Technology and Accounting Processes: BUS285 Take Home Exam Solution

VerifiedAdded on 2022/09/23

|7

|517

|21

Homework Assignment

AI Summary

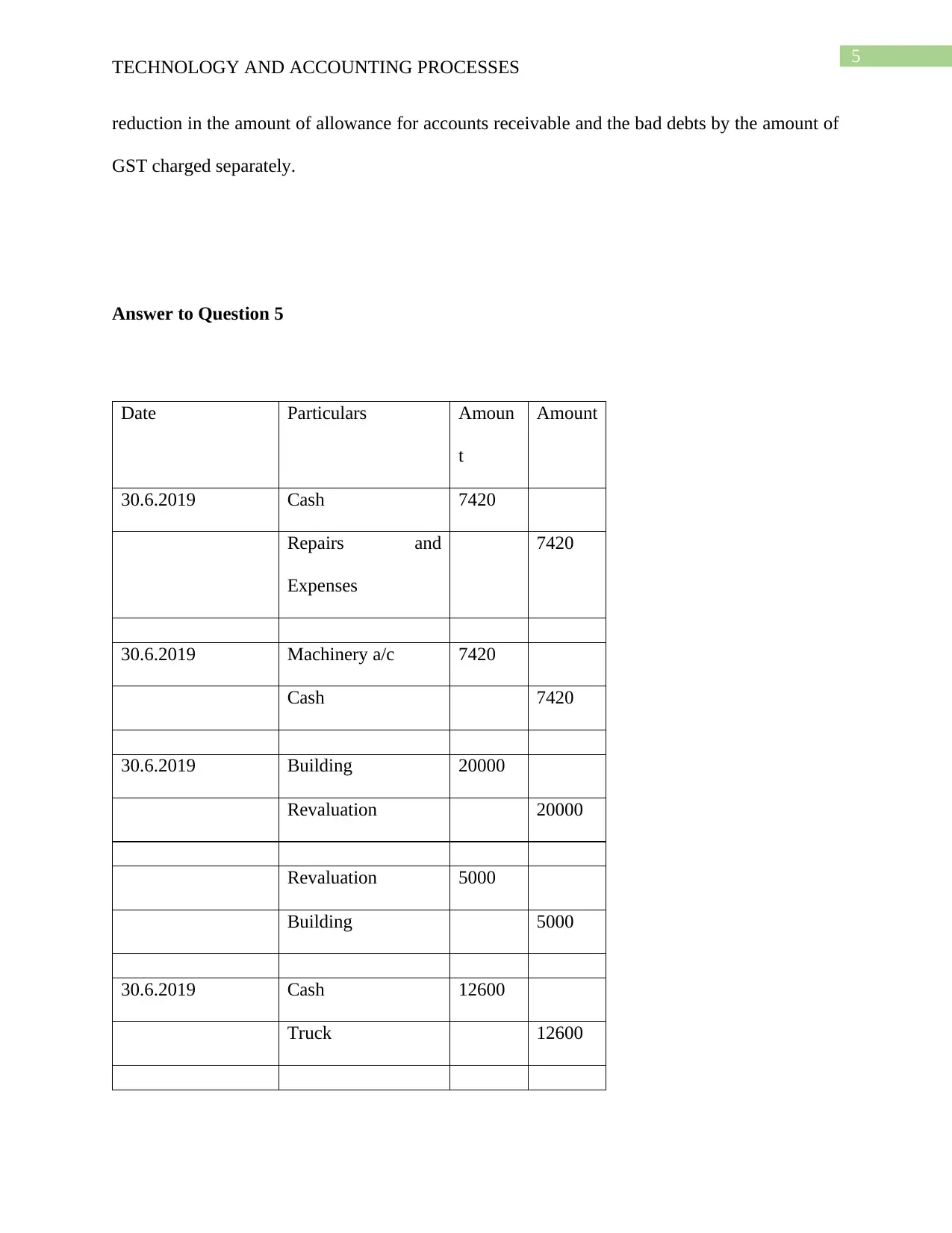

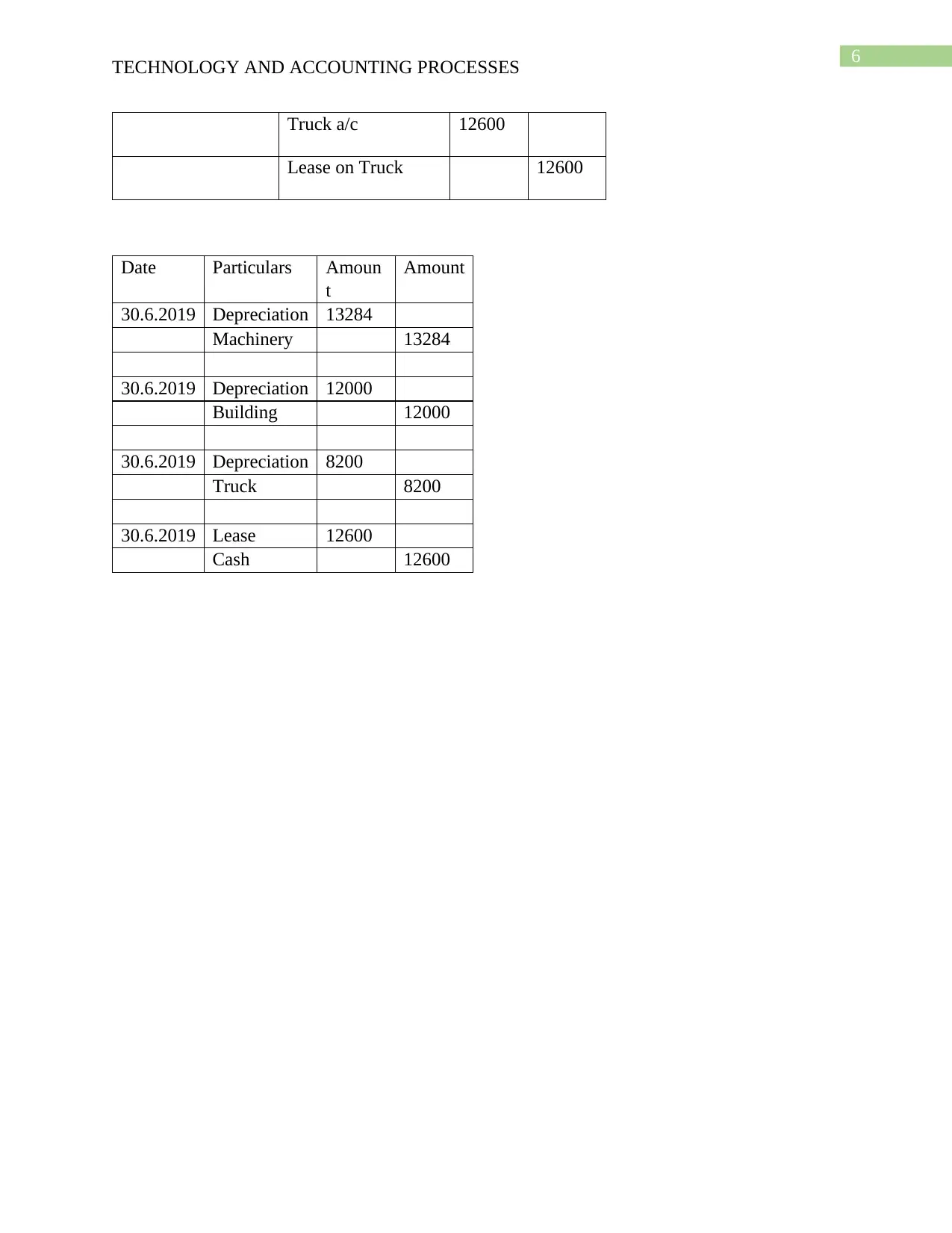

This document presents a comprehensive solution to the BUS285 Technology and Accounting Processes take-home exam from 2020. The solution includes detailed answers to five questions, covering a range of accounting topics. Question 3 provides a net cash flow statement from operating activities, while Question 4 delves into bad debts, including journal entries and calculations for net accounts receivable. Question 5 presents journal entries for various transactions, such as repairs, machinery revaluation, and depreciation. The document provides complete accounting solutions to the exam questions, including tables and calculations, offering a valuable resource for accounting students seeking to understand and solve complex accounting problems.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.