Burberry

company to improve efficiency of the organisation and identify problem well in time and make

plans for the same. Important business reasoning helps managers to form accurate policies and

improve productivity of the business. It also helps to analyse business issues creating hurdles and

problems on the pathway towards success of business. Business reasoning applicable in case of

Burberry company is Complete contract based method because it deals in retail sector and

provides customer's full & final product. The revenue recognition is done at certain interval

when contract is completed and customer has received the product. For example, in case of

construction based company a flyover takes approximately 5-10 years for constructing the bridge

whereas in case of clothing company it is made and delivered to customer at certain time interval

and is not considered time consuming as well. Burberry is considered one of the best company

which is known as a brand for luxury items and providing superior feeling to customer's as well

3.Analysis of Liability Side in Balance Sheet of Burberry Plc Along with Ratio Analysis of

Certain Ratios with Business Reasoning:

Liabilities can be explained as defined obligation of an organisation which has to be met by

them in defined period of time. These can be current or non-current depending upon their nature

and period. The liabilities items can be interpreted in following manner: -

Trade and other payables of Burberry is reduced when compare to previous years which

indicates threat the company has paid their dues which is standing in balance sheet.

Another conclusion can be made that company has Burberry is paying its debts relating

previous years at a faster rate and ignoring new purchases as they have sufficient stock.

The bank overdraft of the entity is increased slightly in current year which indicates that

company is utilising the od limit of banks and financial institution consistently. However,

it creates burden on Burberry with respect to payment of interest. However, the portion of

operating revenues. Operating revenues can be explained as Main business operations

which help to generate business revenues in Burberry company and are directly related to

working of business. Non-operating revenues can be explained as revenues earned

through other related activities which are not directly linked to business operations.

Business reasoning: It helps the company to take important decisions for better functioning of

business and for the long life cycle of business (Jones and Wang, 2019). It also helps Burberry

company to improve efficiency of the organisation and identify problem well in time and make

plans for the same. Important business reasoning helps managers to form accurate policies and

improve productivity of the business. It also helps to analyse business issues creating hurdles and

problems on the pathway towards success of business. Business reasoning applicable in case of

Burberry company is Complete contract based method because it deals in retail sector and

provides customer's full & final product. The revenue recognition is done at certain interval

when contract is completed and customer has received the product. For example, in case of

construction based company a flyover takes approximately 5-10 years for constructing the bridge

whereas in case of clothing company it is made and delivered to customer at certain time interval

and is not considered time consuming as well. Burberry is considered one of the best company

which is known as a brand for luxury items and providing superior feeling to customer's as well

3.Analysis of Liability Side in Balance Sheet of Burberry Plc Along with Ratio Analysis of

Certain Ratios with Business Reasoning:

Liabilities can be explained as defined obligation of an organisation which has to be met by

them in defined period of time. These can be current or non-current depending upon their nature

and period. The liabilities items can be interpreted in following manner: -

Trade and other payables of Burberry is reduced when compare to previous years which

indicates threat the company has paid their dues which is standing in balance sheet.

Another conclusion can be made that company has Burberry is paying its debts relating

previous years at a faster rate and ignoring new purchases as they have sufficient stock.

The bank overdraft of the entity is increased slightly in current year which indicates that

company is utilising the od limit of banks and financial institution consistently. However,

it creates burden on Burberry with respect to payment of interest. However, the portion of

bank ok is 6% approx. of the total current liability which is acceptable in industry

practices.

The derivative liabilities of them are almost 50% compare to 2019-20 when observed

from the balance sheet (Kim, Yeung, and Zhou, 2019). It implies that they encash the

benefit or can be interpreted that the instrument becomes favourable for the organisation

and then they exercise them comparing to previous years. That is the reason there is a

decline in derivative instrument in 2020-21.

The income tax liabilities are almost three times compare to 2019-20 which indicates that

the company has not made payment of tax dues on regular interval of time. There may be

tax authority’s demand of tax of earlier years due to which the company’s tax dues

increased.

The provision has been increased to double which shows that the organisation focuses on

judgement or assumptions more in 2021-20. Further the reason for the same is the

liabilities arising is future in not justified in monetary terms that why judgement or

assumption are made to create provision for those expenses.

The deferred tax liabilities have increased from .10 to .90 when compared to previous

years. It simply means the tax liability of Burberry has risen up that why the company has

created deferred tax liability provision in current years.

The borrowing of the business concern is stable when compare to last year that is 297.10

pound million which shows that repayment of borrowing is not made as they are long

term. Further the companies have sufficient funds that is the reason they not raise more

funds in current year and maintain stability in borrowings.

The structure of liabilities of barberry is based on the generally accepted accounting principles

which is known as UK GAAP standard is FRS 102.” The financial Reporting Standard

applicable in the UK and Republic of Ireland”. The order and format of preparing the statement

of financial position is specified in the above standard. However, identification and classification

of liabilities depends on entity to entity (Knetsch, 2020).

Since barberry is the listed company as listed in London stock exchange therefor their market

price share or bonds is determined by market participant. The valuation of unlisted companies

has been done using various valuation models such as gardens model or dividend valuation

model and so on.

practices.

The derivative liabilities of them are almost 50% compare to 2019-20 when observed

from the balance sheet (Kim, Yeung, and Zhou, 2019). It implies that they encash the

benefit or can be interpreted that the instrument becomes favourable for the organisation

and then they exercise them comparing to previous years. That is the reason there is a

decline in derivative instrument in 2020-21.

The income tax liabilities are almost three times compare to 2019-20 which indicates that

the company has not made payment of tax dues on regular interval of time. There may be

tax authority’s demand of tax of earlier years due to which the company’s tax dues

increased.

The provision has been increased to double which shows that the organisation focuses on

judgement or assumptions more in 2021-20. Further the reason for the same is the

liabilities arising is future in not justified in monetary terms that why judgement or

assumption are made to create provision for those expenses.

The deferred tax liabilities have increased from .10 to .90 when compared to previous

years. It simply means the tax liability of Burberry has risen up that why the company has

created deferred tax liability provision in current years.

The borrowing of the business concern is stable when compare to last year that is 297.10

pound million which shows that repayment of borrowing is not made as they are long

term. Further the companies have sufficient funds that is the reason they not raise more

funds in current year and maintain stability in borrowings.

The structure of liabilities of barberry is based on the generally accepted accounting principles

which is known as UK GAAP standard is FRS 102.” The financial Reporting Standard

applicable in the UK and Republic of Ireland”. The order and format of preparing the statement

of financial position is specified in the above standard. However, identification and classification

of liabilities depends on entity to entity (Knetsch, 2020).

Since barberry is the listed company as listed in London stock exchange therefor their market

price share or bonds is determined by market participant. The valuation of unlisted companies

has been done using various valuation models such as gardens model or dividend valuation

model and so on.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ratio analysis of the following coefficients as under: -

1. Current Ratio: - This ratio measures the relationship between current assets and

liabilities of the enterprise. The ideal current ratio is 2 which implies that the current

assets of the organisation is just doubled of that to current liability (Michener, 2021). The

formula of calculating the same is:

= (Current Assets / Current Liabilities)

The current ratio of Burberry for current and previous year are as under

2020-2021 2019-2020

Current Ratio: - 2.82 times 2.31 times

(1982.20 / 702.80) (1688.60 / 730.50)

The above ratio of both the years depicts that the organisation is regularly maintaining the

ideal mark set in the industry. Further it indicates that the company has made the

sufficient cover with respect to current dues so that they can be paid off against them in

regular interval. The increase of .51 times in ratio when compares to previous year

reflects that Burberry has paid off the liability due to which there is a reduction in current

liabilities as they must have sufficient funds to clear them. Further increase in revenue

along with cash make their current assets higher compare to previous year. These are the

reason of change in above ratio: -

2. Acid Test Ratio: - It is also known as quick ratio. This ratio measures the liquidity of the

organisation to convert its assets into quick cash so that they can repay their current

liabilities (Morrey, 2018).

The formula of calculating the same will be shown below: -

= (Current Assets – Inventory) / Current Liability

The acid test ratio of Burberry for current and previous year are shown under: -

2020-2021 2019-2020

Acid Test Ratio: - 2.25 times 1.69 times

(1982.90 - 402.10)/702.80 (1688.60 - 450.50)/730.50)

The above calculation indicates that the acid ratio of Burberry is increasing from the

previous year which shows that liquidity or cash position of the concern is increasing.

There is not much difference in current and acid test ratio in current year, however in

2019-20 there is higher difference which states that Burberry current assets majorly

1. Current Ratio: - This ratio measures the relationship between current assets and

liabilities of the enterprise. The ideal current ratio is 2 which implies that the current

assets of the organisation is just doubled of that to current liability (Michener, 2021). The

formula of calculating the same is:

= (Current Assets / Current Liabilities)

The current ratio of Burberry for current and previous year are as under

2020-2021 2019-2020

Current Ratio: - 2.82 times 2.31 times

(1982.20 / 702.80) (1688.60 / 730.50)

The above ratio of both the years depicts that the organisation is regularly maintaining the

ideal mark set in the industry. Further it indicates that the company has made the

sufficient cover with respect to current dues so that they can be paid off against them in

regular interval. The increase of .51 times in ratio when compares to previous year

reflects that Burberry has paid off the liability due to which there is a reduction in current

liabilities as they must have sufficient funds to clear them. Further increase in revenue

along with cash make their current assets higher compare to previous year. These are the

reason of change in above ratio: -

2. Acid Test Ratio: - It is also known as quick ratio. This ratio measures the liquidity of the

organisation to convert its assets into quick cash so that they can repay their current

liabilities (Morrey, 2018).

The formula of calculating the same will be shown below: -

= (Current Assets – Inventory) / Current Liability

The acid test ratio of Burberry for current and previous year are shown under: -

2020-2021 2019-2020

Acid Test Ratio: - 2.25 times 1.69 times

(1982.90 - 402.10)/702.80 (1688.60 - 450.50)/730.50)

The above calculation indicates that the acid ratio of Burberry is increasing from the

previous year which shows that liquidity or cash position of the concern is increasing.

There is not much difference in current and acid test ratio in current year, however in

2019-20 there is higher difference which states that Burberry current assets majorly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depend upon inventory which is not the good sign for healthy organisation. Further it is to

be taken care that high acid test ratio is against the entity as it shows that funds in the

form of cash sitting idle. They are not invested by entity in specific assets in order to gain

fruitful return for stakeholders.

3. Debt to Total Assets Ratio: - this ratio signifies that how much the entity is controlled

by debt holders compare to total assets as compare to equity holders (Pande, and et.al.,

2021).

The formula of calculating the same as under: -

= Total debt / Total assets * 100

2020-2021 2019-2020

Debt to total asset ratio: - 8.48% 9.11%

(297.10 / 3502.20 * 100) (300 / 3292.20 * 100)

On the basis of above calculation, we can conclude that debt hold significantly low

portion in the assets of the entity. It signifies that Burberry is owned by equity holders

majorly that represents that controlling power of organisation are in their hands.

4. Times Interest Earned Ratio: - It shows the ability of an entity to provide coverage to

debt holders on their interest (Pickard, 2021).

The formula of calculating the same as mentioned below:

= Earnings before interest and tax (EBIT) / Interest

2020-2021 2019-2020

Earnings before interest and tax (EBIT) / Interest: - 16.86 times 9.34 times

(521.10/30.90) (188.70/20.20)

The above figures show that coverage of interest in 2020-21 is better as compare to 2019-20. The

funds of debtholders are secured in Burberry as their coverage is more than expected.

4. Analysis of compensation structure of Burberry and stock compensation plans with

retirement benefits

Compensation system include all the financial as well as non-financial benefits provided to

employee by employer of an organization. It includes direct financial, indirect financial and non-

financial. In context of Burberry, compensation system can be explained as given below -

be taken care that high acid test ratio is against the entity as it shows that funds in the

form of cash sitting idle. They are not invested by entity in specific assets in order to gain

fruitful return for stakeholders.

3. Debt to Total Assets Ratio: - this ratio signifies that how much the entity is controlled

by debt holders compare to total assets as compare to equity holders (Pande, and et.al.,

2021).

The formula of calculating the same as under: -

= Total debt / Total assets * 100

2020-2021 2019-2020

Debt to total asset ratio: - 8.48% 9.11%

(297.10 / 3502.20 * 100) (300 / 3292.20 * 100)

On the basis of above calculation, we can conclude that debt hold significantly low

portion in the assets of the entity. It signifies that Burberry is owned by equity holders

majorly that represents that controlling power of organisation are in their hands.

4. Times Interest Earned Ratio: - It shows the ability of an entity to provide coverage to

debt holders on their interest (Pickard, 2021).

The formula of calculating the same as mentioned below:

= Earnings before interest and tax (EBIT) / Interest

2020-2021 2019-2020

Earnings before interest and tax (EBIT) / Interest: - 16.86 times 9.34 times

(521.10/30.90) (188.70/20.20)

The above figures show that coverage of interest in 2020-21 is better as compare to 2019-20. The

funds of debtholders are secured in Burberry as their coverage is more than expected.

4. Analysis of compensation structure of Burberry and stock compensation plans with

retirement benefits

Compensation system include all the financial as well as non-financial benefits provided to

employee by employer of an organization. It includes direct financial, indirect financial and non-

financial. In context of Burberry, compensation system can be explained as given below -

Base salary – It is framed on the basis of individual performance and contribution of

employees to an organization. Executive director's salary is increased annually on a basis

of percentage.

Pension – It is a contribution of employer and employee for payments received after

duration of a job in uniform manner. Executive directors of Burberry receive allowance

in cash form.

Other benefits – There are several benefits such as paid sick leave, performance bonus

and paid vacation. Executive directors of Burberry receive cash as well as non-cash

benefits such as private medical, long term disability insurance and life assurance. In its

guidelines it states that value of benefit should not exceed 100000 per annum.

Stock compensation – In this, employers provide stock option to its employees. Stock option is

a right to sell and buy securities but not an obligation (Ryan, 2021). It is usually helpful for

startup companies where they do not have enough funds to provide for its shareholders. Stock

options can be categorized into two major types -

Non-qualified stock options – It is provided to employees but there are no benefits

regarding tax and increases the tax payable on total income.

Qualified stock options – This type of option is available to employees only and not to

the directors of an enterprise. QSO aids in taking various advantages of tax and reduces

the liability of the tax.

In context of Burberry, it issues several securities to its employees. It assists in retention of

personnel which eventually reduces the training and recruitment cost of an enterprise.

Few options provided by Burberry to its personnel can be described as given below-

a) Employee stock options plan – Issuing of stock to its employees at very low or negligible cost

by employers is done in ESOP. It solves the problems regarding decreased value of the firm. It

encompasses several benefits such as it does not reveal the confidentiality of the employees and

helps to gain the trust of its personnel as well as diversify its shares to various holders to

minimize the risk of business failure.

Retirement benefit plans – It is also known as pension plans which delivers monetary security

to its personnel even after completion of service years (Song, Xu, and Yi, 2020). It has several

options such as yearly payments or lump sum payments. Pension benefits of Burberry can be

discussed as given below -

employees to an organization. Executive director's salary is increased annually on a basis

of percentage.

Pension – It is a contribution of employer and employee for payments received after

duration of a job in uniform manner. Executive directors of Burberry receive allowance

in cash form.

Other benefits – There are several benefits such as paid sick leave, performance bonus

and paid vacation. Executive directors of Burberry receive cash as well as non-cash

benefits such as private medical, long term disability insurance and life assurance. In its

guidelines it states that value of benefit should not exceed 100000 per annum.

Stock compensation – In this, employers provide stock option to its employees. Stock option is

a right to sell and buy securities but not an obligation (Ryan, 2021). It is usually helpful for

startup companies where they do not have enough funds to provide for its shareholders. Stock

options can be categorized into two major types -

Non-qualified stock options – It is provided to employees but there are no benefits

regarding tax and increases the tax payable on total income.

Qualified stock options – This type of option is available to employees only and not to

the directors of an enterprise. QSO aids in taking various advantages of tax and reduces

the liability of the tax.

In context of Burberry, it issues several securities to its employees. It assists in retention of

personnel which eventually reduces the training and recruitment cost of an enterprise.

Few options provided by Burberry to its personnel can be described as given below-

a) Employee stock options plan – Issuing of stock to its employees at very low or negligible cost

by employers is done in ESOP. It solves the problems regarding decreased value of the firm. It

encompasses several benefits such as it does not reveal the confidentiality of the employees and

helps to gain the trust of its personnel as well as diversify its shares to various holders to

minimize the risk of business failure.

Retirement benefit plans – It is also known as pension plans which delivers monetary security

to its personnel even after completion of service years (Song, Xu, and Yi, 2020). It has several

options such as yearly payments or lump sum payments. Pension benefits of Burberry can be

discussed as given below -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

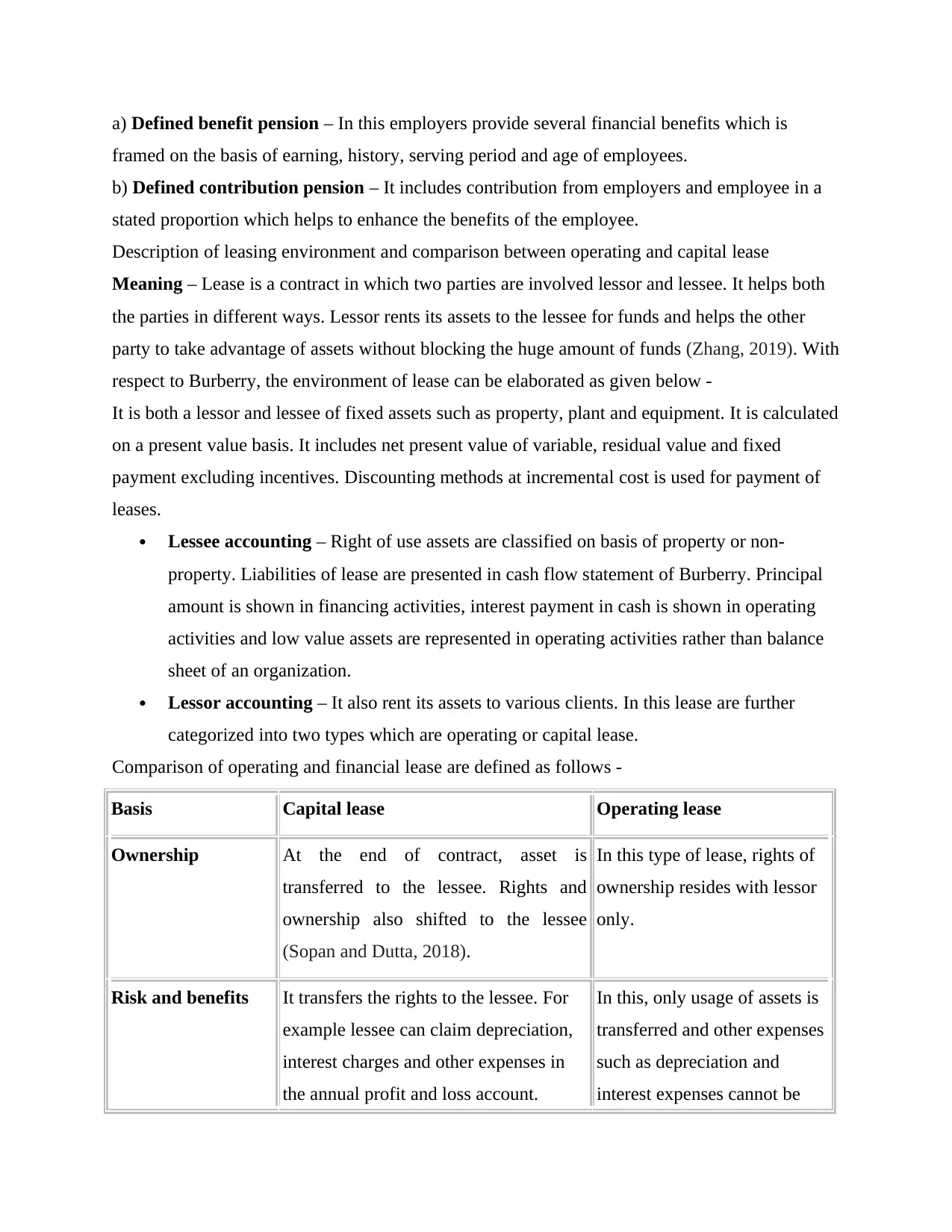

a) Defined benefit pension – In this employers provide several financial benefits which is

framed on the basis of earning, history, serving period and age of employees.

b) Defined contribution pension – It includes contribution from employers and employee in a

stated proportion which helps to enhance the benefits of the employee.

Description of leasing environment and comparison between operating and capital lease

Meaning – Lease is a contract in which two parties are involved lessor and lessee. It helps both

the parties in different ways. Lessor rents its assets to the lessee for funds and helps the other

party to take advantage of assets without blocking the huge amount of funds (Zhang, 2019). With

respect to Burberry, the environment of lease can be elaborated as given below -

It is both a lessor and lessee of fixed assets such as property, plant and equipment. It is calculated

on a present value basis. It includes net present value of variable, residual value and fixed

payment excluding incentives. Discounting methods at incremental cost is used for payment of

leases.

Lessee accounting – Right of use assets are classified on basis of property or non-

property. Liabilities of lease are presented in cash flow statement of Burberry. Principal

amount is shown in financing activities, interest payment in cash is shown in operating

activities and low value assets are represented in operating activities rather than balance

sheet of an organization.

Lessor accounting – It also rent its assets to various clients. In this lease are further

categorized into two types which are operating or capital lease.

Comparison of operating and financial lease are defined as follows -

Basis Capital lease Operating lease

Ownership At the end of contract, asset is

transferred to the lessee. Rights and

ownership also shifted to the lessee

(Sopan and Dutta, 2018).

In this type of lease, rights of

ownership resides with lessor

only.

Risk and benefits It transfers the rights to the lessee. For

example lessee can claim depreciation,

interest charges and other expenses in

the annual profit and loss account.

In this, only usage of assets is

transferred and other expenses

such as depreciation and

interest expenses cannot be

framed on the basis of earning, history, serving period and age of employees.

b) Defined contribution pension – It includes contribution from employers and employee in a

stated proportion which helps to enhance the benefits of the employee.

Description of leasing environment and comparison between operating and capital lease

Meaning – Lease is a contract in which two parties are involved lessor and lessee. It helps both

the parties in different ways. Lessor rents its assets to the lessee for funds and helps the other

party to take advantage of assets without blocking the huge amount of funds (Zhang, 2019). With

respect to Burberry, the environment of lease can be elaborated as given below -

It is both a lessor and lessee of fixed assets such as property, plant and equipment. It is calculated

on a present value basis. It includes net present value of variable, residual value and fixed

payment excluding incentives. Discounting methods at incremental cost is used for payment of

leases.

Lessee accounting – Right of use assets are classified on basis of property or non-

property. Liabilities of lease are presented in cash flow statement of Burberry. Principal

amount is shown in financing activities, interest payment in cash is shown in operating

activities and low value assets are represented in operating activities rather than balance

sheet of an organization.

Lessor accounting – It also rent its assets to various clients. In this lease are further

categorized into two types which are operating or capital lease.

Comparison of operating and financial lease are defined as follows -

Basis Capital lease Operating lease

Ownership At the end of contract, asset is

transferred to the lessee. Rights and

ownership also shifted to the lessee

(Sopan and Dutta, 2018).

In this type of lease, rights of

ownership resides with lessor

only.

Risk and benefits It transfers the rights to the lessee. For

example lessee can claim depreciation,

interest charges and other expenses in

the annual profit and loss account.

In this, only usage of assets is

transferred and other expenses

such as depreciation and

interest expenses cannot be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

charged by the lessee of the

asset.

Bargain purchase

option

Purchasing asset less than the market

value is considered as bargaining. In this

type of lease, option for bargaining is

available to the lessee (Zhang, and

2020).

Bargain purchase option

cannot be obtained by lessee.

It can get benefit of low prices.

CONCLUSION

From the above prepared report, it can be asserted that accounting information system is useful

and financial statement can be prepared with the help revenue earned and expenses incurred. It

helps to recognise which process must be followed for revenue recognition and business

reasoning which would help the company. The report also reflects compensation system for a

company that must be selected, structured and compensation plans helpful for smooth working of

the business. It has been evaluated that contract based method would be beneficial for generating

best results for the company. It helps to differentiate between methods which would help to

generate revenues for the company. In the above report analysis of liability side of Burberry

limited has been carried out in order to judge that whether there is a significance difference

identified comparing with previous year figures and if so then proper reasoning has been made.

At the end of this report ratio analysis along with interpretation has been made.

asset.

Bargain purchase

option

Purchasing asset less than the market

value is considered as bargaining. In this

type of lease, option for bargaining is

available to the lessee (Zhang, and

2020).

Bargain purchase option

cannot be obtained by lessee.

It can get benefit of low prices.

CONCLUSION

From the above prepared report, it can be asserted that accounting information system is useful

and financial statement can be prepared with the help revenue earned and expenses incurred. It

helps to recognise which process must be followed for revenue recognition and business

reasoning which would help the company. The report also reflects compensation system for a

company that must be selected, structured and compensation plans helpful for smooth working of

the business. It has been evaluated that contract based method would be beneficial for generating

best results for the company. It helps to differentiate between methods which would help to

generate revenues for the company. In the above report analysis of liability side of Burberry

limited has been carried out in order to judge that whether there is a significance difference

identified comparing with previous year figures and if so then proper reasoning has been made.

At the end of this report ratio analysis along with interpretation has been made.

REFERENCES

Books and Journals

Banker, L., 2018. Why Hospital-Physician Collaboration Must Improve for the Sake of the

Revenue Cycle. Healthcare Financial Management. 72(10). pp.17-18.

Clarke, J. and et.al., 2020. Fake news, investor attention, and market reaction. Information

Systems Research. 32(1). pp.35-52.

Ganino, M., 2020. Competition law challenges in domestic rail passenger services. In Handbook

on Railway Regulation. Edward Elgar Publishing.

Ildarkhanov, R.F., 2020. Rolling Stock for International Motor Trucking. Journal of

Computational and Theoretical Nanoscience. 17(7). pp.3172-3178.

Jones, S. and Wang, T., 2019. Predicting private company failure: A m

Kim, J.B., Yeung, I. and Zhou, J., 2019. Stock price crash risk and internal control weakness:

presence vs. disclosure effect. Accounting & Finance. 59(2). pp.1197-1233.

Knetsch, A., 2020. Measuring Corporate Investment Horizons and Identifying Short-

Termism. Available at SSRN 3810872.

Michener, G.R., 2021. Use of body mass and sex ratio to interpret the behavioral ecology of

Richardson's ground squirrels. In Interpretation and explanation in the study of animal

behavior (pp. 304-338). Routledge.

Morrey, D.R., 2018. Principles of economic mine closure, reclamation and cost management.

In Remediation and management of degraded lands (pp. 141-150). Routledge.

Pande, V.C. and et.al., 2021. Ecosystem services from ravine agro-ecosystem and its

management. Current Science (00113891). 121(10).

Pickard, J., 2021. Early Australian rabbit-proof fences: paling, slab and stub fences, modified dry

stone walls, and wire netting. Rural History. pp.1-19.

Ryan, M.P., 2021. THE BRITISH AND THE AMERICANS TAKE THE CHESAPEAKE.

In Taking the Land to Make the City (pp. 47-86). University of Texas Press.

Song, S., Xu, X. and Yi, Y., 2020. Shareholder voting in China: The role of large shareholders

and institutional investors. Corporate Governance: An International Review. 28(1).

pp.69-87.

Sopan, J. and Dutta, A., 2018. Determinants of liquidity risk in Indian banks: A panel data

analysis. Asian Journal of Research in Banking and Finance. 8(6). pp.47-59.

Zhang, Q. and et.al., 2020. A novel amplification ratio model of a decoupled XY precision

positioning stage combined with elastic beam theory and Castigliano's second theorem

considering the exact loading force. Mechanical Systems and Signal Processing. 136.

p.106473.

Zhang, X., 2018. Pythagorean fuzzy clustering analysis: a hierarchical clustering algorithm with

the ratio index‐based ranking methods. International Journal of Intelligent

Systems. 33(9). pp.1798-1822.

Books and Journals

Banker, L., 2018. Why Hospital-Physician Collaboration Must Improve for the Sake of the

Revenue Cycle. Healthcare Financial Management. 72(10). pp.17-18.

Clarke, J. and et.al., 2020. Fake news, investor attention, and market reaction. Information

Systems Research. 32(1). pp.35-52.

Ganino, M., 2020. Competition law challenges in domestic rail passenger services. In Handbook

on Railway Regulation. Edward Elgar Publishing.

Ildarkhanov, R.F., 2020. Rolling Stock for International Motor Trucking. Journal of

Computational and Theoretical Nanoscience. 17(7). pp.3172-3178.

Jones, S. and Wang, T., 2019. Predicting private company failure: A m

Kim, J.B., Yeung, I. and Zhou, J., 2019. Stock price crash risk and internal control weakness:

presence vs. disclosure effect. Accounting & Finance. 59(2). pp.1197-1233.

Knetsch, A., 2020. Measuring Corporate Investment Horizons and Identifying Short-

Termism. Available at SSRN 3810872.

Michener, G.R., 2021. Use of body mass and sex ratio to interpret the behavioral ecology of

Richardson's ground squirrels. In Interpretation and explanation in the study of animal

behavior (pp. 304-338). Routledge.

Morrey, D.R., 2018. Principles of economic mine closure, reclamation and cost management.

In Remediation and management of degraded lands (pp. 141-150). Routledge.

Pande, V.C. and et.al., 2021. Ecosystem services from ravine agro-ecosystem and its

management. Current Science (00113891). 121(10).

Pickard, J., 2021. Early Australian rabbit-proof fences: paling, slab and stub fences, modified dry

stone walls, and wire netting. Rural History. pp.1-19.

Ryan, M.P., 2021. THE BRITISH AND THE AMERICANS TAKE THE CHESAPEAKE.

In Taking the Land to Make the City (pp. 47-86). University of Texas Press.

Song, S., Xu, X. and Yi, Y., 2020. Shareholder voting in China: The role of large shareholders

and institutional investors. Corporate Governance: An International Review. 28(1).

pp.69-87.

Sopan, J. and Dutta, A., 2018. Determinants of liquidity risk in Indian banks: A panel data

analysis. Asian Journal of Research in Banking and Finance. 8(6). pp.47-59.

Zhang, Q. and et.al., 2020. A novel amplification ratio model of a decoupled XY precision

positioning stage combined with elastic beam theory and Castigliano's second theorem

considering the exact loading force. Mechanical Systems and Signal Processing. 136.

p.106473.

Zhang, X., 2018. Pythagorean fuzzy clustering analysis: a hierarchical clustering algorithm with

the ratio index‐based ranking methods. International Journal of Intelligent

Systems. 33(9). pp.1798-1822.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.