BUS356 - ABC Ltd and XYZ Ltd: Analysis of Consolidated Statements

VerifiedAdded on 2023/06/10

|10

|1108

|463

Case Study

AI Summary

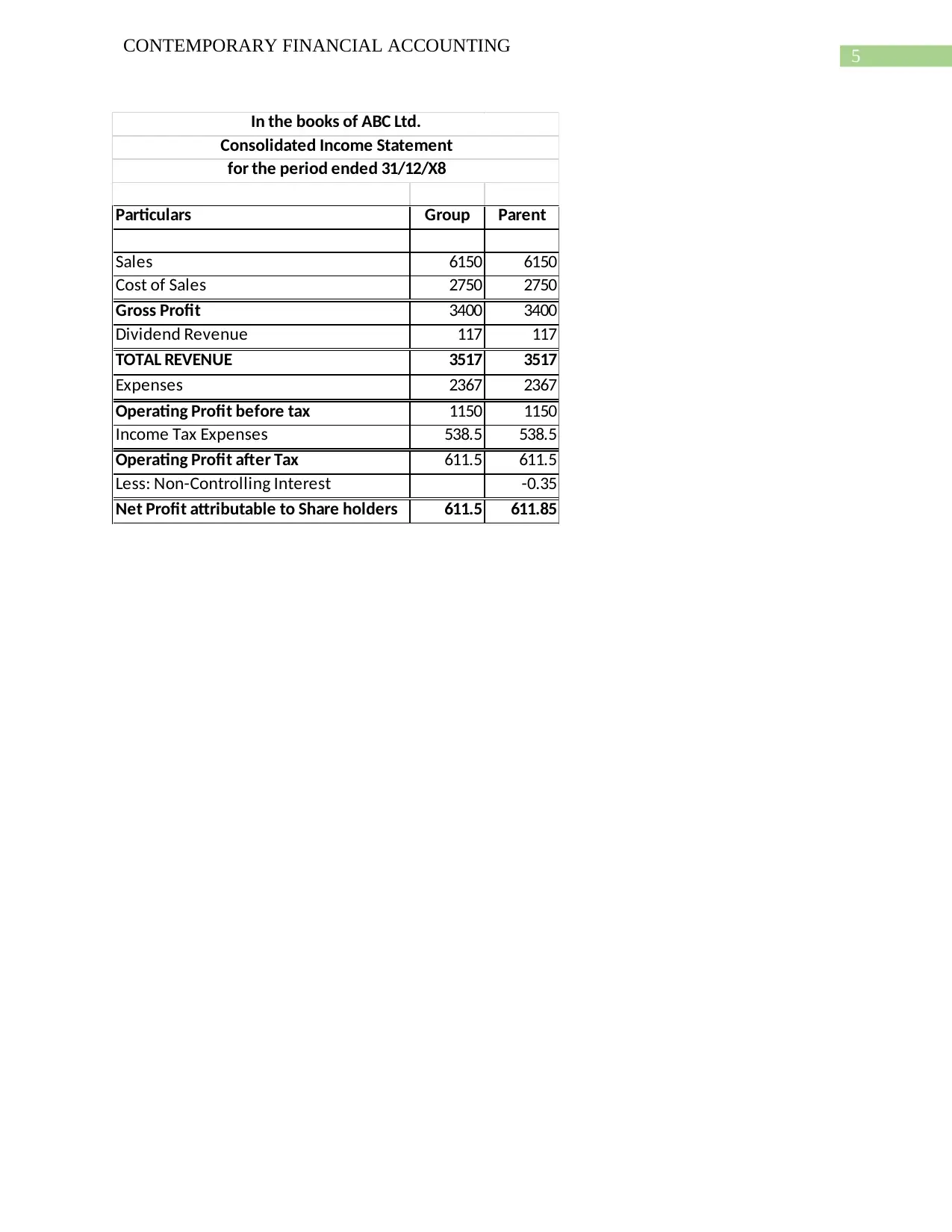

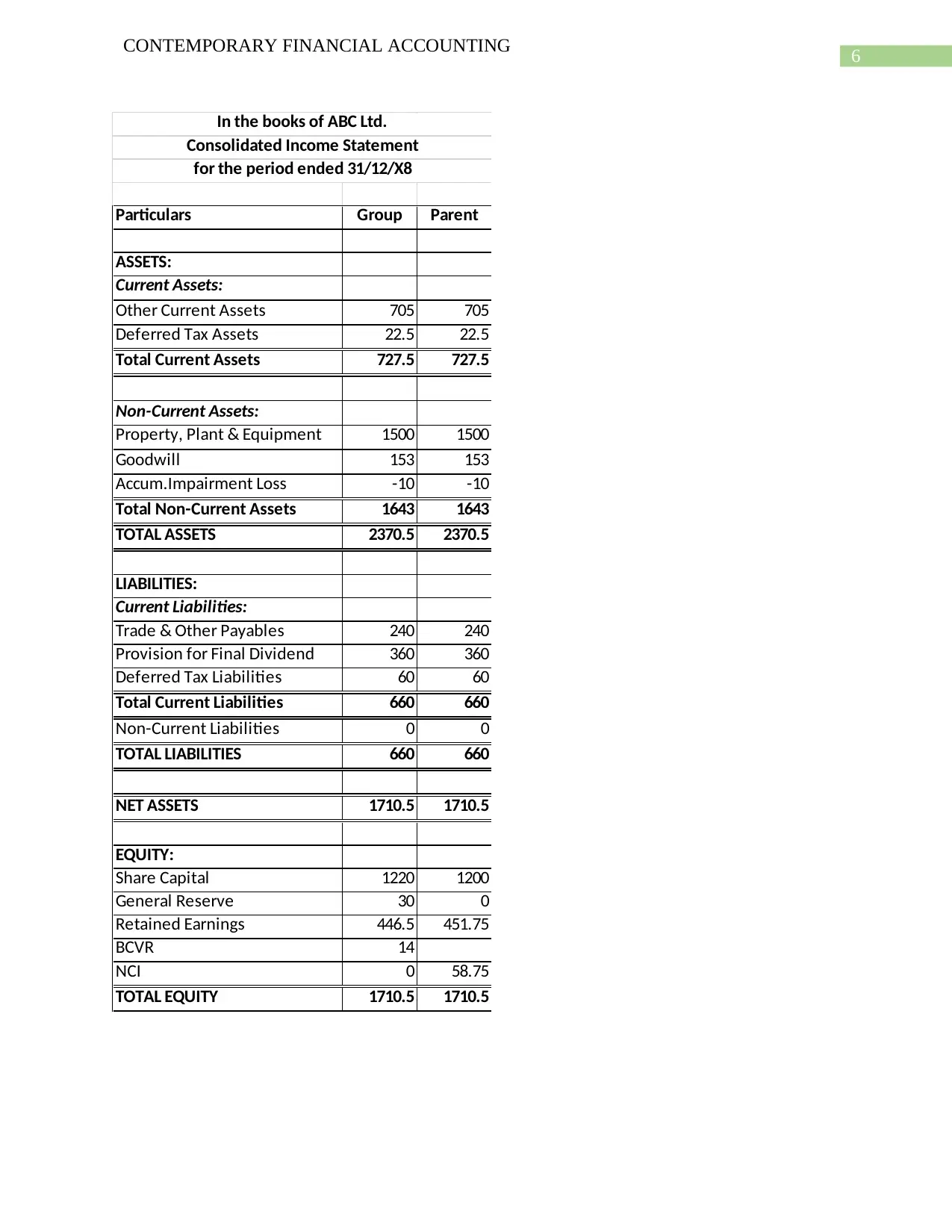

This case study examines the acquisition of XYZ Ltd by ABC Ltd and the subsequent consolidation of their financial statements. It includes a detailed acquisition analysis, journal entries for consolidation adjustments, and the preparation of consolidated income statements and balance sheets. The case study also explores the differences between the partial and full goodwill methods for accounting for the acquisition. Key aspects covered include the calculation of goodwill, the treatment of non-controlling interests, and the impact of intercompany transactions. The solution provides a comprehensive understanding of the accounting principles and procedures involved in business combinations and consolidated financial reporting.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.