Financial Analysis Report: Burton Sensors Acquisition, Finance

VerifiedAdded on 2022/08/15

|11

|2913

|14

Report

AI Summary

This report provides a financial analysis of Burton Sensors, focusing on the potential acquisition of Electro-Engineering. The analysis employs the Discounted Cash Flow (DCF) method to value Electro-Engineering, considering projected free cash flows over a five-year period and a terminal value. The report examines the financial statements of Electro-Engineering, incorporating assumptions about revenue growth, expense reduction, and changes in the working capital cycle. The valuation includes calculations of the cost of equity, cost of debt, and weighted average cost of capital (WACC). The report also discusses the financing aspects of the acquisition, suggesting an equity deal. The conclusion provides insights into the potential benefits of the acquisition for Burton Sensors' shareholders.

Running head: ACCOUNTING FINANCIAL ANALYSIS REPORT

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Financial Analysis

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS

Executive Summary

The assignment aims at evaluating the Burton Sensor Company that operates in the

designing and manufacturing of various types of temperature sensors. The company is well

evaluating at the various possible sources of inorganic as well as organic growth for the purpose

of well expanding its business operations, the same has been done by the company with the help

of acquiring Electro-Engineering Company that operates in the same field. The acquisition

would be helping the Burton Sensor Company not only to increase its revenue base but also

increase the wide base of products and services it offers in the market. The acquisition analysis

has been well carried on by us with the help of Discounted Cash Flow Method and relevant

assumptions and figures have been well considered for analysis purpose.

Executive Summary

The assignment aims at evaluating the Burton Sensor Company that operates in the

designing and manufacturing of various types of temperature sensors. The company is well

evaluating at the various possible sources of inorganic as well as organic growth for the purpose

of well expanding its business operations, the same has been done by the company with the help

of acquiring Electro-Engineering Company that operates in the same field. The acquisition

would be helping the Burton Sensor Company not only to increase its revenue base but also

increase the wide base of products and services it offers in the market. The acquisition analysis

has been well carried on by us with the help of Discounted Cash Flow Method and relevant

assumptions and figures have been well considered for analysis purpose.

2FINANCIAL ANALYSIS

Table of Contents

Introduction-....................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Valuation of Electro Engineering Company................................................................................2

Financial Analysis of Electro-Engineering..................................................................................3

Valuation and Analysis of Thermo-well Machines.....................................................................6

Conclusion and Recommendations..................................................................................................7

Bibliography....................................................................................................................................8

Table of Contents

Introduction-....................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Valuation of Electro Engineering Company................................................................................2

Financial Analysis of Electro-Engineering..................................................................................3

Valuation and Analysis of Thermo-well Machines.....................................................................6

Conclusion and Recommendations..................................................................................................7

Bibliography....................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS

Introduction

The Burton Sensor Company operates in the designing and manufacturing of various

types of temperature sensors. The product had a variety of highly accurate, precise and moderate

set of thermocouple sensors, Resistance Temperature Detectors and Bearing Temperature

Probes. The users of the offered product covered a wide and a varied range of industries, thereby

including oil and gas, petrochemicals, industrial machinery, food processing unit and various

others. The Burton Sensor Company has been seeing rapid growth in its business operations and

this has been primarily due to the increasing demand as well as growing industry needs. The

company is primarily evaluating various courses of actions for the purpose of well increasing

their business operations and production capacity both in the form of organic growth as well as

inorganic growth. Inorganic growth follows the process of acquiring a similar company that is

operating in the same line of business as the Burton Sensor Company. The financing approach

that the company would be adopting given the current state of financial conditions and bank

covenants placed would be placed or taken into consideration for the company. The analysis

of the company has been specifically done by applying the Discounted Cash Flow Approach

whereby important consideration about the company in terms of value of share on an individual

basis has been specifically taken into consideration.

Discussion and Analysis

Valuation of Electro Engineering Company

The valuation of Electro Engineering Company would be done by applying the

discounted cash flow approach wherein the financial statement for the company will be well

reviewed for a sum of five years whereby estimated free cash flows of the company would be

well taken into consideration for valuing the share value of the company. The primary operations

of the EE Company was to deal in the Fiber-Optic Sensors. Technological Advancement and

efficiency well helped the company in delivering innovative as well as efficient products for well

selling the associated range of products (Pinto 2020). From the view perspective of the Burton

Sensors Company, the management of the company have well evaluated that both operational

and financial efficiency can be well brought down into the company. Reduction in Operational

Introduction

The Burton Sensor Company operates in the designing and manufacturing of various

types of temperature sensors. The product had a variety of highly accurate, precise and moderate

set of thermocouple sensors, Resistance Temperature Detectors and Bearing Temperature

Probes. The users of the offered product covered a wide and a varied range of industries, thereby

including oil and gas, petrochemicals, industrial machinery, food processing unit and various

others. The Burton Sensor Company has been seeing rapid growth in its business operations and

this has been primarily due to the increasing demand as well as growing industry needs. The

company is primarily evaluating various courses of actions for the purpose of well increasing

their business operations and production capacity both in the form of organic growth as well as

inorganic growth. Inorganic growth follows the process of acquiring a similar company that is

operating in the same line of business as the Burton Sensor Company. The financing approach

that the company would be adopting given the current state of financial conditions and bank

covenants placed would be placed or taken into consideration for the company. The analysis

of the company has been specifically done by applying the Discounted Cash Flow Approach

whereby important consideration about the company in terms of value of share on an individual

basis has been specifically taken into consideration.

Discussion and Analysis

Valuation of Electro Engineering Company

The valuation of Electro Engineering Company would be done by applying the

discounted cash flow approach wherein the financial statement for the company will be well

reviewed for a sum of five years whereby estimated free cash flows of the company would be

well taken into consideration for valuing the share value of the company. The primary operations

of the EE Company was to deal in the Fiber-Optic Sensors. Technological Advancement and

efficiency well helped the company in delivering innovative as well as efficient products for well

selling the associated range of products (Pinto 2020). From the view perspective of the Burton

Sensors Company, the management of the company have well evaluated that both operational

and financial efficiency can be well brought down into the company. Reduction in Operational

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS

Expenses and increase in the revenue base when viewed from a combined/consolidated company

perspective would be better allowing the company to sell a range of products at a competitive

rates in the industry. The analysis done for the company well shows that the company would be

experiencing a positive increase in the revenue base for the company and this will be primarily

due to the growing demand and development in the industry in terms of products offered (Tham

and Velez-Pareja 2019).

Financial Analysis of Electro-Engineering

The discounted cash flow valuation will be done for the company by taking the free cash

flows which has been well determined for the company for the sum of five years whereby

relevant analysis and assumptions have been taken into consideration. The growth in the revenue

base along with the decrease in the operational expenses have well been taken into consideration

for the purpose of valuing the shares of the company (Karampouzis and Ginoglou 2016). The

financial analysis has been done for the company for a sum of five years where it has been

considered that on a combined basis the Burton Sensor Company will be well decreasing the

selling, general and administrative expenses of the company from 26.54% to 23.58% and this

would be particularly due to the operational efficiency that would be brought down into the

company. The increase in the revenue of the company that has well been taken into consideration

is around 24% in 2017, 17.5% in 2018, 15% in 2019, 12% in 2020, and 10% in 2021. The

estimates for the company that has been well provided to us for the company in the context of

valuation was well taken into consideration. The financial information provided to us also says

that if the consolidation goes off well than the Working Capital Cycle for the EE Company

would improve further in the form of reduction in the days taken by the company for paying off

their accounts payable (Cornell and Gerger 2019).

The valuation for the company will be well done by using the estimate for the company

for the period of 2017-2021 in which the FCFF derived will be taken into the consideration. The

first step in valuing the share price of the company was to analyze the free cash flows that will be

flowing to the firm for this five year trend period and determining the terminal value that would

be flowing to the company after this sum of five years for the company. The terminal value for

the company has been well derived for the company by applying the stated formula as FCFF6/(k-

g). The value of FCFF6 was well determined by well using the value of FCFF multiplied with

Expenses and increase in the revenue base when viewed from a combined/consolidated company

perspective would be better allowing the company to sell a range of products at a competitive

rates in the industry. The analysis done for the company well shows that the company would be

experiencing a positive increase in the revenue base for the company and this will be primarily

due to the growing demand and development in the industry in terms of products offered (Tham

and Velez-Pareja 2019).

Financial Analysis of Electro-Engineering

The discounted cash flow valuation will be done for the company by taking the free cash

flows which has been well determined for the company for the sum of five years whereby

relevant analysis and assumptions have been taken into consideration. The growth in the revenue

base along with the decrease in the operational expenses have well been taken into consideration

for the purpose of valuing the shares of the company (Karampouzis and Ginoglou 2016). The

financial analysis has been done for the company for a sum of five years where it has been

considered that on a combined basis the Burton Sensor Company will be well decreasing the

selling, general and administrative expenses of the company from 26.54% to 23.58% and this

would be particularly due to the operational efficiency that would be brought down into the

company. The increase in the revenue of the company that has well been taken into consideration

is around 24% in 2017, 17.5% in 2018, 15% in 2019, 12% in 2020, and 10% in 2021. The

estimates for the company that has been well provided to us for the company in the context of

valuation was well taken into consideration. The financial information provided to us also says

that if the consolidation goes off well than the Working Capital Cycle for the EE Company

would improve further in the form of reduction in the days taken by the company for paying off

their accounts payable (Cornell and Gerger 2019).

The valuation for the company will be well done by using the estimate for the company

for the period of 2017-2021 in which the FCFF derived will be taken into the consideration. The

first step in valuing the share price of the company was to analyze the free cash flows that will be

flowing to the firm for this five year trend period and determining the terminal value that would

be flowing to the company after this sum of five years for the company. The terminal value for

the company has been well derived for the company by applying the stated formula as FCFF6/(k-

g). The value of FCFF6 was well determined by well using the value of FCFF multiplied with

5FINANCIAL ANALYSIS

the applicable growth rate. The growth rate that has been well taken into consideration for the

purpose of well increasing out the cash flows of the company has been around 3.50%. On the

other hand the cost of capital that was taken for the company was well derived by using the cost

of equity and cost of debt for the company for the trend period analyzed (Frank and Shen 2016).

The cost of equity that has been well considered for the company was calculated with the help of

Capital Asset Pricing Model wherein the key formula that has been applied is as follows:

Cost of Equity (Ke): Risk Free Rate (Rf) + Beta*(Equity Market Risk Premium).

The key inputs used for the purpose of calculating the cost of equity was the risk free rate

which was considered as the 10-Year Risk Free Treasury Note which was about 3.00%, the

equity market risk premium was about 5.80% and the beta value was around 0.88 times. The beta

value for the EE Company has been well determined with the help of data available of

comparable companies whose equity beta was used as a proxy for well calculating the beta for

the EE Company (El Ghoul et al., 2018). In particular it is important to note that average values

of the equity beta for the year 2016 was taken into analysis for calculating the value of beta. On

the other hand, the value for the equity risk premium well shows the amount that has been

calculated for the firm by taking the return on market less the risk free rate. The value

determined for the Cost of Equity was around 8.09%.

Cost of Debt for the EE Company has been well derived with the help of the yield that

has been generated on the Baa Corporate Bonds which was around 4.8%. However, it is

important to note interest expenses are tax deductible and this is the key reason which helps the

company get a lower cost of debt due to the tax shield involved. In order to well incorporate the

same the effective tax rate has been calculated for the EE Company by taking the pretax income

and the income tax expenses of the company for getting the Effective tax rate (Huizinga, Voget

and Wagner 2018). The effective tax rate that has been determined for the company was around

35% and this would be well applied for calculating the post-tax cost of debt. The post-tax cost of

debt for the firm was around 3.12%.

In order to well incorporate the different costs of capitals for the firm the appropriate

weights of equity and debt was well considered for well calculating the cost of capital. The

weight of equity was determined by taking the reported value of shareholders equity by the CC

Company for the year 2016. On the other, hand the value of debt was also considered for the year

the applicable growth rate. The growth rate that has been well taken into consideration for the

purpose of well increasing out the cash flows of the company has been around 3.50%. On the

other hand the cost of capital that was taken for the company was well derived by using the cost

of equity and cost of debt for the company for the trend period analyzed (Frank and Shen 2016).

The cost of equity that has been well considered for the company was calculated with the help of

Capital Asset Pricing Model wherein the key formula that has been applied is as follows:

Cost of Equity (Ke): Risk Free Rate (Rf) + Beta*(Equity Market Risk Premium).

The key inputs used for the purpose of calculating the cost of equity was the risk free rate

which was considered as the 10-Year Risk Free Treasury Note which was about 3.00%, the

equity market risk premium was about 5.80% and the beta value was around 0.88 times. The beta

value for the EE Company has been well determined with the help of data available of

comparable companies whose equity beta was used as a proxy for well calculating the beta for

the EE Company (El Ghoul et al., 2018). In particular it is important to note that average values

of the equity beta for the year 2016 was taken into analysis for calculating the value of beta. On

the other hand, the value for the equity risk premium well shows the amount that has been

calculated for the firm by taking the return on market less the risk free rate. The value

determined for the Cost of Equity was around 8.09%.

Cost of Debt for the EE Company has been well derived with the help of the yield that

has been generated on the Baa Corporate Bonds which was around 4.8%. However, it is

important to note interest expenses are tax deductible and this is the key reason which helps the

company get a lower cost of debt due to the tax shield involved. In order to well incorporate the

same the effective tax rate has been calculated for the EE Company by taking the pretax income

and the income tax expenses of the company for getting the Effective tax rate (Huizinga, Voget

and Wagner 2018). The effective tax rate that has been determined for the company was around

35% and this would be well applied for calculating the post-tax cost of debt. The post-tax cost of

debt for the firm was around 3.12%.

In order to well incorporate the different costs of capitals for the firm the appropriate

weights of equity and debt was well considered for well calculating the cost of capital. The

weight of equity was determined by taking the reported value of shareholders equity by the CC

Company for the year 2016. On the other, hand the value of debt was also considered for the year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS

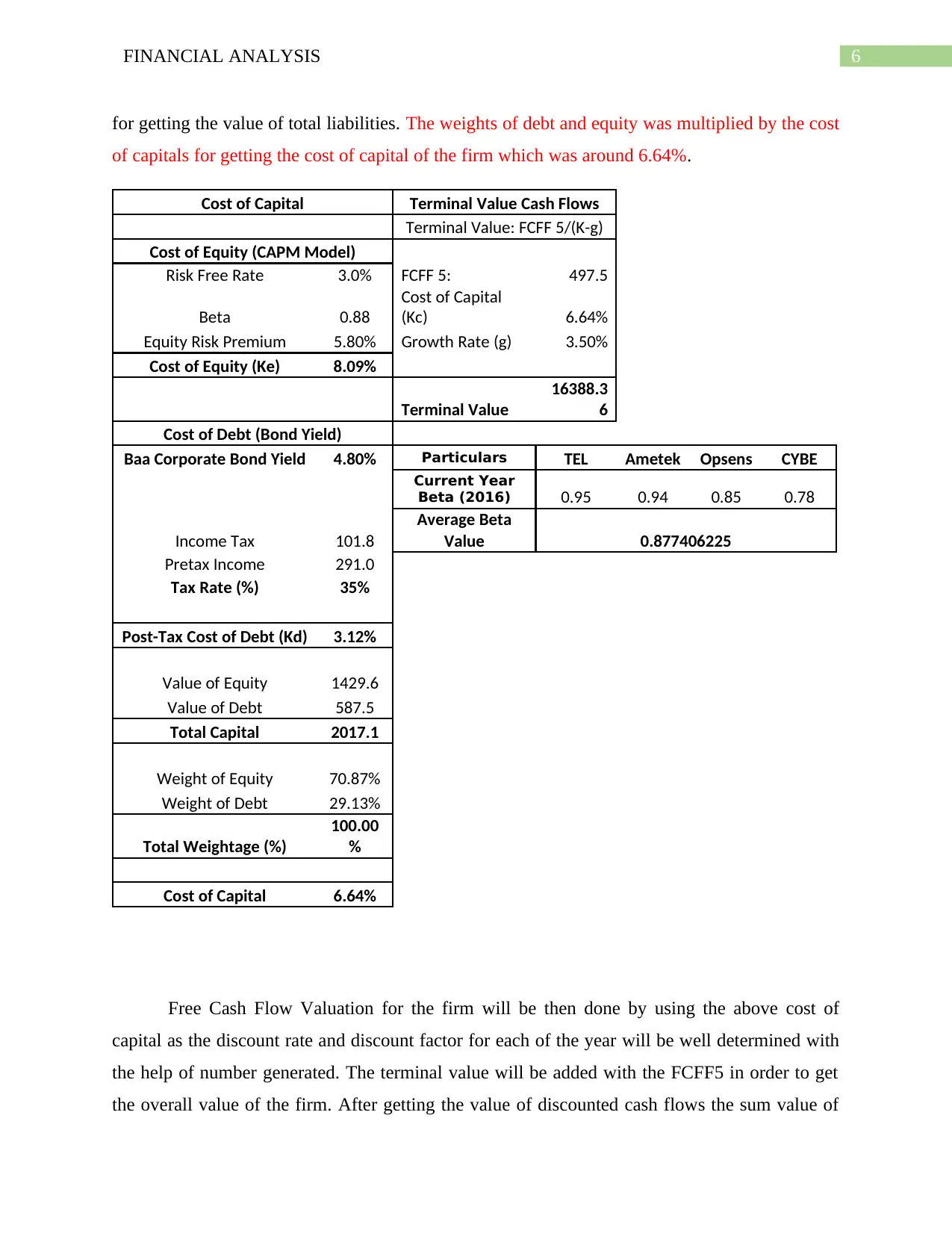

for getting the value of total liabilities. The weights of debt and equity was multiplied by the cost

of capitals for getting the cost of capital of the firm which was around 6.64%.

Cost of Capital Terminal Value Cash Flows

Terminal Value: FCFF 5/(K-g)

Cost of Equity (CAPM Model)

Risk Free Rate 3.0% FCFF 5: 497.5

Beta 0.88

Cost of Capital

(Kc) 6.64%

Equity Risk Premium 5.80% Growth Rate (g) 3.50%

Cost of Equity (Ke) 8.09%

Terminal Value

16388.3

6

Cost of Debt (Bond Yield)

Baa Corporate Bond Yield 4.80% Particulars TEL Ametek Opsens CYBE

Current Year

Beta (2016) 0.95 0.94 0.85 0.78

Income Tax 101.8

Average Beta

Value 0.877406225

Pretax Income 291.0

Tax Rate (%) 35%

Post-Tax Cost of Debt (Kd) 3.12%

Value of Equity 1429.6

Value of Debt 587.5

Total Capital 2017.1

Weight of Equity 70.87%

Weight of Debt 29.13%

Total Weightage (%)

100.00

%

Cost of Capital 6.64%

Free Cash Flow Valuation for the firm will be then done by using the above cost of

capital as the discount rate and discount factor for each of the year will be well determined with

the help of number generated. The terminal value will be added with the FCFF5 in order to get

the overall value of the firm. After getting the value of discounted cash flows the sum value of

for getting the value of total liabilities. The weights of debt and equity was multiplied by the cost

of capitals for getting the cost of capital of the firm which was around 6.64%.

Cost of Capital Terminal Value Cash Flows

Terminal Value: FCFF 5/(K-g)

Cost of Equity (CAPM Model)

Risk Free Rate 3.0% FCFF 5: 497.5

Beta 0.88

Cost of Capital

(Kc) 6.64%

Equity Risk Premium 5.80% Growth Rate (g) 3.50%

Cost of Equity (Ke) 8.09%

Terminal Value

16388.3

6

Cost of Debt (Bond Yield)

Baa Corporate Bond Yield 4.80% Particulars TEL Ametek Opsens CYBE

Current Year

Beta (2016) 0.95 0.94 0.85 0.78

Income Tax 101.8

Average Beta

Value 0.877406225

Pretax Income 291.0

Tax Rate (%) 35%

Post-Tax Cost of Debt (Kd) 3.12%

Value of Equity 1429.6

Value of Debt 587.5

Total Capital 2017.1

Weight of Equity 70.87%

Weight of Debt 29.13%

Total Weightage (%)

100.00

%

Cost of Capital 6.64%

Free Cash Flow Valuation for the firm will be then done by using the above cost of

capital as the discount rate and discount factor for each of the year will be well determined with

the help of number generated. The terminal value will be added with the FCFF5 in order to get

the overall value of the firm. After getting the value of discounted cash flows the sum value of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS

each values helped us in getting the FCFF. The formula of FCFE was applied for getting the

value of shares on an analysis purpose as follows:

FCFE: FCFF + Cash and Cash Equivalents-Total Debt

FCFE: 13,110.27

Outstanding Shares: 1100

Value Per Share: 11.92

Free Cash Flow Valuation Model

Particulars 2017 2018 2019 2020 2021

Free Cash Flows 244.4 280.9 348.8 427.0 497.5

Terminal Value

16388.3

6

Discount Factor @ 6.64% 0.94 0.88 0.82 0.77 0.73

Discounted Cash Flows 229.18

247.0

1

287.6

2

330.1

8

12243.9

8

Free Cash Flows for Firm

13337.9

7

Add: Cash & Cash Equivalents 359.8

Less: Total Debt 587.5

Free Cash Flow for Equity (FCFE)

13110.2

7

Outstanding Shares 1100

Value Per Share 11.92

Now it is important to analyze the value derived from FCFE and the value demanded by

the company for the purchase of EE Company. The value for 100% stake derived was calculated

above as 13,110.27 and the value demanded was around 10 times of EBITDA Value where

reported value of EBITDA in the year 2016 was around 686.7 and the value for EBITDA was

calculated to be around 6867.0. Thus the excess value which would be created for Burton

Sensors Shareholders will be around 3244.90, if the given set of assumptions and analysis

materializes.

Financing

The financing for the project will is usually done by using both the equity and debt

financing sources for the company. However, it is important to note that in this case the EE

each values helped us in getting the FCFF. The formula of FCFE was applied for getting the

value of shares on an analysis purpose as follows:

FCFE: FCFF + Cash and Cash Equivalents-Total Debt

FCFE: 13,110.27

Outstanding Shares: 1100

Value Per Share: 11.92

Free Cash Flow Valuation Model

Particulars 2017 2018 2019 2020 2021

Free Cash Flows 244.4 280.9 348.8 427.0 497.5

Terminal Value

16388.3

6

Discount Factor @ 6.64% 0.94 0.88 0.82 0.77 0.73

Discounted Cash Flows 229.18

247.0

1

287.6

2

330.1

8

12243.9

8

Free Cash Flows for Firm

13337.9

7

Add: Cash & Cash Equivalents 359.8

Less: Total Debt 587.5

Free Cash Flow for Equity (FCFE)

13110.2

7

Outstanding Shares 1100

Value Per Share 11.92

Now it is important to analyze the value derived from FCFE and the value demanded by

the company for the purchase of EE Company. The value for 100% stake derived was calculated

above as 13,110.27 and the value demanded was around 10 times of EBITDA Value where

reported value of EBITDA in the year 2016 was around 686.7 and the value for EBITDA was

calculated to be around 6867.0. Thus the excess value which would be created for Burton

Sensors Shareholders will be around 3244.90, if the given set of assumptions and analysis

materializes.

Financing

The financing for the project will is usually done by using both the equity and debt

financing sources for the company. However, it is important to note that in this case the EE

8FINANCIAL ANALYSIS

Company would be willing to go for an equity deal in which they would be getting the shares of

Burton Sensors Company for the purpose of well exchanging their shares. The share price that is

offered by the EE Company for the purpose of well exchanging the shares of the Burton Sensor

Company has been around $4.75 which will be well used for the exchange purpose. The offered

price is approximately close to the prevailing share price of the company, so the management of

the Burton Sensor Company do not need to worry about. The worked value for the EE Company

has been around $11.92, while at the same time the EE Company is offering around $4.75 for the

shares of Burton Sensors Company. The reason behind the same will be because the merger will

be with a base of equity finance approach where the investors of EE Company would be getting

shares of Burton Company after the merger. The percentage of ownership that the Burton

Company would be enjoying over EE Company would be around 100% and for the same the

equity finance amount that would be required will be around $13,110.27mn. It is important to

note that Burton will be losing the 100% equity stake which they are having after the post-

merger of EE and Burton as they are going for an all equity deal. The key factor which should be

well considering or evaluating the EE and Burton Sensor Merger is that the financing of the

acquisition amount will be well done with the help of the equity finance whereby the value

offered by the EE Company is approximately close to the intrinsic value of share price that has

been well determined by the Burton Company. This gives a clear idea to the management of

Burton Company that forecast and assumptions made in respect to the operations, growth and

development of the company. The financing of equity gives the management and the Burton

Company considerably less risky way for financing as cash or its equivalents would not be paid

for acquiring EE Company.

Conclusion and Recommendations

The analysis that has been done for the company well says that the Burton Sensor

Company should well go ahead with the purchase of EE Company and this has been particularly

due to the positive value that would be created for the shareholders of the Burton Company.

Since, the financing of the project will be done using equity method the management of the

Burton Sensor company would not be facing any issue with the bank covenants placed on the

assets and liabilities match. However, it is important to note that the derived analysis and

estimates for the figures has been well done based on a given set of assumption and figures

Company would be willing to go for an equity deal in which they would be getting the shares of

Burton Sensors Company for the purpose of well exchanging their shares. The share price that is

offered by the EE Company for the purpose of well exchanging the shares of the Burton Sensor

Company has been around $4.75 which will be well used for the exchange purpose. The offered

price is approximately close to the prevailing share price of the company, so the management of

the Burton Sensor Company do not need to worry about. The worked value for the EE Company

has been around $11.92, while at the same time the EE Company is offering around $4.75 for the

shares of Burton Sensors Company. The reason behind the same will be because the merger will

be with a base of equity finance approach where the investors of EE Company would be getting

shares of Burton Company after the merger. The percentage of ownership that the Burton

Company would be enjoying over EE Company would be around 100% and for the same the

equity finance amount that would be required will be around $13,110.27mn. It is important to

note that Burton will be losing the 100% equity stake which they are having after the post-

merger of EE and Burton as they are going for an all equity deal. The key factor which should be

well considering or evaluating the EE and Burton Sensor Merger is that the financing of the

acquisition amount will be well done with the help of the equity finance whereby the value

offered by the EE Company is approximately close to the intrinsic value of share price that has

been well determined by the Burton Company. This gives a clear idea to the management of

Burton Company that forecast and assumptions made in respect to the operations, growth and

development of the company. The financing of equity gives the management and the Burton

Company considerably less risky way for financing as cash or its equivalents would not be paid

for acquiring EE Company.

Conclusion and Recommendations

The analysis that has been done for the company well says that the Burton Sensor

Company should well go ahead with the purchase of EE Company and this has been particularly

due to the positive value that would be created for the shareholders of the Burton Company.

Since, the financing of the project will be done using equity method the management of the

Burton Sensor company would not be facing any issue with the bank covenants placed on the

assets and liabilities match. However, it is important to note that the derived analysis and

estimates for the figures has been well done based on a given set of assumption and figures

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS

which are well expected to change in the due course of the project thus it is recommended that

the management of the company views the project from various perspective and factors that

might help them asses the variability in the profitability generated from the project investment.

which are well expected to change in the due course of the project thus it is recommended that

the management of the company views the project from various perspective and factors that

might help them asses the variability in the profitability generated from the project investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS

Bibliography

Pinto, J.E., 2020. Equity asset valuation. John Wiley & Sons.

Tham, J. and Velez-Pareja, I., 2019. Two Fundamental Principles for Cash Flow Valuation

(CFV). Available at SSRN 3384058.

Karampouzis, A.D. and Ginoglou, D., 2016. Accounting Adjustments on the Discounted Free

Cash Flow Valuation Model for Appraising SMEs in Greece. Chinese Business Review, 15(10),

pp.498-506.

Cornell, B. and Gerger, R., 2019. Consistent Treatment of Inflation in Discounted Cash Flow

Valuation. Available at SSRN 3435615.

Bhandari, S.B. and Adams, M.T., 2017. On the definition, measurement, and use of the free cash

flow concept in financial reporting and analysis: a review and recommendations. Journal of

Accounting and Finance, 17(1).

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), pp.335-361.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Bibliography

Pinto, J.E., 2020. Equity asset valuation. John Wiley & Sons.

Tham, J. and Velez-Pareja, I., 2019. Two Fundamental Principles for Cash Flow Valuation

(CFV). Available at SSRN 3384058.

Karampouzis, A.D. and Ginoglou, D., 2016. Accounting Adjustments on the Discounted Free

Cash Flow Valuation Model for Appraising SMEs in Greece. Chinese Business Review, 15(10),

pp.498-506.

Cornell, B. and Gerger, R., 2019. Consistent Treatment of Inflation in Discounted Cash Flow

Valuation. Available at SSRN 3435615.

Bhandari, S.B. and Adams, M.T., 2017. On the definition, measurement, and use of the free cash

flow concept in financial reporting and analysis: a review and recommendations. Journal of

Accounting and Finance, 17(1).

Frank, M.Z. and Shen, T., 2016. Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), pp.300-315.

El Ghoul, S., Guedhami, O., Kim, H. and Park, K., 2018. Corporate environmental responsibility

and the cost of capital: International evidence. Journal of Business Ethics, 149(2), pp.335-361.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.