BUS105 Computing Assignment Report

VerifiedAdded on 2019/11/26

|11

|1700

|170

Report

AI Summary

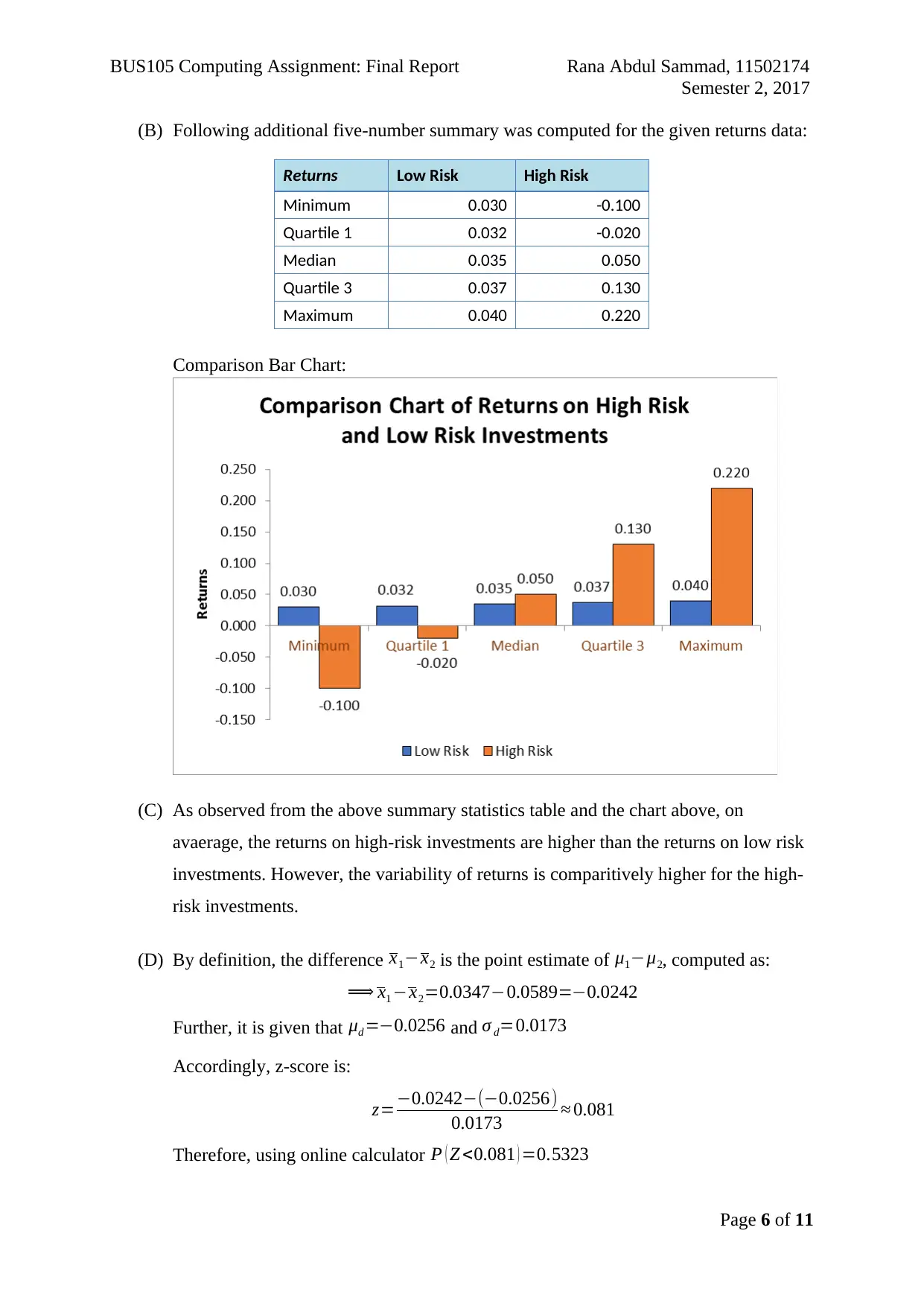

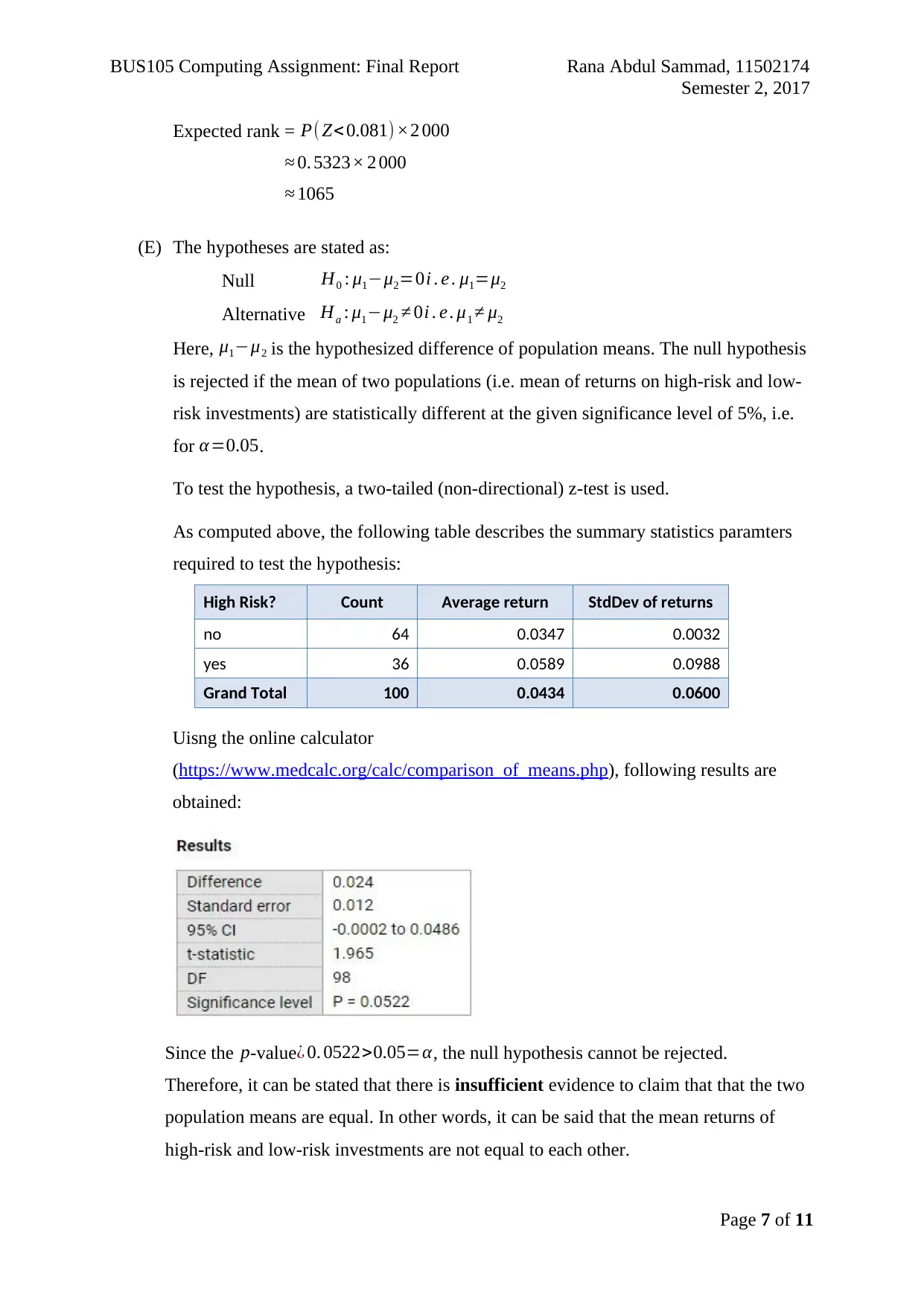

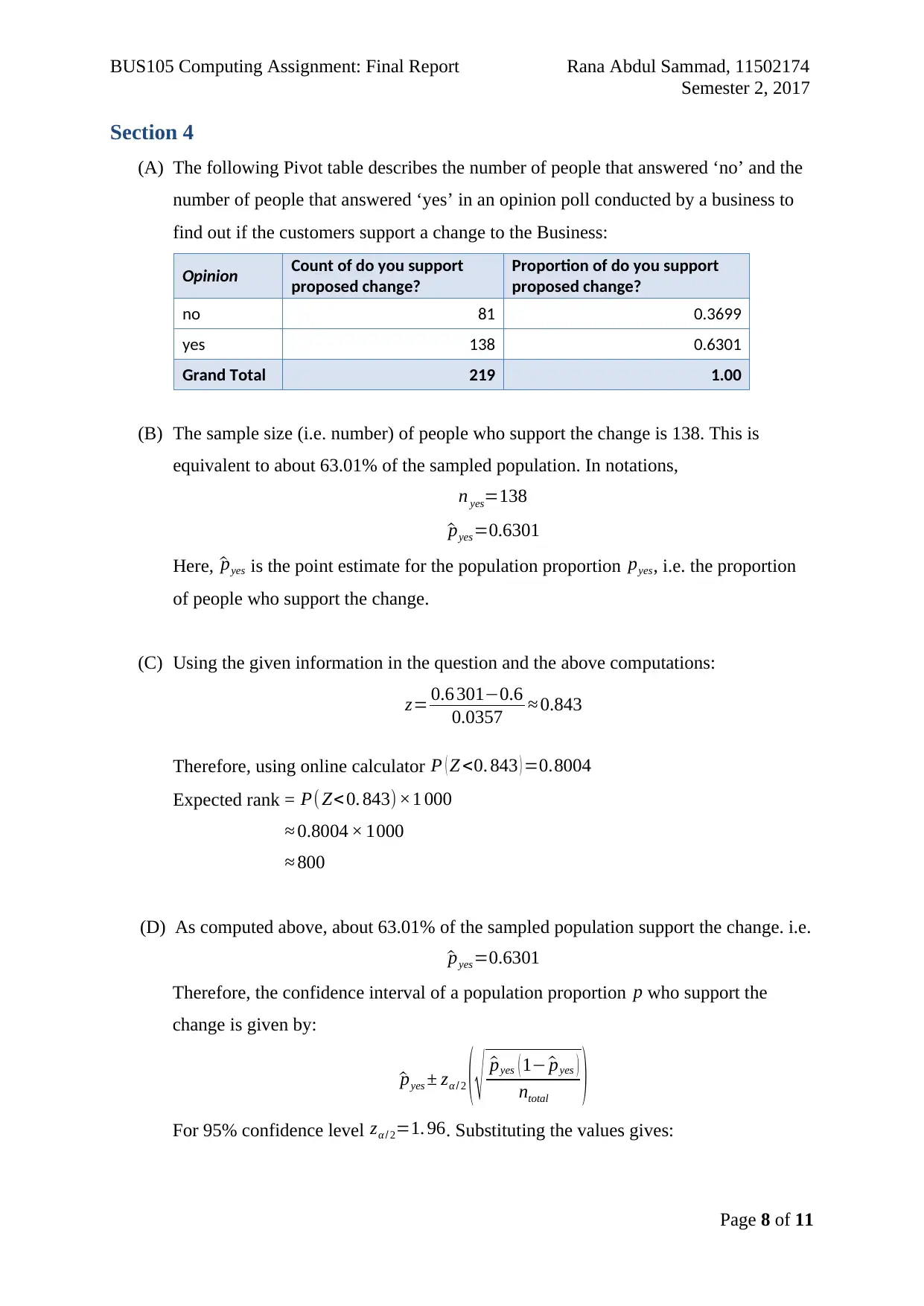

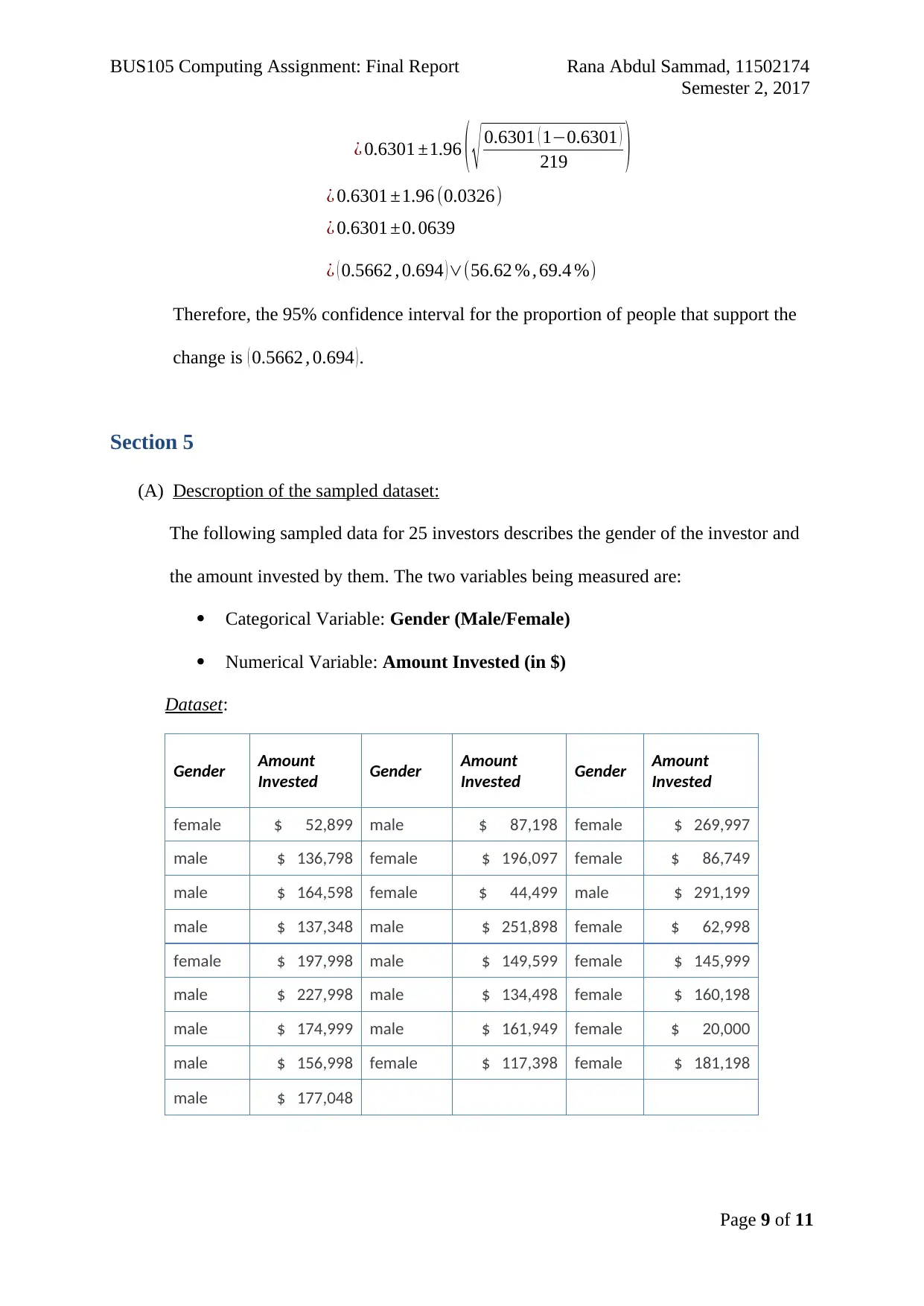

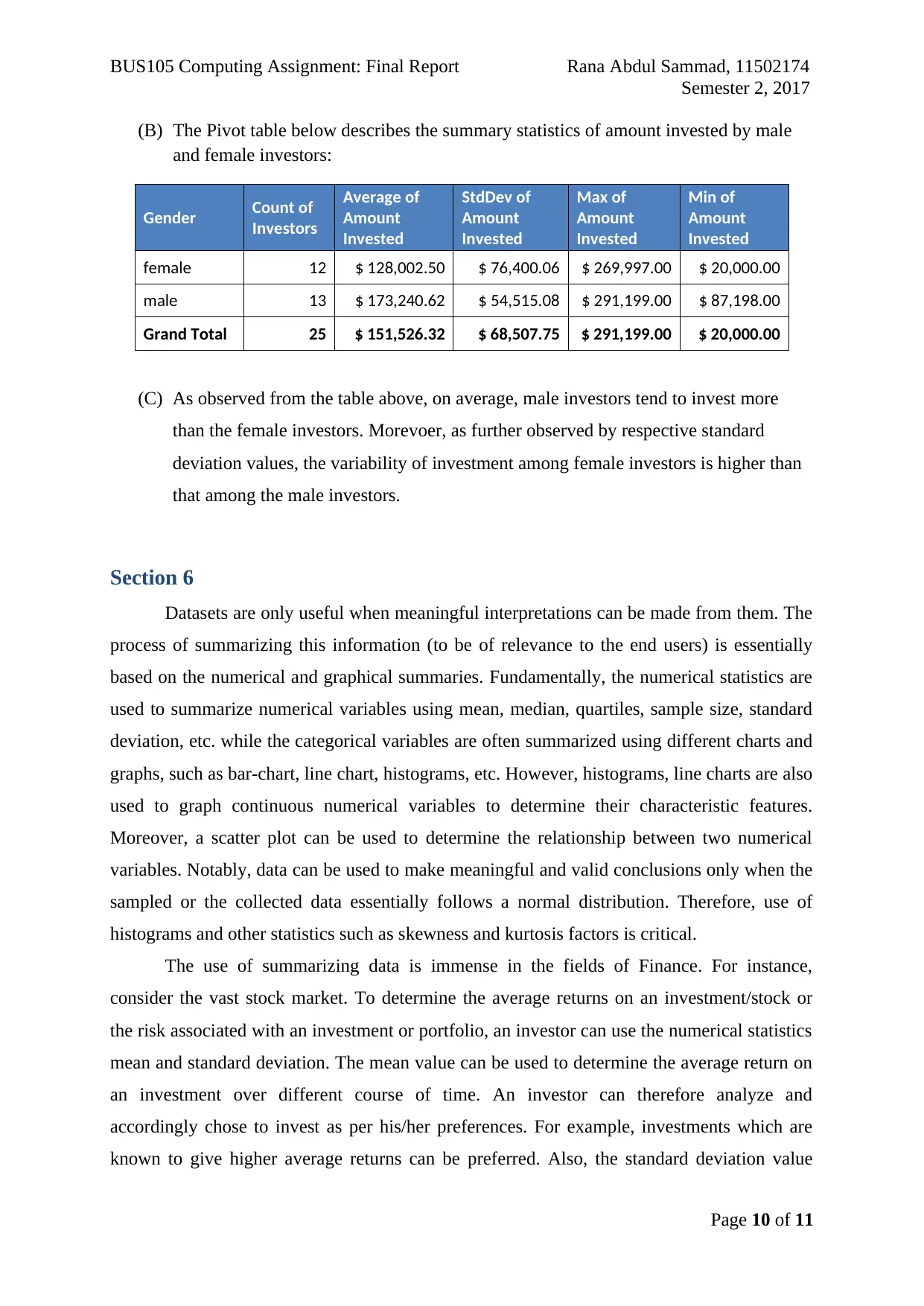

This report presents a comprehensive analysis of various datasets using statistical methods. It begins with a scatter plot analysis to determine the relationship between annual income and savings contributions, followed by the creation of pivot tables to analyze investment risk and profitability. Hypothesis testing is employed to compare the proportions of losses between high-risk and low-risk investments, and a z-test is used to compare the mean returns of these investments. A confidence interval is calculated for the proportion of people supporting a business change based on an opinion poll. Finally, the report includes a descriptive analysis of a dataset on investor gender and investment amounts, summarizing the data using descriptive statistics and pivot tables. The report concludes by discussing the importance of data summarization and its applications in finance, using examples of mean and standard deviation in investment analysis. The report includes references to external resources used for guidance and further explanation.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.